Investor Relations Presentation November, 2018. · investor relations presentation november, 2018....

53

, Investor Relations Presentation November, 2018.

Transcript of Investor Relations Presentation November, 2018. · investor relations presentation november, 2018....

,

Investor Relations PresentationNovember, 2018.

AGENDACOMPANY OVERVIEW1

MAIN BUSINESS DIVISIONS3

FINANCIALS4

APPENDIX: EARNINGS RELEASE 3Q185

CAR RENTAL

FLEET RENTAL

SEMINOVOS

1

2

3

2

COMPETITIVE ADVANTAGES2

3

1973

Founded in Belo Horizonte with 6

VW Beetles

1979

Expasion to 11 capital cities

becoming marketleader in 1981

1984

Expansionstrategy

by adjacencies: Franchising

1991

Expansion strategyby adjacencies:

Seminovos

1992

Internationalizationthrough Franchising

1997

PE firm DL&J enters ata market cap of

US$150 mm

1999

Expansion strategy byadjacencies: Fleet

Rental

2005

IPO with a Market Cap ofUS$295 mm

2014

Beginning ofDigital Transformation

2017

Strategic partnershipwith Hertz -

Phase I: Rise to #1 Phase II: ExpansionPhase III:

Reaching ScalePhase IV: Digital Transformation

COMPANY HISTORY:MILESTONES

2018

Market CapUS$3.8 Billion (09/30/18)

2006

50,000 cars

2011

100,000 cars

150,000 cars

+222,000 cars

1982

1.000 cars

INTEGRATED BUSINESS PLATFORM

THIS INTEGRATED PLATFORM GIVES LOCALIZA

FLEXIBILITY AND SUPERIOR PERFORMANCE

4

• 156,436 CARS• 8.3 MILLION CLIENTS• 395 LOCATIONS• 4,788 EMPLOYEES

CAR RENTAL FLEET RENTAL

•51,236 CARS• +1,000 CLIENTS• 304 EMPLOYEES

USED CAR SALES

• 48% SOLD TO FINAL CONSUMER• 101 STORES• 67 CITIES• 1,317 EMPLOYEES

FRANCHISING• 14,505 CARS• 127 LOCATIONS IN BRASIL • 61 LOCATIONS IN SOUTH AMERICA• 33 EMPLOYEES

SYNERGIES:BARGAINING POWER

COST REDUCTIONCROSS SELLING

OVERHEAD AND SUPPORT: 1,335 EMPLOYEES

3Q18

COMPANY:BUSINESS PLATFORM DIVISIONS

CAR RENTAL FRANCHISING FLEET RENTAL USED CAR SALES

5

• HIGH FIXED COST STRUCTURE

• STANDARDIZED FLEET

• 1 YEAR CYCLE

• HIGHER ENTRY BARRIERS

• GAINS OF SCALE

• CAPITAL INTENSIVE

• CONCENTRATED AIRPORT MARKET

• FRAGMENTED OFF AIRPORT MARKET

RENTS TO INDIVIDUALS AND COMPANIES AT AIRPORTS AND OFF AIRPORT LOCATIONS.

CONTRIBUTES TO EXPAND LOCALIZA’S NETWORK.

• HIGH PROFITABILITY

• LOW CONTRIBUTION TO EARNINGS

• RESPONSIBLE TO DEVELOP NEW

MARKETS

• LOW FIXED COST STRUCTURE

• CUSTOMIZED FLEET

• 2-3 YEARS CYCLE

• LOWER ENTRY BARRIERS

• CAPITAL INTENSIVE

OUTSOURCES FLEET FOR 2-3 YEARS’ TERM CONTRACTS.

SELLS THE USED CARS MAINLY TO FINAL CONSUMERS AFTER THE RENTAL AND ESTIMATES THE RESIDUAL VALUES.

• EFFICIENCY AREA RESPONSIBLE TO SELL

CARS FROM RAC AND FLEET DIVISIONS

• KNOW HOW OF USED CARS MARKET

• LOW DEPENDENCE OF INTERMEDIATES

• ALLOWING FOR LOWER DEPRECIATION

6

BIG NUMBERS

✓Market leader with market cap of R$ 15.2 billion on September 30, 2018

✓ End of period fleet of 222,177 cars in 9M18

✓ R$5.6 billion of net revenues in 9M18

✓ Rented fleet growth of 44.8% in the Car Rental and 21.3% in the Fleet Rental Division in 9M18

✓ ROIC of 12.8%, spread of 7.8 p.p compared with the cost of debt after taxes

Net RevenuesR$5,636

EBITDA

R$1,142

EBIT*

R$907

Consolidated breakdown – 9M18R$ million

7

*Seminovos results recorded in the Car Rental and Fleet Rental Divisions

COMPANY’S PROFITABILITY COMES FROM CAR RENTAL AND FLEET RENTAL DIVISIONS

11910%

40135%

62255% 312

34%

59566%

3,205 57%

624 11%

1,806 32%

AGENDACOMPANY OVERVIEW1

MAIN BUSINESS DIVISIONS3

FINANCIALS4

APPENDIX: EARNINGS RELEASE 3Q185

CAR RENTAL

FLEET RENTAL

SEMINOVOS

1

2

3

8

COMPETITIVE ADVANTAGES2

COMPETITIVE ADVANTAGES

PROFITABILITY COMES FROM RENTAL DIVISIONS

CASH TO RENEW THE FLEET OR PAY DEBT

RAISING MONEY

BUYINGCARS

ALUGUELDE CARS

SELLINGCARS

9

RENTINGCARS

45 YEARS OF EXPERIENCE IN MANAGING ASSETS AND GENERATING VALUE.

COMPETITIVE ADVANTAGES

RAISING MONEYINVESTMENT GRADE: LOWER SPREADS AND LONGER TENORS

Source: Bloomberg October, 2018.

