Indonesia Country Brief: Role of Government in Power...

43

Country Brief: Theme: Role of Government in Power Sector and Energy Market INDONESIA

Transcript of Indonesia Country Brief: Role of Government in Power...

Country Brief:

Theme: Role of Government in

Power Sector and Energy Market

INDONESIA

Contents

A. Overview: Energy, Economy, and Environment

B. Overview: Role of Government in Power Sector

C. Tech. Session: Policy Measures and Regulations for Changing Electric Power Market (Reform)

D. Tech. Session: Other Topics on Energy/Power Market

1

A. Overview:

Energy, Economy, and Environment

2

Country Overview

Area Total: 1,919,440 km2, land: 1,826,440 km2, water: 93,000 km2

Energy Resources Crude oil :3.7 billion barrels (et end of 2012) (BP)

Natural gas: 2.9 Trillion m3 (et end of 2012) (BP)

Coal: 5,529 million tonnes (et end of 2012) (BP)

Population 244.5 million (end of 2012) (IMF)

Annual Growth 1.43% (2000-2012)

GDP 878.2 billion USD (2012) (IMF)

Annual Growth 5.42% (2000-2012)

GDP per Capita 3,592 USD (2012) (IMF)

Total Primary

Energy Supply

159.4 million toe (2012) BP

TPES per Capita 0.65 toe (2012)

TPES per GDP 0.18 toe/thousand USD (2012)

Electrification ratio 76.56% (2012) (PLN + Non PLN) 3

Historical Trend of Energy and Power

• Indonesia is a resource rich country with a growing demand for energy.

From 2000 to 2012, total primary energy supply grew at an average

annual rate of 4.5% from 99.1 million toe to 159.4 million toe for the

same period.

• In 2012, Carbon Dioxide Emissions are 495.2 million tones.

• The government's commitment to reduce GHG emissions up to 26% in

2020 with national efforts and 41% with international assistance.

Renewable energy and energy efficiency both are prioritized to achieve

emission reduction targets

Source: BP [statistical_review_of_world_energy_2013]

4

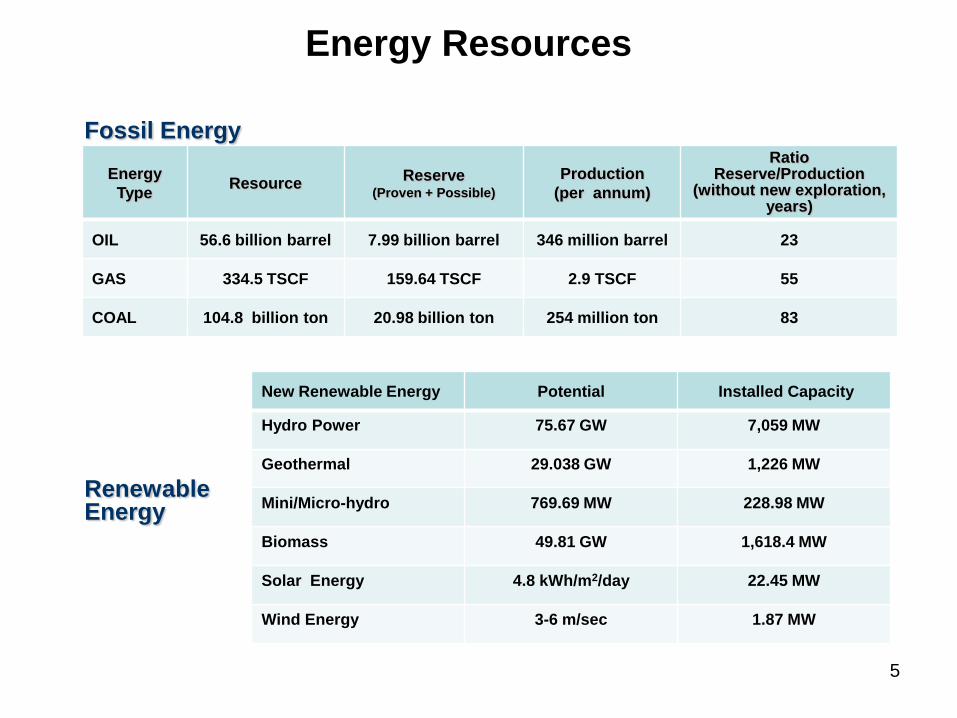

Energy Resources

Energy

Type Resource

Reserve (Proven + Possible)

Production

(per annum)

Ratio Reserve/Production

(without new exploration, years)

