Investor Presentation - Bangkok Bank · Investor Presentation December 2013 ... 2013 , CLMV refers...

42

Investor Presentation December 2013 24.02.2014

Transcript of Investor Presentation - Bangkok Bank · Investor Presentation December 2013 ... 2013 , CLMV refers...

Investor Presentation

December 2013

24.02.2014

Table of Contents

1. Thai economy

2. Strengthening bank and client base

3. BBL’s financial results

Thailand is facing short-term challenges, but fundamentals in the long-term are still intact.

• Short-term challenges:

1) Domestic political situation

2) Global financial markets volatilities

• Long-term opportunities:

1) ASEAN Economic Community integration

2) Urbanization in provincial areas

3) Diversification of cross-border investment

Thai economy in 2014-2015

4

Political issue

AEC Integration

Urbanization

Cross-border investment

Thai economy in 2014-2015

Infrastructure projects will help support the economy later

Headwind Tailwind

Capital outflows

Recoveries in advanced economies

Source: National Economic and Social Development Board of Thailand

Expected GDP growth in 2013 YoY (%)

0.0%

4.0%

8.0%

18 Feb 20 May 19 Aug 18 Nov

5

4.5-5.5% 4.2-5.2%

3.8-4.3%

3.0% (or lower)

Date of revised forecast

Looking back, 2013 GDP growth was lower than expected

40

44

48

52

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Business sentiment index in 2013

Source: Bank of Thailand

145

146

147

148

149

150

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Private consumption index in 2013 Index (2000=100)

Source: Bank of Thailand

0%

10%

20%

30%

1,500

1,750

2,000

2,250

2,500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Tourism industry decline 2013 No. of tourists (‘000)

Source: Bank of Thailand

230

235

240

245

250

255

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Private investment index in 2013

Source: Bank of Thailand

Index (2000=100)

6

For 2014, volatility will continue in short-term

Political uncertainty will slow down the economy

7

31 Oct 13 The

government passed the

amnesty bill, Start of Bangkok protest

9 Dec 13 Government

dissolved parliament

13 Jan 14 1st Day of Bangkok

Shutdown at 7 key inter sections

11 Nov 13 The Senate

voted to reject the amnesty

bill

21 Jan 14 Emergency

Decree invoked

2 Feb 14 General election

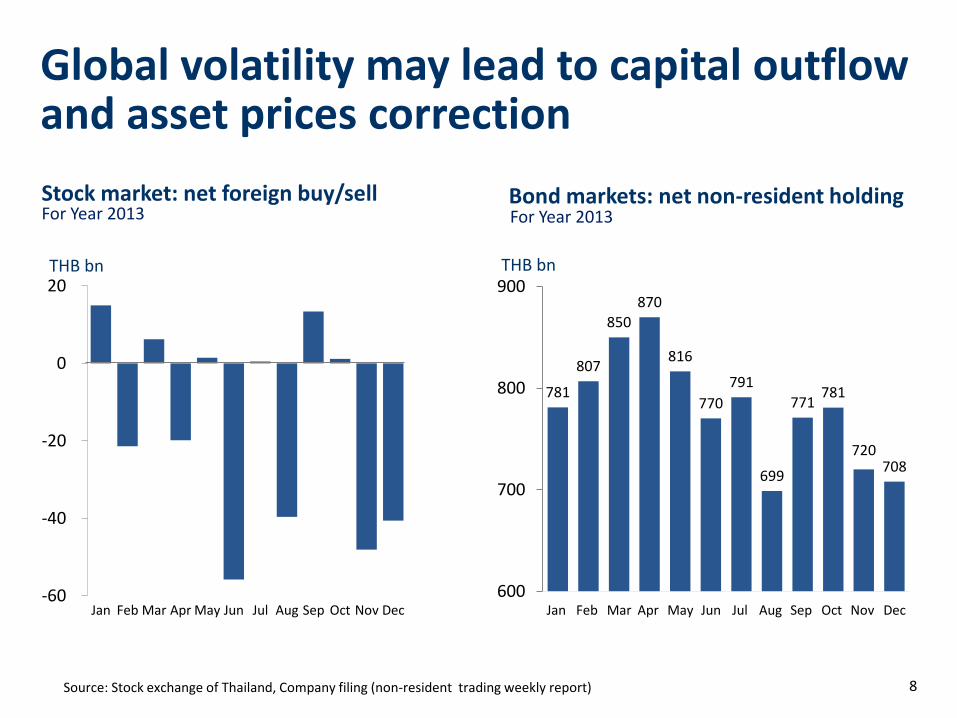

Global volatility may lead to capital outflow and asset prices correction

8 Source: Stock exchange of Thailand, Company filing (non-resident trading weekly report)

-60

-40

-20

0

20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

THB bn

Stock market: net foreign buy/sell For Year 2013 Bond markets: net non-resident holding

