Implementation Completion and Results Report...

61

Document of The World Bank FOR OFFICIAL USE ONLY Report No: ICR00004662 IMPLEMENTATION COMPLETION AND RESULTS REPORT 7816-IN ON A LOAN IN THE AMOUNT OF US$ 300 MILLION EQUIVALENT (INR 20,673 MILLION EQUIVALENT) TO THE Republic of India FOR THE ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT June 20, 2019 Social, Urban, Rural And Resilience Global Practice South Asia Region Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Implementation Completion and Results Report...

Document of

The World Bank FOR OFFICIAL USE ONLY

Report No: ICR00004662

IMPLEMENTATION COMPLETION AND RESULTS REPORT

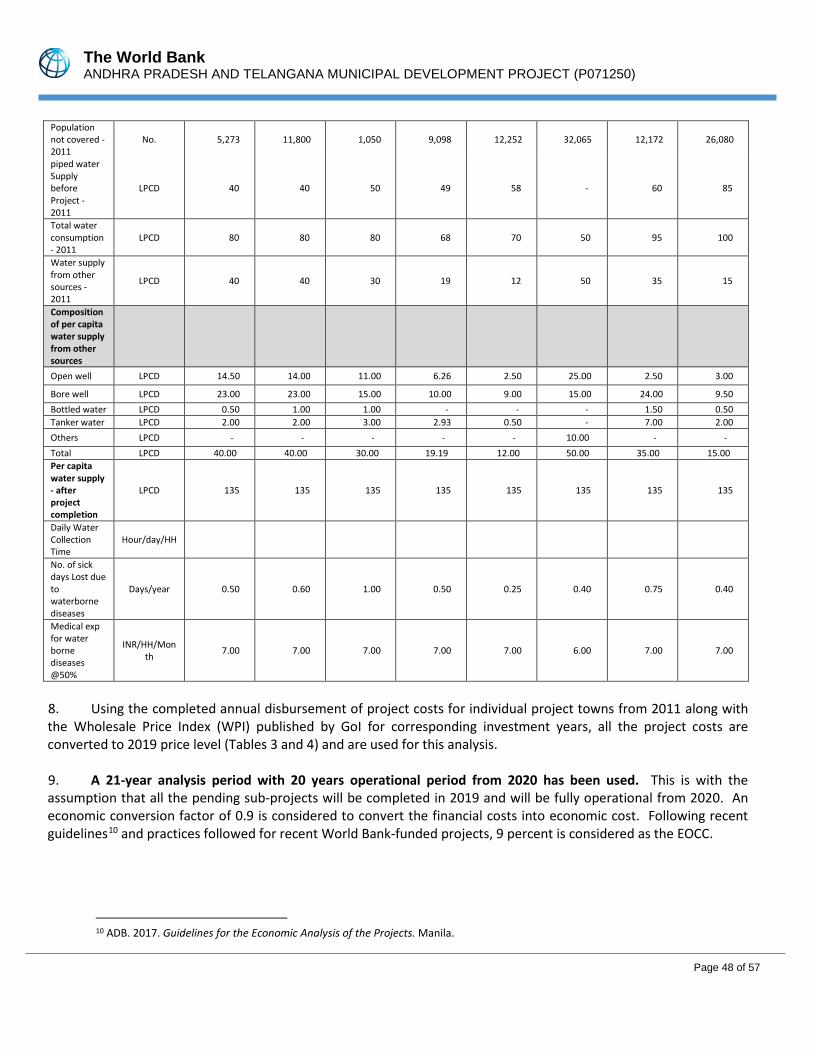

7816-IN

ON A

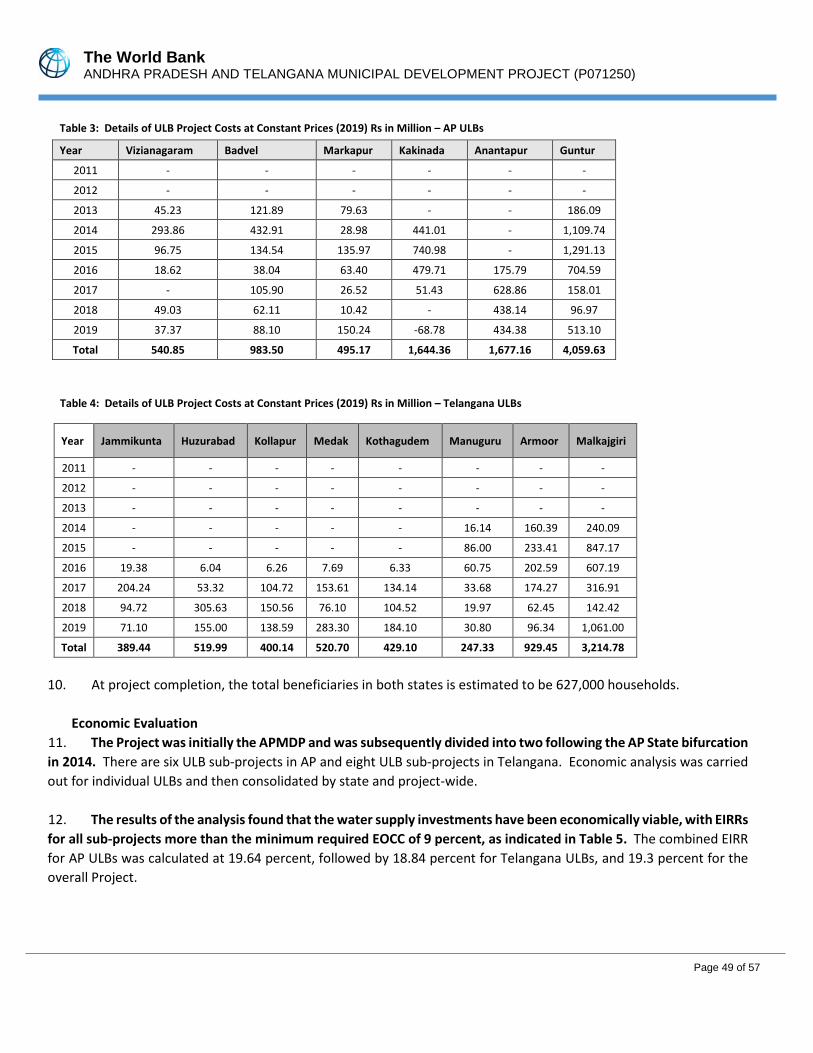

LOAN

IN THE AMOUNT OF US$ 300 MILLION EQUIVALENT

(INR 20,673 MILLION EQUIVALENT)