OIL 56.6 billion barrel 7.99 billion barrel 346 million barrel 23

GAS 334.5 TSCF 159.64 TSCF 2.9 TSCF 55

COAL 104.8 billion ton 20.98 billion ton 254 million ton 83

New Renewable Energy Potential Installed Capacity

Hydro Power 75.67 GW 7,059 MW

Geothermal 29.038 GW 1,226 MW

Mini/Micro-hydro 769.69 MW 228.98 MW

Biomass 49.81 GW 1,618.4 MW

Solar Energy 4.8 kWh/m2/day 22.45 MW

Wind Energy 3-6 m/sec 1.87 MW

Fossil Energy

Renewable Energy

5

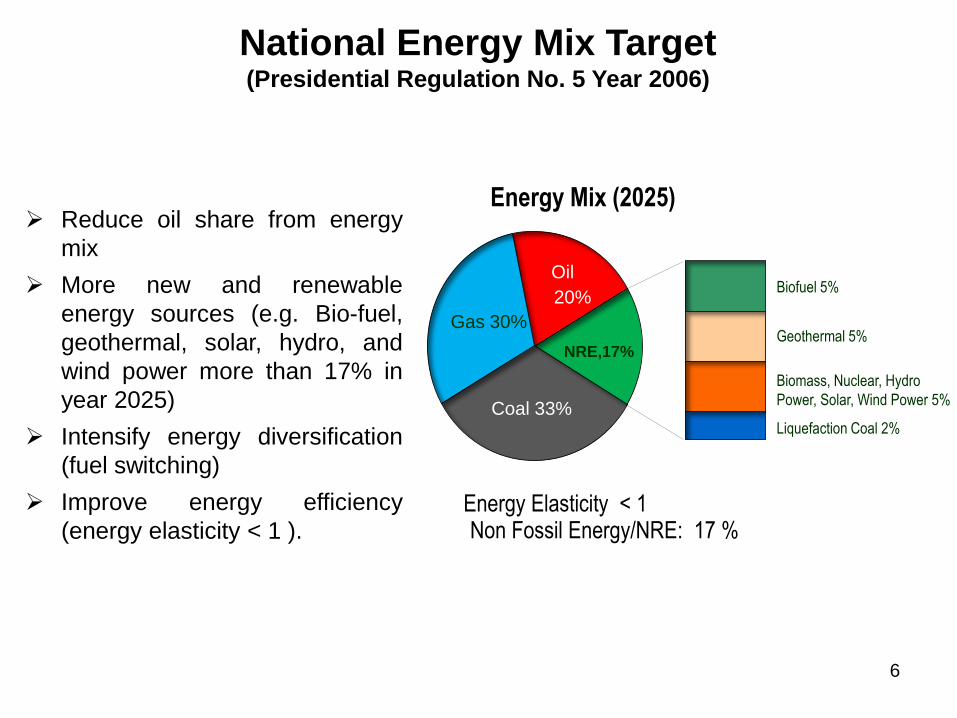

National Energy Mix Target (Presidential Regulation No. 5 Year 2006)

Energy Mix (2025)

Energy Elasticity < 1

Reduce oil share from energy

mix

More new and renewable

energy sources (e.g. Bio-fuel,

geothermal, solar, hydro, and

wind power more than 17% in

year 2025)

Intensify energy diversification

(fuel switching)

Improve energy efficiency

(energy elasticity < 1 ).

Non Fossil Energy/NRE: 17 %

Coal 33%

Oil

20%

NRE,17%

Biofuel 5%

Geothermal 5%

Biomass, Nuclear, Hydro

Power, Solar, Wind Power 5%

Liquefaction Coal 2%

Gas 30%

6

Overview of National Electricity Conditions

Total installed capacity: 44,976 MW (PLN 73%, IPP 23%, and PPU 4%).

Current electrification ratio (2012): 76.56%.

Energy mix in power generation (2012): Coal 50.27%, Gas 23.41%, Oil 14.97%, Hydro

6.39%, Geothermal 4.85%, Bio Diesel & Other NRE 0.11%.

Oil 14.97%

Coal 50.27%

Gas 23.41%

Geothermal 4.85%

Hydro 6.39%

Other 0,11%

INVESTMENT IN POWER SECTOR (MIL. USD) POWER GENERATION CAPACITY (MW)

PLN 73%

IPP 23%

PPU 4%

7

Realization of Energy Mix (2008 – 2013)

2008 2009 2010 2011 2012 2013

APBN-P

Realization

up to June

2013

Oil 36% 25% 22% 22,95% 14,97% 10,87% 12,57%

Gas 17% 25% 25% 21,00% 23,41% 22,45% 23,32%

Coal 35% 39% 38% 44,06% 50,27% 55,15% 50,29%

Hydro 9% 8% 12% 6,80% 6,39% 6,40% 8,99%

Gethermal 3% 3% 3% 5,13% 4,85% 4,60% 4,74%

Bio Diesel & Other RE 0% 0% 0% 0,07% 0,11% 0,52% 0,09%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

