Study On Brand Awareness of HyperCITY Retail India Ltdali Project Report

INVESTMENT IN RETAILBy Shop 4 Solutions

7_4_JAI SUBRAMANIAM.indd 3627_4_JAI SUBRAMANIAM.indd 362 9/13/2008 12:26:31 AM9/13/2008 12:26:31 AM

RETAIL SUPPORT Investments in Retail

INDIA RETAIL REPORT 2009 363

and opportunities in this sector. To facilitate easier flow of Foreign Direct Investments (FDI) inflow, instead of having to seek Foreign Investment Promotion Board (FIPB) approval,

FDI up to 100 per cent is allowed ●

under the automatic route for cash and carry wholesale trading and export trading. FDI up to 51 per cent is allowed, with ●

prior Government approval for retail trade in ‘Single Brand’ products with the objective of attracting investment, technology and global best practices and catering to the demand for such branded goods in India. However, retailing of multiple brands, ●

even if the goods are produced by the same manufacturer, is presently not allowed.Relaxation of FDI restrictions

are being vigorously pursued by the business and trade coalitions and are expected to fall in place over the next 3-5 years.

Strategic license agreements, franchising, distribution, manufacturing, joint ventures and cash and carry wholesale trading are the most common channels for entry of foreign retailers

Strategic license agreements: This route involves the foreign company

India has one of the largest number of retail outlets in the world. Of the 12 million retail outlets present in the country, nearly 5 million sell food and

related products. Organised retail segment has been growing at a blistering pace, exceeding all previous estimates.

The rapid growth of the economy, favourable investment regime, liberal policy changes and procedural relaxations, has resulted in a multitude of global corporations investing in India. The generous inflow of FDI is playing a significant role in the economic growth of the country. Projections say that the country will attract US$ 35 billion in FDI in 2008-09 (as per data released by the Ministry of Commerce and Industry).

The regulatory and supervisory policies are being reshaped and reoriented to meet the new challenges

India is one of the most attractive markets for retail investment. Many national and global players have been investing in the retail segment and have ambitious plans for further expansion. The vast middle class with rising purchasing power are attracting global retail giants into the almost untapped retail industry.

entering into a licensing agreement with a domestic retailer or partnering with Indian promoter owned companies in the Middle East (UAE) or South East Asian countries (Singapore, Malaysia,Thailand, Indonesia).

Franchising: This is a widely taken entry route, with many international brands setting up shop via this provision driven mainly by the need to meet the increasing consumer expectations of quality, ambience and brand experience. In addition, this route also helps the big retail players to rapidly foray into the tier II and III towns and rural areas.

The franchising routes permitted in India are:

Unit franchisee: ● Franchisee is granted rights to operate a single business unitMultiple franchisee: ● Individual unit franchises are given to multiple outlets, a route primarily used by domestic brandsMaster franchisee: ● Rights are granted for an entire territory to the master franchisee and the master franchisee can in turn grant unit and multiple franchisees in that territoryRegional franchisee: ● This route is similar to that of the master franchisee, but applicable on a larger scale

7_4_JAI SUBRAMANIAM.indd 3637_4_JAI SUBRAMANIAM.indd 363 9/13/2008 12:26:39 AM9/13/2008 12:26:39 AM

INDIA RETAIL REPORT 2009364

According to industry estimates, retail franchising has been growing at the rate of 60 per cent in the last three years and is set to grow two-fold in the next five years.

Cash-and-carry wholesale trading: 100 per cent FDI is allowed in wholesale trading which involves building a large distribution infrastructure to assist local retailers and manufacturers.

Joint ventures: International firms can enter into agreements with domestic players, and set up base in India. The share of the multinational is restricted to 49 per cent in this route.

Manufacturing: International retailers can set up manufacturing units for their products in India. Entry through this route entails the company the rights to retail the products in India through individual retailing outlets.

Distribution: An international company can set up distribution offices in India and supply products to the local retailers. Franchisee outlets can also be

set up in this route.The labour laws in India are under

the scanner for higher liberalisation, with the Government permitting flexibilities in the rules in emerging retail hubs like Bangalore and Hyderabad. Also, this policy framework involves numerous licensing formalities for the retailers and hence there is a demand for a single window clearance system which would reduce the entry and establishment timelines.

The Government is expected to take a standardised approach in land and rent reforms to improve the real estate regulatory environment and

facilitate easy access to retail space for international investors. Solutions to problems related to the lease rentals and pro-tenancy laws, which significantly deter international investors, are being pursued by the Government, with initiatives such as the Special Economic Zones (SEZs), allotment of Government controlled land etc.

VAT (Value Added Tax) has been introduced and implemented in most states and territories, and many industry verticals to resolve the multiple taxation issue and maintain uniform prices across regions.

The Agricultural Produce Marketing Committee Act (APMC), which curtails direct sourcing of agriculture produce (grocery, food grains) is proposed to be amended soon. Contract farming is already being pursued in certain states with players like Reliance and Pepsi Co. forging alliances with local farmers for direct procurement of raw materials. The Government is encouraging contract farming practice, as it benefits both the farmers and the corporate retailers, with the former gaining access to better prices and the latter to a source of steady supply.

INVESTMENT SCENARIOInternational retail giants are

increasingly choosing India as the target market, with most of the global retail power-houses exploring entry options into the country’s retail market.

Wal-Mart has entered into a 50:50 Joint Venture and franchisee agreement with Bharti Retail Ltd. and plans to set up its first cash-n-carry outlet by 2007-08. The company plans to open

One of the key players in the rural retail segment is ITC with its Choupal Sagar

initiative. ITC has 14 outlets in operation presently and plans to increase the

number to 700 over the next 7-10 years.

7_4_JAI SUBRAMANIAM.indd 3647_4_JAI SUBRAMANIAM.indd 364 9/13/2008 12:26:45 AM9/13/2008 12:26:45 AM

