IRS Practice and Procedure Update – 2014 · 24/11/2014 · IRS Practice and Procedure Update –...

62

IRS Practice and Procedure Update – 2015 Stuart Sobel Tax Media Network, Inc.

Transcript of IRS Practice and Procedure Update – 2014 · 24/11/2014 · IRS Practice and Procedure Update –...

IRS Practice and Procedure Update – 2015

Stuart SobelTax Media Network, Inc.

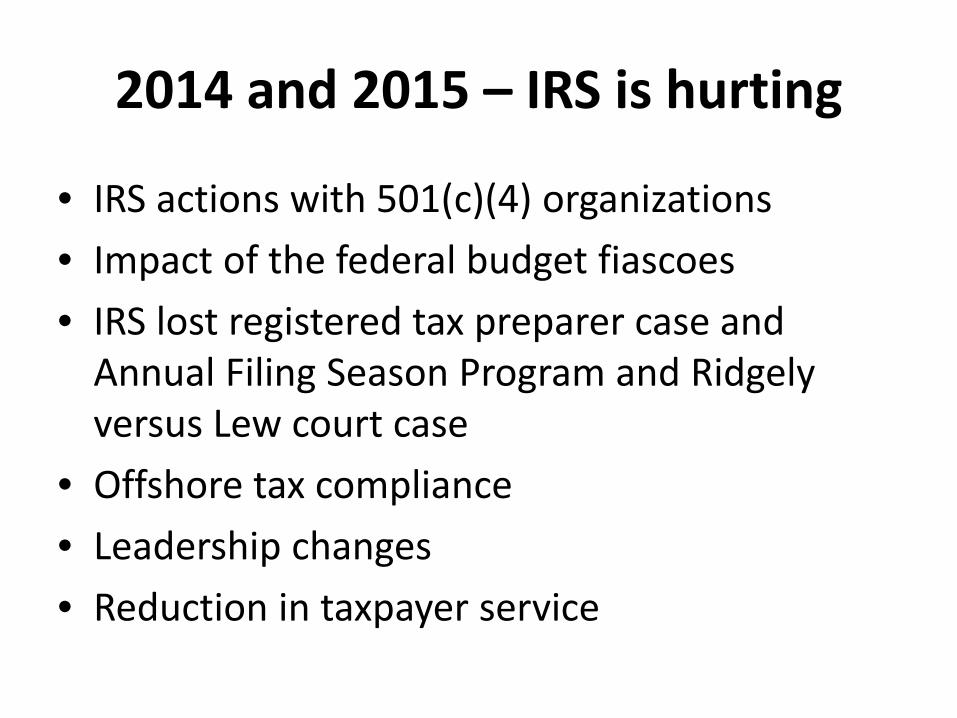

2014 and 2015 – IRS is hurting

• IRS actions with 501(c)(4) organizations• Impact of the federal budget fiascoes• IRS lost registered tax preparer case and

Annual Filing Season Program and Ridgelyversus Lew court case

• Offshore tax compliance• Leadership changes• Reduction in taxpayer service

IRS Taxpayer Advocate, Nina Olsen’s, annual report to Congress

• Need for “Taxpayer Bill of Rights”– Survey showed less than half of respondents

believed they have rights before the IRS, and only 11% said they knew what those rights were.

– The taxpayer advocate proposed specific rights in her report.

Taxpayer Advocate report (cont.)-2014

• IRS funding inadequate– Each year more than 100 million taxpayers call IRS

and millions more visit walk-in sites or send correspondence.

– Cannot keep up with demand– Funding and staffing cut by 8%– Can answer only 61% of calls – 87% answered 10

years ago

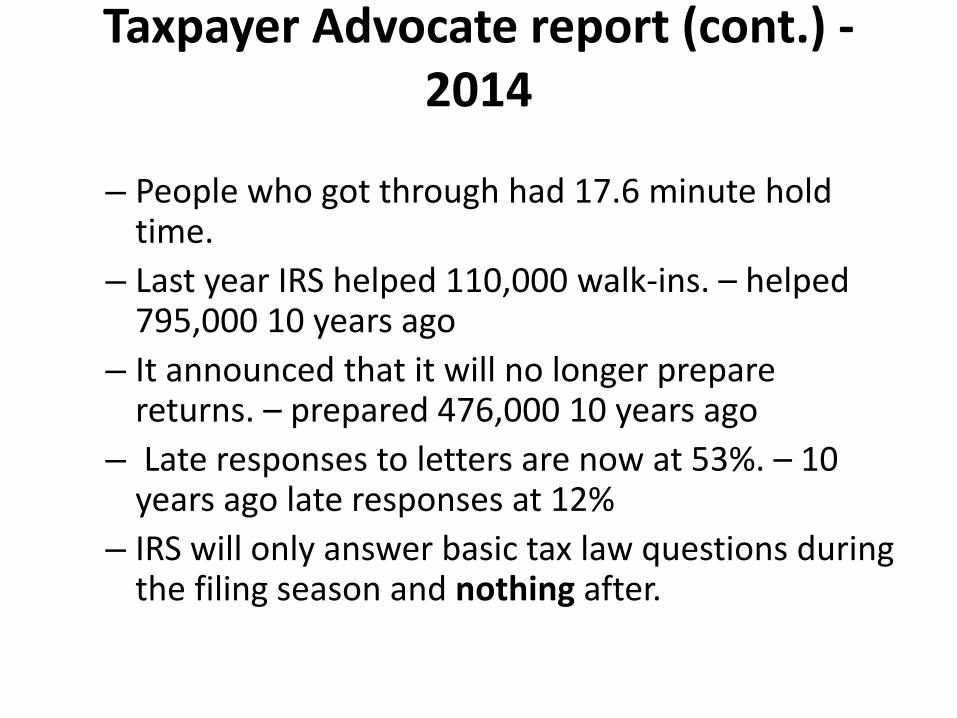

Taxpayer Advocate report (cont.) -2014

– People who got through had 17.6 minute hold time.

