Interpreting Aviation Weather1 INTERPRETING WEATHER INFORMATION.

Upload

iri-intlCategory

view

299download

0

How to interpret the sales stats behind

a new grocery product launch The most important data to see and act on

Tim Eales – Director of Strategic Insight

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 2

Where can you buy it?

How many people are buying it?

What are they paying for it?

Will it make its sales target?

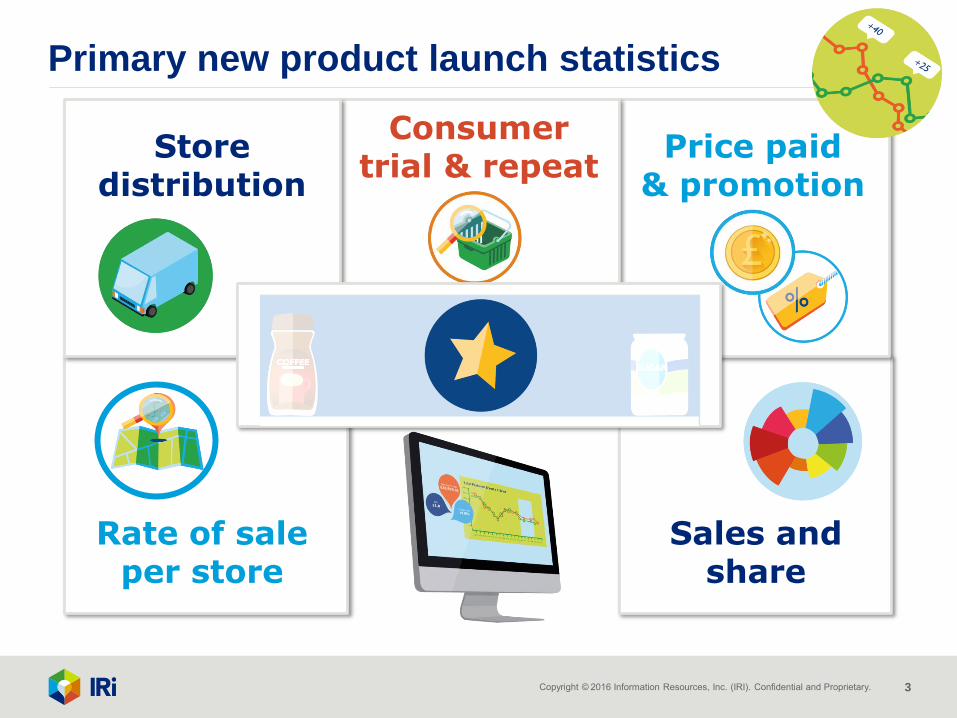

Primary new product launch questions

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 3

Rate of sale per store

Sales and share

Price paid & promotion

Consumer trial & repeat

Store distribution

Primary new product launch statistics

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 4

3 different distribution measures

Numeric

Category Weighted

ACV (Grocery) Weighted

BEST FOR CATEGORIES WHERE AS MUCH PHYSICAL

PRESENCE AS POSSIBLE IS THE CRITICAL FACTOR SUCH AS

SOFT DRINKS AND SWEETS

BEST FOR CATEGORIES WHERE NOT ALL

STORES WOULD SELL THE CATEGORY SUCH AS

HEALTH AND PERSONAL CARE

BEST FOR CATEGORIES THAT ARE

RELATIVELY NEW TO THE GROCERY TRADE

SUCH AS BATTERIES AND LIGHT BULBS

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 5

Distribution calculation – SINGLE ITEM LEVEL (UPC)

50% of coffee sales 30% 20%

50%

70%

80%

CWD

Item 1

Item 2

Item 3

Category Weighted Distribution represents

the proportion of category sales that take place

in the stores where your product is sold

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 6

13.0

24.7

17.5 15.0 14.4 15.3

less than 15% 15% to 30% 30% to 45% 45% to 60% 60% to 75% over 75%

Achieving a very high level of distribution as a new product is relatively

rare. The mid-point, with 50% above and 50% below, is just 36%.