RETAIL SUPPORT Investments in Retail

INDIA RETAIL REPORT 2009 365

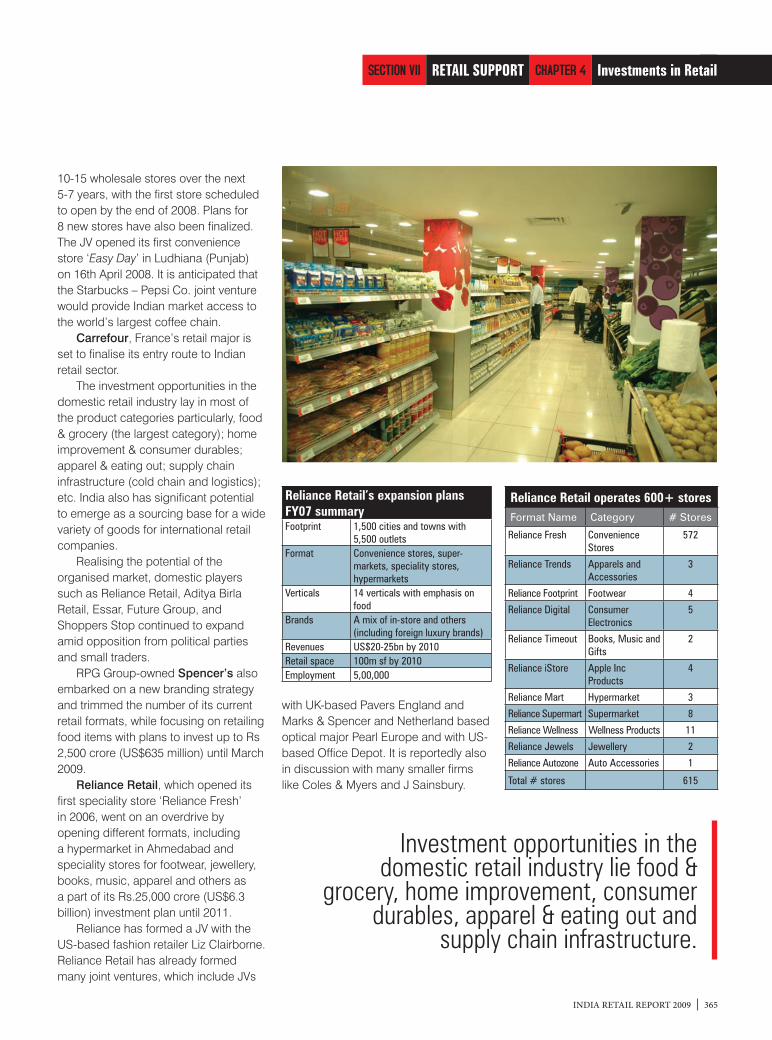

10-15 wholesale stores over the next 5-7 years, with the first store scheduled to open by the end of 2008. Plans for 8 new stores have also been finalized. The JV opened its first convenience store ‘Easy Day’ in Ludhiana (Punjab) on 16th April 2008. It is anticipated that the Starbucks – Pepsi Co. joint venture would provide Indian market access to the world’s largest coffee chain.

Carrefour, France’s retail major is set to finalise its entry route to Indian retail sector.

The investment opportunities in the domestic retail industry lay in most of the product categories particularly, food & grocery (the largest category); home improvement & consumer durables; apparel & eating out; supply chain infrastructure (cold chain and logistics); etc. India also has significant potential to emerge as a sourcing base for a wide variety of goods for international retail companies.

Realising the potential of the organised market, domestic players such as Reliance Retail, Aditya Birla Retail, Essar, Future Group, and Shoppers Stop continued to expand amid opposition from political parties and small traders.

RPG Group-owned Spencer’s also embarked on a new branding strategy and trimmed the number of its current retail formats, while focusing on retailing food items with plans to invest up to Rs 2,500 crore (US$635 million) until March 2009.

Reliance Retail, which opened its first speciality store ‘Reliance Fresh’ in 2006, went on an overdrive by opening different formats, including a hypermarket in Ahmedabad and speciality stores for footwear, jewellery, books, music, apparel and others as a part of its Rs.25,000 crore (US$6.3 billion) investment plan until 2011.

Reliance has formed a JV with the US-based fashion retailer Liz Clairborne. Reliance Retail has already formed many joint ventures, which include JVs

with UK-based Pavers England and Marks & Spencer and Netherland based optical major Pearl Europe and with US-based Office Depot. It is reportedly also in discussion with many smaller firms like Coles & Myers and J Sainsbury.

Investment opportunities in the domestic retail industry lie food &

grocery, home improvement, consumer durables, apparel & eating out and

supply chain infrastructure.

Reliance Retail operates 600+ storesFormat Name Category # Stores

Reliance Fresh Convenience Stores

572

Reliance Trends Apparels and Accessories

3

Reliance Footprint Footwear 4

Reliance Digital Consumer Electronics

5

Reliance Timeout Books, Music and Gifts

2

Reliance iStore Apple Inc Products

4

Reliance Mart Hypermarket 3

Reliance Supermart Supermarket 8

Reliance Wellness Wellness Products 11

Reliance Jewels Jewellery 2

Reliance Autozone Auto Accessories 1

Total # stores 615

Reliance Retail’s expansion plans FY07 summaryFootprint 1,500 cities and towns with

5,500 outletsFormat Convenience stores, super-

markets, speciality stores, hypermarkets

Verticals 14 verticals with emphasis on food

Brands A mix of in-store and others (including foreign luxury brands)

Revenues US$20-25bn by 2010Retail space 100m sf by 2010Employment 5,00,000

7_4_JAI SUBRAMANIAM.indd 3657_4_JAI SUBRAMANIAM.indd 365 9/13/2008 12:26:48 AM9/13/2008 12:26:48 AM

INDIA RETAIL REPORT 2009366

Pantaloon Retail, a Future Group venture, started its operations with Pantaloon Shoppe in 1993 and operates in over twenty diverse store formats, with a spectrum of offerings ranging from food and grocery to carpentry services.

Current retail space: Across 8m sf and over 400 stores in nearly 50 towns and cities. Space addition: 9m sf by June ‘08 and 30m sf June ‘12, after taking into account about 12-month delays.

Pantaloon’s Key JVsJV Partner BusinessStaples Inc. (USA) Offi ce suppliesAxiom Telecom Mobile phonesTalwalkars Fitness centresLiberty Footwear FootwearAlpha Airports Airport retailingBlue Foods Restaurants

Home Solutions Retail plans to invest Rs.5bn for expansion over the next two years.

Shopper’s Stop operates India’s largest chain of department stores under the Shoppers Stop brand. It also has five speciality retail formats:

Crossword Books, Gifts and musicMothercare Mother and Baby CareMAC Cosmetics, ArceliaBrio and Desi Café Fast Food chainsHome Stop Home Furnishings

It also owns 19% stake in HyperCITY and has option to raise this to 51% before Dec 2008.

Current retail space: 1.6m sf across 100+ stores in 15 cities (does not include Hypercity stores).

Space addition plans: Group plans to operate 6m sf by 2011, a delay of 12-months from their earlier plans.

HyperCity has shelved plans to launch its convenience store format, ExpressCity. As per the management, high real estate prices are making the convenience store format unprofitable as the gross margins here are thin. It has filed its prospectus to raise Rs. 3 bn through rights issue Capex for Shopper’s Stop (department store and

specialty retail) will be Rs3-4bn.Titan is India’s largest and world’s

sixth largest manufacturer and retailer of watches (34% FY07 sales) and jewellery (60% FY07 sales). Goldplus (mass market jewellery) and Eye+ (prescriptive eye-wear) formats are being scaled-up.

EXISTING RETAIL FRANCHISE (MAR-08)

World of Titan: 235 storesTanishq stores: 104 stores in 64 citiesMulti-brand outlets: 12,000+Eye+: 10 storesGoldPlus: 22 stores

SPACE ADDITION PLANS BY MARCH 09:

World of Titan: 300 storesTanishq: 124 storesGoldplus: 35 storesEye+: 65 storesTitan Industries is planning a re-

entry into the children’s segment. Titan plans to expand Eye+, eye-wear store, network to 200 stores over next 3-4 years. Eye+ stores stock over 1,000 brands of spectacle frames including Christian Dior, Elle, Montblanc and Tommy Hilfiger.

Vishal Retail plans to increase it retail space from 2.1m sf as on Mar ‘08 to 10m sf by Mar ‘11 across 500 stores from 100 stores as on Mar ‘08.

It plans to invest up to Rs.30bn over the next three years to open 400+ of stores, start a logistics subsidiary and enter wholesale retailing later this year.

Madura Garments currently has 50 Planet Fashion outlets and nine Trouser town outlets and have projected to increase to 300 outlets by 2009 and diversify into the women’s wear segment.

Bata India Ltd. is looking at adding another 40 stores to its existing 1,100 outlets.