TO THE

Republic of India

FOR THE

ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT

June 20, 2019

Social, Urban, Rural And Resilience Global Practice South Asia Region

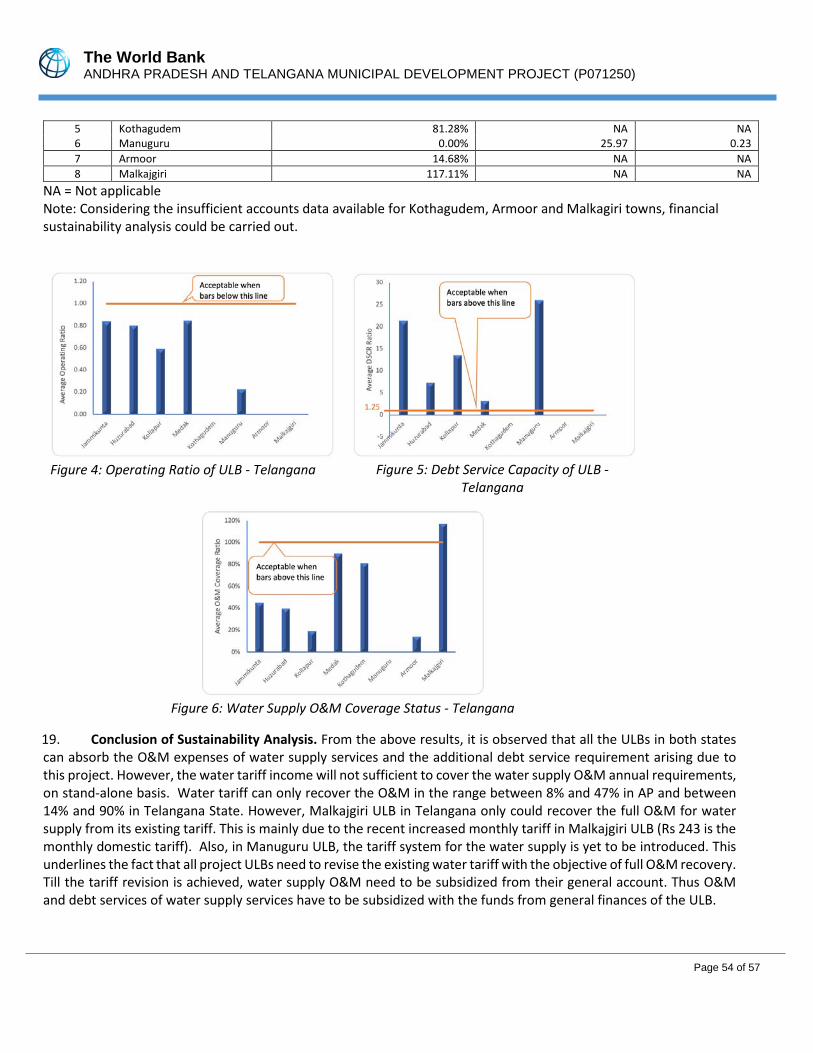

Pub

lic D

iscl

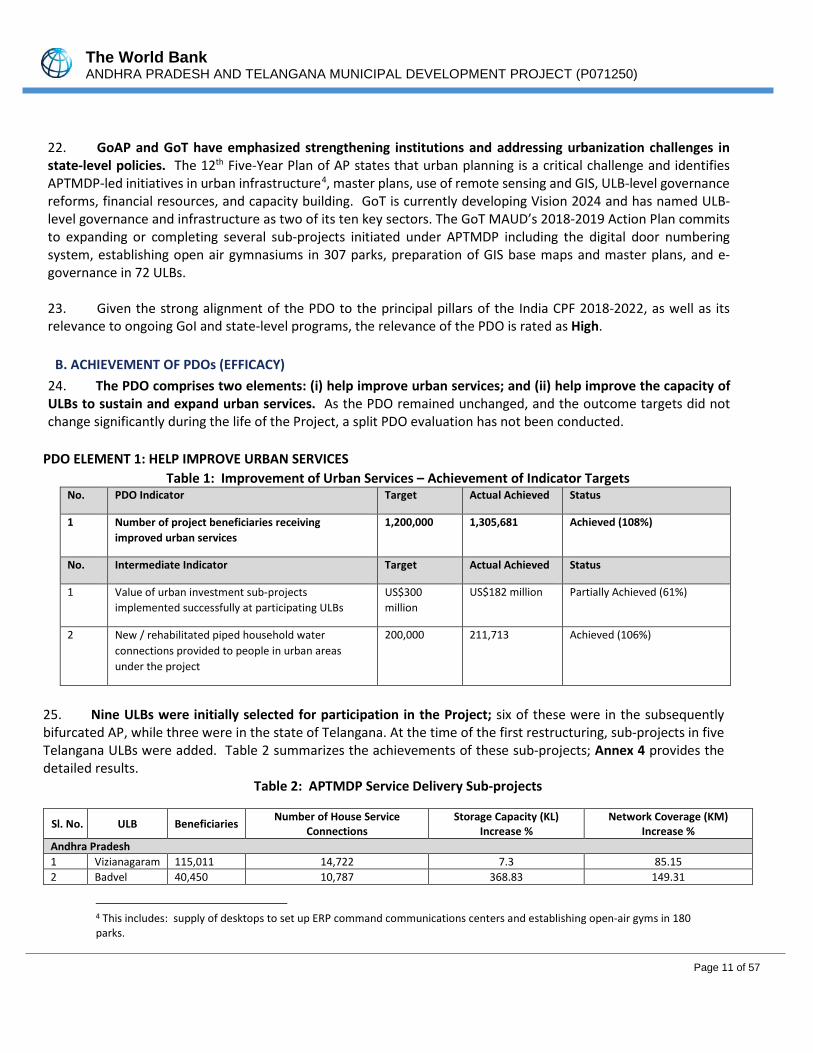

osur

e A

utho

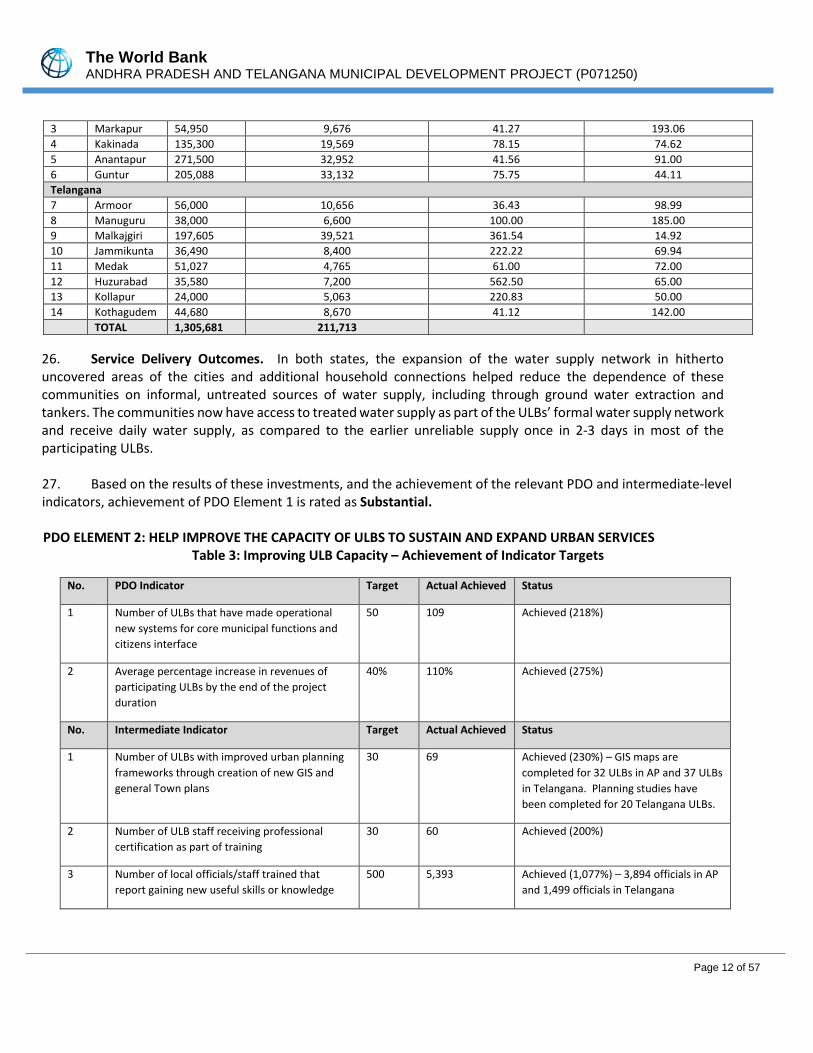

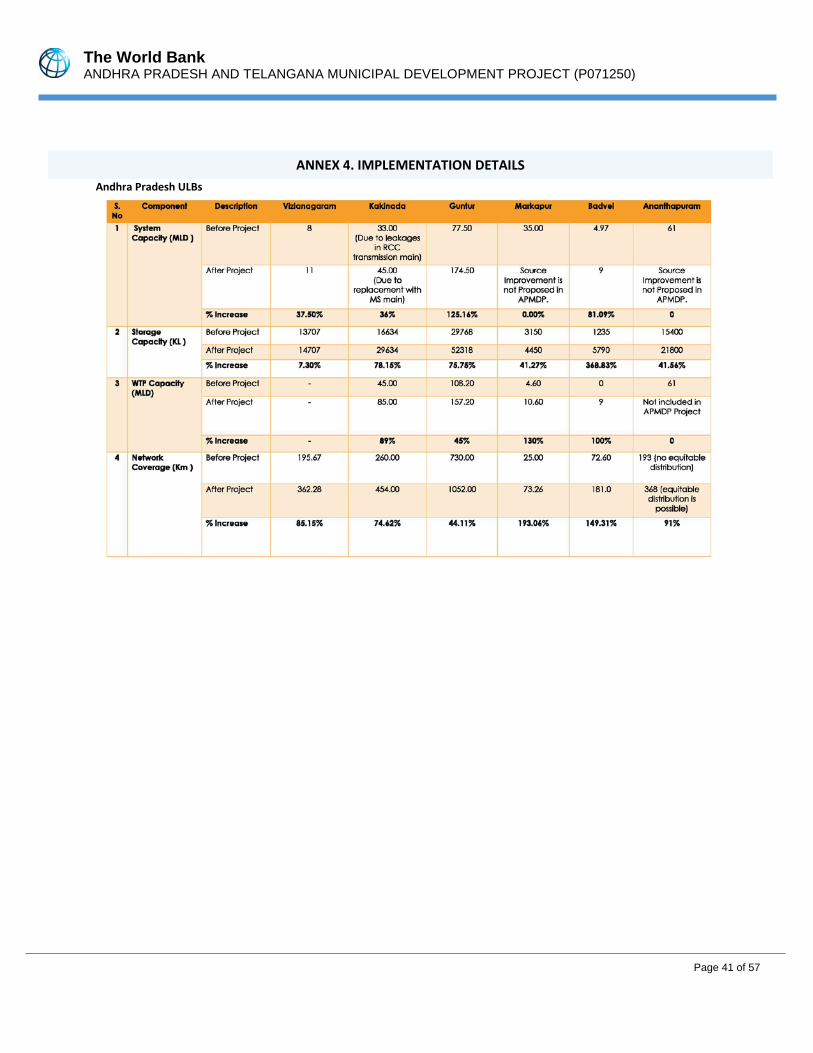

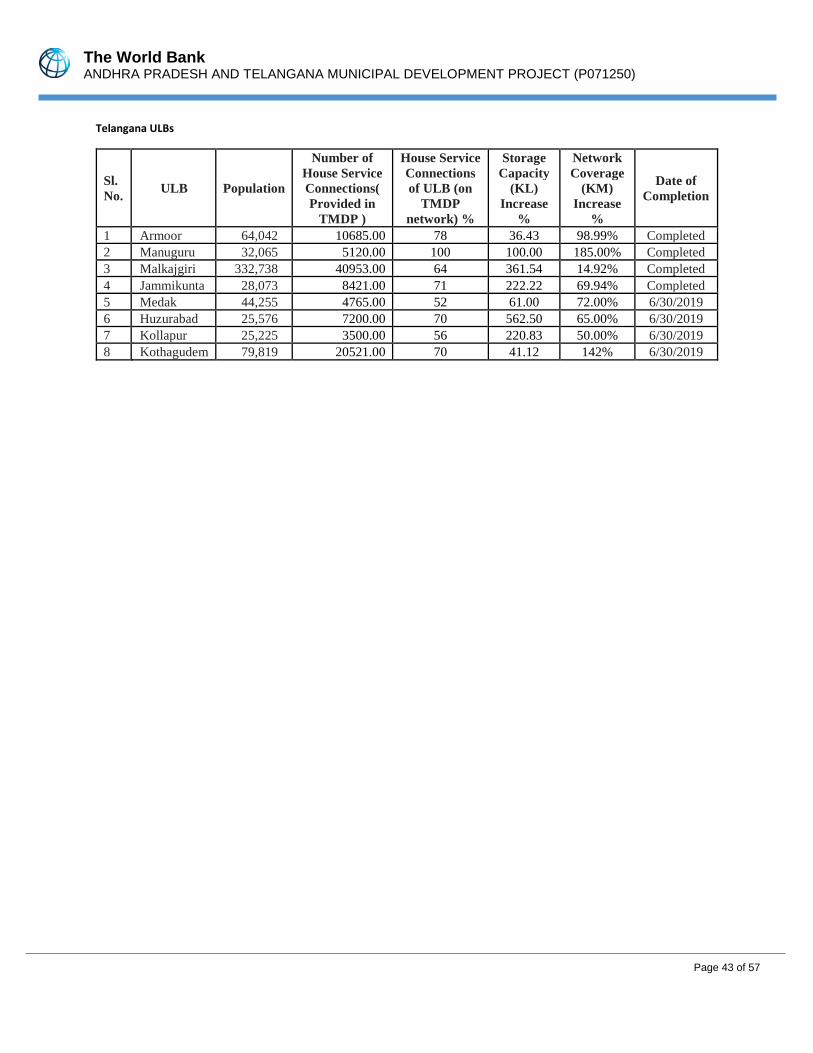

rized

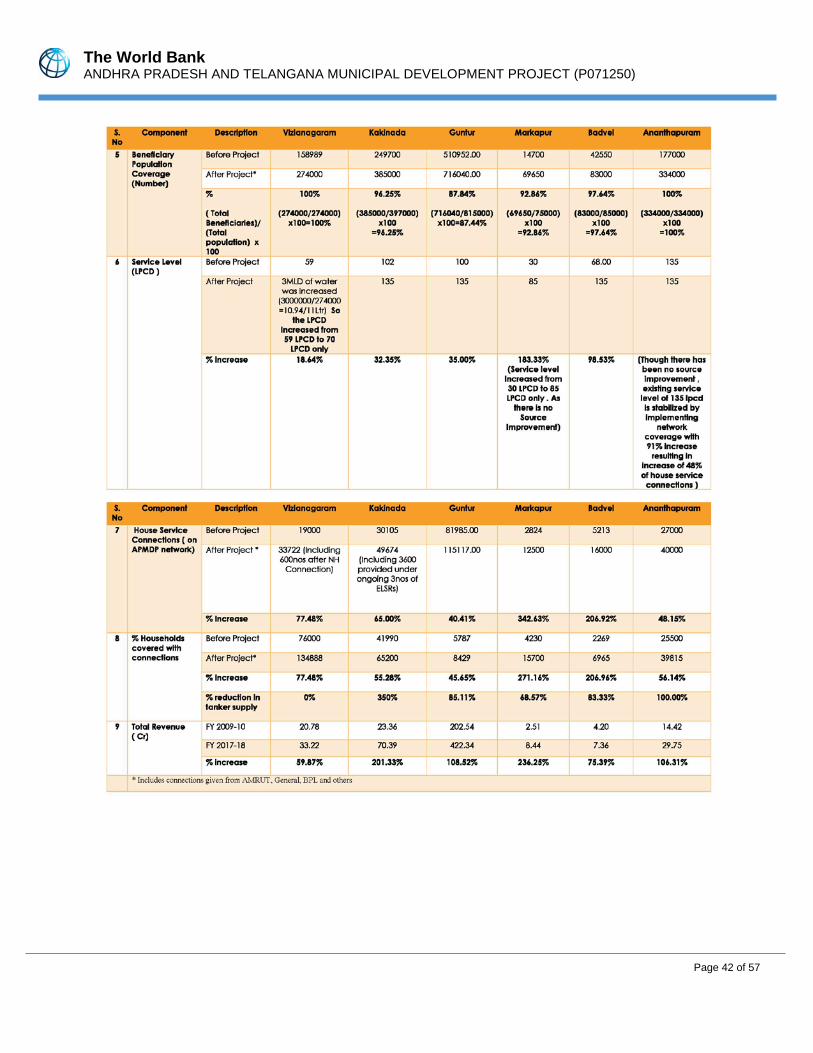

Pub

lic D

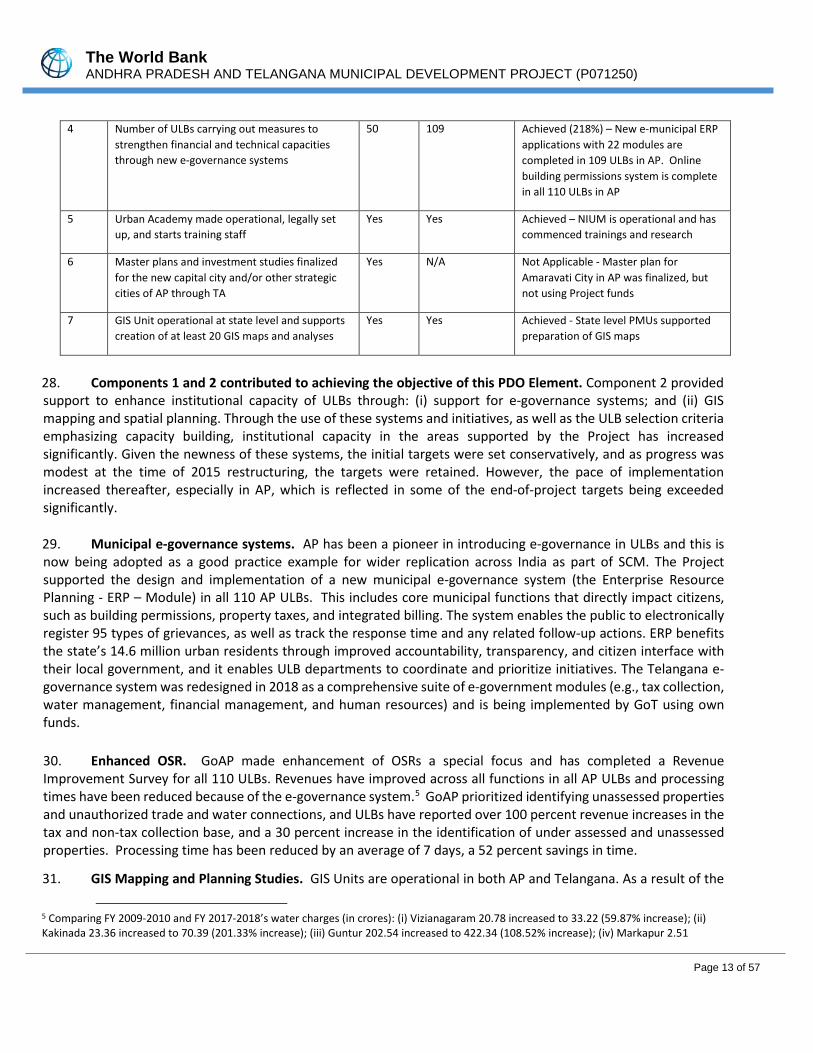

iscl

osur

e A

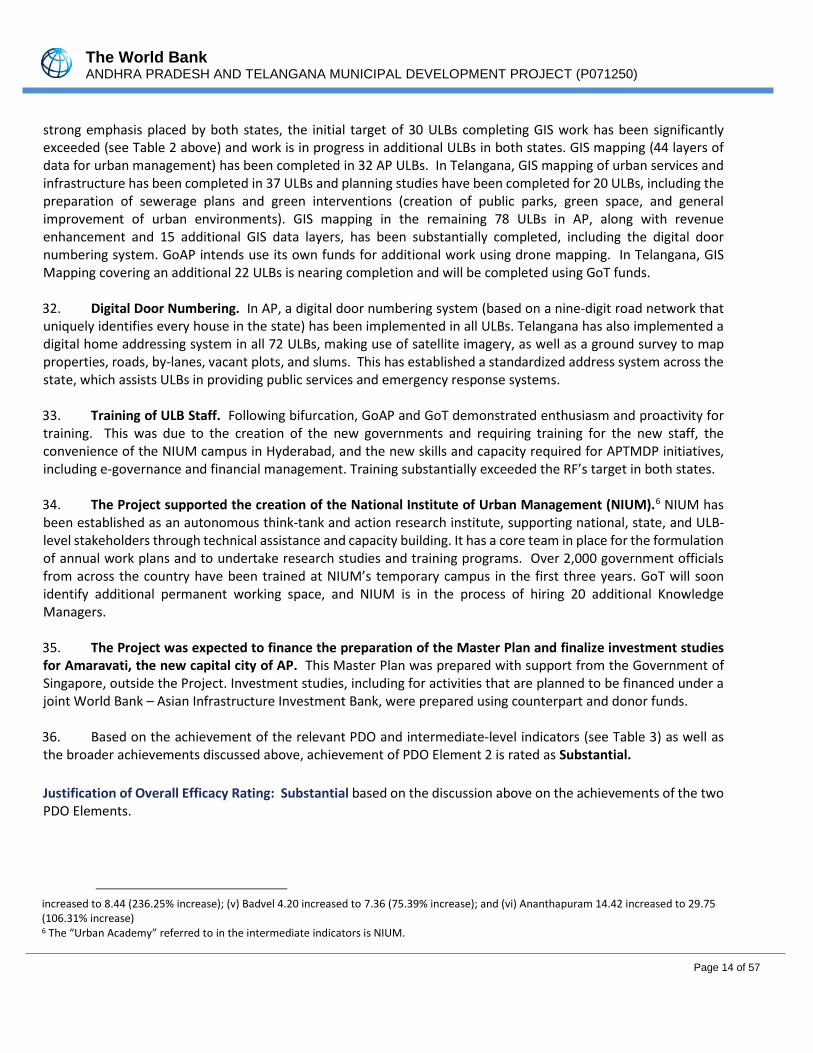

utho

rized

Pub

lic D

iscl

osur

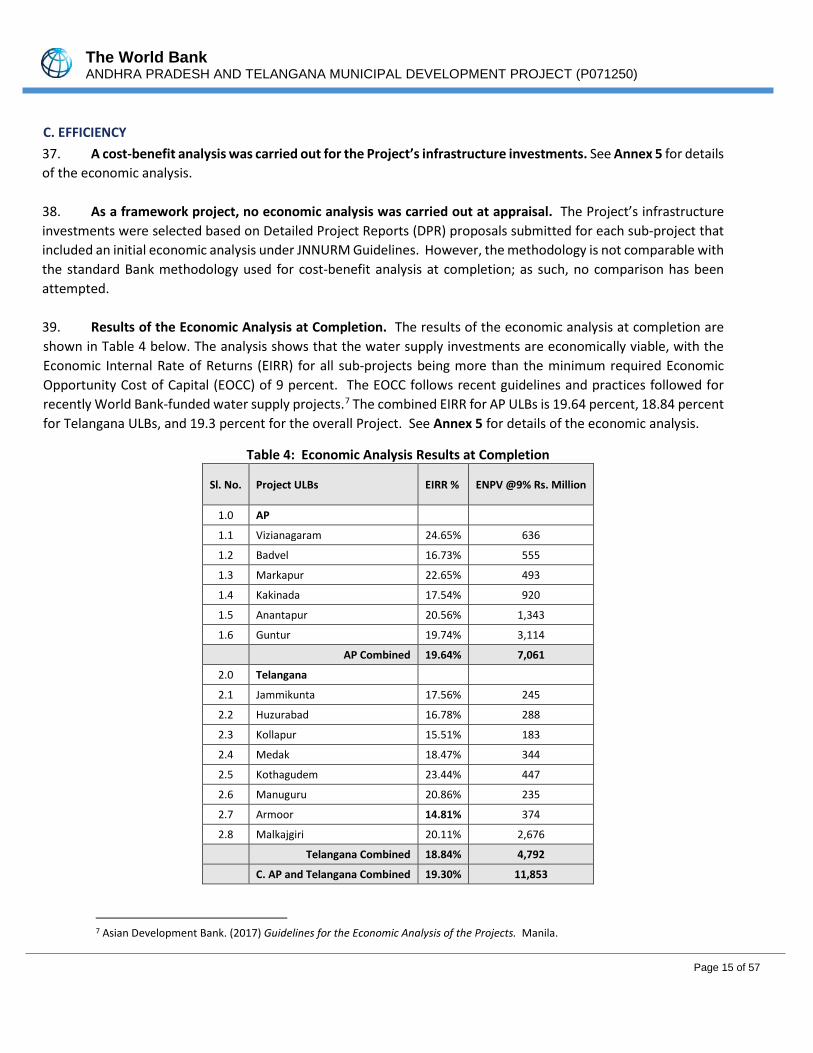

e A

utho

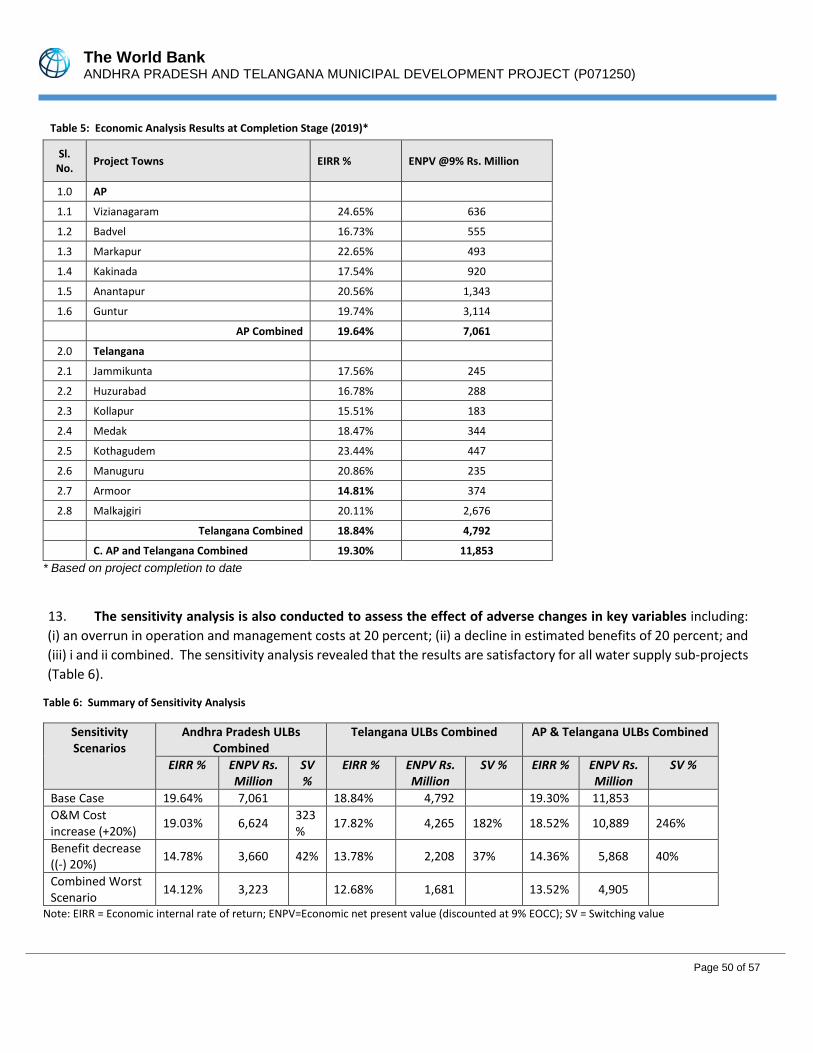

rized

Pub

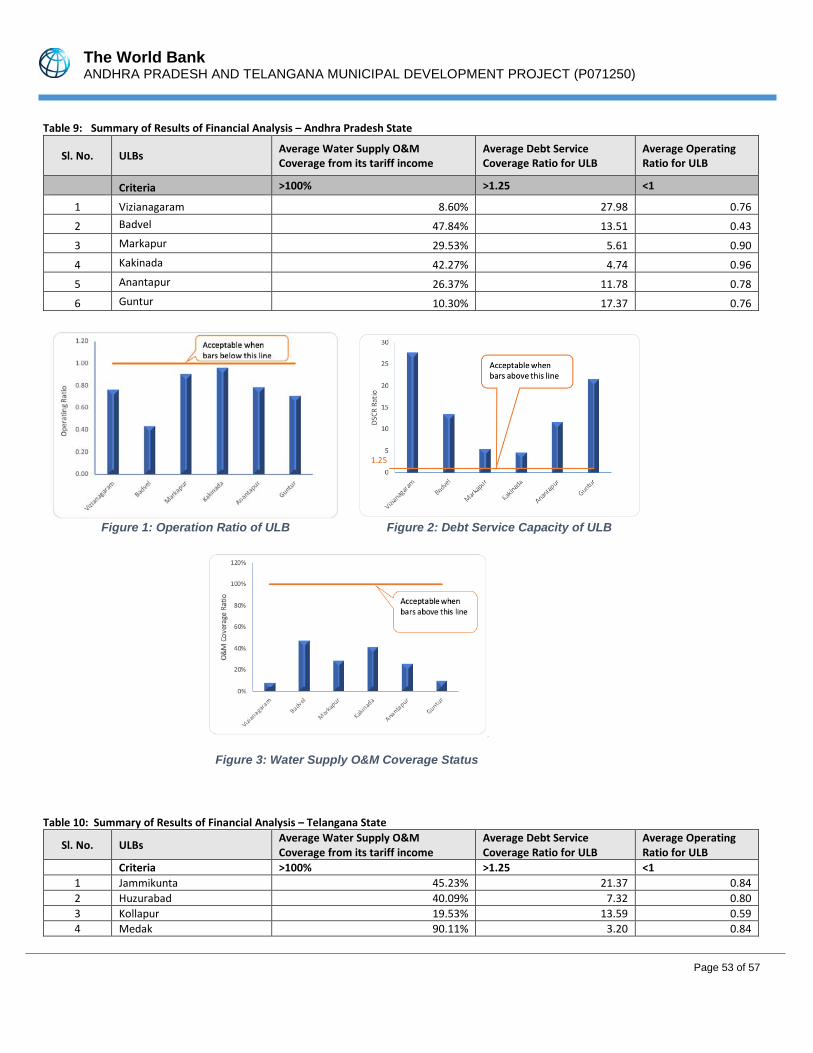

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective May 31, 2019)

Currency Unit = Indian Rupee (INR)

INR70 = US$1

US$1 = INR0.15

FISCAL YEAR

July 1 - June 30

Regional Vice President: Hartwig Schafer

Country Director: Junaid Kamal Ahmad

Senior Global Practice Director: Ede Jorge Ijjasz-Vasquez

Practice Manager: Catalina Marulanda

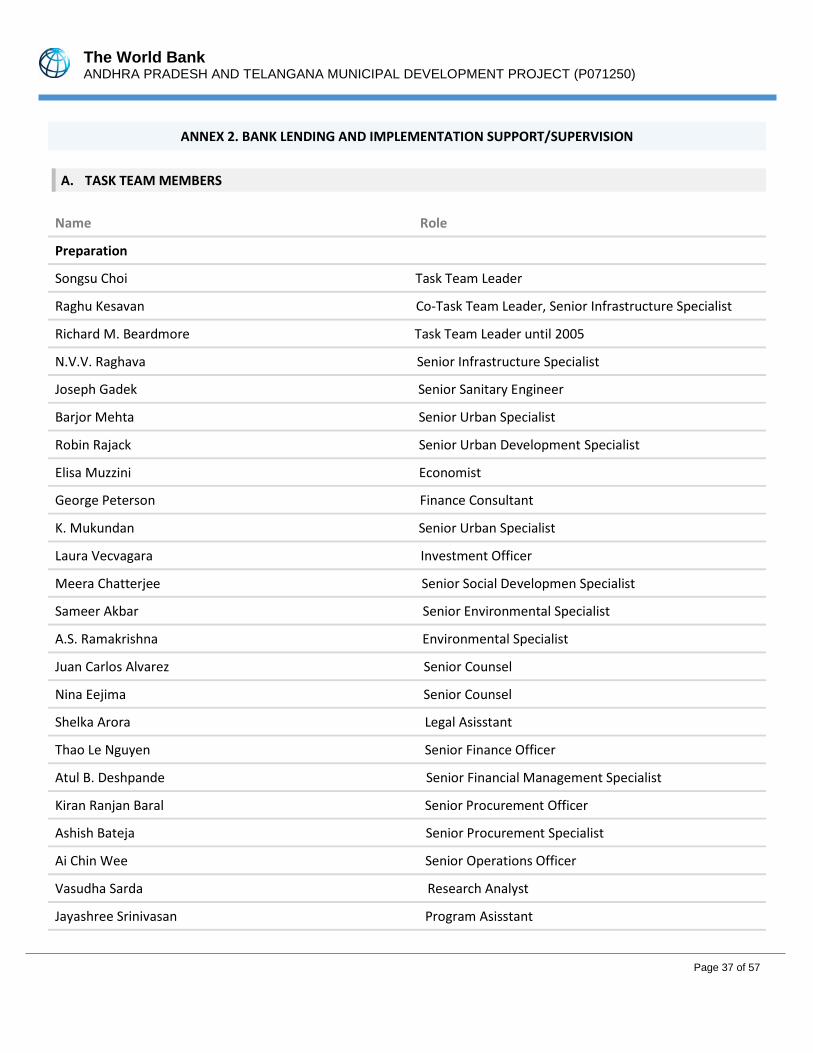

Task Team Leader: Raghu Kesavan

ICR Main Contributor: Jessica Schmidt

ABBREVIATIONS AND ACRONYMS AMRUT Atal Mission for Rejuvenation and Urban Transformation AP Andhra Pradesh APMDP Andhra Pradesh Municipal Development Project APTMDP Andhra Pradesh Telangana Municipal Development Project APUFIDC Andhra Pradesh Urban Finance and Infrastructure Development Corporation CAS Country Assistance Strategy CBA Cost Benefit Analysis CDMA Commissioner and Director of Municipal Administration CMU Country Management Unit CPF Country Partnership Framework CPS Country Partnership Strategy DEA Department of Economic Affairs DFID Development for International Development DPR Detailed Project Report EIRR Economic Internal Rate of Return EOCC Economic Opportunity Cost of Capital ERP Enterprise Resource Planning GIS Geographical Information System GOAP Government of Andhra Pradesh GOI Government of India GOT Government of Telangana ISR Implementation Status Report LPCD Liters per Capita per Day MAUD Municipal Administration and Urban Department M&E Monitoring and Evaluation MOU Memorandum of Understanding MRAP Municipal Reform Action Plan MSU Municipal Strengthening Unit MULB Manual for Urban Local Bodies NIUM National Institute of Urban Management O&M Operations and Maintenance OSR Own Source Revenue PA Project Agreement PDO Project Development Objective PMU Project Management Unit PMM Project Managers Manual RF Results Framework SEAMF Social and Environmental Assessment and Management Framework SCD Systematic Country Diagnostic SCM Smart Cities Mission TUFIDC Telangana Urban Finance and Infrastructure Development Corporation ULB Urban Local Body WTP Willingness to Pay WPI Wholesale Price Index

TABLE OF CONTENTS

DATA SHEET .......................................................................................................................... 1

I. PROJECT CONTEXT AND DEVELOPMENT OBJECTIVES ....................................................... 6

A. CONTEXT AT APPRAISAL .........................................................................................................6

