Indie Business Census 2015 Radio Independents Group 10 March 2015 Gill...

23

Indie Business Census 2015 Radio Independents Group 10 March 2015 Gill Hind [email protected] +44 20 7851 0913 Julian Aquilina [email protected] +44 20 7851 0907

-

Upload

julie-jones -

Category

Documents

-

view

216 -

download

2

Transcript of Indie Business Census 2015 Radio Independents Group 10 March 2015 Gill...

Indie Business Census 2015

Radio Independents Group

10 March 2015

Gill Hind [email protected] +44 20 7851 0913Julian Aquilina [email protected] +44 20 7851 0907

Context

Indie Business Census, March 2015 2

• Radio Independents Group (RIG) commissioned a survey of its members and the wider radio production sector to gain a fuller understanding of the strength and diversity of the independent radio.

• The results of the survey would feed into RIG’s submission to the BBC Trust in response to its consultation paper BBC Trust review of the BBC’s arrangements for the supply of television and radio content and online services in January 2015

• The online survey ran from 8 December 2014 until 13 February 2015, and they were 85 respondents in total

• Enders Analysis, as an independent research company, was asked to analyse the data on behalf of RIG

• We have aggregated the data so as to ensure complete financial confidentiality for all respondents and no RIG member or employee has had access to the individual results

• We have analysed the outputs across all respondents and have also broken down the respondents into three bands, sorted by commissioned radio production revenues:

– Larger indies (5)

– Medium indies (10)

– Smaller indies (70)

• Results are shown on the following slides

Office location

Indie Business Census, March 2015 3

London (within M25)38%

North West England15%

Scotland9%

South East (excl Lon-

don)8%

Wales6%

South West5%

Yorkshire and the Humber

5%

Northern Ire-land3%

West Mid-lands

3%

East Mid-lands

2%

East Anglia1%

North East England1%

Ireland1%

Other5%

Location of all offices by region

[Source: RIG Indie Business Census 2015]

London (within M25)38%

England (excl London)

38%

Nations18%

Ireland1%

Other5%

Location of all offices

[Source: RIG Indie Business Census 2015]

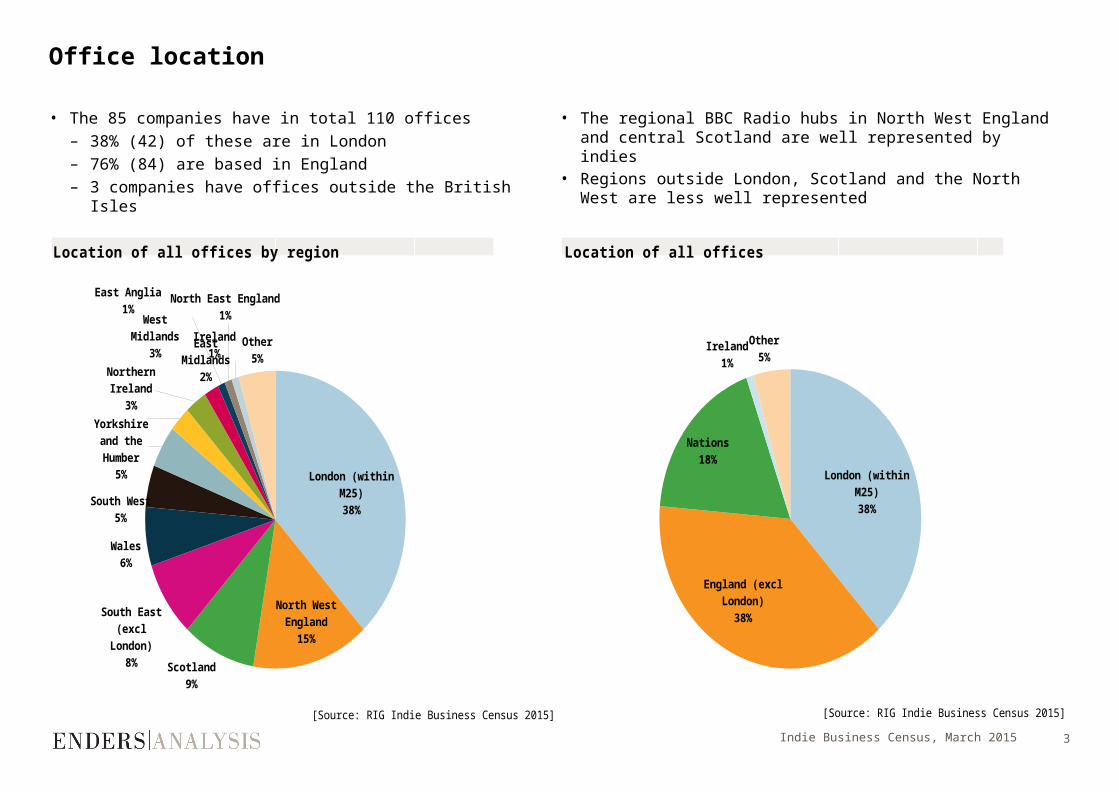

• The 85 companies have in total 110 offices– 38% (42) of these are in London– 76% (84) are based in England– 3 companies have offices outside the British Isles

• The regional BBC Radio hubs in North West England and central Scotland are well represented by indies

• Regions outside London, Scotland and the North West are less well represented

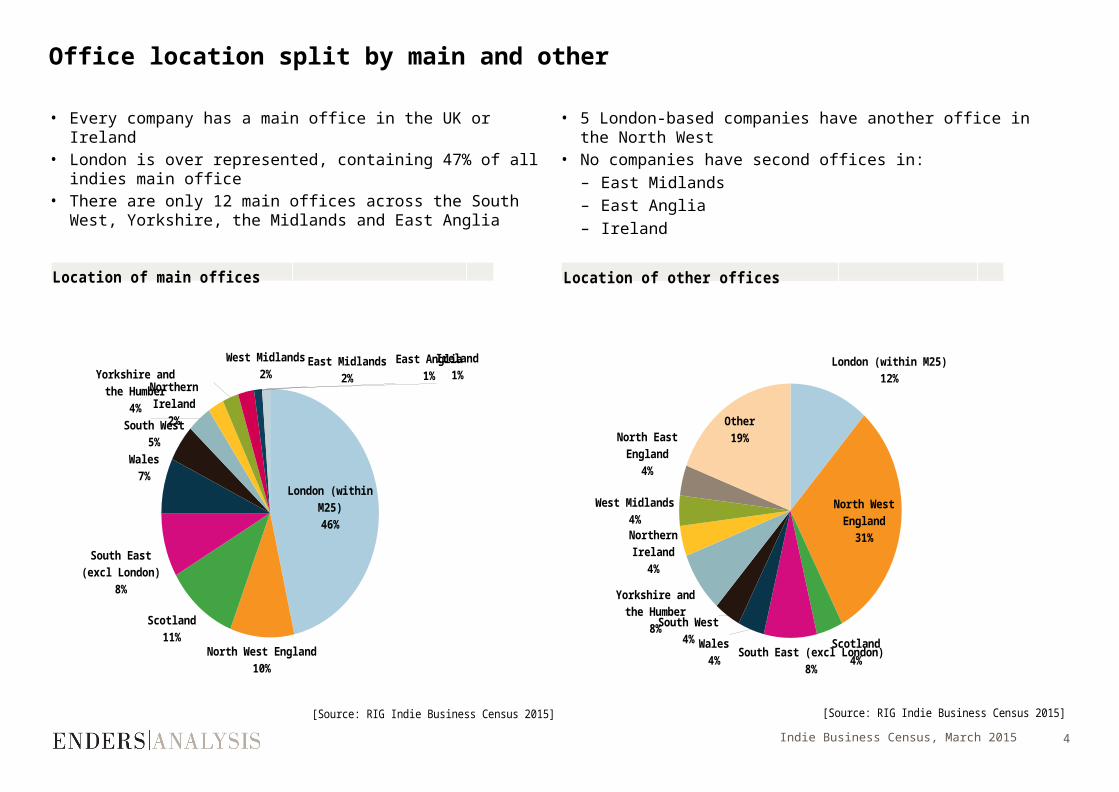

• Every company has a main office in the UK or Ireland• London is over represented, containing 47% of all indies

main office• There are only 12 main offices across the South West,

Yorkshire, the Midlands and East Anglia

Office location split by main and other

Indie Business Census, March 2015 4

London (within M25)

46%

North West England10%

Scotland11%

South East (excl London)

8%

Wales7%

South West5%

Yorkshire and the Humber

4%

Northern Ire-land2%

West Midlands2%

East Midlands2%

East Anglia1%

Ireland1%

Location of main offices

[Source: RIG Indie Business Census 2015]

London (within M25)12%

North West England

31%

Scotland4%South East (excl London)

8%

Wales4%

South West4%

Yorkshire and the Humber

8%

Northern Ire-land4%

West Midlands4%

North East Eng-land4%

Other19%

Location of other offices

[Source: RIG Indie Business Census 2015]

