In the name of Allah, the All-merciful the All-compassionate

Iran‘s rising influence in the petrochemicals industry

In the name of GodThe compassionate

The merciful

Mohammad Mehdi Siamian Gorji,Advisor to the CEO

Source: based on The European House Ambrosetti study, 2013

China is the world leaderin plastics production andconversion. Low productioncosts in plastics’ conversionhave triggered investmentsin the plastics industry, including the plasticsmachinery manufacturing.

Strong growth in plasticsconversion sector (more than22.000 companies and 4 millionemployees).

Key drivers are the growingpopulation and the growth ofmanufacturing sectors such asthe automotive sector.

67% of the world’s oil reservesand 45% of the world gas reservesare located in the Middle East .Feedstock provides opportunitiesfor the plastics industry there.

Forward integration of plasticsprocessing industryis on-going.

One-third of the bio-plasticsare produced in Latin America.Access to bio--based feedstockprovides opportunities for theBrazilian bio-plastics industry.

Low energy costs due tonon-conventional fuels.The rate of shale gas in theUS energy production isexpected to grow fromcurrent 10% to 36% by2035.

Iran’s Foreign Investment Promotion and Protection Act (FIPPA - page 14)

The advantages of investing in Iran’s petrochemical industry

Availability of continuous and accessible feeds

Receiving support of the National Petrochemical Company for developing petrochemical industries

Stabilization of feeds prices during the operation based on formulas approved

Discounts defined up to %30 of feedstock to establish plants in least developed areas includingdownstream chains

Long-term tax exemptions from operating time in free-trade zones, special economic areasand least developed regions Access to experts and professionals

Existence of developed infrastructures (airport, railway, port, jetty, etc.) in petrochemical hubs

Access to qualified engineering companies, suppliers and manufacturers

Iran’s Petrochemical ComplexesBased on the envisaged plans for iranian calander year 2016

Total number: 55

Region No. Capacity (million/tons per year)

Mahshahr 21 25.8Assaluyeh 15 26.9Other regions 19 11.4Total output capacity 64.1 million/tons per year

Including Bandar Imam 3rd NF 66.8 million/tons per yearTotal NO. of Mahshahr & Assaluyeh Complexes include Fajr & Mobin Petrochemical Companies.

