Integrated Accounting Issues Winter 2006 Rodney K. Rogers, Ph.D., CPA School of Business...

29

Integrated Accounting Issues Winter 2006 Rodney K. Rogers, Ph.D., CPA School of Business Administration Portland State University

-

date post

22-Dec-2015 -

Category

Documents

-

view

214 -

download

1

Transcript of Integrated Accounting Issues Winter 2006 Rodney K. Rogers, Ph.D., CPA School of Business...

Integrated Accounting IssuesWinter 2006

Rodney K. Rogers, Ph.D., CPA

School of Business Administration

Portland State University

Traditional Stakeholders of Firm

Operations/Investing Vendor Customer

Goods

$

$

Goods

Creditors Investors

$ $ $ $Financial Intermediaries

InformationIntermediaries

Expanded Stakeholders

Firm

Shareholders

Creditors

Employees

Management

CompetitorsGovernment

Customers

Vendors

ExternalAuditors

Internal Auditors

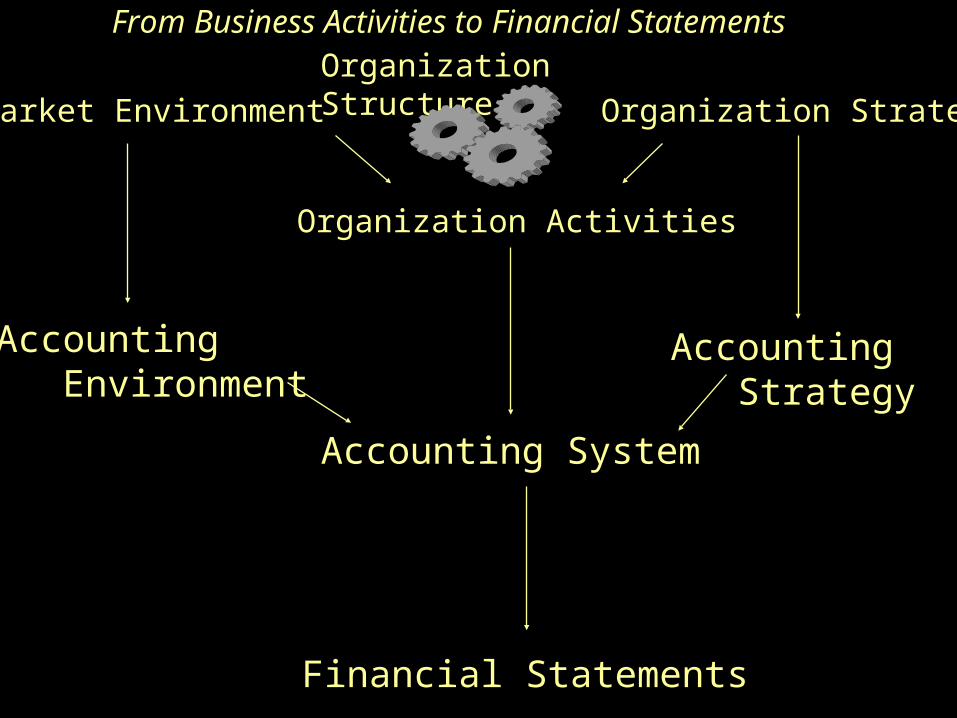

Market Environment Organization Strategy

Organization Activities

Accounting System

Financial Statements

Accounting Environment

Accounting Strategy

From Business Activities to Financial StatementsOrganization Structure

Analysis of a Company• Market Environment – “Context”

– Macroeconomic, governmental, legal considerations,

• Organization Strategy Analysis – “Expectations”– Key profit drivers, business risks and profit potential

• Organization Structure – “Capabilities”– Current structure of organization

• Accounting Analysis– Evaluate the “quality” of the accounting numbers

• Financial Analysis– Evaluate performance using financial and non-financial information – (past

and current results)

