Individual Development Accounts: A strategy for fostering social and economic participation Asset...

43

Individual Development Accounts: A strategy for fostering social and economic participation Asset Development & Tax Policy 2004 Disability Program Navigator Series October 21, 2004 Tobey Davies, School of Community Economic Development

-

Upload

aldous-randall-price -

Category

Documents

-

view

217 -

download

0

Transcript of Individual Development Accounts: A strategy for fostering social and economic participation Asset...

Individual Development Accounts:A strategy for fostering social and

economic participation

Asset Development & Tax Policy2004 Disability Program Navigator Series

October 21, 2004

Tobey Davies, School of Community Economic Development

Introduction

• Asset Building policies

•Relevant of social & economic theories

• Strategies, particularly IDAs

•NH Statewide IDA Collaborative

•Research

Reality

“Few people have spent their way out of being poor. Those who do do so by saving and investing for

long term goals.”

– Michael Sherridan, Assets and the Poor

Theory discussion

Internal locus of control

•life satisfaction

•ability to mobilize resources

Role theory

•Adapting to expectations, rules, circumstances.

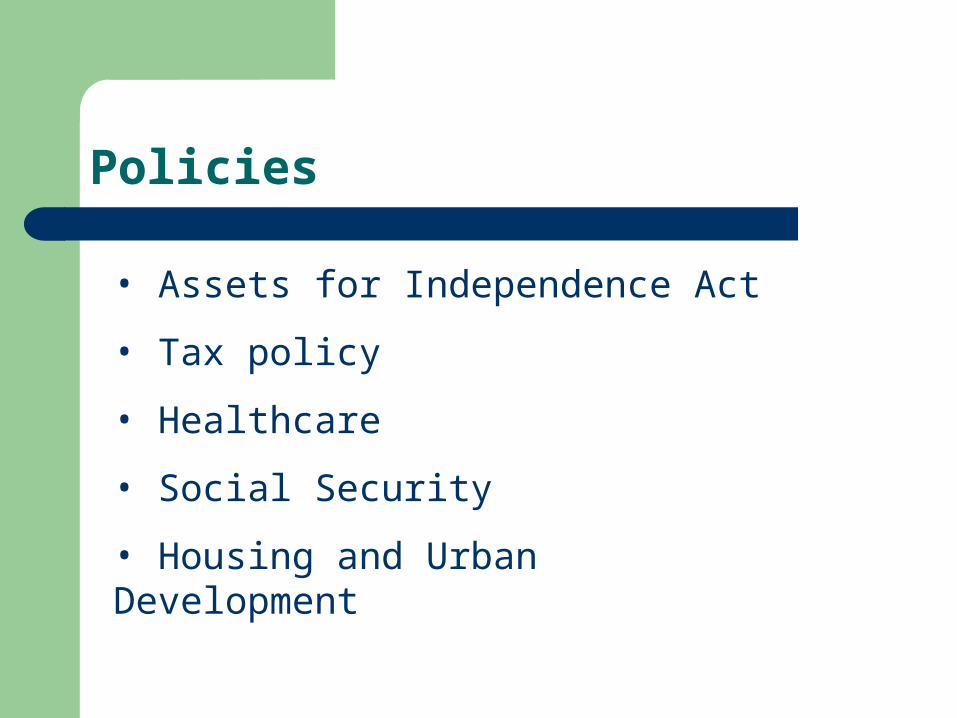

Policies

• Assets for Independence Act

• Tax policy

• Healthcare

• Social Security

• Housing and Urban Development

Bipartisan support

• Conservatives likely to view assets as vehicle for self-reliance

•Liberals often view as re-distribution of resources

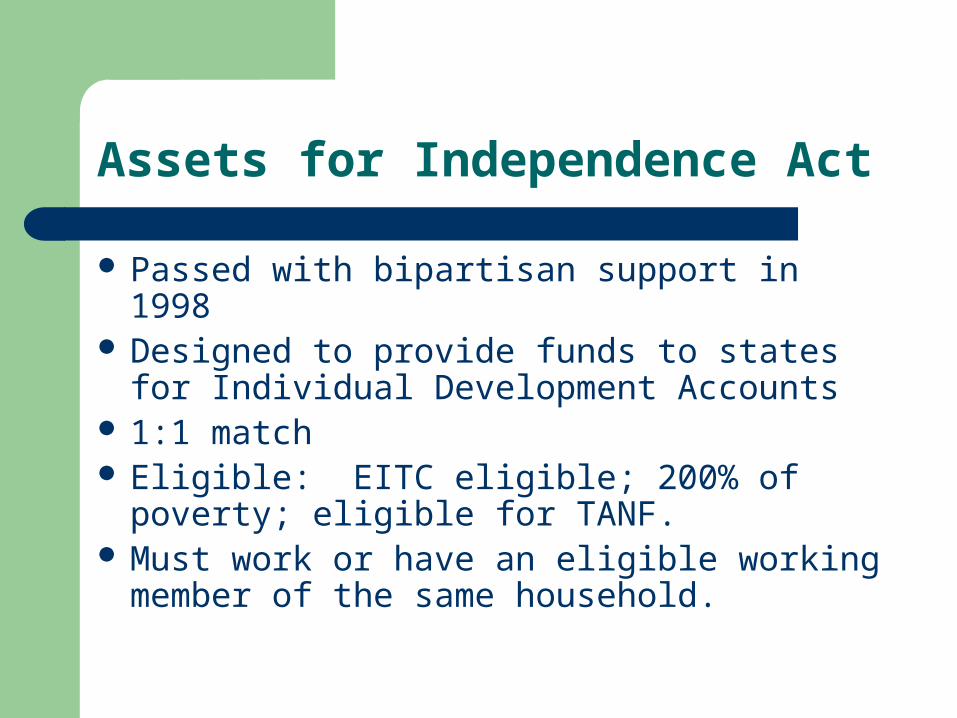

Assets for Independence Act

Passed with bipartisan support in 1998 Designed to provide funds to states for

Individual Development Accounts 1:1 match Eligible: EITC eligible; 200% of poverty;

eligible for TANF. Must work or have an eligible working

member of the same household.

“Making Work Pay”(Center on Budget and Policy Priorities, 2003)

Earned Income Tax Credit Work incentive to workers and self

employed Available to child & childless singles.

Must file for taxes

EITC, cont.

For workers w/o children between ages of 25-65, credit exceeds $382

Gives back some or all of federal income tax taken out of pay.

May get additional cash back from IRS

EITC, cont.