• 5 London-based companies have another office in the North West

• No companies have second offices in:– East Midlands– East Anglia– Ireland

Total turnover of all companies was £38.7m

Indie Business Census, March 2015 5

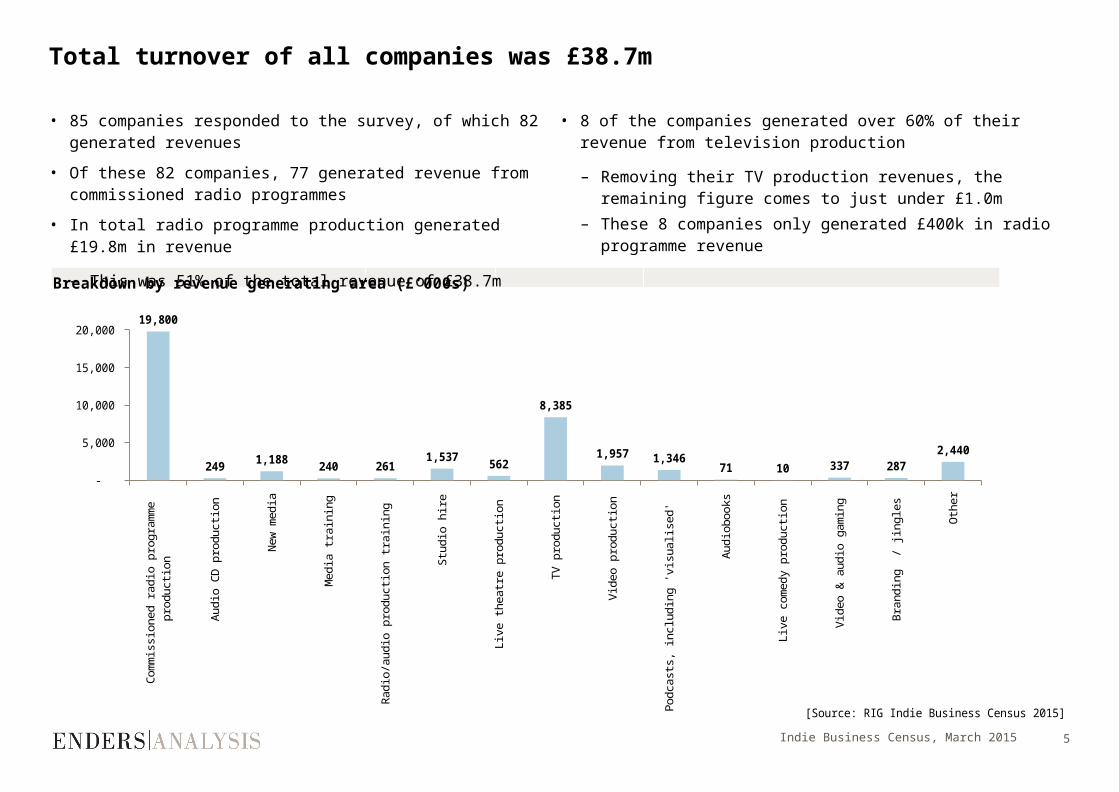

• 8 of the companies generated over 60% of their revenue from television production

– Removing their TV production revenues, the remaining figure comes to just under £1.0m

– These 8 companies only generated £400k in radio programme revenue

Com

mis

sion

ed

rad

io p

rog

ram

me p

rod

ucti

on

Au

dio

CD

pro

du

cti

on

New

med

ia

Med

ia t

rain

ing

Rad

io/a

ud

io p

rod

ucti

on

tra

inin

g

Stu

dio

hir

e

Liv

e t

heatr

e p

rod

ucti

on

TV

pro

du

cti

on

Vid

eo p

rod

ucti

on

Pod

cast

s, in

clu

din

g 'vis

ualis

ed

'

Au

dio

books

Liv

e c

om

ed

y p

rod

ucti

on

Vid

eo &

au

dio

gam

ing

Bra

nd

ing

/

jing

les

Oth

er

-

5,000

10,000

15,000

20,000 19,800

249 1,188 240 261 1,537 562

8,385

1,957 1,346 71 10 337 287

2,440

Breakdown by revenue generating area (£’000s)

[Source: RIG Indie Business Census 2015]

• 85 companies responded to the survey, of which 82 generated revenues

• Of these 82 companies, 77 generated revenue from commissioned radio programmes

• In total radio programme production generated £19.8m in revenue

– This was 51% of the total revenue of £38.7m

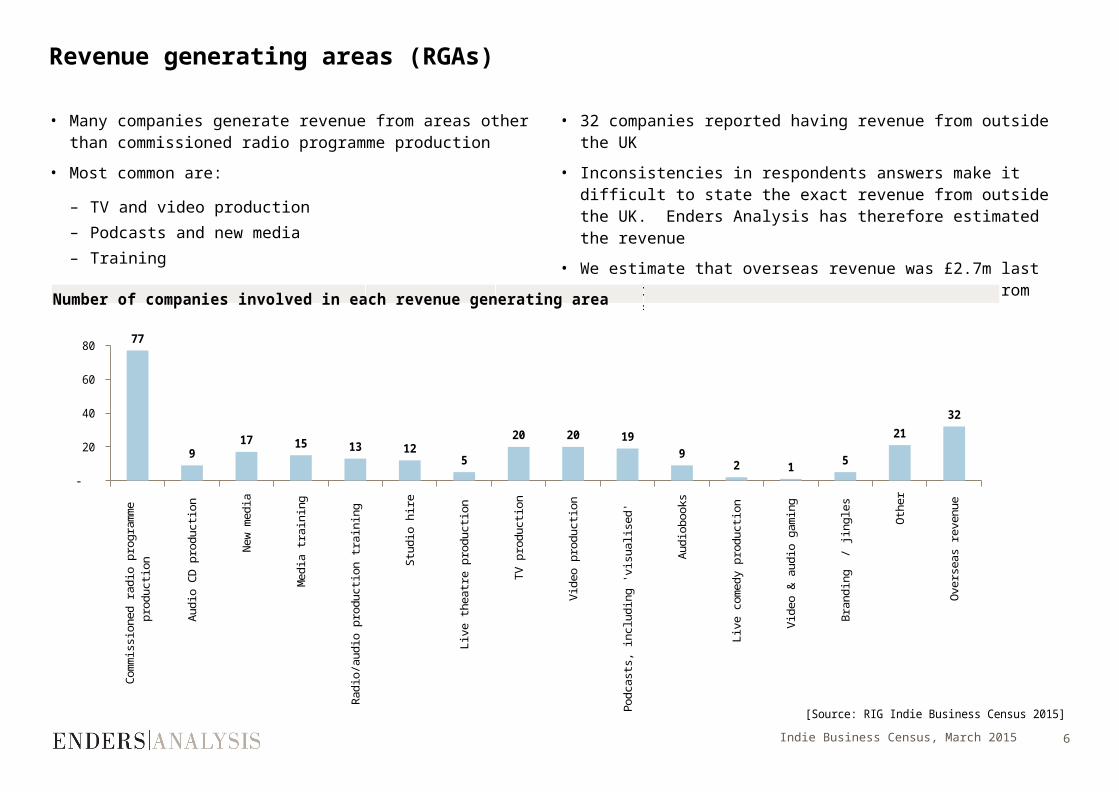

Revenue generating areas (RGAs)

Indie Business Census, March 2015 6

• 32 companies reported having revenue from outside the UK

• Inconsistencies in respondents answers make it difficult to state the exact revenue from outside the UK. Enders Analysis has therefore estimated the revenue

• We estimate that overseas revenue was £2.7m last year, of which £1.2m was radio commissions from 11 different companies

Com

mis

sion

ed r

ad

io p

rog

ram

me p

ro-

du

cti

on

Au

dio

CD

pro

du

ctio

n

New

med

ia

Med

ia t

rain

ing

Rad

io/a

ud

io p

rod

ucti

on

tra

inin

g

Stu

dio

hir

e

Liv

e th

eatr

e p

rod

ucti

on

TV

pro

du

cti

on

Vid

eo p

rod

ucti

on

Pod

cast

s, in

clu

din

g 'v

isu

alis

ed

'

Au

dio

books

Liv

e co

med

y p

rod

uct

ion

Vid

eo &

au

dio

gam

ing

Bra

nd

ing

/

jing

les

Oth

er

Ove

rseas

rev

en

ue

- 10 20 30 40 50 60 70 80 77

9 17 15 13 12

5

20 20 19 9

2 1 5

21 32

Number of companies involved in each revenue generating area

[Source: RIG Indie Business Census 2015]

• Many companies generate revenue from areas other than commissioned radio programme production

• Most common are:

– TV and video production

– Podcasts and new media

– Training

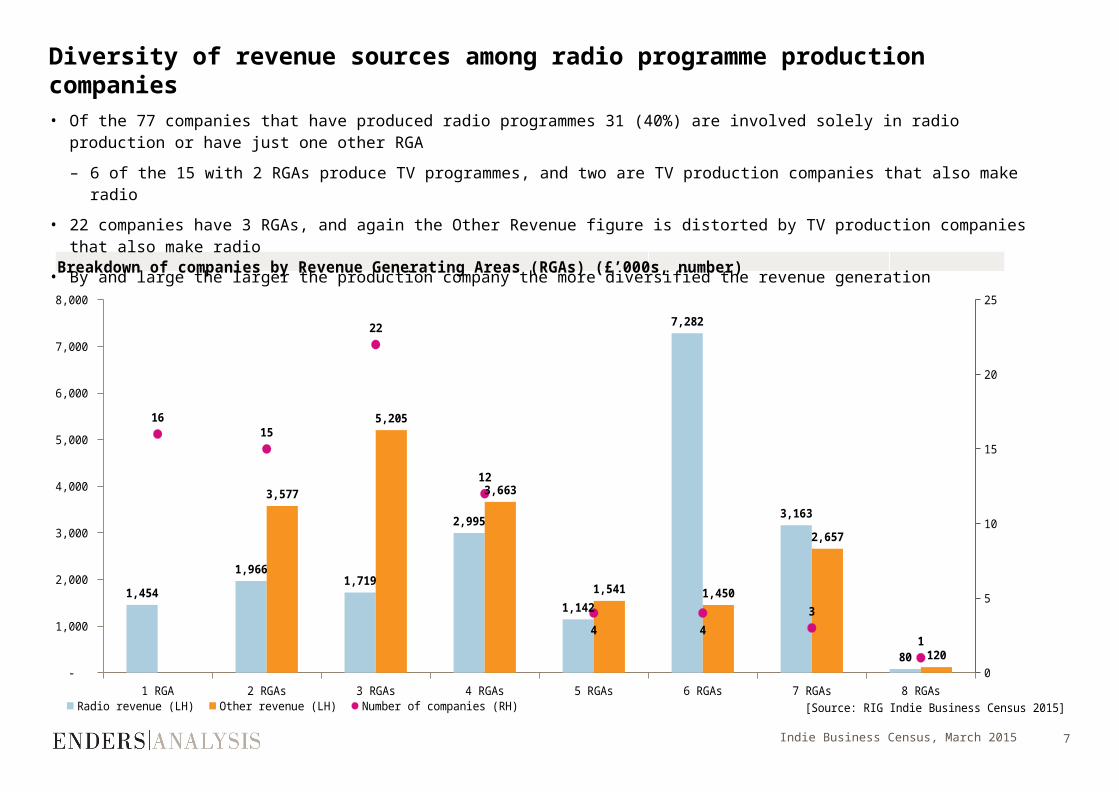

Diversity of revenue sources among radio programme production companies

1 RGA 2 RGAs 3 RGAs 4 RGAs 5 RGAs 6 RGAs 7 RGAs 8 RGAs -

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0

5

10

15

20

25

1,454

1,9661,719

2,995

1,142

7,282

3,163

80

3,577

5,205

3,663

1,541 1,450

2,657

120

1615

22

12

4 43

1

Breakdown of companies by Revenue Generating Areas (RGAs) (£’000s, number)

Radio revenue (LH) Other revenue (LH) Number of companies (RH) [Source: RIG Indie Business Census 2015]

Indie Business Census, March 2015 7

• Of the 77 companies that have produced radio programmes 31 (40%) are involved solely in radio production or have just one other RGA

– 6 of the 15 with 2 RGAs produce TV programmes, and two are TV production companies that also make radio

• 22 companies have 3 RGAs, and again the Other Revenue figure is distorted by TV production companies that also make radio

• By and large the larger the production company the more diversified the revenue generation

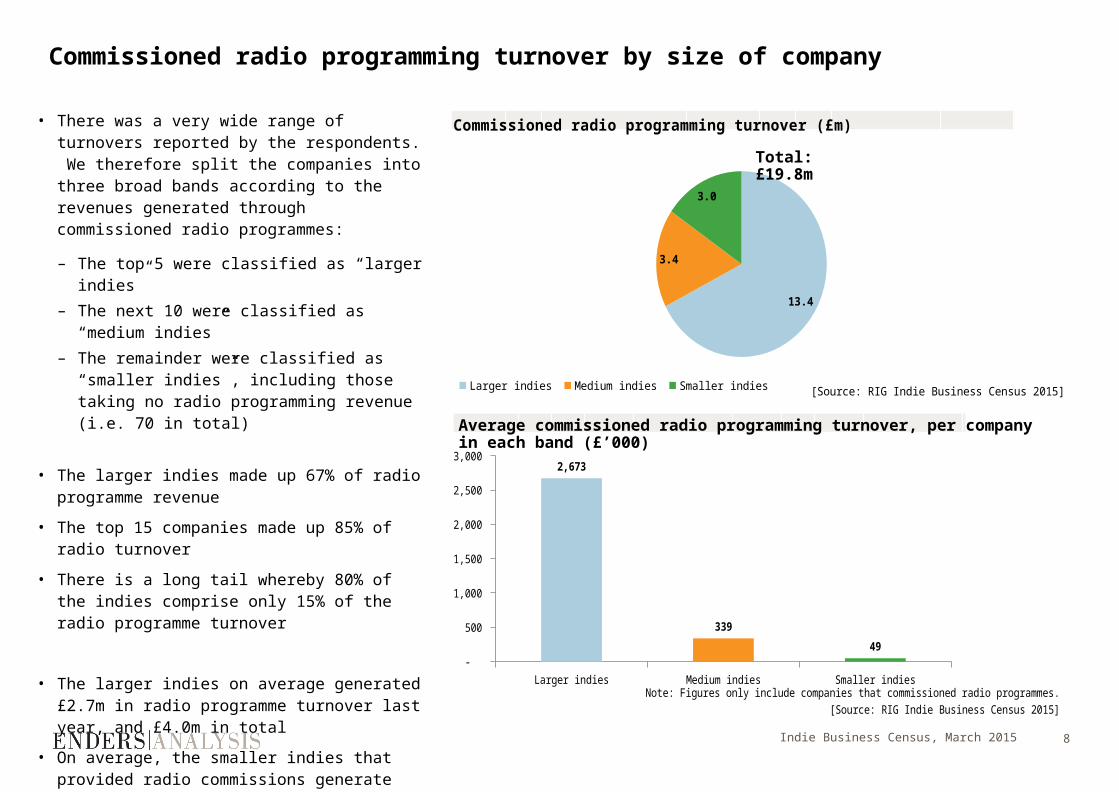

Commissioned radio programming turnover by size of company

Indie Business Census, March 2015 8

13.4

3.4

3.0

Commissioned radio programming turnover (£m)

Larger indies Medium indies Smaller indies [Source: RIG Indie Business Census 2015]

• There was a very wide range of turnovers reported by the respondents. We therefore split the companies into three broad bands according to the revenues generated through commissioned radio programmes:

– The top 5 were classified as “larger indies”

– The next 10 were classified as “medium indies”

– The remainder were classified as “smaller indies”, including those taking no radio programming revenue (i.e. 70 in total)

• The larger indies made up 67% of radio programme revenue

• The top 15 companies made up 85% of radio turnover

• There is a long tail whereby 80% of the indies comprise only 15% of the radio programme turnover

• The larger indies on average generated £2.7m in radio programme turnover last year, and £4.0m in total

• On average, the smaller indies that provided radio commissions generate just £49,000 turnover in radio programming

Total: £19.8m

Larger indies Medium indies Smaller indies -

500

1,000

1,500

2,000

2,500

3,000 2,673

339

49

Note: Figures only include companies that commissioned radio programmes.[Source: RIG Indie Business Census 2015]

Average commissioned radio programming turnover, per company in each band (£’000)

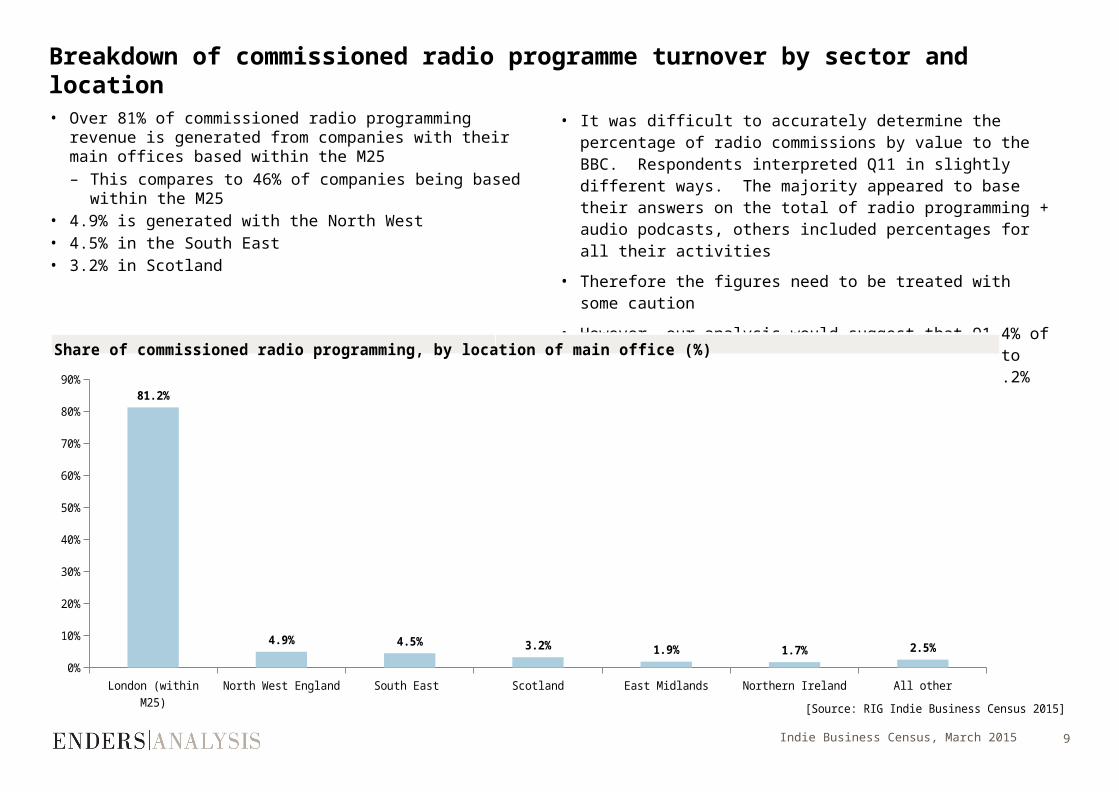

Breakdown of commissioned radio programme turnover by sector and location

Indie Business Census, March 2015 9

• It was difficult to accurately determine the percentage of radio commissions by value to the BBC. Respondents interpreted Q11 in slightly different ways. The majority appeared to base their answers on the total of radio programming + audio podcasts, others included percentages for all their activities