• Prospective Analysis– Forecasts and valuation

SWOT Analysis

• Internal– Strengths– Weaknesses

• External– Opportunities– Threats

Market Environment

• Interest Rates

• US and foreign GNP Growth

• Unemployment Levels

• Trends in Consumer savings/borrowing

• Others

Business Strategy Analysis • Specific Industry Structure (Porter’s “five forces”)

– Rivalry among existing firms• Industry Growth, Concentration, Switching Costs, Fixed/Variable Costs,

Excess Capacity

– Threat of new entrants• Scale Economies, First mover, Relationships

– Threat of substitute products• Price/Performance trade-off

– Bargaining power of buyers and suppliers• Switching cots, number and volume of buyers/suppliers

• Competitive Strategy– Cost Leadership– Differentiation

Competitive Strategy

• Cost Leadership– Same product or service at lower cost

• Economies of scale, efficient production, design

• Differentiation– Unique product or service at a premium price

• Product design, variety, customer service, brand, R&D, innovation

• How to maintain competitive status?

Business Strategy Analysis

• Quality of Management

• Regulatory Developments

• Social Issues

• Technology

Output: Basic Financial Statements

• Balance Sheet

• Income Statement

• Statement of Cash Flows

• Retained Earnings Statement

• Statement of Comprehensive Income

Analyzing a Firm

Operations/Investing Vendor Customer

Goods

$

$

Goods

Creditors Investors

$ $ $ $Financial Intermediaries

InformationIntermediaries

Accounting Analysis

• Quality of Disclosures

• Quality of Numbers

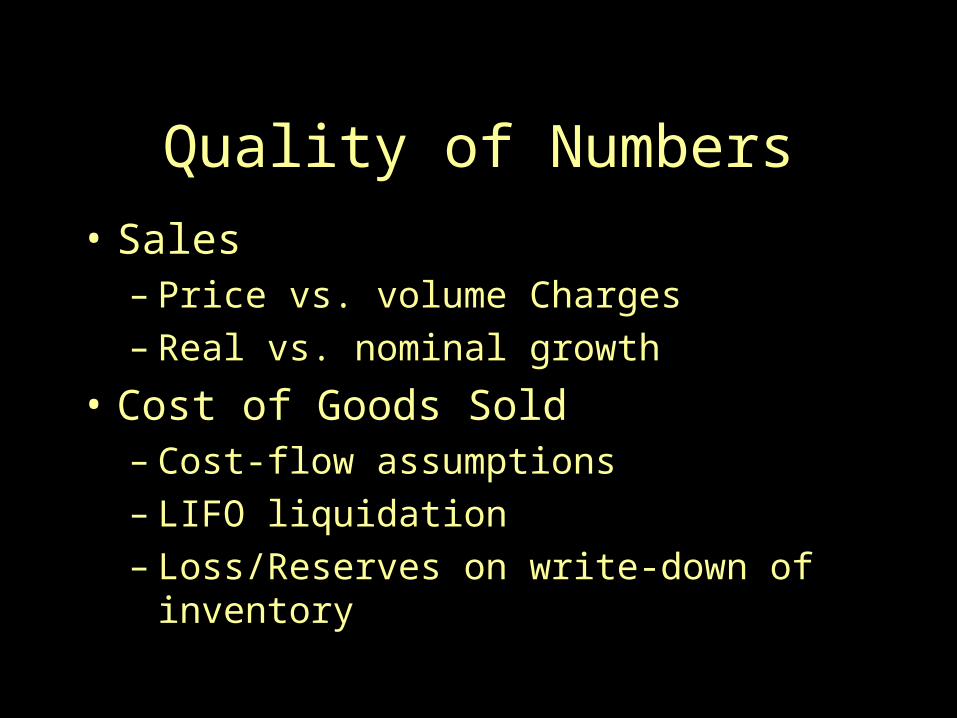

Quality of Numbers

• Sales– Price vs. volume Charges– Real vs. nominal growth

• Cost of Goods Sold– Cost-flow assumptions– LIFO liquidation– Loss/Reserves on write-down of inventory