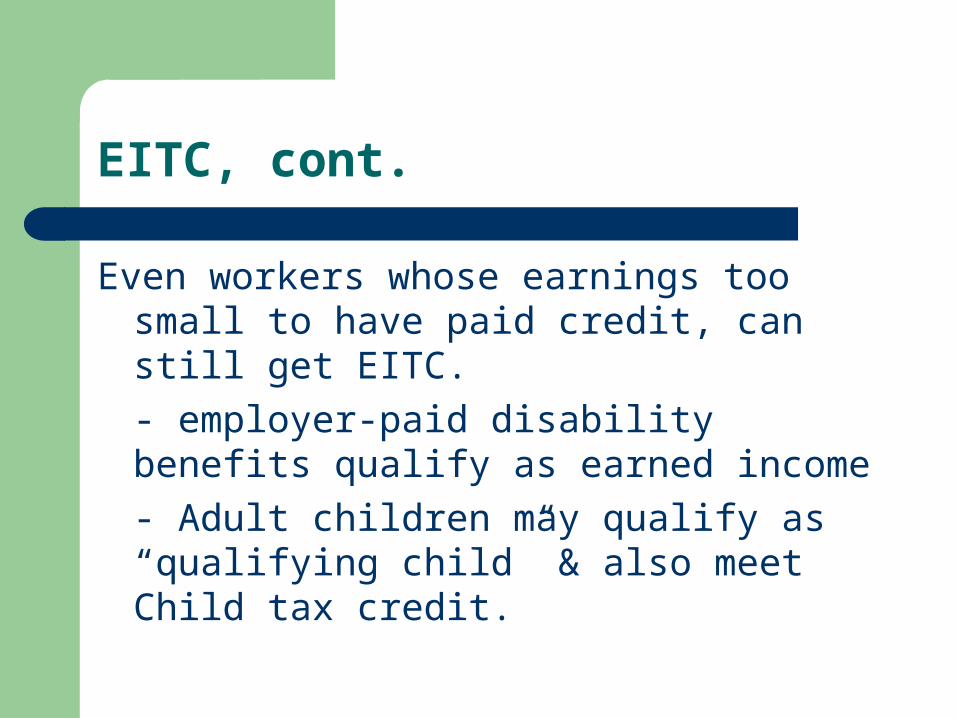

Even workers whose earnings too small to have paid credit, can still get EITC.

- employer-paid disability benefits qualify as earned income

- Adult children may qualify as “qualifying child” & also meet Child tax credit.

Medicaid Buy In Programs

Work incentive: maintaining healthcare coverage

Sliding fee scale

Income standards for eligibility

Changed treatment of savings from earnings

Social Security Work Incentives

2 for 1 disregard

Impairment related work expenses

Plans for Achieving Self Support

Unencumbered Business Expenses

Other mechanisms for asset building

Independence Building Accounts

Special Needs Trusts*

*Not owned by beneficiaries

Social Security Protection Act 2003

For a period of 9 months…. Disregard retroactive checks from SSA or

SSI

EITC refunds

Child Tax Credit refunds

SSPA 2003, cont.

Effective June 2004, disregarding: All education related income, scholarship, fellowships, and gifts income.

Not counting as a resource in SSI for 9 months

SSPA, cont.

Individual Development Accounts Allowable to individuals

Disregard income placed in exempt IDA, reducing countable income

Adapting economic policy to create the means for social outcome.

Other policies

Section 8 Home Ownership Voucher

CARE Act, S.476 = 300,000 IDAs

Special Needs Trusts*

Background NHCLF (CDFI)

Mission

To serve as a catalyst, leveraging financial, human, and civic resources to enable traditionally under-served people to participate more fully in NH economy.

Strategies

•Provide loans, capital, and technical assistance

•Complementing and extending the reach of conventional lenders and public institutions; and

•Bringing people and institutions together to solve problems

Program Areas

•Affordable housing

•Community facilities

•Economic opportunity

NH Statewide IDA Collaborative

AFIA-funded Statewide IDA Collaborative designed to help eligible low income

workers of New Hampshire achieve the dream of homeownership, post-secondary

education or small business startup/development.