8

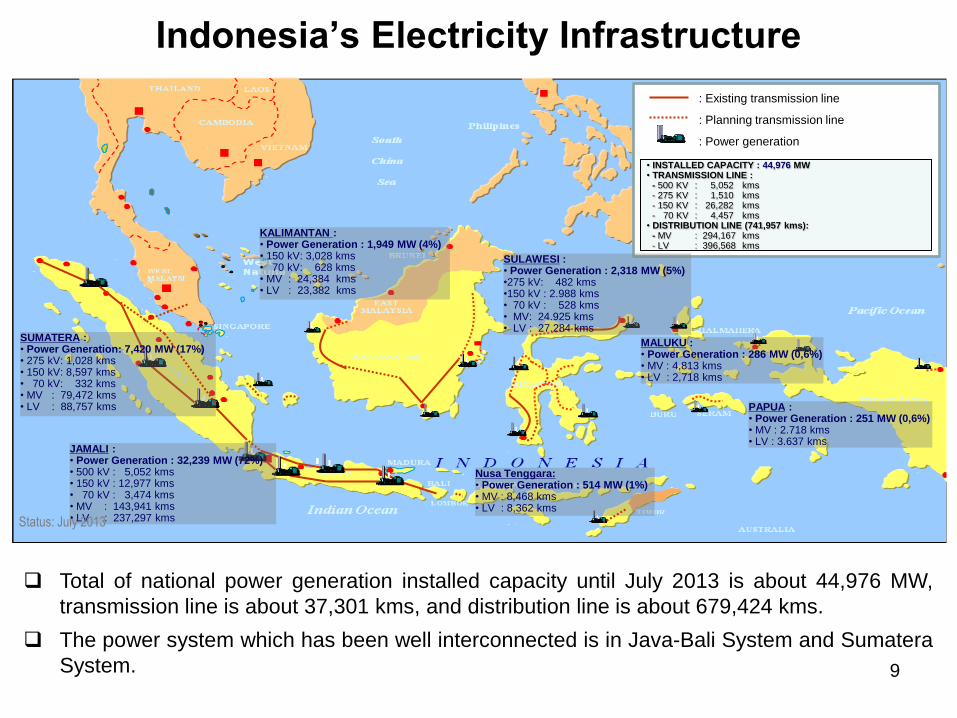

: Existing transmission line

: Planning transmission line

: Power generation

• INSTALLED CAPACITY : 44,976 MW • TRANSMISSION LINE : - 500 KV : 5,052 kms - 275 KV : 1,510 kms - 150 KV : 26,282 kms - 70 KV : 4,457 kms • DISTRIBUTION LINE (741,957 kms): - MV : 294,167 kms - LV : 396,568 kms

SUMATERA : • Power Generation: 7,420 MW (17%) • 275 kV: 1,028 kms • 150 kV: 8,597 kms • 70 kV: 332 kms • MV : 79,472 kms • LV : 88,757 kms

JAMALI : • Power Generation : 32,239 MW (72%) • 500 kV : 5,052 kms • 150 kV : 12,977 kms • 70 kV : 3,474 kms • MV : 143,941 kms • LV : 237,297 kms

Nusa Tenggara: • Power Generation : 514 MW (1%) • MV : 8,468 kms • LV : 8,362 kms

KALIMANTAN : • Power Generation : 1,949 MW (4%) • 150 kV: 3,028 kms • 70 kV: 628 kms • MV : 24,384 kms • LV : 23,382 kms

SULAWESI : • Power Generation : 2,318 MW (5%) •275 kV: 482 kms •150 kV : 2.988 kms • 70 kV : 528 kms • MV: 24.925 kms • LV : 27.284 kms

PAPUA : • Power Generation : 251 MW (0,6%) • MV : 2.718 kms • LV : 3.637 kms

MALUKU : • Power Generation : 286 MW (0,6%) • MV : 4,813 kms • LV : 2,718 kms

Indonesia’s Electricity Infrastructure

Total of national power generation installed capacity until July 2013 is about 44,976 MW,

transmission line is about 37,301 kms, and distribution line is about 679,424 kms.

The power system which has been well interconnected is in Java-Bali System and Sumatera

System.

Status: July 2013

9

Category :

> 60 %

41 - 60 %

20 - 40 %

Aceh 90,96%

Sumut 86,70%

Sumbar 76,14%

Riau 85,09%

Sumsel 73,97.%

Bengkulu 79,37%

Babel 94,13%

Lampung 74,91%

Jakarta 99,99%

Banten 77,52%

Jabar 76,03%

Jateng 79,95%

Jambi 70,37%

DIY 77,26%

Jatim 74,31%

Bali 74,95%

NTB 53,63%

NTT 53,42%

Kalbar 71,46%

Kalsel 76,74%

Kaltim 73,08%

Sulut 76,22%

Sulteng 66,83%

Sulsel 76,29%

Malut 74,12%

Maluku 72,07%

Papua 34,62%

Sulbar 66,65%

Kepri 83,56%

Sultra 60,53%

Papua Barat 67,88%

Kalteng 73,32%

Gorontalo 60,99%

Electrification Ratio (2012)

10

B. Overview:

Role of Government in Power Sector

Under Law 30/2009 on Electricity

11

Important Points of

Law No. 30/2009 on Electricity

Electricity supply for public use will be controlled by the state, carried out by both the

Government and Regional Government based on the principles of regional autonomy.

Electricity provision is principle carried out by state owned enterprise (BUMN), but

regional owned enterprise (BUMD), private business entity, cooperative and self-

supporting community can also participate in this business.

Existing regulations in the electricity business is strengthened to encourage private

sector participation, such as Independent Power Producers (IPPs) can sell

electricity to PLN and Private Power Utilities (PPUs) can sell electricity to public within

their concession areas.

Regional tariff pricing will be introduced. Issues related to retail tariff will be regulated

by the Government and its values must be approved by Parliament (DPR) and local

parliament (DPRD). This value is determined by several factors i.e.: cost of supply,

consumer’s capabilities, quality of supply and services. Whenever the retail tariff is set

below its cost of supply, the Government or local government should provide subsidy

(The detail in Government Regulation 14/2002 on Electricity Supply Business).

Cross border trade/transactions of electricity is allowed with certain requirement

(Government Regulation 42/2012 concerning on Cross Border Electricity Trade).

Safety and environmental standard is applied in the development of power plants

(Government Regulation 62 on Supporting Electricity Business).