B. SIGNIFICANT CHANGES DURING IMPLEMENTATION (IF APPLICABLE) .......................................9

II. OUTCOME .................................................................................................................... 10

A. RELEVANCE OF PDOs ............................................................................................................ 10

B. ACHIEVEMENT OF PDOs (EFFICACY) ...................................................................................... 11

C. EFFICIENCY ........................................................................................................................... 15

D. JUSTIFICATION OF OVERALL OUTCOME RATING .................................................................... 17

E. OTHER OUTCOMES AND IMPACTS (IF ANY) ............................................................................ 17

III. KEY FACTORS THAT AFFECTED IMPLEMENTATION AND OUTCOME ................................ 18

A. KEY FACTORS DURING PREPARATION ................................................................................... 18

B. KEY FACTORS DURING IMPLEMENTATION ............................................................................. 18

IV. BANK PERFORMANCE, COMPLIANCE ISSUES, AND RISK TO DEVELOPMENT OUTCOME .. 19

A. QUALITY OF MONITORING AND EVALUATION (M&E) ............................................................ 20

B. ENVIRONMENTAL, SOCIAL, AND FIDUCIARY COMPLIANCE ..................................................... 21

C. BANK PERFORMANCE ........................................................................................................... 23

D. RISK TO DEVELOPMENT OUTCOME ....................................................................................... 24

V. LESSONS AND RECOMMENDATIONS ............................................................................. 25

ANNEX 1. RESULTS FRAMEWORK AND KEY OUTPUTS ........................................................... 26

ANNEX 2. BANK LENDING AND IMPLEMENTATION SUPPORT/SUPERVISION ......................... 37

ANNEX 3. PROJECT COST BY COMPONENT ........................................................................... 40

ANNEX 4. IMPLEMENTATION DETAILS .................................................................................. 41

ANNEX 5. EFFICIENCY ANALYSIS ........................................................................................... 44

ANNEX 6. IMPACT EVALUATION OF LAND ACQUISITION AND RESETTLEMENT ...................... 55

ANNEX 7. BORROWERS’ COMMENTS ................................................................................... 56

ANNEX 8. MAP .................................................................................................................... 56

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 1 of 57

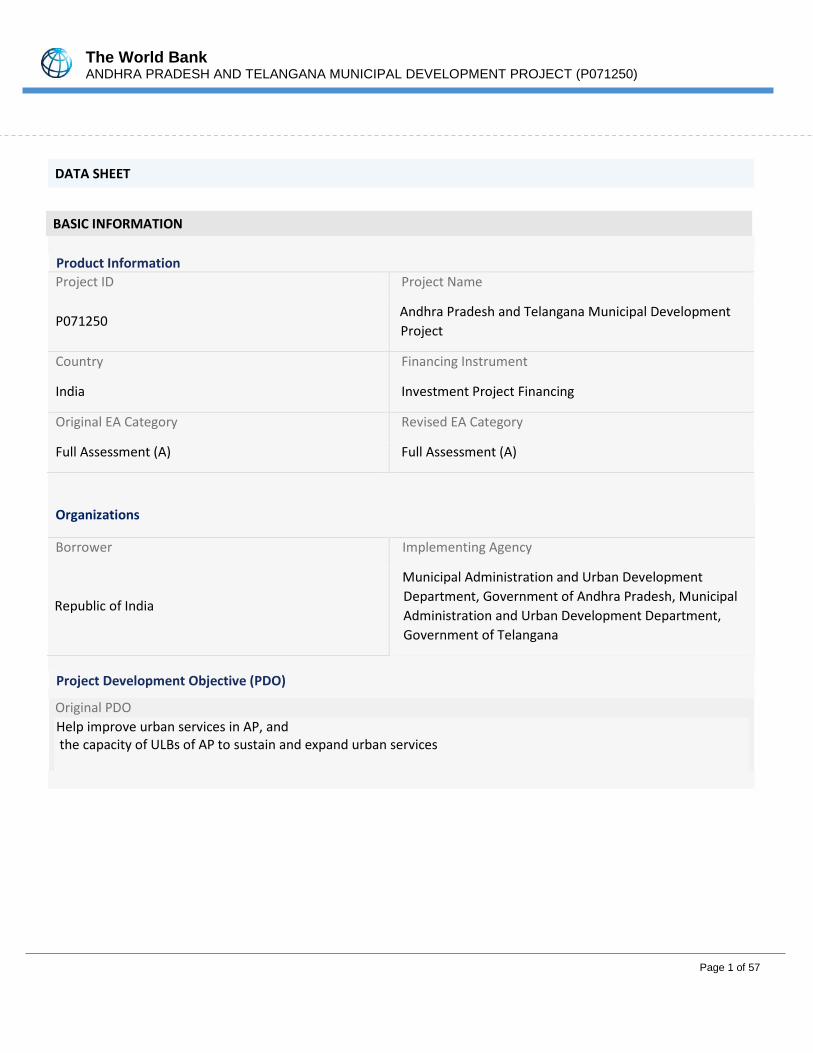

DATA SHEET

BASIC INFORMATION Product Information Project ID Project Name

P071250 Andhra Pradesh and Telangana Municipal Development Project

Country Financing Instrument

India Investment Project Financing

Original EA Category Revised EA Category

Full Assessment (A) Full Assessment (A)

