Islamic banking & Finance Introduction Evolution · PDF fileIslamic banking & Finance...

13

Lehrstuhl für Bankwirtschaft und Finanzdienstleistungen Prof. Dr. Hans-Peter Burghof with Ahmad Abu-Alkheil and Ulli Spankowski 2 Islamic banking & Finance •Introduction •Evolution

Transcript of Islamic banking & Finance Introduction Evolution · PDF fileIslamic banking & Finance...

Lehrstuhl für Bankwirtschaft und Finanzdienstleistungen

Prof. Dr. Hans-Peter Burghof with

Ahmad Abu-Alkheil and Ulli Spankowski

2

Islamic banking & Finance

•Introduction

•Evolution

3

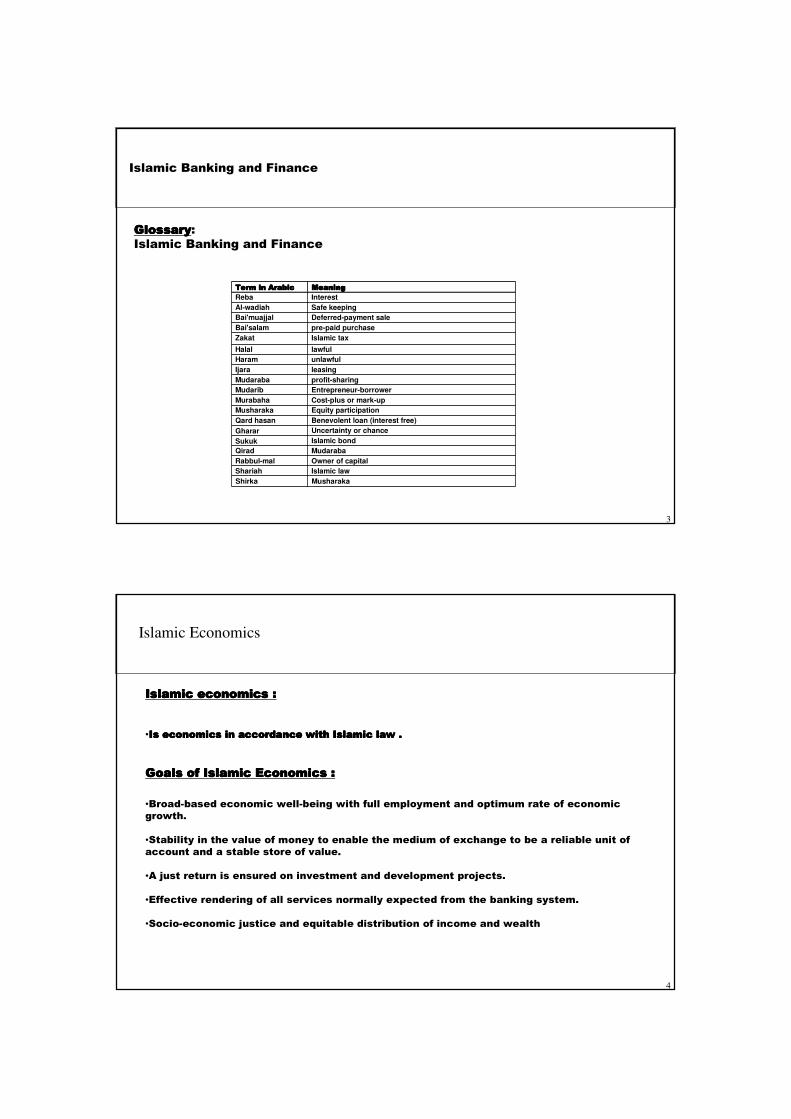

Term in ArabicTerm in ArabicTerm in ArabicTerm in Arabic MeaningMeaningMeaningMeaning

Reba Interest

Al-wadiah Safe keeping

Bai'muajjal Deferred-payment sale

Bai'salam pre-paid purchase

Zakat Islamic tax

Halal lawful

Haram unlawful

Ijara leasing

Mudaraba profit-sharing

Mudarib Entrepreneur-borrower

Murabaha Cost-plus or mark-up

Musharaka Equity participation

Qard hasan Benevolent loan (interest free)