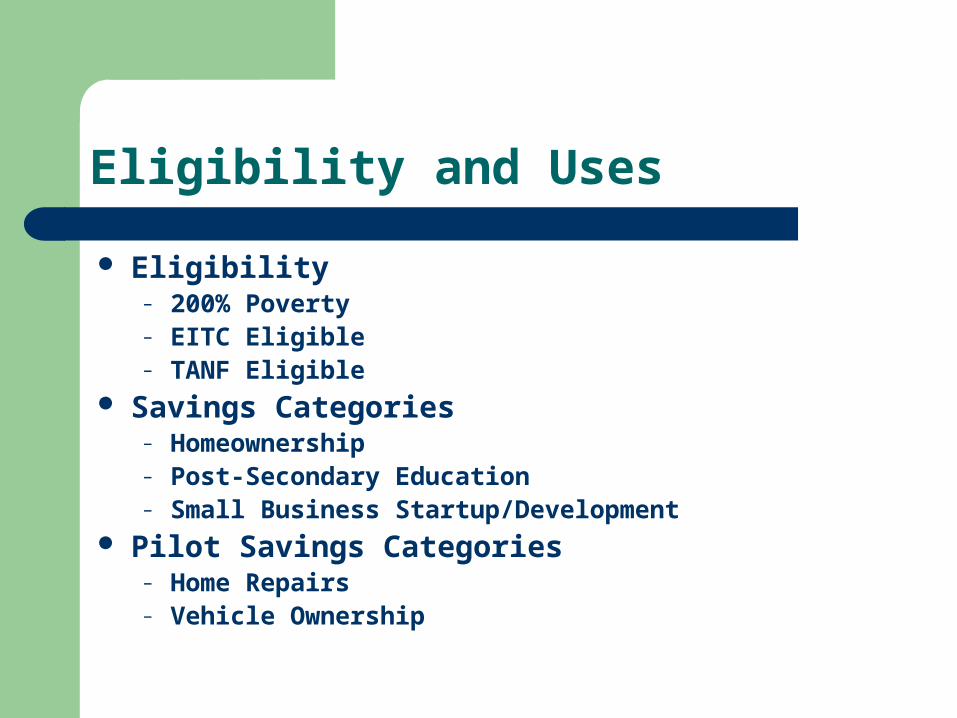

Eligibility and Uses

Eligibility– 200% Poverty– EITC Eligible– TANF Eligible

Savings Categories– Homeownership– Post-Secondary Education– Small Business Startup/Development

Pilot Savings Categories– Home Repairs– Vehicle Ownership

Match Structure

3:1 match $25/month minimum savings $100/month maximum savings $1,000/year savings cap $2,000 lifetime savings cap

$6,000 maximum match per individual

Organizational Structure

• 20 Community Partners – Front End

• NHCLF- Backroom Operations

• Financial Institutions – Hold IDA Accounts

•Other Partners – Provide training and referrals

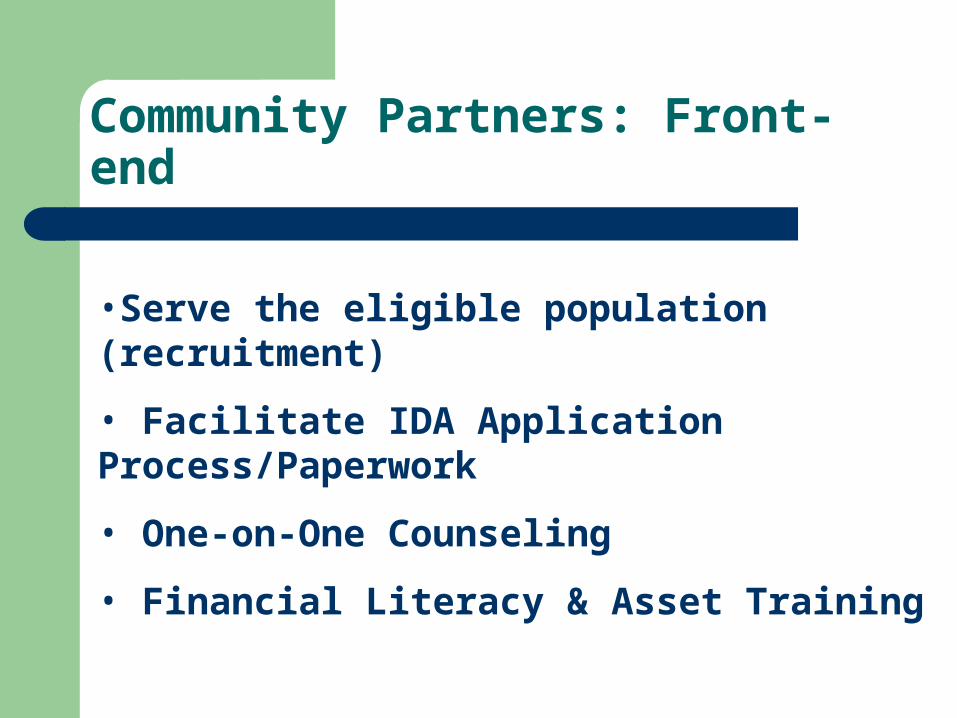

Community Partners: Front-end

•Serve the eligible population (recruitment)