Organizations

Borrower Implementing Agency

Republic of India

Municipal Administration and Urban Development Department, Government of Andhra Pradesh, Municipal Administration and Urban Development Department, Government of Telangana

Project Development Objective (PDO)

Original PDO Help improve urban services in AP, and the capacity of ULBs of AP to sustain and expand urban services

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 2 of 57

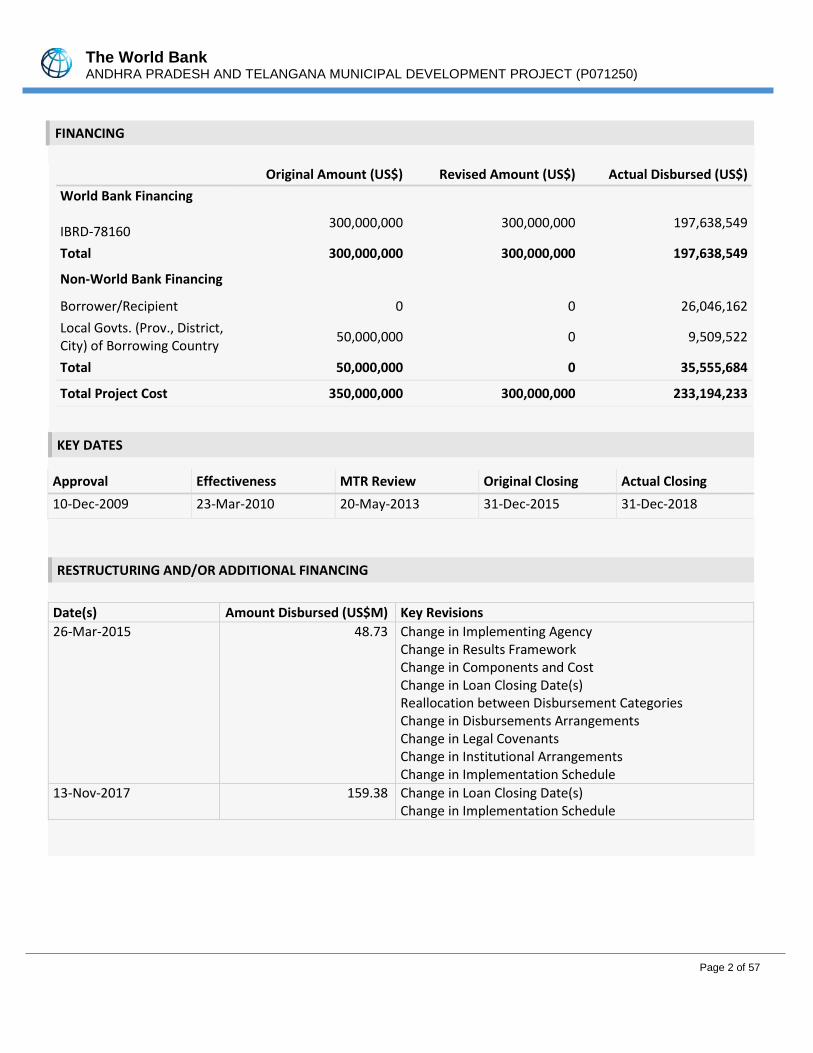

FINANCING

Original Amount (US$) Revised Amount (US$) Actual Disbursed (US$) World Bank Financing IBRD-78160 300,000,000 300,000,000 197,638,549

Total 300,000,000 300,000,000 197,638,549

Non-World Bank Financing 0 0 0

Borrower/Recipient 0 0 26,046,162 Local Govts. (Prov., District, City) of Borrowing Country 50,000,000 0 9,509,522

Total 50,000,000 0 35,555,684

Total Project Cost 350,000,000 300,000,000 233,194,233

KEY DATES

Approval Effectiveness MTR Review Original Closing Actual Closing 10-Dec-2009 23-Mar-2010 20-May-2013 31-Dec-2015 31-Dec-2018

RESTRUCTURING AND/OR ADDITIONAL FINANCING

Date(s) Amount Disbursed (US$M) Key Revisions 26-Mar-2015 48.73 Change in Implementing Agency

Change in Results Framework Change in Components and Cost Change in Loan Closing Date(s) Reallocation between Disbursement Categories Change in Disbursements Arrangements Change in Legal Covenants Change in Institutional Arrangements Change in Implementation Schedule

13-Nov-2017 159.38 Change in Loan Closing Date(s) Change in Implementation Schedule

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 3 of 57

KEY RATINGS

Outcome Bank Performance M&E Quality

Moderately Satisfactory Moderately Satisfactory Modest

RATINGS OF PROJECT PERFORMANCE IN ISRs

No. Date ISR Archived DO Rating IP Rating Actual

Disbursements (US$M)

01 17-May-2010 Satisfactory Satisfactory 20.00

02 12-Dec-2010 Satisfactory Satisfactory 20.18

03 27-Jun-2011 Satisfactory Satisfactory 21.48

04 14-Dec-2011 Satisfactory Satisfactory 22.06

05 31-May-2012 Satisfactory Satisfactory 22.77

06 22-Dec-2012 Satisfactory Moderately Satisfactory 23.01

07 13-Mar-2013 Moderately Satisfactory Moderately Unsatisfactory 23.38

08 27-Sep-2013 Moderately Satisfactory Moderately Unsatisfactory 38.15

09 10-Mar-2014 Moderately Satisfactory Moderately Unsatisfactory 41.01

10 15-Sep-2014 Moderately Satisfactory Moderately Unsatisfactory 48.73

11 25-Apr-2015 Moderately Satisfactory Moderately Unsatisfactory 51.65

12 23-Jun-2015 Moderately Satisfactory Moderately Unsatisfactory 65.66

13 30-Dec-2015 Moderately Satisfactory Moderately Unsatisfactory 90.61

14 05-May-2016 Moderately Satisfactory Moderately Satisfactory 115.68

15 11-Oct-2016 Moderately Satisfactory Moderately Satisfactory 122.10

16 07-Jun-2017 Moderately Satisfactory Moderately Satisfactory 152.58

17 03-Nov-2017 Moderately Satisfactory Moderately Satisfactory 158.51

18 27-Apr-2018 Moderately Satisfactory Moderately Unsatisfactory 171.87

19 03-Jan-2019 Moderately Satisfactory Moderately Unsatisfactory 185.11

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 4 of 57

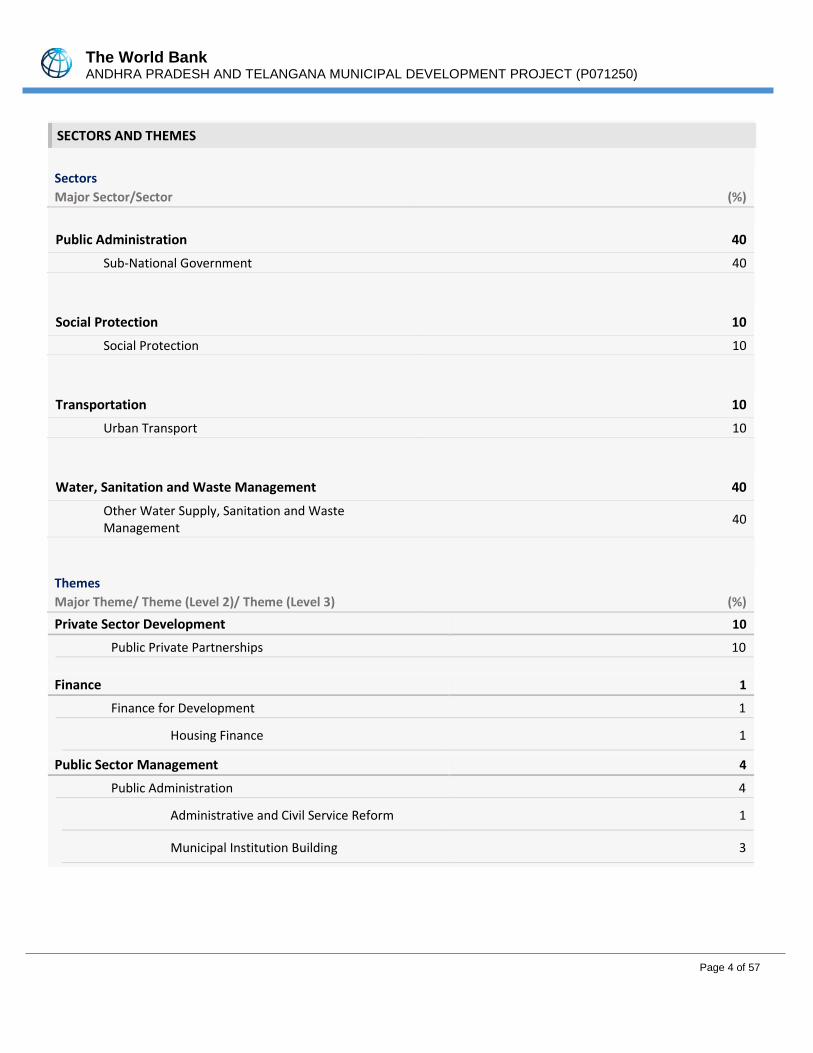

SECTORS AND THEMES

Sectors Major Sector/Sector (%)

Public Administration 40

Sub-National Government 40 Social Protection 10

Social Protection 10 Transportation 10

Urban Transport 10 Water, Sanitation and Waste Management 40

Other Water Supply, Sanitation and Waste Management 40

Themes Major Theme/ Theme (Level 2)/ Theme (Level 3) (%) Private Sector Development 10

Public Private Partnerships 10

Finance 1

Finance for Development 1 Housing Finance 1

Public Sector Management 4

Public Administration 4 Administrative and Civil Service Reform 1

Municipal Institution Building 3

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 5 of 57

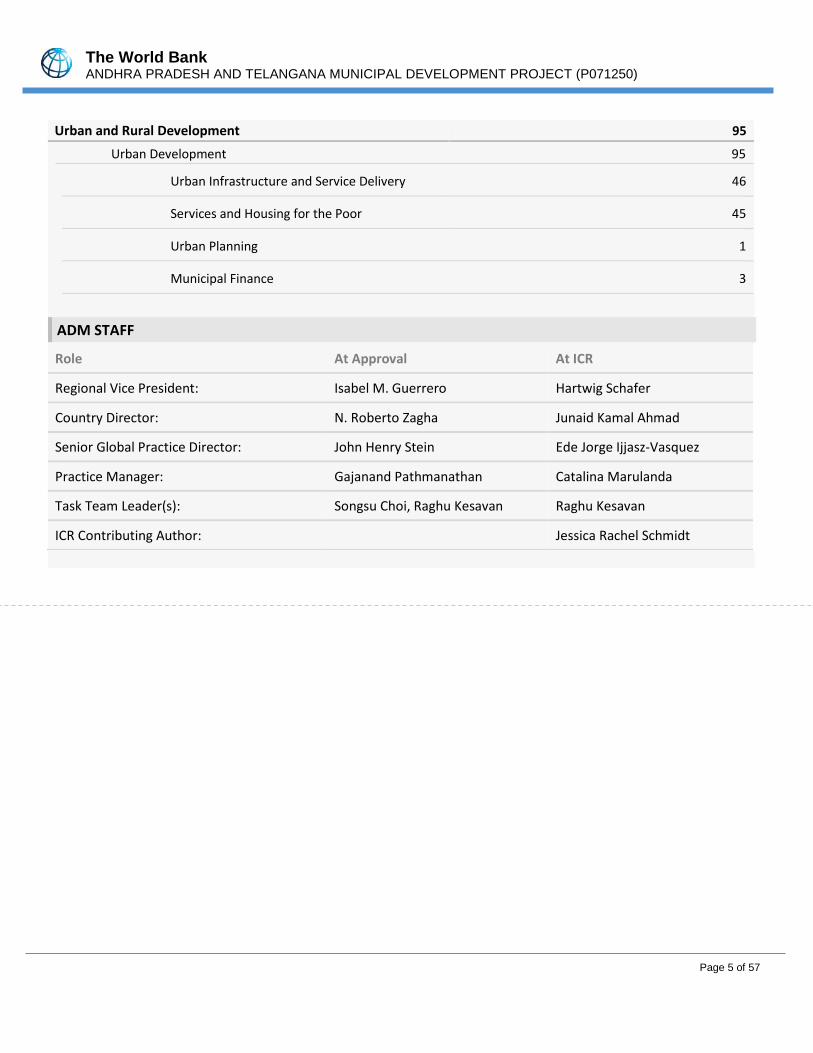

Urban and Rural Development 95 Urban Development 95

Urban Infrastructure and Service Delivery 46

Services and Housing for the Poor 45

Urban Planning 1

Municipal Finance 3

ADM STAFF

Role At Approval At ICR

Regional Vice President: Isabel M. Guerrero Hartwig Schafer

Country Director: N. Roberto Zagha Junaid Kamal Ahmad

Senior Global Practice Director: John Henry Stein Ede Jorge Ijjasz-Vasquez

Practice Manager: Gajanand Pathmanathan Catalina Marulanda

Task Team Leader(s): Songsu Choi, Raghu Kesavan Raghu Kesavan

ICR Contributing Author: Jessica Rachel Schmidt

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 6 of 57

I. PROJECT CONTEXT AND DEVELOPMENT OBJECTIVES

A. CONTEXT AT APPRAISAL 1. India was on a high economic growth trajectory at appraisal, following two decades of economic reforms, but many cities continued to struggle with service provision. Economic growth in India was accompanied by corresponding increases in spending on health, education, drinking water, sanitation, rural and urban infrastructure, and employment programs. However, progress improving urban service delivery was limited. Cities struggled with inadequate levels of basic services, coupled with the pressure of the increasing pace of urbanization. Overall, local level service delivery remained poor, and improvements were not commensurate with the levels of public expenditures. 2. In 2009, Andhra Pradesh (AP), with a population of 76 million1, was India’s fifth most populous state. The urban population was 21 million, with over 70 percent of the population living in 44 cities of more than 100,000 residents. Urban economic growth had accelerated, and the number of urban centers had increased from 210 in 2001 to 353. However, provision of urban services such as roads, water, and sanitation had fallen behind growing demand. The piped water coverage ratio had declined by over 10 percent in AP cities between 1991 and 2001, and municipal sewerage systems served fewer than 20 percent of residents. These service deficiencies were partly due to AP’s climate and geography (e.g., low rainfall) but were largely a result of inadequate local financial and managerial capacity.

3. The 73rd and 74th Constitutional Amendments gave constitutional recognition to Urban Local Bodies (ULBs) and provided a basis for the State Legislatures to transfer responsibilities to ULBs. At appraisal, own source revenues (OSRs) of AP ULBs represented less than 1 percent of estimated value. ULBs were typically responsible for urban planning, water supply for domestic, industrial, and commercial purposes, and provision of urban amenities and public facilities. Property taxes and water tariffs were ULBs’ two main sources of revenue.