Trent is one of India’s leading retailers and is a part of the Tata group. It operates through three verticals of 42 stores: Westside (Department stores): 29; Star Bazaar (Hypermarket stores): 3; Landmark (Books and gifts stores): 10

Expansion plans by Mar ‘10: 100 stores: Westside: 60 stores; Star Bazaar : 15-20 stores; Landmark: 25 stores

This will take their retail space from the current 1mn sft to 1.6mn sft by 2009. Tata group has launched mall development and operation business

Trent is planning to launch a value apparel chain in next six months. The proposed

format would penetrate 50 towns within three years. Trent already operates four

Star Bazaar hypermarkets.

7_4_JAI SUBRAMANIAM.indd 3667_4_JAI SUBRAMANIAM.indd 366 9/13/2008 12:26:51 AM9/13/2008 12:26:51 AM

RETAIL SUPPORT Investments in Retail

INDIA RETAIL REPORT 2009 367

and the electronic stores ‘Croma’ (17 stores) through a separate subsidiary of Tata sons, Infiniti Retail. Recently Trent’s management announced plans to more than double the store count from 40 presently to 100 by Mar ‘10.Trent is also planning to launch a new value apparel chain in next six months. The proposed value chain would penetrate 50 towns within three years. Trent already operates four hypermarket stores under brand name of Star Bazaar. UK’s supermarket giant Tesco Plc. has made a foray into India, announcing that it would set up a cash-and-carry (C&C) business even as it inked an exclusive franchise agreement with Trent, the retail arm of India’s Tata Group, for providing merchandise and logistic support. The supermarket group would make an initial investment of £60 million ($120 million) in the C&C business over the first two years. It plans to open at least three large “hubs” in Delhi, Mumbai and Bangalore and set up smaller ones in satellite towns and cities.In January 2007, Aditya Birla group announced plans to enter the retail sector with the acquisition of south India based Trinethra Super Retail. Trinethra group operated 170 stores across 0.5m sf retailing food and grocery in Andhra

Pradesh, Kerala, Karnataka and Tamil Nadu.

RETAIL FRANCHISECurrently: 500+ “More” storesStore size: Super markets 5,000-

10,000 sf and hypermarket stores 50,000-75,000 sf

Expansion plans over 3 years:1,000 supermarkets and hypermarkets

Investment plans: US$2-2.5bnEmployment: 60,000 peopleThe group has relaunched 35

Trinethra stores as a part of ‘More’ chain and 300 more will be opened by March 2008. The group also plans to open consumer durables and information technology (CDIT) stores. CDIT stores

will be on the lines of Pantaloon’s e-zone, Tata group’s Croma and Reliance Digital. It plans to open 150 CDIT stores by 2010 and has tied up with companies like Godrej, Videocon, LG and Samsung. Cure & Care, the retail healthcare arm of Manipal Education and Medical group, has tied up with the retail ventures of Aditya Birla group and Jubilant Organosys, to set up wellness boutiques within their departmental stores.

Subhiksha currently has a nation-wide presence with over 1,300 outlets spread across 2.5m sf. It plans to have 2,000 stores by 2009 and 3,000 by 2010 with an investment of Rs. 5 billion by 2009. Subhiksha recently launched exclusive mobile stores and currently operates 145 such stores and sold 60,000 mobile sets in the month of June-07. Subhiksha also plans a foray into internet retailing and plans to launch the website by 2008.

Microsoft launched its first shop-in-shop pilot with Tata Group firm Infiniti Retail’s multi-brand consumer durables retail format - Croma. In January this year, Croma announced its entry into North India with its outlet in Delhi.

Apple Inc entered into an exclusive marketing and distribution deal with Reliance Retail through “iStore by Reliance Digital”. Pioneer of organised retail in India, Kishore Biyani’s Future Group carried on with its expansion plans aiming a revenue of Rs 30,000 crore (US$7.6 billion) by 2010.

With increase in the number of broadband and dial-up internet connections, limited personal time for shopping, increased use of plastic money and large base of young population that spends a considerable time online, there has been a tremendous boost in e-tailing – the online version of retail shopping. Most retailers are developing and maintaining their own online sale portals for easy consumer access, facilitating online purchase of merchandise. Tata

Retail Sector Valuations:Company Market

PriceMarket

Cap (Rs. Crs)

Trent Ltd 515.15 1004.54Pantaloon Retail India Ltd 337 4947.16Shopper’s Stop Ltd 299.5 1045.26Vishal Retail Ltd 389.8 873.15Koutons Retail India Ltd 801 2451.06Raymond Ltd 193 1185.02Archies Ltd 123.6 84.05Indiabulls Retail Services Ltd 73.25 146.5Bata India Ltd 166 1067.38Celebrity Fashions Ltd 25.6 45.57Liberty Shoes Ltd 69.4 117.98

7_4_JAI SUBRAMANIAM.indd 3677_4_JAI SUBRAMANIAM.indd 367 9/13/2008 12:27:02 AM9/13/2008 12:27:02 AM

INDIA RETAIL REPORT 2009368

Indicom’s i-choose.in and G&B’s godrejlifespace.com are good examples of this trend. Players like Rediff.com, eBay.in, Indiatimes.com were some of the early entrants in the Indian online retail space, clocking impressive revenues through online transactions. Some of the more recent players to enter this niche market include Pantaloons Retail India Ltd., through its Futurebazaar.com venture. Many smaller retail portals are also thriving on the internet, meeting the niche Indian consumer requirements such as ethnic apparel, handicrafts and jewellery. With value-added services like cash-on-delivery to facilitate online transactions by consumers without credit/debit card, unique bidding schemes etc, e-commerce is fast gaining acceptance in India. An estimated 10 per cent of the total e-commerce market is accounted by e-tailing. According to the Indian Marketing Research Bureau (IMRB) and Internet and Mobile Association of India (IAMAI), the e-tail market is estimated to grow by 30 per cent to US$ 273.02 million in 2007-08, from US$ 210.01 million in 2006-07.

India’s gems and jewellery industry has been allowed 51 per cent foreign direct investments by the government in single brand retail stores attracting both global and domestic players to this sector. By 2013, India is expected to become the biggest consumer of jewellery. In the recent years a large number of players like Reliance Retail, Damas India, Swarovski, The Gitanjali Group and Dubai based Joy Alukkas have been attracted to the Indian gems

and jewellery retail sector: Mumbai-based Vardhaman Developers plans to build four more jewellery malls in the city and is already set to launch Jewel World, Mumbai’s first jewellery mall. Gold Souk India plans to set up 100 Souks in 100 months

The government’s decision to allow 100 per cent FDI in the emerging apparel industry has led to an increase in the investment inflows into the sector. The domestic textiles and apparels market in India is witnessing strong growth owing to a young population, an increase in disposable incomes and a rapid growth in organised retail which has fuelled the growth of the textiles market and is estimated to grow at the rate of 12-15 per cent annually. Riding on the back of high aspiration value, strong branding and high margins, international brands in India like Giordano, Gas, Tommy and Esprit have already got off to a good, early start.

With an impressive conversion ratio

across malls, the market trend promises a positive outlook for the future. Mall development activity is being pursued aggressively across all the metros and the high-growth cities, with significant investments in the pipeline. The total mall space across seven cities (NCR, Mumbai, Bangalore, Kolkatta Hyderabad, Pune and Chennai), was spread over 40 million square feet in 2006-07. Mall space is projected to increase to over 60 million square feet in 2007-08.

