Individual vs. Collective Choice in Latin America Social Security Systems Augusto Iglesias P....

31

Individual vs. Collective Individual vs. Collective Choice in Choice in Latin America Latin America Social Security Systems Social Security Systems Augusto Iglesias P. Augusto Iglesias P. PrimAmérica Consultores PrimAmérica Consultores Santiago, Chile Santiago, Chile A A p p ril, 2002 ril, 2002

-

Upload

silas-stafford -

Category

Documents

-

view

215 -

download

1

Transcript of Individual vs. Collective Choice in Latin America Social Security Systems Augusto Iglesias P....

Individual vs. Collective Individual vs. Collective Choice inChoice in Latin AmericaLatin America Social Security SystemsSocial Security Systems

Augusto Iglesias P.Augusto Iglesias P.

PrimAmérica ConsultoresPrimAmérica Consultores

Santiago, ChileSantiago, Chile

AAppril, 2002ril, 2002

Personal pension plans in LAPersonal pension plans in LA

• The objective of this presentation is to explain and discuss the role of individual choice in personal pension plans in LA Social Security Systems.

• When private pension funds (PPF) were introduced as part of LA Social Security Systems, they were designed as personal pension plans, and all forms of collective choice were excluded. So, in LA, PPF members must decide on an individual basis which fund manager will handle their personal account and which pension mode to contract at retirement.

• Now, with many years of accumulated experience, we are in better position to assess the costs and benefits of this particular form of design in the context of the operation of a mandatory and funded Pension System.

A brief review of pension reformA brief review of pension reform in in LALA

• In the last decade, a number of LA countries have introduced extended reforms to their pension systems, which include the creation of private pension funds (PPF).

• LA PPF share some common characteristics. In particular:

They are DC. They are managed by competitive, private and single-

purpose firms. Several pension options (modes) are offered to

participants. Pensions can be offered by the fund managers (under the scheduled withdrawal mode) or by life insurance companies (under the life annuities mode).

They are based almost exclusively on personal savings accounts.

They are regulated and supervised by specialized agencies.

Continue

Characteristics of private pension funds Characteristics of private pension funds in LAin LA

Source: Schmidt-Hebbel (1999)

Results of private pension funds in Results of private pension funds in LALA

Argentina (09.01) 21.102 8,87% 8.751.559 30.545Bolivia (11.01) 1.024 NA 669.679 NAColombia (11.01) 4.799 7,54% 4.303.892 3.529Chile (02.02) 35.365 10,70% 6.427.656 634.740El Salvador (09.01) 688 12,94% 907.388 NAMéxico (01.02) 2.298 9,35% 26.518.534 NAPerú (12.01) 4.063 NA 2.732.071 27.806Uruguay (09.01) 993 NA 591.751 NA

Source: PrimAmérica Consultores.

(2) Annual average since commencement of operations

(3) Old Age, Disability and Survivorship

For conversion to US$ the value of the exchange rate at the end of each month is used.

PENSIONERS (4)

PENSION FUND YIELD (2)

MEMBERS (3)PENSION FUND (US$ Billion) (1)

Country

Individual choice en LA PPFIndividual choice en LA PPF

• PPF members can choose between:

Different fund managers; In few countries, different pension funds offered by

each manager; Different pension modes.

• Although regulators did realize that individual choice has some costs compared to different forms of collective choice (higher information costs; marketing costs; etc.) they decided not to introduce any element of collective decisions into the pension systems.

Why Why the option in favor of PPF with the option in favor of PPF with personal accounts and individual personal accounts and individual

choice in LA?choice in LA?

Continue

Reformers wanted to foster individual responsibility in pension decisions. They had the intention to build new pension systems based on different foundations compared to the traditional systems, and these new systems should be consistent with the new market oriented strategy of economic development of their countries.

Individual responsibility implies individual choice, and from this follows the existence of personal savings accounts.

Continue

Some countries feared that labor unions could play an undesired role in pension decisions if some specific forms of collective choice were authorized.

There is a strong belief that the combination of

personal accounts + individual choice + competition, should protect the pension systems from political risk.