– Last year IRS helped 110,000 walk-ins. – helped 795,000 10 years ago

– It announced that it will no longer prepare returns. – prepared 476,000 10 years ago

– Late responses to letters are now at 53%. – 10 years ago late responses at 12%

– IRS will only answer basic tax law questions during the filing season and nothing after.

Taxpayer Advocate report (cont.) -2015

• THE MOST SERIOUS PROBLEMS ENCOUNTERED BY TAXPAYERS

• The Right to Quality Service• 1. TAXPAYER SERVICE: Taxpayer Service Has Reached Unacceptably Low Levels and• Is Getting Worse, Creating Compliance Barriers and Significant Inconvenience for• Millions of Taxpayers . • 2. TAXPAYER SERVICE: Due to the Delayed Completion of the Service Priorities• Initiative, the IRS Currently Lacks a Clear Rationale for Taxpayer Service Budgetary• Allocation Decisions• 3. IRS LOCAL PRESENCE: The Lack of a Cross-Functional Geographic Footprint• Impedes the IRS’s Ability to Improve Voluntary Compliance and Effectively Address• Noncompliance . • 4. APPEALS: The IRS Lacks a Permanent Appeals Presence in 12 States and Puerto

Rico, Thereby Making It Difficult for Some Taxpayers to Obtain Timely and Equitable Face to-Face Hearings with an Appeals Officer or Settlement Officer in Each State .

Taxpayer Advocate report (cont.) -2015

• 5. VITA/TCE FUNDING: Volunteer Tax Assistance Programs Are Too Restrictive and the Design Grant Structure Is Not Adequately Based on Specific Needs of Served Taxpayer Populations .

• The Right to a Fair and Just Tax System: Complexity• 6. HEALTH CARE IMPLEMENTATION: Implementation of the

Affordable Care Act may Unnecessarily Burden Taxpayers . • 7. OFFSHORE VOLUNTARY DISCLOSURE (OVD): The OVD

Programs Initially undermined the Law and Still Violate Taxpayer Rights .

• 8. PENALTY STUDIES: The IRS Does Not Ensure Penalties Promote Voluntary Compliance, as Recommended by Congress and Others

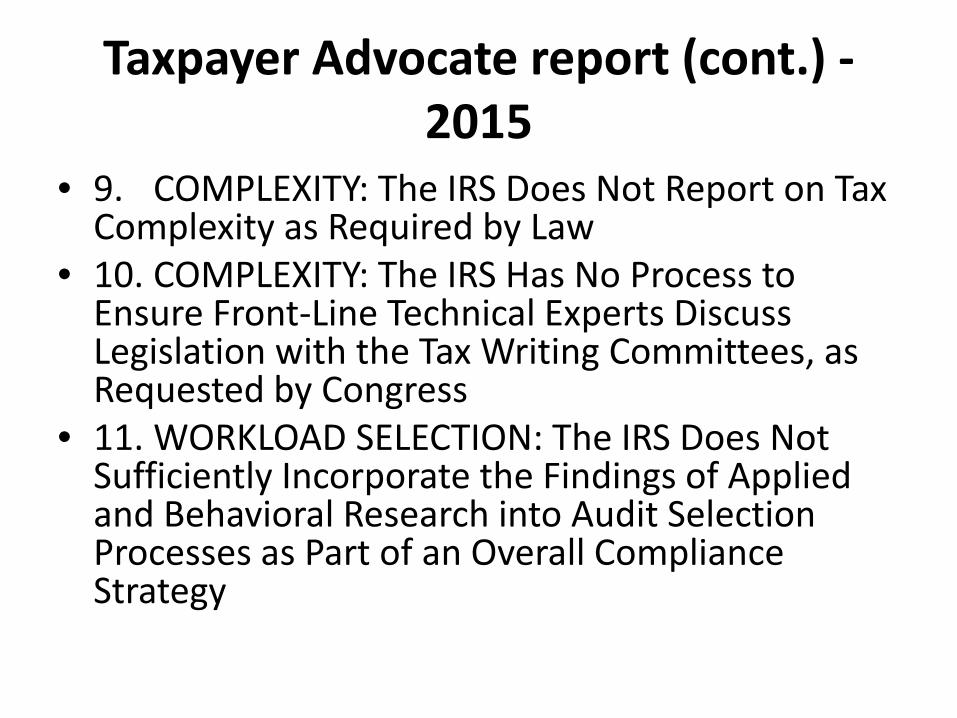

Taxpayer Advocate report (cont.) -2015

• 9. COMPLEXITY: The IRS Does Not Report on Tax Complexity as Required by Law

• 10. COMPLEXITY: The IRS Has No Process to Ensure Front-Line Technical Experts Discuss Legislation with the Tax Writing Committees, as Requested by Congress

• 11. WORKLOAD SELECTION: The IRS Does Not Sufficiently Incorporate the Findings of Applied and Behavioral Research into Audit Selection Processes as Part of an Overall Compliance Strategy

Taxpayer Advocate report (cont.) -2015

• The Right to Be Informed: Access to the IRS• 12. ACCESS TO THE IRS: Taxpayers Are Unable to Navigate the IRS and Reach the• Right Person to Resolve Their Tax Issues• 13. CORRESPONDENCE EXAMINATION: The IRS Has Overlooked the• Congressional Mandate to Assign a Specific Employee to Correspondence Examination• Cases, Thereby Harming Taxpayers . • 14. AUDIT NOTICES: The IRS’s Failure to Include Employee Contact Information on• Audit Notices Impedes Case Resolution and Erodes Employee Accountability . • 15. VIRTUAL SERVICE DELIVERY: Despite a Congressional Directive, the IRS Has• Not Maximized the Appropriate Use of Videoconferencing and Similar Technologies to• Enhance Taxpayer Services .

