Intro to Financial Reports PPT

68

Introduction to Financial Reports 1 Welcome! We will begin promptly at 9 a.m. Make sure your first and last name displays in the “Participant” list so we can mark your attendance. Training materials: https://go.iu.edu/handouts

Transcript of Intro to Financial Reports PPT

Introduction to Financial Reports

1

Welcome! We will begin promptly at 9 a.m. Make sure your first and last name displays in the

“Participant” list so we can mark your attendance.

Training materials: https://go.iu.edu/handouts

Introduction to Financial ReportsVPCFO TRAINING & COMMUNICATIONS

Agenda Accounting review. Financial reports vocabulary. 5-minute break. Activity 1. Org reversion and consolidation hierarchies. Financial reporting options at IU. Activity 2.

3

Learning objectives Apply report-related terminology to the

interpretation of a simple financial report. Identify the three environments in which financial

reports can be run at IU. Describe the similarities and differences between

KFS Balance Inquiries, IUIE reports, and the Controller’s Office Reporting Tools.

4

Accounting review

5

What is the purpose of accounting? The organization of financial data (income,

expenses, assets, and liabilities). The organization of financial data allows us to

effectively manage our organization.

6

What is the Chart of Accounts (COA)? The COA provides structure for all accounting,

reporting, and budgeting at IU. The structure is built using chart codes,

responsibility centers, organizations, accounts, object codes, and other COA components.

7

If IU’s financial system was a building, the COA would be the building’s blueprints.

What are chart codes? IU is broken up into different “charts” at campus

and auxiliary levels.

8

IU

UA BL

BA

IN

IA

EA KO NW SE SB

If IU’s financial system was a building, each chart code would be a room in the building.

What are fund groups? Accounts that are grouped by category based on

shared activity or objective.

9

Account prefix Fund group Details

03-19 General Fund Expense-driven, base-budgeted accounts used for daily operating expenses (e.g., office supplies, payroll, etc.). Each chart has its own general fund account prefix.

11, 20-24 Designated Fund

Funds set aside by the university for a specific purpose or function. Examples: Continuing Education, Public Service, and Faculty Research.

25-29 Restricted Funds Funds provided from an external source, often as a gift, with restrictions on how the funds may be used.

If IU’s financial system was a building, fund groups would be the file cabinets in each room.

What are accounts? Identify a pool of funds assigned to a specific IU

organizational entity for a specific purpose. Store information about financial transactions –

they tell us who and for what purpose.

10

If IU’s financial system was a building, accounts would be the drawers in the file cabinets.

What are object codes? Categorizations that tell us about the nature of

each transaction (income, expense, asset, liability, or fund balance).

Tells us what kind of transaction is being made.

11

Prefix Object code

0 or 1 Income2 or 3 Salaries and Wages4 or 5 General Expense56 or 57 Benefits6 Employee Travel (non-employee travel: 4089)

What is the General Ledger (GL)? The official repository of IU’s financial and budget

information. Stores detailed records of all financial

transactions. When an e-doc reaches final status, it is recorded

to the GL and affects balances. The basis for IU’s financial reports.

12

Financial reports vocabulary

13

What is a financial report? How we retrieve data about IU’s financial activity.o Transactions are generated in e-docs.o Transaction data is saved to the General Ledger.o Financial reports extract data from the General Ledger.

14

General Ledger

E-Doc ReportTransaction Data

Financial decision cycle

15

General Ledger

ReportE-doc

Financial reports are used to: Assess current financial situations. Make decisions about future transactions. Identify financial trends. Make sure that past transactions were in

compliance with IU policy. Communicate IU’s financial position to interested

parties.

16

Vocabulary terms Budget. Base budget. Current budget. Actuals. Encumbrances. Variance.

17

Budget A budget is a plan for how resources will be used. Budgets are built using object codes.o Each object code is a budget line in an account.

Two kinds of budgets:o Base.o Current.