Entertainment retail is redefining Indian lifestyles with the rate of growth in the number of multiplexes and gaming zones matching the growth story of malls and retail space. The immense potential in the entertainment and leisure segment is reflected by fact that there exist 10 screens per million of population in India as compared to 40 screens in the European market and 117 in the US. Reliance Infotech’s Adlabs and Shoppers Stop’s Timezone have aggressive expansion plans in the pipeline, with retailers exploring the joint venture option with international giants in the sector having a global presence. The top multiplex chains, including DLF, Adlabs, PVR and Cineplex have plans of adding 300-500 screens each by FY-10.

The Indian health and wellness market, estimated at US$ 4.6 billion, is booming with a year-on-year growth

Riding on the back of high aspiration value, strong branding and high margins,

international brands in India like Giordano, Gas, Tommy and Esprit have already got off

to a good, early start.

7_4_JAI SUBRAMANIAM.indd 3687_4_JAI SUBRAMANIAM.indd 368 9/13/2008 12:27:08 AM9/13/2008 12:27:08 AM

RETAIL SUPPORT Investments in Retail

INDIA RETAIL REPORT 2009 369

of over 25 per cent. Thanks to rising awareness and growing consciousness among urban Indians, there is a big niche for products that can enable freedom from stress, and the ill-effects of a sedentary lifestyle. FMCG major Dabur has set up a subsidiary – H&B Stores – to run its ‘New U’ branded stores with an initial investment of Rs 140 crore (US$35 million) for opening retail stores across the country to sell products in the health and beauty segment. Retail giants like Reliance Retail and the Birla group are also joining hands with wellness experts.

With consumers for luxury goods more in numbers than adult populations of several countries, the Indian luxury retail market is estimated to leap-frog from around US$ 3.5 billion to US$ 30 billion by 2015. The luxury retail segment is a substantial opportunity for retail industry players. Many international investors are actively pursuing an entry route into India for opportunities in the luxury segment. Currently, the location of these outlets is primarily limited to five-star hotel mall spaces, with limited footfalls and consumer exposure. Industry players have aggressive expansion plans in the pipeline, with investor confidence reinforced by the booming sales in the luxury segment. Some of the international luxury retailing brands in India are Louis Vuitton, BVLGARI, Gucci, Hugo Boss, Florsheim, etc.

Innovative formats like the Wedding Malls for instance, stock the complete range of wedding product offerings from

apparel to jewellery. The retail industry players are successfully blending knowledge from the experiences of the global retail industry with the unique requirements and preferences of the Indian consumer. Khadi & Village Industries Commission is set to roll out a string of swanky “Khadi Plazas”, which would showcase the traditional handloom textiles in a completely new form. Over 7,000 existing outlets are to be beefed up to cater to the changing tastes of the young Indian consumer and thereby provide a boost to the presently stagnant sales of the khadi textiles. The latest addition to the list of diverse retail formats are the “Village Malls”, with the fair price shops being revamped to cater to the larger needs of local populations. The Government of Gujarat has spearheaded one such initiative with 512 “Village malls” launched in the state with further plans for 508 such malls.

Rural hypermarkets are growing at a blistering pace meeting the unique requirements of the rural consumer. The range of services provided by the rural retailers extends from creating a platform to buy and sell farm produce, to banking services, to restaurants etc. One of the key players in the rural retail segment is ITC with its Choupal Sagar initiative. ITC has 14 outlets in operation presently and plans to increase the number to 700 over the next 7-10 years. Other players include DSCL’s Hariyali Kisan Bazaar and Indian Oil Corporation’s Kisan Seva Kendra.

DSCL’s Hariyali Kisan Bazaar has over 70 outlets currently and the company proposes to operate a total of 200 outlets over the next 12 months. Indian Oil Corporation’s Kisan Seva Kendra offerings extend over fuel, agri-produce, fast moving consumer goods and other value added services, and has a network of over 1,400 outlets currently. Reliance Retail and Pantaloon Retail India Ltd. are expected to undertake more ventures to capture the vast untapped potential in the rural retail segment.

FDI can supplement and complement the Indian industry and make it globally competitive, open up export markets and provide access to international quality goods and services. It can raise resources through technological up gradation, optimal utilisation of human and natural resources, and backward and forward linkages. And as the Government is in a process to initiate a second phase of reforms, it is cautiously exploring the avenues for multi-brand segment. The Government is seeking these options keeping in view the existing social framework of India and will ensure that the entry of global retail giants do not displace the existing employment in the retail business.

Looking back, the sector faced quite a few hurdles in the last year, such as the controversy over the involvement of foreign direct investors (FDI) in multi-brand retail and a nationwide protest by small traders against the big retailers. ■

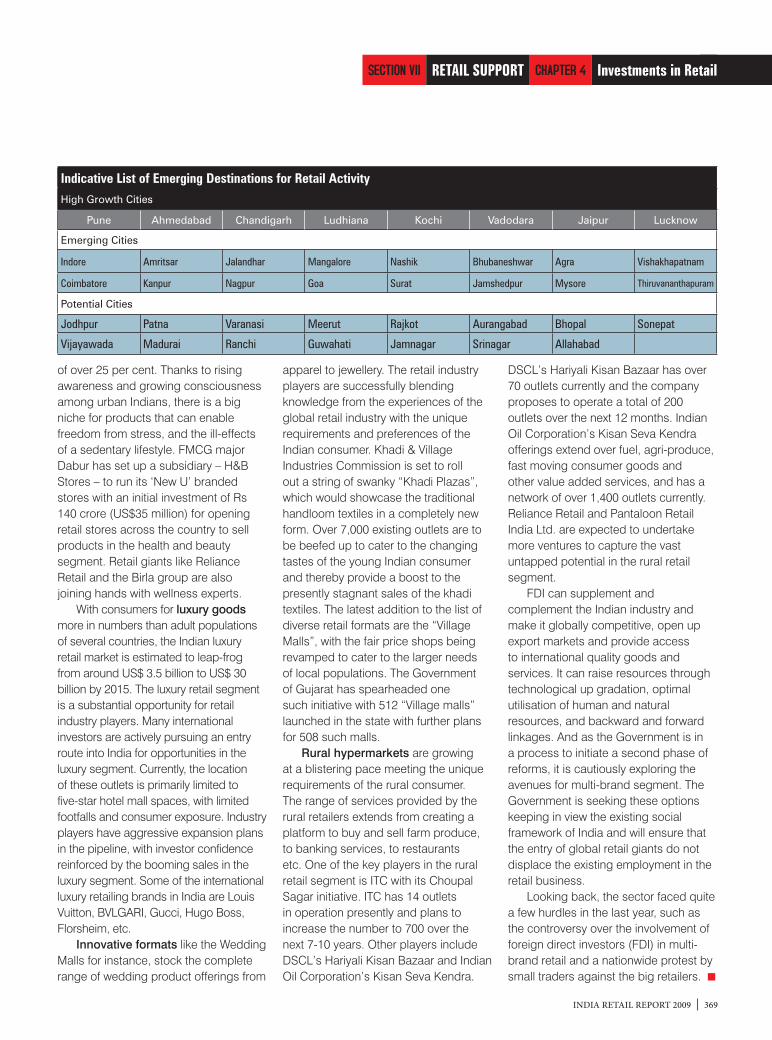

Indicative List of Emerging Destinations for Retail Activity

High Growth Cities

Pune Ahmedabad Chandigarh Ludhiana Kochi Vadodara Jaipur Lucknow

Emerging Cities

Indore Amritsar Jalandhar Mangalore Nashik Bhubaneshwar Agra Vishakhapatnam

Coimbatore Kanpur Nagpur Goa Surat Jamshedpur Mysore Thiruvananthapuram

Potential Cities

Jodhpur Patna Varanasi Meerut Rajkot Aurangabad Bhopal Sonepat

Vijayawada Madurai Ranchi Guwahati Jamnagar Srinagar Allahabad

7_4_JAI SUBRAMANIAM.indd 3697_4_JAI SUBRAMANIAM.indd 369 9/13/2008 12:27:13 AM9/13/2008 12:27:13 AM

INVESTING IN THE NEW-WORLD RETAIL ECONOMY – INDIA

By Srinath Sridharan

7_4_SRINATH SRIDHARAN.indd 3707_4_SRINATH SRIDHARAN.indd 370 9/13/2008 12:28:50 AM9/13/2008 12:28:50 AM

INDIA RETAIL REPORT 2009 371

RETAIL SUPPORT Investments In Retail

aspect of any industry’s growth: non-financial aspects including — people, systems, training, infrastructure — which ensure that an all-inclusive growth is achieved rather than just financial growth.