• The Right to Be Informed: Adequate Explanations• 16. MATH ERROR NOTICES: The IRS Does Not Clearly Explain Math Error• Adjustments, Making it Difficult for Taxpayers to Understand and Exercise Their Rights . • 17. NOTICES: Refund Disallowance Notices Do Not Provide Adequate Explanations

Taxpayer Advocate report (cont.) -2015

• The Rights to Privacy and to a Fair and Just Tax System

• 18. COLLECTION DUE PROCESS: The IRS Needs Specific Procedures for Performing the Collection Due Process Balancing Test to Enhance Taxpayer Protections

• 19. FEDERAL PAYMENT LEVY PROGRAM: Despite Some Planned Improvements, Taxpayers Experiencing Economic Hardship Continue to Be Harmed by the Federal Payment Levy Program

• 20. OFFERS IN COMPROMISE: Despite Congressional Actions, the IRS Has Failed to Realize the Potential of Offers in Compromise

• 21. OFFERS IN COMPROMISE: The IRS Does Not Comply with the Law Regarding Victims of Payroll Service Provider Failure .

• 22. MANAGERIAL APPROVAL FOR LIENS: The IRS’s Administrative Approval Process for Notices of Federal Tax Lien Circumvents Key Taxpayer Protections in RRA 98

• 23. STATUTORY NOTICES OF DEFICIENCY: Statutory Notices of Deficiency Do Not Include Local Taxpayer Advocate Office Contact Information on the Face of the Notices .

Tax Gap - 2014

• IRS loses $450 billion annually due to taxpayer noncompliance that includes underreporting, income, overstating deductions and credits, non-filing, and nonpayment.

• IRS notices increased 570% from 2001.• IRS examinations increased 100% from 2001

with correspondence exams making up 74% of the total.

Tax Gap (cont.)

• The IRS assessed about 37.9 million (or $25.9 billion in aggregate) civil penalties in FY 2013, up from about 15 million (or $1.3 billion in aggregate) in FY 1978 (the earliest year available). It also abated about 4.9 million civil penalties (or $11.5 billion in aggregate) in FY 2013, up from 1.4 million (or $338 million in aggregate) in FY 1978.

• IRM 20 – Penalty Handbook discussion

IRS employees disciplined for bypassing representatives

• Ignoring powers of attorney and going directly to taxpayers

• More prevalent with collection function• Powers of attorney for a husband and wife • Powers of attorney should be specific for tax,

penalties, or other items.

New IRS commissioner, John Koskinen– priorities

• Improve tax compliance– Fight refund fraud– Fight identity theft– Improve international tax compliance – Properly implement the Affordable Care Act

• Improve IRS morale

IRS commissioner priorities (cont.)

• Restore budget cuts• Supports voluntary certification of tax

preparers as a result of Loving case– Inspire preparers to apply and comply with the

requirements– Do some lobbying with Congress to legislate the

RTP

Internal Revenue Service Advisory Council (IRSAC) 2014 Report and

Recommendations

• Declining Federal Revenues• Every dollar devoted to tax enforcement yields

a substantial increase in tax collections, and reducing funding in the IRS’s tax enforcement efforts results in significantly lower tax collections

Internal Revenue Service Advisory Council (IRSAC) 2014 Report and

Recommendations• Lack of Necessary Service Personnel at Required Experience

Levels• The IRS must recruit and properly train a sufficient staff to perform the critical

functions that Congress has assigned it in the face of complex and constantly changing tax laws. With many senior IRS personnel opting for retirement, and funding limits preventing many vacancies from being filled, IRSAC is concerned that the IRS will not have sufficient personnel to address taxpayer needs. Since the IRS’s training budget has already been reduced by 85 percent since fiscal year 2009[4] we are concerned about the adverse effects this reduction may have on tax administration and taxpayer rights.

• Although the IRS made major strides to automate its systems and operations in its taxpayer service and enforcement functions, many essential IRS programs remain people-intensive and highly dependent on qualified personnel, supported by appropriate levels of funding for compensation, training, travel, and other items. The IRS responded to current cuts through hiring freezes, reduced funding for grants and other expenditures, and cuts in travel, training, facilities, supplies and other costs.

Internal Revenue Service Advisory Council (IRSAC) 2014 Report and

Recommendations• Negative Effects on the Service’s Ability to

Administer the Law Fairly• The decline in budget resources unavoidably

adversely impacted enforcement programs. Further, the IRS is required by law to implement congressionally enacted laws, such as FATCA and the ACA, and a number of other complex statutes.[5] The IRSAC commends the IRS’s efforts to blunt the effects of a reduced budget, but reluctantly concluded that the agency’s ability to carry out these duties runs the risk of being significantly compromised because the necessary resources are simply not available.