Why Why the option in favor of PPF with the option in favor of PPF with personal accounts and individual personal accounts and individual

choice in LA?choice in LA?

Why Why the option in favor ofthe option in favor of PPF PPF with with personalpersonal accounts accounts and and individual individual

choice in LA?choice in LA?

• Also, there were some objective conditions that made difficult to design the new system on the basis of employers (occupational) pension plans:

In many LA countries the largest employer is the government.

The average size of firms is small; long term careers are not very common; and the informal sector plays an important role in LA economies.

Labor mobility was to be encouraged. One objective of pension reform was to give workers

as much freedom as possible to decide their age of retirement.

How effective How effective havehave been been PPF with PPF with individual choice asindividual choice as an instrument to an instrument to

reach those reach those goalsgoals??• Since the counterfactual (for example, a funded and

private system based on employers pension plans) does not exist in LA, it´s particularly difficult to offer any strong evidence that could help to support an answer to this question.

• However, we believe that personal pension plans with individual choice have been very effective to:

Increase worker´s demand for information regarding the characteristics and operation of the pension system.

Develop a new awareness of pension fund members regarding the relationship between personal and political decisions and the results of the pension system.

Continue

Improve the quality of pension funds governance.

Promote competition among fund managers.

(Then, personal pension plans with individual choice have been effective in protecting the new pension systems from political risk).

How effective How effective havehave been been PPF with PPF with individual choice asindividual choice as an instrument to an instrument to

reach those reach those goalsgoals??

What have been the cWhat have been the costs osts (problems)(problems) of of PPF with individual PPF with individual

choice?choice?

• Compared with pension plans wich include elements of collective choice (like employers or occupational pension plans) the LA solution faces some difficult challenges:

Lower price elasticity of demand. Higher marketing costs for pension fund managers. The information costs for members are high. High marketing costs of annuities. Adverse selection in the market for annuities High operational costs of the pension system.

Fees in LAC´s PPFFees in LAC´s PPF

FIXED TOTAL PERCENTAGE INSUR.PREMIUM % NET % OF ACCOUNT

(US $) (OF WAGE) /(a) (a) (OF WAGE) BALANCE

(1) (2) (1) - (2)

Argentina (09.01) 2,90 2,98% 1,41% 1,57% N.A.Bolivia (11.01) - 2,50% 2,00% 0,50% 0,23%Colombia (11.01) 0,00 3,50% 1,91% 1,59% N.A.Chile (04.02) 0,90 2,36% 0,67% 1,69% N.A.El Salvador (09.01) 0,00 2,98% 1,29% 1,69% N.A.

México (01.02) - 1,50% - 1,50% 0,30%Perú (12.01) 0,00 3,73% 1,34% 2,39% N.A.Uruguay (09.01) 0,42 2,81% 0,83% 1,99% N.A.

FOR COMPULSORY CONTRIBUTIONS

(a) FEES AS A % OF THE WAGE.

SOURCE: PRIMAMERICA CONSULTORES

Marketing costs in LAC´s PPF (*)Marketing costs in LAC´s PPF (*)

Argentina (07.00 / 06.01) 285.315 553.947 51,5% 8.751.559 32,6 Chile (01,01-12.01) 48.220 136.641 35,3% 6.427.656 7,5 El Salvador (09.01) 4.582 27.074 16,9% 907.388 5,0 México (01.01-12.01) 85.752 704.634 12,2% 26.518.534 3,2 Perú (01.01-12.01) 29.904 70.247 42,6% 2.732.071 10,9

Source: PrimAmérica Consultores.

(1) Includes marketing cost and compensations to sales agents.

(2) Includes compensation to administrative staff and administration and computational costs.