There’s a sense of renewed confidence amongst the Indian business houses, short-time economic slow-down or rather its expectations, included. This confidence stems from the fact that as a country, we have faced tough times together, grown stronger by the years and this confidence to take on the world is here to stay. Call it youthful aggression balanced with wisdom of the mature nation that we are.

FINANCIAL INVESTMENTS IN RETAIL

Investment ScenarioIndia is in the top three of the

AT Kearney’s annual Global Retail

Retail, as an official industry in India, has emerged as one of the most dynamic sunrise sectors in the country and is here to

stay! India is indeed a market that the world would look at and many would want a share-of-the-pie. As the economy grows, so would India’s middle class. With ever changing consumer behaviour of a market where world’s one-sixth population lives, talking over 1,000 languages and dialects, practicing many religions with belief in various customs and traditions, to claim that “we understand the Indian consumer”, would be a real tall-claim for years to come.

INVESTMENTS IN RETAILMost of the Nay-sayers or critics of

the Indian retail industry have been talking of the investments into the industry. But, they have been talking only of the financial investments. But to be balanced in argument, they miss the important

Though consumer behaviour might differ with geography, it is but natural for us humans to have ‘wants’ and ‘needs’. Hence to me, the Indian brethren across so-called urban vs rural divide are treated as first-among-equals in the consumerism space.

Development Index (GRDI) for the third consecutive year, maintaining its position as the most attractive market for retail investment. Furthermore, a report by Pricewaterhouse Coopers foresees India and China to continue as the top sourcing hubs in retail and consumer sector in the coming years.

Continuing the robust growth of the organised retail in India, according to the Credit Rating and Information Services of India, the industry raked in US$ 25.44 billion turnover in 2007-08 as against US$ 16.99 billion in 2006-07, a whopping growth rate of 49.73 per cent.

Top dollars are today being pumped into the retail sector by both Indian and international retailers alike.

INVESTMENT ROUTESInvestments in the retail industry are

pouring in various forms of the business. The major routes of investments seem to be the licensing or the franchisee route. Though few brands have started entering India through the FDI approved route, the wait is just getting interestingi’.

iMany brands when they filed for FDI permissions to enter India, had assumed certain financials/cost parameters in their business plans. Either by coincidence or sheer passage of time, when they received the FDI approvals, the real estate prices & employee costs had shot up much higher than their original business plans. And also the non-availability of the ‘right’ real estate zoning for certain types of businesses, meant that they use surrogate real estate space, which does not necessarily guarantee consumer walk-ins.

7_4_SRINATH SRIDHARAN.indd 3717_4_SRINATH SRIDHARAN.indd 371 9/13/2008 12:29:24 AM9/13/2008 12:29:24 AM

INDIA RETAIL REPORT 2009372

While multi-brand retailing remained out of bounds for overseas firms, a number of foreign luxury brands lined up for permission to enter through the single-brand retail window. Few brands have also entered through the back-end service agreement contracts.

Lets look at the scope of financial investments at length, before we discuss the non-financial investments into the industry.

FDI IN RETAIL & REGULATIONSThe most often used word or phrase

in the retail industry. Sounds very similar to the word ‘strategy’ that management folks use!

With the opening up of the Indian economy in the early 1990s, the retail industry seems to be benefitted. Though entry barriers do exist, India has witnessed a flurry of investments made by international retailers through various means within the regulatory framework.

FDI (Foreign Direct Investment) under ●

the ‘automatic’ route in a majority of the sectors requires no specific government approval but requires prescribed filings with the RBI.I00% FDI under the automatic route ●

is allowed in wholesale cash and carry, power trading, trading in exports, and with prior approval, in trading of items sourced from Small Scale Industries (SSI). ‘Single Brand’ product retailing can ●

avail of FDI upto 51 per cent with prior approval from the Foreign Investment Promotion Board (FIPB)/Secretariat for Industrial Assistance (SIA) under the conditions that the

product sold is a ‘single’ brand. It has to be ensured that a product is branded, while it is being manufactured and has to be sold under the same brand name it holds, in the international market. FDI in multi-brand retailing is ●

completely prohibited.Besides, the franchise route is ●

available for big operators.

FOREIGN TECHNOLOGY AGREEMENTS

Acquisition of foreign technology is permitted either through the automatic route or with prior Government approval. Payment for foreign technology collaboration by Indian companies is allowed under the automatic route subject to the following limits:

Lump sum payments not exceeding ●

US$2 millionRoyalty payable being limited to 5 ●

per cent for domestic sales and 8 per cent for exports, without any restriction on the duration of the royalty payments ii

CONSULTANCY FEES AND USAGE OF TRADEMARKS AND BRAND NAME

In the case of non-transfer of technology, the trademarks and brand name of the foreign collaborator are allowed to be used upon payment of a 2 per cent royalty for exports and 1 per cent for domestic sales. Payment for architectural/consultancy services,

procured from abroad, is permitted upto US$1 million per project and US$10 million for infrastructure projects.

SERVICE TAXRetail industry is not able to avail

CENVAT credit of service tax paid on input services. Service tax charged by a service provider to another service provider can generally be set off against the output service tax liability, subject to applicable conditions. A retailer, however, is not a service provider but is primarily involved in the sale of goods to the consumer. Accordingly, the retailer would not be able to utilise the credit of service tax paid on the input services consumed by them and would have to bear the additional cost. This is likely to impact profitability for retailers or raise costs for consumers.

INDIRECT TAXESThe levels of indirect taxes in India

are amongst the highest in the world. Coupled with this, the compliance requirements are very rigorous and any gap in the same can result in significant exposure, which in many cases surface long after the transaction is made.

The framework concerning levy of indirect taxes especially in respect of Sales Tax/ VAT, Central Sales Tax (CST) and Service Tax and compliance thereof, is further evolving, resulting in compliance risks as well as emerging opportunities, as the experts might tell us.

CUSTOMS DUTYCustoms duty is levied as a

percentage of the value of the goods imported into India. The duties are calculated according to the Customs

iiAll the rates & figures mentioned in the taxation / royalty structures are figures as mandated at the time of printing

While multi-brand retailing remained out of bounds for overseas firms, a number

of foreign luxury brands lined up for permission to enter through the single-

brand retail window.

7_4_SRINATH SRIDHARAN.indd 3727_4_SRINATH SRIDHARAN.indd 372 9/13/2008 12:29:33 AM9/13/2008 12:29:33 AM

INDIA RETAIL REPORT 2009 373

RETAIL SUPPORT Investments In Retail

Tariff Act, 1975 (CTA). The customs duty rate is 34.13 per cent in India, which is low as compared to other countries in the region.