Internal Revenue Service Advisory Council (IRSAC) 2014 Report and

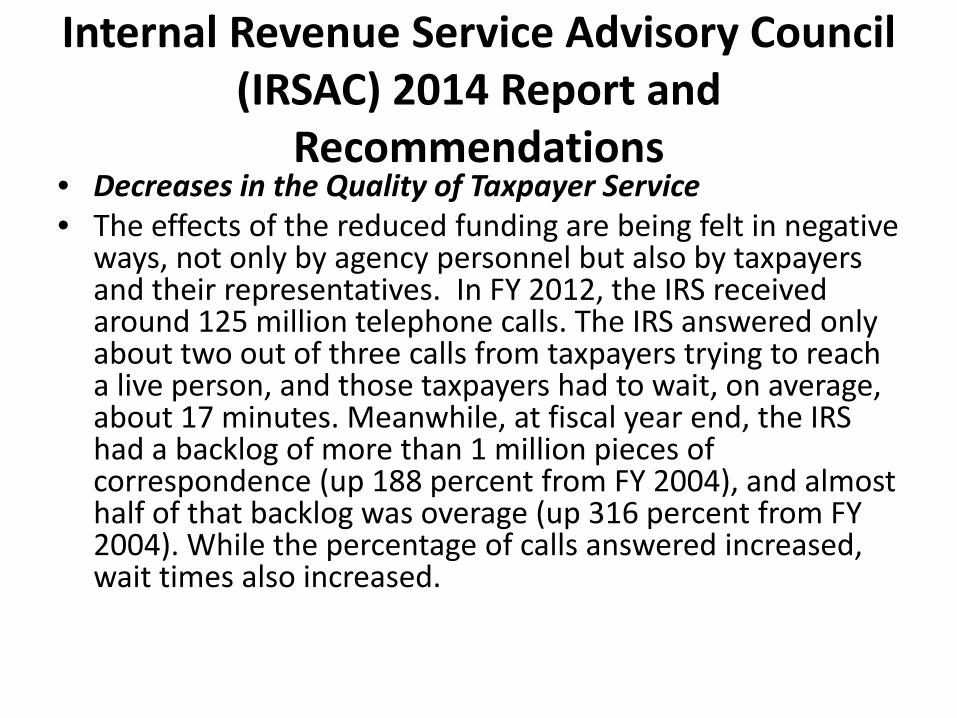

Recommendations• Decreases in the Quality of Taxpayer Service• The effects of the reduced funding are being felt in negative

ways, not only by agency personnel but also by taxpayers and their representatives. In FY 2012, the IRS received around 125 million telephone calls. The IRS answered only about two out of three calls from taxpayers trying to reach a live person, and those taxpayers had to wait, on average, about 17 minutes. Meanwhile, at fiscal year end, the IRS had a backlog of more than 1 million pieces of correspondence (up 188 percent from FY 2004), and almost half of that backlog was overage (up 316 percent from FY 2004). While the percentage of calls answered increased, wait times also increased.

Internal Revenue Service Advisory Council (IRSAC) 2014 Report and

Recommendations• Effects on a System Based on Voluntary Compliance• The IRS’s enforcement efforts — its work to close the

“tax gap” (which has been estimated at nearly $400 billion a year) — are also affected by the funding question. In FY 2012, the IRS brought in federal revenue of about $2.52 trillion on a budget of $11.8 billion, a return-on-investment (ROI) of 214:1. As the IRS recently estimated in a letter to Congress, reductions in the enforcement budget will inevitably and negatively affect the level of tax collections by as much as seven times the amount of the budget cuts.

TIGTA report – IRS needs to improve pickup of prior, subsequent, or related

returns• Overemphasis on correspondence

examinations – 74% of all examinations• Correspondence returns should consider the

pickups of other returns• Secure extensions of time to older years for

examinations

IRS exams of individuals at lowest rate since 2005

• IRS examined 0.96% of individual tax returns in 2013.

• Revenue generated from audits was $9.83 billion. – The first time since 2007 that it was less than $10 billion.

• IRS has 19,531 in enforcement , which is down 14% since 2010

IRS targets small businesses

• IRS Warns Tax Return Preparers About Schedule C Errors • The IRS has mailed out more than 2,500 letters in December 2014 to tax

return preparers who have been guilty of foiling a faulty Schedule C, Profit or Loss from Business (Sole Proprietorship). The gist of the message: Do better next time.

• However, while the IRS appears to treating wayward practitioners with kid gloves for the time being, don’t expect examiners to be as lenient during the 2015 tax-filing season. Repeat offenders could be slapped with penalties for as much as $5,000 per return.

• This isn’t the first time the IRS has addressed this issue. After sending out tens of thousands of such letters in the past, the IRS updated its posting of Letter 5105 on November 24, 2014. It says that the IRS has reviewed tax returns the recipient prepared in the past year and discovered many have a high percentage of traits typically resulting in errors on Schedule C. The letter reminds tax professionals of their responsibilities and stresses the need for continued educational assistance.

IRS plans to reduce large corporate examinations

• IRS is planning 18% reduction in the audits of large businesses for the current fiscal year.

• Why did the IRS implement the recent repair and capitalization regulations?

IRS Taxpayer Service changes in 2014 and 2015

• IRS tax preparation at offices disappearing and taxpayers being referred to VITA sites

• Instantly view and print copies of transcripts of five types of accounts from IRS website.– Tax account– Tax return– Record of account – Wage and income– Verification of non-filing

IRS Taxpayer Service changes (cont.)

• Tax law –IRS provides minimal assistance– Refers people to IRS website tools and

publications– Encourages people to use software, i.e., TurboTax – Suggests calling a tax professional

• Tax refund inquiries– Where’s my refund?– IRS2GO phone app.

TIGTA report on return preparer penalties

• IRS did not pursue penalties in many cases.• IRS managers were lax in the assertion of

penalties.• IRS examiners did not properly document

their case files.• IRS did not adequately pursue unpaid return

preparer penalties that had been asserted.

IRS visiting preparers for EITC and EITC improvement

• Questionable returns will require preparers to have face-to-face contact with the IRS.

• Preparers will have to show documentation as to EITC to determine whether their client’s claims are valid

• TIGTA says the IRS is not in compliance with certain requirements of Executive Order 13520 for Fiscal Year 2013. The IRS has not established annual improper payment reduction targets as required. Nonetheless, the IRS is making some progress related to its inability to comply with this requirement.