• Facilitate IDA Application Process/Paperwork

• One-on-One Counseling

• Financial Literacy & Asset Training

NHCLF – Backroom Operations

• Raise Match Funds

• Provide Technical Assistance and

• Tracking Savings, Match & Training

• Match Savings Statements

• Central Coordinating Agency of all Partners

Financial Institutions

• Specific Features

•Custodial

•No Fees & Interest Earning

•Duplicate Statements (1 to client, 1 to NHCLF)

•Provide Funding for the IDA Collaborative

• Training and TA on financial education topics

Other Partners

Other Partners include: Cooperative Extensions, Homebuyer Education Centers, Higher Education Assistance Centers

Provide Financial Fitness and/or Asset Specific Training

Work with Community Partners to enhance/develop curriculums

NH Statewide IDA Collaborative highlights….

Each Community Partner holds “ownership” over their Program.

Program rules/updates are discussed at Quarterly Community Partner Meetings

NHCLF Provides no operational dollars to the partners to run the Program

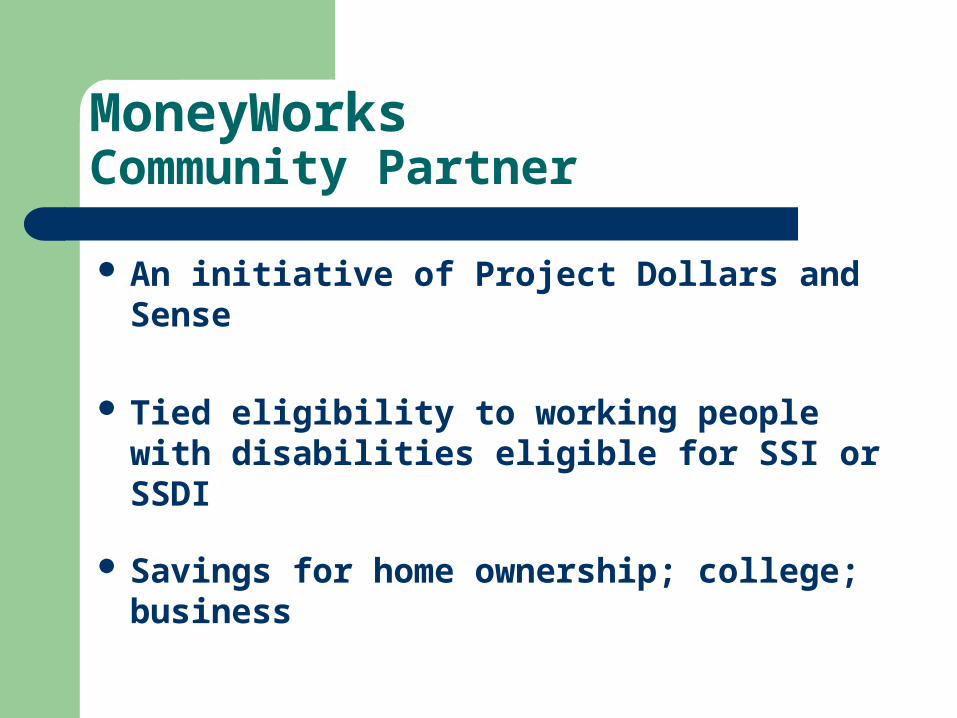

MoneyWorksCommunity Partner

An initiative of Project Dollars and Sense

Tied eligibility to working people with disabilities eligible for SSI or SSDI

Savings for home ownership; college; business

Problem

Real or perceived financial disincentives

Difficulty navigating public benefit system

Un-served or under-served by financial institutions

Low-wages

Lack of support

Goals

Plan public benefits necessary in order to work and improve economic well-being

Use financial services successfully

Develop positive financial habits and credit history

Methods

Integrated counseling (benefits, credit, asset training)