Import duties in other nearby Asian countries where organised retail penetration is high, are:

China-0% to 270% ●

Vietnam- 0% to 60% ●

Indonesia - 0% to 170% ●

Thailand - 5% to 60% ●

This ensures a cost-effective entry for all imported goods into India and helps retailers maintain their profit margins on importing specific products.

Though the other side of the argument is that the import duty of 34.13 per cent is still high as a stand-alone factor for the growing organised

retail market. This compounded with other cost factors can make certain businesses like luxury industry highly restricted & scare away the consumer or the retailer or both!

FOREIGN TRADE POLICY & EPCGThe various export promotion

schemes under the country’s foreign trade policy benefit the retail sector. These schemes are supported by corresponding exemption notifications under the Customs and Excise laws.

The Export Promotion of Capital Goods (EPCG) scheme allows 5 per cent customs duty on capital goods at pre-production, production and post-production levels, provided an export obligation equivalent to eight times of

duty saved to be fulfilled in eight years is met, and the retailer has a minimum area of 1,000 sq meters.

The EPCG scheme requires a retailer to fulfill the condition of export obligation of eight times of duty saved in eight years.

Retailers are the final link between the manufacturer and the ultimate consumers, and with few exceptions, most consumers would be from India. In such cases, fulfillment of export obligations can be a concern in terms of goods not crossing the geographic boundaries of India.

Until April 2007, there was a provision under EPCG scheme to the effect that payments received against counter sales in free foreign exchange through banking channels, as per the Reserve Bank of India (RBI) guidelines, shall be counted for fulfillment of export obligations. This provision has, however, been deleted under the Annual Supplement 2007-08. Given this, fulfillment of export obligation can only be achieved by physical exports by group companies.

SERVICE TAXUnder the Finance Act 1994, the

central government is empowered to notify certain services as liable to the levy of Service Tax. At present, 107 service categories have been specified as taxable in India.

The service tax rate applicable is 12.36 per cent (12 per cent basic rate and 3 per cent education cess on the basic rate). The tax is also imposed in a situation, wherein the consideration received for provision of services is partly or wholly not consisting of money.

Under the CENVAT credit rules, service tax charged by a service provider to a manufacturer or another service provider is generally available as credit to the manufacturer/receiving service provider, and such credit can be set off against the output liability of excise duty or service tax subject to applicable conditions.

7_4_SRINATH SRIDHARAN.indd 3737_4_SRINATH SRIDHARAN.indd 373 9/13/2008 12:29:34 AM9/13/2008 12:29:34 AM

INDIA RETAIL REPORT 2009374

VATVAT law in most states allows VAT

credit on goods purchased from a vendor within the state. However, credit of CST paid on purchase of goods from outside the state will not be available to the dealer. Accordingly, CST charged by the vendor would become an additional cost for the retailer!

VAT is applicable on sale of goods in all Indian states except Uttar Pradesh, which still operates under the old regime of sales tax. Sales tax/VAT is also applicable on the value of materials transferred in ‘works contract’ involving procurement of service and material. Typical VAT rates in India are 4 per cent and 12.5 per cent, depending on the product. Food grains being a daily necessity are exempted from VAT across all major Indian states. Readymade garments, edible oils and medicines are typically subject to 4 per cent VAT whereas footwear, furniture, watches and biscuits are typically subject to 12.5 per cent.

Conventionally in the organised retail industries, Central warehousing concept allows single point and efficient distribution to front-end retail stores or regional warehouses. However, in India, in case the central warehouse is located outside the state, stock transfer from the central warehouse to the warehouses/retail outlet outside the state shall warrant a retention (deduction) from the VAT paid on purchases (i.e. Input Tax Credit) within the state. The retention rate is 4 per cent of the purchase price.

Alternatively, central warehousing can be useful for foreign import or inter-state trade where credit is unavailable. Regional warehouse would be a better option from the perspective of credit availability and utilisation.

ENTRY TAXThis tax is applicable on entry of

goods into local area (typically, the area of a state). In the absence of credit of entry tax being available for setting off

against output VAT liability, entry tax paid would be an additional cost for the retailers.

CENTRAL SALES TAXA sale that involves the movement

of goods from one state to another is referred to as an inter-state sale and is governed by the Central Sales Tax Act, 1956 (CST Act).

Presently, for buyers such as retailers, inter-state purchases are either taxable at the rate applicable in the state of purchase or will be taxable at a rate in the range of 1 per cent to 3 per cent provided the retailers furnish declaration forms to the vendors. Also, no credit is available to the buyer on the CST paid on inter-state purchase.

GOODS & SERVICES TAXThe Government of India has decided

to introduce a unified Goods and Service Tax (GST) regime from fiscal 2010. The GST act would integrate state level VAT and service tax and phase out CST.

OTHER TAXESOctroi – levied on entry of goods ●

into the jurisdiction of a municipal corporation in a few states such as Maharashtra, Gujarat, PunjabProfession Tax – on the profession, ●

trade or calling of a person

NON-FINANCIAL INVESTMENTS

Wait or BaitTrue, the retail potential is huge

going by the numbers tabulated by research agencies and consultancies,

but amidst the frenzy, are we not missing out on a critical point? Is there adequate returns to millions of dollars been pumped in? What would be the Return on Investment (RoI)? When would pay-backs be achieved, if at all? When would industry talk openly about numbers and share it within themselves like players in the other evolved sectors? The previous decade (1990s) saw a frenzy of players in the Dotcom boom chasing ‘eye-balls’. Is this decade, the chase for ‘foot-falls’? Let’s look at some issues of the non-financial aspects of investments that are currently being done in the retail industry.

OPPORTUNITY TO EVOLVE INTO GLOBAL DESTINATION

Favourable demographic and psychographic changes in India’s consumer class coupled with global exposure that the consumer is being exposed to, along with the wider availability of products and brand communication, are some of the factors that are driving the retail in India.

Over the last few years, many international retailers have entered the Indian market on the strength of increasing affluence levels of the young Indian population along with the heightened awareness of global brands and with an expectation of international-class shopping experiences along with ease in availability of quality retail real estate space.

Read the above paragraph carefully again!

Is that a paradox? Has the Indian consumer opened up his/her purse

7_4_SRINATH SRIDHARAN.indd 3747_4_SRINATH SRIDHARAN.indd 374 9/13/2008 12:29:54 AM9/13/2008 12:29:54 AM

INDIA RETAIL REPORT 2009 375

RETAIL SUPPORT Investments In Retail

strings easily? Has the global brands awareness created the urge to shop for them in India? And, do we really have quality real estate in India, as we see globally? Or should we evolve an India-specific global model for retail real estate?

Questions & Questions – and there are more questions. There are no rights or wrong answers. It is for all of us associated with the retail industry to think, discuss, debate dispassionately and decide.

RETAILERS – THE EVOLVING TRIBE

The common belief is that retailers have clout that’s growing by the day and that the manufacturers in various related industries such as FMCG & consumer durables bowing down to it. There cannot be any less of a statement made that’s inappropriate.

The point is that the retailers are in short direct-to-consumer businesses and the clout is due to the fact that consumers are demanding high service levels of retail efficiency, which in turn they expect from their associates.

Look around the retailers’ associates – be it the packaging company or the bankers or the communication agencies or the real estate providers… The truth is that the entire value chains of partners work with each other to ensure highest levels of service delivery to the consumer. There can be many phrases or words that management service providers use to define these relationships; I would use the word “inter-dependency”. Each of us in the value chain need each other & we are better off with a good relationship than a poor one!