18

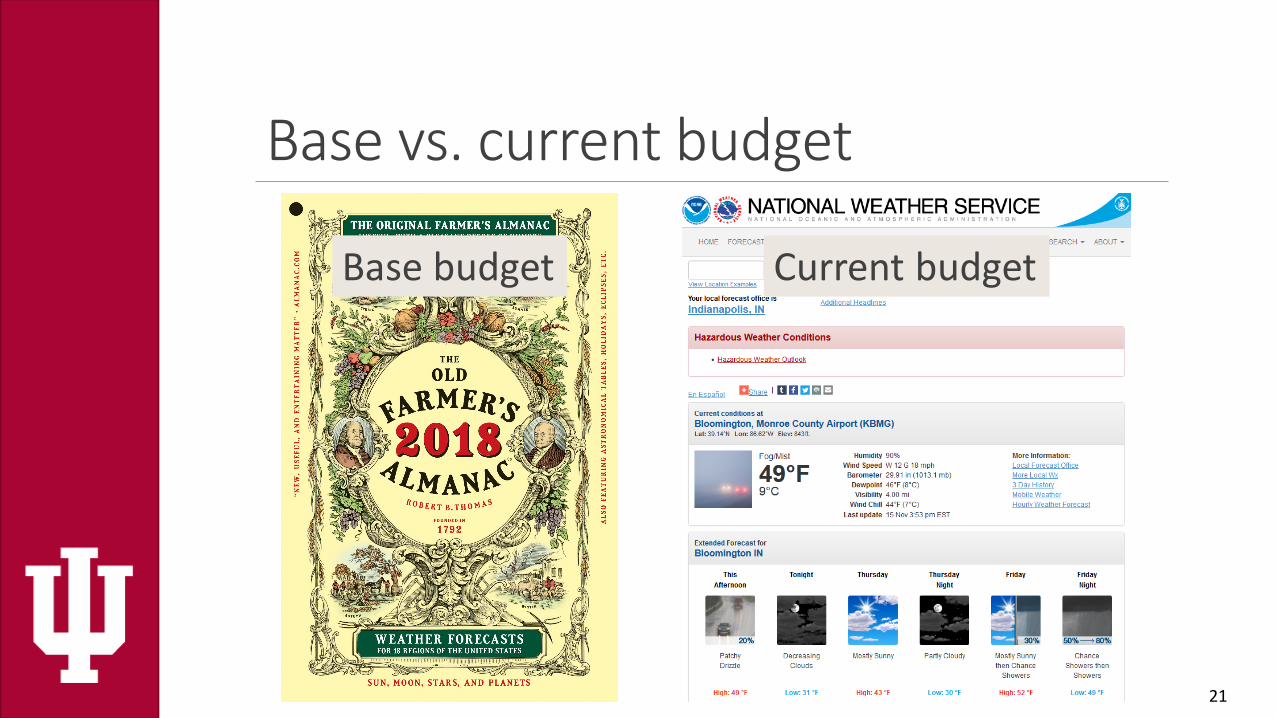

Base budget Account’s foundation amount that is created and

guaranteed annually for a unit by the RC or the campus.

Based on historical performance and future plans. Designates an ongoing fiscal commitment. General Fund accounts are base-budgeted.o The authority to spend is based on the budget, not cash.

19

Current budget A plan for the resources a unit has to work with

during the fiscal year. A temporary budget that only applies to the fiscal

year and is based on real-time events. All accounts, including General Fund accounts,

have a current budget. At the start of the fiscal year, the base budget and

current budget will be the same.

20

Base vs. current budget

21

Base budget Current budget

Example: current budget

22

ObjectCode

Object CodeName

Current BudgetAmount

1523 Equipment Sales 1,000.00

2400 Professional Salaries 60,000.00

4100 Office Supplies 1,500.00

4035 Laboratory Supplies 10,000.00

6100 Out of State Travel 3,500.00

Actuals The total of all actual activity for a given balance

line of the selected fiscal year. Only transactions that have posted to the General

Ledger are included in the Actuals calculation.