TIGTA report – penalties not asserted on erroneous refund and credit claims

• IRS improperly interpreted the Small Business and Work Opportunity Tax Act of 2007 – IRC 6676

• Excessive tax credits or refunds may be penalized up to 20%.

• IRS asserted only 84 penalties in a 5-year period. • IRS had not established guidance or written

directions.• Cases cannot go to tax court.

Ridgely v. Lew

• In Ridgely, the taxpayer was a CPA who prepared tax returns and provided tax planning and audit protection to his clients. Ridgely filed an original claim for refund for a client — meaning that without first being contacted by the IRS, Ridgelycarried back the client’s loss to a previous period and requested a refund of previously paid tax —and wished to charge the client a contingent fee for his services based on the amount of the refund.

Ridgely v. Lew

• In 2007, Circular 230 was amended to prohibit tax practitioners from charging contingent fees for certain services, including filing tax returns or refund claims. The rule was enacted because the IRS was concerned that if a tax preparer took lucrative contingent fees from companies whose books they also audit, it would jeopardize auditor independence because it leads accountants and their clients to share financial interests.

Ridgely v. Lew

• Ridgely brought suit against the IRS arguing, similar to Loving, that he wasn’t subject to Circular 230 — and thus the bar on contingent fees — because merely filing an original claim for refund did not constitute “practice before the IRS. Ridgely wouldn’t be subject to Circular 230, in his estimation, until such time that the IRS challenged the refund claim, creating the type of dispute that would require Ridgely to “present his client’s case” and “practice before the IRS.”

Ridgely v. Lew • As it did in Loving, the DC District Court agreed with the

taxpayer, concluding that Ridgely was not subject to Circular 230 when all he did was file an original claim for refund. Essentially, the court established that when determining whether a CPA, attorney, enrolled agent or TRP is subject to the rules of Circular 230, you must consider scope.

• Citing Loving, it was clear to the court that when a taxpayer merely files a tax return, in the absence of an established adversarial dispute with the IRS, the filing of the return does not constitute practice before the IRS. This should hold true, the court determined, whether the return was field by a TRP, CPA, enrolled agent, or attorney.

Senators Unveil Bill to Regulate Tax Preparers – January 2015

• Two Democrats on the Senate Finance Committee have introduced legislation to regulate paid tax preparers in response to the federal court decision that found the Internal Revenue Service had exceeded its statutory authority in regulating preparers.

Senate Finance Committee ranking member Ron Wyden, D-Ore., and Senator Ben Cardin, D-Md., unveiled legislation Thursday that provides the Treasury Department and the IRS explicit authority to regulate paid tax return preparers. Wyden chaired the committee until control of the Senate changed after last November’s elections.

10 most litigated tax issues

TIGTA: Billions lost to potential child tax credit fraud

• Potential abuse of a popular tax-credit program is costing the government billions of dollars, the IRS inspector general said in findings that may ramp up the debate over undocumented workers getting government benefits.

• The IRS paid out at least $5.9 billion in improper payments of the additional child tax credit in fiscal year 2013, or about 25 percent to 30 percent of total payments, the Treasury inspector general for tax administration said Tuesday.

• The IG previously reported that unauthorized workers were a major source of the improper payments, though that wasn’t spelled out in its most recent report.

• The inspector general took the IRS to task for not taking the potential fraud seriously, like it does with another popular credit program prone to abuse, the earned income tax credit.

TIGTA – IRS does not notify practitioners about clients’ tax liens

• Must notify taxpayers within five days after filing

• Forgot about the powers of attorney• Recommended changes to the notice of the

lien identifying the power of attorney

IRS installment agreements

• Fee is $120 – No change for prior year• Restructuring or restating an agreement is $50• Direct debit installment is $52 • Offer in compromise is $186 - Use Pre-

Qualifier Tool on IRS website

Post-Appeals Mediation For Offers in Compromise Available Nationwide

• The Internal Revenue Service released a revenue procedure providing rules for the nationwide rollout of post-Appeals mediation for Offer in Compromise (OIC) and Trust Fund Recovery Penalty (TFRP) cases. The IRS Office of Appeals originally launched post-Appeals mediation for OIC and TFRP cases as a pilot programavailable in certain cities in December 2008.

• Post-Appeals mediation is available to help resolve disputes after unsuccessful negotiations with the IRS Office of Appeals and is available for both factual and legal issues. The mediator’s role is to assist the parties in reaching their own agreement collaboratively, but the mediator does not have settlement authority over any issue. Appeals Officers trained in mediation techniques will serve as mediators at no cost to taxpayers. Taxpayers also have the option of paying for a qualified non-IRS co-mediator.

Offers In Compromise

• A new revision of the Form 656-B booklet, with forms and instructions for submitting an Offer in Compromise (OIC), will be available on IRS.gov in January 2015. The use of earlier versions after Jan. 1 will delay the processing of OIC applications

IRS, National Tax Groups Offer Help Selecting a Tax Preparer; Tips, New Web

Page Unveiled• The Internal Revenue Service joined with national tax

organizations to provide people with new options to get information and tips on selecting tax professionals and avoiding unscrupulous preparers.

• The effort includes new information available at IRS.gov/chooseataxpro, including a list of consumer tips for selecting a tax professional. There will also be a new gateway page with links to national non-profit tax professional groups, which can help provide additional information for taxpayers seeking the right type of qualified help.

IRS Fast Track Settlement Program for small businesses

• Fast Track Settlement (FITS) is modeled after a program long available to businesses with $10 million plus in assets.

• FITS is a new program that enables small businesses under audit to settle more quickly with IRS.

• IRS uses alternative dispute resolution and avoids formal appeal or litigation.

• Cases can be resolved in 60 days.• Taxpayers work with exam and appeals before IRS

issues a 30-day letter.