• Therefore the figures need to be treated with some caution

• However, our analysis would suggest that 91.4% of commissioned radio programmes by value were to the BBC, 4.4% to the commercial sector and 4.2% to other broadcasters

• Over 81% of commissioned radio programming revenue is generated from companies with their main offices based within the M25– This compares to 46% of companies being based within

the M25• 4.9% is generated with the North West• 4.5% in the South East• 3.2% in Scotland

London (within M25) North West England South East Scotland East Midlands Northern Ireland All other0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

81.2%

4.9% 4.5% 3.2% 1.9% 1.7% 2.5%

Share of commissioned radio programming, by location of main office (%)

[Source: RIG Indie Business Census 2015]

Other

Unpaid internships / placements

Internships (paid)

Freelance, full-time equivalent

Short-term contract

Part-time permanent

Full-time permanent

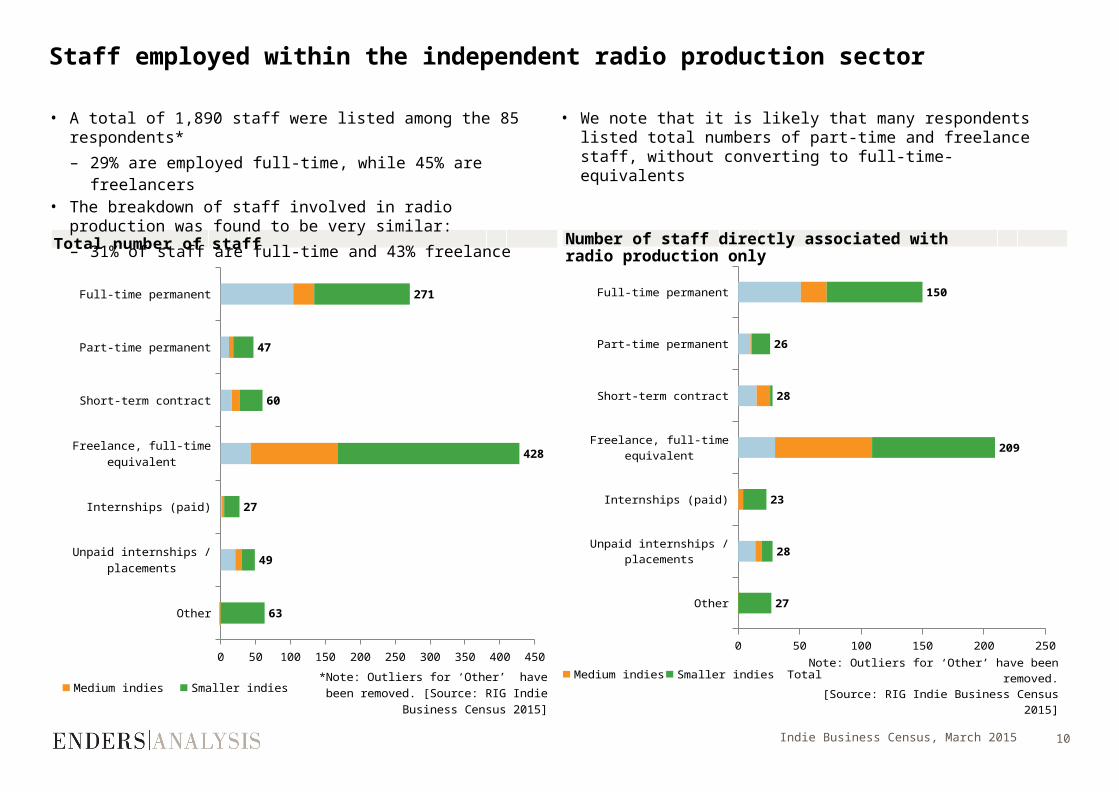

0 50 100 150 200 250 300 350 400 450

63

49

27

428

60

47

271

Total number of staff

Medium indies Smaller indies Total*Note: Outliers for ‘Other’ have been removed. [Source: RIG Indie Business

Census 2015]

Staff employed within the independent radio production sector

Indie Business Census, March 2015 10

Other

Unpaid internships / placements

Internships (paid)

Freelance, full-time equivalent

Short-term contract

Part-time permanent

Full-time permanent

0 50 100 150 200 250

27

28

23

209

28

26

150

Medium indies Smaller indies TotalNote: Outliers for ‘Other’ have been removed.

[Source: RIG Indie Business Census 2015]

• A total of 1,890 staff were listed among the 85 respondents*

– 29% are employed full-time, while 45% are freelancers • The breakdown of staff involved in radio production was

found to be very similar:

– 31% of staff are full-time and 43% freelance

• We note that it is likely that many respondents listed total numbers of part-time and freelance staff, without converting to full-time-equivalents

Number of staff directly associated with radio production only

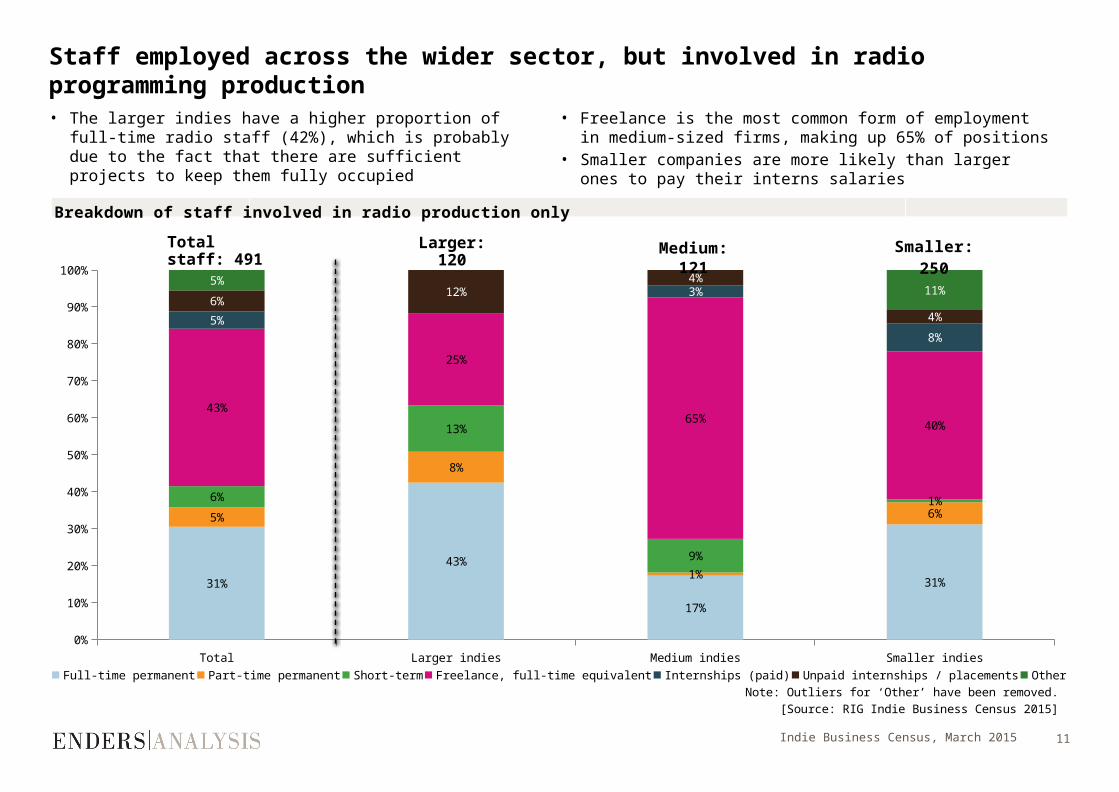

Total Larger indies Medium indies Smaller indies0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

31%

43%

17%

31%

5%

8%

1%

6%6%

13%

9%

1%

43%

25%

65%40%

5%

3%

8%

6%12%

4%

4%

5%11%

Breakdown of staff involved in radio production only

Full-time permanent Part-time permanent Short-term Freelance, full-time equivalent Internships (paid) Unpaid internships / placements OtherNote: Outliers for ‘Other’ have been removed.