23

Base vs. current budget vs. actuals

24

Base budget Current budgetActuals

Example: actuals

25

ObjectCode

Object CodeName

Current BudgetAmount

ActualsAmount

1523 Equipment Sales 1,000.00 900.00

2400 Professional Salaries 60,000.00 10,500.00

4100 Office Supplies 1,500.00 250.00

4035 Laboratory Supplies 10,000.00 9,000.00

6100 Out of State Travel 3,500.00 0.00

Encumbrances An amount set aside to cover a future anticipated

expense. Allow us to have a more accurate picture of funds

remaining on an object code. Different types of encumbrances represent

different types of expenses.

26

Types of encumbrances External Encumbrance (EX)o Anticipated disbursement of funds to an entity outside

IU.

Internal Encumbrance (IE)o Anticipated disbursement of funds to an entity inside IU.

Pre-Encumbrance (PE)o Encumbrance is manually placed on an account.o Must also be manually removed.

27

Example: encumbrances

28

ObjectCode

Object CodeName

Current BudgetAmount

ActualsAmount

EncumbranceAmount

1523 Equipment Sales 1,000.00 900.00 0.00

2400 Professional Salaries 60,000.00 10,500.00 49,500.00

4100 Office Supplies 1,500.00 250.00 50.00

4035 Laboratory Supplies 10,000.00 9,000.00 0.00

6100 Out of State Travel 3,500.00 0.00 5,500.00

Variance The amount of funds remaining for the rest of the

fiscal year.o For income: what we expect to earn.o For expense: what we have left to spend.

Variance is calculated differently depending on the object type code (income/expense).

29

Calculating expense varianceEquation

Current Budget– Actuals– Encumbrance

Variance

Office supplies (4100)

1,500.00– 250.00– 50.00

1,200 variance

30

Calculating income varianceEquation

Actuals– Current Budget

Variance

Equipment sales (1523)

900.00– 1,000.00

(100.00) variance

31

Example: variance

32

ObjectCode

Object CodeName

Current BudgetAmount

ActualsAmount

EncumbranceAmount Variance

1523 Equipment Sales 1,000.00 900.00 0.00 (100.00)

2400 Professional Salaries 60,000.00 10,500.00 49,500.00 0.00

4100 Office Supplies 1,500.00 250.00 50.00 1,200.00

4035 Laboratory Supplies 10,000.00 9,000.00 0.00 1,000.00

6100 Out of State Travel 3,500.00 0.00 5,500.00 (2,000.00)

Where does my account stand?

33

ObjectCode

Object CodeName

Current BudgetAmount

ActualsAmount

EncumbranceAmount Variance

1523 Equipment Sales 1,000.00 900.00 0.00 (100.00)

Income 1,000.00 900.00 0.00 (100.00)

ObjectCode

Object CodeName

Current BudgetAmount

ActualsAmount

EncumbranceAmount Variance

2400 Professional Salaries 60,000.00 10,500.00 49,500.00 0.00

4100 Office Supplies 1,500.00 250.00 50.00 1,200.00

4035 Laboratory Supplies 10,000.00 9,000.00 0.00 1,000.00

6100 Out of State Travel 3,500.00 0.00 5,500.00 (2,000.00)

Expense 75,000.00 19,750.00 55,050.00 200.00

Variance vs. balanceVariance

Describes a budgeted line item.

Used with budgeted and cash accounts.

Balance Describes an account

as a whole. Used with cash

accounts. Equal to cash on hand,

less encumbrances and payables.

