Indonesia Industry Focus Indonesia Construction - dbs.com Wijaya Karya Beton : Wika beton (a...

51

ed-TH / sa- MA, PY Adjusting expectations Decelerating new contract growth and rising capital needs cap sector’s upside potential; turning Neutral on the sector Contractors with ample balance sheet capacity stand a better chance of winning more projects Execution and earnings are key catalysts. Top picks: PTPP and WTON Turning Neutral on Indonesia’s construction sector; the stock-picking game continues. We are turning Neutral on the sector (from Positive previously) as we expect new contract growth to decelerate while the higher capital needs pose a risk to profitability. We advise investors to stay selective. We like PTPP due to its attractive valuation at 0.34x EV/order book, lower than peers. PTPP also has a smaller capex commitment compared to its peers, and a less leveraged balance sheet to support its future earnings and new contract growth. As the government and project owners accelerate the execution of infrastructure projects, we believe precast producers, including WTON, are in a sweet spot. Contractors with ample balance sheet capacity stand a better chance of winning more projects. Job opportunities are aplenty for contractors given Indonesia’s massive need for infrastructure. Nonetheless, funding remains a challenge with fiscal deficit being capped at 3% by law while the government has been taking a break from injecting capital into SOEs. A number of funding alternatives are taking place but mostly require the contractors to also invest in the infrastructure projects or work under a turnkey scheme. Capital requirements to win a project will continue to rise, hence we prefer contractors with ample balance sheet capacity, established JVs with foreign players and good cash flow management. Where we differ. Consensus' blanket overweight stance on the sector implies an expectation that earnings delivery will be smooth for all listed state-owned contractors, which may not be the case as some contractors are facing land acquisition issues and funding constraints. We also expect new contracts to peak out this year and decline by 6% in 2018. On contrary to consensus Buy call on all listed state-owned contractors, we believe selective investing in the sector is the best approach given the peaking new contract growth and differing risk profile among the contactors. Our top picks in the sector are PTPP and WTON. JCI : 5,825.10 Analyst Chong Tjen-San +60 3 26043972 [email protected] Tiesha PUTRI +6221 30034931 [email protected] STOCKS Source: AllianceDBS, DBSVI, Bloomberg Finance L.P. Closing price as of 5 Jul 2017 Waskita Karya : Waskita Karya is a stated owned construction company engaging in a wide variety of construction activities including highways, bridges, ports, airports, and LRT. Pembangunan Perumahan : PT PP (Persero) is Indonesia's leading construction company with business portfolio encompassing from building and civil infrastructure constructions. Wijaya Karya : Wijaya Karya is a construction company with interests in EPC, civil, building works, precast and realty. Wijaya Karya Beton : Wika beton (a subsidiary of Wikaya Karya) is a leader in precast in Indonesia with c.40% market share. Construction companies’ PE valuation range since 2012 (x) Source: AllianceDBS, DBSVI 5 15 25 35 45 55 65 75 WSKT PTPP WIKA WTON DBS Group Research . Equity 5 Jul 2017 Indonesia Industry Focus Indonesia Construction Refer to important disclosures at the end of this report Price Mkt Cap Target Price Performance (%) Rp US$m Rp 3 mth 12 mth Rating Waskita Karya 2,270 2,306 2,400 (2.1) (6.8) HOLD Pembangunan Perumahan 3,330 1,545 4,100 2.8 (7.2) BUY Wijaya Karya 2,220 1,491 2,050 (4.7) (15.6) HOLD Wijaya Karya Beton 605 395 760 (21.5) (33.7) BUY

Transcript of Indonesia Industry Focus Indonesia Construction - dbs.com Wijaya Karya Beton : Wika beton (a...

ed-TH / sa- MA, PY

Adjusting expectations

Decelerating new contract growth and rising capital needs cap sector’s upside potential; turning Neutral on the sector

Contractors with ample balance sheet capacity stand a better chance of winning more projects

Execution and earnings are key catalysts. Top picks: PTPP and WTON

Turning Neutral on Indonesia’s construction sector; the

stock-picking game continues. We are turning Neutral on the sector (from Positive previously) as we expect new contract growth to decelerate while the higher capital needs pose a risk to profitability. We advise investors to stay selective. We like PTPP due to its attractive valuation at 0.34x EV/order book, lower than peers. PTPP also has a smaller capex commitment compared to its peers, and a less leveraged balance sheet to support its future earnings and new contract growth. As the government and project owners accelerate the execution of infrastructure projects, we believe precast producers, including WTON, are in a sweet spot. Contractors with ample balance sheet capacity stand a

better chance of winning more projects. Job opportunities are aplenty for contractors given Indonesia’s massive need for infrastructure. Nonetheless, funding remains a challenge with fiscal deficit being capped at 3% by law while the government has been taking a break from injecting capital into SOEs. A number of funding alternatives are taking place but mostly require the contractors to also invest in the infrastructure projects or work under a turnkey scheme. Capital requirements to win a project will continue to rise, hence we prefer contractors with ample balance sheet capacity, established JVs with foreign players and good cash flow management. Where we differ. Consensus' blanket overweight stance on the sector implies an expectation that earnings delivery will be smooth for all listed state-owned contractors, which may not be the case as some contractors are facing land acquisition issues and funding constraints. We also expect new contracts to peak out this year and decline by 6% in 2018. On contrary to consensus Buy call on all listed state-owned contractors, we believe selective investing in the sector is the best approach given the peaking new contract growth and differing risk profile among the contactors. Our top picks in the sector are PTPP and WTON.

JCI : 5,825.10

Analyst Chong Tjen-San +60 3 26043972 [email protected] Tiesha PUTRI +6221 30034931 [email protected]

STOCKS

Source: AllianceDBS, DBSVI, Bloomberg Finance L.P. Closing price as of 5 Jul 2017 Waskita Karya : Waskita Karya is a stated owned construction company engaging in a wide variety of construction activities including highways, bridges, ports, airports, and LRT.

Pembangunan Perumahan : PT PP (Persero) is Indonesia's leading construction company with business portfolio encompassing from building and civil infrastructure constructions.

Wijaya Karya : Wijaya Karya is a construction company with interests in EPC, civil, building works, precast and realty.

Wijaya Karya Beton : Wika beton (a subsidiary of Wikaya Karya) is a leader in precast in Indonesia with c.40% market share.

Construction companies’ PE valuation range since 2012 (x)

Source: AllianceDBS, DBSVI

5

15

25

35

45

55

65

75

WSKT PTPP WIKA WTON

DBS Group Research . Equity 5 Jul 2017

Indonesia Industry Focus

Indonesia Construction

Refer to important disclosures at the end of this report

Price Mkt Cap Target Price Performance (%)

Rp US$m Rp 3 mth 12 mth Rating

Waskita Karya 2,270 2,306 2,400 (2.1) (6.8) HOLD Pembangunan Perumahan 3,330 1,545 4,100 2.8 (7.2) BUY

Wijaya Karya 2,220 1,491 2,050 (4.7) (15.6) HOLD Wijaya Karya Beton 605 395 760 (21.5) (33.7) BUY

Industry Focus

Page 2

We identify three key issues that will shape the sector's

performance for the rest of the year:

1) The speed of project execution. The three contractors

under our coverage are now sitting on a record-high order book. After two years of stellar new contract growth, we expect the pace of project awards for the big three state-owned contractors (Wijaya Karya, PT PP and Waskita Karya) to decelerate in the coming months given the already high new contract base last year (Rp157tr vs Rp84tr in 2015). That said, the focus will shift to project delivery, and consequently earnings.

2) Land acquisition funding. A number of land-intensive toll road projects have been awarded by the government and there are more new toll road concessions that are in talks. We identify over 2,500 km toll roads in the pipeline, exceeding the government’s initial target of developing 1,000 km new toll roads by 2019.

Land acquisition for infrastructure projects are typically funded by the government, but the disbursement of the funds has been delayed since last year due to bureaucratic hurdles.

A new scheme that allows the project owner to pre-finance the land acquisition cost while awaiting the government to disburse the funds has been adopted since then. However, this has also become an additional burden for the project owners’ balance sheets.

We believe the fund disbursement would be a positive catalyst for the sector to speed up land acquisition activities and project delivery.

3) Asset recycling and securitisation, particularly for Waskita Karya (WSKT), which has the highest exposure to toll road projects. WSKT has been actively acquiring stakes in greenfield toll road projects with the aim of selling them after the construction works complete. This strategy has also been adopted by other listed contractors, albeit at a much less aggressive pace.

A timely and value-accretive divestment will be a positive catalyst for the contractors. In addition, we estimate that a potential new contract worth Rp80tr would come from JSMR. However, given JSMR’s hefty funding needs, the execution of its securitisation and divestment plans are important to ensure that its new projects would take off.

Industry Focus

Page 3

New contract growth to peak out; execution to take the

spotlight

The three state-owned contractors under our coverage booked Rp47.5tr worth of new contracts in 5M17, a 71% increase y-o-y. This was driven largely by SOE and to some extent private contracts. We nonetheless anticipate the new contract growth to slow down in the coming months with the three contractors only guiding for a 4% increase in new contracts for FY17.

5M17 new contracts

*based on management’s target Source: Company, AllianceDBS, DBSVI Among the three state-owned contractors under our coverage, PTPP is guiding for the highest new contract growth of 25%, coming from a relatively low base last year where it won Rp32.6tr new contracts over the year (vs. WSKT at Rp70tr and WIKA at Rp54.8tr). WSKT announced its ambitious new contract growth of 14% to Rp80tr after more than doubling its new contracts last year. This forecast is above our expectations. WSKT has been able to secure large order books in the past two years by shifting its business model from a pure civil contractor to toll road developer. The company currently owns 18 toll road concessions through its subsidiary Waskita Toll Road. We estimate that most of the construction contracts were awarded and included in WSKT’s 2016 order book. Unlike last year where its new contract target was relatively secured, the company has to resume its toll road acquisition spree. This means that a strong and sustainable new contract growth will likely come at the expense of its balance sheet strength. In our view, this is a key negative given its already poor operating cashflow. Meanhile, WIKA expects its new contracts to decline by 21% due to the high base last year where the company was

awarded the Rp15.8tr Jakarta-Bandung HSR civil works construction contract. As new contracts are peaking out this year, project execution and earnings delivery would take the spotlight. New contract trend

*based on management’s target Source: Company, AllianceDBS, DBSVI New contract growth trend

*based on management’s target Source: Company, AllianceDBS, DBSVI Due to the government’s fiscal constraint, the rule of the game has changed. In the past, contractors were largely dependent on government-funded projects (with the exception of PTPP which in the past won a number of projects from private property developers), specifically infrastructure projects under Ministry of Public Works and Housing and Ministry of Transportation. Nowadays, balance sheet strength is becoming increasingly important as more big-ticket projects are implemented using the Public-Private Partnership (PPP) scheme. That said, contractors typically had to acquire equity stakes in the project to be able to win the civil work contracts.