Gharar Uncertainty or chance

Sukuk Islamic bond

Qirad Mudaraba

Rabbul-mal Owner of capital

Shariah Islamic law

Shirka Musharaka

GlossaryGlossaryGlossaryGlossary:

Islamic Banking and Finance

Islamic Banking and Finance

4

Islamic Economics

Islamic economics :Islamic economics :Islamic economics :Islamic economics :

•Is economics in accordance with Islamic law .Is economics in accordance with Islamic law .Is economics in accordance with Islamic law .Is economics in accordance with Islamic law .

Goals of Islamic Economics :Goals of Islamic Economics :Goals of Islamic Economics :Goals of Islamic Economics :

•Broad-based economic well-being with full employment and optimum rate of economic

growth.

•Stability in the value of money to enable the medium of exchange to be a reliable unit of

account and a stable store of value.

•A just return is ensured on investment and development projects.

•Effective rendering of all services normally expected from the banking system.

•Socio-economic justice and equitable distribution of income and wealth

5

Rules regarding Islamic finance :Rules regarding Islamic finance :Rules regarding Islamic finance :Rules regarding Islamic finance :

•Any predetermined payment over and above the actual amount of prAny predetermined payment over and above the actual amount of prAny predetermined payment over and above the actual amount of prAny predetermined payment over and above the actual amount of principal is prohibitedincipal is prohibitedincipal is prohibitedincipal is prohibited

•The lender must share in the profits or losses arising out of thThe lender must share in the profits or losses arising out of thThe lender must share in the profits or losses arising out of thThe lender must share in the profits or losses arising out of the enterprise for which the e enterprise for which the e enterprise for which the e enterprise for which the

money was lentmoney was lentmoney was lentmoney was lent

•Making money from money is not Making money from money is not Making money from money is not Making money from money is not IslamicallyIslamicallyIslamicallyIslamically acceptable (Asset Based Financing)acceptable (Asset Based Financing)acceptable (Asset Based Financing)acceptable (Asset Based Financing)

•GhararGhararGhararGharar (Uncertainty, Risk or Speculation) is also prohibited(Uncertainty, Risk or Speculation) is also prohibited(Uncertainty, Risk or Speculation) is also prohibited(Uncertainty, Risk or Speculation) is also prohibited

•Investments should only support practices or products that are nInvestments should only support practices or products that are nInvestments should only support practices or products that are nInvestments should only support practices or products that are not forbiddenot forbiddenot forbiddenot forbidden

Islamic Banking and Finance

6

Islamic banking :Islamic banking :Islamic banking :Islamic banking :

A banking system that is based on the principles of Islamic law (also known as Sharia,

and guided by Islamic economics).

Islamic banking distinguishing features:Islamic banking distinguishing features:Islamic banking distinguishing features:Islamic banking distinguishing features:

•Zero interest and capital guarantee (interest-free)

•Multi-purpose and not purely commercial

•Strongly equity-oriented

•Full-reserve banking

Islamic Banking and Finance

7

Types of Islamic financing:

•Trade financing

•Investment financing

•Lending

• Services

Uses Of Funds ( Financing Techniques ):

•Musharaka (finance by way of partnership partnership partnership partnership ---- Joint VentureJoint VentureJoint VentureJoint Venture)

•Mudarabah (Profit Loss Sharing)

•Murabahah (cost-plus financing)

•Bai'salam ( prepaid purchase)

•Bai' muajjal (deferred payment)

•Istisnaa (manufacturing).

•ijara (Leasing )…

Islamic Banking and Finance

8

MusharakaMusharakaMusharakaMusharaka ::::

It means partnership. It involves you placing your capital with another person and both

sharing the risk and reward. The difference between Musharaka arrangements

and normal banking is that you can set any kind of profit sharing ratio, but

losses must be proportionate to the amount invested.