Petrochemical complexes

Petrochemical projects

Projects enroute theethylene pipeline

6th development plan:private sector

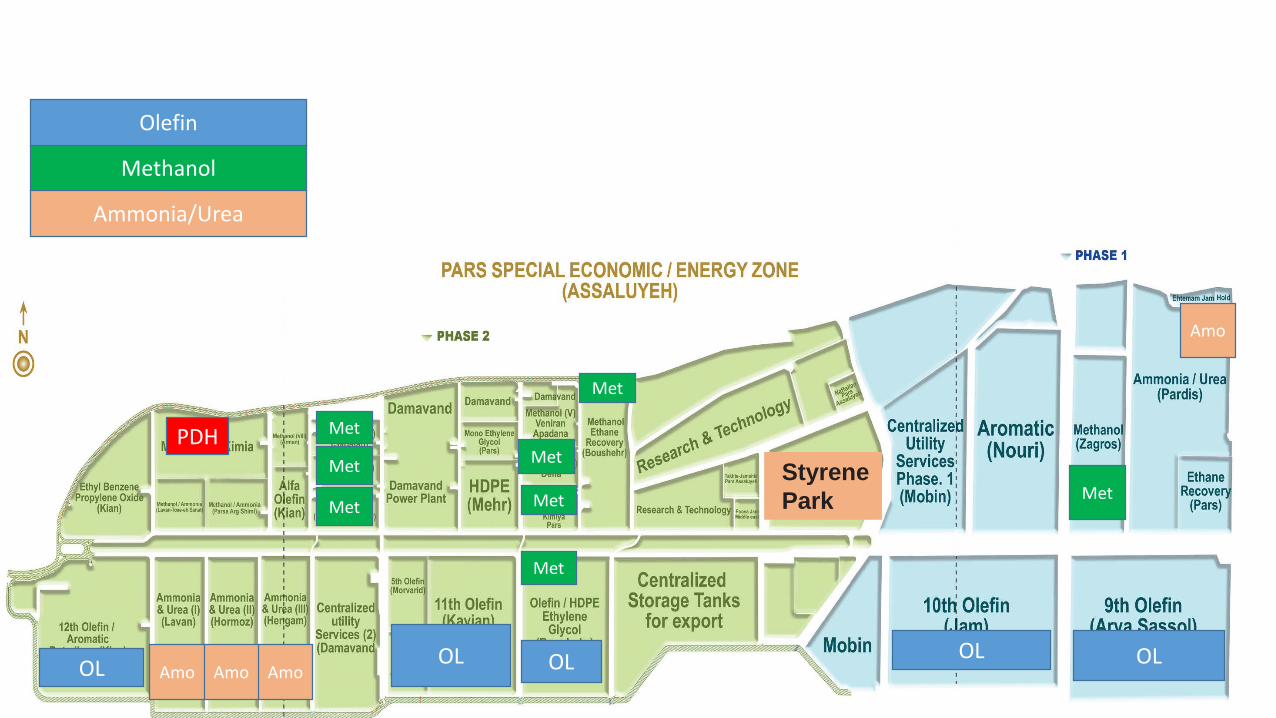

Special Economic Zone

Future petrochemical Hubs

Parsian QeshmJaskMahshahr development Assaluyeh development

Iran is ready to develop the petrochemical industryMahshahrAssaluyeh

Other areasWest Ethylene Pipeline

Central Ethylene Pipeline

The ongoing projectsComplexes under operation The future hub for the petrochemical industryChabahar

