Inputs for outputs: Improving farmers’ access to seeds and ...

Important disclosures can be found in the Disclosures Appendix All rights reserved. Standard Chartered Bank 2014 http://research.standardchartered.com

l Equity Research l India | Emerging Companies l 26 February 2014

India agriculture inputs

Seeds of prosperity

India’s food grain yield is among the lowest in the world, yet demand is projected

to increase by 57mtpa over the next decade. This increase will far outstrip the

incremental supply (8mtpa), if yields remain at current levels.

The natural response is to increase yields by boosting agro-inputs, and this should

underpin the INR1tn market in fertilizers, micro-irrigation, pesticides and seeds.

We see growth and medium-term investment opportunity in pesticides and seeds;

and project this market to grow from INR 350bn in 2012 to INR 650bn by 2017

(CAGR 13%).

Our on-the-ground checks with 33 agro-input dealers across 7 states indicate that

brand and distribution are the key drivers of success for agro-input companies.

Our proprietary framework assesses agro-input companies on six key parameters

- Rallis and PI Industries emerge as our top picks. We initiate coverage on Kaveri

Seed (OP), UPL (OP) and Coromandel International (IL).

Click here to get The Scoop, an audiovisual summary of the report.

Share prices as of 25 February 2014 Source: Companies, FactSet, Standard Chartered Research estimates

India agriculture inputsSeeds of prosperity

Click here to get The Scoop, an audiovisual summary of the report

February 2014

Mkt cap Price hide column-old rating PT Up/(Dn)

Ticker (USD mn) (lc) New Old Rec New Chg (%) (lc) side (%) FY1E FY2E FY1E FY2E FY1E FY2E

Rallis India^ RALI IN 492.1 156.85 OP - OP 200.00 - 200.00 27.5 20.7 16.5 12.1 10.0 1.9 2.4

PI Industries^ PI IN 519.1 252.90 OP - OP 325.00 - 325.00 28.5 19.7 15.3 11.8 9.4 0.6 0.8

Kaveri Seed^ KSCL IN 567.0 513.00 OP - OP 600.00 - 600.00 17.0 17.3 13.5 15.4 11.1 1.2 1.5

UPL^ UPLL IN 1,351.2 185.15 OP - OP 235.00 - 235.00 26.9 9.5 8.2 5.9 5.3 1.6 1.6

Coromandel International^ CRIN IN 939.6 203.85 IL - IL 215.00 - 215.00 5.5 13.9 12.2 9.0 8.3 2.2 2.2

PER (x) EV/EBITDA (x) Div yield (%)Rating PT (lc)

Sumit Choudhary [email protected]

+91 22 4205 5916

RALI IN INR 157.00 INR 200.00

Equity Research l India agriculture inputs

26 February 2014 2

Contents

Executive summary 3

Yield – Only road to food self-sufficiency 5

Agro-inputs: Key beneficiary of reach for yield 9

Pesticides: Domestic tailwind and huge export opportunity 13

Brand and distribution driven market 17

Seeds: Set to accelerate 21

Our framework for evaluating companies 24

Sector valuation 27

Companies

Rallis India 28

PI Industries 37

Kaveri Seed 45

UPL 54

Coromandel International 64

Dhanuka Agritech 72

Jain Irrigation 76

Appendix 1: Overview of companies 80

Appendix 2: Hazardous pesticides 83

SCout is Standard Chartered’s premium research product that offers Strategic, Collaborative, Original ideas on Universal and Thematic opportunities

Equity Research l India agriculture inputs

26 February 2014 3

Executive summary Yield: Only way to food self-sufficiency. We expect India’s food grain demand to

grow to 293mt by 2022 from 236mt in 2012. At current yields, the incremental

production (8mtpa) will be sharply lower vs incremental demand (57mtpa) over this

period. Much higher yields vs. history is required to sustain food self-sufficiency.

Lower arable land availability could magnify the need for higher yields (refer Fig. 9).

Higher use of agro-inputs is therefore key.

Figure 1: Food grain consumption and production in India

Source: OECD-FAO, Planning Commission, Ministry of Agriculture, Standard Chartered Research

Agro-inputs: Key beneficiary of reach for yield. We estimate India’s overall agro-

inputs market to be worth c.INR 1tn, comprising fertilizers, micro irrigation, pesticides

and seeds. In addition to the need for higher adoption of these inputs given requisite

yield increase, rising rural incomes provide a tailwind for the growth of the agro-inputs

market. We prefer the non-subsidised segment of this market, viz. pesticides and

seeds, given relatively lower exposure to policy and subsidy delay related issues. We

expect the pesticides and seeds market to grow at a CAGR of 13% from INR

350bn to INR 650bn over 2012-22.

Pesticides: Brand play. India’s pesticide usage levels are lower vs. global peers

(refer Fig 20). The domestic pesticides market is estimated at INR 105bn and

projected to grow at a CAGR of 9% to INR 180bn by FY18 (refer Fig 21). Exports are

a high-growth segment within the pesticides market and this segment is expected to

grow at a CAGR of 15% over FY12-20 to USD 5.8bn (refer Fig. 23). As revealed by

our on-the-ground survey of over 33 agro-input distributors across seven

states, brand strength and distribution push are the key determinants of farmer

preferences in the pesticides market. (refer Fig. 26).

Seeds: Set to accelerate. India’s seed market is the sixth largest globally yet

underpenetrated vs. global peers. We expect the seeds market to grow to INR 230bn

by 2017 from INR 110bn in 2012 (refer Fig 30). The seeds industry is attractive given

the high barrier to entry and non-linear growth. The introduction of genetically

modified seeds for more crops besides just cotton could provide further upside

potential, but we have not factored this into our projections.

150,000

170,000

190,000

210,000

230,000

250,000

270,000

290,000

310,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Foodgrains consumption (kt)

Foodgrain production with enhanced yields (kt)

Foodgrain production at constant yields (kt) Projected

benefit from yields

Equity Research l India agriculture inputs

26 February 2014 4

Proprietary framework for ranking agro-input companies. Based on the findings

from our survey, we rank companies under coverage based on their brand and

distribution strengths. We also evaluate the relative attractiveness of the companies

based on four other parameters (product diversification, geographic diversification,

leverage and working capital) that can provide sustainable long-term advantages to

companies. Rallis and PI Industries fare well on our framework and are our top picks.

Figure 2: Ranking of companies under our coverage

Rallis PI Kaveri UPL** Coromandel*

Strength of brand 1 3 2 2 3

Distribution/ farmer engagement 1 2 4 4 2

Product diversification 1 4 5 2 3

Geographic diversification 3 1 4 1 NA

Leverage 2 3 1 4 NA

Working capital 2 3 1 4 NA

Overall Rank 1 2 3 4 NA

Source: Standard Chartered Research

Note: * CRIN financials not available separately for non-fertilizer business beyond EBITDA line.

Note: ** We have rated UPL’s India business only for ranking of exports, leverage/ working capital at global levels

While this framework is instrumental in identifying long-term winners, valuation

distortions can impact short-term stock preferences.

Initiate coverage on five companies. We initiate coverage on five companies:

Rallis, UPL, Coromandel International, PI Industries and Kaveri Seed. We also

present non-rated notes on Jain Irrigation and Dhanuka Agritech.

Equity Research l India agriculture inputs

26 February 2014 5

Yield – Only road to food self-sufficiency Given a rising population, better demographics and economic growth, we expect

India’s food grain consumption to rise to 293mt from 236mt over the next decade.

At current yields, we expect food production to fall materially short of this

requirement (incremental production of only 8mtpa vs incremental demand of

57mtpa over the next decade).

Yields need to improve much faster than history, especially considering land

constraints.

India’s food grain demand

India has seen her food grain demand grow at a CAGR of 1.8% over the past decade

(2002-2012). According to OECD-FAO projections, India’s cereal (wheat, rice and

coarse cereals) consumption is expected to move to 266mt by 2022 from 217mt in

2012. According to the Planning Commission, consumption of pulses is likely to grow

to c.22mt by FY17 from 19mt in FY13. Overall, we expect food grain demand to grow

to 293mt by 2022 from 236mt – an incremental 57mtpa at a CAGR of 2.2%.

Figure 3: Food grain consumption in India

Source: OECD-FAO, Planning Commission, Ministry of Agriculture, Standard Chartered Research

We believe that higher food grain demand would be driven by multiple factors

including:

Population growth. India’s population grew at a CAGR of 1.5% over the past

decade and we project it to grow at a CAGR of 1.1% going forward.

Figure 4: India’s population growth

Source: Standard Chartered Research estimates

150,000

170,000

190,000

210,000

230,000

250,000

270,000

290,000

310,000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

India foodgrain consumption (kt)

CAGR 1.8%

CAGR 2.2%

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

1,400

1,450

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

India population (mn)

CAGR 1.5%

CAGR 1.1%

Food grain consumption is set to increase by 57mtpa over the next

decade

Equity Research l India agriculture inputs

26 February 2014 6

Demographic shift. As the bulk of India’s population pyramid continues to shift

towards the 15-59 age bracket, there would be higher food grain consumption per

capita over time.

Figure 5: Proportion of prime age citizens in India’s population

Source: Standard Chartered Research estimates

Government initiatives. While we have not explicity forecast growth in food grain

demand owing to recent legislations, we believe that the availability of cheaper food

grains through national food security programs will push up demand for food grains.

Please refer to Food security bill: A costly affair by Anubhuti Sahay for more details

on the recently launched national food security program.