(*) EXPRESSED AS AN ANNUAL FIGURE

MEMBERS (4)(3) = (1)/(2)(5) = (1)/(4)

(US$)COMMERCIAL

EXPENSES (M US$) (1)OPERATIONAL EXPENSES

(M US$) (2)Country

Chile: life annuities intermediation Chile: life annuities intermediation costscosts

(% of premium paid)(% of premium paid)

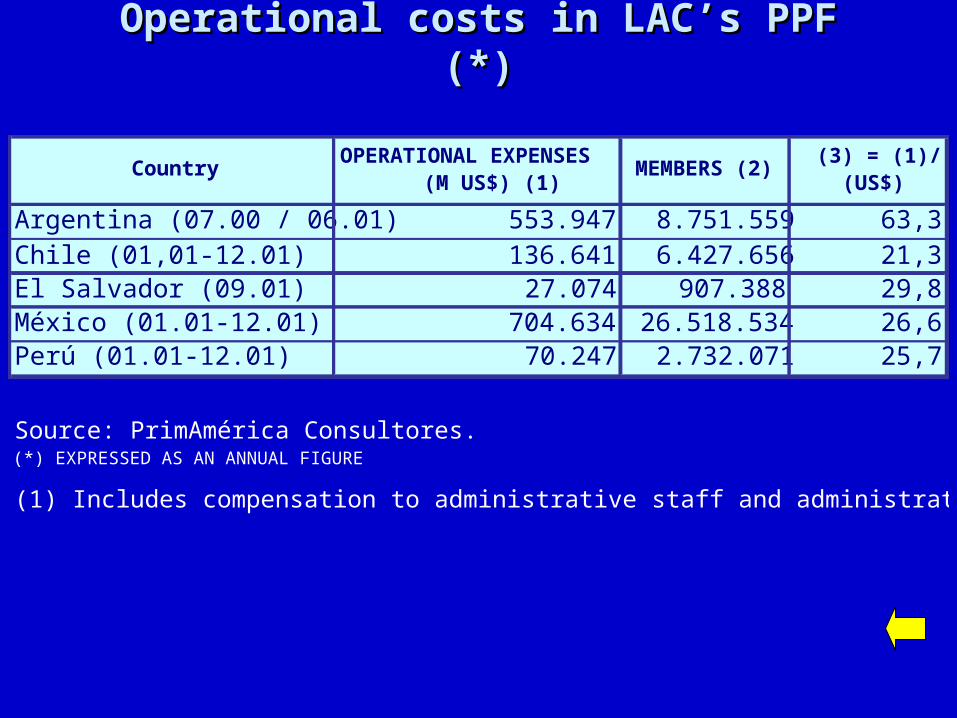

Operational costs in LAC’s PPF (*)Operational costs in LAC’s PPF (*)

Argentina (07.00 / 06.01) 553.947 8.751.559 63,3 Chile (01,01-12.01) 136.641 6.427.656 21,3 El Salvador (09.01) 27.074 907.388 29,8 México (01.01-12.01) 704.634 26.518.534 26,6 Perú (01.01-12.01) 70.247 2.732.071 25,7

Source: PrimAmérica Consultores.

(1) Includes compensation to administrative staff and administration and computational costs.

(*) EXPRESSED AS AN ANNUAL FIGURE

MEMBERS (2)(3) = (1)/(2)

(US$)OPERATIONAL EXPENSES

(M US$) (1)Country

Limits to individual choice in LA Limits to individual choice in LA PPFPPF

• To control for at least some of these problems, regulation of personal pension plans in LA include some specific provisions which restrict individual choice:

Each member can select only one fund manager (personal savings accounts can not be split between managers). Also, in most countries each pension fund manager can manage only one fund and the structure of the fund´s portfolio is regulated.

Fees are non-negotiable (same fees for everybody). Each pensioner can not take the accumulated balance

as a lump-sum and can choose only one pension mode (personal balances cannot be split in different pension modes and there is a limited number of pension modes).

The impact of limits to individual The impact of limits to individual choice: perceived benefitschoice: perceived benefits and and

costs costs

• Those regulations have helped to decrease information and supervision costs of PPF. Then, from this perspective they have been succesful.

• However the problem of high operational and marketing costs which is associated to personal pension plans with individual choice, has not been avoided. Also, price competition among fund managers is not intense.