160

230

0

50

100

150

200

250

2015 2025

World

7/8

14

0

2

4

6

8

10

12

14

16

2015 2025

Iran

Ethylene production (capacity)2015-2025

44%

80%

1/1

5/8

0

1

2

3

4

5

6

7

2015 2025

Iran

114

170

0

20

40

60

80

100

120

140

160

180

2015 2025

World

Propylene production (capacity)2015-2025

49%* 4/3

5

23

0

5

10

15

20

25

2015 2025

Iran

110

167

0

20

40

60

80

100

120

140

160

180

2015 2025

World

52%

Methanol production (capacity)2015-2025

*4/6

2/3

4/9

0

1

2

3

4

5

6

2015 2025

Iran

44

70

0

10

20

30

40

50

60

70

80

2015 2025

World

59%

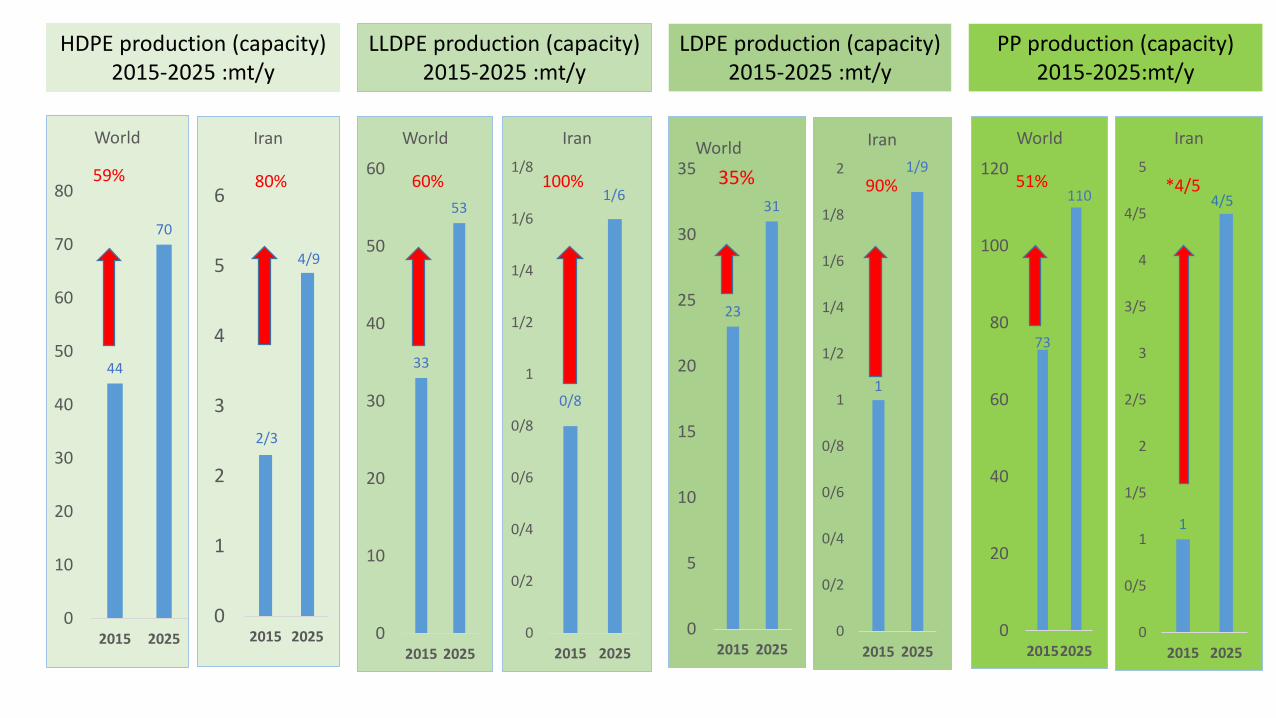

HDPE production (capacity)2015-2025 :mt/y

LLDPE production (capacity)2015-2025 :mt/y

LDPE production (capacity)2015-2025 :mt/y

PP production (capacity)2015-2025:mt/y

0/8

1/6

0

0/2

0/4

0/6

0/8

1

1/2

1/4

1/6

1/8

2015 2025

Iran

33

53

0

10

20

30

40

50

60

2015 2025

World

1

1/9

0

0/2

0/4

0/6

0/8

1

1/2

1/4

1/6

1/8

2

2015 2025

Iran

23

31

0

5

10

15

20

25

30

35

2015 2025

World

35%

1

4/5

0

0/5

1

1/5

2

2/5

3

3/5

4

4/5

5

2015 2025

Iran

*4/5

73

110

0

20

40

60

80

100

120

20152025

World

80% 60% 100% 90% 51%

OLOLOLOLOL

Amo

AmoAmoAmo

Met

Met

Met

Met

Met

Met

Met

Methanol

Olefin

Ammonia/Urea

StyrenePark

Met

PDH

Met

Amo

ol

ol

ol

ol

Pvc

Pvc