Supply – Yield response needed

We believe that given the current yields and recent trends in land availability, meeting

the incremental food grain demand would be an uphill task. Against incremental

demand of 57mtpa of food grains over the next decade, at current yields, the

incremental production will be only 8mtpa.

Figure 6: Food grain consumption and production in India

Source: OECD-FAO, Planning Commission, Ministry of Agriculture, Standard Chartered Research estimates

56%

57%

58%

59%

60%

61%

62%

63%

64%

2000 2005 2010 2015 2020

Proportion of population in 15-59 age group

150,000

170,000

190,000

210,000

230,000

250,000

270,000

290,000

310,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Foodgrains consumption (kt)

Foodgrain production with enhanced yields (kt)

Foodgrain production at constant yields (kt) Projected

benefit from yields

If yields do not improve, food grain supply will fall materially short of

the incremental demand

Equity Research l India agriculture inputs

26 February 2014 7

In other words, at current yields, annual food production/capita will shrink to 188kg by

2022 from 207kg currently. This compares to current food grain production per capita

of 337kg globally.

Figure 7: Food grain production per capita globally

* At current yields.

Source: OECD-FAO, World Bank, Standard Chartered Research estimates

While we have assumed land under cultivation according to OECD projections for

cereals and have used similar growth in land usage for pulses, the projections of land

under cultivation look optimistic compared with patterns witnessed historically. In

case we assume total land under food grains to be constant, overall yield for food

grains will need to improve to 2.43 t/ha by 2022 from 2.09 t/ha in 2012.

Figure 8: Area under food grains

Source: OECD-FAO, Ministry of Agriculture, Standard Chartered Research estimates

While the above chart points to the optimism built into OECD (and our) agricultural

land projections, the trend of falling arable land in India over the past two decades

can potentially render maintaining even the current pace of agricultural land addition

difficult. Arable land availability in India has been on a downward trend over the past

two decades driven by factors such as land being rendered barren owing to nutrient

depletion and shift to industrial/urban usage. A reversal of this pattern would need (1)

1,135

492 458 448

354 291 266

337

207 188

0

200

400

600

800

1,000

1,200

US Russia Thailand Brazil China South Africa

Indonesia World India - 2012

India - 2022E*

Pro

du

ctio

n k

g p

er c

apit

a

Foodgrain production kg per capita

105,000

110,000

115,000

120,000

125,000

130,000

135,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Area under foodgrains (000 ha)

CAGR 0.01%

CAGR 0.6%

There is ample scope for yields to improve

Arable land constraints accentuate the need for material yield

response

Equity Research l India agriculture inputs

26 February 2014 8

agriculture economics to look attractive enough for land to be migrated away from

industrial and urban usage and back to agriculture or (2) aggressive rehabilitation of

nutrient depleted land.

Figure 9: India’s arable land

Source: World Bank, Standard Chartered Research. Arable land includes land defined by the FAO as land under temporary

crops (double-cropped areas are counted once), temporary meadows for mowing or for pasture, land under market or kitchen gardens, and land temporarily fallow. Land abandoned as a result of shifting cultivation is excluded.

It is also worthwhile to mention that India already imports over 60% of her vegetable

oil demand (11,000kt vs demand of 18,000kt) and the need to bridge the vegetable

oil import gap could put further pressure on land available for food grains in the

country.

Weather volatility demands focus on agro-inputs. Given the high dependence on

rainfed irrigation, it is not surprising to find a high correlation between monsoons and

food grain production in India. Such high dependence on weather further

neccessitates improvement in irrigation facilities and use of agro-inputs to have an

adequate buffer in the system against weather-related weakness in production.

Figure 10: India monsoons vs. food grain production (1970-2012)

Source: OECD-FAO, IMD, Standard Chartered Research

154

155

156

157

158

159

160

161

162

163

164

1980

19

81

1982

19

83

1984

19

85

1986

19

87

1988

19

89

1990

19

91

1992

19

93

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

Mn

hec

tare

s

India arable land

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-30% -20% -10% 0% 10% 20% 30% 40% 50%

Monsoon rain % yoy

Foodgrain production % yoy R2 = 72%

Agro-input usage needs to improve to reduce weather-related supply

uncertainty

Equity Research l India agriculture inputs

26 February 2014 9

Agro-inputs: Key beneficiary of reach for yield We believe yield needs to improve faster than it did in the past decade, especially

considering that prospects of additional land coming under agriculture are minimal.

Yields in India are lower than for global peers for most crops and increasing agro-

input usage is key for enhancing yields.

Of the c.INR 1tn agro-inputs market, c.65% is in subsidised segments (fertilizer

and micro irrigation) that are saddled with high working capital and delays in

subsidy receipts. We prefer the non-subsidised pesticides/seeds markets.

The pesticides and seeds markets are estimated to grow to INR 650bn by 2017

from INR 350bn in 2012 at an impressive 13% CAGR.

Need for yield. To achieve the projections for food grain production in India as

provided in the previous section, overall yields will need to improve to 2.30 t/ha by

2022 from 2.09 t/ha in 2012. As mentioned in the section above, in case land under

cultivation does not increase as per OECD-FAO projections, yields would need to

improve even further to 2.43 t/ha by 2022. The required rate of improvement in yields

in this case would need to be significantly higher than what India has actually

achieved over the past decade.

Figure 11: India food grain yield

Source: OECD-FAO, PlanningCommission, Ministry of Agriculture, Standard Chartered Research estimates

Ample scope for yields to improve. India has significantly lower yields versus

global averages for most crops. While part of this yield differential could be explained

by the lower size of farm holdings in India, we believe that there is still significant

scope for yields to improve.

Figure 12: Comparison of Indian crop productivity

Mt/ ha World India China

Rice 4.2 2.3 6.6

Corn 5.0 2.2 5.0

Soybean 2.2 0.9 1.6

Rapeseed 1.9 1.1 1.9

Peanut 1.6 0.9 3.3

Sugarcane 74.0 67.0 69.8

Wheat 3.0 2.8 4.7

Source: Companies, Standard Chartered Research

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

2.5

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

t/h

a

Yield assuming no incremental land Yield

Faster yield response vs. history is required and higher agro-input

usage will help achieve this

Equity Research l India agriculture inputs

26 February 2014 10

A number of factors including better and judicious use of fertilizers, pesticides and

speciality nutrients, higher share of irrigated land, farm mechanisation and higher

usage of seeds, including hybrid seeds can help in optimising yields.

Agro-input market in India. The overall agro-input market in India is estimated at c.

INR 1tn. We have estimated the market for fertilizers, pesticides, seeds and micro

irrigation only for the purpose of our analysis. The market is split as follows.

Figure 13: Market for pesticides, seeds, micro irrigation, fertilizers

Source: Ministry of Agriculture, FICCI, Assocham, Companies, Standard Chartered Research

Aside from the above inputs, there is relatively small, but fast growing market for

agro-inputs such as organic manures and plant growth nutrients in India, too.

Rising rural incomes to provide support. There has been a significant increase in

minimum support prices in recent years, boosting farmer incomes. In addition, the

government has increased its budget on rural welfare schemes manifold over the

past decade, boosting rural incomes.

Figure 14: Trend in MSPs for major crops in India

Source: Ministry of Agriculture, Standard Chartered Research

Crop protection market - domestic,

INR 115 bn

Crop protection market - export, INR

121 bn

Seed market, INR 113 bn

Fertilizer market, INR 598 bn

Micro Irrigation market, INR 33 bn

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

FY08 FY13 FY08 FY13 FY08 FY13 FY08 FY13 FY08 FY13

INR

per

MT

Wheat Maize Pulses (arhar) Cotton Paddy

Agro-input market in India has tailwind from rural welfare

schemes

Equity Research l India agriculture inputs

26 February 2014 11

Figure 15: Trend in the government’s rural welfare scheme expenditure

Source: India Budget, Standard Chartered Research

Subsidised markets – Fertilizers and micro-irrigation

Fertilizers and micro-irrigation markets have traditionally been subsidised in India

owing to the need to promote higher usage and affordability among farmers.

Subsidies usually are a help in increasing demand; however, given the poor state of

government finances and inefficient processes, this has been a headwind rather than

a tailwind for the Indian agro-inputs sector. We also note that India features poorly in

our global sustanability report for agriculture, predominantly owing to increases in

subsidy levels. Refer Measuring sustainable development by John Calverley.

Fertilizers. While fertilizers is the biggest segment of the farm inputs market, the

segment is saddled with issues of high subsidies and is often hostage to the

government’s policy decisions. The urea (N) market is the largest in terms of tonnage

at 30mt, followed by phosphatic (DAP) fertilizers at 9mt and complex fertilizers at

7.3mt. Urea players are subsidised on the basis of a fixed RoE on their regulated

capital employed and retail prices are regulated by the government. Phosphatic and

potassium players are remunerated on a nutrient-based subsidy (NBS) and the

government periodically fixes the amount of subsidy for such fertilizers with the

manufacturers being free to price their products in the market. Owing to delays in

subsidy payments from the government, most fertilizer companies have been

struggling with high working capital requirements of late, curtailing their return ratios.

Average subsidy receivable days for the Indian fertilizer industry have increased to

over 110 days in FY13 from c. 50 days in FY08.