7.6 7.2 13.0 1.6

20.0 12.6 14.9 2.3

46%

31%

19%

33%

0%5%10%15%20%25%30%35%40%45%50%

-

5.0

10.0

15.0

20.0

25.0

WIKA PTPP WSKT WTON

Rp tr

5M16 new contracts 5M17 new contracts % of FY17 guidance (RHS)

17.6 20.2 22.6

60.5

25.3 27.0

32.1

84.4

54.8

32.6

70.0

157.4

43.2 40.6

80.0

163.9

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

WIKA PTPP WSKT Total

Rp tr

FY14A FY15A FY16A FY17F*

-1%

3%

70%

19%

43%34%

42% 40%

117%

21%

118%

87%

-21%

25%

14%4%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

WIKA PTPP WSKT Total

FY14A FY15A FY16A FY17F*

Industry Focus

Page 4

Government-funded projects that are up for bidding remain aplenty, but are more prone to delay, especially if the state’s revenue collection falls short of target. Meanwhile, the government’s strategy to decentralise its infrastructure budget from ministries to regional government also means a smaller chance for large-scale state-owned contractors, i.e. WIKA, PTPP and WSKT, to win the projects due to their relatively small ticket size, slower execution and tighter competition against regional players. New contracts from government-funded projects

Source: Company, AllianceDBS, DBSVI Contribution of government-funded projects* to total

new contract

*Excluding projects funded by SOE Source: Company, AllianceDBS, DBSVI Record-high order book to support revenue visibility On the positive side, the three contractors under our coverage are now sitting on a record-high order book. WSKT is leading with Rp92.9tr outstanding order book supported by the greenfield toll road acquisition spree by its 70%-owned subsidiary Waskita Toll Road. In second position is WIKA with

Rp76.2tr backlog contracts, of which 21% comes from the Jakarta-Bandung high-speed railway project (where WIKA has an effective stake of 23%). Meanwhile, PTPP has Rp58.1tr backlog contracts. Among the three contractors, PTPP’s order book is more diverse and least concentrated to a single or one type of project. Note that the majority of WKST’s order book are highly leveraged to toll road projects in Java while 21% of WIKA’s order book is from the Jakarta-Bandung high-speed railway project.

Contractors’ revenue visibility

*As et end of May 2017 Source: Company, AllianceDBS, DBSVI Land acquisition risk – same old story?

The three contractors under our coverage recorded a strong new contract growth of 86% y-o-y in FY16. Nonetheless, execution was slower than expected, particularly in 4Q16 with combined revenue of WSKT, WIKA and PTPP (ex-property and toll road operations) in the quarter only growing by 21% y-o-y, decelerating from the 40% growth booked in 9M16. The deceleration was mostly due to WIKA and PTPP, whose revenue ex-property grew by only 6% and 2% y-o-y respectively. Based on our checks, land acquisition issue remained the key hurdle as most of the contracts awarded in the past 12 months are land-intensive toll road projects. In our view, aside from technical issues, the project execution to some extent hinges on the disbursement of land acquisition funds. Our discussions with industry players suggest that land clearing process is typically faster when the funding is ready.

2.7

10.7 10.9 7.9

9.9 15.6

4.0

5.1

6.1

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2014A 2015A 2016A

Rp tr

WIKA WSKT PTPP

15%

35%

20%

24%

43%

31%

19%

30%

20% 22%

19% 21%

-

5%

10%

15%

20%

25%

30%

35%

40%

45%

WIKA WSKT PTPP Total

2014 2015 2016

76.2 58.1

92.9

22.8 21.9

37.7

3.3

2.7

2.5

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

-10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0

100.0

WIKA PTPP WSKT

(x)Rp tr

Outstanding order book* (LHS)Revenue FY17F (LHS)Outst. order book/revenue FY17F (RHS)

Industry Focus

Page 5

Under the 2016 revised state budget and 2017 state budget, the government allocated Rp16tr and Rp20tr respectively to fund land acquisitions for infrastructure projects. As at the time of writing, a large part of the budget has yet to be disbursed due to bureaucratic and regulatory hurdles. As a result, toll road concession owners are asked to cover for the land costs to speed up execution. Land acquisition bailout fund from project owners

Source: Company, AllianceDBS, DBSVI Our discussions with project owners suggest that reimbursement will likely take time as the claim must be verified by two government agencies, Audit Board (BPK) and State’s Asset Management Agency (BLU LMAN). It is also worth noting that the budget allocation can only cover 57% of land acquisition cost estimated by Ministry of Public Work and Housing. Hence, the concession owners will likely continue to pre-finance the shortage to speed up the project execution. We have highlighted that more capital is required by contractors to grow their order books – either to acquire some stakes in the infrastructure projects they bid for or to work under semi-turnkey or turnkey projects. Given the high capital needs, the disbursement of the land acquisition budget will help to ease the cash flow burden of the project owners and allow them and the contractors to execute more projects.

Projects up for bidding In our past report (Indonesia Construction: Bridging ASEAN connectivity gap through port build-out), we listed down a number of transport-based infrastructure projects in the government’s pipeline. Job opportunities remain aplenty for contractors given Indonesia’s massive need for infrastructure upgrade. We however note that funding remains a challenge

especially with fiscal deficit being capped at 3% by law. In addition, the government is no longer actively injecting capital into SOEs. Alternative funding such as Private-Public Partnership (PPP) is required to enable the project to take off, but bureaucratic bottlenecks and complexity of land acquisition issues may push these projects backward. The government may also be more active in leveraging on foreign funding in line with One Belt One Road where the Jakarta-Bandung High Speed Rail is being financed by the China Development Bank. We narrow down our list to a number of transport-based infrastructure projects that in our view are the most plausible to be executed in the next 12 months based on our checks with contractors and project owners. Toll road – Rp80tr potential new contracts in 2017-2019 The government continues its aggressive rollout of new toll road projects although toll roads entering land acquisition or construction phases already far exceed the initial goal of 1,000 km. At the end of last year, Indonesia’s leading toll road operator Jasa Marga (JSMR) announced its plan to further expand its toll road network by another 800 km. This toll road expansion plan, if realised, will translate to c. Rp80tr worth of new jobs for contractors in 2017-2019. In our previous sector reports, we had noted that among all infrastructure projects, toll roads have shown the best progress among all of the government’s infrastructure initiatives, supported by land acquisition reform, capital injection to infra-related SOEs and given the less complex designing and civil work process. Based on our discussion with JSMR, a number of new toll roads will be rolled out in the near future. However, due to JSMR’s hefty funding needs, most of the projects will adopt contractor pre-financing (CPF) scheme (also known as “turnkey”) where contractors will only receive the payment once the toll road construction is entirely completed. We see a risk that these projects would command a lower profit margin compared to non-CPF toll road projects won in the past due to the higher working capital requirement. Port – eyes on Patimban project Port projects, on the other hand, have moved slower than our expectation. Two key issues are funding and the higher complexity of the projects, particularly on the design. Two port projects are currently in the tender process with one of them being the mega Patimban port project in West Java

16.4

5.4

20.2

7.0 4.7

7.1

43%

86%

35%

-10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

-

5.0

10.0

15.0

20.0

25.0

Jasa Marga* Hutama Karya** Waskita Karya*

Rp tr

Total equity (LHS) Bailout fund (LHS) Bailout fund/total equity (RHS)

Industry Focus

Page 6

worth US$3bn (c. Rp40tr). Japan will likely finance most of the projects with the loan deal expected to be signed this year. Based on our channel check, local contractors can win at least 40% of the total contract value, or approximately Rp16tr, while the remaining will likely be awarded to foreign contractors, depending on the loan term. In a recent Belt and Road Forum in Beijing, there are also two port projects offered to China for financing, namely Kuala Tanjung port and Bitung port. The projects will comprise several phases. Both ports are estimated to cost Rp34tr each. High-speed and urban railway – some changes to the initial plans The likelihood of government expanding the planned Jakarta-Bandung high-speed railway network to Surabaya appears to be lower now. Instead, it is mulling over revitalising the existing railway by building an elevated track. Nevertheless, the potential new order book from this railway revitalisation project would still be sizeable at Rp80tr. The plan to build an LRT in Bandung was also called off. Based on our checks, the project will likely be replaced by metro capsule which has a lower investment cost (c. Rp1tr). Meanwhile, there has been a discussion on LRT development in Surabaya. A feasibility study for the project is currently taking place, however the contract size is estimated to only reach Rp3.8tr. Another urban railway project scheduled to start this year is MRT phase 2. The MRT track will be entirely underground and span 14 km from Hotel Indonesia Roundabout to Ancol. The project is estimated to cost at least Rp22.5tr. Note that WIKA has constructed 15% of the underground portion for the current Jakarta MRT line and should be a front runner for this portion.

We expect 2018 new contracts to start declining. New contracts of the big three state-owned contractors have surged from a mere Rp60.5tr in FY14 to Rp157.3tr in FY16, supported by higher government infrastructure spending, both through ministerial spending and the multiplier of capital injection to SOEs. In 2017, the big three state contractors only guided for a 4% y-o-y growth after almost doubling their new contracts y-o-y in 2016. With the government being less active in injecting capital into SOEs and given that the contractors already have a sizable outstanding order book to be delivered over the next 1-2 years, we think a further surge in new contracts is less likely.