IRS Makes Novel Use Of Outside Contractors---To Audit Microsoft

• Is this a new concept?• What could the future look like?

IRS updates procedures for letter rulings, technical advice, determination letters, and

closing agreements• IRS issued revenue procedures 2015-1 through 2015-6• Specified “no ruling” areas for which the IRS will not issue letter rulings• Defined the areas that are covered by automatic approval procedures• The basic fee to get a private letter ruling from IRS is soaring to $28,300• for requests received by the agency after Feb. 1, 2015. The current levy is

$19,000.• The charge is much lower for taxpayers with gross income of less than $1

million…$2,200 for those with incomes under $250,000, and $6,500 for filers with incomes between $250,000 and $1 million.

IRS Issues Updated No-Ruling Lists

• On January 2, 2015, the Internal Revenue Service (IRS) issued revenue procedures to update the list of those areas of the United States tax code in which the agency will not issue letter rulings or determination letters under any circumstances, or will issue letters only if unique and compelling circumstances justify it.

IRS issues virtual currency (Bitcoin) guidelines

• Notice 2014-21was issued March 25, 2014• Wages paid in virtual currency are taxable to the

employees and subject to employer payroll tax reporting.

• Payments to independent contractors have 1099 requirements.

• Gain or loss from a sale or exchange depends upon whether or not the virtual currency was a capital asset.

• Virtual payments subject to information reporting just like any other property.

• CPA disbarred for multiple Circular 230 violations• Anthony A. Tiongson of California disbarred• Charged unconscionable fees, gave irresponsible advice

to clients, and made false statements to IRS and state authorities

• Advised clients to show California earned income as foreign source income on Form 2555

• Charged contingent fees and was dilatory• Prohibited from preparing returns or representing

clients for a minimum of five years

IRS' Automatic Taxpayer Levy Too Harsh, Tax Court Says

• Budish versus Commissioner• The U.S. Tax Court ordered the Internal Revenue

Service to reassess whether it can appropriately maintain that a taxpayer can enter a tax installment agreement only if the agency can also issue a levy notice, saying the IRS must address potential intrusiveness concerns.

An agency appeals officer said that it had to file a notice of levy in spite of the agreement because James B. Budish’s liability exceeded $200,000, and that the IRS needed the lien to protect the government’s interest. The taxpayer balked...

Noncustodial parents need Form 8332 to claim children as dependents

• Shenk, 140 T.C. No. 10• Wife did not sign Form 8332 to release her

claim to children.• Failure to sign also cost head-of-household

status and child tax credit.• Divorce decrees after 2008 cannot be used in

lieu of Form 8332.

Preparer’s error in not using the installment method can be corrected

• Private letter ruling:• Taxpayer wanted to report gain on the sale of

assets on the installment method.• Preparer made a mistake by reporting full gain

in the first year.• IRS approved the late installment election,

because the request was made soon after the error was found and within the 3-year statute

IRS New Method to Find Money Off-Shore

• It’s sending summonses to delivery companies such as FedEx, UPS, and DHL in a probe of Sovereign Management & Legal Ltd., an offshore financial services firm.

• This helps the IRS sniff out the names of customers who it suspects are evading taxes.

• A federal court OK’d the summonses.

Collection due process hearing cannot be used to review an unprocessible

offer in compromise

• Reed v. Commissioner 2013 U.S. Tax Ct.• IRS returns unprocessable offers when they do

not meet specific requirements, i.e., out-of-date financial information.

• The return of an offer is not a rejection of the offer

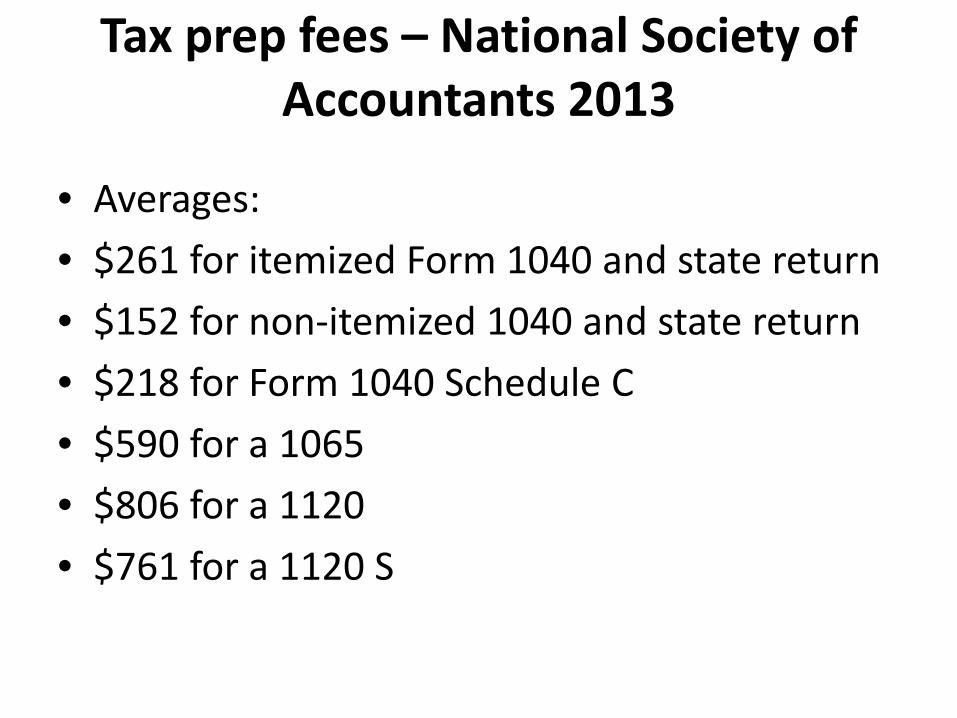

Tax prep fees – National Society of Accountants 2013

• Averages:• $261 for itemized Form 1040 and state return• $152 for non-itemized 1040 and state return• $218 for Form 1040 Schedule C• $590 for a 1065• $806 for a 1120• $761 for a 1120 S