Types of Types of Types of Types of MusharakaMusharakaMusharakaMusharaka ::::

• DecliningDecliningDecliningDeclining----Balance Shared Equity: Commonly used to finance a home purchase,Balance Shared Equity: Commonly used to finance a home purchase,Balance Shared Equity: Commonly used to finance a home purchase,Balance Shared Equity: Commonly used to finance a home purchase,

thethethethe declining balance method calls for the bank and the investor to declining balance method calls for the bank and the investor to declining balance method calls for the bank and the investor to declining balance method calls for the bank and the investor to purchase purchase purchase purchase

the home jointly, with the institutional investor gradually tranthe home jointly, with the institutional investor gradually tranthe home jointly, with the institutional investor gradually tranthe home jointly, with the institutional investor gradually transferring its sferring its sferring its sferring its

portion of the equity in the home to the individual homeowner, wportion of the equity in the home to the individual homeowner, wportion of the equity in the home to the individual homeowner, wportion of the equity in the home to the individual homeowner, whose hose hose hose

payments constitute the homeowner's equity.payments constitute the homeowner's equity.payments constitute the homeowner's equity.payments constitute the homeowner's equity.

• Permanent Permanent Permanent Permanent Musharaka:In this form of Musharaka an Islamic bank

participates in the equity of a project and receives a share of profit on a

pro rata basis. The period of contract is not specified. So it can continue

so long as the parties concerned wish it to continue.

Islamic Banking and Finance

9

Mudaraba :

Refers to an investment on your behalf by a more skilled person. It takes the form of a

contract between two parties, one who provides the funds and the other who provides

the expertise and who agree to the division of any profits made in advance. In other

words, Islamic Bank would make Sharia’a compliant investments and share the profits

with the customer, in effect charging for the time and effort. If no profit is made, the loss

is borne by the customer and Islamic Bank.

ADCB

Islamic Banking and Finance

10

Sayyid Tahir

(MurabahahMurabahahMurabahahMurabahah (cost(cost(cost(cost----plus financing) :plus financing) :plus financing) :plus financing) :

Murabaha is a contract for purchase and resale and allows the customer to make

purchases without having to take out a loan and pay interest. Islamic Bank purchases the

goods for the customer, and re-sells them to the customer on a deferred basis, adding an

agreed profit margin. The customer then pays the sale price for the goods over

instalments, effectively obtaining credit without paying interest.

Islamic Banking and Finance

11

Islamic Banking and Finance

Leasing or ijara is also frequently practiced by Islamic banks. Under this mode, the banks

would buy the equipment or machinery and lease it out to their clients who may opt to buy

the items eventually,(HireHireHireHire Purchase)Purchase)Purchase)Purchase) in which case the monthly payments will consist of two

components, i.e., rental for the use of the equipment and installment towards the purchase

price.

The description given above, contains the following essential ingredients for

outlining the basic rules under Shari'ah:

�That there has to be a valuable use of the asset and transferability of that usufruct.

� That the ownership of the asset is retained by the transferor or lessor throughout the

lease period. Consumable cannot be leased.

� That the risk and liabilities of ownership lie with the lessor. The leased asset shall

remain the risk of the lessor throughout the lease period. Any loss or harm caused by

factors beyond the control of the lessee shall be borne by the lessor

� That the risk and liabilities associated with the use of the asset shall be borne by

the lessee

Islamic leasing :Islamic leasing :Islamic leasing :Islamic leasing :

12

Islamic Forward Modes : Islamic Forward Modes : Islamic Forward Modes : Islamic Forward Modes :

•IstisnaaIstisnaaIstisnaaIstisnaa (manufacturing) (manufacturing) (manufacturing) (manufacturing)

Is a contract to acquire goods on behalf of a third party where the price is paid to the

manufacturer in advance and the goods produced and delivered at a later date .

A contract in which advance payment is made for goods to be delivered later on. The seller

undertakes to supply some specific goods to the buyer at a future date in exchange of an

advance price fully paid at the time of contract. It is necessary that the quality of the

commodity intended to be purchased is fully specified leaving no ambiguity leading to

dispute.