[Source: RIG Indie Business Census 2015]

Medium: 121

Smaller: 250

Staff employed across the wider sector, but involved in radio programming production

Indie Business Census, March 2015 11

Total staff: 491

• The larger indies have a higher proportion of full-time radio staff (42%), which is probably due to the fact that there are sufficient projects to keep them fully occupied

• Freelance is the most common form of employment in medium-sized firms, making up 65% of positions

• Smaller companies are more likely than larger ones to pay their interns salaries

Larger: 120

Training/skills development

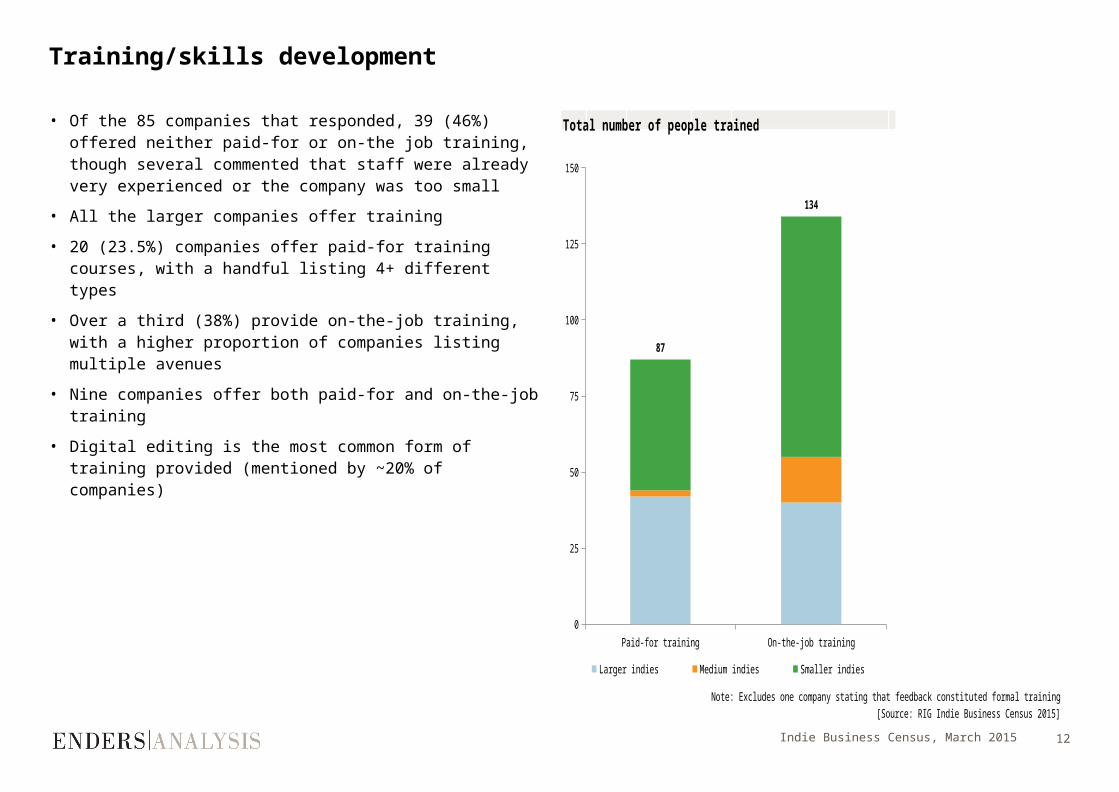

• Of the 85 companies that responded, 39 (46%) offered neither paid-for or on-the job training, though several commented that staff were already very experienced or the company was too small

• All the larger companies offer training

• 20 (23.5%) companies offer paid-for training courses, with a handful listing 4+ different types

• Over a third (38%) provide on-the-job training, with a higher proportion of companies listing multiple avenues

• Nine companies offer both paid-for and on-the-job training

• Digital editing is the most common form of training provided (mentioned by ~20% of companies)

Paid-for training On-the-job training0

25

50

75

100

125

150

87

134

Total number of people trained

Larger indies Medium indies Smaller indies

Note: Excludes one company stating that feedback constituted formal training[Source: RIG Indie Business Census 2015]

Indie Business Census, March 2015 12

• On average, the larger indies have invested in studios four times as much as medium indies, which invest twice as much as the smaller ones

• This difference largely holds true for other capex

Capital investment over the last three years

Indie Business Census, March 2015 13

0

20

40

60

80

100

120

140

160

180

70 70

3336

58

74

120

163

128

Larger indies Medium indies Smaller indies[Source: RIG Indie Business Census 2015]

0

2

4

6

8

10

12

14

16

14.1 14.0

6.6

3.6

5.8

7.4

1.8 2.4

1.9

Larger indies Medium indies [Source: RIG Indie Business Census 2015]

• The average annual investment across the sector has been £752,000 for the last three years

• This breaks down into £226,000 on studios, £291,000 on other capex, and £235,000 on buildings

Average annual investment across entire sector, last 3 years (£’000)

Average annual investment per company, last 3 years (£’000)

Planned investment over the next two years

Indie Business Census, March 2015 14

0

20

40

60

80

100

120

140

160

180

200

130

48

3022

39

51

124

176

131

Planned annual investment across entire sector (£’000)

Larger indies Medium indies[Source: RIG Indie Business Census 2015]

0

5

10

15

20

25

30

26.0

9.5

6.0

2.2

3.9 5.1

1.9 2.6

1.9

Average planned annual investment per company (£’000)

Larger indies Medium indies [Source: RIG Indie Business Census 2015]

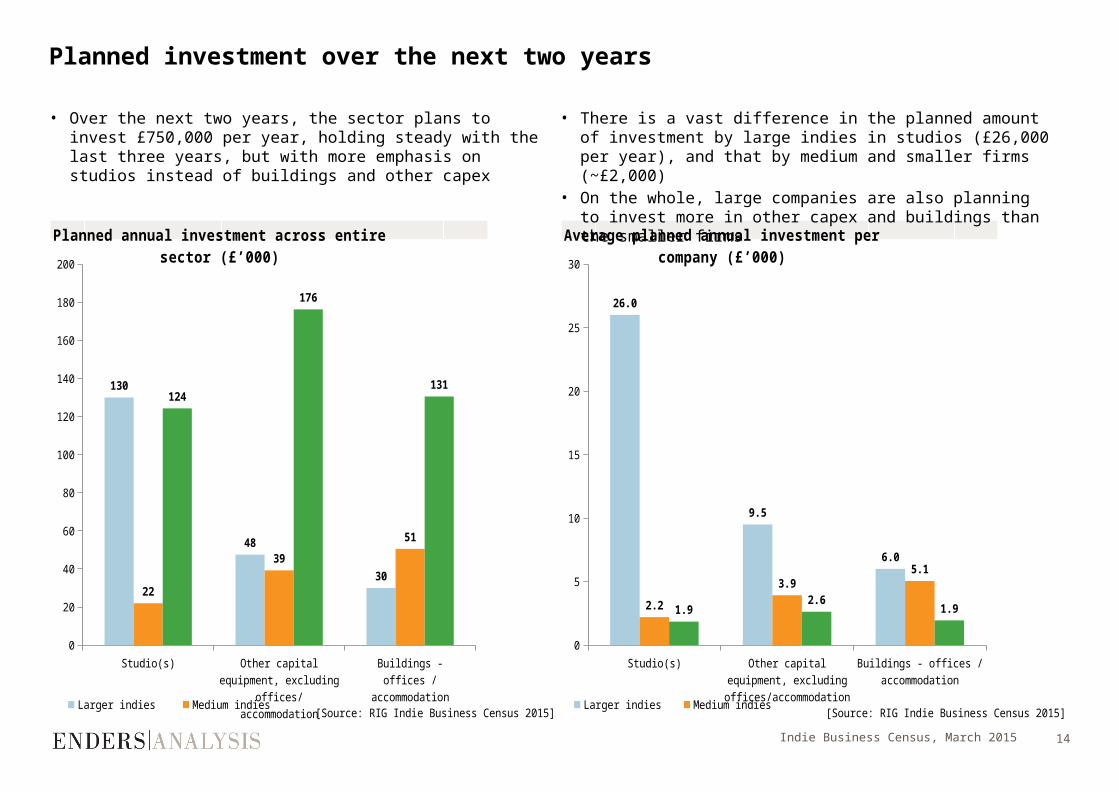

• Over the next two years, the sector plans to invest £750,000 per year, holding steady with the last three years, but with more emphasis on studios instead of buildings and other capex

• There is a vast difference in the planned amount of investment by large indies in studios (£26,000 per year), and that by medium and smaller firms (~£2,000)

• On the whole, large companies are also planning to invest more in other capex and buildings than the smaller firms

0

10

20

30

40

50

60

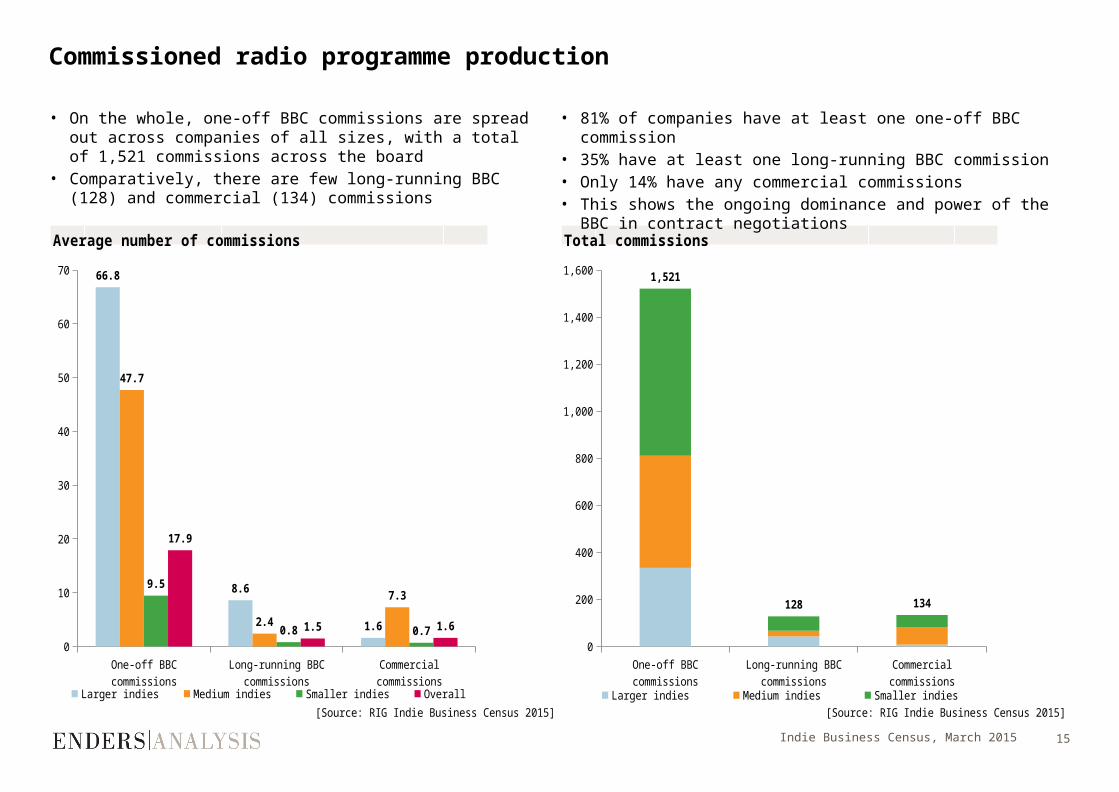

70 66.8

8.6

1.6

47.7

2.4

7.39.5

0.8 0.7

17.9

1.5 1.6

Average number of commissions

Larger indies Medium indies Smaller indies Overall[Source: RIG Indie Business Census 2015]