Continue

The impact of limits to individual The impact of limits to individual choice: perceived benefitschoice: perceived benefits and and

costscosts

• Moreover, limits to individual choice have created some other problems:

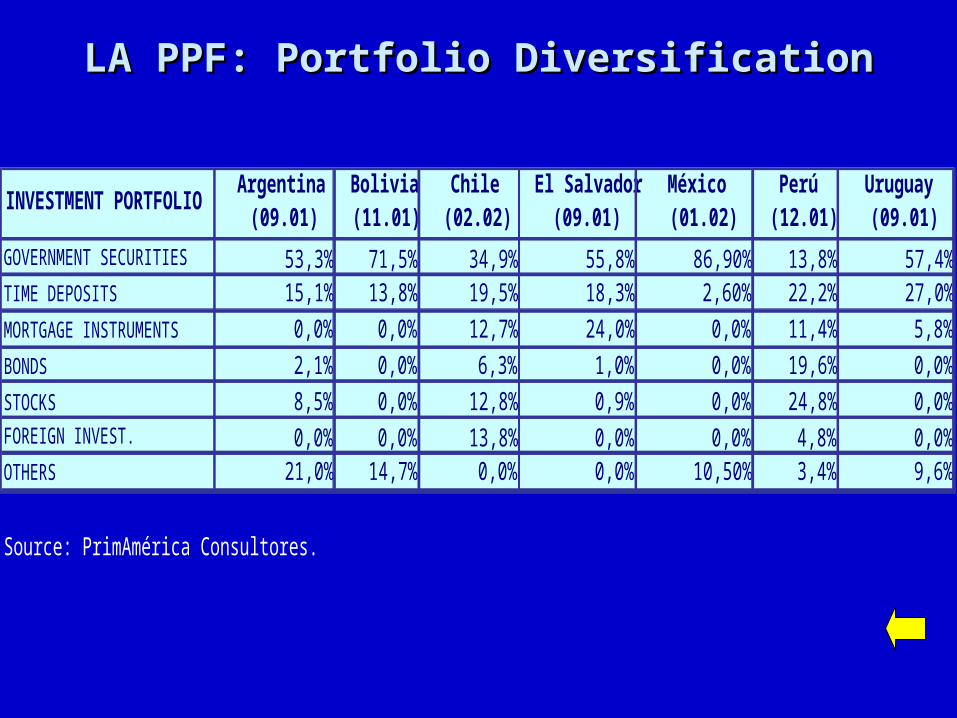

Limited opportunities for portfolio diversification mean lower long term expected returns and increased political risks (Argentina´s case). It could also mean a higher cost of government guarantees.

Limits on the number of available different pension funds and the imposibility of splitting the balance of personal accounts among different managers have also increased the political risks faced by the pension system, since they have contributed to a trend towards industry concentration.

LA PPF: Portfolio DiversificationLA PPF: Portfolio Diversification

GOVERNMENT SECURITIES 53,3% 71,5% 34,9% 55,8% 86,90% 13,8% 57,4%TIME DEPOSITS 15,1% 13,8% 19,5% 18,3% 2,60% 22,2% 27,0%

MORTGAGE INSTRUMENTS 0,0% 0,0% 12,7% 24,0% 0,0% 11,4% 5,8%

BONDS 2,1% 0,0% 6,3% 1,0% 0,0% 19,6% 0,0%

STOCKS 8,5% 0,0% 12,8% 0,9% 0,0% 24,8% 0,0%FOREIGN INVEST. 0,0% 0,0% 13,8% 0,0% 0,0% 4,8% 0,0%OTHERS 21,0% 14,7% 0,0% 0,0% 10,50% 3,4% 9,6%

Source: PrimAmérica Consultores.

INVESTMENT PORTFOLIOEl Salvador

(09.01)México (01.02)

Perú (12.01)

Uruguay (09.01)

Argentina (09.01)

Bolivia (11.01)

Chile (02.02)

Organization of PPF´s in LAC: Organization of PPF´s in LAC: trend to industry concentrationtrend to industry concentration

Organization of PPF´s in LAC: Organization of PPF´s in LAC: trend to industry concentrationtrend to industry concentration

• Collective choice mechanisms could be used:

To select fund manager (and, eventually, to select among different portfolios);

To negotiate fees with fund managers;

To buy pensions (particulary, annuities).