BB FitchBa2 Moody’s

BB+ S&PB+ S&P BB S&P

B1 Moody´sB+ S&P

Player A Player B/C Player D

brAAA S&P Aa1.br Moody’sAAA(bra) Fitch

A+(bra) FitchAA (bra) Fitch

brAA+ S&PA+(bra) FitchNational scale

Global scale

10

RAISING MONEY

BUYINGCARS

SELLINGCARS

RENTINGCARS

LOCALIZA RAISES MONEY WITH BETTER CONDITIONS THEN ITS COMPETITORS.

COMPETITIVE ADVANTAGES

11

RAISING MONEY

2018 Bonds - R$ million

% CDI

Years

RAISING MONEY

BUYINGCARS

SELLINGCARS

RENTINGCARS

Player C R$411 114.7%Player C R$88

113.2%

Player C R$350119.0%

Player A R$138118.4%

Player A R$182 123.1%

Player A R$130 119.9%

Player A R$250 121.0%

Player B R$500 117.5%

Localiza R$300108.0%

Localiza Fleet R$300112.0%

Player D R$99123.0%

Localiza R$200 107.9%

Localiza R$800,0112.3%

Player B R$150,0 110.6%Player C R$113.0%

90%

95%

100%

105%

110%

115%

120%

125%

130%

135%

140%

1.5 2.5 3.5 4.5 5.5 6.5 7.5 8.5 9.5

Number of cars purchased – 9M18 Localiza’s share in the internal sales of the OEMs* - 9M18

Source: website of each company and ANFAVEA. 12

COMPETITIVE ADVANTAGESBUYING CARS

111,383

41,318 49,738

Localiza* Player A Player B+C*

*it includes Franchisees

7.1%

LOCALIZA BUYS CARS WITH BETTER CONDITIONS DUE TO THE VOLUME OF PURCHASES.

RAISING MONEY

BUYINGCARS

SELLINGCARS

RENTINGCARS

*it considers the 12 OEMs listed above

Most recognized and desired brand in the category

13

• Co-branding with Hertz, the most well-known brand, with presence in +150 countries

• 24th most valuable brand in Brazil in 2017 (Interbrand ranking) • Brand with the largest awareness and preference in the sector• Presence online and offline

• Winner of Época ReclameAqui award for the 3rd consecutive year • Customer superior satisfaction (NPS) • Culture of delighting• Modern and diversified fleet

Leader in loyalty and superior quality

COMPETITIVE ADVANTAGESRENTING CARS

BRAZILIAN DISTRIBUTION

# OF LOCATIONS # OF CITIES

522

218

186

404

Localiza Competitors

360

145 96

Localiza Player B Player A

RAISING MONEY

BUYINGCARS

SELLINGCARS

RENTINGCARS

Source: Locations and cities: Localiza 3Q18 results and each company’s website as of As of 10/24/18 for its competitors