12

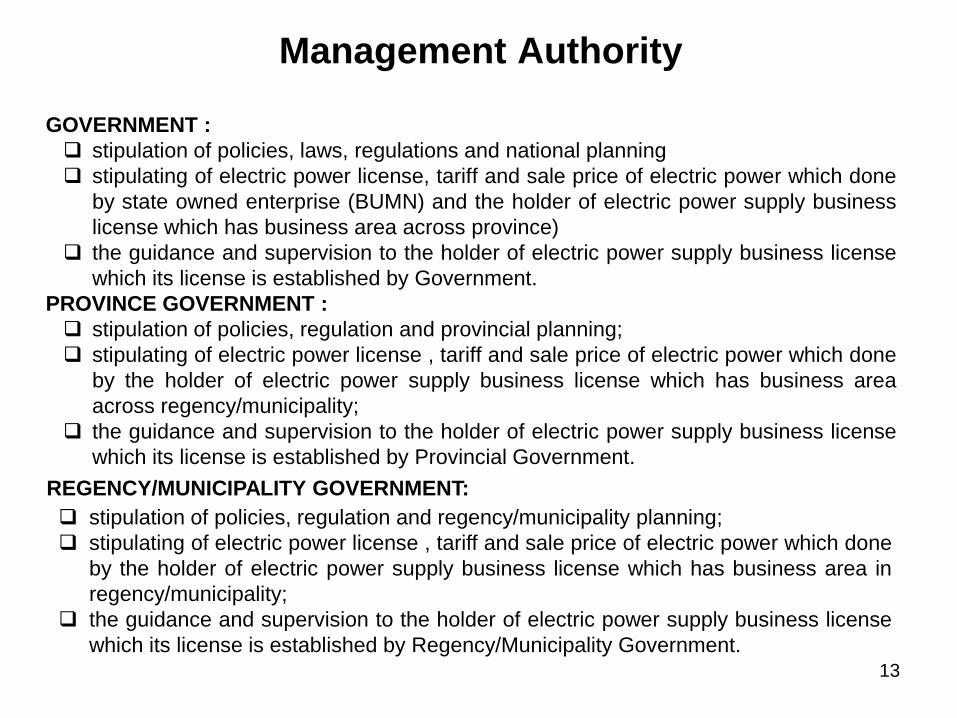

Management Authority

13

GOVERNMENT :

stipulation of policies, laws, regulations and national planning

stipulating of electric power license, tariff and sale price of electric power which done

by state owned enterprise (BUMN) and the holder of electric power supply business

license which has business area across province)

the guidance and supervision to the holder of electric power supply business license

which its license is established by Government.

PROVINCE GOVERNMENT :

stipulation of policies, regulation and provincial planning;

stipulating of electric power license , tariff and sale price of electric power which done

by the holder of electric power supply business license which has business area

across regency/municipality;

the guidance and supervision to the holder of electric power supply business license

which its license is established by Provincial Government.

REGENCY/MUNICIPALITY GOVERNMENT:

stipulation of policies, regulation and regency/municipality planning;

stipulating of electric power license , tariff and sale price of electric power which done

by the holder of electric power supply business license which has business area in

regency/municipality;

the guidance and supervision to the holder of electric power supply business license

which its license is established by Regency/Municipality Government.

Role Of Government In Power Sector

Issuance of Business license of electric power supply (IUPL)

MINISTER

GOVERNOR

REGENT/

MAYOR

- State Own Enterprise (PLN)

- business area across province

- Selling electricity to the holder of electric power

supply business license which is established by

Minister

business area across regency/ municipality

business area in regency/municipality

AUTHORITY OF LICENSE ESTABLISHMENT

Role of Minister/Governor/Regent/Major based on authority related to issuance of IUPL

1. set tariff for consumers

2. approval of the sale price electricity and rental network

3. permit utilization of electricty network for telematics

4. direct and supervise

5. impose administrative sanctions 14

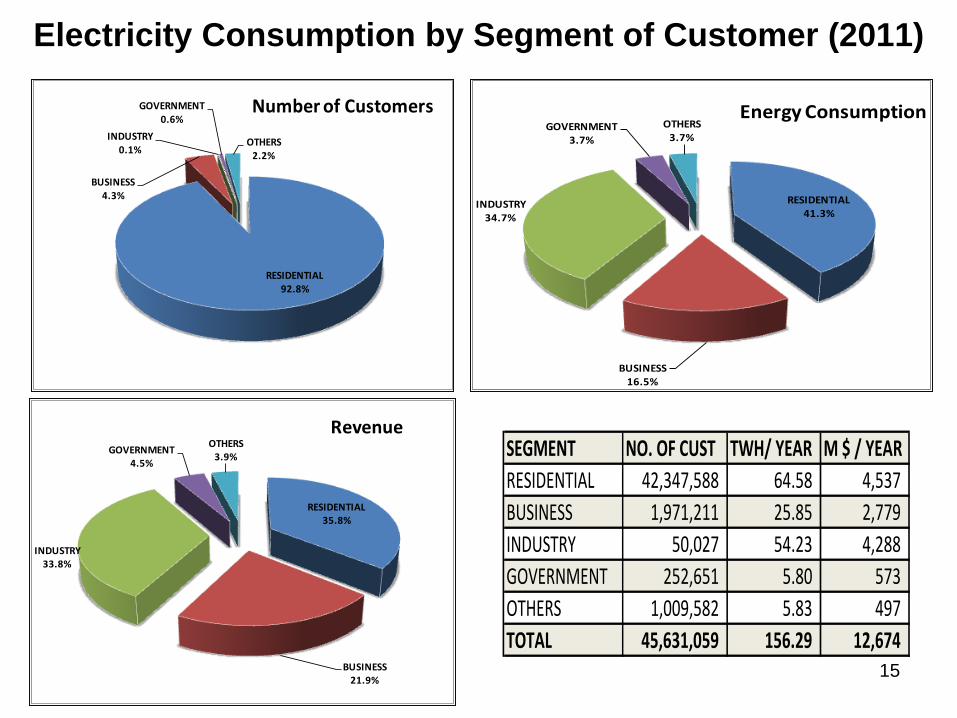

Electricity Consumption by Segment of Customer (2011)