34

35

Break

Activity 1REPORT INTERPRETATION

36

37

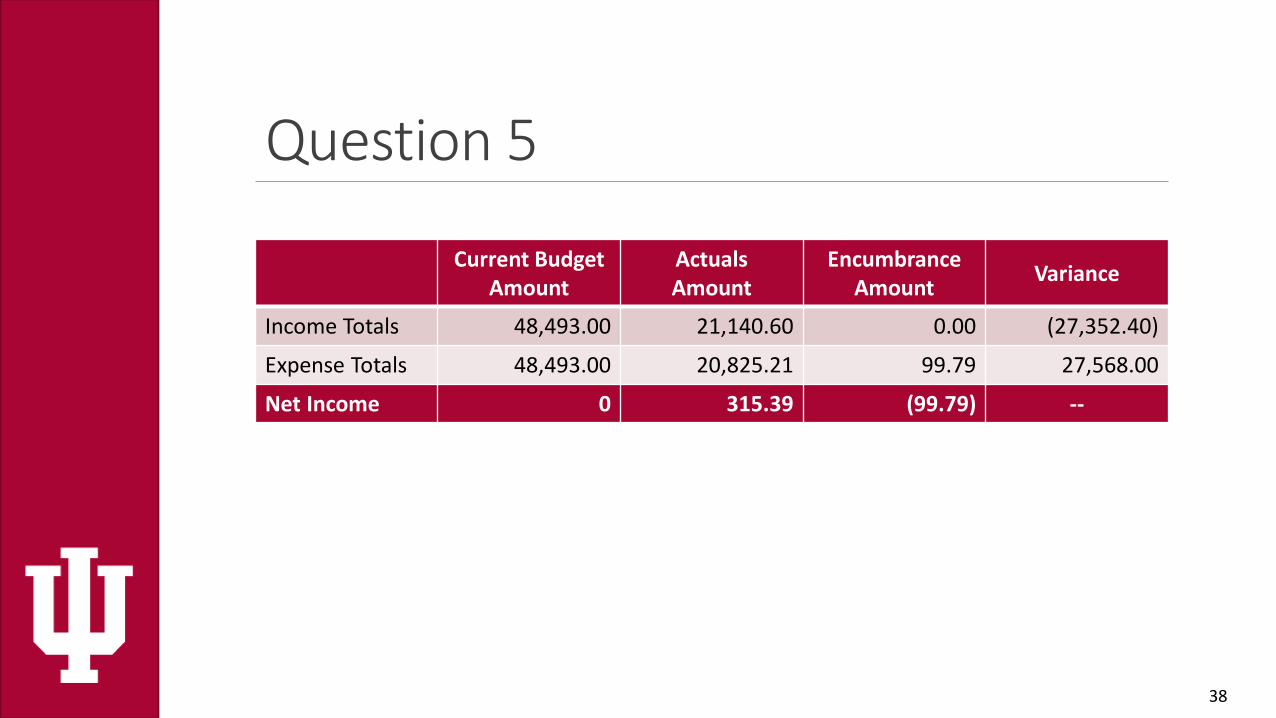

Question 5

38

Current Budget Amount

ActualsAmount

Encumbrance Amount Variance

Income Totals 48,493.00 21,140.60 0.00 (27,352.40)

Expense Totals 48,493.00 20,825.21 99.79 27,568.00

Net Income 0 315.39 (99.79) --

Available Balance: 215.60

Two more definitions

39

Why general fund variances matter Organization reversion and carry forward

(referred to as ‘org reversion’). A year-end process for general fund accounts that

either carries forward budget variances or reverts those variances to the Responsibility Center.

o RC = a collection of schools or major administrative units.

Remember: a general fund’s authority to spend is based on budget, not cash.

40

Org reversion table Defined for an organization at the discretion of

the RC and campus. Seven org reversion codes.

41

Code Encumbrances Positive Variance Negative Variance

A Carry Forward Carry Forward Carry Forward

C1 Carry Forward Carry Forward Revert

C2 Don’t Carry Forward Carry Forward Revert

N1 Carry Forward Revert Carry Forward

N2 Don’t Carry Forward Revert Carry Forward

R1 Carry Forward Revert Revert

R2 Don’t Carry Forward Revert Revert

Object code consolidation hierarchy Organizational system used for reporting. Groups similar object codes together so reports

show additional layers of detail. Made up of:o Object codes.o Levels (groups of object codes).o Consolidations (groups of levels).

42

Hierarchy example

43

Object

Level

Consolidation CMPN (Compensation)

BENF (Benefits)

Examples: 5625, 5760, 5772

(total of 20)

HRCO (Hourly

Compensation)

Examples: 3000, 3200, 3210

(total of 55)

PRSA (Professional

Salaries)

Examples: 2400, 2408, 2480

(total of 14)

Financial reporting options

44

3 reporting options at IU: Kuali Financial System (KFS) Balance Inquiries. Controller’s Office Reporting Tools. IU Information Environment (IUIE).