REAL ESTATE When the retailing boom began

and gathered pace, everyone, from developers to retailers to non retailers and even PE firms rushed to grab a piece of action. No body wanted to be left out in what can be called the El Dorado of the East. The rush is still taking place and even today, one reads and hears of another player jumping onto the retail brand wagon.

However the real picture is slowly getting unveiled. Although long term prospects are promising, there are challenges which players are coming to terms with.

Infrastructure, availability of prime locations is becoming a cause of concern. Delay in project completion is leading to huge overheads and inflating the already exorbitant input costs for retailers.

The constantly increasing interest rates have forced many a players, including the serious ones to have a relook at the feasibility or even the basic viability of their projects.

Retailing, particularly food and groceries is about volumes and volumes accrue when you have a sizeable network. And when retailers are not able to get deliveries of properties on time, revenue projections go awry. And as more and more players join the retail arena, the situation will become even grimmer.

Surely, there’s a shakeout in the making. Or if those who like the wordings prim & proper, ‘consolidation phase in the industry is in the making’. But the question is whether the non-serious players use prudence to

understand that enough is enough and this game is not for them. And will other players keep pumping money in the hope that turnaround is just round the corner?

At this point in time, there is not adequate retail-ready-real estate! Most of the me-too-malls seem to be cement-steel-glass structures rather than consumer-friendly retail-zoned developments. Of course, to be fair, there are good developers, who are thinking long-term and hence investing in consumer insights and developing their properties.

In general, many malls currently under construction might fail the retailers’ expectations & consumers’ interests in them. Are malls just free air-conditioned spaces or is it for creating an experience where retailers offer their services to the consumers profitably?

The ideal situation would be when Government, retailers, developers work together to ensure that it is a 3-way street with “win” for everyone. For example, government may need to work on its taxation structure and laws to ensure that developers can afford to give affordable real estate space to the retailers, which in turn would keep the prices affordable & attractive to the consumers.

The government in turn should bring in transparency in land documentation and ease of availability of information. Simplification of local laws would help in ease of transactions and also in the right pricing mechanism for the sellers.

The fact is organised retail is here to stay and grow; hence if it is self-moderated by the retail industry under the governance of the government, it can be profitable and all-inclusive for all sectors of the population.

INFRASTRUCTUREThe roadmap to fuelling the retail

story is dependent on how soon can we develop the necessary infrastructure comprising of roads, cold storages and

The constantly increasing interest rates have forced many a players, including

the serious ones to have a relook at the feasibility or even the basic viability of

their projects.

7_4_SRINATH SRIDHARAN.indd 3757_4_SRINATH SRIDHARAN.indd 375 9/13/2008 12:29:59 AM9/13/2008 12:29:59 AM

INDIA RETAIL REPORT 2009376

even cold chains, necessary for efficient retailing to function.

The debate all these while has been the entry of players into the front-end retail. The fact is there is a great opportunity in the back-end of retail and this sector has been open for investments including FDI since long. It is time that we look at this with interest and look at developments. As a model, we can look at adopting Private-Public sector joint participation in developing infrastructure.

Rules and regulations such as shops and establishments act, APMC act need to be made contemporary so that it acts as an enabler to retail’s growth. Given that each state has its own taxes and rules, which differ from one state to another, retailers have to grapple with multiple regulations. If a uniform policy is created, it will help improve efficiencies of the operations, which will give a fillip to retail expansion. The more the network spreads, leads to more employment opportunities.

Let’s remember that KISS works – Keep It Short & Simple, even for laws so that evasion is reduced. If the common man can understand his rights, he is empowered automatically and corruption drastically drops.

PEOPLE. FOR THE PEOPLE. Retail is an industry. And a highly

respectable one at that. It employs high volume of people and offers employability to countless number of those, who otherwise might not have had similar growth opportunities in alternate vocations.

Retailers are today working on the issues of talent sourcing, management and retention. Governments can work

hand-in-hand with private players to ensure retailing education and training becomes part of the curriculum. Talent can be absorbed by the retailers given their huge expansion plans across the country. Constant talent upgradation is also the need of the hour for existing retailers.

From the retail industry’s perspective, the industry has to evolve out of its straight-jacketed thinking to ensure above-board people practices including recruitment, grooming, training and career planning. Poaching within industry would need a re-look as it’s similar to the concept of in-fighting. The salary for the same talent that’s being poached is increasing and not necessarily overall volumes of talent. At certain management cadres, poaching could be a quick-solution but when looked at across cadres, it is not a sustainable practice.

We need to chalk out a clear career path highlighting the training and skill sets upgradation, which he or she will acquire in the job. Retailer industry has to work towards creating the industry as the ‘Best Employer Industry’. After all, happy employees ensure happy consumers!

CONSUMER BEHAVIOURWith industry with very little modern

retail penetration (the debate is where the word “organized retail” should be used vis-à-vis modern retail; modern retailers have not yet evolved to a stage where we know the consumers more than the traditional retailers; yes, the modern retail has brought in processes and systems that would facilitate better consumer and category management)

Over the next few years, consumers would be exposed to variety of experiments that the industry would attempt on them – this would mean that that both sides would learn and evolve; the science of consumer behavior could see metamorphosis and a change from the conventional way of shopping is

a given; new shopping habits, credit habits, credit products could emerge, as well. Given this scenario, it is too early for retail formats to be frozen as the correct one. And the question of consumer loyalty would be further questioned with emerging volume trends.

COMPETITION & COLLABORATIVE APPROACH

While one talks about public-private participation, it is also necessary for retailers and major vendors to come together and collaborate. From a situation of conflict, one should look at a consensus to look at ways of growing together. Best practices, learnings, information and data should be shared within the industry, which will be beneficial in growing modern trade in the country. Retailers and manufacturers have to come out of skepticism mindset and get into a partnership frame of mind. As the market evolves, intra-market collaborative approach between competitors might be the need-of-the-hour.

Let’s face this: Best practices, both in front-end and back-end are welcome and this marketplace is huge to accommodate large number of players. With increased competition & global standards, consumers would be the ultimate beneficiary.

In other words, industry needs to share data amongst themselves through an industry body and ensure that the industry speaks one voice!

TIME TO THINK BIG, STAND TALL AND WALK AHEAD

Note:1. Views expressed by the author are his

personal ones, formed with exposure to multiple consumer businesses;

2. All due credits are due to the industry exposure accorded by his employer Wadhawan Group and his interactions with consumers, colleagues & friends in the retail industry ■

Retailer industry has to work

towards creating the industry as the

‘Best Employer Industry’.

7_4_SRINATH SRIDHARAN.indd 3767_4_SRINATH SRIDHARAN.indd 376 9/13/2008 12:29:59 AM9/13/2008 12:29:59 AM

RETAIL RATING –THE MISSING PIECE OF

RETAIL INVESTMENTSBy Rajan Chhibba

7_4_RAJAN CHHIBBA.indd 3777_4_RAJAN CHHIBBA.indd 377 9/13/2008 12:27:58 AM9/13/2008 12:27:58 AM

INDIA RETAIL REPORT 2009378

by ineffective or inefficient working can have a far higher impact on performance than market volatility or political volatility or financial volatility. Retail rating therefore has two equally important elements

Operational rating ●

Financial rating ●

OPERATIONAL RATINGSustainable advantage in retail

fundamentally derives from key process costs of a store of a set of stores – e.g. cost of customer acquisitions; cost of sourcing; cost of customer retention – which unfortunately most retailers today fail to understand even themselves.