781

807

850

870

816

770

791

699

771 781

720 708

600

700

800

900

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

For Year 2013

THB bn

Thus, 2014 GDP growth is at 3.0-4.0%

Source: National Economic and Social Development Board of Thailand

Recent GDP growth YoY (%)

7.8%

0.1%

6.4%

2.9% 3.0-4.0%

0.0%

4.0%

8.0%

2010 2011 2012 2013 2014f

4.1%

9

10

28.4%

16.4%

3.1%

-0.2%

5.0-7.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

2010 2011 2012 2013 2014F

Source: NESDB

Supported partly by exports that will increase given economic recovery in advanced countries

Export growth

YoY (%)

11

We continue to strengthen ourselves according to long-term fundamental

drivers that are still intact

1. With our strategic location, Thailand will benefit from AEC integration

12

1,110

1,182

626

403

487

432

BOI application value Baht bn

2008

2009

2010

2011

2012

2013 525

648

396

236

351

297

Foreign Direct Investment Baht bn

2008

2009

2010

2011

2012

2013 Japan 283

China 43

Source: Ministry of Transport

2. Benefits of connectivity still valid

Economic corridors New bridges and economic zones

13

3. Increasing connectivity and border trade remain in trend

14 Note: For the year ended December 31, 2013 , CLMV refers to Cambodia, Laos, Myanmar and Vietnam. Source: The customs Department, Bangkok Bank analysis

Myanmar US 3.8 billion

+21% Ex: Refine fuel, Beverages, Machinery

Im: Natural gas, Wood

Laos US 3.8 billion +5% Ex: Refine fuel, Cars, Iron and steel Im: Fuel, Metal ores, Wood

Cambodia US 4.3 billion +13% Ex: Refine fuels, Sugar, Precious stone, Beverage Im: Electrical machinery, Fruit, Vegetables

Vietnam US 7.2 billion +11% Ex: Refine fuel, Polymers, Chemical products Im: Electrical household appliances, Iron, Steel

Malaysia US 13.0 billion

+5% Ex: Refine fuel, Motor cars, Machines Im: Computers, Crude oil

15

CLMV countries are growing

6.1% 7.1% 7.3% 7.0%

3.0%

6.0%

9.0%

2009 2010 2011 2012f 2013f

Note : Since 2011 estimated by International Monetary Fund Source: Bloomberg

Cambodia GDP growth % YoY

5.1% 5.3% 5.9%

6.4% 6.8%

3.0%

6.0%

9.0%

2009 2010 2011 2012f 2013f

Myanmar GDP growth % YoY

7.5% 8.1% 8.0% 7.9%

8.3%

3.0%

6.0%

9.0%

2009 2010 2011 2012f 2013f

Lao P.D.R GDP growth % YoY

5.4% 6.4% 6.2%

5.2% 5.3%

3.0%

6.0%

9.0%

2009 2010 2011 2012f 2013f

Vietnam GDP growth % YoY

0.0%

Thai companies have taken advantage of strong balance sheets to invest abroad

16

Bangkok Bank

Conservative balance sheet and superior liquidity management– no concerns from short-term challenges

1. Asset quality remains high

18

BBL’s loan portfolio Over 60% in large corporate,

mid-sized SMEs

Note: As at December 2013 Consolidated

Large Corporate

44%

Mid-sized SMEs

17%

Small-sized SMEs

11%

Consumer 12%

International 16%

10%

2%

55.6

45.6 42.6 42.3 43.2

4.4%

3.0% 2.7%

2.3% 2.2%

-1%

1%

3%

5%

0

20

40

60

80

100

2009 2010 2011 2012 2013

NPL NPL Ratio

NPL ratio declines

Baht bn

19

2. Large reserves for NPLs

157%

71%

BBL System

Excess LLR

Required LLR by BOT

BBL System

214%

148%

BBL System

5.3%

4.0%

Note : /1 System refers to average of top 5 banks’ consolidated figure and includes BBL, KBANK, SCB, KTB and BAY