4. The Andhra Pradesh Municipal Development Project (APMDP, “the Project”) was well aligned with the

Government of India’s (GoI) 10th (2002-2007) and 11th Five-Year Plans (2007-2012), which for the first time highlighted urban infrastructure and management as a key national development priority. The Swajaldhara Program, which advocated for decentralization of water and sanitation functions under the oversight of the District Water and Sanitation Mission, was announced in 2002. In 2005, the Jawaharlal Nehru National Urban Renewal Mission (JNNURM), which provided grants for urban infrastructure and housing while requiring state and local institutional reforms, was launched by GoI. The Mission became the country’s largest source of financing for urban infrastructure investments. At appraisal, 215 projects had been approved in AP under JNNURM, totaling US$103 billion of GoI funding for large-scale projects in the state’s three largest urban areas: Hyderabad, Visakhapatnam, and Vijayawada. 5. By supporting local infrastructure and service delivery needs, as well as the institutional arrangements for promoting an enabling environment for long term sustainability, the Project contributed directly to the World Bank Group’s India Country Assistance Strategy (CAS) for 2009-12. In line with India’s 11th Five-Year Plan’s goal of

1 Office of the Registrar General & Census Commissioner. (2001) Census of India.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 7 of 57

comprehensive growth and service delivery, the Bank’s CAS aimed at helping India meet the challenges of: (i) achieving rapid and inclusive growth; (ii) ensuring the sustainability of development; and (iii) increasing the effectiveness of public service delivery. The Project directly contributed to Pillars 1 and 3 and complemented ongoing assistance to AP focused on the development of institutions and infrastructure.2 6. An earlier version of the Project was negotiated in July 2005, but a condition for Board presentation – a repeal of the Urban Land Ceiling Act by the state legislature – was met only in March 2008. Project design was then updated to take account of subsequent developments, including JNNURM, AP’s recent urbanization and development, completion of the U.K. Development for International Development-funded (DFID) AP Urban Services for the Poor Project, and the Bank’s increased emphasis on governance and accountability. This also meant that the 30 percent of sub-project investments that were ready for award (a GoI condition for negotiations) in 2005 had to be substantially revised. At Board presentation, a framework approach was adopted, with the remaining 70 percent of investments to be identified during implementation.

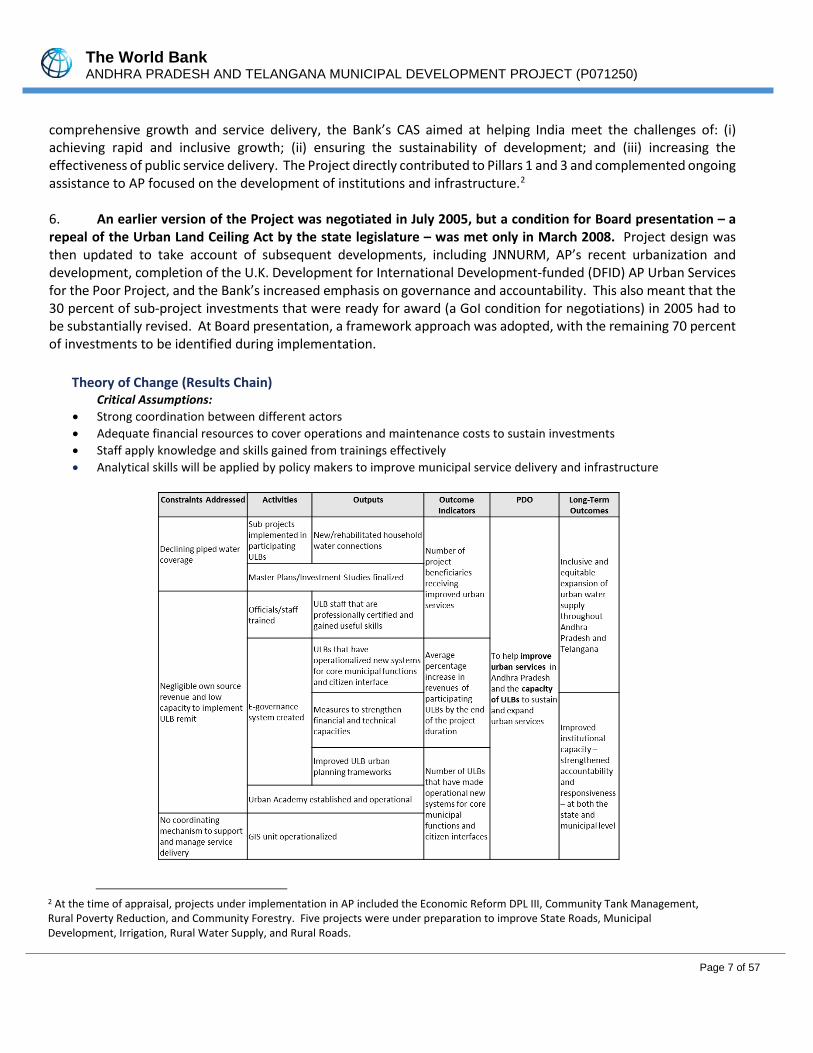

Theory of Change (Results Chain) Critical Assumptions:

• Strong coordination between different actors • Adequate financial resources to cover operations and maintenance costs to sustain investments • Staff apply knowledge and skills gained from trainings effectively • Analytical skills will be applied by policy makers to improve municipal service delivery and infrastructure

2 At the time of appraisal, projects under implementation in AP included the Economic Reform DPL III, Community Tank Management, Rural Poverty Reduction, and Community Forestry. Five projects were under preparation to improve State Roads, Municipal Development, Irrigation, Rural Water Supply, and Rural Roads.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 8 of 57

Project Development Objectives (PDOs) The original PDO was “to help improve urban services in Andhra Pradesh, and the capacity of ULBs to sustain and expand urban services.”

Key Expected Outcomes and Outcome Indicators The key outcome indicators included in the main text of the PAD were:

• Increase in residents’ satisfaction with municipal services in participating cities • Sub-project specific outcomes including the increase in hours of water supply per day, volume of liquid

or solid waste collected and sanitarily disposed of, number of water and sewer connections, and the number of people receiving significant such benefits

• Increase in ULB revenues • Number and quality of ULB service (assessment and plan) reports, signifying improvements in staff

capacity and systems 7. The Results Framework (RF) in Annex 3 of the PAD provided specific outcome indicators for each of the two PDO elements (i.e., improved urban services and improved capacity of ULBs), intermediate outcome indicators, and targets. The outcome indicators captured by the initial Implementation and Status Reports (ISR) measured: (i) residents’ satisfaction with urban services at participating ULBs; and (ii) revenue increases of participating ULBs, as sub-projects had not yet been identified. Intermediate indicators can be found in Annex 1.

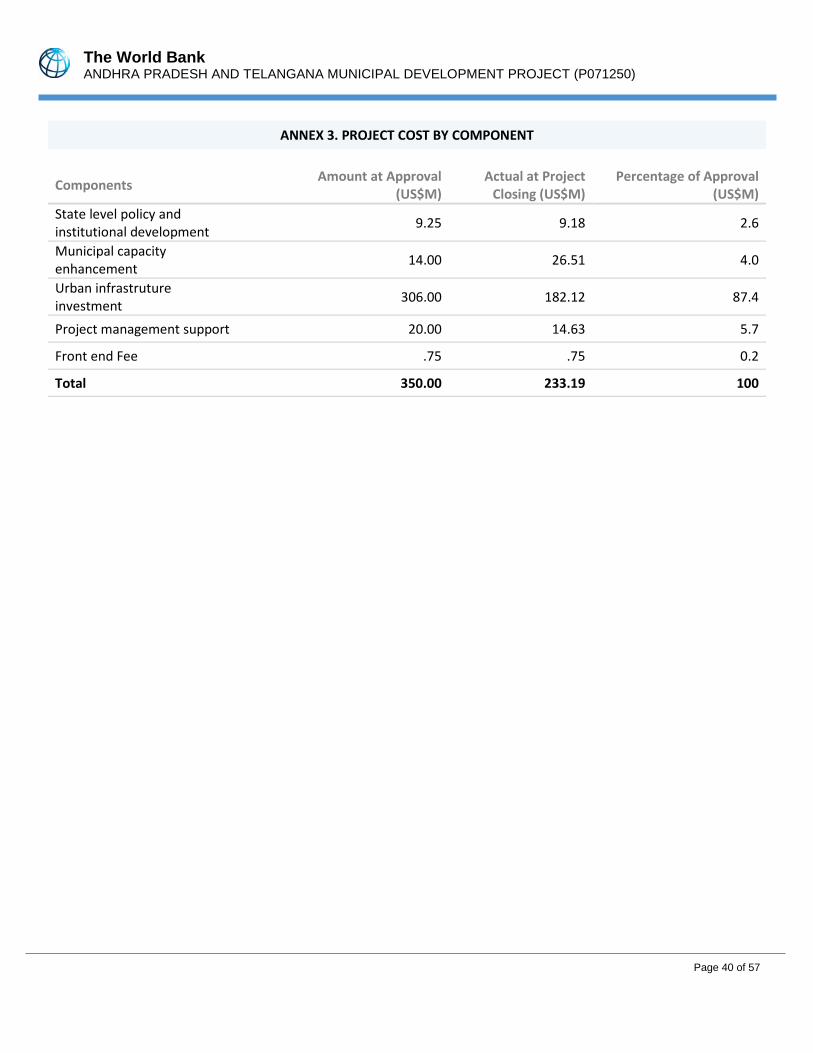

Original Components as in the Loan Agreement 8. Component A: State Level Policy and Institutional Development Support (cost US$9.2 million, Bank financing US$ 8.8 million) (i) establishment of the Andhra Pradesh Urban Academy to provide monitoring, analysis, training and knowledge dissemination, related to urban development and management in AP to urban sector officials through the provision of works, goods, and technical assistance, and incremental costs financing; (ii) studies on urban finance, town planning procedures, and the implementation of programs of the Mission to Eliminate Poverty in Municipal Areas through the provision of technical assistance; and (iii) the establishment of a Geographic Information System (GIS) Cell to support the monitoring and planning of urban development through the provision of computer hardware and software and technical assistance. 9. Component B: Municipal Capacity Enhancement (cost US$14 million, Bank financing US$12.7 million) (i) enhancement of institutional capacity of ULBs in AP in the areas of urban finance, management, e-governance, development and planning, procurement, and engineering through the provision of training and technical assistance; and (ii) establishment of a program on GIS mapping and spatial planning through the provision of technical assistance. 10. Component C: Urban Infrastructure Investment (cost US$306 million, Bank financing US$259.7 million) financed sustainable, high-priority investments identified by ULBs through the provision of investment sub-loans, sub-grants, and technical assistance. To be eligible, ULBs had to demonstrate adequate financial capacity to sustainably finance and operate the facilities and an adequate plan to improve their financial and management capacity.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 9 of 57

11. Component D: Project Management Technical Assistance (cost US$20.0 million, Bank financing US$18.1 million) financed the provision of project design, implementation, monitoring, and audit support to state-level agencies and ULBs through the provision of technical assistance and incremental operating costs.

B. SIGNIFICANT CHANGES DURING IMPLEMENTATION (IF APPLICABLE)

12. In June 2014, AP formally bifurcated into two states; the inland northern area became a new state called Telangana, and remainder retained the name Andhra Pradesh. The events before and after the bifurcation delayed project implementation considerably. The bifurcation followed prolonged protests by residents of Telangana, who felt the region had been neglected with regard to water distribution, budget allocations, and jobs. The new state of Telangana had a population of 35 million and was comprised of 10 former districts of AP, including the former capital of Hyderabad. The bifurcation created delays for the Project, as sub-projects could not be approved until the loan split between the two states was determined and finalized. Project staff were re-assigned and re-trained. The Governments of Andhra Pradesh (GoAP) and Telangana (GoT) and World Bank responded to the bifurcation and the resulting circumstances by restructuring the Project two times during the implementation period. 13. Two national demand-driven service delivery programs were introduced in 2015: Smart Cities Mission (SCM) and Atal Mission for Rejuvenation and Urban Transformation (AMRUT). SCM’s stated objective is to promote sustainable and inclusive cities that provide core infrastructure, a clean and sustainable environment, and the application of Smart Solutions. AMRUT focuses on water and sewage infrastructure for urban transformation. SCM covers 100 cities, while AMRUT has selected 500 cities across the country. Four of the Project’s ULBs were selected for inclusion in these programs: Kakinada (AMRUT and SCM), Guntur (AMRUT), Anantapur (AMRUT), and Vizianagaram (AMRUT).

Restructurings 14. In March 2015, following the bifurcation, GoI and Bank Management decided that Bank projects under implementation in the erstwhile AP state would retain their original PDOs and continue with one (combined) Project code, but implementation arrangements would be modified to reflect the new situation. Accordingly, the Project underwent a Level Two restructuring to divide the Project between the two successor states of AP and Telangana, as well as to make adjustments based on the status of implementation at that time. The Project would now be implemented by two state governments. Other changes included: (i) renaming the Project as “Andhra Pradesh and Telangana Municipal Development Project” (APTMDP); (ii) extending the closing date to December 15, 2017; (iii) revising project activities including the deletion of state finance study in Component 1 and the addition of urban planning and sector specific studies; (iv) reallocating funds from Components C and D to Component B to fund the above studies; (v) revising the RF and disbursement schedule; and (vi) entering into a new Project Agreement with the State of Telangana. The restructuring’s overall disbursement mechanism remained the same and was amended to include additional institutions in the state of Telangana. The restructuring allocated US$174 million to AP and US$126 to Telangana, apportioning savings identified based on the priorities of the two states.3 15. The Project was extended again in November 2017 by 12 months to allow for completion of works and consultancy contracts that were in progress. The implementation schedule, disbursement estimates, and RF were

3 The revised amounts of the 2015 Restructuring are as follows: Component A: US$9.20 million to US9.18 million; Component B: US$14.00 million to US$26.51 million; Component C: US$306.00 million to US$298.93 million; Component D: US$20.00 million to US$14.63 million. The additional funds in Component B were used to fund sectoral plans and city plans in both States. Additional GIS mapping and planning activities of new ULBs were to be funded under Component B.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 10 of 57

updated to reflect the revised timeline. Revised PDOs and Outcome Targets 16. The PDO remained unchanged during project implementation. However, in order to reflect the participation of the two bifurcated states in the Project, the PDO was informally changed in mission documents as: “to help improve urban services in Andhra Pradesh and Telangana, and the capacity of ULBs to sustain and expand urban services.”

Revised PDO Indicators

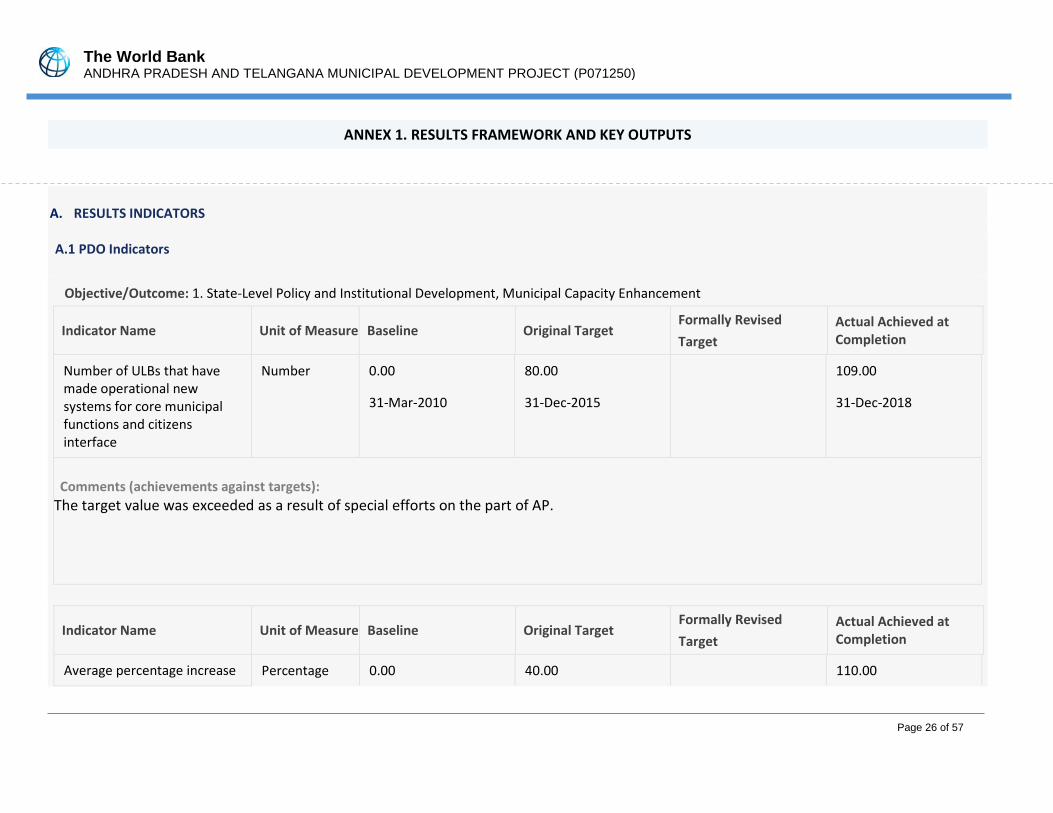

17. PDO Indicators. The 2015 restructuring modified the PDO-level service delivery indicator from the percentage of resident satisfaction to instead measure the number of Project beneficiaries. This was meant to clarify Project results and for ease of measurement. It also added an indicator: “Number of ULBs that have made operational new systems for core municipal functions and citizens interface” to track achievement of the PDO element “to help improve the capacity of ULBs to sustain and expand urban services.” Annex 1 shows the original and new outcome and intermediate indicators, along with their target values.