Quality of Numbers• Operating Expenses

– Discretionary expenses• R&D• Repair and Maintenance• Advertising and Marketing

– Depreciation• Methods• Estimates

– Pension Accounting

Quality of Numbers• Nonoperating Revenue and Expenses

– Gains/Losses from Sales of Assets– Interest Income– Equity Income– Loss recognition on write-down of assets– Accounting changes– Extraordinary items– Reserves on restructuring charges

Financial Analysis:Levers for Value Creation

Return on Equity = Net Income

Shareholder’s Equity

Return on = Profit Margin x Asset Turnover x FinancialEquity Leverage

net income = net income x sales x assets owner’s equity sales assets owner’s equity

Change revenueshigher pricesgreater volume

Change costsproduct/process designsupply relationships

Reduce needfor investment(capital intensity)

Advantageousfinancing(external)

Interrelationships of Ratios

Managing Rev/Exp Assets Liabilities/Equity

Managing Sales and Expenses

• Gross Profit

• Operating Profit

• Issues to Consider– Price vs. Volume Changes– Real vs. Nominal Growth– Inventory Issues

Many terms

• Net Income

• EBIDA

• EBIT or Operating Income (pre-tax)

• EBITDA

• FCF

• NOPAT or prefinancing operating earnings

Profitability Ratios

Gross Profit Margin = Gross Profit Net Sales

Operating Profit Margin = Operating Profit Net Sales

Net Profit Margin = Net Earnings Net Sales

Profitability Ratios

Return on Investment (ROI) = Net Earnings Total Assets

SGA % = Selling, General and Admin. Expenses Net Sales

Cash Flow Margin = Cash flow from operations Net Sales

Return on Assets (ROA) = NOPAT Total Assets

Managing AssetsDays in Receivables = Accounts Receivable

Avg.Daily Sales

A.R. Turnover = Net SalesAccounts Receivables

Inventory Turnover = Cost of Goods Sold Inventory

Fixed Asset Turnover = Net SalesNet Prop.Plant&Equip.

Total Asset Turnover = Net Sales Total Assets

Managing Liabilities and Equity

Current Ratio = Current AssetsCurrent Liabilities

Quick Ratio = Current Assets-Inventory Current Liabilities

Managing Liabilities and EquityDebt Ratio = Total Liabilities

Total Assets

L.T. Debt to Total Capital = LT Debt LT Debt + S.E.

Debt to Equity = Total LiabilitiesShareholders’ Equity

Times Interest Earned = Operating ProfitInterest Expense

Return on = Profit Margin x Asset Turnover x FinancialEquity Leverage

net income = net income x sales x assets owner’s equity sales assets owner’s equity

Change revenueshigher pricesgreater volume

Change costsproduct/process designsupply relationships

Reduce needfor investment(capital intensity)

Advantageousfinancing(external)

Interrelationships of Ratios

Managing Rev/Exp Assets Liabilities/Equity

(common earnings leverage) (capital structure leverage)

Market RatiosEarnings Per Share = Net Earnings

Avg. Shares Outstanding

Price to Earnings Ratio = Market Price of Common StockEarnings Per Share

Dividend Payout Ratio = Dividends Per Share Earnings Per Share

Dividend Yield = Dividends Per Share Market Price of Common Stock

Financial Performance Measures by Area and Viewpoint

Management Owners LendersOperational AnalysisGross ProfitProfit MarginOperating Exp.AnalysisContribution

ProfitabilityReturn on Net WorthReturn on Comm.EquityEarnings Per Share

LiquidityCurrent RatioAcid Test Ratio

Asset ManagementAsset TurnoverWorking CapitalInventory TurnA.R. Turn; A.P.

Disposition ofEarningsCash flow per shareDividends per shareDividend yieldPayout/retention

LeverageDebt to AssetsDebt to CapitalizationDebt to Equity

ProfitabilityReturn on AssetsEarnings before Int/TaxReturn on Assets

Market IndicatorsPrice/Earnings RatioMarket to Book Value

Debt ServiceInterest CoverageInterest/Principal Cov.