COMPETITIVE ADVANTAGENS

14

RAINSINGMONEY

BUYING CARS SELLING CARSFLEET RENTAL

New ways of developing technologies with agility and customer collaboration

Innovations that generate strategic information for the customer´s business and

added value for the business

Good interaction with customers, facilitating the resolution of problems

FLEET RENTAL

15

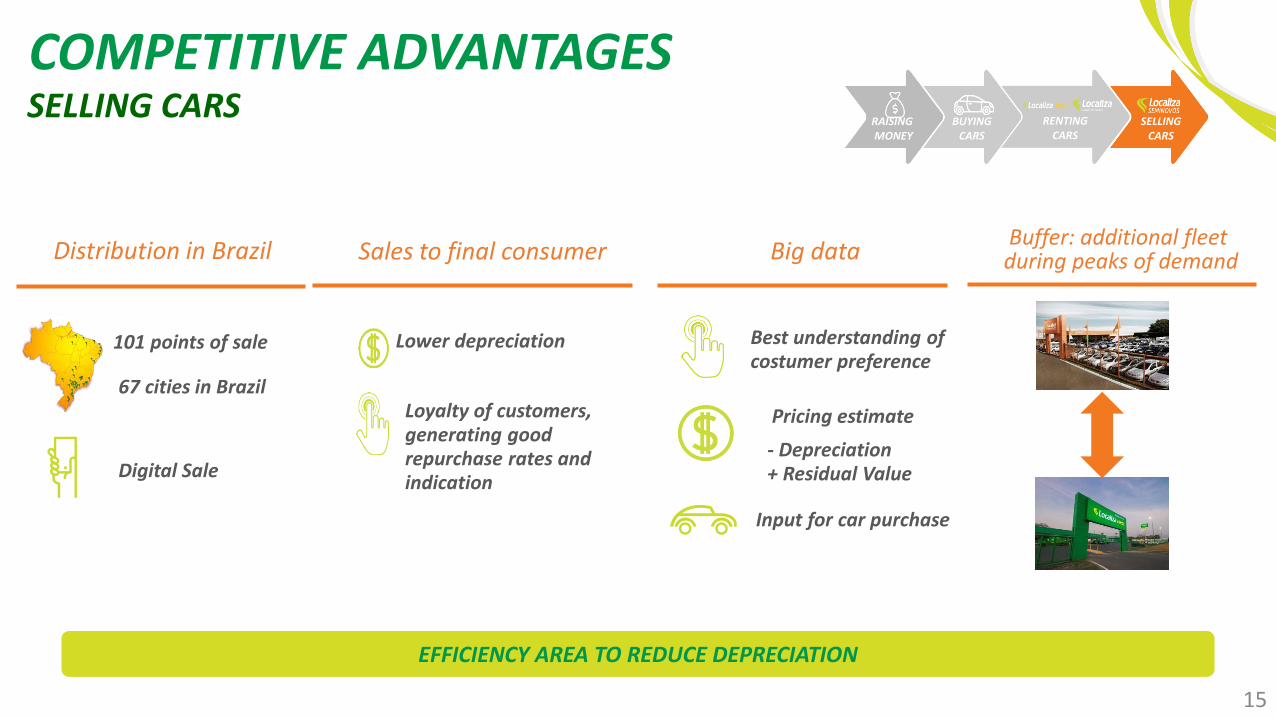

Distribution in Brazil

Digital Sale

101 points of sale

67 cities in Brazil

COMPETITIVE ADVANTAGESSELLING CARS

Big data

Best understanding of costumer preference

Pricing estimate

- Depreciation+ Residual Value

Input for car purchase

Buffer: additional fleet during peaks of demandSales to final consumer

Lower depreciation

Loyalty of customers, generating good repurchase rates and indication

EFFICIENCY AREA TO REDUCE DEPRECIATION

RAISING MONEY

BUYINGCARS

SELLINGCARS

RENTINGCARS

16

COMPETITIVE ADVANTAGESWITH OPERATIONAL EXCELLENCE

CAR PREPARATION

• Quality control of the cars delivered by OEM’S

• Car licensing

DELIVERY IN THE BRANCHES

• Transport tracking• Logistic management

optimization

OPERATING CAR

• Maintanance and repair• Traffic fines processing• Licensing renewal

CAR DECOMISSIONING

• Car checking • Preparation for sales• Transportation to

Seminovos stores

RAISING MONEY

BUYINGCARS

SELLINGCARS

RENTINGCARS

17

Anti fraudLocaliza FastChatbot® Digital register and self check-in

Taylor-made solution for fraud prevention in car

rentals

Mobile-based counterbypass. Customers can pick-up car bypassing our counter

Facebook / messengerbooking assistant

Automatic capture of the driver’s license for new costumers and

expedite check-in.

Connected Fleet Mobile SolutionIntegrated mobile solution to

fleet rental services for drivers and contract manager.

Online Fleet RentalFast diagnosis and

friendly dashboard for fleet manager.

Integrated technology solution that increases competitive intelligence and

leverages productivity gains.

RAISING MONEY

BUYINGCARS

SELLINGCARS

RENTINGCARS

... AND INNOVATION

DIFFERENTIATED OFFER WITH HIGHER VALUE ADDED TO CUSTOMERS

R$38.2

Average car price

(2 years)

Car sale revenue

net of SG&A

R$36.01 year cycle

1 2 3 4 5 6 7 8 9 10 11 12Expenses, interest and tax

Revenue

CAR RENTAL: FINANCIAL CYCLE 2017Per car

18

Total

1 year

R$ % R$ % R$

Net revenues 19.6 100.0% 38.8 100.0% 58.4

Costs - fixed and variable (9.2) -47.1% (9.2)

SG&A (3.5) -18.0% (2.9) -7.4% (6.4)

Net revenues of car sold 36.0 92.6% 36.0

Book value of car sold (33.9) -87.2% (33.9)

EBITDA 6.9 34.9% 2.1 5.4% 9.0

Cars Depreciation (1.2) -3.2% (1.2)

Others depreciation (0.3) -1.3% (0.1) -0.3% (0.4)

Financial expenses (2.4) -6.3% (2.4)

Taxes (1.5) -7.6% 0.4 1.0% (1.1)

Net Income (Loss) 5.1 26.0% (1.3) -3.4% 3.8

NOPAT 5.7

ROIC (it consideres only cars in capital invested) 14.9%

Cost of debt after taxes 7.6%

Car Rental Seminovos

Per car soldPer operating car

1 2 3 4 5 6 31 32 33 34 35 36Expenses, interest and tax

Revenue

Car sale revenue

net of SG&A

R$31.8

R$43.1

Average car price

(3 years)

3 year cycle

FLEET RENTAL: FINANCIAL CYCLE 2017Per car

19

Total

3 years

R$ % Seminovos % R$

Net revenues 60.5 100.0% 34.1 100.0% 94.6

Costs - fixed and variable (17.9) -29.7% (17.9)

SG&A (5.1) -8.4% (2.4) -7.0% (7.5)

Net revenues of car sold 31.7 93.0% 31.7

Book value of car sold (28.7) -84.1% (28.7)

EBITDA 37.5 61.9% 3.0 8.9% 40.5

Cars Depreciation (9.3) -27.3% (9.3)

Others depreciation (0.3) -0.5% (0.1) -0.4% (0.4)

Financial expenses (6.5) -19.1% (6.5)

Taxes (8.4) -13.9% 2.9 8.6% (5.5)

Net Income (Loss) 28.8 47.6% (10.0) -29.4% 18.8

Net Income (Loss) - per year 9.6 47.6% (3.3) -29.4% 6.3

NOPAT 7.9

ROIC (it consideres only cars in capital invested) 18.4%

Cost of debt after taxes 7.6%

Per operating car

Fleet Rental Seminovos

Per car sold

ROIC versus COST OF DEBT AFTER TAXES

ROIC considered each year´s effective income tax and social contribution rate

(*)Adjusted by the one-time costs incurred - Hertz Brasil acquisition and Franchisees incorporation

2013 2014 2015 2016 2017 9M18

ROE 29.0% 30.6% 24.3% 21.1% 25.6% 24.5%

20

16.7%17.8%

17.0%15.4% 15.6%

12.8%

6.0%

8.0%9.5% 10.2%

7.6%

5.0%

2013 2014 2015 2016 2017 9M18

ROIC Cost of debt after taxes

9.8p.p.10.7p.p.7.5p.p. 5.2p.p.

8.0p.p.

*

7,8p.p.

STABLE SPREAD WITH STRONG PACE OF GROWTH

AGENDACOMPANY OVERVIEW1

MAIN BUSINESS DIVISIONS3

FINANCIALS4

APPENDIX: EARNINGS RELEASE 3Q185

CAR RENTAL

FLEET RENTAL

SEMINOVOS

1

2

3

21

COMPETITIVE ADVANTAGES2

22

MARKET SIZE 2016:R$5.8 BILLION

OTHERS

MARKET SIZE 2017:R$6.5 BILLION

CAR RENTAL: MARKET SHAREGROSS REVENUE - CAR RENTAL

Source: ABLA, considering the breakdown reported applied on the revenues

OTHERS

29.3%*

11.8%

6.7%

52.2%

32.3%*

13.9%7.8%

46.0%

PLAYER B

PLAYER A

PLAYER B

PLAYER A

*Localiza’s market share includes revenues from franchisees in Brazil. There are no public data on the revenue of other players’ franchisees.