Figure 16: Average subsidy receivable days – Indian fertilizer industry

* For Chambal Fertilizers, Coromandel International, Rashtriya Chemical Fertilizers

Source: Company, Standard Chartered Research

0

50

100

150

200

250

300

350

400

450

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

INR

bn

Rural development - total disbursement

40

50

60

70

80

90

100

110

120

FY07 FY08 FY09 FY10 FY11 FY12 FY13

Average subsidy days receivables*

CAGR 17%

Subsidy delays and policy exposure makes fertilisers and micro-irrigation less attractive

Equity Research l India agriculture inputs

26 February 2014 12

Micro-irrigation (MIS). Micro-irrigation refers to the drip irrigation and sprinkler

irrigation markets. Jain Irrigation is the largest domestic company in the micro

irrigation segment and estimates the total micro-irrigation market to be worth INR

33bn with 5mn ha under coverage. According to the company, 17mn ha can be

brought under micro irrigation by 2017. While the potential for the MIS market in India

seems big, one concern for the micro irrigation industry is the high level of subsidies

provided by the government (between 50-70%). Like in the case of fertilizers, subsidy

payments are usually delayed, resulting in bloated balance sheets for most players.

Non-subsidised markets – Our preferred play

Owing to issues related to process inefficiencies and risk of delays in subsidy

payments or changes in government policies, we prefer playing the agro-input theme

through non-subsidised segments such as pesticides, seeds and other nutrients. The

combined size of the Indian pesticides and seeds market is estimated to grow to INR

650bn by 2017 from INR 350bn in 2012 – a CAGR of 13%. According to the

Federation of Indian Chambers of Commerce and Industry (FICCI), the domestic

pesticides market is estimated to grow at a CAGR of 9% over FY13-18 and

pesticides export market is estimated to grow at a CAGR of 15% up to FY20. We

estimate the seed market to grow at a CAGR of 15% over 2012-17 in line with

projections from Assocham.

Figure 17: Indian pesticides and seeds market size

Source: FICCI, Assocham, Standard Chartered Research estimates

0

100

200

300

400

500

600

700

2008 2009 2010 2011 2012 2017E

INR

bn

Domestic pesticides market

Pesticides export market

Seeds market

CAGR 17%

CAGR 13%

Pesticides and seeds are our preferred plays on agro-inputs

space

Equity Research l India agriculture inputs

26 February 2014 13

Pesticides: Domestic tailwind and huge export opportunity Around 85% of India’s crop losses are due to causes that can be controlled by

pesticides (INR 1.2tn of avoidable crop losses annually).

Pesticide penetration is low in India (0.6kg/ha) vs. global peers (5-17 kg/ha).

The domestic pesticides market is expected to grow at a CAGR of 9% p.a. to INR

180bn by FY18. Rallis and UPL are the prominent domestic players.

Pesticide exports are projected to grow faster at 15% p.a. to USD 5.8bn by FY20.

PI and Rallis are best positioned to tap the export opportunity.

Direct impact on yields. According to estimates from Crop Care Federation of India

(CCFI), 85% of annual crop losses are due to pest infestation, diseases and weeds.

Total annual losses owing to these factors is estimated at INR 1.2tn. Total crop

losses across key crops such as rice, cotton and sugarcane are estimated to be in

the region of 20-30%.

Figure 18: Avoidable crop losses by cause Figure 19: Avoidable crop losses by key crop

Source: CCFI, Standard Chartered Research Source: CCFI, Standard Chartered Research

Low penetration of pesticides in the country. We estimate India’s domestic

pesticides market at INR 105bn for FY12. The country has a very low pesticides use

per acre of arable land as can be seen from the following chart.

Figure 20: Pesticides/ha of arable land

Source: FICCI, Standard Chartered Research

Weeds, 33%

Insects, 26%

Diseases, 26%

Rodents & Others, 15% 30% 30%

20% 20% 20%

0%

5%

10%

15%

20%

25%

30%

35%

Rice Cotton Sugarcane Potato Soybean

% c

rop

loss

INR 300bn

INR 99bn INR 44bn INR 42bn

INR 280bn

17

13 12

7 7

5 5

0.6

0

2

4

6

8

10

12

14

16

18

Taiwan China Japan USA Korea France UK India

kg/h

a

Equity Research l India agriculture inputs

26 February 2014 14

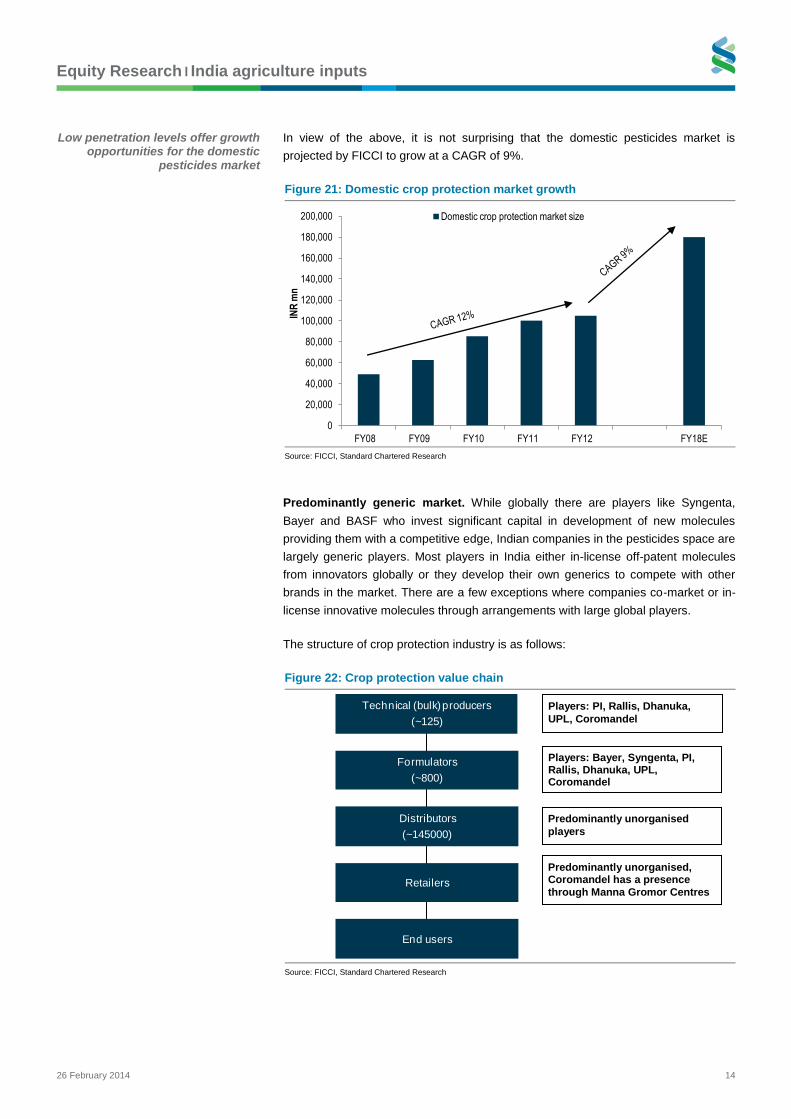

In view of the above, it is not surprising that the domestic pesticides market is

projected by FICCI to grow at a CAGR of 9%.

Figure 21: Domestic crop protection market growth

Source: FICCI, Standard Chartered Research

Predominantly generic market. While globally there are players like Syngenta,

Bayer and BASF who invest significant capital in development of new molecules

providing them with a competitive edge, Indian companies in the pesticides space are

largely generic players. Most players in India either in-license off-patent molecules

from innovators globally or they develop their own generics to compete with other

brands in the market. There are a few exceptions where companies co-market or in-

license innovative molecules through arrangements with large global players.

The structure of crop protection industry is as follows:

Figure 22: Crop protection value chain

Source: FICCI, Standard Chartered Research

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

FY08 FY09 FY10 FY11 FY12 FY18E

INR

mn

Domestic crop protection market size

Technical (bulk) producers

(~125)

Formulators

(~800)

Distributors

(~145000)

Retailers

End users

Players: PI, Rallis, Dhanuka,

UPL, Coromandel

Players: Bayer, Syngenta, PI, Rallis, Dhanuka, UPL, Coromandel

Predominantly unorganised

players

Predominantly unorganised, Coromandel has a presence

through Manna Gromor Centres

Low penetration levels offer growth opportunities for the domestic

pesticides market

Equity Research l India agriculture inputs

26 February 2014 15

Exports – High growth opportunity. We believe that Indian companies have a

strong potential to grow their exports for crop protection products. Pesticide exports

by Indian companies are estimated to be c.USD 2bn. According to FICCI, the export

market is projected to increase at a CAGR of 15% to reach USD 5.8bn by FY20. We

estimate the pesticides export market to double to INR 247bn by 2017 from INR

121bn in 2012.

Figure 23: Pesticides exports from India

Source: FICCI, Standard Chartered Research

Indian players’ competitive advantages in the export market include low-cost

manufacturing and availability of trained manpower and capacities for production.

The major export markets for Indian companies are the US, Europe and Asia

(predominantly Japan).

In addition to exporting generic pesticides to international markets, Indian companies

are also tying up with global pesticide manufacturers for contract manufacturing of

technical compounds. Industry sources believe that the contract manufacturing space

could grow substantially in the future owing to increased interest from Japanese

players (driven by a desire to diversify away the concentration risk in Japan) and

western players (driven by a need to cut costs and diversify their manufacturing base

away from China).

We believe that a robust export market can also help Indian companies diversify their

revenue stream away from only the domestic market given that the Indian market can

be impacted in times of unusual weather conditions.