Pvc

AmoMet

PDH

Pvc

AcrylonitrileAcrylates

Maleic Anhydride

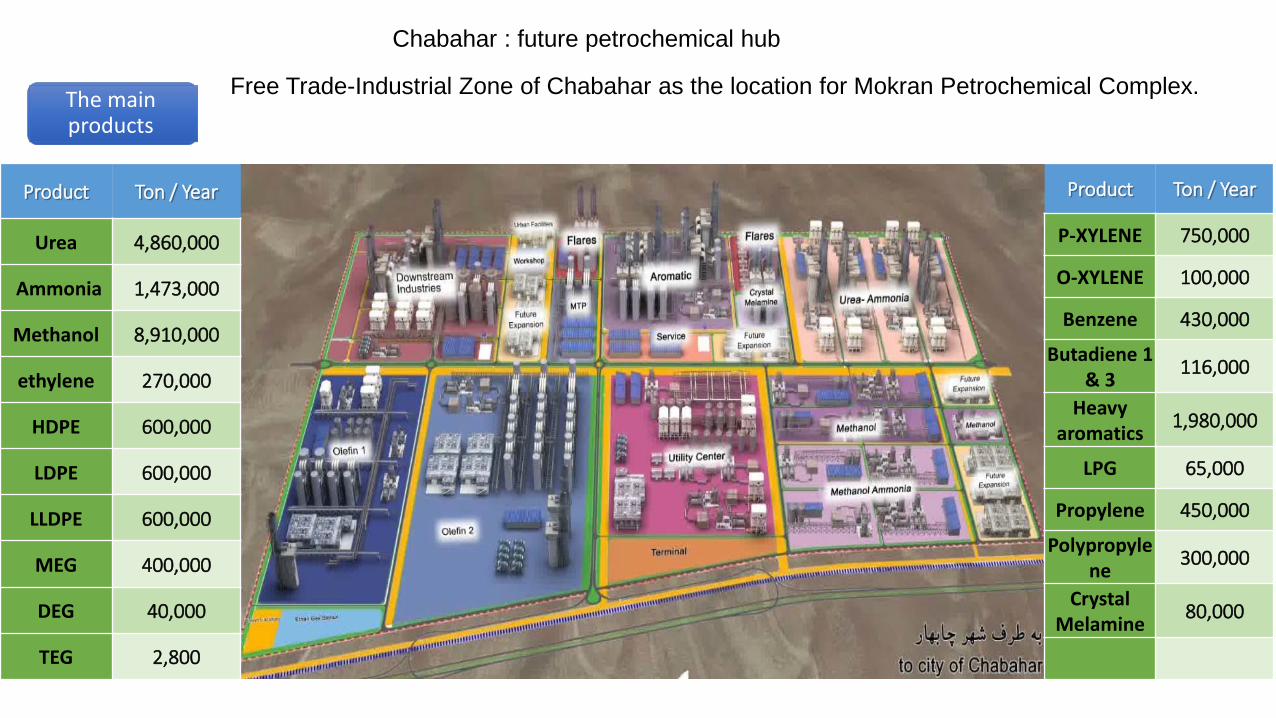

Product Ton / Year

Urea 4,860,000

Ammonia 1,473,000

Methanol 8,910,000

ethylene 270,000

HDPE 600,000

LDPE 600,000

LLDPE 600,000

MEG 400,000

DEG 40,000

TEG 2,800

Product Ton / Year

P-XYLENE 750,000

O-XYLENE 100,000

Benzene 430,000

Butadiene 1 & 3 116,000

Heavy aromatics 1,980,000

LPG 65,000

Propylene 450,000

Polypropylene 300,000

Crystal Melamine 80,000

The main products

Chabahar : future petrochemical hub

Free Trade-Industrial Zone of Chabahar as the location for Mokran Petrochemical Complex.

1. Chabahar, The southernmost city of Iran: Free Trade & Industrial Zone situated in on the Coast of Oman Sea

out of Persian Gulf region.

2. Strategically being located in the cross section of the North and South International Corridors.

3. only port with direct access to Indian Ocean and Oman Sea where the location well qualifies it for Industrial

Development, Trade and Transit of Goods.

.

The Advantages of Petrochemical Hub Establishment in CFZ

Marun petrochemical company was established in 1999

first designed Iranian plants in which C2+ (mainly ethane) is separated from natural gas, and reformed to olefin products and then to polymeric and chemical products

1- Ahwaz: Ethane recovery unit 2- Mahshar: Petrochemical Special Economic Zone Olefin Plant