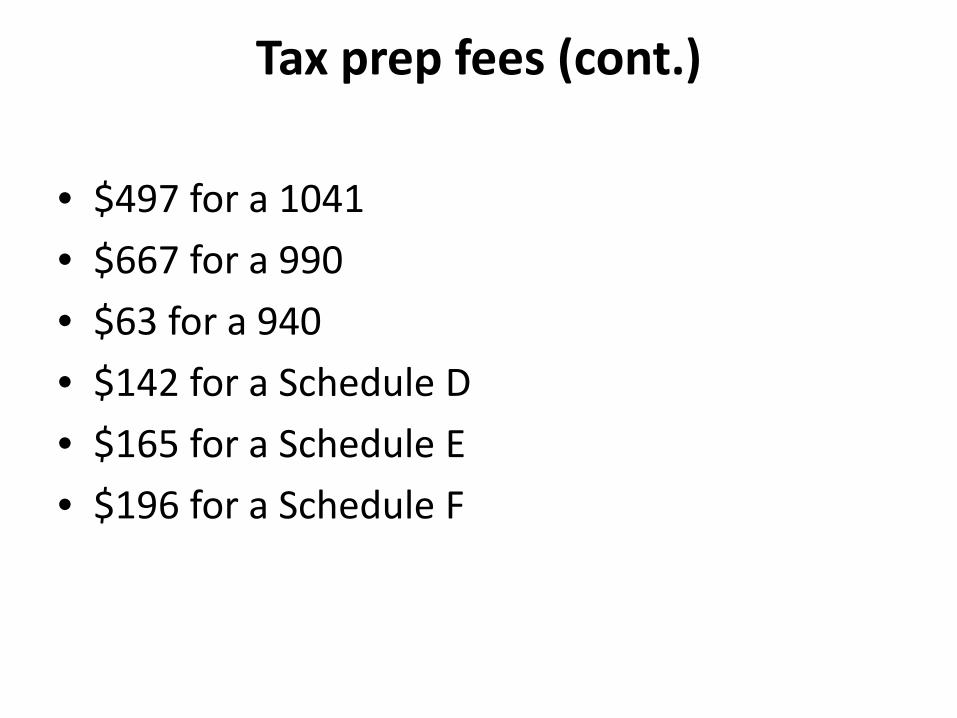

Tax prep fees (cont.)

• $497 for a 1041• $667 for a 990• $63 for a 940• $142 for a Schedule D • $165 for a Schedule E• $196 for a Schedule F

Marijuana sellers – heavy tax burden

• Sales are taxable, but sellers cannot write off any business expenses except the cost of the marijuana.

• This applies in any state whether it is allowed for medicinal or recreational use.

• IRC 280

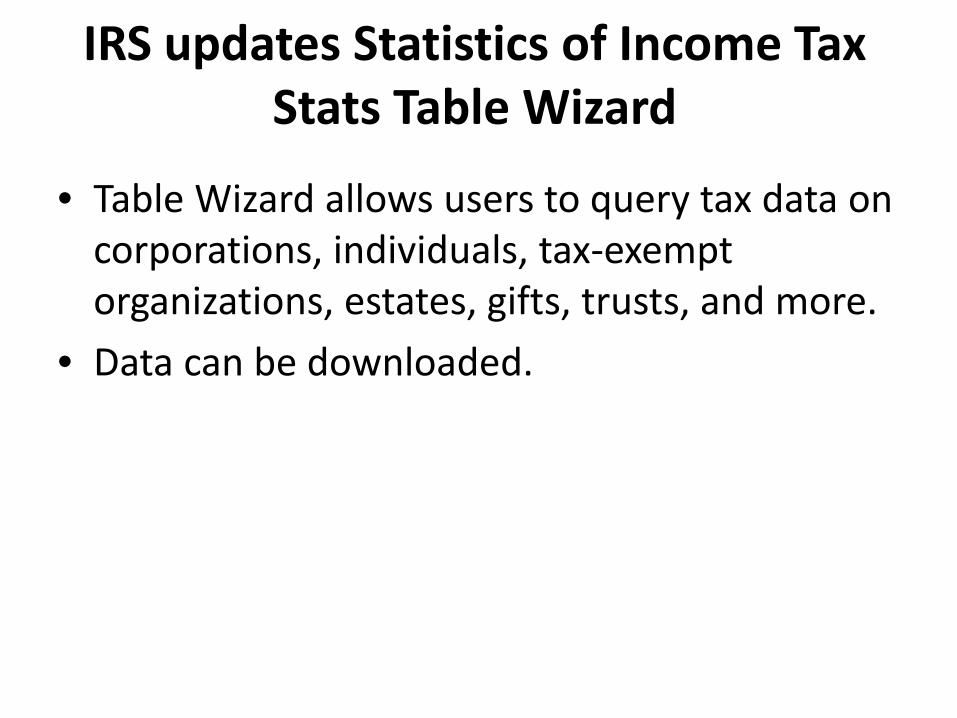

IRS updates Statistics of Income Tax Stats Table Wizard

• Table Wizard allows users to query tax data on corporations, individuals, tax-exempt organizations, estates, gifts, trusts, and more.

• Data can be downloaded.

New IRS Discovery Tool debuts for international taxpayers

• Taxpayers with international filing requirements now have a great IRS tool.

• Over 500 IRS.gov web pages with international content were linked to topics.

• Web pages were integrated to forms, publications, and FAQs.

• An international index was created.