45

KFS Balance Inquiries Seven lookups available to KFS users. Retrieve transactional data posted to the General

Ledger, including budgets, actuals, and encumbrances.

Must have KFS system user role to run.

46

47

Available Balances example

48

Controller’s Office Reporting Tools Ever-growing collection of financial reports used

to research financial activity within your organization.

Maintained by University Accounting & Reporting Services (UARS)

o Group within University Controller’s Office that helps with development of reports & publishes report instructions.

Must have KFS system user role to run.

49

50

51

52

53

IUIE Reports Enterprise-wide, web-based operational reporting

system. Collection of reports that allow users to access

IU’s institutional data, including financial data. Maintained by Decision Support Services (DSS). Must be added to the KFS Labor Reports group to

access financial reports.

54

55

Current Balances example report

56

Which reporting tool?KFS

Real time data.

Able to include pending transactions.

Limited to one Fiscal Year, may be limited to one account per report.

Limited search parameters and result fields.

Can drill down through hotlinked data.

Good for pointed, quick inquiries

IUIE Data is current as of the

previous day.

Only includes finalized transactions.

Reports can span multiple Fiscal Years and multiple accounts.

Unable to drill down through multiple reports.

Search parameters and output result fields are customizable.

Good for large data sets & payroll inquiries

57

Controller’s Reporting Tools Data is current as of the

previous day.

Reports can span multiple Fiscal Years and multiple accounts.

Customizable, dynamic report parameters.

Can drill down through multiple reports.

Only system that generates BUY.IU reports & offers in-app instructions for each report.

Good for analysis of financial position of account/department.

Activity 2KFS, CONTROLLER’S REPORTING TOOLS, IUIE?

58

Question 1Dr. Nadir, a faculty member in your department, recently retired. Your co-worker transferred the outstanding balance from Dr. Nadir's research account to your department's general fund account. The TF routed to final this morning. Your Fiscal Officer (FO) asks you to pull a report that shows the new balance of the general fund account.

59

KFS.

Question 2You are building your department’s budget for the upcoming fiscal year. The data from the current fiscal year indicates that your department spent $25,000 more than planned on uniforms. You want to compare the data from five fiscal years to determine if the $25,000 overage was an anomaly or a trend.

60

IUIE.

Question 3You are the FO for the Media School and you need to review activity on your accounts each fiscal period. You want to establish a report with saved settings that automatically runs each month.

61

Controller’s Office Reporting Tools.

Question 4You are a Supervisor in your department. Your FO asks you audit timesheets for your department to identify those containing timestamps inconsistent with the actual hours worked.

62

IUIE.

Question 5You are a FO delegate in the Nursing department. While preparing for fiscal year-end, your FO asks you for a report that identifies outstanding BUY.IU encumbrances.

63

Controller’s Office Reporting Tools.

Question 6You know a $75.00 charge hit your account in September, but you cannot remember what the charge was for. You want to run a report to find a $75.00 charge and then drill down to the original document to see what was purchased.

64

KFS.

Wrap-up

65

Next steps VPCFO trainings:o KFS Balance Inquiries (2 hours).o IUIE Financial Reports (2 hours).o Learn more about these and other offerings on our

What We Offer page

Review your reference guide.

66

Resources For general resources for all three systems, see

the Resources section of the reference guide for this class• KFS resources coming soon

• Support: contact Customer Service via the UCO Contact Us form.

• Controller’s Office Reporting Tools• Support: contact UARS via the UCO Contact Us form

• IUIE • Support: contact Customer Service via the UCO Contact Us form.

UITS IT Training: IUIE Reporting Basics and Excel 2016: Formatting and Analyzing IUIE Data.

67

Training evaluation Let us know what you thought!o https://go.iu.edu/fineval

You will receive an email this afternoon with a link to the survey.

Feedback is anonymous.

68