CAR RENTAL LOCATIONS IN BRAZIL

AIRPORT LOCATIONS OFF – AIRPORT LOCATIONS

Localiza423

Player B157

Player E26

Player A101

Others7,852

23Source: ABLA, each company’s website on 10/24/2018 and Localiza’s 3Q18 Earnings Release..

1/3 OF CAR RENTAL’S REVENUES COMES

FROM AIRPORT LOCATIONS

OFF -AIRPORT LOCATIONS

AIRPORT LOCATIONS

OFF – AIRPORT MARKET IS STILL FRAGMENTED

Localiza99

Player A51

Player B49

Player E33

Others38

Localiza Player A Player B Player E Others

180200 240

260300 350 380

415465

510545

622678

724788

880937

38% 37% 35%31%

27% 22% 20%

18% 16% 15% 15% 13% 13% 12% 11% 9% 8%

-50

50

150

250

350

450

550

650

750

850

950

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Monthly minimum salary (R$) Daily rental price over minimum salary (%)

CAR RENTAL AFFORDABILITY

Source: BCB and Localiza rates

Sources: IPEADATA, Localiza’s loyalty program and BCB as of 2016

*Considering that each credit card owner owns 1,3 credit cards, BCB estimated that were 84 million active credit cards in Brazil in 2016.

CAR RENTAL: DRIVERS

24INCREASING AFFORDABILITY AND LOW PENETRATION BRINGS GROWTH OPPORTUNITIES.

3.1 3.8

4.3

5.7 6.4

7.6 8.3

2012 2013 2014 2015 2016 2017 9M18

LOCALIZA RAC USERS (MILLION)*84.0

64.0

8.3

Adult population (age>20years) Class A+B+C

Credit Card owners Users

In million

*considering only the individual segment.

CAR RENTAL: DRIVERS

25

*

40.645.7

49.756.9

70.3

81.587.0 88.2 93.3 94.4 89.0 90.8

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

AIRLINE MARKET EVOLUTION

RPK (REVENUE SEAT KILOMETER) IN MILLION

* Annualized with the available data until November/17

Source: ANAC

DEMAND FORECASTING

PASSANGERS ESTIMATE (IN MILLION)

Source: Ministério dos Transportes / Transportation Ministry (September/2017)

EVOLUTION IN AIRLINE MARKET BRINGS GROWTH OPPORTUNITIES .

201.3

267.8

401

2017 2027 2037

AGENDACOMPANY OVERVIEW1

MAIN BUSINESS DIVISIONS3

FINANCIALS4

APPENDIX: EARNINGS RELEASE 3Q185

CAR RENTAL

FLEET RENTAL

SEMINOVOS

1

2

3

26

COMPETITIVE ADVANTAGES2

FLEET RENTAL: MARKET SHAREGROSS REVENUE - FLEET RENTAL

27Source: ABLA, considering the breakdown reported applied on the revenues

MARKET SIZE 2017:R$9 BILLION

MARKET SIZE 2016:R$8 BILLION

8.4%2.6%

3.6%

7.6%77.9%OTHERS

PLAYER B

PLAYER C

PLAYER A 8.3%

2.6%4.4%

5.5%79.1%OTHERS

PLAYER B

PLAYER C

PLAYER A

FLEET RENTAL: DRIVERS

28

Corporate fleet:5,000,000*

Rented fleet:440,737**

41,266

BRAZILIAN MARKET

*Frost&Sullivan research **Localiza estimates

WORLD

8.8% 8.9%13.3%

16.5%

24.5%

37.4%

46.9%

58.3%

Source: Datamonitor for European countries and Localiza’s estimate for Brazil

LOW PENETRATION OF RENTED FLEET IN BRAZIL

AGENDACOMPANY OVERVIEW1

MAIN BUSINESS DIVISIONS3

FINANCIALS4

APPENDIX: EARNINGS RELEASE 3Q185

CAR RENTAL

FLEET RENTAL

SEMINOVOS

1

2

3

29

COMPETITIVE ADVANTAGES2

SEMINOVOS: NEW vs USED CAR MARKET (BRAZIL)

Source: Fenabrave (light and commercial cars) October 31,2018. 30

New cars

Used cars

TOTAL MARKET OF 13.1 MILLION CARS.

8.48.9 9.0

9.410.1 9.9 10.0

10.7 10.7

3.3 3.5 3.6 3.6 3.32.5

2.0 2.2 2.4

2010 2011 2012 2013 2014 2015 2016 2017 untilOctober

2018Carros usados Carros novos

*

*

(*)Annualized

2.5x 2.5x2.6x 2.6x 3.1x 4.0x 5.0x 4.9x 4.5x

SEMINOVOS: DRIVERS

# OF INHABITANTS PER CARAFFORDABILITY TO BUY CARS – AVERAGE PUBLIC PRICE

OF ECONOMIC CARS

AFFORDABILITY AND PENETRATION

Source: Anfavea, Bradesco. Source: BCB and Localiza

Reference: for calculation was considered the cheapest car in our fleet

31

300 350 380 415

465 510 545 622

678 724

788 880

934 954 84

71 6961

5551 49

43 43 43 41 4147 47

-

10

20

30

40

50

60

70

80

90

-100

100

300

500

700

900

1,100

20052006200720082009201020112012201320142015201620172018

Minimum wage (R$) Minimum wages needed to buy a new car

4.8

3.5

3.3

2.5

1.9

1.9

1.8

1.7

1.7

1.7

1.7

1.7

1.6

1.6

1.5

1.4

1.2

Brasil

Mexico

Argentina

South Korea

Czech Republic

Sweden

Belgium

Germany

Austria

UK

France

Spain

Japan

Canada

Italy

Australia

USA

30.5%

Up to 2 years - 2017296,756

SEMINOVOS: CARS SALESOPERATING DATA

0.8%

Used cars – 201710,730,763

4.2%

Main players

Examples • Retailers • Dealers • Rental Operators

Points of sale • 48,000 (Fenauto) • 5,535 (Anfavea) • +137 (Unidas, Movida, Locamerica)

Source: Anfavea 2018 e Fenabrave / Unidas, Locamerica e Movida 1Q18.