1

95 km pipe line

1

5

3

100%Marun petrochemical complex

64%Laleh Petrochemical Company

40%Bushehr Petrochemical Complex

34%Salman Farsi Petrochemical

7%Ilam Petrochemical Complex

100Marun supplementary industry

264

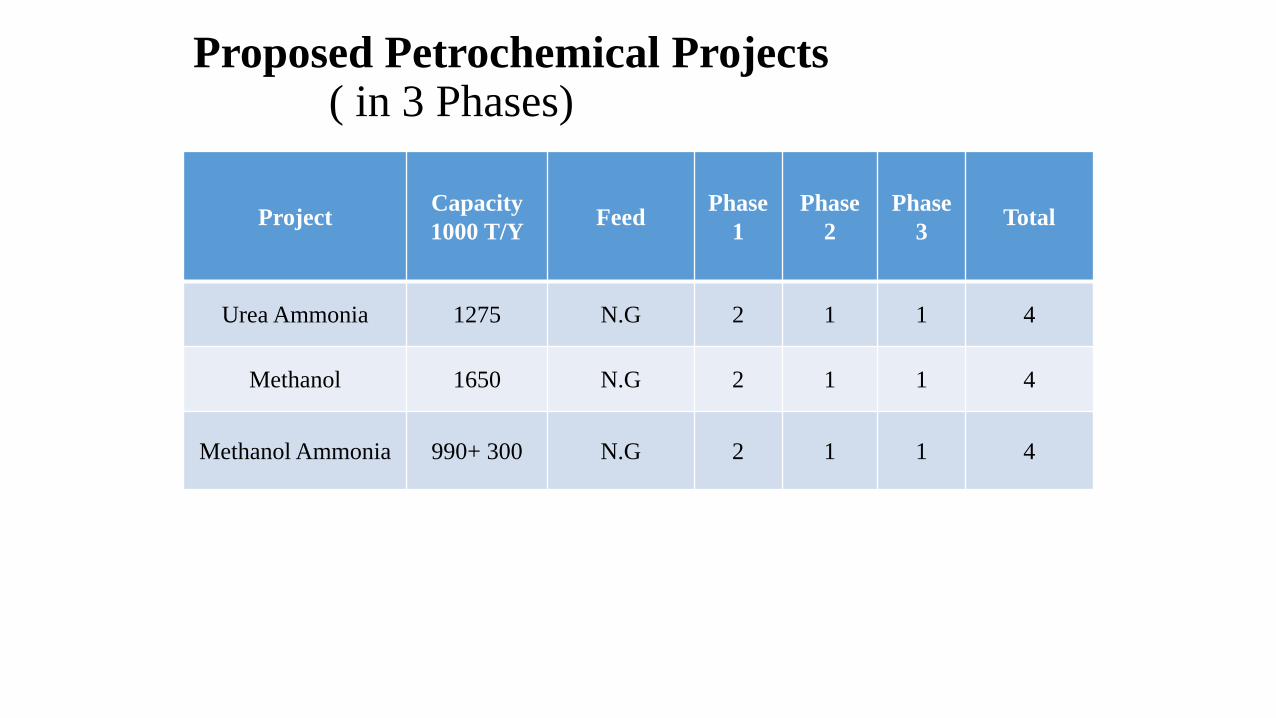

Proposed Petrochemical Projects( in 3 Phases)

