Investors guide to line lnco

20

An Investor's Guide to LINN Energy and LinnCo Photo credits: LINN Energy LLC

-

Upload

the-motley-fool -

Category

Business

-

view

12.831 -

download

3

Transcript of Investors guide to line lnco

An Investor's Guide to

LINN Energy and LinnCo

Photo credits: LINN Energy LLC

LINN Energy 101

• Founded in 2003 by Michael Linn.

• Went public in 2006 raising $261 million.

• LINN was the first of a new wave of exploration and production MLPs to go public.

• Company has grown from a handful of natural gas wells to a top-15 exploration and production company.

• Created LinnCo to serve as a growth vehicle.

LINN Energy vs. LinnCo

• LINN Energy took LinnCo public in 2012.

• LinnCo’s sole purpose is to own units of LINN Energy.

• Owns no operating assets.

• 1 LinnCo share = 1 vote of LINN Energy unit.

• LinnCo is a vehicle that LINN can use to acquire other public or private C-Corps (ex. Berry Petroleum).

LinnCo 101

LINN Energy vs. LinnCo

LINN Energy vs. LinnCo

• Benefits of LinnCo– No Schedule K-1– No UBTI implications– Corporate taxes at LinnCo estimated at zero through 2018– Better in an IRA than LINN Energy

• Drawbacks of LinnCo– No assets other than units of LINN Energy– Corporate taxes after 2018 will be a drag on dividend

growth

LinnCo 101

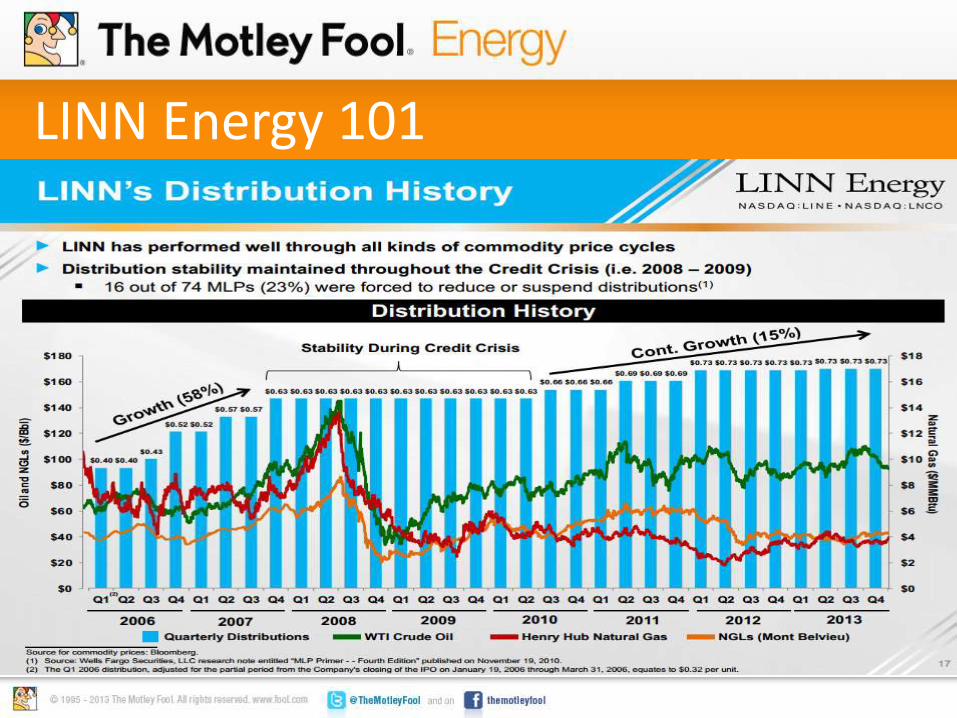

LINN Energy 101

LINN Energy 101

• Acquire mature oil and gas assets.

• Invest minimally to keep production roughly flat.

• Hedge virtually all of the production to lock in margins.

Core Business Model

LINN Energy 101

• Virtually all of LINN’s excess cash flow is distributed back to investors.

• Model yields as stable and growing income stream for investors.

Core Business Model

LINN Energy 101

LINN Energy 101

• LINN Energy and peers like BreitBurn Energy Partners and Vanguard Natural Resources are in a MLP like structure.

• Key to that structure is balanced and secure revenue stream.

• Yields predictable income stream.

Core Business Model vs. peers

LINN Energy Core Business vs. Peers

LINN Energy Core Business vs. Peers

LINN Energy Core Business vs. Peers

LINN Energy Core Business vs. Peers

• LINN Energy’s production is balanced while Breitburn is heavier into oil and Vanguard is gas heavy.

• LINN’s oil production isn’t 100% hedged as it’s still digesting the oil-rich Berry acquisition.

• LINN’s natural gas production is 100% hedged.

• Overall combination yields better income stability.

Key takeaways vs. peers

LINN Energy Upsides

• Last year LINN grew production by 11% (including acquisitions)

• In 2014 LINN is expected to grow production 3%-4%.

• Organic growth opportunities abound in LINN’s portfolio.

Organic growth

LINN Energy Upsides

• 55,000 net acres prospective for horizontal Wolfcamp

• 1,000+ well locations

• Currently exploring strategic optionsfor acreage.

Midland Basin

LINN Energy Upsides

Options:

1. Develop internally or JV.

2. Trade assets for long-life, mature properties.

3. Sell assets and eventually replace assets via a “like-kind-exchange.”

Midland Basin

LINN Energy Upsides

• $20-$30 billion in mature assets expected to hit the market.

• Shale focused drillers continue to shed mature production.

• Slow growth C-Corps (both public and private) could sell to LinnCo as an exit strategy.

Acquisitions

LINN Energy Key Takeaways

• Production now more oil/liquids focused.

• Ample upside from organic and acquired opportunities.

• Distribution stable and very likely to grow over the long-term.

Stable core with upside

Our special report "The

IRS Is Daring You To Make

This Energy Investment."