RESIDENTIAL92.8%

BUSINESS4.3%

INDUSTRY0.1%

GOVERNMENT0.6%

OTHERS2.2%

Number of Customers

RESIDENTIAL41.3%

BUSINESS16.5%

INDUSTRY34.7%

GOVERNMENT3.7%

OTHERS3.7%

Energy Consumption

RESIDENTIAL35.8%

BUSINESS21.9%

INDUSTRY33.8%

GOVERNMENT4.5%

OTHERS3.9%

RevenueSEGMENT NO. OF CUST TWH/ YEAR M $ / YEAR

RESIDENTIAL 42,347,588 64.58 4,537

BUSINESS 1,971,211 25.85 2,779

INDUSTRY 50,027 54.23 4,288

GOVERNMENT 252,651 5.80 573

OTHERS 1,009,582 5.83 497

TOTAL 45,631,059 156.29 12,674 15

Standards of Life: electrification, residential tariff rates

• Electrification ratio:76.5% (as of end 2012).

• The Indonesian government sets the electricity tariff for all consumer types. The amount of subsidy is determined annually by the government, based on the difference between the average cost of electricity production proposed by (PLN),

• There are six electricity tariff blocks (Residential) for subscription options. • In 2011, the government spent 93.18 trillion Rp on electricity subsidy.

Year

Average Electricity

Cost

(Rp/kWh)

Subsidy

(Trillion Rp)

2005 710 10,64

2006 934 33,90

2007 920 37,48

2008 1.271 78,58

2009 1.009 53,72

2010 1.008 58,11

2011 1.251 93,18

16

S.1 / 220 VA

S.2 / 450 VA

S.2 / 900 VA

S.2 / 1.300 VA

S.2 / 2.200 VA

S.2 / > 2.200 s/d 200 kVA

S.3 > 200 kVA

R.1 / s/d 450 VA

R.1 / 900 VA

R.1 / 1.300 VA

R.1 / 2.200 VA

R.2 / > 2.200 s/d 6.600 VA

R.3 / > 6.600 VA

B.1 / s/d 450 VA

B.1 / 900 VA

B.1 / 1.300 VA

B.1 / 2.200 VA

B.2 / > 2.200 s/d 200 kVA

B.3 / > 200 kVA

I.1 / 450 VA

I.1 / 900 VA

I.1 / 1.300 VA

I.1 / 2.200 VA

I.1 / 2.200 s/d 14 kVA

I.2 / > 14 kVA s/d 200 kVA

I.3 / > 200 kVA

I.4 / > 30.000 kVA

P.1 / s/d 450 VA

P.1 / 900 VA

P.1 / 1.300 VA

P.1 / 2.200 VA

P.1 / > 2.200 s/d 200 kVA

P.2 / > 200 kVA

P.3

TRACTION / > 200 kVA

BULK / > 200 kVA

L (Special Service)

Subsidy vs Average Price 2011Average Price Subsidy

10.6

33.9 37.5

78.6

53.7 58.1

93.2

2005 2006 2007 2008 2009 2010 2011

GOVERNMENT SUBSIDY(Trillion Rupiah)

Tariff Category # Customer % Subsidy

1 R.1 / s/d 450 VA 19,837,021 20.44%

2 I.3 / > 200 kVA 9,342 20.22%

3 R.1 / 900 VA 15,080,552 18.72%

4 I.4 / > 30.000 kVA 55 7.74%

5 R.1 / 1.300 VA 5,074,509 7.31%

6 B.3 / > 200 kVA 4,576 4.56%

7 R.1 / 2.200 VA 1,657,310 4.29%

8 B.2 / > 6.600 s/d 200 kVA 287,408 2.38%

9 R.2 / > 3.500 s/d 5.500 VA 563,501 2.32%

10 I.2 / > 14 kVA s/d 200 kVA 27,984 2.21%

17

Tariff Policy

• Maintain the sustainability of electricity supply

• Improving the quality of customer service

• Considering: – Fairness

– Affordability

– Cost of Production

– Operational Efficiency

– Operational Size

– Interconnection System

18

PLN Electricity Tarif Adjusment For 2013

S2/sd 20

0K

S.1 S2/450

S2/900

S2/1300

S2/2200

S3I1/sd 14

K

LR1/450

R1/900

R1/1300

R1/2200

R2 B1/450

B1/900

B1/1300

B1/sd 55

00

P1/sd 55

00

I2 B3R3 B2 I1/450

I1/900

I1/1300

I1/2200

P2P3 T CI3 I4P1/450

P1/900

P1/1300

P1/sd 20

0K

S2

/sd

20

0K

S.1

S2

/45

0

S2

/90

0

S2

/13

00

S2

/22

00

S3

I1/s

d 1

4K

LR1/4

50

R1/9

00

R1/1

300

R1/2

200

R2

B1

/45

0

B1

/90

0

B1

/13

00

B1

/sd

55

00

P1

/sd

55

00

I2 B3

R3

B2

I1/4

50

I1/9

00

I1/1

30

0

I1/2

20

0

P2

P3

T CI3 I4P1

/45

0

P1

/90

0

P1

/13

00

P1

/sd

20

0K

COST LV:

1352 Rp/kWh

MV

1113

HV

1006

Subsidiy

(Rp/kWh) Decreasing of

Subsidy (Rp/kWh)

Electricity Bill

(Rp/kWh)

(Rp/k

Wh)