Revised Components

N/A

Other Changes

18. Implementing Agency. Following the June 2014 bifurcation and the 2015 Project restructuring, responsibility for implementation was assigned to the respective Municipal Administration and Urban Departments (MAUD) of AP and Telangana. Rationale for Changes and their Implications for the Original Theory of Change 19. The changes made to the Project during the two restructurings did not change the PDO or affect the original Theory of Change.

II. OUTCOME A. RELEVANCE OF PDOs

Assessment of Relevance of PDOs and Rating 20. The PDO remains aligned to the World Bank Group’s 2018 India Systematic Country Diagnostic (SCD) as well as the 2018-2022 India Country Partnership Framework (CPF). The SCD identified supporting local government as a key priority for strengthening India’s service delivery system. Similarly, the CPF recognized the relationship between empowered local governments and improved quality of life. Focus Area 1: Promoting Resource-Efficient Growth aims to improve the livability and sustainability of cities (Objective 1.2) and Focus Area 3: Investing in Human Capital sets the goal for efficient and sustainable water and sanitation service delivery (Objective 3.3). 21. Urban development continues to be a priority for GoI, and as indicated earlier, the current administration (in office from May 2014 and reelected in May 2019) launched the SCM and AMRUT missions, with which the Project is well-aligned. The continuation of the national programs until at least 2021 indicates that GoI’s commitment to the urban sector remains strong.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 11 of 57

22. GoAP and GoT have emphasized strengthening institutions and addressing urbanization challenges in state-level policies. The 12th Five-Year Plan of AP states that urban planning is a critical challenge and identifies APTMDP-led initiatives in urban infrastructure4, master plans, use of remote sensing and GIS, ULB-level governance reforms, financial resources, and capacity building. GoT is currently developing Vision 2024 and has named ULB-level governance and infrastructure as two of its ten key sectors. The GoT MAUD’s 2018-2019 Action Plan commits to expanding or completing several sub-projects initiated under APTMDP including the digital door numbering system, establishing open air gymnasiums in 307 parks, preparation of GIS base maps and master plans, and e-governance in 72 ULBs. 23. Given the strong alignment of the PDO to the principal pillars of the India CPF 2018-2022, as well as its relevance to ongoing GoI and state-level programs, the relevance of the PDO is rated as High. B. ACHIEVEMENT OF PDOs (EFFICACY)

24. The PDO comprises two elements: (i) help improve urban services; and (ii) help improve the capacity of ULBs to sustain and expand urban services. As the PDO remained unchanged, and the outcome targets did not change significantly during the life of the Project, a split PDO evaluation has not been conducted.

PDO ELEMENT 1: HELP IMPROVE URBAN SERVICES

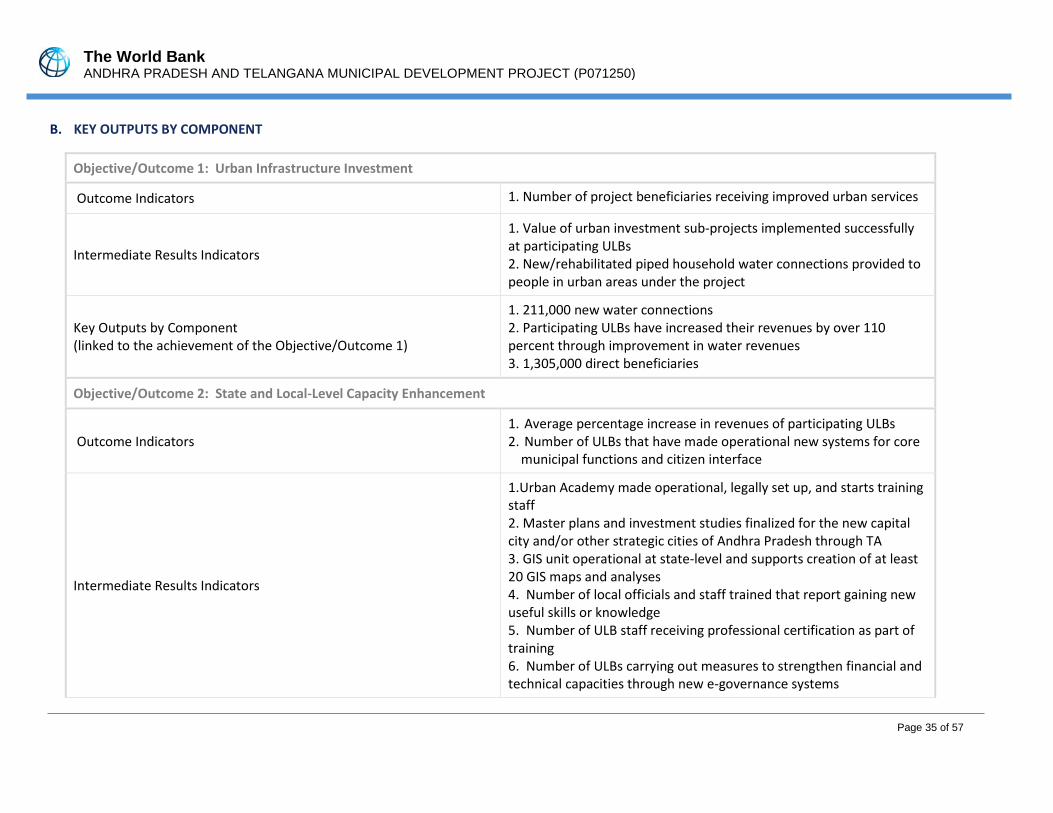

Table 1: Improvement of Urban Services – Achievement of Indicator Targets No. PDO Indicator Target Actual Achieved Status

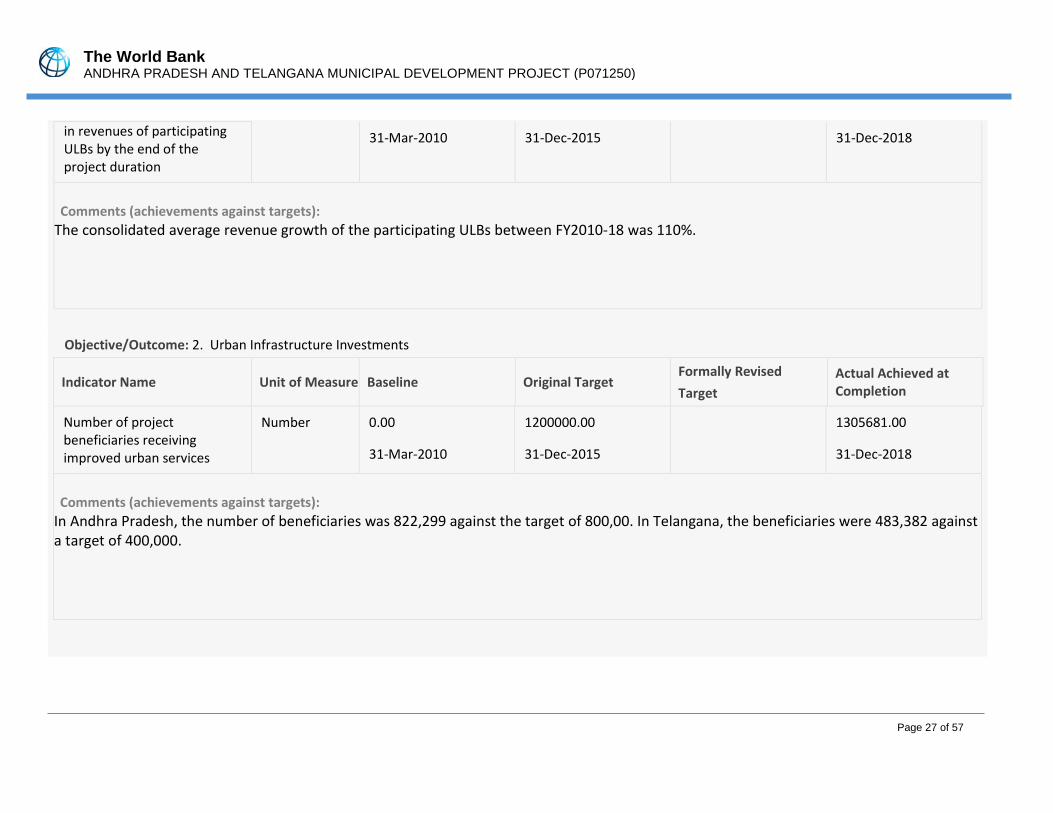

1 Number of project beneficiaries receiving improved urban services

1,200,000 1,305,681 Achieved (108%)

No. Intermediate Indicator Target Actual Achieved Status

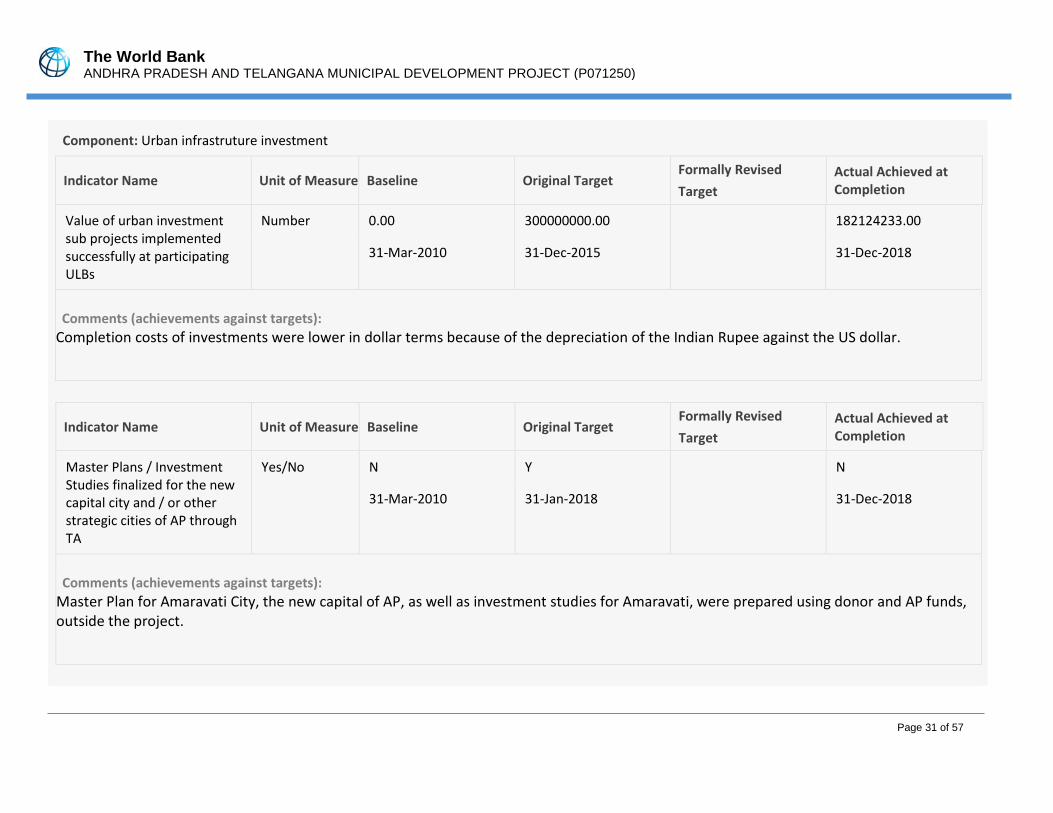

1 Value of urban investment sub-projects implemented successfully at participating ULBs

US$300 million

US$182 million Partially Achieved (61%)

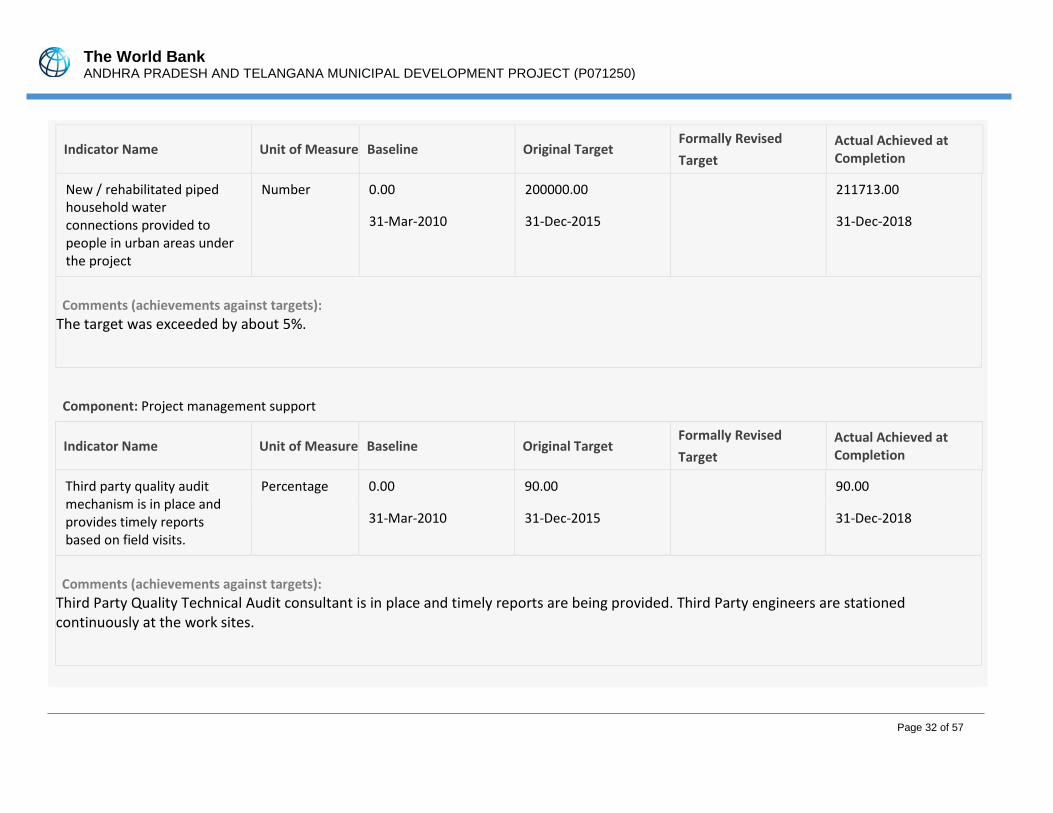

2 New / rehabilitated piped household water connections provided to people in urban areas under the project

200,000 211,713 Achieved (106%)

25. Nine ULBs were initially selected for participation in the Project; six of these were in the subsequently bifurcated AP, while three were in the state of Telangana. At the time of the first restructuring, sub-projects in five Telangana ULBs were added. Table 2 summarizes the achievements of these sub-projects; Annex 4 provides the detailed results.