/2 System refers to average of top 7 banks’ consolidated figure and includes BBL, KBANK, SCB, KTB, BAY, TMB,

TISCO Top 7 banks accounted for 81% of commercial banks registered in Thailand's assets as at December 2013

/1

Excess reserves to required reserves at 157% or Baht 57 Billion December 2013

High LLR/NPL December 2013

High LLR/Loan December 2013

/2 /2

3. Balance sheet is liquid

20

20

Note: Liquid assets refer to cash, interbank assets and investments.

High liquid assets of Baht 839 billion

610 670

631

814 839

0

200

400

600

800

1,000

2009 2010 2011 2012 2013

Source: Bangkok Bank filings

Baht bn

Liquid assets at 1/3 of total assets

As at December 2013

Liquid assets 32%

Other assets 68%

4. Business loan demand continues

21

88% in business loans

Note: As at December 2013 Consolidated

• Demand for business loans remains strong, largely due to export sector recovery, more than offsetting slowdown in consumer loan growth

• International Lending provide diversification

Business loans 88%

Customer loans 12%

16% in international loans

International 16%

Others 84%

Strong fundamentals – well placed to benefit from opportunities

Bangkok Bank

1. Sizable international banking operations, best placed to service clients expanding in the region

23

Long-standing international presence

Japan Branches: 2 Number of Years: 59

UK Branches: 1 Number of Years: 57

USA Branches: 1 Number of Years: 30

Laos Branches: 1 Number of Years: 22

Philippines Branches: 1 Number of Years: 19

Vietnam Branches: 2 Number of Years: 22

China/1

Branches: 4 Number of Years: 28

Myanmar/2

Rep. Office: 1 Number of Years: 19

Malaysia/1

Branches: 5 Number of Years: 55

Singapore Branches: 1 Number of Years: 57

Indonesia Branches: 3 Number of Years: 46

Taiwan Branches: 3 Number of Years: 49

Hong Kong Branches: 2 Number of Years 60

Note: As at December 2013

/1 Wholly-owned subsidiaries

/2 Representative office

Source: Bangkok Bank filings

International lending as a % of total lending

15.9%

1.8% 1.5% 1.4% 1.3% 0.2% 0%

4%

8%

12%

16%

20%

BBL SCB TMB KTB Kbank BAY

Note: As at December 2013 for BBL and December 2012 for others Source: Bangkok Bank filings

Number of international branches/1

27

8 5 4 4

2

0

5

10

15

20

25

30

BBL KTB Kbank SCB BAY TMBNote: As at December 2013 /1 Including the representative office in Myanmar Source: Bangkok Bank filings

Well-established operations to support Chinese and Japanese who want to expand in the region