Is collective choice the solution for Is collective choice the solution for present problems of LA PPF?present problems of LA PPF?

Continue

Is collective choice the solution for Is collective choice the solution for present problems of LA PPF?present problems of LA PPF?

• There are three main different ways to introduce elements of collective choice into LA PPF:

Employers (ocupational) pension plans. Labor Unions making some pension decisions for their

members. Voluntary groups formed by PPF members.

Continue

• Employers pension plans are criticized because they could impose limits to labor movility and to the pension decision. Also, the characteristics of LA labor market do not favor this solution.

• There is a strong opposition to leave pension decisions in the hands of labor unions, because of political reasons and their very limited coverage.

• The idea of voluntary groups has not yet received systematic consideration (It could be used to buy life annuities).

Is collective choice the solution for Is collective choice the solution for present problems of LA PPF?present problems of LA PPF?

Continue

• Collective choice is always associated to principal-agent problems. Because in LA there is a high risk of political interference in decisions regarding the operation of the pension system, this problem can be particularly difficult to manage.

• Since individual responsibility is weakened under collective choice arrangements, some incentives to efficiency in the operation of the pension system are lost.

• A strong opposition to the idea of “going collective” must be expected.

Is collective choice the solution for Is collective choice the solution for present problems of LA PPF?present problems of LA PPF?

Policy lessons from LA: the Policy lessons from LA: the importance of preserving importance of preserving

((enhancingenhancing) individual choice) individual choice in in mandatory mandatory pension systemspension systems

1. LA experience shows that personal pension plans with individual choice can play an effective role in the solution of social security problems and that, in particular, they help to protect the pension system from political risk and contribute to the creation of a “culture” of personal savings.

Continue

2. Although some limits to individual choice within personal pension plans are necessary (since there are differences between private and social objectives regarding pension systems), in some LAC (those with more developed PPF) present limits to individual choice may have more costs than benefits.

3. These costs come mainly from: Investments regulations: if members were to have the opportunity

to choose between more and different funds, this would imply (in the aggregate) better portfolio diversification. This should help to increase long term pension funds return (and so, pensions) and to decrease the political risk faced by the pension system even further.

Current restrictions on portfolio manager selection increase the obstacles to entry to the pension fund management industry and may lead to higher market concentration.

Policy lessons from LA: the Policy lessons from LA: the importance of preserving importance of preserving

((enhancingenhancing) individual choice) individual choicein pension systemsin pension systems

Continue

4. On the other hand, the area where limits to individual choice may always be necessary, is on the use of personal balances at retirement: most pensioners will have a strong preference for present consumption so there is risk of them maximizing short term pensions and taking too much longevity risk, which is contrary to the social objectives of the pension systems. To mandate a minimum degree of annuitization may then be necessary.

Policy lessons from LA: the Policy lessons from LA: the importance of preserving (importance of preserving (enhancingenhancing) )

individual choiceindividual choicein pension systemsin pension systems

Continue

5. The benefits of limiting individual choice are more evident at the early stages of pension reform and in countries with underdeveloped financial markets and where people have limited personal savings (and limited financial “literacy”). However, as the new pension systems mature and workers, pensioners, supervisors and fund managers gain experience, the costs of these limits become evident. So, changes in regulation wich open more space to individual choice (including the freedom to form groups to make collective choices) should come gradually.

Policy lessons from LA: the importance of Policy lessons from LA: the importance of preserving (preserving (enhancingenhancing) individual choice) individual choice

in pension systemsin pension systems

Continue

6. From this perspective, it seems that, at least, in LA personal pension plans with individual choice have advantages over pension plans based on collective choice (like employers pension plans) to become a part of mandatory social security.

However, employer pension plans should have a greater role as a voluntary complement to social security.

7. In fact the role of employers pension plans will increase gradually with:

Economic development (increases in income and improvements of the tax systems);

Increase in average size of firms; Increase in wages (over contributable wage).

Policy lessons from LA: the importance Policy lessons from LA: the importance of preserving (of preserving (enhancingenhancing) individual ) individual

choicechoice in pension systems in pension systems