Table 2: APTMDP Service Delivery Sub-projects

Sl. No. ULB Beneficiaries Number of House Service Connections

Storage Capacity (KL) Increase %

Network Coverage (KM) Increase %

Andhra Pradesh 1 Vizianagaram 115,011 14,722 7.3 85.15 2 Badvel 40,450 10,787 368.83 149.31

4 This includes: supply of desktops to set up ERP command communications centers and establishing open-air gyms in 180 parks.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 12 of 57

26. Service Delivery Outcomes. In both states, the expansion of the water supply network in hitherto uncovered areas of the cities and additional household connections helped reduce the dependence of these communities on informal, untreated sources of water supply, including through ground water extraction and tankers. The communities now have access to treated water supply as part of the ULBs’ formal water supply network and receive daily water supply, as compared to the earlier unreliable supply once in 2-3 days in most of the participating ULBs.

3 Markapur 54,950 9,676 41.27 193.06 4 Kakinada 135,300 19,569 78.15 74.62 5 Anantapur 271,500 32,952 41.56 91.00 6 Guntur 205,088 33,132 75.75 44.11 Telangana 7 Armoor 56,000 10,656 36.43 98.99 8 Manuguru 38,000 6,600 100.00 185.00 9 Malkajgiri 197,605 39,521 361.54 14.92 10 Jammikunta 36,490 8,400 222.22 69.94 11 Medak 51,027 4,765 61.00 72.00 12 Huzurabad 35,580 7,200 562.50 65.00 13 Kollapur 24,000 5,063 220.83 50.00 14 Kothagudem 44,680 8,670 41.12 142.00 TOTAL 1,305,681 211,713

27. Based on the results of these investments, and the achievement of the relevant PDO and intermediate-level indicators, achievement of PDO Element 1 is rated as Substantial. PDO ELEMENT 2: HELP IMPROVE THE CAPACITY OF ULBS TO SUSTAIN AND EXPAND URBAN SERVICES

Table 3: Improving ULB Capacity – Achievement of Indicator Targets

No. PDO Indicator Target Actual Achieved Status

1 Number of ULBs that have made operational new systems for core municipal functions and citizens interface

50 109 Achieved (218%)

2 Average percentage increase in revenues of participating ULBs by the end of the project duration

40% 110% Achieved (275%)

No. Intermediate Indicator Target Actual Achieved Status

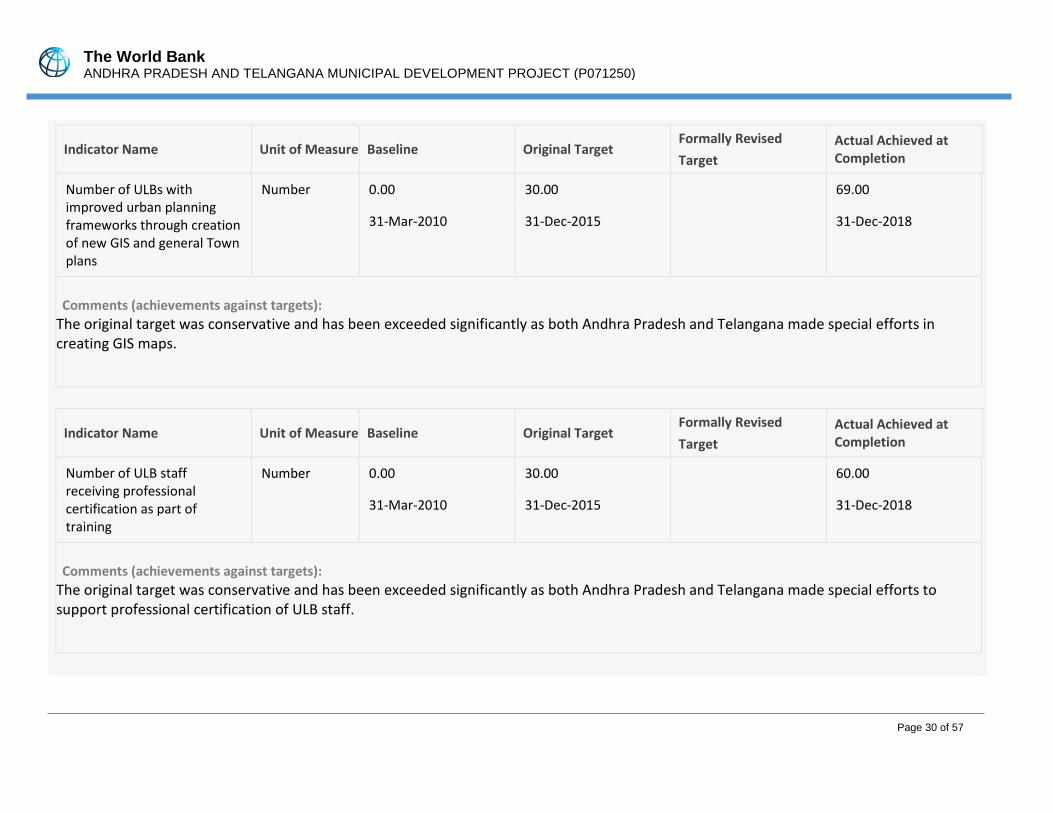

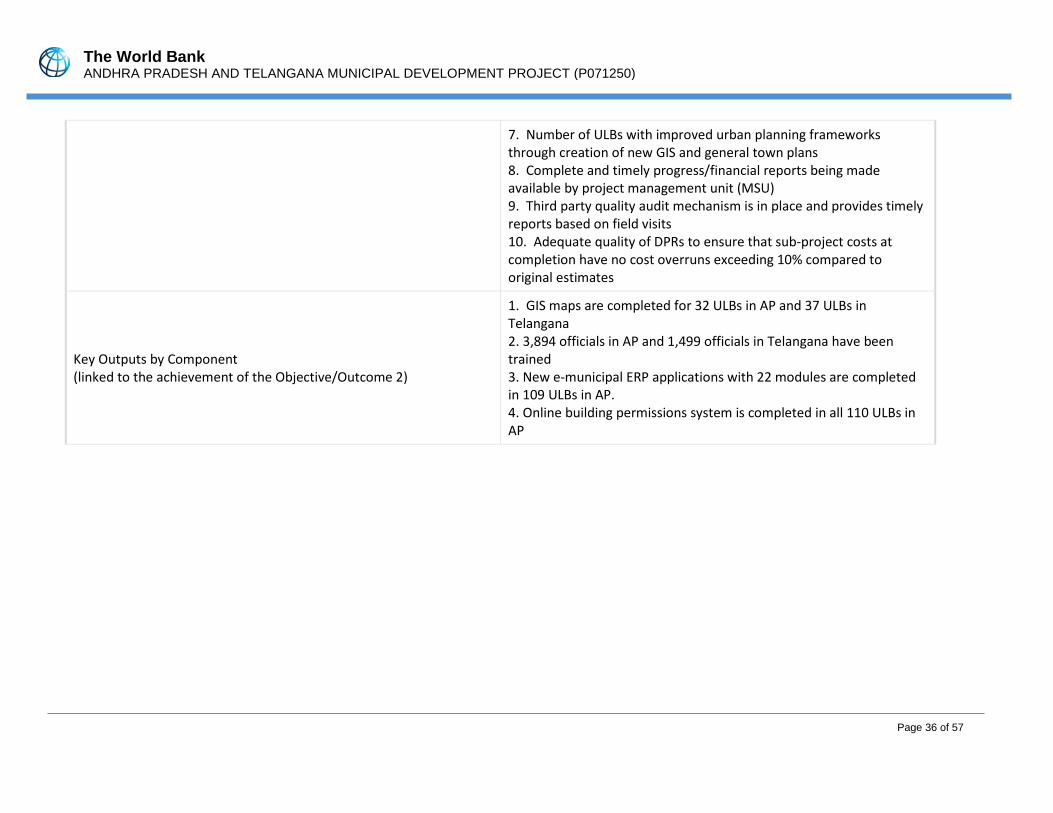

1 Number of ULBs with improved urban planning frameworks through creation of new GIS and general Town plans

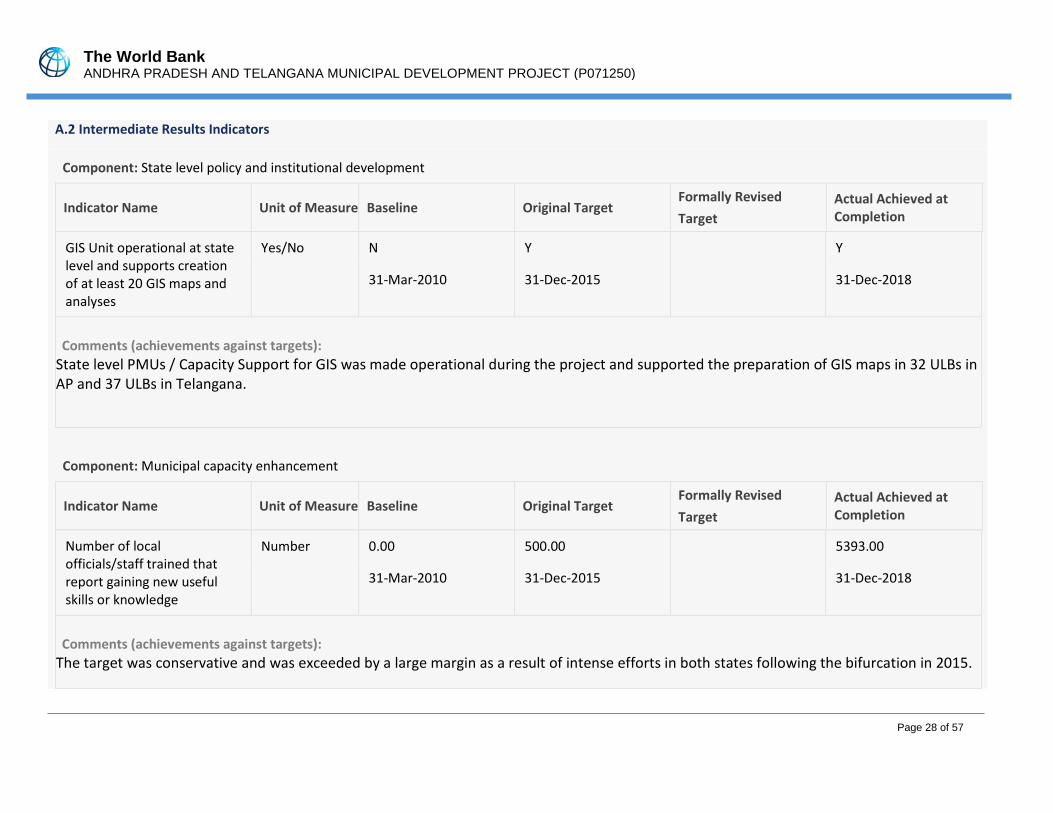

30 69 Achieved (230%) – GIS maps are completed for 32 ULBs in AP and 37 ULBs in Telangana. Planning studies have been completed for 20 Telangana ULBs.

2 Number of ULB staff receiving professional certification as part of training

30 60 Achieved (200%)

3 Number of local officials/staff trained that report gaining new useful skills or knowledge

500 5,393 Achieved (1,077%) – 3,894 officials in AP and 1,499 officials in Telangana

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 13 of 57

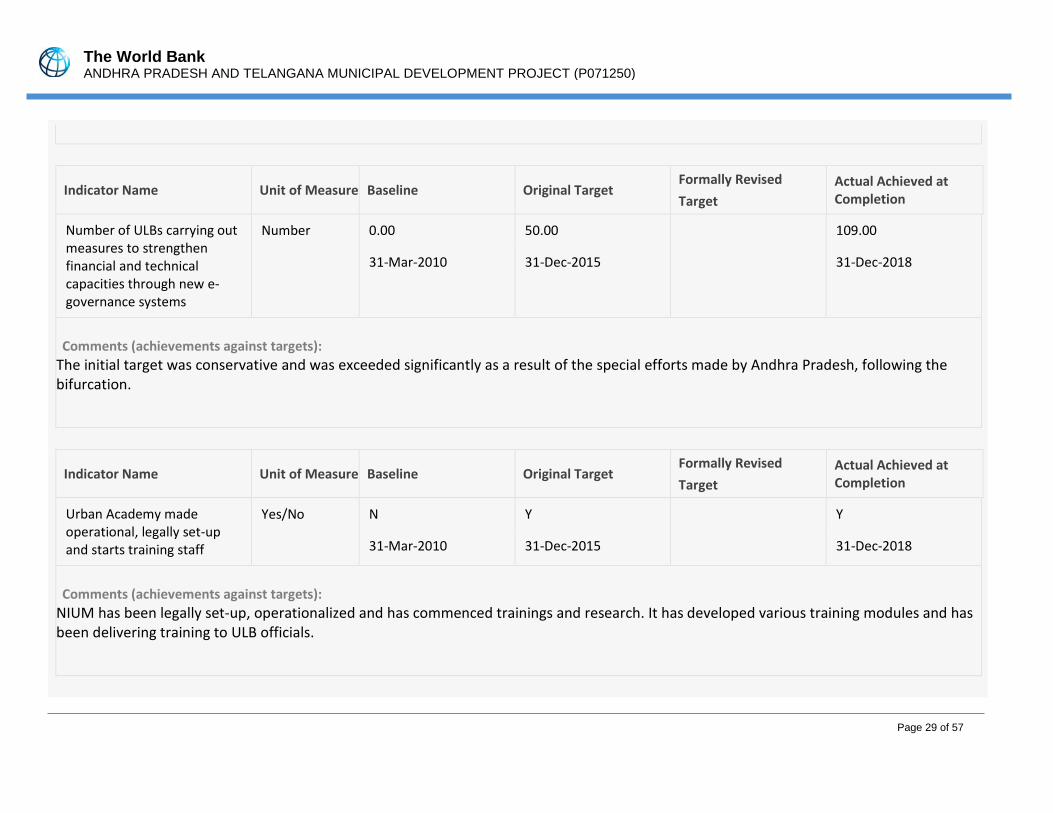

4 Number of ULBs carrying out measures to strengthen financial and technical capacities through new e-governance systems

50 109 Achieved (218%) – New e-municipal ERP applications with 22 modules are completed in 109 ULBs in AP. Online building permissions system is complete in all 110 ULBs in AP

5 Urban Academy made operational, legally set up, and starts training staff

Yes Yes Achieved – NIUM is operational and has commenced trainings and research

6 Master plans and investment studies finalized for the new capital city and/or other strategic cities of AP through TA

Yes N/A Not Applicable - Master plan for Amaravati City in AP was finalized, but not using Project funds

7 GIS Unit operational at state level and supports creation of at least 20 GIS maps and analyses

Yes Yes Achieved - State level PMUs supported preparation of GIS maps

28. Components 1 and 2 contributed to achieving the objective of this PDO Element. Component 2 provided support to enhance institutional capacity of ULBs through: (i) support for e-governance systems; and (ii) GIS mapping and spatial planning. Through the use of these systems and initiatives, as well as the ULB selection criteria emphasizing capacity building, institutional capacity in the areas supported by the Project has increased significantly. Given the newness of these systems, the initial targets were set conservatively, and as progress was modest at the time of 2015 restructuring, the targets were retained. However, the pace of implementation increased thereafter, especially in AP, which is reflected in some of the end-of-project targets being exceeded significantly. 29. Municipal e-governance systems. AP has been a pioneer in introducing e-governance in ULBs and this is now being adopted as a good practice example for wider replication across India as part of SCM. The Project supported the design and implementation of a new municipal e-governance system (the Enterprise Resource Planning - ERP – Module) in all 110 AP ULBs. This includes core municipal functions that directly impact citizens, such as building permissions, property taxes, and integrated billing. The system enables the public to electronically register 95 types of grievances, as well as track the response time and any related follow-up actions. ERP benefits the state’s 14.6 million urban residents through improved accountability, transparency, and citizen interface with their local government, and it enables ULB departments to coordinate and prioritize initiatives. The Telangana e-governance system was redesigned in 2018 as a comprehensive suite of e-government modules (e.g., tax collection, water management, financial management, and human resources) and is being implemented by GoT using own funds. 30. Enhanced OSR. GoAP made enhancement of OSRs a special focus and has completed a Revenue Improvement Survey for all 110 ULBs. Revenues have improved across all functions in all AP ULBs and processing times have been reduced because of the e-governance system.5 GoAP prioritized identifying unassessed properties and unauthorized trade and water connections, and ULBs have reported over 100 percent revenue increases in the tax and non-tax collection base, and a 30 percent increase in the identification of under assessed and unassessed properties. Processing time has been reduced by an average of 7 days, a 52 percent savings in time.