On the subsequent page, we present our new contract estimates after taking into account the contribution from the central government’s annual capex spending. New contracts – what can surprise on the upside? For power plant projects, competition is tighter as state-owned contractors also compete with private players, both from local and foreign countries. As at end of December 2016, only power plants with total capacity of 14.6 GW were still in the initial phase (planning and procurement). Assuming US$1.5m investment per megawatt, this would translate to potential new contracts of Rp291.9tr. However, a big chunk of the investment is related to EPC while for the civil works, the size is typically less than 30% of the total investment. Given the high complexity of power plant projects and intense competition from more experienced foreign EPC players, we only take into account the civil works with 50% winning rate for the three contractors. An increase in winning rate is possible if the contractors actively participate as an equity investor in the power plant projects. Progress of 35 GW programme (as at end of 2016)

Source: PLN

Planning, 5,824

Procurement, 8,810

Power Purchase

Agreement, 10,063

Construction, 10,291

Operational, 707 Start

Industry Focus

Page 7

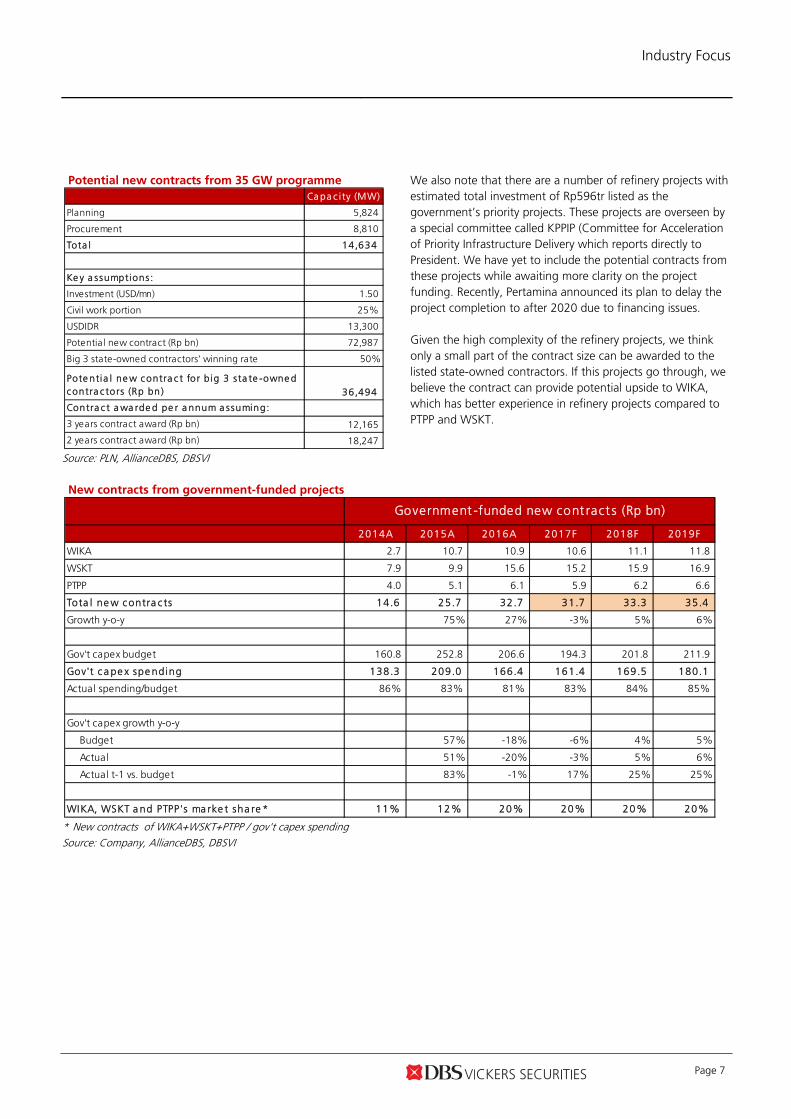

Potential new contracts from 35 GW programme

Source: PLN, AllianceDBS, DBSVI

We also note that there are a number of refinery projects with estimated total investment of Rp596tr listed as the government’s priority projects. These projects are overseen by a special committee called KPPIP (Committee for Acceleration of Priority Infrastructure Delivery which reports directly to President. We have yet to include the potential contracts from these projects while awaiting more clarity on the project funding. Recently, Pertamina announced its plan to delay the project completion to after 2020 due to financing issues. Given the high complexity of the refinery projects, we think only a small part of the contract size can be awarded to the listed state-owned contractors. If this projects go through, we believe the contract can provide potential upside to WIKA, which has better experience in refinery projects compared to PTPP and WSKT.

New contracts from government-funded projects

* New contracts of WIKA+WSKT+PTPP / gov't capex spending Source: Company, AllianceDBS, DBSVI

Ca pa c i ty (MW)

Planning 5,824

Procurement 8,810

Tota l 14,634

Ke y a ssumptions :

Investment (USD/mn) 1.50

Civil work portion 25%

USDIDR 13,300

Potential new contract (Rp bn) 72,987

Big 3 state-owned contractors' winning rate 50%

Pote ntia l ne w contra c t for b ig 3 s ta te -owne d contra c tors (Rp bn) 36,494

Contra c t a wa rde d pe r a nnum a ssuming:

3 years contract award (Rp bn) 12,165

2 years contract award (Rp bn) 18,247

2014A 2015A 2016A 2017F 2018F 2019F

WIKA 2.7 10.7 10.9 10.6 11.1 11.8

WSKT 7.9 9.9 15.6 15.2 15.9 16.9

PTPP 4.0 5.1 6.1 5.9 6.2 6.6

Tota l ne w contra c ts 14.6 25.7 32.7 31.7 33.3 35.4

Growth y-o-y 75% 27% -3% 5% 6%

Gov't capex budget 160.8 252.8 206.6 194.3 201.8 211.9

Gov't c a pe x spe nding 138.3 209.0 166.4 161.4 169.5 180.1

Actual spending/budget 86% 83% 81% 83% 84% 85%

Gov't capex growth y-o-y

Budget 57% -18% -6% 4% 5%

Actual 51% -20% -3% 5% 6%

Actual t-1 vs. budget 83% -1% 17% 25% 25%

WIKA, WSKT a nd PTPP's ma rke t sha re * 11% 12% 20% 20% 20% 20%

Government -funded new cont ract s (Rp bn)

Industry Focus

Page 8

Identifiable projects in 2017F – 2018F

Project Location Investment (Rp bn)

Toll road

Jasa Marga's toll road expansion plan Indonesia 80,000

Railway

Bandung-Surabaya railway revitalisation West Java, East Java 80,000

Bandung Metro Capsule West Java 1,000

Surabaya LRT East Java 3,800

Jakarta MRT Phase 2* Jakarta 3,375

Port

Patimban Port Stage 1 Phase 1* West Java 7,052

Kuala Tanjung Port Phase 2* North Sumatra 3,200

Power

2018F Indonesia 18,247

Government-funded projects

2018F state budget Indonesia 33,281

Total 229,955

2018F new contract assuming two years of contract award 149,955

New contracts

FY15A 84,380

FY16A 157,337

FY17F 159,787

FY18F 149,955

New contract growth y-o-y

FY16A 86%

FY17F 2%

FY18F -6%

* Civil work portion only Source: Company, various media sources, AllianceDBS, DBSVI

Industry Focus

Page 9

On to the next catalysts Below we highlight five upcoming events and two mega projects that will likely become the key catalysts for the sector and the individual companies. 1) 2018 Fiscal Budget proposal (August 2017)

The government is scheduled to submit the budget proposal to parliament in August 2017. The amount the government allocates for infrastructure development and state-owned enterprises (if any) will be important to gauge the direction of contractors’ order book growth in 2018.

2) Waskita Toll Road divestment WSKT plans to further divest its stake, while Waskita Toll Road also plans to sell 3-4 toll roads this year. The contractor has shifted its business model to become a toll road developer, which is highly capital intensive. While the impact on WSKT will depend on the toll road’s valuation, the divestment proceeds should help to ease WSKT’s cash flow burden.

3) CDB loan disbursement for Jakarta-Bandung high-speed railway (HSR) project The construction of Jakarta-Bandung HSR has come to a halt after the groundbreaking ceremony in January 2016 due to prolonged delay on financial close. The loan agreement was finally signed in May 2017. Nonetheless, the disbursement will be pending the verification of land acquisition progress by an independent auditor. WIKA, which leads the local consortium for the project, expects the loan to be disbursed and the construction works to resume in July 2017. The resumption of the project will be positive for both WIKA and WTON.

4) PTPP’s 2Q17 earnings release

After recording a weaker-than-expected construction revenue in the past two consecutive quarters mainly due to land acquisition issue, 2Q17 will be an important quarter to regain investor’s confidence on PTPP’s ability to execute its large outstanding order book. In May 2017 analyst briefing, the management assured investors that the revenue should catch up in 2Q17 with a target revenue of Rp10tr in 1H17. This implies Rp7.1tr revenue target in 2Q17 vs. Rp2.9tr achieved in 1Q16.

5) Jasa Marga’s securitisation and subsidiary IPO plan JSMR is planning to expand its toll road network up to 800 km by 2019, on top of the c. 600 km greenfield toll roads in its existing pipeline. Due to the hefty investment needed, any fund-raising activities, particularly the securitisation of its mature toll roads and divestment of its subsidiaries, will help to ensure that its existing and upcoming pipelines can be executed timely.

6) Patimban port The location of Patimban port has been approved by the government. More clarity on the project should come after the signing of the loan commitment from Japan, which is expected to take place in July 2017. The tender of the project is ongoing. Based on our checks, two contractors under our coverage, PTPP and WIKA, are vying for the project.

7) Jakarta-Surabaya railway revitalisation Given the sizeable project size, that is Rp80tr or approximately 51% of the combined FY16 new contract achievement of WIKA, PTPP and WSKT, more clarity on the project would be positive catalyst for the sector.

Industry Focus

Page 10

What is consensus expecting?

Consensus is expecting 47% y-o-y revenue growth in FY17 for the big three state-owned contractors with net profit growing slower at 33% y-o-y. As a comparison, the big three state-owned contractors booked 34% y-o-y revenue growth and 54% headline net profit growth in FY16. Current consensus’ earnings forecasts imply an expectation that consolidated EBIT and net margin would shrink in FY17. A similar trend was also implied on consensus’ 2018 earnings forecast. We believe this is because the consensus expects competition among contractors to tighten, coupled with higher financing needs. The magnitude of net margin decline in 2017 based on consensus expectation is the largest on WSKT, followed by WIKA. Consensus’ 2017 net profit revision

Source: Bloomberg Finance L.P Consensus’ 2018 net profit revision

Source: Bloomberg Finance L.P

Valuation and recommendation

Construction sector’s 12-month forward PE

Source: Bloomberg Finance L.P, AllianceDBS, DBSVI Construction sector’s 12-month forward PE relative to JCI

Source: Bloomberg Finance L.P, AllianceDBS, DBSVI

We are turning Neutral on Indonesia’s construction sector from Positive previously. The sector’s PE multiple has derated significantly in the past few months. However, we do not see any significant catalyst that will support a broad-based upward re-rating in the near future. We expect new contract growth to decelerate in the coming months and we think government-funded projects are unlikely to provide significant upside potential to our order book forecasts as the government continues to decentralise infrastructure development. As the government seeks funding alternatives and push the PPP scheme, capital requirement to win a project will continue to rise up to the point where contractors have to choose between growing their order books (at the expense of higher interest expense and margins) or coping with a declining order book. We like PTPP due to its attractive valuation and promising growth outlook. The company now trades at 0.34x EV/order

28%27%

15%

-6%

16%

6%

1%-1%1%

-3%

3%

-0.2%

0%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

WSKT WIKA PTPP WTON

Past 12 months YTD Post FY16 audited results Post 1Q17 results

28%

12%

17%

-18%

14%

5%

-1%

1% -4% 3%-1%

-20%

-10%

0%

10%

20%

30%

40%

WSKT WIKA PTPP WTON

Past 12 months YTD Post FY16 audited results Post 1Q17 results

5

10

15

20

25

30

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

+2sd

+1sd

‐1sd

‐2sd

Avg.