•Bai'salamBai'salamBai'salamBai'salam ( prepaid purchase)( prepaid purchase)( prepaid purchase)( prepaid purchase)

Islamic Banking and Finance

13

SUMMARY:SUMMARY:SUMMARY:SUMMARY:

An Islamic bank is a deposit-taking banking institution whose scope of activities

includes all currently known banking activities, excluding borrowing and lending

on the basis of interest. On the liabilities side, it mobilizes funds on the basis of a

Mudarabah or Wakalah (agent) contract. It can also accept demand deposits which

are treated as interest-free loans from the clients to the bank. and which are

guaranteed. On the assets side, it advances funds on a profit-and–loss sharing or a

debt-creating basis, in accordance with the principles of the Sharīah. It plays the

role of an investment manager for the owners of time deposits, usually called

investment deposits. In addition, equity holding as well as commodity and asset

trading constitute an integral part of Islamic banking operations. An Islamic bank

shares its net earnings with its depositors in a way that depends on the size and

date-to-maturity of each deposit. Depositors must be informed beforehand of the

formula used for sharing the net earnings with the bank.

Difference between Islamic & Conventional BankingDifference between Islamic & Conventional BankingDifference between Islamic & Conventional BankingDifference between Islamic & Conventional Banking

Islamic Banking and Finance

14

Sayyid Tahir

Difference between Islamic & Conventional BankingDifference between Islamic & Conventional BankingDifference between Islamic & Conventional BankingDifference between Islamic & Conventional Banking

Islamic Banking and Finance

15

At the deposit end of the scale, Islamic banks normally operate four broad categories of

account :

•The current account

•The savings account

•Investment accounts

•Special investment accounts

Categories of Account :

Islamic Banking and Finance

16

Islamic Islamic Islamic Islamic SukukSukukSukukSukuk ( Bonds):( Bonds):( Bonds):( Bonds):

Is commonly described as an “Islamic bond”. which represent an undivided beneficial represent an undivided beneficial represent an undivided beneficial represent an undivided beneficial

ownership of an underlying assetownership of an underlying assetownership of an underlying assetownership of an underlying asset, , , , SukukSukukSukukSukuk is a Trust certificate in which investor returns is a Trust certificate in which investor returns is a Trust certificate in which investor returns is a Trust certificate in which investor returns

are derived from legal or beneficial ownership of assets . Certiare derived from legal or beneficial ownership of assets . Certiare derived from legal or beneficial ownership of assets . Certiare derived from legal or beneficial ownership of assets . Certificates of equal value ficates of equal value ficates of equal value ficates of equal value

representing proportionate ownership of tangible assets or usufrrepresenting proportionate ownership of tangible assets or usufrrepresenting proportionate ownership of tangible assets or usufrrepresenting proportionate ownership of tangible assets or usufructs or services or of ucts or services or of ucts or services or of ucts or services or of

the assets of a project or in an investment activity. (AAOIFI) the assets of a project or in an investment activity. (AAOIFI) the assets of a project or in an investment activity. (AAOIFI) the assets of a project or in an investment activity. (AAOIFI)

Islamic Banking and Finance

•Kinds of Kinds of Kinds of Kinds of SukukSukukSukukSukuk ::::

• SukukSukukSukukSukuk representing ownership in tangible assets (mostly based on Salerepresenting ownership in tangible assets (mostly based on Salerepresenting ownership in tangible assets (mostly based on Salerepresenting ownership in tangible assets (mostly based on Sale andandandand

Lease back or direct lease)Lease back or direct lease)Lease back or direct lease)Lease back or direct lease)

• SukukSukukSukukSukuk representing Usufructs or Services (based on sub lease or sale representing Usufructs or Services (based on sub lease or sale representing Usufructs or Services (based on sub lease or sale representing Usufructs or Services (based on sub lease or sale ofofofof

services)services)services)services)

• SukukSukukSukukSukuk representing equity share in a particular business or investmenrepresenting equity share in a particular business or investmenrepresenting equity share in a particular business or investmenrepresenting equity share in a particular business or investment portfoliot portfoliot portfoliot portfolio

(based on (based on (based on (based on MusharakahMusharakahMusharakahMusharakah/ / / / MudarabahMudarabahMudarabahMudarabah))))

• SukukSukukSukukSukuk representing receivable or future goods (based on representing receivable or future goods (based on representing receivable or future goods (based on representing receivable or future goods (based on MurabahaMurabahaMurabahaMurabaha or or or or SalamSalamSalamSalam ))))

IstisnaIstisnaIstisnaIstisna’’’’).).).).