PROPORTION OF NEW

PRODUCTS BY MAXIMUM

DISTRIBUTION IN MULTIPLES

ONLY 15% OF NEW

LAUNCHES EVER

ACHIEVE GREATER

THAN 75% CWD

IRI New Product study – 3378 New products launched from January 2013 to June 2015

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 7

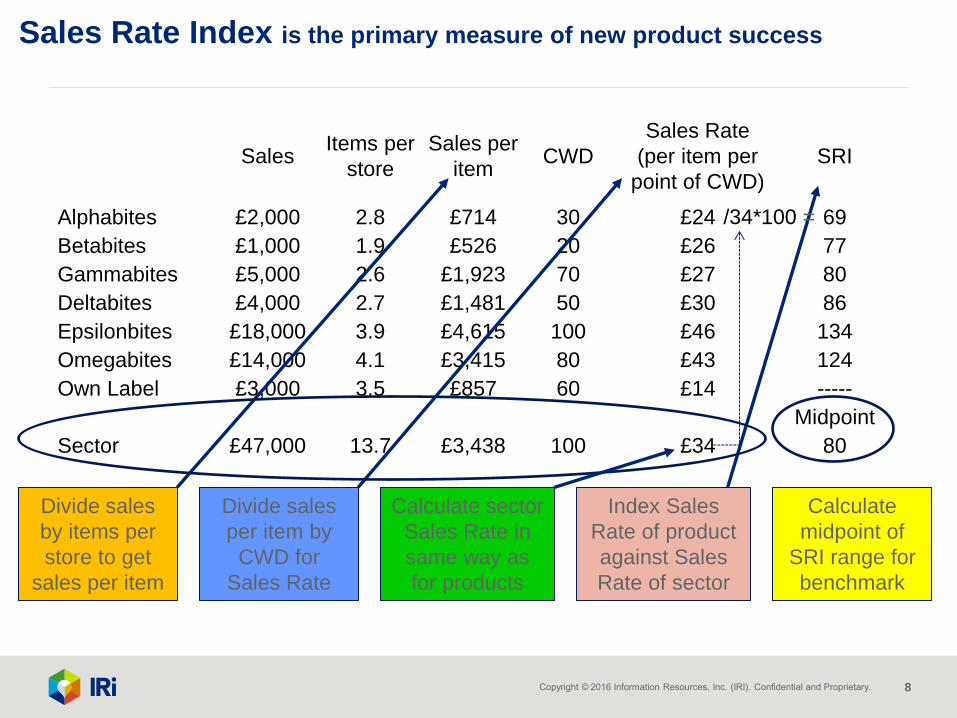

Sales Rate Index is the primary measure of new product success

“The test of selling at least as well as most of their

competition on the shelves next to them”

Which product is

going to make it into

the shopper’s

trolley?

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 8

Sales Rate Index is the primary measure of new product success

Sales Items per

store

Sales per

item CWD

Sales Rate

(per item per

point of CWD)