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

5

10

15

20

25

30

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Construction PE premium to JCI (RHS) Construction PE

JCI PE Avg. construction PE premium to JCI (RHS)

Industry Focus

Page 11

book, lower than WSKT at 0.61x. It is also worth noting that PTPP has a smaller capex commitment compared to WSKT, and a relatively less leveraged balance sheet to support its future earnings and new contract growth. We forecast PTPP’s net profit to grow at a CAGR of 27% in 2016A-2018F. While WIKA’s EV/order book multiple is on par with PTPP, it is now trading at 17.5x 17F PE (vs. PTPP at 15.4x 17F PE). Given the higher PE multiple and downside risk on earnings, we prefer to wait for the Jakarta-Bandung HSR progress to accelerate before turning more positive on the stock. As work on the projects commence, WTON is in a sweet spot as it starts to receive new orders from contractors/project owners. We view WTON as a good proxy to the infrastructure sector given its strong presence across Indonesia. EV/order book

*As at end of March 2017; ** As of 5 July 2017 Source: Company, AllianceDBS, DBSVI Gross and net gearing*

*As at end of March 2017 Source: Company, AllianceDBS, DBSVI

Where we differ

We are less bullish on the sector compared to the street, particularly on WIKA and WSKT. The consensus Buy call on all listed state-owned contractors (refer to the table below) suggests that a broad-based execution improvement is expected to lift the share prices of all state-owned contractors. On the contrary, given the peaking new contract growth and differing risk profile among the contractors, we believe selective investing in the sector is the best approach. DBS vs. consensus’ recommendation

Source: AllianceDBS, DBSVI, Bloomberg Finance L.P. Our FY17 net profit forecasts for WIKA and WSKT are one of the lowest on the street. We have a HOLD call among consensus Buy calls on both companies. WIKA. WIKA’s FY17 net profit largely depends on the construction progress of Jakarta-Bandung high-speed railway. Assuming 6.3% net margin and 37% progress for FY17, the project (ex-precast) should contribute Rp183bn net profit to WIKA or 30% of management’s net profit target for FY17. We see downside risk on WIKA’s net profit given that the construction work is expected to resume only in July 2017. Our FY17 net profit forecast for WIKA is 9% lower than consensus as we expect higher capital requirement and debt to support its new contract and earnings growth. WSKT. Our net profit forecasts for WSKT are 9%/27% lower relative to consensus as we have factored in potential start-up losses from its toll road business. Summary of net profit forecast changes

Source: AllianceDBS, DBSVI

76.2 58.1 92.9 20.0 19.9

56.8 0.26 0.34

0.61

0.41

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

-

20.0

40.0

60.0

80.0

100.0

WIKA PTPP WSKT Avg.

(x)Rp tr

Outstanding order book* (LHS) EV** (LHS) EV/outst. order book* (RHS)

0.54 0.47

1.28

0.32

-0.08 -0.16

0.83

0.25

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

WIKA PTPP WSKT WTON

Gross gearing Net gearing

BUY HOLD SELL

WIKA 32 25 7 0 HOLDPTPP 29 29 0 0 BUYWSKT 29 25 4 0 HOLDWTON 16 14 1 1 BUY

No. of a na lyst

Conse nsus ' re c omme nda tion DBS' re c omme nda tion

Old New Change Old New Change

WSKT 1,824 2,168 19% 1,745 2,209 27%

WIKA 1,111 1,140 3% 1,530 1,595 4%

PTPP 1,331 1,341 1% 1,645 1,644 0%

WTON 366 366 0% 418 418 0%

A ggregate 4,632 5,016 8% 5,338 5,865 10%

F Y17F net prof it F Y18F net prof it

Industry Focus

Page 12

Summary of recommendation and TP changes

Source: AllianceDBS, DBSVI

DBS’s net profit forecast relative to consensus

Source: AllianceDBS, DBSVI, Bloomberg Finance L.P

Key risks

Delay in project execution due to technical, land acquisition and funding issues, and bureaucratic hurdle. Tax revenue shortfall. The government has set a target to increase tax revenue by 17% this year to Rp1,499tr. Failure to meet this target could lead to spending cuts and delays in project execution. Political headwinds. Conflicting interest between government and opposing parties may impede reform momentum. A case in point is the delay in SOE capital injection last year. Tightening competition among contractors, especially in 2018 where we project aggregate new contracts to decline. This may lead to a drop in margins. Further slowdown in property sector. PTPP, and to a lesser extent WIKA, have exposure to the property sector.

Old New Change

WSKT 2,950 2,400 -19% Maintain Hold

WIKA 2,780 2,050 -26% Maintain Hold

PTPP 4,950 4,100 -17% Maintain Buy

WTON 1,050 760 -28% Maintain Buy

T arget PriceRecommendat ion

0.92 0.91 0.99 0.99

0.73

1.05 0.96 0.94

-

0.20

0.40

0.60

0.80

1.00

1.20

WSKT WIKA PTPP WTON

FY17F

FY18F

Industry Focus

Page 13

Valuation summary

*Non-rated; based on Bloomberg consensus **Order book as at end of May 2017 Source: AllianceDBS, DBSVI, Bloomberg Finance L.P

M arketC ap P rice R ec. T P EP S C A GR EV/ N et

( ID R bn) ( ID R ) F Y17 F Y18 F Y17 F Y18 F Y17 F Y18 F Y17 F Y18 F Y16A -18F

o rder bo o k**

Gearing(x)

Wijaya Karya 19,913 2,270 HOLD 2,050 17.5 12.5 1.6 1.5 9.1 7.4 10% 12% 6% 0.26 Net Cash

PT PP (Persero) 20,646 3,330 BUY 4,100 15.4 12.6 1.9 1.7 8.6 7.4 13% 14% 12% 0.34 Net Cash

Waskita Karya 30,813 2,270 HOLD 2,400 14.2 13.9 2.4 2.1 13.0 12.4 18% 16% 14% 0.61 0.83

Adhi Karya* 7,763 2,180 N/R N/A 12.8 8.8 1.3 1.1

Wijaya Karya Beton 5,273 605 BUY 760 14.4 12.6 1.9 1.7 8.4 7.4 14% 15% 24% 1.07 0.25

Simple average 14.8 12.1 1.8 1.6 9.7 8.7 14% 14%

Weighted average 15.1 12.7 2.0 1.7 9.5 8.6 13% 13%

P / B (x)

D ilutedP E (x)

EV/EB IT D A (x) R OA E

Industry Focus

Page 14

Company Guides

ASIAN INSIGHTS VICKERS SECURITIES ed: JS / sa:MA, PY

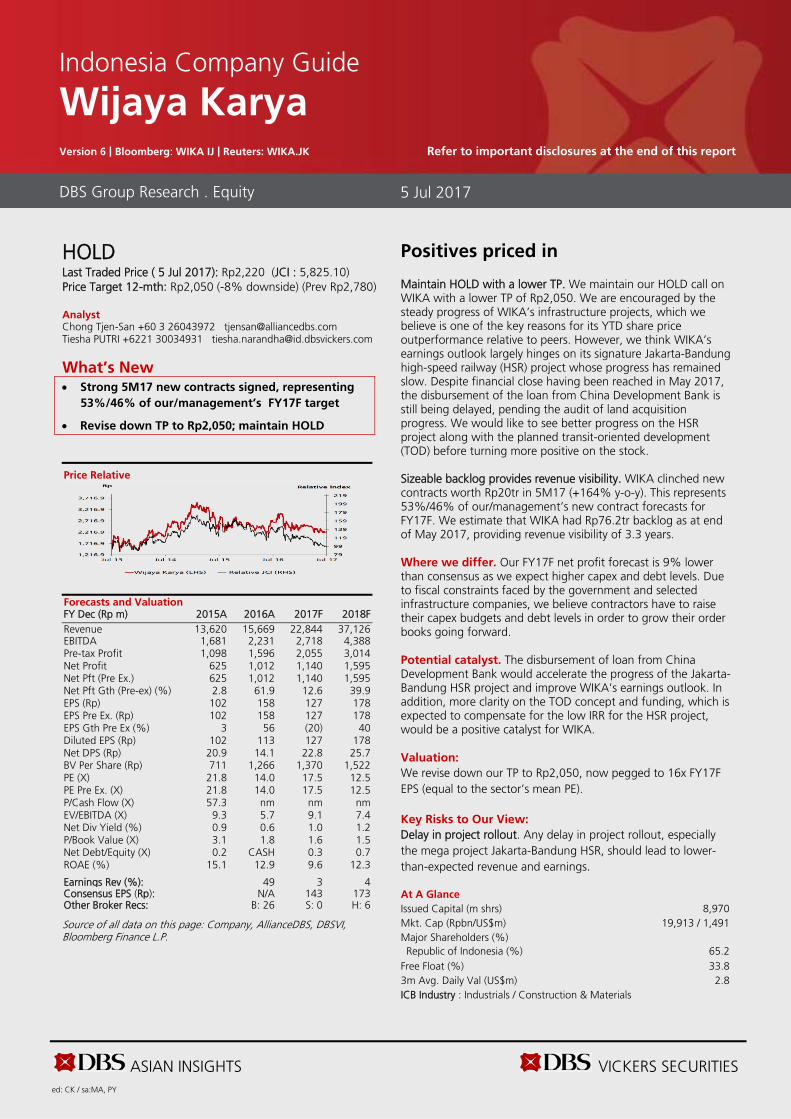

HOLD

Last Traded Price ( 5 Jul 2017): Rp2,270 (JCI : 5,865.40) Price Target 12-mth: Rp2,400 (6% upside) (Prev Rp2,950) Analyst Chong Tjen-San +60 3 26043972 [email protected] Tiesha PUTRI +6221 30034931 [email protected]