32

Brand new- 20172,172,235

AGENDACOMPANY OVERVIEW1

MAIN BUSINESS DIVISIONS3

FINANCIALS4

APPENDIX: EARNINGS RELEASE 3Q185

CAR RENTAL

FLEET RENTAL

SEMINOVOS

1

2

3

33

COMPETITIVE ADVANTAGES2

34

# of cars sold

Average rented fleet – Car Rental

End of period fleet

Average rented fleet – Fleet Rental

3Q18 OPERATING HIGHLIGHTS

127,221 156,436

44,655

51,236 13,514

14,505 185,390 222,177

3Q17 3Q18

Car rental Fleet rental Franchising

23,941 30,084

3Q17 3Q18

72,200

98,199

3Q17 3Q18

36,009 43,421

3Q17 3Q18

35

Net revenues (R$ million)

Net income (R$ million)EBIT (R$ million)

EBITDA (R$ million)

3Q18 FINANCIAL HIGHLIGHTS

332.3 396.2

3Q17 adjusted 3Q18

139.5 159.9

3Q17 adjusted 3Q18

263.9 300.5

3Q17 adjusted 3Q18

+38,0%4T/4T

+38,6%4T/4T665.0 859.0

898.4 1,214.2

1,563.4 2,073.2

3Q17 3Q18

Rental Seminovos

21.5

21.5

16.3

One-time costs incurred - Hertz Brasil acquisition and Franchisees incorporation

CAR RENTAL

1,163.5 1,284.4 1,258.0 1,428.0

1,848.5

1,273.6

1,793.7

472.6 637.4

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

Average rented fleet

STRONG GROWTH OF RENTED FLEET AND REVENUE

39,475 42,999 43,315 51,515 69,762 64,536

93,424 72,200

98,199

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

Net revenues (R$ million)

36

37

CAR RENTAL

Average rental rate (in R$) Utilization rate (%)

POSITIVE TREND OF THE AVERAGE RENTAL RATE

79.374.1 74.1 74.0 74.7

69.572.5

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

75.8%

79.0%81.0%

78.5% 78.7%77.0%

81.1%

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

CAR RENTAL NETWORK EVOLUTION

Number of car rental locations Brazil and abroad

286 304 320 333 384 395

193 172 174 158133 127

63 64 70 70 71 61542 540 564 561 588 583

2013 2014 2015 2016 2017 3Q18

Localiza's branches - Brazil Franchisees' branches - Brazil Franchisees' branches - abroad

+11

11 NEW OWNED BRANCHES

38

FLEET RENTAL Average rented fleet

MAINTENANCE OF THE GROWTH RATE

575.9 571.9 608.5 651.8 742.1

538.2 624.3

188.5 217.4

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

Net revenues (R$ million)

30,121 28,787 30,280 31,22235,424 34,013

41,26636,009

43,421

-

5,00 0

10,0 00

15,0 00

20,0 00

25,0 00

30,0 00

35,0 00

40,0 00

45,0 00

50,0 00

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

39

NET INVESTMENT Car purchase and sales (quantity)

GROWTH OF THE FLEET TO SUPPORT STRONG DEMAND FOR RENTALS 40

Net investment in fleet (R$ million)

Cars purchased Cars sold Hertz Brasil

Purchases (includes accessories) Used car sales net revenues Hertz Brasil

69,744 79,804 64,032

87,833

143,414

108,271 107,852

57,213 44,464 62,641 70,621

64,305 68,44990,554

64,45178,998

23,94130,084

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

7,103 9,183(273)

19,384

88,619

1,935

135,252

8,162

43,820

52,860

33,272

2,026.22,483.2

2,278.4

3,289.6

5,754.4

4,316.64,536.9

2,208.9 1,959.81,747.3 2,018.2 2,044.92,342.6

3,451.22,424.7

3,205.4

898.4 1,214.2

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

465.0278.9 233.5

947.0

61.95,467.9

286.5

3,389.3

1,891.9

2,303.2

1,310.5

* It does not consider theft / crashed cars written off.

28,854

14,380

1,331.5

745.6

267

8,162

267

8,162

64,18423,67449,051

100,109

9,0

286.5

4,030.1

2,415.79.0

286.5

1,922.4889.4

41

NUMBER OF POINTS OF SALE

7475 77

84

9993

10193

101

62,641 70,621

64,305 68,449

90,554

64,451 78,998

23,941 30,084

-

20,0 00

40,0 00

60,0 00

80,0 00

100 ,000

120 ,000

140 ,000

160 ,000

0

20

40

60

80

100

120

140

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

Points of sale Cars sold

NEW POINTS OF SALE WILL BE OPENED TO SUPPORT FUTURE NEEDS OF FLEET RENEWAL

42

END OF PERIOD FLEET

CURRENT FLEET: MORE THAN 220,000 CARS

(Quantity)

70,717 77,573 76,755 94,156 135,578 127,221

156,436 32,809 34,312 33,948 34,960

44,877 44,655

51,236

14,233 13,339 13,992 14,015

13,824 13,514

14,505

117,759 125,224 124,695143,131

194,279 185,390222,177

2013 2014 2015 2016 2017 9M17 9M18

Car Rental Fleet Rental Franchising

43

CONSOLIDATED NET REVENUES(R$ million)