Some of the prominent players in pesticide exports are Rallis and PI Industries. PI

Industries has shown significant growth in its custom synthesis and manufacturing

business (CSM) over the past few years, underscoring the strong potential of the

industry.

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2017E

INR

bn

Pesticides exports, especially custom manufacturing offers

strong growth potential

Equity Research l India agriculture inputs

26 February 2014 16

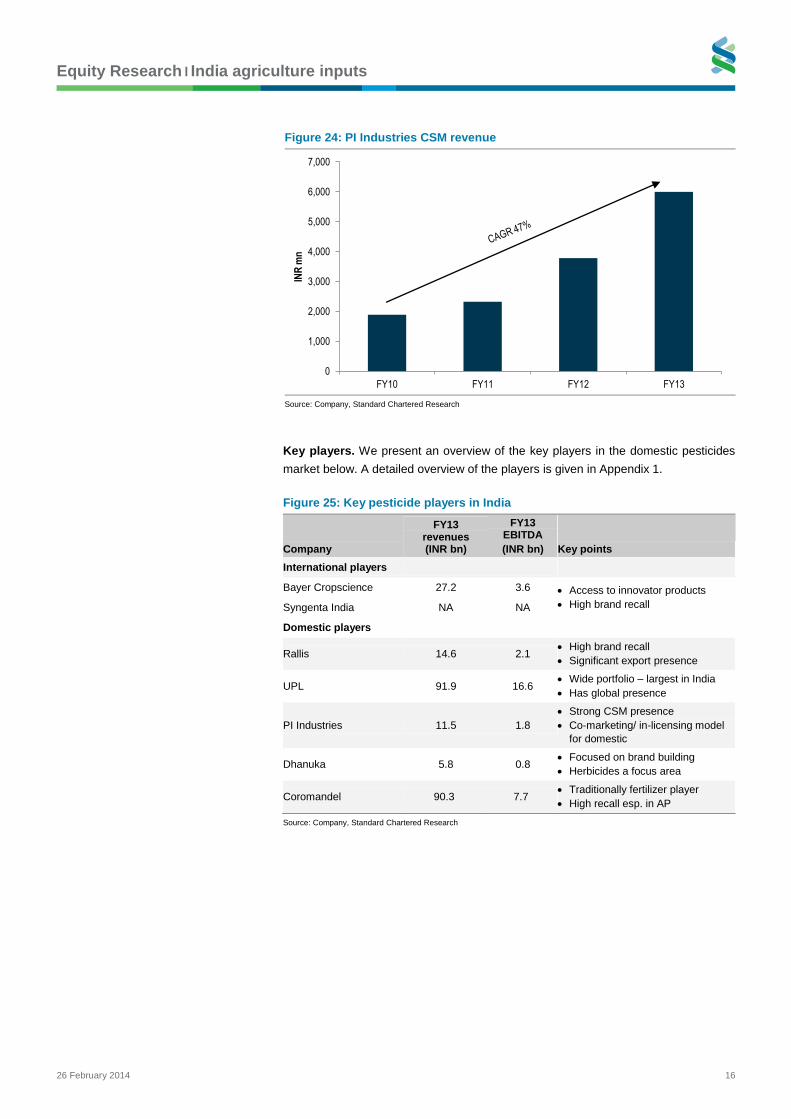

Figure 24: PI Industries CSM revenue

Source: Company, Standard Chartered Research

Key players. We present an overview of the key players in the domestic pesticides

market below. A detailed overview of the players is given in Appendix 1.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY10 FY11 FY12 FY13

INR

mn

Figure 25: Key pesticide players in India

Company

FY13 revenues (INR bn)

FY13 EBITDA

(INR bn) Key points

International players

Bayer Cropscience 27.2 3.6 Access to innovator products

High brand recall Syngenta India NA NA

Domestic players

Rallis 14.6 2.1 High brand recall

Significant export presence

UPL 91.9 16.6 Wide portfolio – largest in India

Has global presence

PI Industries 11.5 1.8

Strong CSM presence

Co-marketing/ in-licensing model

for domestic

Dhanuka 5.8 0.8 Focused on brand building

Herbicides a focus area

Coromandel 90.3 7.7 Traditionally fertilizer player

High recall esp. in AP

Source: Company, Standard Chartered Research

Equity Research l India agriculture inputs

26 February 2014 17

Brand and distribution driven market The pesticides market is unorganised and identifying key attributes that distinguish

winners can be difficult.

We conducted on the ground checks with over 33 dealers across seven states in

India to identify key differentiators between companies.

With the market being dominated by generic products, brands stood out as a

winning attribute almost unanimously across states. The strength of distribution

and farmer engagement were the other key winning attributes.

Rallis and UPL are among the top domestic branded players. Rallis and

Coromandel have differentiated distribution/farmer engagement models.

To identify the key attributes distinguishing the winners in the Indian crop protection

space, we spoke with over 33 agriculture distributors across various geographies in

India. The strength of a brand emerged as the single largest differentiator and

determinant of buyer behaviour.

Figure 26: State-wise key determinants of buyer behaviour

States Brand

Distribution/ farmer

engagement Chemical

composition

Other factors

(price, word of mouth etc)

Maharashtra

Karnataka

Andhra Pradesh

Gujarat

Punjab

Haryana

Uttar Pradesh

Rank Colour Rank Colour

1 3

2 4

Source: Standard Chartered Research

Survey breadth and methodology. We surveyed 33 agro input distributors across

seven states in India. These seven states together accounted for 69% of India’s

agriculture output in FY13.

Brand and distribution/ farmer engagement are critical for

success in pesticides market

Equity Research l India agriculture inputs

26 February 2014 18

Figure 27: Location of dealers surveyed

Source: RBI, Standard Chartered Research

Our questions to dealers were focussed on determining the key determinants of

buyer preferences and indentifying companies that are most distinguished based on

the winning factors thus determined.

Brand. From our survey, the strength of a brand emerged as the single most

important variable impacting buyer decisions across the states. During our visits and

conversations, we came across the instance of a branded product from Bayer,

Confidor, which sells at over 2x its generic peers. The fact that Confidor is rated

among the top brands in the Indian agrochemicals space despite this fact highlights

the strength of the brand.

Rallis featured as the most successful domestic brand, followed by UPL, from our

survey. Most dealers were of the view that level of brand stickiness is medium to high

among their customers.

Aurangabad

(4 dealers)

Nashik

(1 dealer)

Ahmedabad

(3 dealers)

Vadali

(1 dealer)Rajkot

(1 dealer)

Ludhiana

(3 dealers)

Chandigarh

(2 dealers)Kurukshetra

(1 dealer)

Sirsa

(4 dealers)

Bilhaur

(1 dealer)

Hamirpur

(1 dealer)

Saharanpur

(2 dealers)

Bangalore

(3 dealers)Mysore

(1 dealer)

Hubli

(1 dealer)

Rajanagaram

(2 dealers)

Jaggampet

(2 dealers) > 10

5 - 10

< 5

NA

% of India's agriculture output

Brand emerged as key differentiator across the seven

states we surveyed

Equity Research l India agriculture inputs

26 February 2014 19

Figure 28: Brand performance ranking

Distributors brand performance ranking

States 1 2 3 4

Maharashtra Syngenta Bayer Dow Rallis

Karnataka Bayer Rallis Syngenta Dupont

Andhra Pradesh Bayer Syngenta Rallis Coromandel

Gujarat Bayer Rallis UPL Dupont

Punjab Bayer Syngenta Indofil Rallis

Haryana Syngenta Bayer Rallis Monsanto

Uttar Pradesh Bayer UPL Rallis Syngenta

Source: Standard Chartered Research

Distribution. As seen in Fig. 28 above, the width of distribution and farmer

engagement is key for industry players to be able to differentiate their offerings. This

is understandable given the generic nature of the Indian crop protection market and

the lack of exclusivity from retailers and dealers. A summary of distribution networks

of companies under our coverage is given below.

Figure 29: Distribution network strength

Rallis PI Kaveri UPL Coromandel

No. of dealers c.2,500 >9,000 c.15,000 c.7,000 > 7,000

No. of retailers >40,000 >40,000 NA NA NA

Source: Standard Chartered Research

We believe that while breadth of reach through third-party retail channels is

important, there is sustainable advantage to be achieved through direct farmer

outreach programs. According to our dealer survey, the demonstration of product

strength through field trials has proved to be the most successful method when

launching a new product in most of the markets. Therefore, we believe that

companies that have stronger farmer engagement programs are better placed vs.

their peers and such programs can be instrumental in establishing brand equity.

Two examples of farmer outreach programs are in the case of Rallis and Coromandel

Fertilizers.

I. Rallis Kisan Kutumbha: The Rallis Kisan Kutumbha (RKK) is one of the most

extensive privately run farmer outreach programs in the country and has a strength

of c.1mn farmers currently. Under this program, Rallis maintains a comprehensive

data base of the member farmers including their cropping patterns, yields and input

usage. Rallis provides on the ground support including regular farm visits, providing

extensive technical advice, appraising farmers of latest developments and

organizing seminars for interaction with agronomists and experts. In addition to this,

Rallis also sets up demo farms at the member farmer areas to demonstrate the

difference in yields owing to adoption of best practices and agro inputs. Besides

providing a strong relationship with farmers and an avenue to promote Rallis’ own

products, RKK also allows the company to get inputs and market demand

assessment from farmers for determining future product launch pipeline.