What’s New Funding risk reduced post sale of stake in Waskita

Toll Road but further fund raising required

Maintain HOLD with a lower SOP-based TP of

Rp2,400

Toll road divestment is key catalyst

Price Relative

Forecasts and Valuation FY Dec (Rp m) 2015A 2016A 2017F 2018F Revenue 14,153 23,788 37,666 49,997 EBITDA 2,041 3,527 5,332 6,674 Pre-tax Profit 1,398 2,481 3,688 4,113 Net Profit 1,048 1,713 2,168 2,209 Net Pft (Pre Ex.) 955 1,713 2,168 2,209 Net Pft Gth (Pre-ex) (%) 90.4 79.4 26.6 1.9 EPS (Rp) 77.2 126 160 163 EPS Pre Ex. (Rp) 70.4 126 160 163 EPS Gth Pre Ex (%) 35 79 27 2 Diluted EPS (Rp) 77.2 126 160 163 Net DPS (Rp) 15.4 25.2 32.0 32.5 BV Per Share (Rp) 703 816 950 1,081 PE (X) 29.4 18.0 14.2 13.9 PE Pre Ex. (X) 32.3 18.0 14.2 13.9 P/Cash Flow (X) 46.8 nm nm nm EV/EBITDA (X) 16.4 14.5 13.0 12.4 Net Div Yield (%) 0.7 1.1 1.4 1.4 P/Book Value (X) 3.2 2.8 2.4 2.1 Net Debt/Equity (X) 0.3 0.9 1.7 2.1 ROAE (%) 17.0 16.6 18.1 16.0 Earnings Rev (%): 7 19 27 Consensus EPS (Rp): N/A 181 230 Other Broker Recs: B: 25 S: 0 H: 4

Source of all data on this page: Company, AllianceDBS, DBSVI, Bloomberg Finance L.P

Further fund raising needed Funding risk reduced post sale of stake in Waskita Toll Road but further fund raising is needed. Waskita Karya (WSKT) has shifted to a more capital-intensive business model with 18 toll road concessions in its portfolio (of which 10 concessions are majority owned by WSKT through Waskita Toll Road or WTR). Hefty funding will be required to keep growing its order book and earnings at the current pace. WSKT recently raised Rp3.5tr cash through a 29% stake sale in WTR to SMI and a state-owned pension fund Taspen. We view this positively as it would help to reduce funding concerns and ease potential start-up losses. Nonetheless, further fund raising or divestments would be needed. Post divestment to Taspen and SMI, we estimate that WSKT would still need more than Rp7.2tr cash to fund its equity portion for its toll road concessions over the next three years. Where we differ. We are one of the few houses in the market with a HOLD call compared to Buy calls on the stock. Our earnings forecast for FY17F/FY18F are 8%/27% below consensus as we have factored in potential start-up losses from WSKT’s toll road business. We are also concerned on its persistent negative operating cash flow arising from increasing contribution of turnkey projects. We believe consensus may be over estimating the ease of further equity raising to fund its toll road expansion. This is especially in light of diminishing prospects of more capital injections by the government. Potential catalysts. WSKT plans to further divest its stake in WTR, while its subsidiary Waskita Toll Road also plans to sell 3-4 toll roads this year. While the impact on WSKT will depend on the toll road’s valuation, divestment proceeds should help to ease WSKT’s cash flow burden. Valuation:

We valued WSKT’s construction business at 10x FY17F EPS (-1.5SD below sector historical mean PE), precast business at 15x FY17F EPS and toll road concessions using the DCF method. Our sum-of-the-parts TP of Rp2,400 implies 15x FY17F PE. Key Risks to Our View:

Failure to divest its toll roads could result in lower earnings and an overstretched balance sheet. At A Glance Issued Capital (m shrs) 13,574 Mkt. Cap (Rpbn/US$m) 30,813 / 2,306 Major Shareholders (%) Republic of Indonesia 68.0

Free Float (%) 32.0 3m Avg. Daily Val (US$m) 2.7 ICB Industry : Industrials / Construction & Materials

DBS Group Research . Equity 5 Jul 2017

Indonesia Company Guide

Waskita Karya Version 6 | Bloomberg: WSKT IJ | Reuters: WSKT.JK Refer to important disclosures at the end of this report

ASIAN INSIGHTS VICKERS SECURITIES Page 16

Company Guide

Waskita Karya

WHAT’S NEW

Cutting TP to Rp2,400; further toll road divestment is key catalyst

Order book at record high, boosting its revenue visibility to 2.5 years. We estimate WSKT’s outstanding order book stood at Rp92.9tr as at end of May 2017 after winning Rp14.9tr worth of new contracts in 5M17. WSKT’s sizeable backlog which mainly comprises of Trans Java toll roads and Palembang LRT offers revenue visibility for 2.5 years.

Revised up new contract assumptions and earnings. Due to the strong new contract flows in 4Q17, we raised our FY17F new contract assumption to Rp78tr (from Rp40tr previously). With a higher order book, we revised up our FY17F/FY18F net profit by 19%/27%. Despite the upward revision, our earnings forecast for FY17F/FY18F are 8%/27% below consensus as we have factored in potential start-up losses from WSKT’s toll road business.

Cutting TP to Rp2,400. We updated our sum of parts (SOP) valuation, resulting in a lower TP of Rp2,400, from Rp2,950 previously. We value WSKT’s ex-precast and toll road business at 10x PE 17F (1.5SD below sector’s historical mean). Our PE multiple is at discount to sector’s historical mean PE given the nature of WSKT’s business where the big chunk of the construction earnings can only be converted to cash upon the divestment of its toll road concession.

We pegged Waskita’s precast business, WSBP, at 15x PE FY17F, a 20% discount to our target multiple for Wijaya Karya Beton (WTON). We think the discount is justified

because of its smaller geographical presence, less extensive product range and narrower clientele. Lastly, we value WSKT’s toll road concessions using DCF. We apply 10% WACC and 0% long-term growth as we run our DCF until the end of the concession period. Note that we have yet to take into account WSKT’s five newly acquired toll roads into our calculation i.e. Kuala Tanjung – Tebing Tinggi – Parapat (143 km), Cileunyi – Sumedang – Dawuan (60 km), Cibitung – Cilincing (35 km), Krian – Legundi – Blunder – Manyar (38 km) and Kaya Agung – Palembang – Betung (112 km), as we await more details on these concessions.

Looking beyond this year’s strong earnings outlook. We maintain our Hold call on WSKT. We think the stock is fairly valued at current price, trading at 14.2x 17F PE with net profit CAGR of 14% in 2016-2018F. Despite the strong earnings growth outlook this year (we forecast 27% net profit growth in FY17F), we reserve our concern over the company’s cash flow generation and its high capex commitment to fund its toll road concessions. We believe hefty funding is needed to keep growing its order book and earnings at the current pace. Further divestment of its toll road concession at a favourable price is key catalyst for the stock.

Operating cash flow and capex trend and forecasts

Source: Company, AllianceDBS, DBSVI

Gearing trend and forecasts

Source: Company, AllianceDBS, DBSVI

WSKT’s sum of parts (SOP) valuation

Equity value

(Rp bn)

WSKT's effective

ownership

Equity value (adj. to

ownership)

Equity value per share % of TP Remarks

WSKT ex-precast and toll road business

18,118 100% 18,118 1,335 56% Based on target PE of 10x; -1.5SD below sector historical mean

Precast (WSBP IJ) 14,389 60% 8,633 636 27% Based on target PE of 15x

Toll road (WTR) 5,366 395 16% DCF; 10% WACC

Target price (Rp/share) 2,400

Implied PE 17F (x) 15.0

Source: AllianceDBS, DBSVI

(89) 658

(7,762)

(3,201)(1,747)

1,210

7,086 6,261

13,983

10,661

(10,000)

(5,000)

0

5,000

10,000

15,000

20,000

2014A 2015A 2016A 2017F 2018F

Rp bn

Operating cash flow Capex

0.54

0.26

0.87

1.68

2.05

1.14

0.83

1.50

1.84 2.10

-

0.50

1.00

1.50

2.00

2.50

2014A 2015A 2016A 2017F 2018F

(x)

Net gearing Gross gearing

ASIAN INSIGHTS VICKERS SECURITIES Page 17

Company Guide

Waskita Karya

Earnings revision

2017F 2018F

Old New % change Old New % change

Revenue 32,055 37,666 18% 37,900 49,997 32%

Gross profit 4,687 6,111 30% 5,381 7,699 43%

EBIT 3,767 4,932 31% 4,281 6,141 43%

Net Profit 1,824 2,168 19% 1,745 2,209 27%

GP margin (%) 14.6 16.2 14.2 15.4

EBIT margin (%) 11.8 13.1 11.3 12.3

Net margin (%) 5.7 5.8 4.6 4.4

New contracts (Rp bn) 40,000 78,000 95% 25,000 67,939 172%

Cum. order book (Rp bn) 116,219 155,514 34% 114,361 184,788 62%

Net interest exp. 641 1,245 94% 783 2,029 159%

Source: AllianceDBS, DBSVI

ASIAN INSIGHTS VICKERS SECURITIES Page 18

Company Guide

Waskita Karya

CRITICAL DATA POINTS TO WATCH

Critical Factors

A shift in business model. Following the toll road acquisition spree over the past two years, WSKT has shifted its business model to become more of a toll road developer from a pure civil contractor previously. The company would continue to acquire greenfield toll road concessions in the foreseeable future, build them and divest the stakes after the construction is completed to free up capital. This way, it would be able to secure profit in a shorter time span compared to if it operates the toll roads over the concession period on its own, as the company would be able to reap gains from both the civil work (during construction phase) and the asset divestment. Its subsidiary Waskita Toll Road is the majority stakeholder for nine toll road concessions in Java and one in Sumatra with a total investment value of Rp65tr. It also owns minority stakes in eight other toll road concessions. All eyes on toll road divestment. The change in business model makes toll road divestments crucial for WSKT given the high capital requirements to build the toll roads. Assuming a capital structure of 70% debt and 30% equity for its toll roads, we estimate that WSKT would need to raise Rp7.2tr cash over the next three years to fund its equity stakes. With the current shareholding structure of Waskita Toll Roads, we estimate WSKT would have to raise debt by c.Rp25tr. This would further exacerbate its weak operating cash flow position. Given the potential surge in interest expense, its earnings outlook could be at risk. We believe toll road divestments will remain a key focus from 2017 onwards. New wins from government or external parties. The award of new contracts had been a key positive driver of WSKT’s share price. This was evident where the strong growth in new contracts in 2015-2016 drove the shares’ outperformance in the same period. However, we think the concern over the sustainability of its new contract wins has outweighed the excitement over its recent new contract wins, especially since most of the growth in its order book has been driven by its internal toll road projects instead of the government or external projects. Note that internal toll road projects are riskier in nature as the profit would only fully translate into cash upon the divestment of the concessions – a process that would likely take additional time. This has caused WSKT’s share price to underperform the market despite the company’s relatively strong new contract and earnings growth (refer to Appendix 1) in the past few months.