No more Subsidy

S2

/sd

20

0K

S.1

S2

/45

0

S2

/90

0

S2

/13

00

S2

/22

00

S3

I1/s

d 1

4K

LR1/4

50

R1/9

00

R1/1

300

R1/2

200

R2

B1

/45

0

B1

/90

0

B1

/13

00

B1

/sd

55

00

P1

/sd

55

00

I2 B3

R3

B2

I1/4

50

I1/9

00

I1/1

30

0

I1/2

20

0

P2

P3

T CI3 I4P1

/45

0

P1

/90

0

P1

/13

00

P1

/sd

20

0K

RA

KS

I

UR

AH

AY

AN

AN

KH

US

US

19

Electricity Tariff Structure

20

Electricity Tariff Road-map

MID TERM:

To increase the tariff, towards

the economic price

Cost of Goods Sold

2012 2013 2014 2015

Rp/kWh

LONG TERM:

- Automatic tariff adjustment

- Subject to primary energy

prices and exchange rate

fluctuation

COGS

2015

Rp/kWh

21

Environmental/Low carbon initiatives:

renewables, energy efficiencies, fuel switching

• The Clean Technology Fund (of the World Bank) and the Asian Development

Bank (ADB) have established a fund for lending to renewable energy projects

in Indonesia, including those developed by PLN. The funds will be used to

finance 880 MW of geothermal development, as well as biomass projects.

• The objective of Law on Energy No. 30 of 2007 is to secure sustainable energy

supplies and promote conservation and the use of renewable energy

resources.

• The government has set objectives to increase the use of renewable sources

for power generation. The goal is that renewables account for 17% of

Indonesia’s installed generating capacity by 2025. The 17% would be

comprised of 5% from biofuel, 5 % from geothermal, 5% from a combination of

biomass, hydro, solar, wind and nuclear, and 2% from liquefied coal.

• The Government of Indonesia has promoted Feed-in Tariff for Geothermal,

Hydro ≤ 10 MW, and Biomass ≤ 10 MW and also Ceiling Price for Photovoltaic.

22

Energy Security for Electricity

a. Demand and Supply of Electricity

• Determinant of electricity demand associated with economic growth targets and the

Government's commitment to increase the supply of electricity evenly.

• Electricity demand growth in the past 5 years is higher (7.5%) than the power plant

capacity growth (7,6%), but there are the crisis of electricity supply in some areas

because additional capacity mostly in Java island. So far, the outage outside Java Bali

has been resolved temporary, in some areas have been resolved with the rent of

power generation and purchase of excess power.

b. Price for Electricity

• Electricity tariffs determined by the Government to ensure affordability for majority

people and still consider the business competitiveness. But the electricity tariff is also

important to ensure sustainability of electricity supply in accordance with increased

demand

• Along with the trend of rising prices in general, including primary energy, the

production cost (BPP) of electricity tended to increase, so electricity tariffs need to be

adjusted in order to maintain the sustainability of supply

c. Accesibility of Electricity

• Government's commitment to continuously improve the electrification ratio is to

increase the number of household customers about 2.4 million per year in average.

PLN’s majority of customers and revenue derived from unaffordable house hold

category (450-900 VA), so that need the efforts to strengthen PLN's revenue structure

• Development of electricity distribution system for the next 3 years prioritized to

distribute electricity from new power plant 10,000 MW fast track program phase I and

phase II

23

Regulation

MR 04/2012 • Electricity Purchase from Small and Medium

Scale Renewable Energy or Excess Power (Ceiling price under 10 MW)

PR 4/2010

• Assigment to PLN Inc. for Acceleration Establishment of Renewable Energy, Coal and Gas Power Plant *)

MR 0010/2005 • Power business licence procedure on

crossing provinces or connecting to national power transmission grid

MR 002/2006 • Medium Scale Renewable Energy

Power Plant (1-10 MW)

MR 1122K/30/MEM/2002

•Small Scale Distributed Power Generation (under 1 MW) *)

Note :

GR : Government Regulation

PR : Presidential Regulation

MR : Ministerial Regulation

*) Implementing

regulations in the

electricity sector

which is still

enforced in

accordance with

the old Electricity

Act 15/1985 is

still used as long

as not contrary to

the New

Electricity Act

30/2009

MR 22/2012 • Price of Electricity Purchase from Geothermal

Power Plant

MR ESDM 004/2007

Amandement of MR 001/2006

• Buy and/or Rent Power Grid Procedure by

Holding Licence of Power Public Business

PR 71/2006 Jo PR 59/2009 Jo PR 47/2011

•Assigment to PLN Inc. for Accelaration Estbalishment Coal Power Plant *)

MR 28/2012

• Electricity Business Area

MR 01/2012 • Project List of Acceleration Establishment of Renewable Energy, Coal and Gas Power Plant

and transmission related

GR 62/2012

Supportive Electricty Business

GR 14/2012

Powerb Supply Business

Activities

GR 42/2012

Cross-State Power Sale

Purchase

Electricity Act 30/2009

24

C. Technical Session:

Policy Measures and Regulations for Changing

Electric Power Market (Reform)

25

PRIVATE PARTICIPATION

NEEDED

Population growth, economic growth, industrial development,

technological advances and living standard improvement, has led

electricity demand increase.

After the economic crisis that hit Indonesia a few years ago, led to the

development of some power plants that had been planned to be

delayed.

Government funds allocation to invest in the power sector as well as

the budget of PLN especially for the construction of new power plants

is very limited on the other hand the cost of investment in the

electricity sector is very high.

Background Of Private Participation

26

• A major structural Electricity Sector Reform designed since early 1990s by World Bank and development donor agencies (such USAID). – Driving by larger industrial deregulation attempt in 1980s

– Main objective to end the monopoly of state-owned electric utility, introducing market-oriented industrial structure, creation of electricity market, facilitation for private investment.