Farmer engagement programmes that build relationship and trust are as critical as breadth of distribution

Equity Research l India agriculture inputs

26 February 2014 20

II. Manna Gromor Centres (Coromandel Fertilizers): Manna Gromor Centres are

retail outlets promoted by Coromandel Fertilizers. The company currently has over

600 centres spread across Andhra Pradesh and Karnataka, servicing close to 2mn

farmers. The company targets to have 1,000 centres over the next few years. We

visited a few MGCs and from our visits, some of the differentiated services being

offered by MGCs to local farmers are as follows:

a) Farmer helpline

b) Transparent pricing and sale price disclosures

c) Advice on best and optimum pesticide usages

d) Comprehensive farm solutions under one roof.

Equity Research l India agriculture inputs

26 February 2014 21

Seeds: Set to accelerate We expect India’s seed market to grow at a CAGR of 15% to INR 230bn in 2017

from INR 110bn in 2012.

We view the industry as attractive owing to low penetration of hybrid seeds, high

barriers to entry and potential for non-linear growth.

Kaveri Seed and Rallis are our preferred picks to play this theme.

According to the International Seed Federation (ISF), India’s seed market is the sixth

largest in the world and is estimated at c. USD 2bn (INR 113bn) for 2012. According

to Assocham, the seeds market is expected to grow at a 15% CAGR over the

medium term and we estimate the market to grow to INR 230bn by 2017.

The size of India’s seed market looks low in comparison to global emerging market

peers as shown in the chart below.

Figure 30: India’s seed market

Source: ISF, Assocham, Standard Chartered Research

Figure 31: Seed market vs. land area

Source: ISF, OECD-FAO, Standard Chartered Research

0

50

100

150

200

250

2008 2009 2010 2011 2012 2017E

INR

bn

Seed market

0

2,000

4,000

6,000

8,000

10,000

12,000

0 20 40 60 80 100 120 140 160 180

Do

mes

tic

seed

mar

ket

(U

SD

mn

)

Arable land (mn hectares)

China

India

Russia

Brazil

Argentina

Turkey

Ample scope for increasing hybrid seed penetration in India

Equity Research l India agriculture inputs

26 February 2014 22

While cotton has been dominating the hybrid market with 80% hybridization, crops

such as rice have an extremely low hybridization rate (less than 5%). We believe that

going forward, stronger emphasis on yield would necessitate higher use of hybrids in

the country.

High barrier to entry. The key differentiator for seed companies is the strength of

their research and development (R&D) franchise. Typically, development of a new

seed takes 8-10 years between controlled atmosphere evaluation and commercial

production, given seeds cannot be manufactured but only grown as part of biological

processes. In addition, it takes another 3-4 years to generate acceptability of the

seed among farmers. Therefore, once a seed variety is established in the market, it

becomes difficult for a new entrant to challenge it for a long period of time and the

innovator enjoys a strong competitive advantage.

Non-linear growth. Typically, farmers test a seed in a small section of their farms to

assess its viability and merits under local conditions. Once they are comfortable, the

growth in area under new seed for a given farmer can be exponential. This offers

opportunities for non-linear growth to companies that have seeds under testing with

farmers.

An instance of non-linear growth can be seen from the pattern of growth of Bt Cotton

acreage in India since its introduction in 2002. Bt Cotton is the only large scale

genetically modified seed being used in India currently.

Figure 32: Bt cotton market in India

Source: ISAAA, Standard Chartered Research

Genetically modified seeds can provide the next leg up

Genetically modified (GM) seeds have relatively little adoption in India at the moment

given GM seeds have been only approved for use in cotton so far. However,

persistent low productivity, high food inflation and the strong impact of GM seeds

witnessed on the cotton crop would necessitate the introduction of GM seeds in India

over the medium term, in our view. However, it is difficult to predict the timing of such

approvals given that attempts to introduce GM seeds have been met with strong

resistance from various interest groups in the past. We are not currently building in

any upside from the adoption of GM seeds into our forecasts.

0.8 0.8 5.3

13.0

38.4

62.1

76.2

83.5

93.6

0

10

20

30

40

50

60

70

80

90

100

0

5,000

10,000

15,000

20,000

25,000

30,000

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

Are

a in

lakh

ha

INR

mn

Bt cotton market India Bt cotton area hectares

Seed market offers non-linear growth and higher barrier to entry

Equity Research l India agriculture inputs

26 February 2014 23

Figure 33: Productivity of cotton after introduction of Bt cotton

Source: Cotton Advisory Board, Standard Chartered Research

Issues related to GM seeds – Currently, use of GM seeds is banned in India except

in the case of cotton. Also, Bt gene currently used for GM cotton seeds is patented by

Monsanto and domestic players pay a royalty to Monsanto for the use of this gene.

Even in future, if and when Bt is introduced in other crops, domestic players would

need to pay a royalty for use of specific patented genes. The impact of GM on

pesticides and other agro inputs is another issue that needs to be assessed further in

the event GM is allowed into the country. Note that while initially after the introduction

of Bt Cotton, pesticide usage for the cotton crop declined, however, newer varieties

of pests (sucking pests) have since emerged, necessitating introduction of new

pesticide molecules.

Key players. We present an overview of the key players in the seeds market below.

A detailed overview of the players is given in Appendix 1.

Figure 34: Key seed players in India

Company

FY13 revenues (INR bn)

FY13 EBITDA (INR bn) Key points

International players

Syngenta NA NA Focus on maize and rice seeds

Predominantly a seeds player

Only listed subsidiary of Monsanto

globally

Monsanto 4.4 0.7

Domestic players

Nuziveedu Seeds NA NA Largest cotton seed player – unlisted

Kaveri Seed 7.1 1.4 No. 2 player in cotton seeds market –

only listed seeds pure play

Rallis 14.6 2.1 Through 80% subsidiary – Metahelix

Advanta Seeds 10.7* 1.7* Associate of UPL

Significant export presence

* Advanta seeds revenue and EBITDA is CY ended 2012

Source: Company, Standard Chartered Research

0

100

200

300

400

500

600

FY

91

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

Yie

ld k

gs

per

hec

tare

Cotton yield kgs (per hectare)

Eventual introduction of GM seeds can boost seed market but can also

impact pesticides demand

Equity Research l India agriculture inputs

26 February 2014 24

Our framework for evaluating companies We value companies under our coverage on six key parameters – brand,

distribution, product mix, export mix, leverage and working capital.

Rallis fares the best on the two attributes (brand and distribution/ farmer

engagement) that are considered key differentiators based on our on-the-ground

dealer survey.

Rallis and PI Industries emerge as our top two picks based on their financial and

operational factors mentioned above.

While this framework is instrumental in identifying long-term winners, valuation

distortions can impact short-term stock preferences.

Based on our understanding of industry fundamentals, we introduce our proprietary

framework to evaluate the relative attractiveness of the listed agro-input players in

India. We assess each company individually and rank each of the five companies

under our coverage between 1 to 5 with 1 being the most attractive. To narrow down

on the attributes, we have used findings from our on-the-ground survey of agro-input

dealers and ranked companies based on their brand and distribution/farmer

engagement strength. In addition, we use attributes such as product and

geographical diversification to assess the ability of a business to withstand domestic

weather-related volatility; and leverage and working capital to the assess their

financial strength.

Our overall ranking for companies under our coverage is shown below.

Figure 35: Ranking of companies under our coverage

Rallis PI Kaveri UPL** Coromandel*

Strength of brand 1 3 2 2 3

Distribution/ farmer engagement 1 2 4 4 2

Product diversification 1 4 5 2 3

Geographic diversification 3 1 4 1 NA

Leverage 2 3 1 4 NA

Working capital 2 3 1 4 NA

Overall Rank 1 2 3 4 NA

Source: Standard Chartered Research

Note: * CRIN financials not available separately for non-fertilizer business beyond EBITDA line.

Note: ** We have rated UPL’s India business only for ranking of exports, leverage/ working capital at global levels

We believe that our framework can serve as a useful tool in assessing the long-term

winners in the Indian agro-input space. We, however, recognize that valuations would

also play a crucial role in determining short-term preferences within our coverage

universe.

A detailed assessment of the six factors considered by us above is given below.

Strength of brand. We rate companies with stronger brand perception higher. Based

on our survery of agro-input distributors, Rallis stands out as the player with the

highest brand recall in our coverage universe, followed by UPL. Kaveri Seed is seen

as one of the top 2 brands in cotton seeds.

Our framework evaluates companies based on six operational and financial

parameters- Rallis and PI emerge as top picks

Equity Research l India agriculture inputs

26 February 2014 25

Figure 36: Ranking based on brand and distribution strength

Rallis PI Kaveri UPL Coromandel

No. of districts with recall 7 1 2 2 1

Rank 1 3 2 2 3

No. of districts with recall based on our survey of 33 dealers across 7 states in the country

Source: Standard Chartered Research

Distribution/ farmer engagement. While the companies under our coverage have

varying degrees of reach through distributors and retailers, we also assess

differentiated farmer outreach programs adopted by companies to rank them. On this

basis, Rallis – with the RKK program – stands out as a differentiated player with a

competitive edge while Coromandel’s focus on farmer engagement through Manna

Gromor Centres (MGC) makes it stand out. RKK is a farmer engagement program

with over 1mn members and aims to provide on-site assitance to its members.

Similarly, Coromandel’s MGC initiative helps it engage directly with the farmers

though its 650 retail outlets. PI Industries with its differentiated product offering

(exclusive molecules) has a differentiated offering, in our view.