32.6% INCREASE IN CONSOLIDATED NET REVENUE

1,758.9 1,874.0 1,883.1 2,096.8 2,607.1 1,824.1 2,430.7

665.0 859.0

1,747.3 2,018.2 2,044.9 2,342.5

3,451.2

2,424.7

3,205.4

898.4 1,214.2

3,506.2 3,892.2 3,928.0

4,439.3

6,058.3

4,248.8

5,636.1

1,563.4 2,073.2

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

Rental Used car sales

44

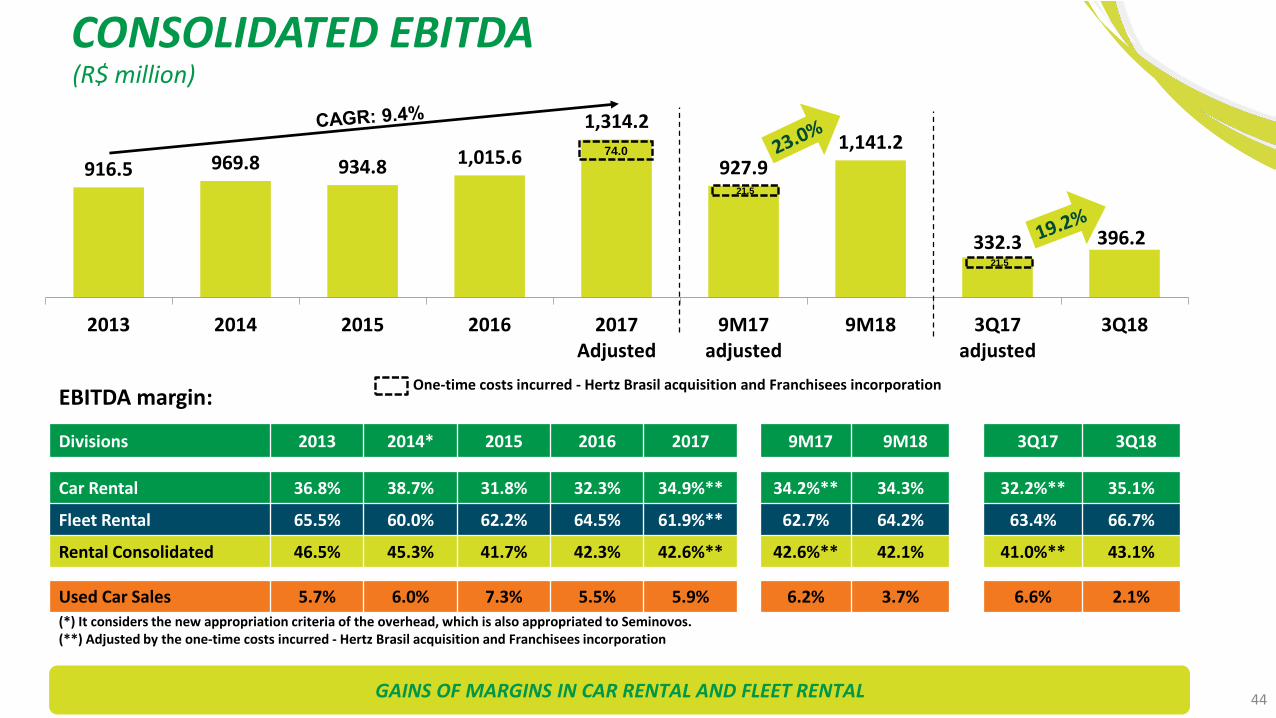

CONSOLIDATED EBITDA(R$ million)

(*) It considers the new appropriation criteria of the overhead, which is also appropriated to Seminovos.(**) Adjusted by the one-time costs incurred - Hertz Brasil acquisition and Franchisees incorporation

Divisions 2013 2014* 2015 2016 2017 9M17 9M18 3Q17 3Q18

Car Rental 36.8% 38.7% 31.8% 32.3% 34.9%** 34.2%** 34.3% 32.2%** 35.1%

Fleet Rental 65.5% 60.0% 62.2% 64.5% 61.9%** 62.7% 64.2% 63.4% 66.7%

Rental Consolidated 46.5% 45.3% 41.7% 42.3% 42.6%** 42.6%** 42.1% 41.0%** 43.1%

Used Car Sales 5.7% 6.0% 7.3% 5.5% 5.9% 6.2% 3.7% 6.6% 2.1%

EBITDA margin:

916.5 969.8 934.8 1,015.6

1,314.2

927.91,141.2

332.3 396.2

2013 2014 2015 2016 2017Adjusted

9M17adjusted

9M18 3Q17adjusted

3Q18

One-time costs incurred - Hertz Brasil acquisition and Franchisees incorporation

74.0

GAINS OF MARGINS IN CAR RENTAL AND FLEET RENTAL

21.5

21.5

45

AVERAGE ANNUALIZED DEPRECIATION PER CAR(In R$)

Fleet Rental

Car Rental

INCREASE IN DEPRECIATION IN THE QUARTER AS A RESULT OF LOWER INFLATION ON NEW CAR PRICES

1,452.4 1,270.0

622.1

1,251.2 1,250.1 1,351.4946.5

1,222.6 1,305.2

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

4,592.3 4,202.1 3,935.2 3,714.03,104.3 3,105.1

3,475.63,012.6

3,747.4

2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

46

CONSOLIDATED EBIT(R$ million)

652.1 726.7 735.5 771.1

1,043.1

729.4907.3

263.9 300.5

2013 2014 2015 2016 2017 Adjusted 9M17 adjusted 9M18 3Q17 adjusted 3Q18

Divisions 2013 2014 2015 2016 2017 9M17 9M18 3Q17 3Q18

Car Rental 32.8% 36.2% 34.3% 30.2% 35.5%* 34.8%* 32.9% 34.4%* 29.8%

Fleet Rental 45.1% 44.3% 48.9% 51.2% 51.4%* 52.7% 50.0% 53.1% 50.4%

Consolidated 37.1% 38.8% 39.1% 36.8% 40.0%* 40.0%* 37.3% 39.7%* 35.0%

74.0

One-time costs incurred - Hertz Brasil acquisition and Franchisees incorporation

(*) Adjusted by the one-time costs incurred - Hertz Brasil acquisition and Franchisees incorporation