New Contract Wins (Rp bn)

Carry Over Contract (Rp bn)

Construction Gross Margin (%)

Source: Company, AllianceDBS, DBSVI

ASIAN INSIGHTS VICKERS SECURITIES Page 19

Company Guide

Waskita Karya

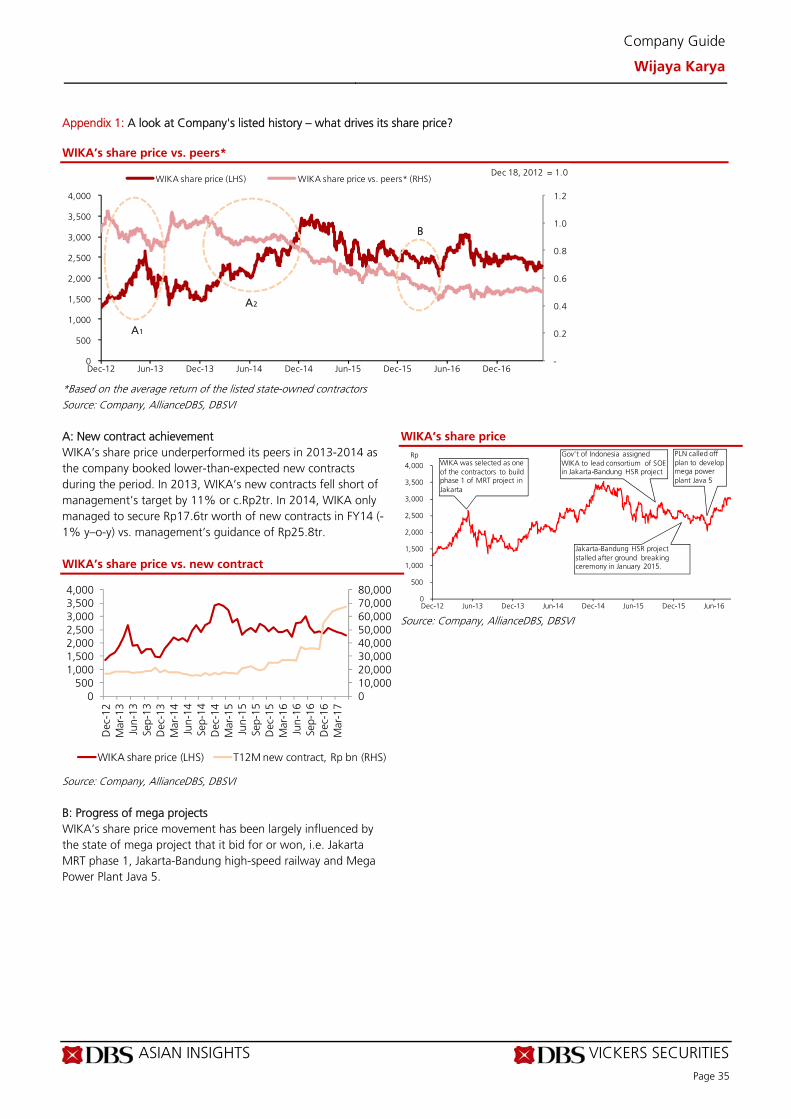

Appendix 1: A look at the company's listed history – what drives its share price?

WSKT share price vs. peers*

*Based on the average return of the listed state-owned contractors Source: Company, AllianceDBS, DBSVI A: Rupiah fluctuation WSKT’s share price was hit by concerns over profitability after the sharp depreciation of Rupiah in mid-2013. Investors saw infra project’s cost overrun as a key risk, which could lead to a decline in contractors’ profitability. The risk was deemed higher on WSKT as it was more reliant on government contracts compared to peers. WSKT’s share price vs. Rupiah

Source: Bloomberg Finance L.P. B: Share price moved in line with new contract growth WSKT’s new contracts grew strongly by 70% y-o-y in FY16, outperforming its peers, PT PP (PTPP) and Wijaya Karya (WIKA), whose new contracts were flat y-o-y.

WSKT’s share price vs. growth in new contracts

Source: Company, AllianceDBS, DBSVI, Bloomberg Finance L.P. C: Earnings momentum The company delivered strong earnings in 1H16, fueled by enlarged capital post rights issue. In addition, strong earnings momentum (with consensus upgrading earnings forecasts by 43% in the same period) led to a rally in its share price. WSKT’s share price vs. consensus’ earnings forecasts

Source: Bloomberg Finance L.P.

-

0.5

1.0

1.5

2.0

2.5

0

500

1,000

1,500

2,000

2,500

3,000

Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16

WSKT share price (LHS) WSKT share price vs. peers* (RHS)Dec 18, 2012 = 1.0

AB

C

D

E

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

0

100200

300

400500

600

700800

900

WSKT share price (LHS) USDIDR (RHS)

-50%

0%

50%

100%

150%

200%

-

500

1,000

1,500

2,000

2,500

3,000

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

WSKT share price (LHS) T12M new contract growth y-o-y (RHS)

50

70

90

110

130

150

170

190

1,000 1,200 1,400 1,600 1,800 2,000 2,200 2,400 2,600 2,800 3,000

WSKT share price (LHS) Consensus EPS 16F (RHS) Consensus EPS 17F (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 20

Company Guide

Waskita Karya

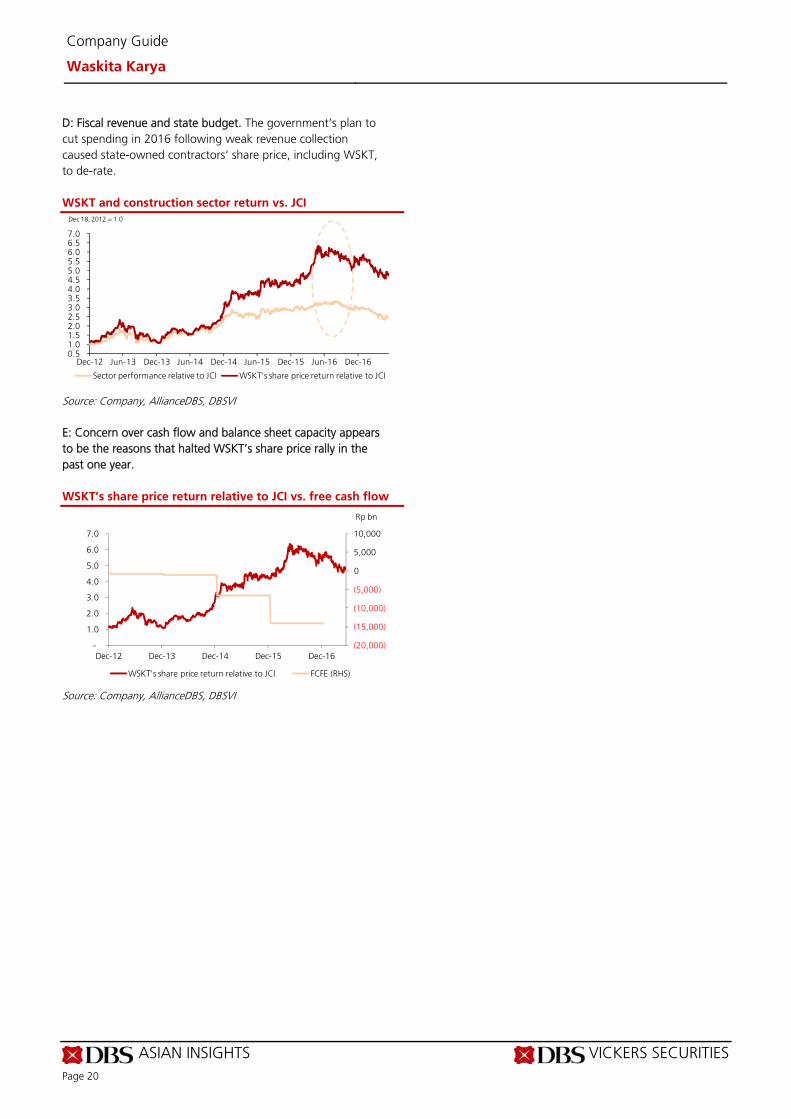

D: Fiscal revenue and state budget. The government’s plan to cut spending in 2016 following weak revenue collection caused state-owned contractors’ share price, including WSKT, to de-rate.

WSKT and construction sector return vs. JCI

Source: Company, AllianceDBS, DBSVI E: Concern over cash flow and balance sheet capacity appears to be the reasons that halted WSKT’s share price rally in the past one year. WSKT’s share price return relative to JCI vs. free cash flow

Source: Company, AllianceDBS, DBSVI

0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5 6.0 6.5 7.0

Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16

Sector performance relative to JCI WSKT's share price return relative to JCI

Dec 18, 2012 = 1.0

(20,000)

(15,000)

(10,000)

(5,000)

0

5,000

10,000

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

Rp bn

WSKT's share price return relative to JCI FCFE (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 21

Company Guide

Waskita Karya

Balance Sheet:

Further fund raising needed. As at end-March 2017, WSKT had a net debt of Rp6.7tr, translating to gross and net gearing of 1.28x and 0.83x respectively. We expect its debt to rise as the company extends its business model to include the capital-intensive toll road operating business and expansion of its precast business. Management has budgeted Rp32tr capex this year, most of which is for toll road expansion. Share Price Drivers:

Award of large-sized infrastructure contracts. The award of large-sized, multi-year projects will improve WSKT’s revenue and earnings visibility, and ultimately lead to an upward re-rating of its share price. Toll road divestment. After divesting a 29% stake in Waskita Toll Road to SMI and Taspen, WSKT is planning to raise more funds by further divesting its stakes in WTR and conducting rights issue. Both corporate actions are targeted to take place this year and are crucial for WSKT given its high capex needs. Key Risks:

Persistently weak operating cash flow. We have yet to see positive operating cash flows at WSKT despite strong contract wins last year. Its venture into the toll road operating business could also deteriorate WSKT’s operating cash flow during the early years of operations. As such, its balance sheet could remain stretched, forcing it to make another rights or bond issue in the future. Delay in toll road divestment. A delay in toll road divestment would be negative for WSKT. As it continues to acquire new greenfield toll road concessions to grow its order book, a timely fund raising is needed to make sure that the projects do not stall due to cash flow constraints. Company Background

PT Waskita Karya Tbk (WSKT) is a state-owned contractor engaged in a wide variety of construction activities including toll roads, bridges, ports and buildings. It is the most leveraged proxy to the Indonesian construction sector, deriving c. 95% of its revenues from construction.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, AllianceDBS, DBSVI

