Insurance Market Incentives and constraints ...

23

Insurance Market Incentives and constraints and complementary public policies and complementary public policies … a policy practitioners’ perspective Dr Andrew Fronsko September 2011

Transcript of Insurance Market Incentives and constraints ...

Insurance Market Incentives and constraints and complementary public policiesand complementary public policies

… a policy practitioners’ perspective

Dr Andrew FronskoSeptember 2011

FirstFirst

response to some burning issues raised yesterday… response to some burning issues raised yesterday

Australia Road Toll leading to 1978 f(n) populationAustralia Road Toll leading to 1978 f(n) population

Australian Road Fatalities

3 500

4,000

30

35Introduction

T ffi Li ht

MandatoryFitting Seatbelts (1969)

Wearing Seatbelts (1973)

2 000

2,500

3,000

3,500

20

25

30Traffic Lights (1930) Random Breath Testing

Vic (1979), NSW (1987)Aust Wide (1988)

500

1,000

1,500

2,000

5

10

15

-

500

1925 1935 1945 1955 1965 1975 1985 1995 20050

5

Fatalities (LHS) Rate per 100 000 population (RHS)Fatalities (LHS) Rate per 100,000 population (RHS)

Statutory Insurance ProductStatutory Insurance ‐ ProductCTP Workers’ Compensation

Common LawNo-FaultBlended (No-Fault, restricted Common Law)

NSW has No-Fault Benefits for Catastrophic Care Limits on Statutory Benefits for Income Replacement

Statutory Insurance DeliveryStatutory Insurance ‐ DeliveryCTP Workers’ Compensation

PrivatePublic Monopoly

Claims and Policy Administration Outsourced

Rudimentary Scheme Assessment: Road TraumaRudimentary Scheme Assessment: Road Trauma

Rudimentary Scheme Assessment: Road Trauma

Road Deaths per 100,000 people 20084.16

4.12

UK

Netherlands

Rudimentary Scheme Assessment: Road Trauma

6.20

5.46

5.33

5.10

4.40

Ireland

Germany

Norway

Switzerland

Sweden

7 20

7.00

6.84

6.71

6.56

Denmark

Luxembourg

France

Australia

Spain

Ireland

ry

9 96

8.58

8.16

8.13

7.76

7.20

H

Belgium

Italy

Austria

Portugal

Denmark

Cou

ntr

13.72

12.25

10.53

10.25

9.96

Romania

USA

Slovakia

Cyprus

Hungary NT16.2 in 2009

34.10

14.65

14.12

14.09

Northern Territory

Lithuania

Poland

Greece

History of CTP Scheme Premium Rates (% AWE)

0.8

History of CTP Scheme Premium Rates (% AWE)

0.50.60.7

of A

WE

0 20.30.4

opor

tion

o

00.10.2

6 7 8 9 0 1 2 3 4 5 6

Pro

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

NSW VIC QLD SA WATAS NT ACT NZ

Explaining Difference Between NSW and Victorian CTP PremiumsAverage Premium per vehicle Dec Qtr 1999

(Illustrative, not to scale)

400

450NSW

(Illustrative, not to scale)

350

Hi h

Higheraccident

Paymentminorclaims<$450

HigherEco LossPayment

HigherG.D.

Payment

HigherLegal &Other

HigherProfit

250

300Higher

Acquisition &Reinsurance

LowerAdminC t

LowerProgram

rates

Exclude

Payment OtherCosts

Vic

150

200

Costs ProgramCosts At-Fault

Claims

150

Administration Environment Product & Legal Profit

Purpose• Present a policy practitioners’ perspective• Framework to help structure informed debateFramework to help structure informed debate • Seed discussion co-operative/ collaborative opportunities

to align efforts to improve road safety outcomes

QualificationsQualifications• Basic policy practitioner’s “tool-kit”

– Not a dissertation, some over-simplification i i l– suggestions to improve paper welcome

• Metaphors used to stimulate thinking

• Valid comparisons between systems can be made, but p y ,with caution due to statutory differences and variations in local practice. Raw comparisons can be “more misleading than informative, however, comparisons at the broadest aggregate level may be meaningful” (Hunt 1998)level may be meaningful (Hunt 1998)

Characteristics of InsuranceRisk Management

Control the risk… likelihood/consequencesA id th i k

Characteristics of Insurance

Avoid the riskRetain the risk Transfer (or redistribute) the risk… whole or part… whole or part

Features of InsuranceRisk Transfer - legally enforceableConsideration – generally, premium related to risk/benefits Risk pool created if many parties Distribution of benefits from the pool

Insurance: Spectrum of Adequacy ObjectivesInsurance: Spectrum of Adequacy Objectives

General Insurance Medicare Statutory Insurance (CTP/Comp)

Individual AdequacyPremiums largely determined on an actuarial basisRedistributive amongst insureesRedistributive amongst insureesStandard model for competitive insurance market Social Adequacy