SRI

Alphabites £2,000 2.8 £714 30 £24 69

Betabites £1,000 1.9 £526 20 £26 77

Gammabites £5,000 2.6 £1,923 70 £27 80

Deltabites £4,000 2.7 £1,481 50 £30 86

Epsilonbites £18,000 3.9 £4,615 100 £46 134

Omegabites £14,000 4.1 £3,415 80 £43 124

Own Label £3,000 3.5 £857 60 £14 -----

Midpoint

Sector £47,000 13.7 £3,438 100 £34 80

Divide sales

by items per

store to get

sales per item

Divide sales

per item by

CWD for

Sales Rate

Index Sales

Rate of product

against Sales

Rate of sector

Calculate

midpoint of

SRI range for

benchmark

Calculate sector

Sales Rate in

same way as

for products

/34*100 =

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 9

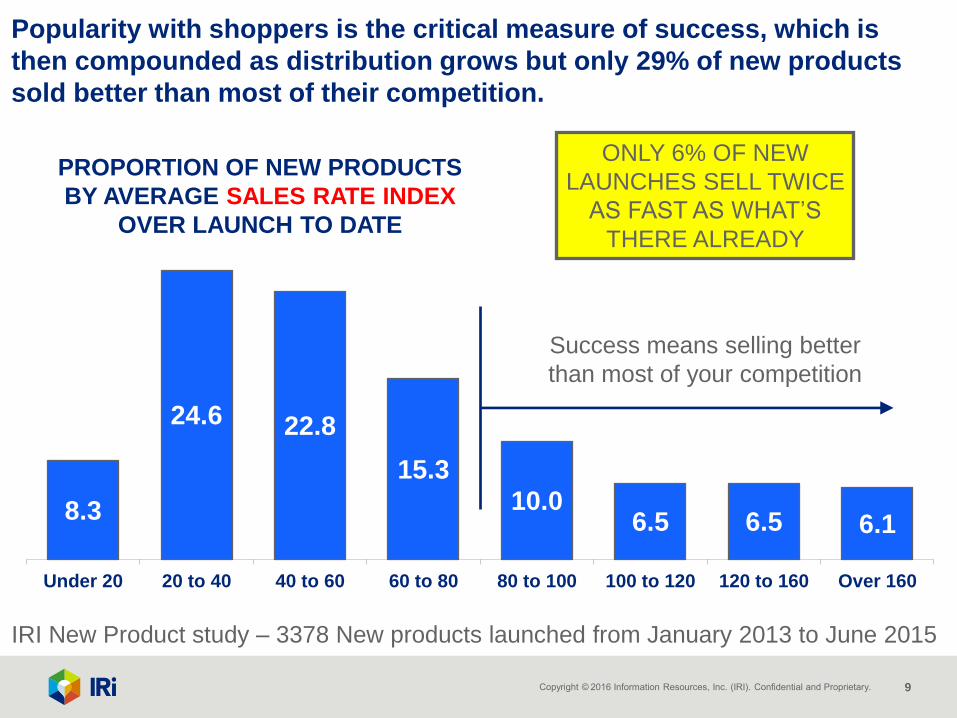

8.3

24.6 22.8

15.3

10.0 6.5 6.5 6.1

Under 20 20 to 40 40 to 60 60 to 80 80 to 100 100 to 120 120 to 160 Over 160

Popularity with shoppers is the critical measure of success, which is

then compounded as distribution grows but only 29% of new products

sold better than most of their competition.

PROPORTION OF NEW PRODUCTS

BY AVERAGE SALES RATE INDEX

OVER LAUNCH TO DATE

ONLY 6% OF NEW

LAUNCHES SELL TWICE

AS FAST AS WHAT’S

THERE ALREADY

Success means selling better

than most of your competition

IRI New Product study – 3378 New products launched from January 2013 to June 2015

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 10

Most branded NPD, 70% of it, undersells what is on the shelf already.

This level has barely changed since 2011.

29.0

21.6

39.3

29.7

20.3

16.8

43.3

41.8

32.6

ALL PRODUCTS

ALL FOOD

NON-FOOD

CONFECTIONERY

FOOD & DRINK

PET FOOD

OTC & HEALTH

PERSONAL CARE

HOUSEHOLD

SUCCESS - measured by outselling the average item in your sector

% of new products with average Value SRI

above 80 across sales to date

Overall, less than 1

in 3 launches sell

better than the

average in their

sector. For food

this is only 1 in 5

When the slowest

selling NPD is

included, success

drops to 1 in 5

overall

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 11

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

4 8 12 16 20 24 28 32 36 40 44 48 52 56 60 64 68 72 76 80 84 88 92 96 100 104 108 112 116 120 124 128

SALES RATE 50% OR MOREABOVE AVERAGE

SALES RATE LESS THAN 50%OF AVERAGE

If a new product is not selling well (low Sales Rate Index) then it

tends to lose distribution after about 9 months.