• ESR getting more momentum after the economic crisis in 1997 – economic stabilization loans from WB and IMF string attached to

the conditionality to do reform (deregulation and privatization) of electricity and oil and gas sector.

– Asian Development Bank (ADB) and USAID assisted the policy formulation for the Power Sector Reform (PSR) and drafted the draft of the law.

Electricity Sector Reform

27

• Element of Proposed Reform (1998 White Paper and Electricity Law

No. 20/2002):

– Separation of PLN’s asset in Java-Bali and non-Java Bali. • Java & Bali system accounted of 75% of energy sold by PLN and more mature

infrastructure.

– Unbundling of the PLN into generation, transmission and distribution

companies; • Later, privatization of unbundled companies.

– Separation of Government policy-making and regulatory function for

electricity sector. • Establishment of electricity market regulatory body.

– Establishment of electricity market (power pool) in Java-Bali system.

– Rationalization of Independent Power Producers (IPP).

• Civil Society Organization and Labor Union took the 2002 Electricity

Law to the Constitutional Court in 2003.

– The Electricity Law were revoked by the Constitutional Court in 2004,

practically ending the “Electricity Sector Restructuring” Program.

Cont’ Electricity Sector Reform

28

Tender

Direct

Selection

Direct

Appointment

Government Control on IPP (Government Regulation No. 14/2012 on Activity of Electricity Provision Business)

Commercial Operation

Operation Worthy Tests

(Adopted by Operation Worthy Certificate)

IUPL Mechanism, Selling Price and Contract

National Electricity General Plan (RUKN) and the

Electricity Supply Business Plan of PLN (RUPTL)

Bidding

Process

29

National Electricity General Plan (RUKN) and the Electricity Supply Business Plan of PLN (RUPTL) as reference for power sector investment program

Private sector participation: Independent Power Producer (IPP)

EPC Contractors

Public Private Partnership (PPP)

Principally, all IPP projects should be based on bidding

process, except for: – Renewable energy power plant – Marginal gas – Mine mouth power plant – Excess power – System in crisis condition – Expansion of the existing/installed power plant.

Investment Mechanism And Private Sector Participation

Scheme

30

Status of IPP Projects

Large Scale (> 10 MW) Medium & Small Scale (up to 10 MW)

Stage Number Total Cap. (MW) Number Total Cap. (MW)

Operation 27 9,552 21 53

Construction 18 1,689 27 111

Financing 42 8,503 104 531

87 19,744 152 695

- Based on the issuance of business licenses, overall there are 239 of IPP plants (20,438.8 MW),

Consist of 87 projects are large-scale IPP’s (capacity > 10 MW, total: 19,744.21 MW), while 152 plants

are the small and medium-scale IPP’s (capacity up to 10 MW, total: 694.59 MW).

- Of 60 large-scale IPP projects under construction and financing, 18 IPP have problems: the financing

(10), Forest area (3), Land (2), others (3).

- Of 131 small and medium-scale IPP projects under construction and financing, 19 IPP have problems:

the financing (1), Forest area (6), Land (8), others (4).

31

Electricity efficiency effort is conducted through diversification of primary energy in

power generation (supply side) by optimizing utilization of gas, reduce of oil utilization,

increasing coal utilization, and developing renewable energy power generation.

Gas and coal are given priority to reduce dependence on oil in power generation.

Target of Energy Mix For Power Generation

Oil 14.97%

Coal 50.27%

Gas 23.41%

Geothermal 4.85%

Hydro 6.39%

Other 0,11%

Oil 0,8%

Coal 62,8%

Gas 18,8%

Geothermal 11,0%

Hydro 6,5%

Other 0,1%

Source: RUPTL PLN 2012-2021

2012 (200 TWh)

2021 (± 411 TWh)

Future (Needs, Plan or Prospects)

32

Power Generation Development Planning

Total power generation that will be developed up to 2021 is about of 57 GW or in average

5.7 GW p.a.

PLN will develop about of 53% of the total capacity and the rest (47%) will be developed by

IPP/private

Source: RUPTL PLN 2012-2021

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

MW

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

GeoPP 110 5 63 188 660 1.375 1.260 1.588 1.045 55

PS - - - - - 1.040 - - 450 450

HEPP 130 85 - 78 546 694 660 936 482 183

MHPP 18 158 150 201 32 6 6 2 2 -

GTPP 272 412 652 1.963 138 131 181 180 30 85

CCPP 740 160 90 550 250 - - - - 750

CFPP 4.304 3.098 2.705 2.199 4.707 5.652 7.213 2.630 2.950 2.240

Other 0,2 25 145 17 7 16 15 6 - -

33

Realization Requirement M

illio

n U

SD

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Generation 2,661.59 1,508.58 2,884.00 4,321.54 3,417.08 1,670.53 3,831.60 6,140.60 9,493.90 10,689.40 12,250.80 11,770.60 9,112.80 6,178.70 4,230.50 3,676.80

Transmission 473.12 1,334.42 1,204.20 973.39 1,434.74 3,100.26 2,470.70 2,527.40 2,667.80 3,340.50 2,182.50 1,176.70 703.50 596.50 268.60 40.70

Distribution 118.28 520.41 671.70 533.12 116.28 317.83 1,214.90 1,158.90 1,194.10 1,206.50 1,337.10 1,384.80 1,452.00 1,529.20 1,594.20 1,694.70

Investment In Power Sector

34

D. Technical Session:

Other Topics on Energy/Power Market

35

To expand renewable energy development in all parts of

Indonesia,

To increase the investment of renewable energy,

To increase the growth of renewable energy industry and jobs,

To increase the ratio of electrified villages.