Public tax-transfer systemBenefits related to needsBenefits related to needsSocial assistance/welfare

Public Monopolies may integrate societal objectivesPublic Monopolies may integrate societal objectives

Statutory Insurance Schemes

Private PublicPrivateUnderwriting

PublicUnderwriting

T i l Obj ti Typical ObjectivesTypical Objectives•Profit Maximisation•Subsidiary Objectives that are aligned to profit maximisation (eg injury prevention)

Typical Objectives• Long term [financial] viability• Injury prevention and trauma reduction• Fair and equitable benefits• Speedy, sustainable and cost effective rehabilitation• Affordable premiums j y p )

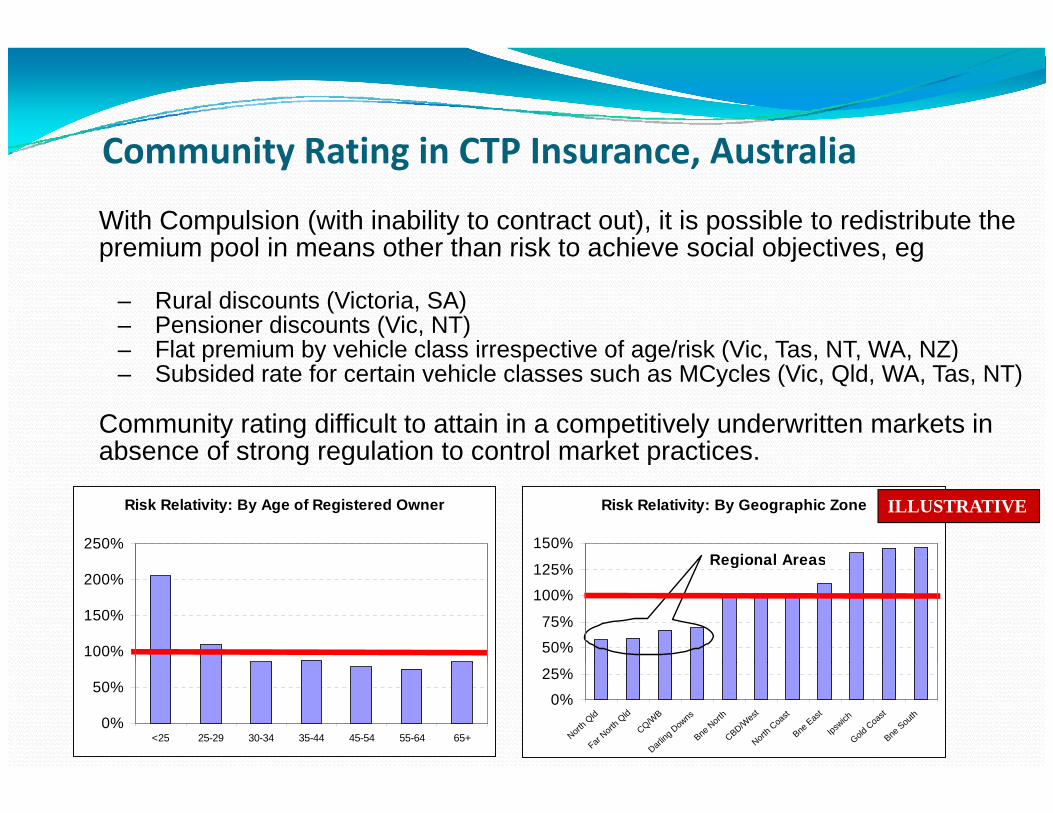

Community Rating in CTP Insurance AustraliaCommunity Rating in CTP Insurance, Australia

With Compulsion (with inability to contract out), it is possible to redistribute the premium pool in means other than risk to achieve social objectives egpremium pool in means other than risk to achieve social objectives, eg

– Rural discounts (Victoria, SA)– Pensioner discounts (Vic, NT)– Flat premium by vehicle class irrespective of age/risk (Vic, Tas, NT, WA, NZ)Flat premium by vehicle class irrespective of age/risk (Vic, Tas, NT, WA, NZ)– Subsided rate for certain vehicle classes such as MCycles (Vic, Qld, WA, Tas, NT)

Community rating difficult to attain in a competitively underwritten markets in absence of strong regulation to control market practices.

Risk Relativity: By Age of Registered Owner

250%

Risk Relativity: By Geographic Zone

150%Regional Areas

absence of strong regulation to control market practices.