Figure 37: Ranking based on brand and distribution strength

Rallis PI Kaveri UPL Coromandel

No. of dealers c.2,500 >9,000 c.15,000 c.7,000 > 7,000

No. of retailers >40,000 >40,000 NA NA NA

Differentiated strategy Rallis Kisan Kutumbha

Focus on in-licensing

NA NA Manna Gromor

Centre

Rank 1 2 4 4 2

Source: Companies, Standard Chartered Research

Product mix diversification. We believe that players with a more diverse product

mix would have a better and more stable revenue profile vs. players with a single

product focus. This is owing to (1) the higher number of touch points with the

consumer and (2) the ability to offset seasonal and cyclical weakness in one product

line with other products. Rallis and UPL feature best on this measure.

Figure 38: Ranking based on product mix diversification

Rallis PI Kaveri UPL Coromandel

Pesticides X X

X X

Seeds X

X X

PGN X X

X X

Organic manure X

X X

Rank 1 4 5 2 3

Source: Standard Chartered Research.

Equity Research l India agriculture inputs

26 February 2014 26

Geographic diversification. In addition to product diversification, players with

exposure to export markets fare well, given their ability to better withstand the

volatility owing to weather-related issues in one geography. UPL, PI Industries and

Rallis fare best on this metric within our coverage universe. In addition, the presence

in the fast growing contract manufacturing segment of the export market can provide

strong growth given favourable industry dynamics. Rallis and PI are the two players

that have a significant presence in this segment.

Figure 39: Ranking based on geographic diversification

Rallis PI Kaveri UPL Coromandel

Exports/ Sales 29% 55% NA 56% NA

Rank 3 1 4 1 NA

Source: Companies, Standard Chartered Research. Note: UPL standalone export numbers taken for this analysis.

Leverage. Companies with lower leverage are better positioned to withstand any

volatility owing to weather-related hardships, deserving higher rankings.

Figure 40: Ranking based on leverage and working capital

Rallis PI Kaveri UPL CRIN

Net debt/ EBITDA (FY13) 0.5x 1.1x -1.0x 1.4x NA

Rank 2 3 1 4 NA

Source: Companies, Standard Chartered Research

Working capital. A higher working capital intensity can be a sign of potential weak

product demand leading to higher stickiness of inventory or more linient terms of

trade to dealers. Kaveri Seed and Rallis fare best on this parameter.

Figure 41: Rating based on leverage and working capital

Rallis PI Kaveri UPL Coromandel

Net working capital days (FY13) 45 84 31 105 NA

Rank 2 3 1 4 NA

Source: Companies, Standard Chartered Research

Equity Research l India agriculture inputs

26 February 2014 27

Sector valuation Valuations for Indian agro-input companies are at the higher end of their historical

trading range.

Nevertheless, we believe that valuations could sustain at current levels owing to

significantly better EPS growth and RoEs for the industry vs. history.

We have considered the four companies under our coverage that are pure plays on

sub-sectors that we prefer (pesticides, seeds and pesticides export) for the purpose

of assessing sector valuations.The companies are Rallis, UPL, PI Industries and

Kaveri Seed. Valuations for the sector are given below.

Figure 42: Agro-input sector valuation

Source: Bloomberg, Standard Chartered Research

As can be seen above, sector valuations are currently towards the higher end of their

historical trading range. Nevertheless, given the high EPS growth and RoE trends,

we believe that current valuations are sustainable.

Figure 43: Sector valuation vs. EPS growth Figure 44: Sector valuation vs. forward RoE

Source: Bloomberg, Standard Chartered Research Source: Bloomberg, Standard Chartered Research

While we remain convinced of the structural strength of the Indian agro inputs market

one key cyclical risk to valuations is obviously the weather, given the high correlation

Indian farmer incomes have with the monsoons (please refer to Fig. 10).

0

2

4

6

8

10

12

14

16

18

20

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14

PE

R m

ult

iple

Agri sector custom index forward PER

Average

+1 SD

-1 SD

-20%

0%

20%

40%

60%

0

10

20

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

EP

S g

row

th

PE

R m

ult

iple

Agri sector custom index forward PER Average +1 SD -1 SD Agri sector EPS growth

20%

25%

30%

0

10

20

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

RO

E

PE

R m

ult

iple

Agri sector custom index forward PER Average +1 SD -1 SD Agri sector ROE

Equity Research l India agriculture inputs

26 February 2014 28

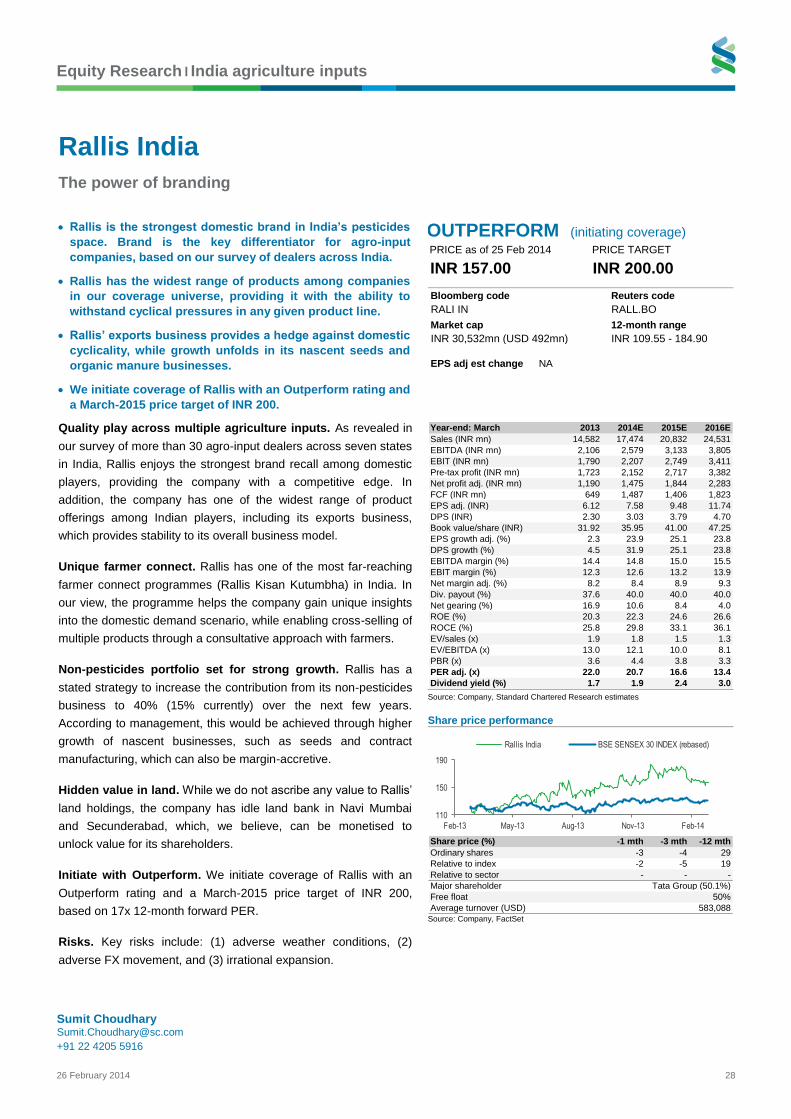

Rallis India

The power of branding

Rallis is the strongest domestic brand in India’s pesticides

space. Brand is the key differentiator for agro-input

companies, based on our survey of dealers across India.

Rallis has the widest range of products among companies

in our coverage universe, providing it with the ability to

withstand cyclical pressures in any given product line.

Rallis’ exports business provides a hedge against domestic

cyclicality, while growth unfolds in its nascent seeds and

organic manure businesses.

We initiate coverage of Rallis with an Outperform rating and

a March-2015 price target of INR 200.

OUTPERFORM (initiating coverage)

Quality play across multiple agriculture inputs. As revealed in

our survey of more than 30 agro-input dealers across seven states

in India, Rallis enjoys the strongest brand recall among domestic

players, providing the company with a competitive edge. In

addition, the company has one of the widest range of product

offerings among Indian players, including its exports business,

which provides stability to its overall business model.

Unique farmer connect. Rallis has one of the most far-reaching

farmer connect programmes (Rallis Kisan Kutumbha) in India. In

our view, the programme helps the company gain unique insights

into the domestic demand scenario, while enabling cross-selling of

multiple products through a consultative approach with farmers.

Non-pesticides portfolio set for strong growth. Rallis has a

stated strategy to increase the contribution from its non-pesticides

business to 40% (15% currently) over the next few years.

According to management, this would be achieved through higher

growth of nascent businesses, such as seeds and contract

manufacturing, which can also be margin-accretive.

Hidden value in land. While we do not ascribe any value to Rallis’

land holdings, the company has idle land bank in Navi Mumbai

and Secunderabad, which, we believe, can be monetised to

unlock value for its shareholders.

Initiate with Outperform. We initiate coverage of Rallis with an

Outperform rating and a March-2015 price target of INR 200,

based on 17x 12-month forward PER.

Risks. Key risks include: (1) adverse weather conditions, (2)

adverse FX movement, and (3) irrational expansion.