Project Capacity1000 T/Y Feed Phase

1Phase

2Phase

3 Total

Urea Ammonia 1275 N.G 2 1 1 4

Methanol 1650 N.G 2 1 1 4

Methanol Ammonia 990+ 300 N.G 2 1 1 4

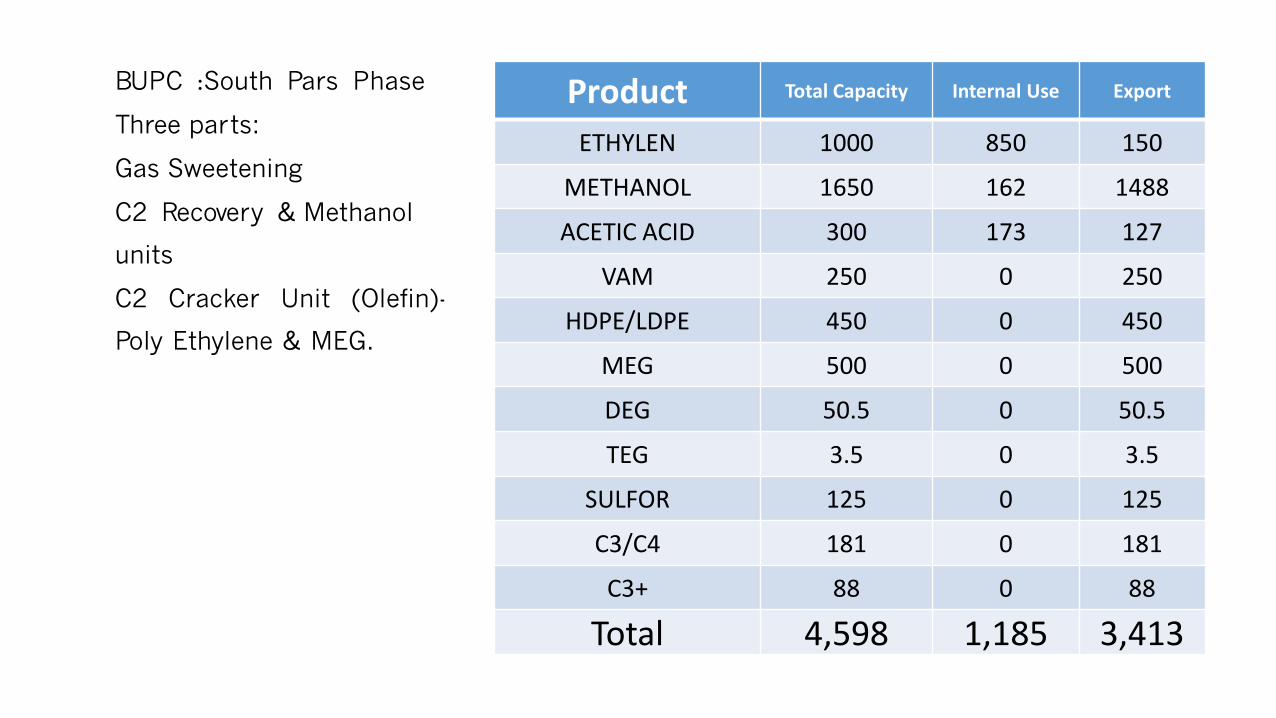

BUPC :South Pars Phase

Three parts:

Gas Sweetening

C2 Recovery & Methanol

units

C2 Cracker Unit (Olefin)-

Poly Ethylene & MEG.

Product Total Capacity Internal Use Export

ETHYLEN 1000 850 150

METHANOL 1650 162 1488

ACETIC ACID 300 173 127

VAM 250 0 250

HDPE/LDPE 450 0 450

MEG 500 0 500

DEG 50.5 0 50.5

TEG 3.5 0 3.5

SULFOR 125 0 125

C3/C4 181 0 181

C3+ 88 0 88

Total 4,598 1,185 3,413

Products - Holding of Marun

Product MPC BUPC ILAM LPC SFPCETHYLEN 1100 1000 460

PROPYLENE 200 127 450

PP 300

METHANOL 1650

ACETIC ACID 300

VAM 250

PE 300 450 300 300

MEG 400 500

DEG 40 50.5

TEG 3 3.5

SULFOR 125

C3/C4 181 33

C3+ 160 88

PG 90 134

% ShareCompany NameRow

100%Marun petrochemical complex

MPC

1

64%Laleh Petrochemical Company

LPC

2

40%Bushehr Petrochemical Complex

BUPC

3

34%Salman Farsi Petrochemical Company

SFPC

4

7%Ilam Petrochemical Complex5

Total production of marun &sharholder(Ilam,Laleh)= 2,162,500 T/Y

Total production of marun &sharholder(BUPC,Salman,Ilam,Laleh,Mppc)= 3,689,050 T/Y

Total production of marun &sharholder (BUPC , Salman , Ilam , Laleh , Mppc &" INTEGRATION-PETROCHEMICAL HUB: 5,000,000 T/Y" )= 8,689,050 T/Y

2021

2022

2016