The first leg of operational rating is therefore the reassessment of a business based on process costs and then evaluating its real strengths. This implies that operational rating can only be done by people who understand activity based process costs and assess the retail business accordingly.

The other issue in retail is that even if the store is operationally great, is it really scalable? Retail chains need to be scalable to achieve materiality. The question is how scalable is a profitable store? This is again an assessment that requires expertise to identify what really is scalable. For example, a coffee chain

We, therefore, have the situation investors looking for projects and projects looking for investors, but the

twain never meet.

RETAIL RATINGS – THE MISSING PIECE

One key reason for this situation is that models for rating a retail operation do not exist. As a result, neither the retailers themselves nor the investment community is able to get comfortable with the projects presented to them.

Ratings in the manufacturing sector are normally assessments of the risk carried by a business. The risks are mainly identified based on market risks, political risks and financial capacity risks. This is because manufacturing is largely impacted by these factors, which may impact business performance more than expected.

Retail is an operational business where the operating risk – driven

Investment in any business is driven by the investor’s formal or informal rating of the company. Retail is no different. Over the last few years billions of precious dollars have been committed to the growth of the retail sector and yet very few projects have actually been funded on the back of strong business models. They have been funded largely on the back of strong groups backing them.

may have no scalability element other than a common brand name. This will get a good rating if there is appropriate brand investment planned; otherwise, this chain will get a poor rating on scalability.

To sum up, operational rating assesses both process cost risks and scalability risks.

FINANCIAL RATINGFinancial rating follows the more

classical model of assessing financial capacity risks of the promoter and the venture. However, in the retail environment, these not only include leveraging but also real estate costs, staff cost trends, fashion index of business.

The key question is – can these assessments be done? The answer fortunately is, yes. We at Intrim have studied hundreds of retail operations from the humble roadside kiosks to large chains and developed models to assess these risks. What does it take? Fortunately, not a lot of time, but more a willingness of the retail management to share information. The best part of the exercise is that the rating not only helps in building investor confidence but also helps management focus and improve itself. ■

RETAIL SUPPORT Investments in Retail

7_4_RAJAN CHHIBBA.indd 3787_4_RAJAN CHHIBBA.indd 378 9/13/2008 12:28:03 AM9/13/2008 12:28:03 AM

REAL ESTATE MUTUAL FUNDS AND MALLS IN INDIA

By Vivek Dahiya

7_4_DTZ.indd 3797_4_DTZ.indd 379 9/13/2008 12:25:38 AM9/13/2008 12:25:38 AM

INDIA RETAIL REPORT 2009380

Many of the suggestions below would also be applicable to larger retailers who are open to acquiring real estate and undertake development as per their own specifications.

PART I: DEVELOPERS’ FOCUSIn case a developer is constructing

a mall or exiting a current one, some of the key points they should consider are elaborated here. These would also be partly applicable to retailers who are part/ full owners of real estate they operate in. 1. Retain ownership: Funding options

have increased over the past decade and even though credit is expensive currently, the temptation of sale to investors and reducing break even period needs to be controlled. A well-planned, located and executed mall project has very high chance of success which can attract FDI (wherever applicable) and exit should be made once lease commitments have been done.

2. Employ mall managers: Many professional agencies are now offering this service and aim at not only facility management but entire

Retailers and mall developers in India have adapted very quickly in the past few years. Both have learnt from their

own, each other’s and industry peers’ mistakes. Introduction of real estate mutual funds provides an opportunity for new funding sources and learning for all stakeholders of the industry. This article provides a few suggestions that developers and investors should consider while undertaking future mall developments.

We are going to witness a new phase in real estate industry once the real estate mutual funds (REMF) start investment in earnest. However are there enough products to evaluate and invest in? Most of the malls that have come up since the ‘90s have multiple owners. The strata-title ownership structure in malls reduces chances of future success of the mall/ retailers and also disqualifies it from being an investment grade project.

business of running the mall. The mall owner should work with the mall manager to (a) increase footfall (b) improve purchase levels and (c) maintain/ improve asset quality. All these points will not only benefit the retailers, but will also attract second-round investors.

3. Buy back to increase holding: In cases a developer is in last stages of construction and has already sold a significant part of the project, they can still make the project attractive for REMFs. Even if the mall developer owns 60%-70% of the project he can still make it attractive to a fund who would want to diversify its asset class and reduce risks. The project could have been sold to individual investors at a rate lower than what it currently commands and buying back would mean excess outflow, but disposal to a fund would allow single ownership to remain and asset value to appreciate in the long run.

4. Improve construction quality: Internationally a typical real estate project is given a 30 year investment life and during that time significant

7_4_DTZ.indd 3807_4_DTZ.indd 380 9/13/2008 12:25:42 AM9/13/2008 12:25:42 AM

RETAIL SUPPORT Investments in Retail

INDIA RETAIL REPORT 2009 381

improvements could be taken up every 10 years. Unfortunately, most real estate projects in India start showing age in the first 10 years itself. It is, hence, important to invest more on construction quality. This is not limited to construction material but also to employing skilled manpower which greatly impacts the finishing levels in each project.

5. Don’t treat mall as a real estate product only: This is perhaps the biggest learning that developers in India need to go through. A developer’s interest and involvement in most other real estate project reduces once it’s completed, however it needs to continue in a mall. In a residential and commercial project maintenance is the prime concern; in a mall continued shopper interest should be prime focus. Many of the above points can

even be used by retailers in their due diligence of mall projects.

PART II: INVESTORS’ STRATEGIES

When an investor looks at a retail development, factors to evaluate are different from a regular real estate project. Manager of REMFs should consider the following:1. Identify at early stages: It has

been noticed in mall developments in India that anchor commitments happen at a very early stage and in most successful projects have over 70% occupancy during launch. So investment discussions can take place with developers during mid construction stage itself. This way the asset need not witness divestment in pre-construction stage which is a pre condition for all FDI.

2. Long-term commitment: Retailers could look at longer term commitment in case of projects which meet all pre-conditions of a professionally planned and managed development. This could be negotiated with both the developers and retailers at an early stage of project planning.

3. Understand retail business models: Each type of retail module has its specific requirement. Cash and carry, discount stores, department stores, hypermarkets, supermarkets etc. – all have a very different business models and real estate requirements. All of these

would have to be understood in detail by investors to determine valuation of a retail project.

4. Promote retail rent structures: It can be expected that going forward many of the retail leases in malls would be signed not as a plain vanilla structures but either with revenue sharing or minimum guarantee models. These would also have an impact on valuation technique for retail malls. A retailer should also be willing to act as a partner in the process of attracting investment for the mall project.

5. Invest in future: A much higher figure needs to be kept aside each year, every three and ten years to plough back into the project. This could be for annual marketing activities, repositioning keeping in mind the market developments and improving infrastructure respectively. To summarise the above thoughts,

REMFs provide a unique opportunity to the retail industry to undertake the next round of significant improvement and change in malls of India. ■

It can be expected that going forward many of the retail leases in malls would be signed

not as a plain vanilla structures but either with revenue sharing or minimum guarantee models.

7_4_DTZ.indd 3817_4_DTZ.indd 381 9/13/2008 12:25:45 AM9/13/2008 12:25:45 AM

Blank.indd 1Blank.indd 1 9/13/2008 2:11:01 AM9/13/2008 2:11:01 AM