Source: Company, Standard Chartered Research estimates

Share price performance

Source: Company, FactSet

PRICE as of 25 Feb 2014

INR 157.00

PRICE TARGET

INR 200.00

Bloomberg code Reuters code

RALI IN RALL.BO

Market cap 12-month range

INR 30,532mn (USD 492mn) INR 109.55 - 184.90

EPS adj est change NA

Year-end: March 2013 2014E 2015E 2016E

Sales (INR mn) 14,582 17,474 20,832 24,531

EBITDA (INR mn) 2,106 2,579 3,133 3,805

EBIT (INR mn) 1,790 2,207 2,749 3,411

Pre-tax profit (INR mn) 1,723 2,152 2,717 3,382

Net profit adj. (INR mn) 1,190 1,475 1,844 2,283

FCF (INR mn) 649 1,487 1,406 1,823

EPS adj. (INR) 6.12 7.58 9.48 11.74

DPS (INR) 2.30 3.03 3.79 4.70

Book value/share (INR) 31.92 35.95 41.00 47.25

EPS growth adj. (%) 2.3 23.9 25.1 23.8

DPS growth (%) 4.5 31.9 25.1 23.8

EBITDA margin (%) 14.4 14.8 15.0 15.5

EBIT margin (%) 12.3 12.6 13.2 13.9

Net margin adj. (%) 8.2 8.4 8.9 9.3

Div. payout (%) 37.6 40.0 40.0 40.0

Net gearing (%) 16.9 10.6 8.4 4.0

ROE (%) 20.3 22.3 24.6 26.6

ROCE (%) 25.8 29.8 33.1 36.1

EV/sales (x) 1.9 1.8 1.5 1.3

EV/EBITDA (x) 13.0 12.1 10.0 8.1

PBR (x) 3.6 4.4 3.8 3.3

PER adj. (x) 22.0 20.7 16.6 13.4

Dividend yield (%) 1.7 1.9 2.4 3.0

110

150

190

Feb-13 May-13 Aug-13 Nov-13 Feb-14

Rallis India BSE SENSEX 30 INDEX (rebased)

Share price (%) -1 mth -3 mth -12 mth

Ordinary shares -3 -4 29

Relative to index -2 -5 19

Relative to sector - - -

Major shareholder Tata Group (50.1%)

Free float 50%

Average turnover (USD) 583,088

Sumit Choudhary [email protected]

+91 22 4205 5916

RALI IN INR 157.00 INR 200.00

Equity Research l India agriculture inputs

26 February 2014 29

Investment thesis High-quality play across the breadth of India’s agriculture inputs space

We view Rallis as a high-quality play on India’s agriculture inputs space. The

company has some of the strongest brands in the country – its products comprise

seven of the top-ten pesticide brands in India.

Figure 45: Rallis – Brand positioning

Source: Company

Following our conversations with dealers (33 dealers in seven states across India),

Rallis emerged as the strongest domestic brand in most of the states.

Figure 46: Rallis – Brand presence

Distributors’ brand performance ranking

States 1 2 3 4

Maharashtra Syngenta Bayer Dow Rallis

Karnataka Bayer Rallis Syngenta Dupont

Andhra Pradesh Bayer Syngenta Rallis Coromandel

Gujarat Bayer Rallis UPL Dupont

Punjab Bayer Syngenta Indofil Rallis

Haryana Syngenta Bayer Rallis Monsanto

Uttar Pradesh Bayer UPL Rallis Syngenta

Source: Standard Chartered Research

In addition, we believe that Rallis’ strong range of products through multiple offerings,

such as seeds, organic manure, agricultural implements and pesticides, provides the

company with multiple touch-points with the farmer.

Figure 47: Rallis’ presence across multiple products

Product Rallis’ presence

Pesticides Herbicides, insecticides and fungicides

Seeds Through Metahelix, an 80% subsidiary of Rallis

Organic manure Through 51% subsidiary, Zero Waste Agro

Source: Company, Standard Chartered Research

Equity Research l India agriculture inputs

26 February 2014 30

Unique farmer connect

Rallis has a wide reach among farmers through its on-the-ground sales force and

farmer outreach programmes. The company also has a practice of conducting

focused group discussions (FGDs) with farmers to gauge their product requirements.

According to management, Rallis conducted FGDs with over 4,000 farmers in more

than 20,000 villages over the seven years up to FY12. We believe such a strategy

provides the company with unique insights into farmer requirements.

Apart from FGDs, Rallis has numerous farmer outreach programmes (see figure

below):

Figure 48: Rallis’ farmer outreach programmes

Rallis Kisan Kutumbha Database of more than 1mn famers and their cropping patterns

and input preferences

Samrudh Krishi For grapes, cumin and chilly farmers

Grow More Pulses (MoPu) 0.9mn acres covered with 0.16mn farmers engaged in FY13 –

support for crop productivity and marketing of pulses

Source: Company, Standard Chartered Research

Such farmer outreach programmes help Rallis cross-sell its products such as seeds

and could prove to be an enabler of strong growth and premium pricing, in our view.

Exports business provides a hedge against domestic volatility

The exports business constitutes c.30% of Rallis’ overall revenues. The business

involves exports of generic pesticides, including registering molecules internationally.

In addition, the company also has a presence in the contract manufacturing space for

international players. Rallis has partnered with numerous players for contract

manufacturing in agrochemicals, fine and specialty chemicals, and polymer/

pharmaceutical intermediates. Moreover, we expect the company’s foray into the

CSM business to help generate strong growth in its exports business.

Figure 49: Rallis – International revenue growth

Source: Company, Standard Chartered Research estimates

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY10 FY11 FY12 FY13 FY14E FY15E FY16E

INR

mn

International revenue

CAGR 23%

Equity Research l India agriculture inputs

26 February 2014 31

Non-pesticide business set for solid growth

Management has a stated strategy to increase the share of its non-pesticide portfolio

to 40% over the next few years, from c.15% in FY13. We believe that while a part of

this shift in the mix would come from inorganic growth, a major portion would also be

driven by organic growth. We expect the share of the non-pesticides business to

organically increase to 26% by FY16E.

Rallis acquired a majority stake in Metahelix Life Sciences, a seed research and

manufacturing company, in December 2010. We believe that given its potential to

leverage on Rallis’ strong distribution strength and brand presence, the seed

business can deliver significant growth going forward. In addition, EBITDA margin of

Rallis’ seeds business is currently lower than its industry peers (we estimate its FY13

EBITDA margin of 14%, versus Kaveri Seeds’ EBITDA margin of more than 20%)

and expected to increase as Metahelix gains scale. We have not assumed any

upside from any potential introduction of GM seeds in non-cotton crops in future.

Figure 50: Metahelix – Revenue growth

Source: Company, Standard Chartered Research

Hidden value in land. While we do not ascribe any value to the land bank owned by

Rallis, we note that the company has idle land in two locations: (1) c.25 acres in Navi

Mumbai; and (2) c.90 acres in Secunderabad. We believe these can be monetised in

future, especially if the company needs additional resources for inorganic expansion.

Valuation We value Rallis on a 12-month forward PER multiple of 17x, to arrive at our March-

2015 price target of INR 200 per share. Our target multiple is in line with the historical

PER for Rallis. We believe that a 17x target multiple is justified, given (1) the

expected RoE improvement (to 27% in FY16E from 20% in FY13); and (2) the

expected robust EPS CAGR of 24% during FY13-16E.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY12 FY13 FY14E FY15E FY16E

INR

mn

Metahelix revenue

CAGR 37%

Equity Research l India agriculture inputs

26 February 2014 32

Figure 51: Rallis – Historical PER band

Source: Bloomberg, Standard Chartered Research

Risks Key risks to our investment view arise from the following:

Adverse weather: Like all agriculture businesses, Rallis is also exposed to

significant swings in domestic weather conditions, particularly the monsoon. In

addition, the company is also exposed, albeit to a lesser extent, to fluctuations and

changes in cropping patterns in international geographies owing to its presence in

markets such as the US and Latin America.

Adverse foreign exchange movements: Rallis imports a sizable portion of its raw

materials, and, therefore, adverse foreign exchange movement could impact its

profitability. However, we believe that the company’s exports business could act as a

cushion in such a scenario.

Irrational expansion: Management has a stated target of achieving 40% revenue

from its non-pesticide business over the next few years. While we think this is the

correct strategy to follow, we believe any haste on its part to achieve this target

through expensive acquisitions would be detrimental to our investment case.

Business description Rallis is a Tata Group company engaged in a wide gamut of agricultural inputs. The

company is one of the largest players in the Indian agriculture inputs space, with

revenue of INR 14.6bn in FY13. The key business divisions of Rallis are as follows:

Pesticides: This division has a wide range of insecticides, fungicides and herbicides,

which target Indian agricultural conditions, with emphasis on crops such as rice,

cotton and vegetables. In the pesticides segment, Rallis introduces its own generic

molecules, in addition to in-licensing and co-marketing products from global players.

Some of its international partners include FMC, Syngenta, Nihon Nohyaku and

DuPont.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14

PE

R m

ult

iple

Rallis India forward PER Average +1 SD -1 SD

Target PER 17x

Equity Research l India agriculture inputs

26 February 2014 33

Some of Rallis’ popular products are given below:

Figure 52: Rallis – Popular products

Product Rallis presence

Insecticides Takumi, Mida, Reeva, Rogor, Asataf, Manik

Fungicides Contaf, Master, Fujione

Herbicides Fateh, Tata Metri, Tata Panida

Source: Company, Standard Chartered Research

Rallis has a distribution network that covers 80% of India’s districts, with c.2,500

dealers and more than 40,000 retailers across India.

Domestic institutional business: This division is engaged in providing technical

and bulk composition of various molecules to companies such as Bayer, Syngenta,

UPL, Cheminova, among others.