Peer Support

Financial education workshops

Affordable financial services

Individual Development Accounts

Money Works Infrastructure

$ CDFI $

Credit Union

Benefit

Planners

Self Help Groups

Certified

Credit

Counselors

Affordable Housing Group

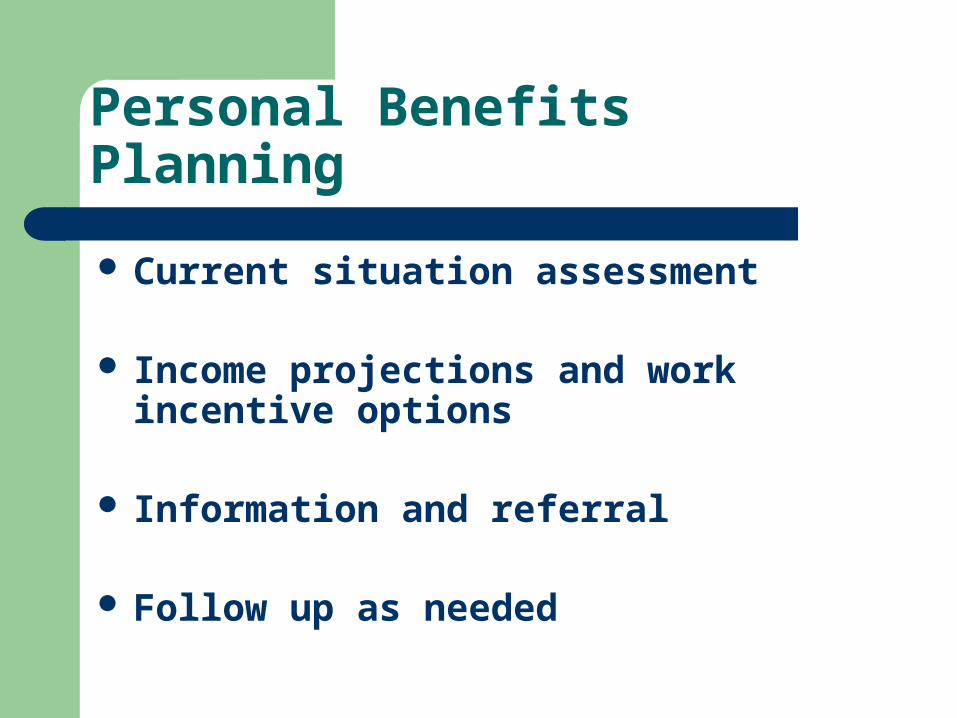

Personal Benefits Planning

Current situation assessment

Income projections and work incentive options

Information and referral

Follow up as needed

Certified Credit Counseling

• Credit history & recommendations

• Spending & Savings Plans

• Credit Use and management

• Survival skills in the marketplace

• Preparing for asset goal

Asset Based Training

Home Ownership

Postsecondary education

Self employment

Peer Support

• Savings clubs and buying coops

• Managing illness and financial wellness

• Organization skills

• Navigating marketplace

• Working toward goals

Equity building….

IDA$3,600 FHLB

$12,000

DMHD$2,500

CPI$20,000

NHHFA$5,000

MNHS$25,000

NH Statewide IDA Collaborative highlights….

After 3 years…– 565 Total Enrolled 330 Actively Enrolled

281 Home; 21 Education; 22 Business; 6 Other

– 78 Graduates of Homeownership (as of 10/21/04)– $532,106 Saved– $1,350,695 Matched– $ 384,940 Match Paid Out

Research

• Asset Accumulation & Tax Policy (NIDRR)

• LIFE Account Feasibility Study & Implementation Plan (CMS)

• National Tax Facts Coalition

• Youth Transition Grants – SSA

Resources

Corporation for Enterprise Development (CFED): www.cfed.org

World Institute on Disability: www.wid.org/equity

Center for Social Development: www.gwbweb.wustl.edu/csd

Center on Budget & Policy Priorities: www.cbpp.org

Contact Information

Tobey DaviesCenter for CED and DisabilitySchool of CED/SNHU2500 No. River RoadManchester, NH 03106-1045

Phone: 603-644-3103 Fax:[email protected]