24

4 Branches in Shanghai, Beijing, Xiamen and Shenzhen

Only Thai bank to get local bank license 28 years operating in China

Chinese Corporate Unit

Chinese Branches

2 Branches in Tokyo and Osaka

59 years operating in Japan

Cooperation agreements with 27 Japanese banks

Japanese Corporate Unit

Japanese Branches

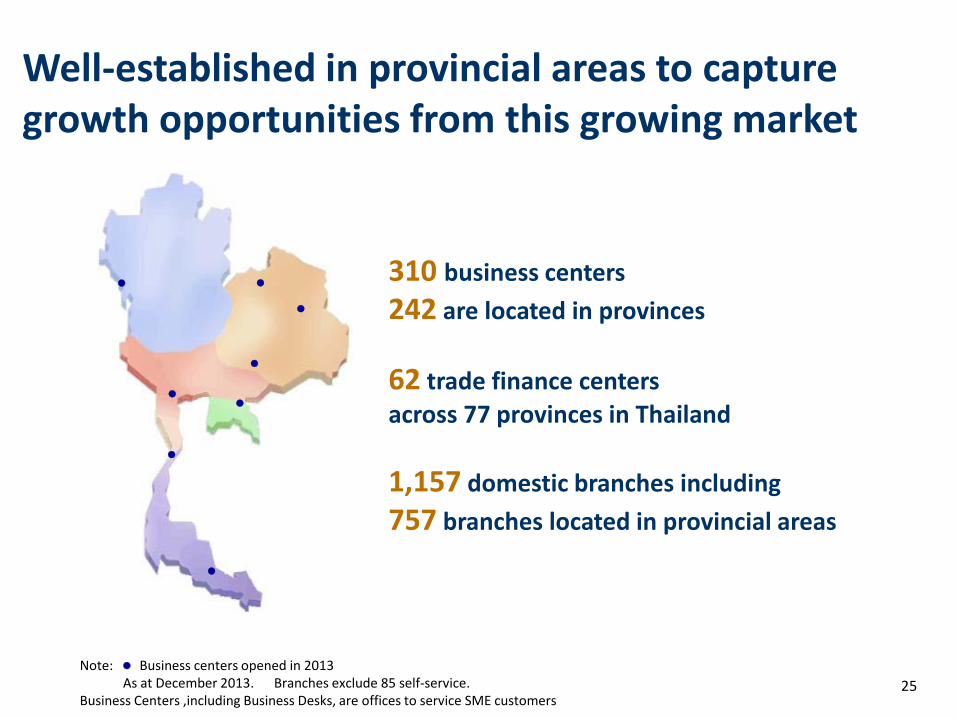

Well-established in provincial areas to capture growth opportunities from this growing market

Note: Business centers opened in 2013 As at December 2013. Branches exclude 85 self-service.

Business Centers ,including Business Desks, are offices to service SME customers

310 business centers

242 are located in provinces

62 trade finance centers

across 77 provinces in Thailand

1,157 domestic branches including

757 branches located in provincial areas

25

26

2. When investment returns, business loans and BBL will benefit

Over 4,400 corporate customers

Over 250,000 SME customers

Including all major construction companies

Note: As at December 2013 *System refers to 16 commercial banks registered in Thailand Source: Bank of Thailand (FI_CB_016_S2), Bangkok Bank analysis

Business lending market share

29% System* (exc. BBL)

71%

BBL 29%

Liquidity and capital to fund lending growth in near-term

27

60%

70%

80%

90%

100%

110%

System LDR/1

96.4%

BBL 90.6%

92.6%

108.2%

LDR always lower than system

Note: /1 System refers to 16 commercial banks registered in Thailand

LDR refers to Loan-to-Deposit ratio Source: Bank of Thailand, Bangkok Bank analysis

14.4%

11.8%

0%

5%

10%

15%

20%

BBL System

Tier 1 capital ratio/1

As at December 2013

Note : /1 Tier 1 ratio is as Bank of Thailand’s definition /2 Tier 1 ratio included net profit for the second-half of 2013

and net of final dividend 2013 /3 System refers to average of 6 bank’s consolidated figure,

including BBL, KBANK, SCB, KTB, BAY, TMB

14.8%/2

/3

Financial results Sustainable growth across business cycles

Year 2013

1,1

43

1,2

56

1,4

70

1,6

04

1,7

53

0

500

1,000

1,500

2,000

2009 2010 2011 2012 2013

Loan growth slightly above target

29

Baht bn

+9.2%

-3.2% +9.9%

+17.0% +9.1%

55.6

45.6 42.6 42.3 43.2

4.4%

3.0% 2.7%

2.3% 2.2%

-1%

1%

3%

5%

0

20

40

60

80

100

2009 2010 2011 2012 2013

NPL NPL Ratio

30

Significant improvement in asset quality

NPL ratio declines

Baht bn

BBL’s loan portfolio

Note: As at December 2013 Consolidated

Large Corporate

44%

Mid-sized SMEs

17%

Small-sized SMEs

11%

Consumer 12%

International 16%

Steady provisioning policy 7

.6

7.6

12.0

7.2

8.6

66 60

82

45 49

-15

0

15

30

45

60

75

90

0

5

10

15

20

2009 2010 2011 2012 2013

Provisioning expenses (Baht bn)

Provisioning expenses / loans - Credit cost (Bps)One-time provisioning expenses (Baht bn)

31

Baht bn Bps Baht bn

37 37 38 36 36

29 35 47 52 57

0

30

60

90

120

2009 2010 2011 2012 2013Excess reserves over BOTrequirement (Baht bn)Allowance required by BOT(Baht bn)

88 93 85 72

66

Stable provision expenses Excess loan loss reserves increase

1,361 1,394 1,588

1,835 1,935

0

500

1,000

1,500

2,000

2009 2010 2011 2012 2013

+5.5%

Deposits Baht bn

32

Deposits steadily increase

Stable deposit funding and among the lowest cost of funds

Lower cost of funds than system

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2009 2010 2011 2012 2013

System/2

2.3%

BBL 2.1%

33

Note: /1 Includes interbank and money market items, debt issued and borrowings, derivatives liabilities, liabilities payable on demand.