13.9% INCREASE IN EBIT

21.5

21.5

47

CONSOLIDATED NET INCOME(R$ million)

384.3 410.6 402.4 409.3

563.4

389.0477.8

139.5 159.9

2013 2014 2015 2016 2017 Adjusted 9M17 adjusted 9M18 3Q17 adjusted 3Q18

Reconciliation EBITDA x Net income 2013 2014 2015 2016 2017* Var. R$ Var. % 9M17* 9M18 Var. R$ Var. % 3Q17* 3Q18 Var. R$ Var. %

Consolidated EBITDA 916.5 969.8 934.8 1,015.6 1,314.2 298.6 29.4% 927.9 1,141.2 213.3 23.0% 332.3 396.2 63.9 19.2%

Cars depreciation (229.0) (207.4) (163.6) (206.3) (232.0) (25.7) 12.5% (170.2) (201.3) (31.1) 18.3% (58.2) (84.5) (26.3) 45.2%

Other property depreciation and amortization (35.4) (35.7) (35.7) (38.2) (39.1) (0.9) 2.4% (28.3) (32.6) (4.3) 15.2% (10.2) (11.2) (1.0) 9.8%

EBIT 652.1 726.7 735.5 771.1 1,043.1 272.0 35.3% 729.4 907.3 177.9 24.4% 263.9 300.5 36.6 13.9%

Financial expenses, net (110.6) (151.1) (202.7) (243.5) (315.0) (71.5) 29.4% (221.3) (261.4) (40.1) 18.1% (79.4) (83.8) (4.4) 5.5%

Income tax and social contribution (157.2) (165.0) (130.4) (118.3) (164.7) (46.4) 39.2% (119.1) (168.1) (49.0) 41.1% (45.0) (56.8) (11.8) 26.2%

Net income of the period 384.3 410.6 402.4 409.3 563.4 154.1 37.6% 389.0 477.8 88.8 22.8% 139.5 159.9 20.4 14.6%

57.7

One-time costs incurred - Hertz Brasil acquisition and Franchisees incorporation, after taxes

(*)Adjusted by the one-time costs incurred - Hertz Brasil acquisition and Franchisees incorporation

14.6% INCREASE IN NET INCOME

16.3

16.3

FREE CASH FLOW

48

In the free cash flow, short-term financial assets were considered as cash equivalents since they have immediately liquidity(*) Adjusted by one-time costs incurred -Hertz Brasil acquisition and franchisees incorporation(**) Discount of credit card receivables and anticipation of accounts payable were demonstrated in a different line so that the Free Cash Flow From Operations, Before Growth considered only the contractual terms, reflectingthe Company's operation

Free cash flow - R$ million 2013 2014 2015 2016 2017 9M18

EBITDA 916.5 969.8 934.8 1,015.60 1314.2 1,141.2

Used car sale revenue, net from taxes (1,747.3) (2,018.2) (2,044.9) (2,342.5) (3,451.2) (3,205.4)

Depreciated cost of cars sold 1,543.8 1,777.0 1,769.1 2,102.5 3,106.6 2,961.2

(-) Income tax and social contribution (108.5) (113.1) (110.7) (93.3) (108.3) (99.7)

Change in working capital 2.9 (27.1) (30.0) (40.8) (47.9) (111.1)

Cash generated by rental operations 607.4 588.4 518.3 641.5 813.4 686.2

Used car sale revenue, net from taxes – fleet renewal 1,747.3 2,018.2 2,036.3 2,342.5 3,451.2 3,205.4

Fleet renewal investment (1,819.7) (2,197.7) (2,278.4) (2,563.6) (3,660.9) (3,323.1)

Change in accounts payable to car suppliers for fleet renewal 144.3 120.0 (25.4) 219.9 227.6 287.7

Net investment for fleet renewal 71.9 (59.5) (267.5) (1.2) 17.9 170.0

Fleet renewal – quantity 62,641 70,621 64,032 68,449 90,554 78,998

(47.5) (46.3) (29.7) (42.2) (48.8) (29.4)

631.8 482.6 221.1 598.1 782.5 826.8

Fleet (growth) investment / Used car sale revenue, net from taxes – fleet reduction (209.4) (286.8) 8.6 (726.0) (1,807.0) (1,213.8)

Change in accounts payable to car suppliers for fleet growth (54.6) 214.4 (23.9) 26.8 168.7 173.7

Hertz Brazil acquisition - fleet - - - - (286.5) -

Fleet growth capex (264.0) (72.4) (15.3) (699.2) (1,924.8) (1,040.1)

Fleet increase / (reduction) – quantity 7,103 9,183 (273) 19,384 52,860 28,854

367.8 410.2 205.8 (101.1) (1,142.3) (213.3)

Hertz Acquisition (Except fleet) / Incurred one-time costs effect - - - - (120.7) -

New headquarters construction and furniture (6.5) (148.3) (30.7) (84.4) (126.2) -

361.3 261.9 175.1 (185.5) (1,389.2) (213.3)

- - (71.9) 98.0 88.3 (288.0)

361.3 261.9 103.2 (87.5) (1,300.9) (501.3)

Ope

rati

ons

Cape

x -

rene

wal

Investment, property and intangible

Free cash flow from operations, before growth

Cape

x -

Gro

wth

Cape

x -

non-

recu

rrin

g

Free cash generated before the cash effects of discounts and anticipation of payables to suppliers

Free cash flow after growth

Cash effects of discount of credit card receivables and anticipation of payables to suppliers (**)