0

200

400

600

800

1,000

1,200

1,400

1,6001,521

128 134

Total commissions

Larger indies Medium indies Smaller indies[Source: RIG Indie Business Census 2015]

• On the whole, one-off BBC commissions are spread out across companies of all sizes, with a total of 1,521 commissions across the board

• Comparatively, there are few long-running BBC (128) and commercial (134) commissions

• 81% of companies have at least one one-off BBC commission

• 35% have at least one long-running BBC commission• Only 14% have any commercial commissions• This shows the ongoing dominance and power of the BBC

in contract negotiations

Commissioned radio programme production

Indie Business Census, March 2015 15

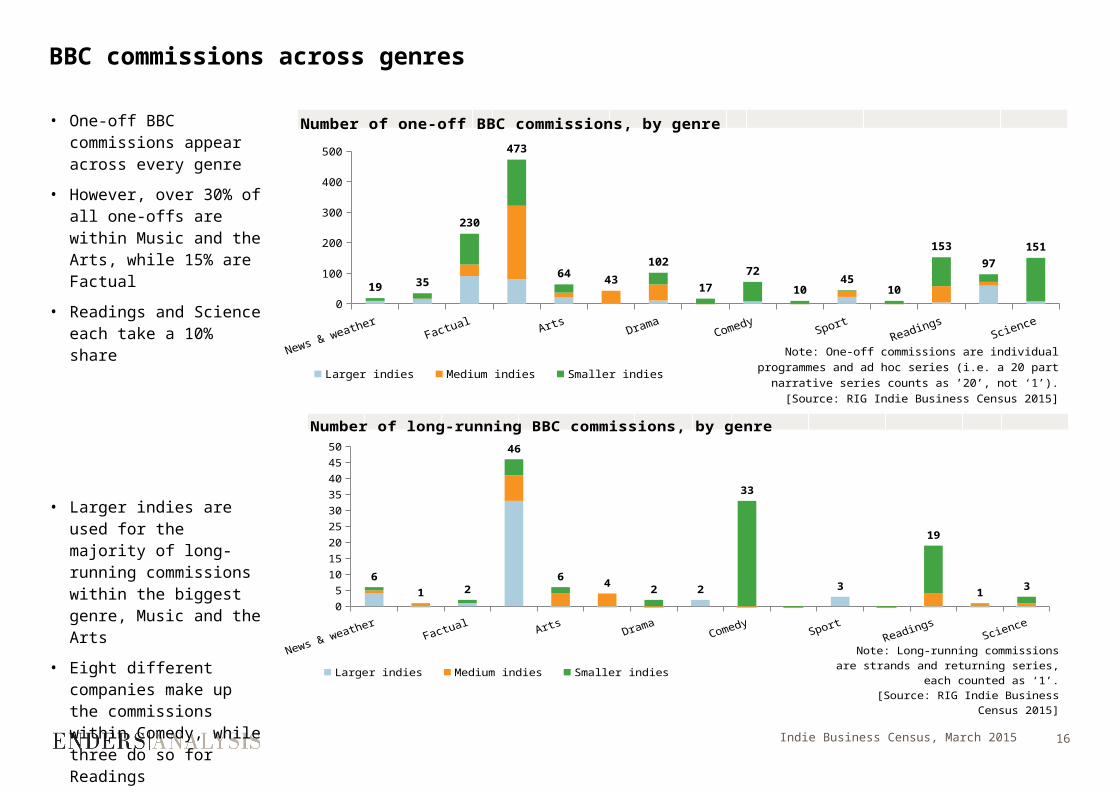

BBC commissions across genres

• One-off BBC commissions appear across every genre

• However, over 30% of all one-offs are within Music and the Arts, while 15% are Factual

• Readings and Science each take a 10% share

• Larger indies are used for the majority of long-running commissions within the biggest genre, Music and the Arts

• Eight different companies make up the commissions within Comedy, while three do so for Readings

Indie Business Census, March 2015 16

050

100150200250300350400450500

19 35

230

473

64 43

102

17

72

1045

10

153

97

151

Number of one-off BBC commissions, by genre

Larger indies Medium indies Smaller indies

Note: One-off commissions are individual pro-grammes and ad hoc series (i.e. a 20 part narrative

series counts as ’20’, not ‘1’).[Source: RIG Indie Business Census 2015]

0

5

10

15

20

25

30

35

40

45

50

6

1 2

46

64

2 2

33

3

19

13

Number of long-running BBC commissions, by genre

Larger indies Medium indies Smaller indies

Note: Long-running commissions are strands and returning series, each

counted as ‘1’.[Source: RIG Indie Business Census

2015]

Comparisons between networks

Indie Business Census, March 2015 17

• Radio 4/4 Extra are together responsible for almost half (48.5%) of all one-off BBC commissions, spread across a large number of companies of varying sizes and in different regions

• For long-running BBC commissions they make up 38% of the market, while Radio 1/1Xtra account for 16%

• Among the regional radio networks, commissions are typically taken by companies based within the relevant country

– Radio Cymru’s commissioning was all from companies located in Wales

– Radio Scotland commissioned 6 companies, 5 of which are based in Scotland

– Half of the companies commissioning for Radio Wales are based in Wales

– Radio Ulster only used one indie, which is based in Ulster

• It should be noted that BBC Asian network was not included in the survey

– While one company did comment on this, others may not have thought to

0

50

100

150

200

250

300

350

18

56

22

232

65 16

49

200

212

184

124

32 29

305

85

6 17

83

29

Number of one-off BBC commissions, by network

Larger indies Medium indies Smaller indies [Source: RIG Indie Business Census 2015]

0

5

10

15

20

25

30

35

40

14

8

3

74

74

2 2

8

1 25

3 2 3

34

2

12

5

Number of long-running BBC commissions, by network

Larger indies Medium indies Smaller indies[Source: RIG Indie Business Census 2015]

Diversity of supply

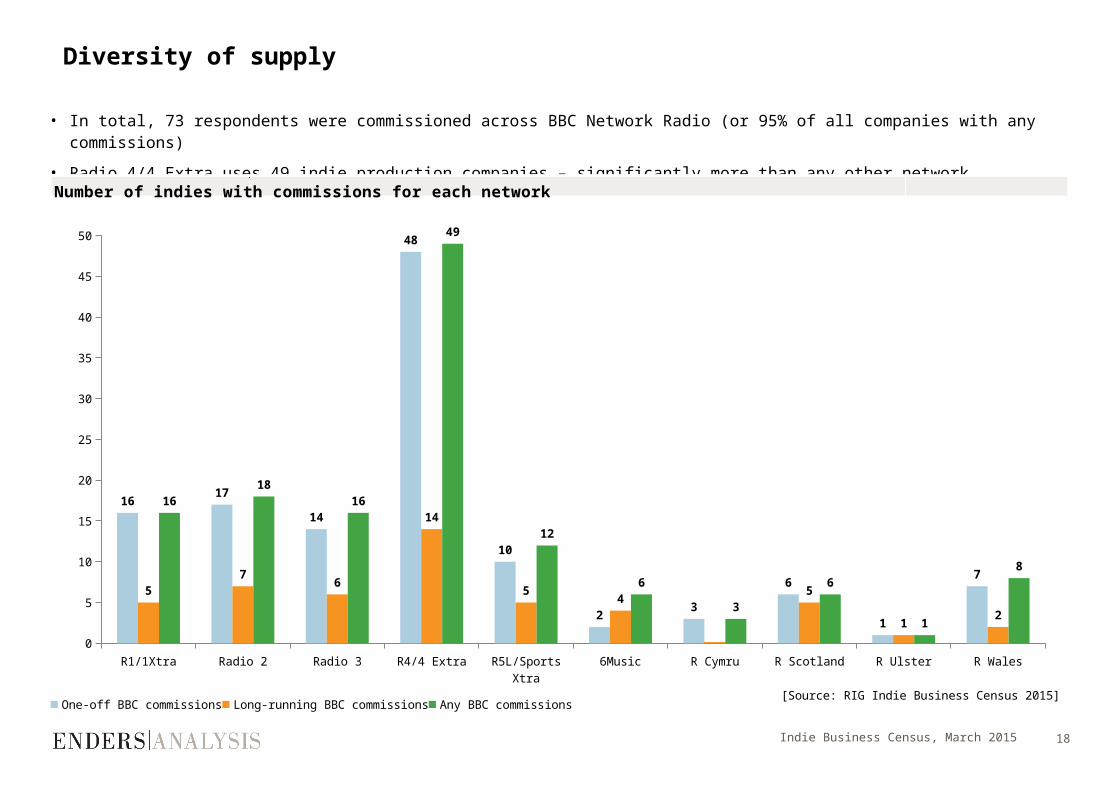

Indie Business Census, March 2015 18

• In total, 73 respondents were commissioned across BBC Network Radio (or 95% of all companies with any commissions)