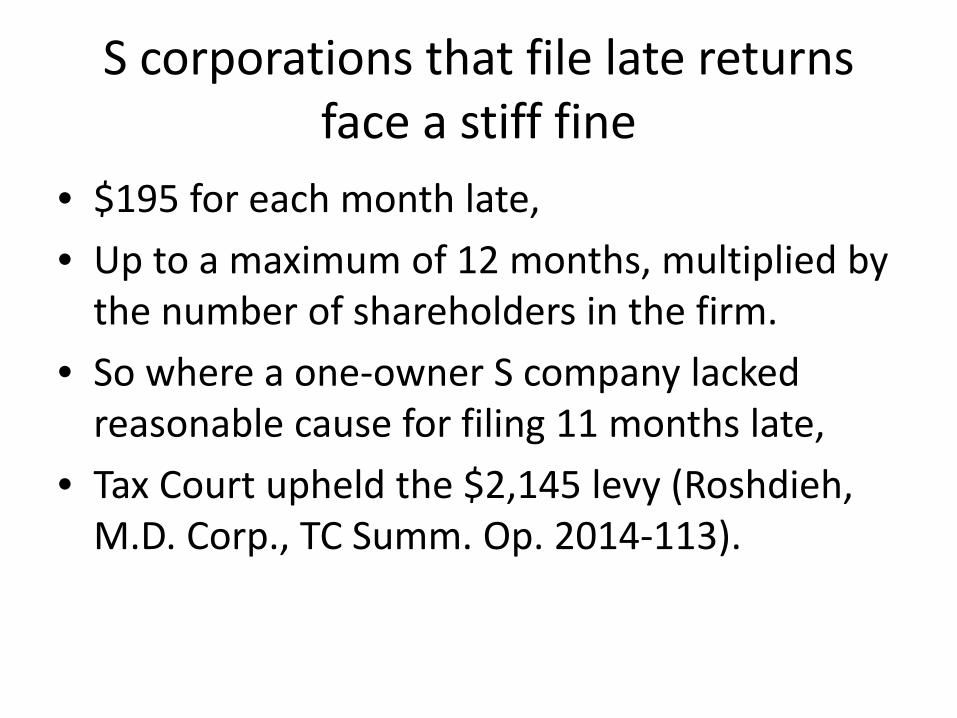

S corporations that file late returns face a stiff fine

• $195 for each month late,• Up to a maximum of 12 months, multiplied by

the number of shareholders in the firm.• So where a one-owner S company lacked

reasonable cause for filing 11 months late,• Tax Court upheld the $2,145 levy (Roshdieh,

M.D. Corp., TC Summ. Op. 2014-113).

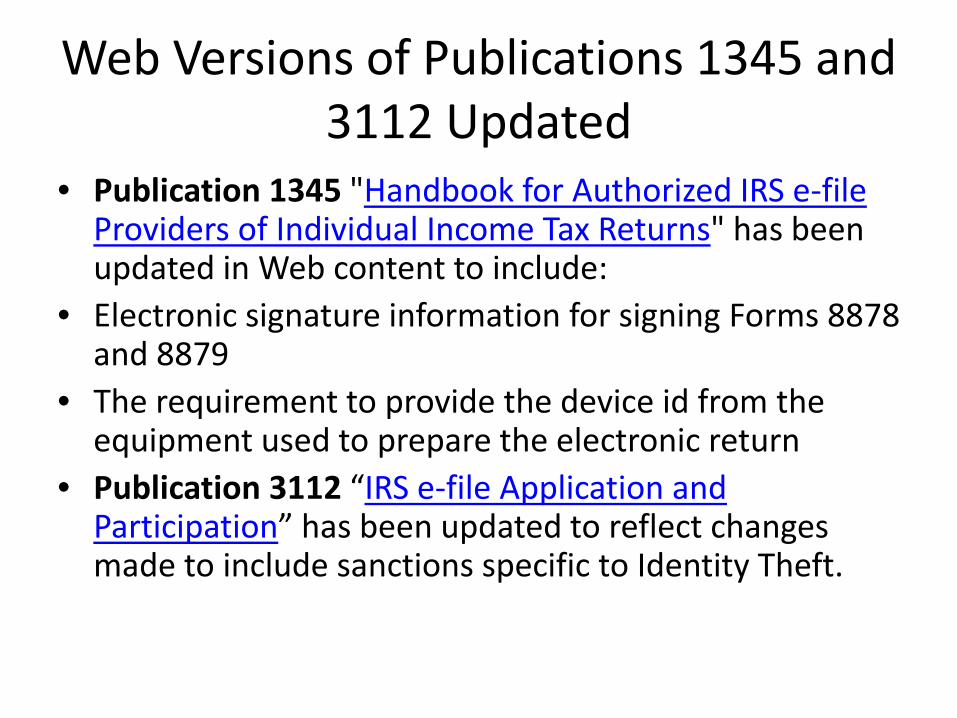

Web Versions of Publications 1345 and 3112 Updated

• Publication 1345 "Handbook for Authorized IRS e-file Providers of Individual Income Tax Returns" has been updated in Web content to include:

• Electronic signature information for signing Forms 8878 and 8879

• The requirement to provide the device id from the equipment used to prepare the electronic return

• Publication 3112 “IRS e-file Application and Participation” has been updated to reflect changes made to include sanctions specific to Identity Theft.

IRS doing a poor job of monitoring energy credits

• TIGTA report• Individuals are not using Form 5695 to claim

the credit.• They are erroneously using Form 8908, which

is for home builders and has much larger tax benefits.

• IRS says it will be more careful in the future.

Summary

• IRS is hurting.• It will not be better soon.• Learn how to research your own answers and

solutions.• I hope this program has not been too taxing

for you!

• Thank you for attending our program.• Stuart Sobel

Tax Media Network, Inc.www.taxmedianetwork.com