/2 System refers to BBL, KBANK, SCB, KTB, BAY and TMB.

Source: Bangkok Bank filings

86

%

81

%

85%

85%

84%

10

%

14

%

11

%

14

%

16

%

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013

Deposits B/Es Other liabilities /1

Reliance on deposits

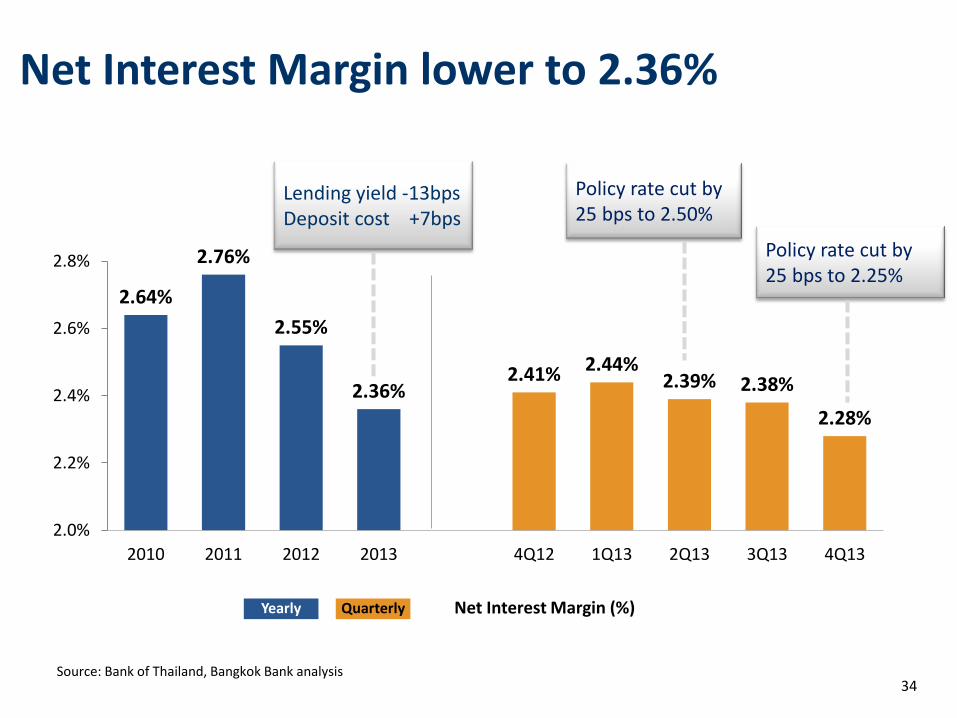

Net Interest Margin lower to 2.36%

Source: Bank of Thailand, Bangkok Bank analysis

2.64%

2.76%

2.55%

2.36% 2.41% 2.44%

2.39% 2.38%

2.28%

2.0%

2.2%

2.4%

2.6%

2.8%

2010 2011 2012 2013 4Q12 1Q13 2Q13 3Q13 4Q13

Quarterly Yearly Net Interest Margin (%)

34

Lending yield -13bps Deposit cost +7bps

Policy rate cut by 25 bps to 2.50%

Policy rate cut by 25 bps to 2.25%

Improvement in fee income revenues

15.8 17.3 18.1 19.1 21.2

0

5

10

15

20

25

2009 2010 2011 2012 2013

Baht bn

+5.5% +4.9% +9.2%

35

+11.1%

+10.5%

Net fee income

Better-diversified fee income

12%

16%

25% 25%

9%

13%

Bancassurance & Mutual funds Loan-related fees

Credit cards Transaction services

Global market services Others

4%

15%

23% 35%

16%

7%

For the year 2007 Baht 4.4 billion

For the year 2013 Baht 28.4 billion

36

Note: /1 CARG of 2007-2013 of net fee income /2 CARG +29.9% of bancassurance & mutual funds during 2007-2013