Feed-in Tariff and Ceiling Price For Renewable

The Government of Indonesia has promoted:

Feed-in Tariff

1. Geothermal

2. Hydro ≤ 10 MW

3. Biomass ≤ 10 MW

Ceiling Price:

1. Photovoltaic

36

1. Geothermal

(MEMR Regulation 22/2012)

PLN shall purchase electricity from the winner of geothermal working area

tender with the price based on the tender it self.

The price is used for Power Purchase Agreement, shall be final and

without negotiation.

In case of failure on the exploration and the feasibility study, then the risk

shall be bear by developer.

Region High Voltage

(sen US$/kWh)

Medium Voltage

(sen US$/kWh)

Sumatera 10 11.5

Java, Madura, Bali 11 12.5

South Sulawesi, West Sulawesi, South East

Sulawesi

12 13.5

North Sulawesi, Central Sulawesi, Gorontalo 13 14.5

NTB, NTT 15 16.5

Maluku, Papua 17 18.5

Feed-in Tariff

37

2. Hydro ≤ 10 MW

Feed-in Tariff (2)

No

.

FIT

(Rp/ kWh)

Interconnected

With Remark

1 656 x F Medium Voltage Ministerial Regulation

No. 04/2012

2 1,004 x F Low Voltage Ministerial Regulation

No. 04/2012

With Factor as follows:

F = 1 Java, Bali Region

F = 1.2 Sumatera, Sulawesi Region

F = 1.3 Kalimantan, Nusa Tenggara

Region

F = 1.5 Maluku, Papua Region

38

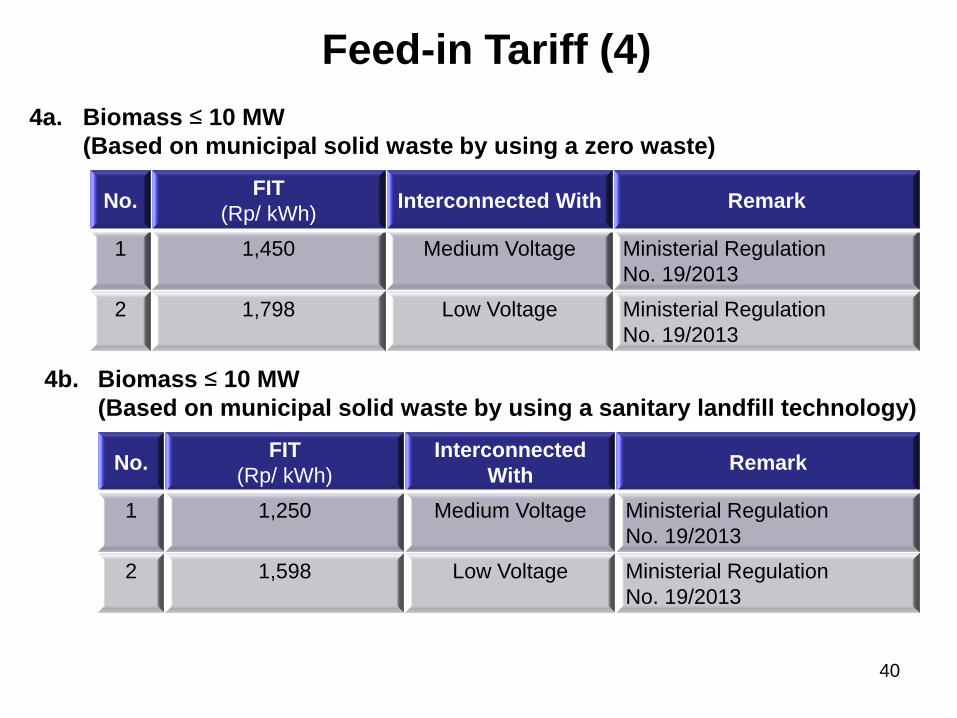

3. Biomass ≤ 10 MW (Based on Biomass and Biogas)

No

.

FIT

(Rp/ kWh)

Interconnected

With Remark

1 975 x F Medium Voltage Ministerial Regulation

No. 04/2012

2 1,325 x F Low Voltage Ministerial Regulation

No. 04/2012

With Factor as follows:

F = 1 Java, Bali, Sumatera Region

F = 1.2 Sulawesi , Kalimantan, Nusa Tenggara

Region

F = 1.3 Maluku, Papua Region

Feed-in Tariff (3)

39

4a. Biomass ≤ 10 MW

(Based on municipal solid waste by using a zero waste)

No. FIT

(Rp/ kWh) Interconnected With Remark

1 1,450 Medium Voltage Ministerial Regulation

No. 19/2013

2 1,798 Low Voltage Ministerial Regulation

No. 19/2013

Feed-in Tariff (4)

4b. Biomass ≤ 10 MW

(Based on municipal solid waste by using a sanitary landfill technology)

No. FIT

(Rp/ kWh)

Interconnected

With Remark

1 1,250 Medium Voltage Ministerial Regulation

No. 19/2013

2 1,598 Low Voltage Ministerial Regulation

No. 19/2013

40

Photovoltaic

Ceiling Price

No

.

FIT

(cent/ kWh)

Requirement

Remark

1 25 - Ministerial Regulation

No. 17/2013

2 30 40 % domestic

component level

Ministerial Regulation

No. 17/2013

41

Thank you

42