• Radio 4/4 Extra uses 49 indie production companies – significantly more than any other network

R1/1Xtra Radio 2 Radio 3 R4/4 Extra R5L/Sports Xtra

6Music R Cymru R Scotland R Ulster R Wales0

5

10

15

20

25

30

35

40

45

50

1617

14

48

10

23

6

1

75

76

14

54

5

12

1618

16

49

12

6

3

6

1

8

Number of indies with commissions for each network

One-off BBC commissions Long-running BBC commissions Any BBC commissions[Source: RIG Indie Business Census 2015]

Distribution of companies across networks and genres

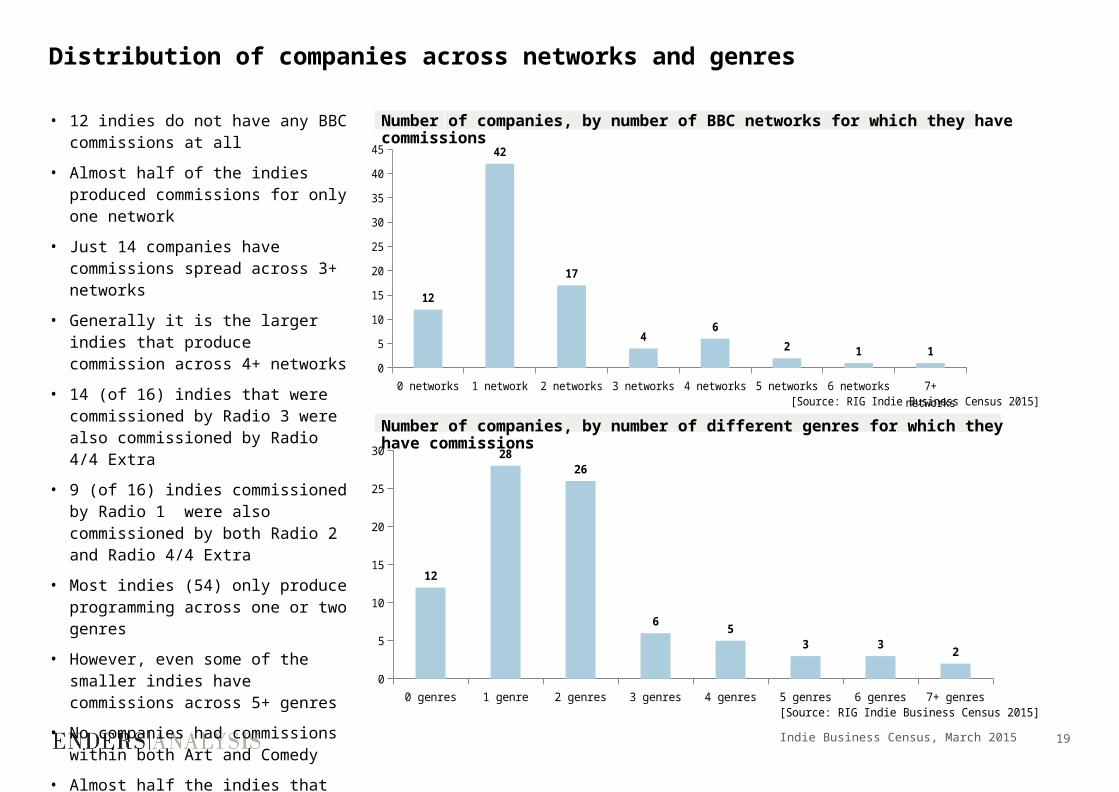

• 12 indies do not have any BBC commissions at all

• Almost half of the indies produced commissions for only one network

• Just 14 companies have commissions spread across 3+ networks

• Generally it is the larger indies that produce commission across 4+ networks

• 14 (of 16) indies that were commissioned by Radio 3 were also commissioned by Radio 4/4 Extra

• 9 (of 16) indies commissioned by Radio 1 were also commissioned by both Radio 2 and Radio 4/4 Extra

• Most indies (54) only produce programming across one or two genres

• However, even some of the smaller indies have commissions across 5+ genres

• No companies had commissions within both Art and Comedy

• Almost half the indies that are commissioned within Music & the Arts, and over half of those that produced History programming, also made commissions for Factual programmes

Indie Business Census, March 2015 19

0 networks 1 network 2 networks 3 networks 4 networks 5 networks 6 networks 7+ networks0

5

10

15

20

25

30

35

40

45

12

42

17

46

2 1 1

[Source: RIG Indie Business Census 2015]

0 genres 1 genre 2 genres 3 genres 4 genres 5 genres 6 genres 7+ genres0

5

10

15

20

25

30

12

2826

65

3 32

[Source: RIG Indie Business Census 2015]

Number of companies, by number of BBC networks for which they have commissions

Number of companies, by number of different genres for which they have commissions

Distribution of commissions across networks, by genres

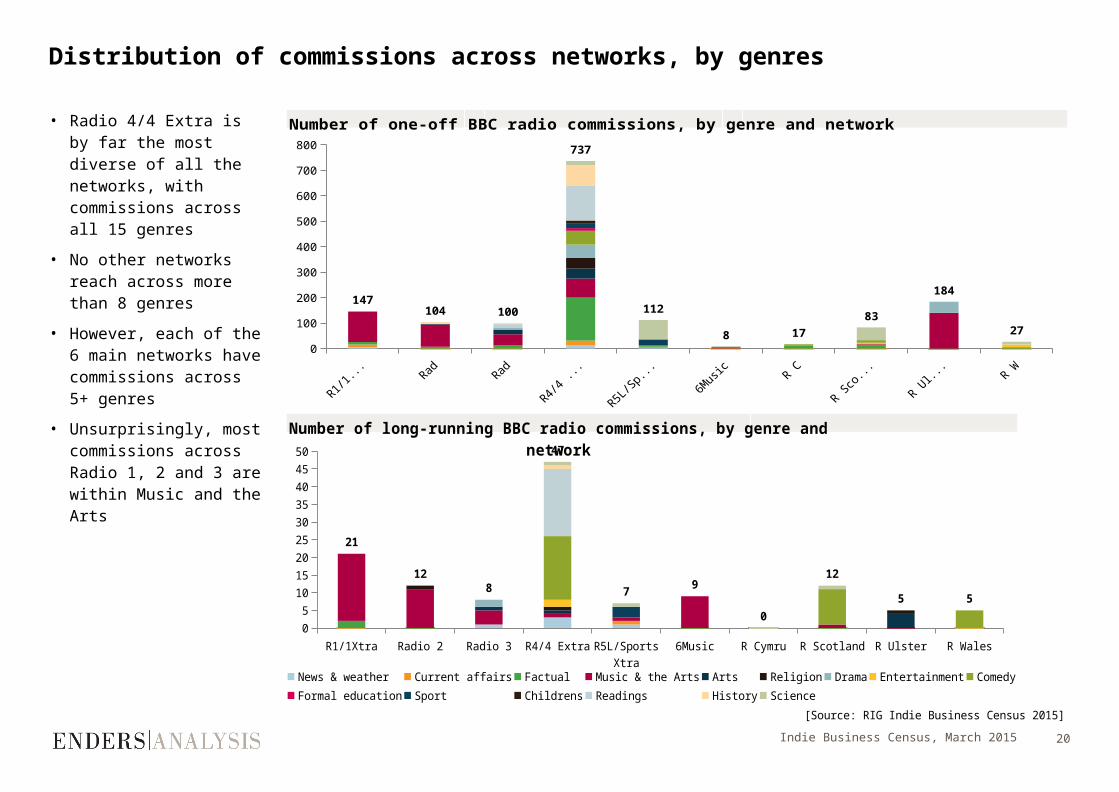

• Radio 4/4 Extra is by far the most diverse of all the networks, with commissions across all 15 genres

• No other networks reach across more than 8 genres

• However, each of the 6 main networks have commissions across 5+ genres

• Unsurprisingly, most commissions across Radio 1, 2 and 3 are within Music and the Arts

Indie Business Census, March 2015 20

R1/1Xtra Radio 2 Radio 3 R4/4 Extra R5L/Sports Xtra

6Music R Cymru R Scotland R Ulster R Wales0

100

200

300

400

500

600

700

800

147104 100

737

112

8 17

83

184

27

Number of one-off BBC radio commissions, by genre and network

R1/1Xtra Radio 2 Radio 3 R4/4 Extra R5L/Sports Xtra

6Music R Cymru R Scotland R Ulster R Wales0

5

10

15

20

25

30

35

40

45

50

21

128

47

79

0

12

5 5

Number of long-running BBC radio commissions, by genre and network

News & weather Current affairs Factual Music & the Arts Arts Religion Drama Entertainment Comedy

Formal education Sport Childrens Readings History Science

[Source: RIG Indie Business Census 2015]