Distribution Trend for HIGH DISTRIBUTION GROUPS

Max CWD over 36%

WEEKS FROM LAUNCH : Average new product trend over first 2.5 years

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 12

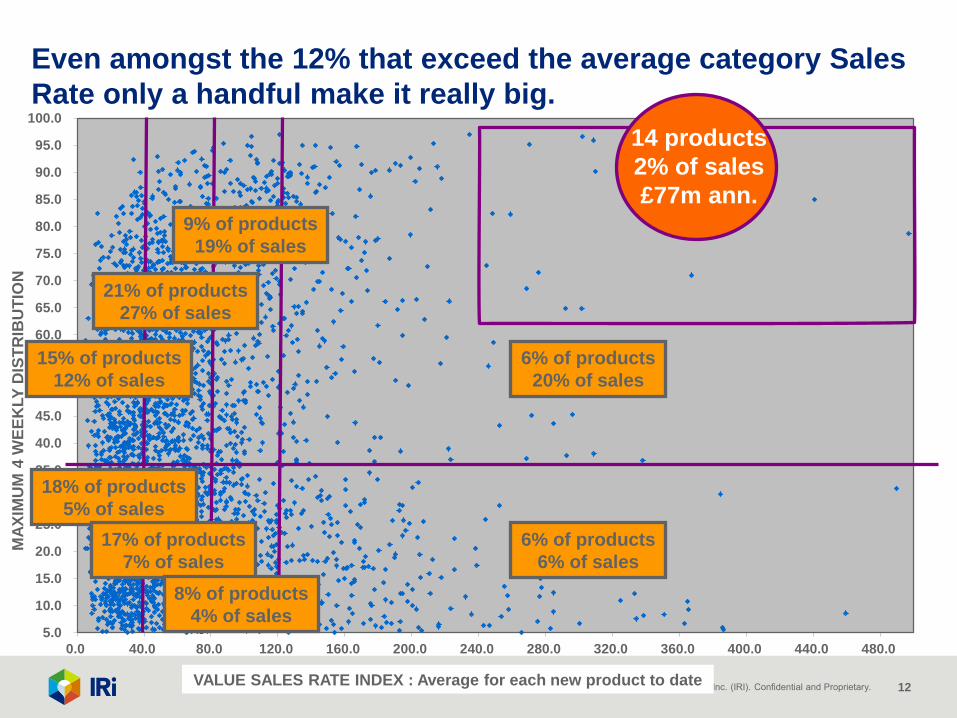

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

95.0

100.0

0.0 40.0 80.0 120.0 160.0 200.0 240.0 280.0 320.0 360.0 400.0 440.0 480.0

VALUE SALES RATE INDEX : Average for each new product to date

MA

XIM

UM

4 W

EE

KLY

DIS

TR

IBU

TIO

N

18% of products

5% of sales

17% of products

7% of sales

8% of products

4% of sales

6% of products

6% of sales

15% of products

12% of sales

21% of products

27% of sales

9% of products

19% of sales

6% of products

20% of sales

14 products

2% of sales

£77m ann.

Even amongst the 12% that exceed the average category Sales

Rate only a handful make it really big.

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 13

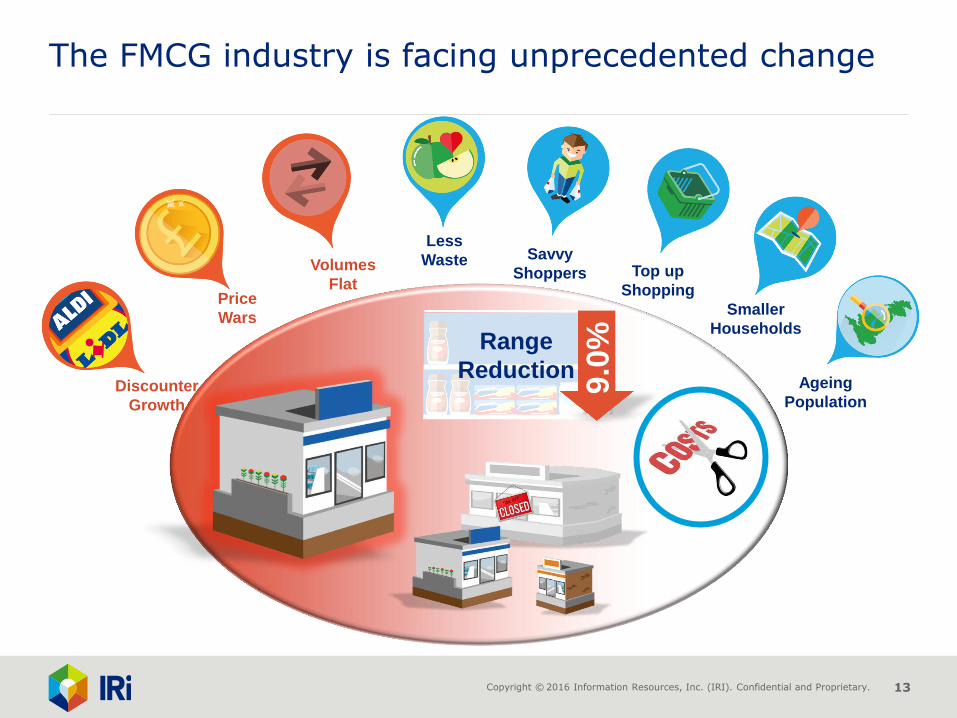

The FMCG industry is facing unprecedented change

Range

Reduction

9.0

%

Savvy

Shoppers Top up

Shopping

Smaller

Households

Ageing

Population

Less

Waste

Discounter

Growth

Price

Wars

Volumes

Flat

Copyright © 2016 Information Resources, Inc. (IRI). Confidential and Proprietary. 14

Which is in turn having an impact on new products

How to interpret the sales stats behind

a new grocery product launch The most important data to see and act on

Tim Eales – Director of Strategic Insight