17

Typical Typical Typical Typical SukukSukukSukukSukuk Structure for sale and leasebackStructure for sale and leasebackStructure for sale and leasebackStructure for sale and leaseback…………

Islamic Banking and Finance

Hamad Rasool

18

Islamic Banking and Finance

Flow of Funds Flow of Funds Flow of Funds Flow of Funds ---- Acquisition & RentalsAcquisition & RentalsAcquisition & RentalsAcquisition & Rentals

Hamad Rasool

19

Flow of Funds Flow of Funds Flow of Funds Flow of Funds ---- Repayment & MaturityRepayment & MaturityRepayment & MaturityRepayment & Maturity

Islamic Banking and Finance

Hamad Rasool

20

Islamic Banking and Finance

SukukSukukSukukSukuk AlAlAlAl----IjaraIjaraIjaraIjara based Model ( Example)based Model ( Example)based Model ( Example)based Model ( Example)

Hamad Rasool

21

Typical International Sukuk Mechanism – Step

by step…

Islamic Banking and Finance

Hamad Rasool

22

Islamic insuranceIslamic insuranceIslamic insuranceIslamic insurance---- TakafulTakafulTakafulTakaful

� Joint guarantee, Islamic alternative to insurance, is based on the concept of social

solidarity, cooperation and mutual indemnification of losses of members. It is an accord

among a group of persons who agree to jointly indemnify the loss or damage that may be

caused, out of the fund they donate collectively.

� Such a contract usually involves the concepts of Such a contract usually involves the concepts of Such a contract usually involves the concepts of Such a contract usually involves the concepts of MudarabaMudarabaMudarabaMudaraba, , , , TabarruTabarruTabarruTabarru (to donate for (to donate for (to donate for (to donate for

benefit of others). It is based on the concept of mutual sharingbenefit of others). It is based on the concept of mutual sharingbenefit of others). It is based on the concept of mutual sharingbenefit of others). It is based on the concept of mutual sharing of losses with the aim of of losses with the aim of of losses with the aim of of losses with the aim of

eliminating the element of uncertainty. eliminating the element of uncertainty. eliminating the element of uncertainty. eliminating the element of uncertainty.

� TakafulTakafulTakafulTakaful represents an important component in the overall Islamic financrepresents an important component in the overall Islamic financrepresents an important component in the overall Islamic financrepresents an important component in the overall Islamic financial system given ial system given ial system given ial system given

its role in the mobilization of longits role in the mobilization of longits role in the mobilization of longits role in the mobilization of long----term funds and providing risk protection. term funds and providing risk protection. term funds and providing risk protection. term funds and providing risk protection.

� TakafulTakafulTakafulTakaful is a way to reduce the financial risk of loss due to accident ais a way to reduce the financial risk of loss due to accident ais a way to reduce the financial risk of loss due to accident ais a way to reduce the financial risk of loss due to accident and misfortunes. In nd misfortunes. In nd misfortunes. In nd misfortunes. In

takafultakafultakafultakaful, the participant would pay particular amount of money as contri, the participant would pay particular amount of money as contri, the participant would pay particular amount of money as contri, the participant would pay particular amount of money as contribution (premium) bution (premium) bution (premium) bution (premium)

partly to risk fund (the participantspartly to risk fund (the participantspartly to risk fund (the participantspartly to risk fund (the participants’’’’ special account) using the concept of special account) using the concept of special account) using the concept of special account) using the concept of tabbarutabbarutabbarutabbaru