Rpbn

ASIAN INSIGHTS VICKERS SECURITIES Page 22

Company Guide

Waskita Karya

Key Assumptions

FY Dec 2014A 2015A 2016A 2017F 2018F New Contract (Rp bn) 22,625 32,084 69,974 78,000 67,940 Carry Over Contr. (Rp bn) 10,516 19,746 34,049 77,514 116,849 Construction GPM (%) 10.1 13.0 16.1 15.0 14.0 Precast Gross Margin (%) 18.2 15.9 22.2 20.0 19.0 Toll road start-up losses (287) (1,282)

Segmental Breakdown

FY Dec 2014A 2015A 2016A 2017F 2018F Revenues (Rpbn) Construction 9,484 12,052 22,373 30,120 40,340 Building rentals/Property 0.30 0.60 46.8 46.8 46.8 Precast 803 2,069 1,149 7,219 8,862 Energy 0.0 0.0 1.80 0.0 0.0 Others 0.0 31.8 218 280 748 Total 10,287 14,153 23,788 37,666 49,997 Gross Profit (Rpbn)

Construction 963 1,561 3,591 4,518 5,648 Building rentals/Property 0.30 0.60 17.7 17.7 17.7 Precast 146 328 255 1,444 1,684 Energy 0.0 0.0 1.70 0.0 0.0 Others 0.0 0.0 102 131 350 Total 1,109 1,889 3,968 6,111 7,699 Gross Profit Margins (%)

Construction 10.1 13.0 16.1 15.0 14.0 Building rentals/Property 99.7 100.0 37.9 37.9 37.9 Precast 18.2 15.9 22.2 20.0 19.0 Energy N/A N/A 94.9 N/A N/A Others N/A 0.0 46.8 46.8 46.8 Total 10.8 13.4 16.7 16.2 15.4

Income Statement (Rpbn)

FY Dec 2014A 2015A 2016A 2017F 2018F Revenue 10,287 14,153 23,788 37,666 49,997 Cost of Goods Sold (9,178) (12,232) (19,821) (31,555) (42,298) Gross Profit 1,109 1,921 3,968 6,111 7,699 Other Opng (Exp)/Inc (431) (518) (788) (1,179) (1,558) Operating Profit 678 1,403 3,180 4,932 6,141 Other Non Opg (Exp)/Inc 20.5 159 103 0.0 0.0 Associates & JV Inc 197 10.1 (7.4) 0.0 0.0 Net Interest (Exp)/Inc (140) (267) (795) (1,245) (2,029) Exceptional Gain/(Loss) 0.0 92.8 0.0 0.0 0.0 Pre-tax Profit 756 1,398 2,481 3,688 4,113 Tax (254) (350) (667) (1,019) (888) Minority Interest 0.30 0.10 (99.8) (500) (1,016) Preference Dividend 0.0 0.0 0.0 0.0 0.0 Net Profit 502 1,048 1,713 2,168 2,209 Net Profit before Except. 502 955 1,713 2,168 2,209 EBITDA 934 2,041 3,527 5,332 6,674 Growth Revenue Gth (%) 6.2 37.6 68.1 58.3 32.7 EBITDA Gth (%) 27.3 118.5 72.9 51.2 25.2 Opg Profit Gth (%) 18.9 106.9 126.6 55.1 24.5 Net Profit Gth (Pre-ex) (%) 36.3 90.4 79.4 26.6 1.9 Margins & Ratio Gross Margins (%) 10.8 13.6 16.7 16.2 15.4 Opg Profit Margin (%) 6.6 9.9 13.4 13.1 12.3 Net Profit Margin (%) 4.9 7.4 7.2 5.8 4.4 ROAE (%) 19.7 17.0 16.6 18.1 16.0 ROA (%) 4.7 4.9 3.7 3.0 2.4 ROCE (%) 8.2 7.8 7.1 6.9 7.5 Div Payout Ratio (%) 20.0 20.0 20.0 20.0 20.0 Net Interest Cover (x) 4.8 5.3 4.0 4.0 3.0

Source: Company, AllianceDBS, DBSVI

Revenue contribution from toll road operation business.

ASIAN INSIGHTS VICKERS SECURITIES Page 23

Company Guide

Waskita Karya

Quarterly / Interim Income Statement (Rpbn)

FY Dec 1Q2016 2Q2016 3Q2016 4Q2016 1Q2017 Revenue 3,072 5,013 5,923 9,780 7,142 Cost of Goods Sold (2,552) (4,043) (4,986) (8,239) (6,107) Gross Profit 520 970 937 1,541 1,034 Other Oper. (Exp)/Inc 58.2 (143) (114) (430) (45.4) Operating Profit 578 827 823 1,111 989 Other Non Opg (Exp)/Inc (151) (1.5) 26.1 70.2 (90.9) Associates & JV Inc (35.2) 27.4 (14.3) 14.7 6.90 Net Interest (Exp)/Inc (132) (190) (225) (249) (287) Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0 Pre-tax Profit 260 663 610 947 618 Tax (136) (205) (105) (222) (168) Minority Interest 3.20 0.80 (157) 53.4 (43.1) Net Profit 127 459 348 779 407 Net profit bef Except. 127 459 348 779 407 EBITDA 447 900 906 1,273 1,004 Growth Revenue Gth (%) (54.4) 63.2 18.2 65.1 (27.0) EBITDA Gth (%) (65.0) 101.3 0.7 40.5 (21.1) Opg Profit Gth (%) (26.1) 43.1 (0.4) 35.0 (11.0) Net Profit Gth (Pre-ex) (%) (78.0) 260.5 (24.1) 123.6 (47.8) Margins Gross Margins (%) 16.9 19.3 15.8 15.8 14.5 Opg Profit Margins (%) 18.8 16.5 13.9 11.4 13.8 Net Profit Margins (%) 4.1 9.2 5.9 8.0 5.7

Balance Sheet (Rpbn)

FY Dec 2014A 2015A 2016A 2017F 2018F Net Fixed Assets 622 1,923 3,275 16,859 26,988 Invts in Associates & JVs 735 1,572 2,071 2,071 2,071 Other LT Assets 1,080 11,009 19,197 19,197 19,197 Cash & ST Invts 1,700 5,522 10,664 3,122 942 Inventory 327 442 1,819 1,800 2,412 Debtors 6,842 7,824 19,795 31,748 42,142 Other Current Assets 1,237 2,018 4,605 7,021 9,260 Total Assets 12,542 30,309 61,425 81,817 103,011 ST Debt 1,917 3,483 15,344 15,344 15,344 Creditor 5,272 8,773 14,653 22,735 30,478 Other Current Liab 539 1,409 1,464 1,464 1,464 LT Debt 1,246 4,547 9,890 19,875 30,536 Other LT Liabilities 803 2,394 3,300 3,300 3,300 Shareholder’s Equity 2,759 9,547 11,070 12,895 14,670 Minority Interests 5.90 157 5,704 6,204 7,219 Total Cap. & Liab. 12,542 30,309 61,425 81,817 103,011 Non-Cash Wkg. Capital 2,594 102 10,101 16,370 21,873 Net Cash/(Debt) (1,463) (2,508) (14,570) (32,097) (44,939) Debtors Turn (avg days) 220.2 189.1 211.9 249.7 269.7 Creditors Turn (avg days) 186.9 217.9 218.5 219.0 232.5 Inventory Turn (avg days) 12.1 11.9 21.1 21.2 18.4 Asset Turnover (x) 1.0 0.7 0.5 0.5 0.5 Current Ratio (x) 1.3 1.2 1.2 1.1 1.2 Quick Ratio (x) 1.1 1.0 1.0 0.9 0.9 Net Debt/Equity (X) 0.5 0.3 0.9 1.7 2.1 Net Debt/Equity ex MI (X) 0.5 0.3 1.3 2.5 3.1 Capex to Debt (%) 10.4 11.7 2.4 39.7 23.2

Source: Company, AllianceDBS, DBSVI

Net gearing to increase from capex at its toll road subsidiary.

ASIAN INSIGHTS VICKERS SECURITIES Page 24

Company Guide

Waskita Karya

Cash Flow Statement (Rpbn)

FY Dec 2014A 2015A 2016A 2017F 2018F Pre-Tax Profit 756 1,398 2,480 3,687 4,112 Dep. & Amort. 38.0 468 251 400 532 Tax Paid (254) (350) (667) (1,019) (888) Assoc. & JV Inc/(loss) 0.0 0.0 0.0 0.0 0.0 Chg in Wkg.Cap. (417) 2,417 (10,099) (6,269) (5,503) Other Operating CF (211) (3,275) 272 0.0 0.0 Net Operating CF (88.7) 658 (7,762) (3,201) (1,747) Capital Exp.(net) (329) (938) (611) (13,983) (10,661) Other Invts.(net) 0.0 0.0 0.0 0.0 0.0 Invts in Assoc. & JV (755) (498) (172) 0.0 0.0 Div from Assoc & JV 1.10 0.0 0.0 0.0 0.0 Other Investing CF 0.0 (5,491) (8,772) 0.0 0.0 Net Investing CF (1,083) (6,927) (9,555) (13,983) (10,661) Div Paid (110) (100) (210) (343) (434) Chg in Gross Debt 1,782 (729) 17,227 9,985 10,661 Capital Issues 59.2 5,348 0.0 0.0 0.0 Other Financing CF (3.1) 5,580 5,442 0.0 0.0 Net Financing CF 1,728 10,099 22,459 9,642 10,228 Currency Adjustments (1.2) 5.90 0.60 0.0 0.0 Chg in Cash 556 3,836 5,143 (7,542) (2,181) Opg CFPS (Rp) 34.0 (130) 172 226 277 Free CFPS (Rp) (43.2) (20.7) (617) (1,266) (914)

Source: Company, AllianceDBS, DBSVI

Target Price & Ratings History

Source: AllianceDBS, DBSVI

Analyst: Chong Tjen-San

Tiesha PUTRI

We expect operating cash flow to remain negative due to the high contribution of turnkey projects.