/2

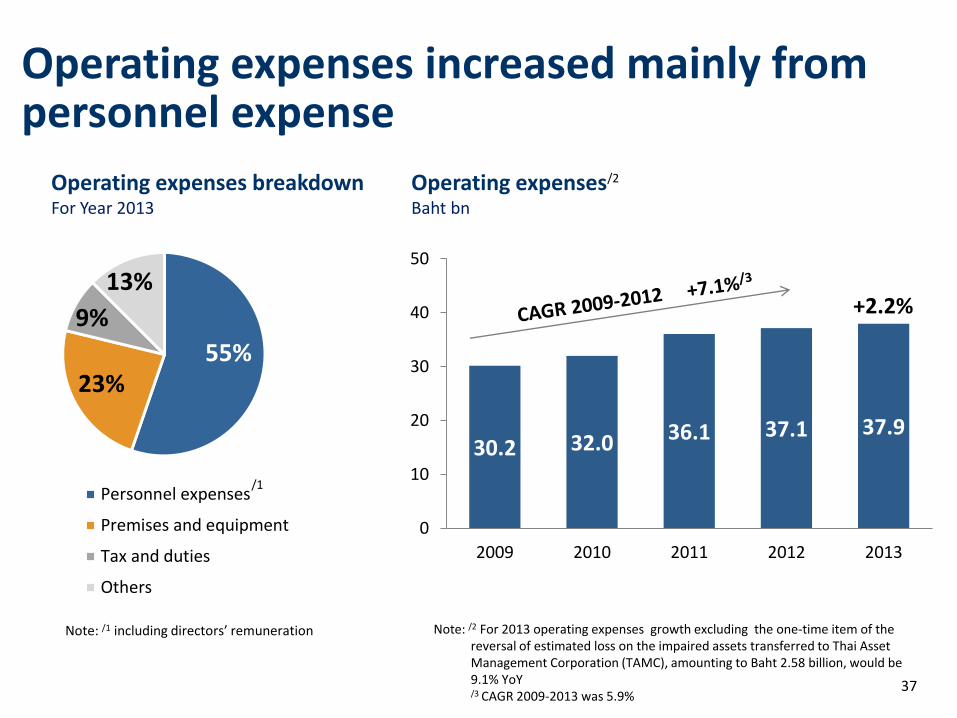

Operating expenses increased mainly from personnel expense

30.2 32.0 36.1 37.1 37.9

0

10

20

30

40

50

2009 2010 2011 2012 2013

+2.2%

37

Operating expenses breakdown For Year 2013

55% 23%

9%

13%

Personnel expenses

Premises and equipment

Tax and duties

Others

/1

Note: /1 including directors’ remuneration

Operating expenses Baht bn

/2

Note: /2 For 2013 operating expenses growth excluding the one-time item of the reversal of estimated loss on the impaired assets transferred to Thai Asset Management Corporation (TAMC), amounting to Baht 2.58 billion, would be 9.1% YoY /3 CAGR 2009-2013 was 5.9%