(donation) and another party ((donation) and another party ((donation) and another party ((donation) and another party (takafultakafultakafultakaful organization) with a mutual agreement that there organization) with a mutual agreement that there organization) with a mutual agreement that there organization) with a mutual agreement that there

would be a legal responsibility to provide for the participants would be a legal responsibility to provide for the participants would be a legal responsibility to provide for the participants would be a legal responsibility to provide for the participants a financial protection against a financial protection against a financial protection against a financial protection against

unexpected loss, should it happen within the agreed period.unexpected loss, should it happen within the agreed period.unexpected loss, should it happen within the agreed period.unexpected loss, should it happen within the agreed period.

Islamic Banking and Finance

23

Islamic Banking and Finance

Recapitulations in Islamic Money and banking :Recapitulations in Islamic Money and banking :Recapitulations in Islamic Money and banking :Recapitulations in Islamic Money and banking :

1111---- There is no need to be concerned with supply of money as long asThere is no need to be concerned with supply of money as long asThere is no need to be concerned with supply of money as long asThere is no need to be concerned with supply of money as long as factors of production exist. In other factors of production exist. In other factors of production exist. In other factors of production exist. In other

words, supply of money is closely tied with availability of factwords, supply of money is closely tied with availability of factwords, supply of money is closely tied with availability of factwords, supply of money is closely tied with availability of factors of production. This will necessarily lead ors of production. This will necessarily lead ors of production. This will necessarily lead ors of production. This will necessarily lead

to full employment. to full employment. to full employment. to full employment.

2222---- In the absence of interest, interestIn the absence of interest, interestIn the absence of interest, interestIn the absence of interest, interest----based loans disappear and banks become "asset" producers. based loans disappear and banks become "asset" producers. based loans disappear and banks become "asset" producers. based loans disappear and banks become "asset" producers.

3333---- The elimination of interest erodes money whirlpool, as well asThe elimination of interest erodes money whirlpool, as well asThe elimination of interest erodes money whirlpool, as well asThe elimination of interest erodes money whirlpool, as well as any speculative demand for money. This any speculative demand for money. This any speculative demand for money. This any speculative demand for money. This

4444---- History testifies that rate of profit is much higher than longHistory testifies that rate of profit is much higher than longHistory testifies that rate of profit is much higher than longHistory testifies that rate of profit is much higher than long----term interest rates. In fact, so long as term interest rates. In fact, so long as term interest rates. In fact, so long as term interest rates. In fact, so long as

speculation is permitted they never become equal. Therefore, depspeculation is permitted they never become equal. Therefore, depspeculation is permitted they never become equal. Therefore, depspeculation is permitted they never become equal. Therefore, depositors in Islamic banking system will ositors in Islamic banking system will ositors in Islamic banking system will ositors in Islamic banking system will

enjoy high rates of profit, however volatile. This will somehow enjoy high rates of profit, however volatile. This will somehow enjoy high rates of profit, however volatile. This will somehow enjoy high rates of profit, however volatile. This will somehow bridge the gap among income strata. bridge the gap among income strata. bridge the gap among income strata. bridge the gap among income strata.

5555---- Risk of depositing in an Islamic banking system is less than tRisk of depositing in an Islamic banking system is less than tRisk of depositing in an Islamic banking system is less than tRisk of depositing in an Islamic banking system is less than that of buying a share in stock market, hat of buying a share in stock market, hat of buying a share in stock market, hat of buying a share in stock market,

This is due to several factors:This is due to several factors:This is due to several factors:This is due to several factors:(a) deposits and returns to numerous financed projects are bein(a) deposits and returns to numerous financed projects are bein(a) deposits and returns to numerous financed projects are bein(a) deposits and returns to numerous financed projects are being pooled .Further more, risks of these g pooled .Further more, risks of these g pooled .Further more, risks of these g pooled .Further more, risks of these

projects are not of the same kind neither of the same magnitude.projects are not of the same kind neither of the same magnitude.projects are not of the same kind neither of the same magnitude.projects are not of the same kind neither of the same magnitude. It follows that pooled risk is logically It follows that pooled risk is logically It follows that pooled risk is logically It follows that pooled risk is logically

expected to be less than that of one individual share.expected to be less than that of one individual share.expected to be less than that of one individual share.expected to be less than that of one individual share.