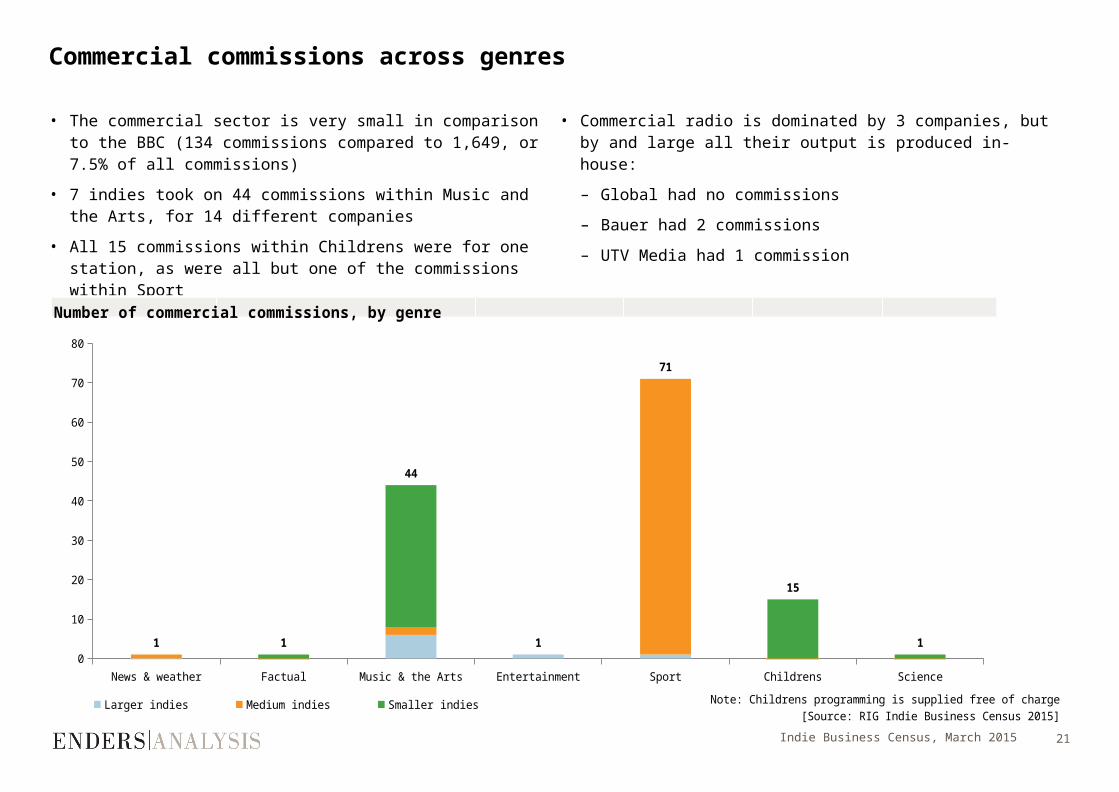

Commercial commissions across genres

Indie Business Census, March 2015 21

• Commercial radio is dominated by 3 companies, but by and large all their output is produced in-house:

– Global had no commissions

– Bauer had 2 commissions

– UTV Media had 1 commission

• The commercial sector is very small in comparison to the BBC (134 commissions compared to 1,649, or 7.5% of all commissions)

• 7 indies took on 44 commissions within Music and the Arts, for 14 different companies

• All 15 commissions within Childrens were for one station, as were all but one of the commissions within Sport

News & weather Factual Music & the Arts Entertainment Sport Childrens Science0

10

20

30

40

50

60

70

80

1 1

44

1

71

15

1

Number of commercial commissions, by genre

Larger indies Medium indies Smaller indiesNote: Childrens programming is supplied free of charge

[Source: RIG Indie Business Census 2015]

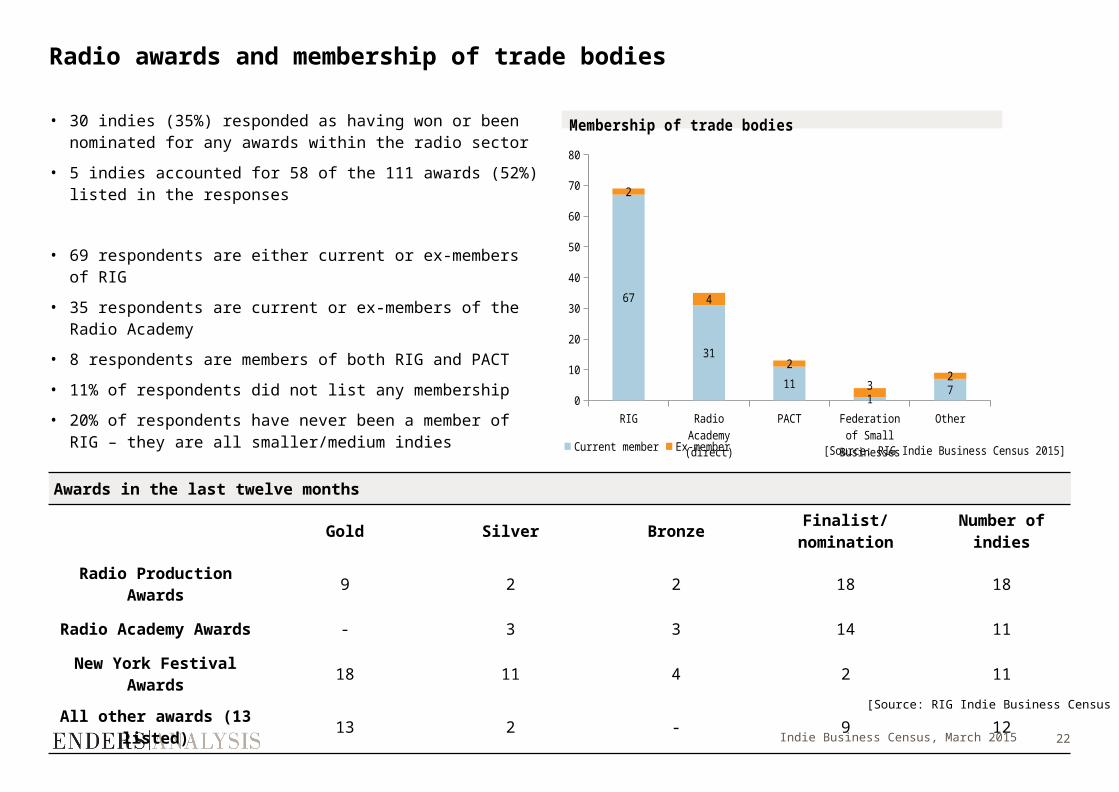

Radio awards and membership of trade bodies

Awards in the last twelve months

Gold Silver BronzeFinalist/

nominationNumber of

indies

Radio Production Awards

9 2 2 18 18

Radio Academy Awards

- 3 3 14 11

New York Festival Awards

18 11 4 2 11

All other awards (13 listed)

13 2 - 9 12Indie Business Census, March 2015 22

• 30 indies (35%) responded as having won or been nominated for any awards within the radio sector

• 5 indies accounted for 58 of the 111 awards (52%) listed in the responses

• 69 respondents are either current or ex-members of RIG

• 35 respondents are current or ex-members of the Radio Academy

• 8 respondents are members of both RIG and PACT

• 11% of respondents did not list any membership

• 20% of respondents have never been a member of RIG – they are all smaller/medium indies

[Source: RIG Indie Business Census 2015]

0

10

20

30

40

50

60

70

80

67

31

111

7

2

4

2

32

Membership of trade bodies

Current member Ex-member [Source: RIG Indie Business Census 2015]

Disclaimer

23

About Enders Analysis

Enders Analysis is a research and advisory firm based in London. We specialise in media, entertainment, mobile and fixed telecoms, with a special

focus on new technologies and media, covering all sides of the market, from consumers and leading companies to regulation. For more information

go to www.endersanalysis.com or contact us at [email protected].

Important notice: By accepting this research note, the recipient agrees to be bound by the following terms of use. This research note has been

prepared by Enders Analysis Limited and published solely for guidance and general informational purposes. It may contain the personal opinions of

research analysts’ based on research undertaken. This note has no regard to any specific recipient, including but not limited to any specific

investment objectives, and should not be relied on by any recipient for investment or any other purposes. Enders Analysis Limited gives no

undertaking to provide the recipient with access to any additional information or to update or keep current any information or opinions contained

herein. The information and any opinions contained herein are based on sources believed to be reliable but the information relied on has not been

independently verified. Enders Analysis Limited, its officers, employees and agents make no warranties or representations, express or implied, as to

the accuracy or completeness of information and opinions contained herein and exclude all liability to the fullest extent permitted by law for any

direct or indirect loss or damage or any other costs or expenses of any kind which may arise directly or indirectly out of the use of this note,

including but not limited to anything caused by any viruses or any failures in computer transmission. The recipient hereby indemnifies Enders

Analysis Limited, its officers, employees and agents and any entity which directly or indirectly controls, is controlled by, or is under direct or indirect

common control with Enders Analysis Limited from time to time, against any direct or indirect loss or damage or any other costs or expenses of any

kind which they may incur directly or indirectly as a result of the recipient’s use of this note.

© 2015 Enders Analysis Limited. All rights reserved. No part of this note may be reproduced or distributed in any manner including, but not limited

to, via the internet, without the prior permission of Enders Analysis Limited. If you have not received this note directly from Enders Analysis Limited,

your receipt is unauthorised. Please return this note to Enders Analysis Limited immediately.Indie Business Census, March 2015