International business: Rallis’ international business is engaged in the competitive

generic pesticide segment in more than 50 countries globally. The growth strategy is

through partnerships, new registrations and contract manufacturing. For contract

manufacturing, Rallis has the largest pesticide manufacturing capacity in the country,

with a production capacity of more than 10,000MT of technical grade pesticide and

30,000 tonnes of formulations annually.

Non-pesticides portfolio: Rallis’ non-pesticide portfolio comprises divisions such as

seeds, organic manure and plant growth nutrients. The company plans to increase

the proportion of non-pesticide sales to 40% over the next few years.

Metahelix: Rallis has an 80.46% stake in Metahelix, which is predominantly engaged

in the development and sale of hybrid seeds through its 100% subsidiary, Dhanya

Seeds. Dhanya is a technology-driven, hybrid seeds business, with seeds

predominantly in rice, maize, pearl millet and vegetable crops.

Zero Waste Agro Organics (ZW): Rallis has a 51.02% stake in ZW, which is an

organic soil conditioner manufacturing company. Rallis has a majority representation

on the board of the company.

Management: An overview of Rallis’ key management is given below:

Figure 53: Rallis – Board of directors

Gopalakrishnan Chairman

V Shankar Managing Director and CEO

Homi R Khusrokhan Director

B D Banerjee Director

Eknath A Kshirsagar Director

Prakash R Rastogi Director

Bharat Vasani Director

R Mukundan Director

Y K Alagh Director

Y S P Thorat Director

Source: Company

Equity Research l India agriculture inputs

26 February 2014 34

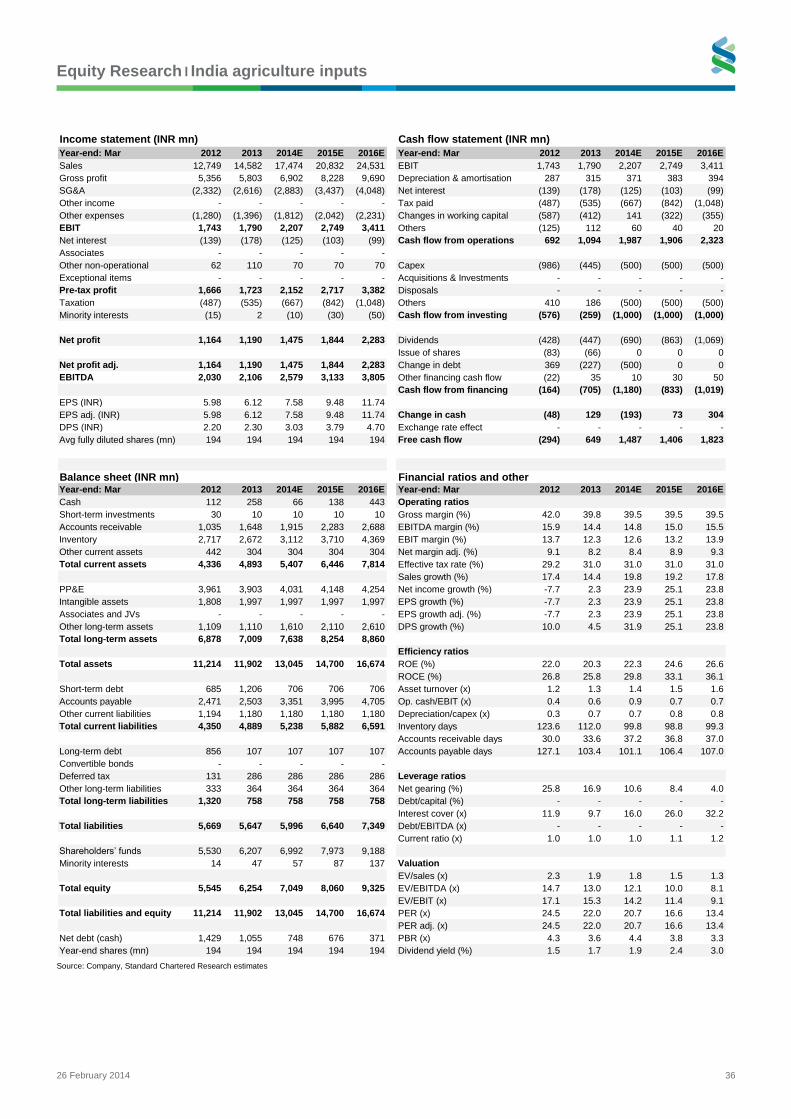

Financials We present below the key assumptions used to project Rallis’ financials:

Domestic formulation and institutional business: We assume a CAGR of 11% in

FY14-16E in our projections. This is in line with the growth which the company has

been witnessing in FY08-14E.

International business: Despite the renewed focus of management on the custom

synthesis business and the company having recently entered into new geographies

like Latin America, we project a 17% CAGR in the international business in FY14-

16E, versus a 20% CAGR generated in FY08-14E.

Non crop business: We project the non-crop business to grow at a CAGR of 41% in

FY14-16E. This would largely be driven by growth in the company’s seeds portfolio.

We estimate that the seeds business (predominantly the hybrid seed selling business

through Metahelix) will constitute more than 60% of Rallis’ non-crop business

revenue by FY16E.

Given these assumptions, we estimate the non-crop portfolio will comprise 26% of

Rallis’ total revenues by FY16E.

Figure 54: Non-crop business revenue and non-crop business revenue as % of

total

Source: Company, Standard Chartered Research estimates

Revenues: We expect Rallis’ overall revenues to increase at a CAGR of 18% in

FY14-16E owing to our aforementioned assumptions.

Figure 55: Rallis – Revenue and revenue CAGR

Source: Company, Standard Chartered Research estimates

2% 4%

11%

15%

18%

22%

26%

0%

5%

10%

15%

20%

25%

30%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY10 FY11 FY12 FY13 FY14E FY15E FY16E

as % o

f revenu

e

INR

mn

Non-corp revenue As % of total company revenue

0

5,000

10,000

15,000

20,000

25,000

30,000

FY10 FY11 FY12 FY13 FY14E FY15E FY16E

INR

mn

Revenue

CAGR 18%

Equity Research l India agriculture inputs

26 February 2014 35

Margins: We estimate EBITDA margin for the seeds business will increase to 19%

by FY16E from 16% in FY14E. Pure-play seed companies such as Kaveri Seeds

currently have an EBITDA margin of more than 20%. We believe that as Metahelix’s

business gathers scale, margins should increase to similar levels as other pure-play

seed players in the industry. We estimate EBITDA margins for the crop protection

business will continue to be in the 14-15% range over FY14-16E.

Figure 56: Seeds and overall EBITDA margins

Source: Company, Standard Chartered Research estimates

EPS growth: Given our revenue and margin projections, we believe that Rallis’ EPS

would increase to INR 11.74 by FY16E from INR 7.58 in FY14E, implying a CAGR of

24% over the two-year period. We also expect its RoE to improve to 27% by FY16E

from 22% in FY14E.

17%

14%

16% 17%

19%

16%

14% 15% 15% 16%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

FY12 FY13 FY14E FY15E FY16E

EB

ITD

A m

arg

in

Seed business EBITDA margin (%) Overall EBITDA margin (%)

Equity Research l India agriculture inputs

26 February 2014 36

Source: Company, Standard Chartered Research estimates

Income statement (INR mn) Cash flow statement (INR mn)

Year-end: Mar 2012 2013 2014E 2015E 2016E Year-end: Mar 2012 2013 2014E 2015E 2016E

Sales 12,749 14,582 17,474 20,832 24,531 EBIT 1,743 1,790 2,207 2,749 3,411

Gross profit 5,356 5,803 6,902 8,228 9,690 Depreciation & amortisation 287 315 371 383 394

SG&A (2,332) (2,616) (2,883) (3,437) (4,048) Net interest (139) (178) (125) (103) (99)

Other income - - - - - Tax paid (487) (535) (667) (842) (1,048)

Other expenses (1,280) (1,396) (1,812) (2,042) (2,231) Changes in working capital (587) (412) 141 (322) (355)

EBIT 1,743 1,790 2,207 2,749 3,411 Others (125) 112 60 40 20

Net interest (139) (178) (125) (103) (99) Cash flow from operations 692 1,094 1,987 1,906 2,323

Associates - - - - -

Other non-operational 62 110 70 70 70 Capex (986) (445) (500) (500) (500)

Exceptional items - - - - - Acquisitions & Investments - - - - -

Pre-tax profit 1,666 1,723 2,152 2,717 3,382 Disposals - - - - -

Taxation (487) (535) (667) (842) (1,048) Others 410 186 (500) (500) (500)

Minority interests (15) 2 (10) (30) (50) Cash flow from investing (576) (259) (1,000) (1,000) (1,000)

Net profit 1,164 1,190 1,475 1,844 2,283 Dividends (428) (447) (690) (863) (1,069)

Issue of shares (83) (66) 0 0 0

Net profit adj. 1,164 1,190 1,475 1,844 2,283 Change in debt 369 (227) (500) 0 0

EBITDA 2,030 2,106 2,579 3,133 3,805 Other financing cash flow (22) 35 10 30 50

Cash flow from financing (164) (705) (1,180) (833) (1,019)

EPS (INR) 5.98 6.12 7.58 9.48 11.74

EPS adj. (INR) 5.98 6.12 7.58 9.48 11.74 Change in cash (48) 129 (193) 73 304