ILLUSTRATIVE

100%

150%

200%

50%

75%

100%

125% Regional Areas

0%

50%

<25 25-29 30-34 35-44 45-54 55-64 65+

0%

25%

North Q

ld

Far Nort

h Qld

CQ/WB

Darling

Dow

ns

Bne N

orth

CBD/Wes

t

North C

oast

Bne Eas

t

Ipswich

Gold C

oast

Bne Sou

th

Varied Nature of Australian Insurance SchemesVaried Nature of Australian Insurance Schemes

Segment / Characteristic

General (Motor) Insurance

Auto Liability (CTP) Insurance

Workers’ CompensationInsurance

Public Liability Insurance

Private Health and Disability Insurance

Social Health Insurance

Unemployment Insurance

Adequacy Objective

Individual Hybrid Hybrid Individual Individual Social Social

Funding Fully Funded Fully Funded Fully Funded Fully Funded Fully Funded PAYG PAYG

Community Rating No Partial No No No Yes Yes

Underwriting Private Blend Blend Private Private Public Public

Typical Exposure Short Tail Long Tail Long Tail Med-Long Tail Short Tail Long Tail Long Tail

Beneficiary Party First Third + First Third + First Third First First First

Claim Order First Resort First Resort First Resort First ResortFirst call on CTP/WC

First Resort First call on CTP/WC

Last Resort Means Tested First call on CTP/WC

Last ResortMeans TestedFirst call on CTP/WC

P ti i ti Di ti C l C l Di ti Di ti U i l U i lParticipation Discretionary Compulsory Compulsory Discretionary Discretionary Universal Universal

CTP Insurance EvolutionCTP Insurance EvolutionHistorical Epoch

Dramatic growth in injury ratesDramatic growth in injury rates, associated with vehicle population growth and increased travel speedInjurers ability to fully compensate injured third parties limited in cases of catastrophic injuries

Motives for Compulsion Thi d t t lit ( t fThird party externality (aspects of judgment proof argument)

Judgment Proof problemJudgment Proof problem… potential policy responses:

Policy Response Injurer’s excessive engagement in risky activity & dulling of incentives to take adequate care

Inadequate compensation by injurers (to victims)

M d t h li bilit [thi d t ] iMandate purchase liability [third party] insurance

Prohibition to purchase liability [third party] insurance

Minimum level of assets to engage in a [risky] activity

Extension of liability to parties related to the injurer (e.g employer liability, vicarious liability, joint & several action)

Safety Regulation

C CCivil and Criminal penalties

Prohibition of risky activities

Victims mandated to obtain [first party] insurance

Adapted from Shavell, 1986

Other Issues confronting regulatorsOther Issues confronting regulators

MORAL HAZARDMORAL HAZARDInsured has an economic incentive to cause the situation he isinsured against, an incentive that is not present when he is not insured

ADVERSE SELECIONinformation asymmetry between the insured and insurerCross subsidisation may weaken or be in conflict with price signalling incentives

MARKET IMPERFECTIONSMissing marketsLack of economies leading to high transactional costsg g

CONSUMER IGNORANCE AND IRRATIONALITYReasons why persons do not purchase insurance, or undertake risky activities

.

Other Issues confronting regulatorsOther Issues confronting regulators

COMPETITIVE DYNAMICSBenefit shareholders in the short-term as a key priority

incentive to maintain/encourage information asymmetriesincentive to maintain/encourage information asymmetries

BASIS OF DETERMINING BENEFITS AND COSTS ?

Insurance system = Income/Capacity + Health/Medical + Pain Suffering + Legal/Admin

+ Societal = Health/medical & Unemployment (not funded by insurer) Societal Health/medical & Unemployment (not funded by insurer)+ Lost Opportunity = Loss of productivity and contribution to society by injured & carers+ Internalisation = Internalised grief of injured & carers (non-economic) +/- Other Offsets = Contribution of insurance sector to economy (employment/taxes) ?

Competitive Federalism MetaphorCompetitive Federalism Metaphor

in theory, schemes are free to adapt and respond to needs specific to the jurisdiction, and this provides the opportunity to act as “policy laboratories” that over time jurisdictions may identify and gravitate to policies that demonstrate success (Osborne 1988) and learn from policy failures in other jurisdictions (Jewett 2001)from policy failures in other jurisdictions (Jewett 2001)

A key challenge under “competitive federalism” is to minimize the risk of destructive competition and coordination failure.

To this extent, Australia has developed extensive and varied array of intergovernmental cooperative arrangements including:

• mutual recognition regimes• mutual recognition regimes• harmonisation of regulation• adoption of national standards• integrated inter-jurisdictional frameworks to

develop and oversee the implementation of various reform measures

• promotion of benchmarking

Ideas to open discussionIdeas to open discussion

Cooperative/Collaborative efforts among stakeholders to improve Road Safety Outcomes

• clear accountabilities within the road safety system• integrated cooperative frameworks to

implementation of reform measuresimplementation of reform measures• improve the accessibility of information to the

public to make informed [safety] choices• public education where ignorance or irrationality of

risk assessment may be present• pooling of scheme data to assist with risk

identification, policy development, public education and informed consumer choicea d o ed co su e c o ce

• benchmarking activities/projects • coordination of micro-activities among road safety

stakeholders to amplify impact of initiatives

embracing new technologies….

Open for QuestionsOpen for Questions

If it helps I can email you these publicationsIf it helps, I can email you these publications