(b) Two kinds of deposits can be suggested to depositors; one w(b) Two kinds of deposits can be suggested to depositors; one w(b) Two kinds of deposits can be suggested to depositors; one w(b) Two kinds of deposits can be suggested to depositors; one with variable return and the other with ith variable return and the other with ith variable return and the other with ith variable return and the other with

fixed return. Both of these, of course, shall be compensated forfixed return. Both of these, of course, shall be compensated forfixed return. Both of these, of course, shall be compensated forfixed return. Both of these, of course, shall be compensated for by the pooled returns of the financed by the pooled returns of the financed by the pooled returns of the financed by the pooled returns of the financed

projects.projects.projects.projects.

7777---- Inflation does not have an adverse effect on the balance sheetInflation does not have an adverse effect on the balance sheetInflation does not have an adverse effect on the balance sheetInflation does not have an adverse effect on the balance sheet of an Islamic bank. This derives from of an Islamic bank. This derives from of an Islamic bank. This derives from of an Islamic bank. This derives from

the nature of profit and loss sharing in which the real values othe nature of profit and loss sharing in which the real values othe nature of profit and loss sharing in which the real values othe nature of profit and loss sharing in which the real values of assets and liabilities would move in the f assets and liabilities would move in the f assets and liabilities would move in the f assets and liabilities would move in the

same direction in the event of economic shocks. Whereas, in casesame direction in the event of economic shocks. Whereas, in casesame direction in the event of economic shocks. Whereas, in casesame direction in the event of economic shocks. Whereas, in case of conventional banking, the of conventional banking, the of conventional banking, the of conventional banking, the

purchasing power of loans decline during inflationary periods. Hpurchasing power of loans decline during inflationary periods. Hpurchasing power of loans decline during inflationary periods. Hpurchasing power of loans decline during inflationary periods. Hence, the Islamic banking protects ence, the Islamic banking protects ence, the Islamic banking protects ence, the Islamic banking protects

depositors against any decline in the real value of their (monetdepositors against any decline in the real value of their (monetdepositors against any decline in the real value of their (monetdepositors against any decline in the real value of their (monetary) assets.. ary) assets.. ary) assets.. ary) assets..

Iraj Toutounchian, Ph.D.

Banking and Finance

24

1.1.1.1. Time Value of Money Time Value of Money Time Value of Money Time Value of Money

Islamic principles differ from the capitalist theory as money and commodity have different

characteristics, for instance money has no intrinsic value but is only a measure of value

or a medium of exchange, it is not capable of fulfilling human needs by itself, unless

converted into a commodity.

2.2.2.2. Trading in stocks :Trading in stocks :Trading in stocks :Trading in stocks :

As long as the company’s business and financial position are acceptable, there is no reason

to believe that trading in the company’s shares is not permissible.

Subjects in QuestionsSubjects in QuestionsSubjects in QuestionsSubjects in Questions

3. legal status of loans in Islamic law :3. legal status of loans in Islamic law :3. legal status of loans in Islamic law :3. legal status of loans in Islamic law :

Loans are a charitable contract

Islamic Banking and Finance

25

Islamic Windows in the conventional banks :

•Commerz bank

•Deutsche Bank

•HSBC Bank

•Standard Chartered

Deutsche Bank … An Example:

Islamic Banking and Finance

ADCB

26

Islamic Banking and Finance

Thank you for attention

For Questions , please contact me at :

![[123doc.vn] Bai Tap Trac Nghiem Tieng Anh 12 Tu Bai de Bai 7 0476](https://static.fdocuments.us/doc/165x107/55cf8f51550346703b9b23a1/123docvn-bai-tap-trac-nghiem-tieng-anh-12-tu-bai-de-bai-7-0476.jpg)