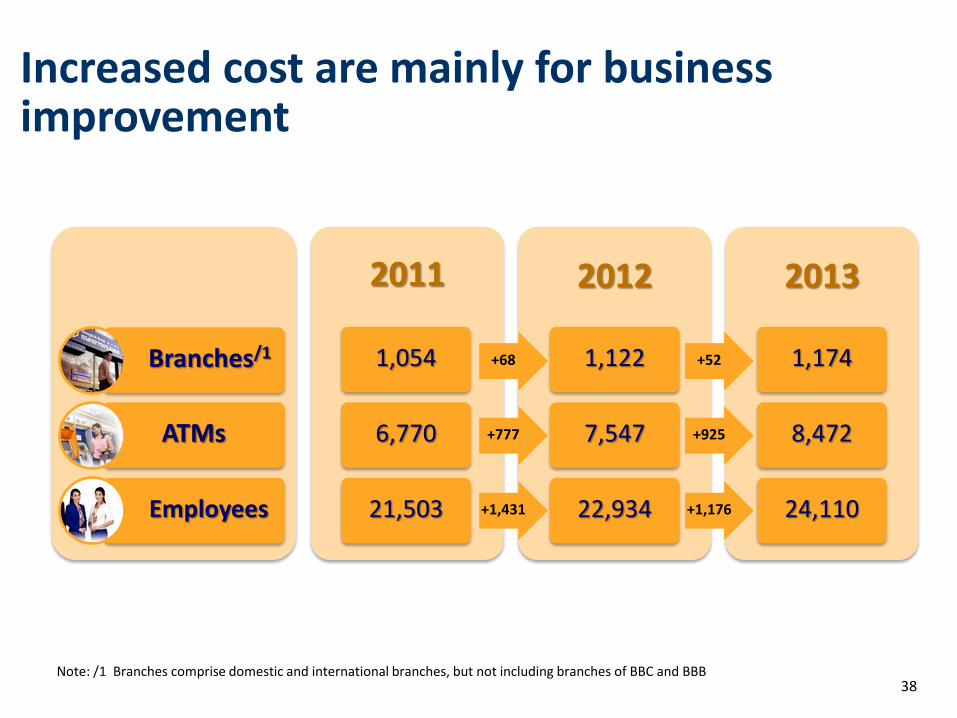

Increased cost are mainly for business improvement

38 Note: /1 Branches comprise domestic and international branches, but not including branches of BBC and BBB

Branches/1

ATMs

Employees

2011

1,054

6,770

21,503

2012

1,122

7,547

22,934

2013

1,174

8,472

24,110

+68

+777

+1,431

+52

+925

+1,176

1.5%

2.1%

41.5% 44.9%

0%

20%

40%

60%

0%

1%

2%

3%

4%

BBL System

Cost to average assets (L)

Cost to income (R)

Low cost to asset and cost to income ratio For the year 2013

BBL’s cost-to-income ratio

Efficient cost management

39

42.2% 43.8% 43.5% 41.5%/1

0%

10%

20%

30%

40%

50%

2010 2011 2012 2013

Note: /1 For 2013 operating expenses include the one-time item of the reversal of estimated loss on the impaired assets transferred to Thai Asset Management Corporation (TAMC), amounting to Baht 2.58 billion. If this is not included, such item, the cost to income ratio would be 44.3%.

/1

Note : /1 System refers to average of top 6 bank’s consolidated figure and includes BBL, KBANK, SCB, KTB, BAY and TMB

Source: Bangkok Bank filings

Consistently delivering profits across business cycles

20.6 24.6

27.3 31.8

35.9

0

10

20

30

40

2009 2010 2011 2012 2013

Baht bn

+12.7%

40 Note: Corporate tax rate reduced from 30% to 23% in 2012 and to 20% in 2013 onwards

Summary

With our prudent and conservative approach, BBL will be able to withstand short-term volatility

and continues to deliver steady growth across business cycles

41

This presentation is made by Bangkok Bank and may not be copied, altered, offered, sold or otherwise distributed to any other person by any recipient without the consent of Bangkok Bank. Although all reasonable effort has been made to ensure the facts stated herein are accurate and that the opinions contained herein are fair and reasonable, this document is selective in nature and is intended to provide an introduction to, and overview of, the business of Bangkok Bank. Where any information and statistics are quoted from any external source, such information or statistics should not be interpreted as having been adopted or endorsed by Bangkok bank as being accurate. Neither Bangkok Bank nor any of its directors, officers, employees, and advisors nor any other person shall have any liability whatsoever for loss howsoever arising, directly or indirectly, from any use of this information. The facts and information contained herein are as up to date as is reasonably possible and may be subject to revision in the future. Neither Bangkok Bank nor any of its directors, officers, employees or advisors nor any other person makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained in this presentation. Neither Bangkok Bank nor any of its directors, officers, employees and advisors nor any other person shall have any liability whatsoever for loss howsoever arising, directly or indirectly, from any use of this presentation. This presentation may contain projections or other forward-looking statements related to Bangkok Bank that involve risks and uncertainties. Readers are cautioned that these statements are only projections and may differ materially from actual future results or events. All forward-looking statements are based on information available to Bangkok Bank on the date of its posting and Bangkok Bank assumes no obligation to update such statements unless otherwise required by applicable law. This presentation does not constitute an offer or invitation to subscribe for, or purchase, any shares of Bangkok Bank.

Contact: Investor Relations Team Tel (66) 2 626 4981 Fax (66) 2 231 4890 Email: [email protected] Bangkok Bank Website www.bangkokbank.com

For further information

42