Free cash flow before interest

*

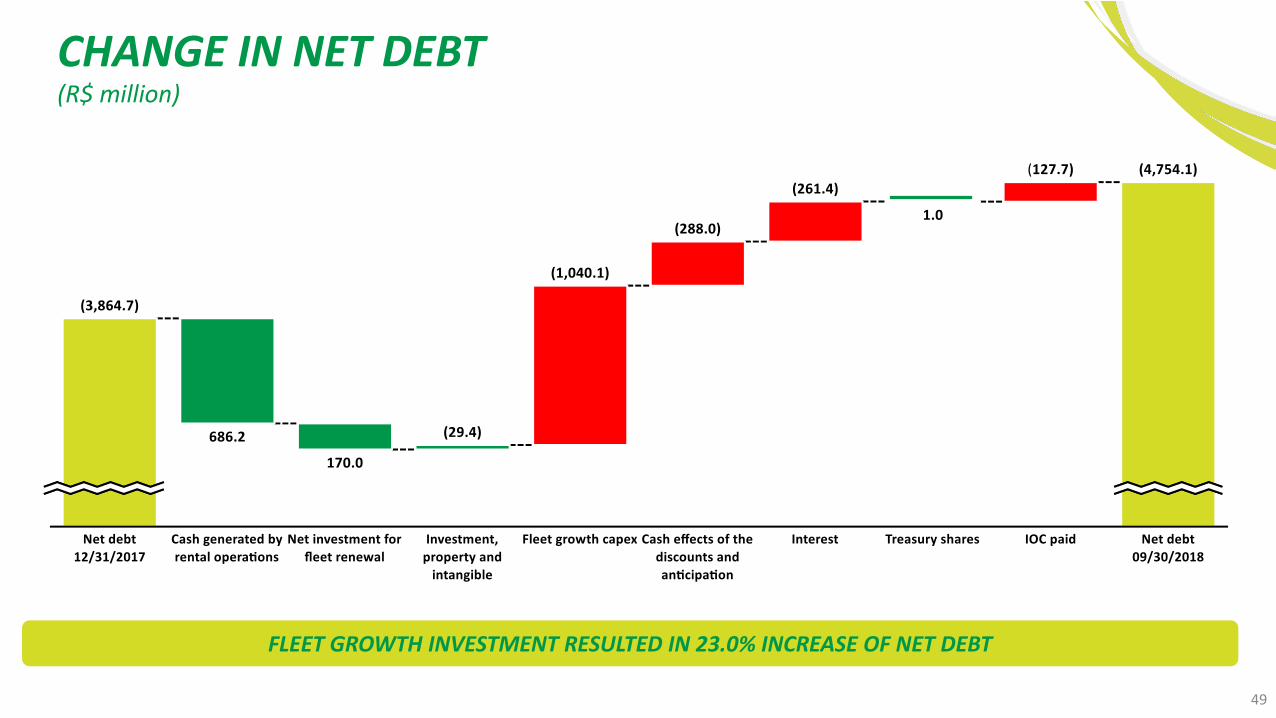

49

FLEET GROWTH INVESTMENT RESULTED IN 23.0% INCREASE OF NET DEBT

CHANGE IN NET DEBT(R$ million)

50

DEBT RATIOS

NET DEBT/EBITDA STABLE IN RELATION TO 2Q18, EVEN WITH GROWING FLEET

Net debt versus fleet value

BALANCE AT THE END OF PERIOD 2013 2014 2015 2016 2017 9M18

Net debt / Fleet value 48% 40% 44% 45% 55% 56%

Net debt / annualized EBITDA 1.5x 1.4x 1.7x 2.1x 2.9x 3.1x

Net debt / Equity 1.0x 0.8x 0.8x 0.9x 1.5x 1.6x

EBITDA / Net financial expenses 8.3x 6.4x 4.6x 4.2x 4.2x 4.4x

1,332.8 1,322.3 1,588.62,084.0

3,864.74,754.1

2,797.93,296.3 3,642.7

4,623.6

7,038.18,416.0

2013 2014 2015 2016 2017 9M18

Net debt Fleet value

(R$ million)

51

DEBT MATURITY PROFILE (PRINCIPAL)(R$ million)

As of September 30, 2018

STRONG CASH POSITION TO SUPPORT COMPANY’S GROWTH

2,666.3

146.9532.8

1,187.0

330.6

1,093.4 1,096.7

1,573.0

628.1425.1

258.3

Cash andfinancial assets

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 to 2032

2,197.3

ROIC VERSUS COST OF DEBT AFTER TAXES

STRONG PACE OF GROWTH WITH VALUE CREATION

16.7%17.8%

17.0%15.4% 15.6%

12.8%

6.0%

8.0%9.5% 10.2%

7.6%

5.0%

2013 2014 2015 2016 2017 9M18 annualized

ROIC Cost of debt after taxes

9.8p.p.10.7p.p.7.5p.p. 5.2p.p.

8.0p.p.

ROIC considered each year´s effective income tax and social contribution rate

*

(*)Adjusted by the one-time costs incurred - Hertz Brasil acquisition and Franchisees incorporation

7.8 p.p.

21

53

Website: www.localiza.com/ir E-mail: [email protected] Phone: 55 31 3247-7024

The material presented is a presentation of general background information about LOCALIZA as of the date of the presentation. It is information in summary form and does not purport to becomplete. It is not intended to be relied upon as advice to potential investors. No representation or warranty, express or implied, is made concerning, and no reliance should be placed on, theaccuracy, fairness, or completeness of the information presented herein.

This presentation contains statements that are forward-looking within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements are only projections and are not guarantees of future performance. Investors are cautioned that any such forward-looking statements are and will be, as the case may be, subjectto many risks, uncertainties and factors relating to the operations and business environments of LOCALIZA and its subsidiaries that may cause the actual results of the companies to be materiallydifferent from any future results expressed or implied in such forward-looking statements.

Although LOCALIZA believes that the expectations and assumptions reflected in the forward-looking statements are reasonable based on information currently available to LOCALIZA’s management,LOCALIZA cannot guarantee future results or events. LOCALIZA expressly disclaims a duty to update any of the forward-looking statement.

Securities may not be offered or sold in the United States unless they are registered or exempt from registration under the Securities Act of 1933.

This presentation does not constitute an offer, invitation or solicitation of an offer to subscribe to or purchase any securities. Neither this presentation nor anything contained herein shall form the basis ofany contract or commitment whatsoever.

DISCLAIMER