ASIAN INSIGHTS VICKERS SECURITIES ed: JS / sa:MA, PY

BUY Last Traded Price ( 5 Jul 2017): Rp3,330 (JCI : 5,825.10) Price Target 12-mth: Rp4,100 (23% upside) (Prev Rp4,950) Analyst Chong Tjen-San +60 3 26043972 [email protected] Tiesha PUTRI +6221 30034931 [email protected]

What’s New New contract flow in line with 5M17 new contract

wins representing 33% of our full-year forecast

Maintain BUY with lower TP of Rp4,100

Price Relative

Forecasts and Valuation FY Dec (Rp m) 2015A 2016A 2017F 2018F Revenue 14,217 16,459 21,911 26,878 EBITDA 1,678 2,071 3,019 3,879 Pre-tax Profit 1,288 1,704 2,207 2,747 Net Profit 740 1,023 1,341 1,644 Net Pft (Pre Ex.) 740 1,023 1,341 1,644 Net Pft Gth (Pre-ex) (%) 38.8 38.2 31.1 22.5 EPS (Rp) 153 211 216 265 EPS Pre Ex. (Rp) 153 211 216 265 EPS Gth Pre Ex (%) 39 38 2 23 Diluted EPS (Rp) 153 165 216 265 Net DPS (Rp) 36.5 39.5 51.7 63.4 BV Per Share (Rp) 911 1,580 1,757 1,970 PE (X) 21.8 15.8 15.4 12.6 PE Pre Ex. (X) 21.8 15.8 15.4 12.6 P/Cash Flow (X) 625.1 16.3 42.0 22.4 EV/EBITDA (X) 10.2 7.0 8.6 7.4 Net Div Yield (%) 1.1 1.2 1.6 1.9 P/Book Value (X) 3.7 2.1 1.9 1.7 Net Debt/Equity (X) 0.0 CASH 0.3 0.5 ROAE (%) 22.0 14.4 13.0 14.2 Earnings Rev (%): 0 1 0 Consensus EPS (Rp): N/A 220 280 Other Broker Recs: B: 29 S: 0 H: 0

Source of all data on this page: Company, AllianceDBS, DBSVI, Bloomberg Finance L.P

All eyes on project execution Maintain BUY. Pembangunan Perumahan (PTPP)’s share price has underperformed the JCI by 23% YTD on the back of choppy execution in the past two quarters due to delays in land acquisitions and rollout of contracts. Revenue ex-property grew by only 15% y-o-y in 1Q17 despite value of new contracts growing by 68% y-o-y during the same period as land acquisition issues had hindered construction works. During the recent analyst meeting, management reaffirmed that revenue should catch up in 2Q17 as progress on land acquisitions has picked up pace.

Orderbook provides revenue visibility for 2.7 years. We estimate that PTPP’s order backlog stood at Rp58tr as at the end of May 2017. In May 2017, the company won new contracts worth Rp12.6tr, representing 33%/31% of our/management’s new contract forecast. The management has guided for 25% growth in new contracts in FY17 (vs. our forecast of 19%), the highest growth among our coverage. We are confident that PTPP will be able to record an increase in new contracts awarded over the next two years supported by its enlarged equity base post IPO.

Where we differ. Our Buy call is in line with consensus.

Potential catalysts. A better progress of toll road land acquisitions should help to boost earnings and restore investor confidence after two quarters of posting weaker-than-expected earnings. In addition, having a long standing experience in port construction, we think PTPP stands a chance to win the mega project at Patimban Port. The tender of the project is underway. Positive newsflow on the financing and execution of the project should lead to a re-rating of its share price. Potential M&A as a precursor to the listing of PTPP’s subsidiaries represent another catalyst.

Valuation: We cut our TP to Rp4,100 (from Rp4,950) as we lower our target PE multiple to 19x PE (20% premium to the sector’s historical mean PE). PTPP is trading at 15.4x/12.6x 17F/18F PE, on par with peers despite its stronger balance sheet to fuel new contract growth in the coming years.

Key Risks to Our View: Prolonged slowdown in property sector. PTPP has both direct and indirect exposure to the property sector. A prolonged slowdown in the economy and demand for property can negatively impact earnings and cash flows. At A Glance Issued Capital (m shrs) 6,200 Mkt. Cap (Rpbn/US$m) 20,646 / 1,545 Major Shareholders (%) Republic of Indonesia (%) 51.0

Free Float (%) 49.0 3m Avg. Daily Val (US$m) 6.3 ICB Industry : Industrials / Construction & Materials

CRITICAL DATA POINTS TO WATCH

DBS Group Research . Equity 5 Jul 2017

Indonesia Company Guide

Pembangunan Perumahan Version 6 | Bloomberg: PTPP IJ | Reuters: PTPP.JK Refer to important disclosures at the end of this report

ASIAN INSIGHTS VICKERS SECURITIES Page 27

Company Guide

Pembangunan Perumahan

Critical Factors

Maintaining positive new contract growth momentum post rights issue. PTPP successfully raised Rp4.4tr cash through a rights issue in December 2016. It intends to use 76% of the proceeds to fund equity investments in infrastructure projects, among which are Kuala Tanjung Multi-Purpose Terminal and Industrial Estate, five toll roads (such as Balikpapan-Samarinda toll road, Manado-Bitung toll road, Pandaan-Malang toll road), a 2x200MW power plant in Sumatra, and low-cost apartments, while the remaining 24% will be used for working capital. With ample cash post rights issue, the company should be able to take on more projects in FY17. This year, the company is eyeing new contracts worth Rp40.6tr, representing 25% increase y-o-y. Beneficiary of Indonesia’s port build-out. PTPP has over the years developed a niche in port construction in Indonesia. According to Bapennas, Indonesia would need as much as Rp59tr to develop and expand 24 ports from 2015-2019. Among the larger projects is the multi-year expansion projects at Kuala Tanjung port (Rp18.4tr). The port was initially built by PTPP, hence this would raise the company's competitive edge to secure work contracts once the projects are out for tender. This year, Pelindo I-IV, state-run port operators that will carry out a significant part of the government’s port development plan, have allocated capex of more than Rp13tr for port expansion. Progress on the mega project at Patimban Port is also important to watch as the company eyes the construction contract. More clarity on the funding of the project is expected to come this year, while construction is scheduled to start in 2018. Redirecting focus to government-related infrastructure projects. We estimate that 15%-20% of PTPP’s backlog is from private property developers. The pace of project execution may be slower amid the still subdued property market, and may potentially negatively affect the company’s contract burn rate and earnings. Since 2016, management has redirected its focus to government-related infrastructure projects, including the higher margin EPC projects. Currently, PTPP has three power plant projects in its order book with total capacity of 420 MW. The company plans to bid for more small-scale power plant projects in the future. With this strategy, the company expects to clinch 30% higher new EPC contracts in FY17 from FY16’s Rp6tr. Subsidiaries’ IPOs. Management is still pursuing inorganic growth ahead of the planned IPO of its subsidiaries. Recently, it acquired three companies through its precast and power business. The IPOs will likely be in 2H17 at the soonest, awaiting green light from the parliament and government.

New Contract Win (Rp bn)

Carry Over Contract (Rp bn)

New Contract

Contractors’ revenue visibility

Source: Company, AllianceDBS, DBSVI

4,300 4,300

7,000

9,000

12,600

11%

11%

17%

22%

31%

-

5%

10%

15%

20%

25%

30%

35%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1M17 2M17 3M17 4M17 5M17

PTPP's new contracts (Rp bn) as % of FY17 target

76.2 58.1

92.9

22.8 21.9

37.7

3.3

2.7

2.5

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

-10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0

100.0

WIKA PTPP WSKT

(x)Rp tr

Outstanding order book* (LHS)Revenue FY17F (LHS)Outst. order book/revenue FY17F (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 28

Company Guide

Pembangunan Perumahan

Appendix 1: A look at the company's listed history – what drives its share price?

PTPP’s share price vs. peers*

*Based on the average return of the listed state-owned contractors Source: Company, AllianceDBS, DBS Vickers A: Rupiah depreciation PTPP’s share price along with the other state-owned contractors were under pressure due to concerns over cost overruns, particularly related to government’s infrastructure projects. A portion of raw materials are imported, hence Rupiah depreciation may impact margins and earnings negatively. However, PTPP has been least affected compared to other state-owned contractors due to its lower exposure to government infrastructure projects in the past. PTPP’s share price vs. USDIDR

Source: Bloomberg Finance L.P. B: Fiscal revenue collection and state budget The government’s plan to cut spending in 2016 following weak revenue collection caused state-owned contractors’ share prices, including PTPP, to de-rate.

C: Higher exposure to power plant projects and awards of big ticket infrastructure projects Earnings recovery in 2Q16 was strong with core profit surging by 260% y-o-y, mainly driven by EPC business (power plant construction). Furthermore, the management shared its plan to expand its higher margin EPC business. PTPP’s share price re-rated upwards following the award of two mega toll road projects in June 2016. PTPP’s share price vs. new contract

Source: Company, AllianceDBS, DBS Vickers D: Slow project execution and concern over investment in property sector PTPP’s order book replenishment has picked up pace since mid-2016 after winning a number of infrastructure projects. However, construction progress had been slow due to land acquisition issues, causing earnings to fell short of market expectations. In addition, PTPP’s equity injection into its property arm PP Properti (PPRO) through a rights issue created some concerns among investors, given the still weak property market.

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16

PTPP share price (LHS) PTPP share price vs. peers (RHS)

A

Dec 18, 2012 = 1.0

B

C

D

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

-

1,000

2,000

3,000

4,000

5,000

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

PTPP share price (LHS) USDIDR (RHS)

05,00010,00015,00020,00025,00030,00035,00040,000

-

1,000

2,000

3,000

4,000

5,000

Dec

-12

Mar

-13

Jun-

13Se

p-13

Dec

-13

Mar

-14

Jun-

14Se

p-14

Dec

-14

Mar

-15

Jun-

15Se

p-15

Dec

-15

Mar

-16

Jun-

16Se

p-16

Dec

-16

Mar

-17

PTPP share price (LHS) T12M new contract, Rp bn (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 29

Company Guide

Pembangunan Perumahan

Balance Sheet:

Strong balance sheet enables PTPP to take on more projects. PTPP is in a net cash position after receiving rights issue proceeds of Rp4.4tr in December 2016. We forecast PTPP’s debt to rise with gross gearing of 0.12x in FY17 as the company starts to fund its equity investments in a number of infrastructure projects. Subsidiaries’ IPOs. Management is still pursuing inorganic growth ahead of the planned IPO of its subsidiaries - PP Perlatan (construction equipment rental), PP Urban (low cost housing and precast concrete) and PP Energi (power plant). Recently, it acquired three companies through its precast and power business. The IPOs will likely be in 2H17 at the soonest, awaiting green light from the parliament and government. Management seeks to raise Rp7tr from these IPOs. Share Price Drivers:

Award of a large-sized, multi-year infrastructure contracts. The award of large-sized, multi-year contracts will further improve PTPP’s revenue and earnings visibility, and ultimately lead to re-rating of its share price. Key Risks:

Slowdown in property sector. PTPP’s exposure to the property sector has increased notably with net profit contribution from the property arm at 23% in FY16. We estimate that 15%-20% of PTPP’s outstanding order book are contracts from private developers. A prolonged slowdown in the property market may pose risks to PTPP’s earnings and cash flows. Slow execution of infrastructure project. Delay in project execution due to land acquisition and technical issues or funding constraints such as government’s budget cut may cause revenue and earnings to fall short of our projections. Company Background