31. GIS Mapping and Planning Studies. GIS Units are operational in both AP and Telangana. As a result of the

5 Comparing FY 2009-2010 and FY 2017-2018’s water charges (in crores): (i) Vizianagaram 20.78 increased to 33.22 (59.87% increase); (ii) Kakinada 23.36 increased to 70.39 (201.33% increase); (iii) Guntur 202.54 increased to 422.34 (108.52% increase); (iv) Markapur 2.51

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 14 of 57

strong emphasis placed by both states, the initial target of 30 ULBs completing GIS work has been significantly exceeded (see Table 2 above) and work is in progress in additional ULBs in both states. GIS mapping (44 layers of data for urban management) has been completed in 32 AP ULBs. In Telangana, GIS mapping of urban services and infrastructure has been completed in 37 ULBs and planning studies have been completed for 20 ULBs, including the preparation of sewerage plans and green interventions (creation of public parks, green space, and general improvement of urban environments). GIS mapping in the remaining 78 ULBs in AP, along with revenue enhancement and 15 additional GIS data layers, has been substantially completed, including the digital door numbering system. GoAP intends use its own funds for additional work using drone mapping. In Telangana, GIS Mapping covering an additional 22 ULBs is nearing completion and will be completed using GoT funds. 32. Digital Door Numbering. In AP, a digital door numbering system (based on a nine-digit road network that uniquely identifies every house in the state) has been implemented in all ULBs. Telangana has also implemented a digital home addressing system in all 72 ULBs, making use of satellite imagery, as well as a ground survey to map properties, roads, by-lanes, vacant plots, and slums. This has established a standardized address system across the state, which assists ULBs in providing public services and emergency response systems. 33. Training of ULB Staff. Following bifurcation, GoAP and GoT demonstrated enthusiasm and proactivity for training. This was due to the creation of the new governments and requiring training for the new staff, the convenience of the NIUM campus in Hyderabad, and the new skills and capacity required for APTMDP initiatives, including e-governance and financial management. Training substantially exceeded the RF’s target in both states. 34. The Project supported the creation of the National Institute of Urban Management (NIUM).6 NIUM has been established as an autonomous think-tank and action research institute, supporting national, state, and ULB-level stakeholders through technical assistance and capacity building. It has a core team in place for the formulation of annual work plans and to undertake research studies and training programs. Over 2,000 government officials from across the country have been trained at NIUM’s temporary campus in the first three years. GoT will soon identify additional permanent working space, and NIUM is in the process of hiring 20 additional Knowledge Managers. 35. The Project was expected to finance the preparation of the Master Plan and finalize investment studies for Amaravati, the new capital city of AP. This Master Plan was prepared with support from the Government of Singapore, outside the Project. Investment studies, including for activities that are planned to be financed under a joint World Bank – Asian Infrastructure Investment Bank, were prepared using counterpart and donor funds. 36. Based on the achievement of the relevant PDO and intermediate-level indicators (see Table 3) as well as the broader achievements discussed above, achievement of PDO Element 2 is rated as Substantial. Justification of Overall Efficacy Rating: Substantial based on the discussion above on the achievements of the two PDO Elements.

increased to 8.44 (236.25% increase); (v) Badvel 4.20 increased to 7.36 (75.39% increase); and (vi) Ananthapuram 14.42 increased to 29.75 (106.31% increase) 6 The “Urban Academy” referred to in the intermediate indicators is NIUM.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 15 of 57

C. EFFICIENCY 37. A cost-benefit analysis was carried out for the Project’s infrastructure investments. See Annex 5 for details of the economic analysis. 38. As a framework project, no economic analysis was carried out at appraisal. The Project’s infrastructure investments were selected based on Detailed Project Reports (DPR) proposals submitted for each sub-project that included an initial economic analysis under JNNURM Guidelines. However, the methodology is not comparable with the standard Bank methodology used for cost-benefit analysis at completion; as such, no comparison has been attempted. 39. Results of the Economic Analysis at Completion. The results of the economic analysis at completion are shown in Table 4 below. The analysis shows that the water supply investments are economically viable, with the Economic Internal Rate of Returns (EIRR) for all sub-projects being more than the minimum required Economic Opportunity Cost of Capital (EOCC) of 9 percent. The EOCC follows recent guidelines and practices followed for recently World Bank-funded water supply projects.7 The combined EIRR for AP ULBs is 19.64 percent, 18.84 percent for Telangana ULBs, and 19.3 percent for the overall Project. See Annex 5 for details of the economic analysis.

Table 4: Economic Analysis Results at Completion

Sl. No. Project ULBs EIRR % ENPV @9% Rs. Million

1.0 AP

1.1 Vizianagaram 24.65% 636

1.2 Badvel 16.73% 555

1.3 Markapur 22.65% 493

1.4 Kakinada 17.54% 920

1.5 Anantapur 20.56% 1,343

1.6 Guntur 19.74% 3,114

AP Combined 19.64% 7,061

2.0 Telangana

2.1 Jammikunta 17.56% 245

2.2 Huzurabad 16.78% 288

2.3 Kollapur 15.51% 183

2.4 Medak 18.47% 344

2.5 Kothagudem 23.44% 447

2.6 Manuguru 20.86% 235

2.7 Armoor 14.81% 374

2.8 Malkajgiri 20.11% 2,676

Telangana Combined 18.84% 4,792

C. AP and Telangana Combined 19.30% 11,853

7 Asian Development Bank. (2017) Guidelines for the Economic Analysis of the Projects. Manila.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 16 of 57

40. A sensitivity analysis was also conducted to assess the effect of adverse changes in key variables including: (i) an overrun in operations and maintenance (O&M) costs of 20 percent; (ii) a decline in estimated benefits of 20 percent; and (iii) variables (i) and (ii) combined. The sensitivity analysis revealed that the results are robust for all water supply sub-projects. See Annex 5 for details. 41. Financial Analysis of Water Supply Operations. The financial analysis concluded that the ULBs in both states can absorb the O&M expenses of water supply services and the additional debt service requirements. However, water tariff revenues will not be sufficient to recover the annual O&M costs of the water supply systems, except in Malkajgiri in Telangana, which can recover the full O&M costs based on its existing tariff. Until the other ULBs revise their existing water tariffs to achieve full O&M cost recovery, water supply O&M will be subsidized from the ULB general account. 42. Administrative and Operational Efficiency. Over the course of implementation, the loan closing date was extended through two restructurings for a total of three years. These extensions stemmed largely from political and largely exogenous factors related to the 2014 bifurcation, and the subsequent need to establish and incorporate a new institutional structure in Telangana and to reorganize the existing structures in AP. More endogenous to the Project, additional time was required to revise ULB-level water supply planning studies, which had initially not contemplated adequate coverage levels in order to improve the equitable distribution of services among beneficiaries. Other major issues encountered during implementation included the time required for permissions from GoI departments, e.g., the Ministry of Railways and the National Highways Authority of India (for water pipelines to cross railway lines and roads, respectively) and the Department of Archaeology (for issues relating to the Project’s impact on cultural property), as well as natural hazards such as floods. 43. Utilization of the loan. As of the ICR writing, US$197.64 million (65.9 percent) of the loan amount of US$300 million has been disbursed. The principal reasons for underutilization of the loan include: the significant depreciation of the Indian Rupee vis-à-vis the US dollar; deletion of some activities from the Project; and the joint decision of GoI and the Bank not to extend the loan closing date beyond December 31, 2018 for additional activities. The rupee depreciated from INR47.7 per US$1 (PAD estimate) to INR70.4 per US$1 at project closing, leading to significant savings in US dollars, as the costs in INR did not increase by a corresponding amount. The July 2014 Aide Memoire that discussed the upcoming restructuring detailed net savings of US$42 million; in 2018, the rupee depreciated a further 14 percent. Cancellations were discussed at multiple meetings between the Bank, GoI Department of Economic Affairs, and the two states and were explicitly highlighted in mission packages. Ultimately, GoI decided to retain the original loan amount. The final two ISRs downgraded IP to Moderately Unsatisfactory due to slow disbursement and delays in contract execution. The disbursement grace period was extended on April 23, 2019 to June 30, 2019, and it is expected that the final disbursement numbers will reflect approximately 70 percent disbursement. Assessment of Efficiency and Rating: Modest. Despite the high EIRR rating, due to administrative and operational factors, the Efficiency of the Project is rated Modest.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 17 of 57

D. JUSTIFICATION OF OVERALL OUTCOME RATING Moderately Satisfactory. The Overall Outcome of the Project is rated as Moderately Satisfactory based on the ratings of Relevance of the PDO (High), Efficacy (Substantial), and Efficiency (Modest). E. OTHER OUTCOMES AND IMPACTS (IF ANY)

Gender 44. Women participated in the community meetings ahead of sub-project selection and were employed for sub-project implementation. Water supply interventions also disproportionately benefit women and girls as they are primarily responsible for water collection and benefit from the time and energy saved as a result of the house connections.

Institutional Strengthening 45. Strengthening local government institutions to deliver public services and build capacity was one of the Project’s core objectives and was captured prominently in the PDO and in the project design. The mutually reinforced approach of building systems such as e-governance and focused capacity building support worked well. NIUM provides an opportunity for continued learning. The key interventions and outcomes have been highlighted in the Efficacy section.

Mobilizing Private Sector Financing N/A

Poverty Reduction and Shared Prosperity

46. By providing water supply services to previously unconnected households and communities, the Project contributed to sharing prosperity and reducing multi-dimensional poverty. Each ULB’s sub-project area was mandated to include low-income neighborhoods, which directly contributed to poverty reduction through boosting service connectivity, creating local employment, and implementing works that led to improved public health outcomes. 47. Local communities participated in the construction of sub-projects, which provided employment opportunities. Of the nearly 96,000 total days of employment for the Telangana sub-projects, around 18 percent (17,200 days) employed local labor, of which 23 percent (3,960) were women. In AP, local labor worked 37 percent (301,550) of the 815,000 days of employment created from the Project, of which 34 percent (102,530 days) were women.

Other Unintended Outcomes and Impacts 48. One of the positive outcomes of APTMDP is the pioneering of new technologies in service delivery and local governance. In both states, the Project supported technologies such as GIS mapping, drones, e-services, smart metering and bill collection, and digital door numbering. Beyond these noteworthy improvements in the level of service provision and improved collection of user charges, the Project has demonstrated the potential for technology and smart solutions at the local level and opportunities for greater stakeholder engagement, transparency, and accountability through digital platforms.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 18 of 57

III. KEY FACTORS THAT AFFECTED IMPLEMENTATION AND OUTCOME A. KEY FACTORS DURING PREPARATION

49. The preparation of the Project was thorough and was based on robust analysis. The Project built on the initial 2005 project preparation and past Bank support to GoAP to remove infrastructure bottlenecks and strengthen institutions and systems. Using these as lessons learned and good practices, APMDP addressed key weaknesses in urban services and institutions. The Project was designed to build on the JNNURM institutional strengthening criteria. In addition, the Project emphasized support for municipal capacity building, anchored within the state’s municipal administration system rather than trying to enhance ULBs’ access to capital markets and risk jeopardizing the Project’s effectiveness due to the lack of local capacity. Support to state-level policies and institutions were specifically designed to enable sustained performance at the local level. This strategy was especially effective after bifurcation, when the relatively simple project design helped to build the new state’s capacity and institutions. 50. Risks and key institutional issues identified were clearly stated in the PAD, and project design included measures to mitigate capacity and accountability risks. Some of the risks identified included lack of political will for local autonomy and accountability, inappropriate selection of sub-projects, and/or weakened demand for state-level reforms. These risks were mitigated by focusing on building systems for accountable and effective local governance and included broad consultations with citizens and political leaders. Sub-projects were demand-driven and agreed with local stakeholders. In addition, ULBs were required to meet criteria demonstrating capacity and commitment to further improve capacity. Priority was given to improving institutional capacity from the outset through assessments of local capacity needs and the identification of training opportunities. State-level reforms and the corresponding Terms of References were agreed before appraisal. Overall, the risk mitigation measures put in place were appropriate.

51. At appraisal, the Project was designed as a framework, and neither the participating ULBs nor the individual sub-projects were identified. It was intended that the Project would support a wide variety of sub-projects, possibly including urban roads, sewerage, water supply, sanitation, solid waste management, street lighting, energy efficiency, and community centers.

B. KEY FACTORS DURING IMPLEMENTATION

52. Selection of sub-projects and ULBs. The state government subsequently determined, in agreement with the Bank, that the Project should focus on ULBs with water scarcity issues as well as ULBs that had not previously participated in earlier national programs (e.g., JNNURM). This was formalized in a 2009 GoAP order. GoAP, in agreement with the Bank, applied a set of criteria to select the participating ULBs that included: a satisfactory and current audit of municipal accounts; an operating budget surplus of more than 15 percent of the identified sub-project; and an approved Municipal Reform Action Plan (MRAP) that included actions to increase the ULBs’ operating surplus and cover the operating costs of the proposed sub-projects. These criteria were aligned with those of JNNURM, which were well-established and had proven successful. 53. ULBs conducted extensive consultations with stakeholders as part of the preparation of the DPR. Outreach to women was a part of the consultation process, and sub-project designs included a household survey for the social baseline of the sub-project area. The City Councils then approved the sub-projects. The selected water supply sub-projects comprised a combination of new distribution networks and house service connections, increased

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 19 of 57

system capacity, reduced ground water extraction and use of water tankers, and improved hours of supply. Investments were made with strategic objectives: (i) universal coverage, including slum households being provided with individual connections; (ii) preparation for the provision of 24x7 water supply; and (iii) sustainability at the local level, including financial, social, and environmental sustainability.

54. Transfer of funds. Once the ULB eligibility criteria for the water supply sub-projects were met, the Andhra Pradesh Urban Finance and Infrastructure Development Corporation (APUFIDC) and Telangana Urban Finance and Infrastructure Development Corporation (TUFIDC) signed MoUs with each of the participating ULBs for the transfer of funds partly as grants and partly as loans. The sub-loans were repayable over 15 years at an interest rate equal to the state’s borrowing cost, plus one percent per annum (replicating the JNNURM model). Funds were released to ULBs in tranches, depending on their utilization in ongoing sub-project contracts.

55. Restructurings. At the time of the 2015 restructuring, the nine ULBs participating under the Project had completed procurement and 85 percent of funds allocated for investment sub-projects had been committed. The institutional and capacity building components were largely on track. However, disbursements were low (16.5 percent) because of the difficulties preceding the bifurcation, the time required for the new governments to be organized, delays in receiving permissions from GoI Ministries, and the depreciation of the rupee. As a result, the end-of-project targets in the RF were retained unchanged. Despite the restructuring, implementation delays continued, which impacted sub-projects’ progress and the scope of work. A second restructuring extended the project closing date by 12 months to accommodate the delivery of sub-projects. 56. The bifurcation of the state into Telangana and AP was extremely disruptive for project implementation. The agitations prior to the bifurcation, particularly in Telangana, resulted in serious delays for over two years. The Project followed the AP Reorganization Act to determine the split of the loan amount between the successor states. Five Telangana ULBs were added to the GoT portfolio, as loan funds were available under the loan allocation for Telangana. These ULBs did not receive as many opportunities for capacity building support and training opportunities and had smaller sub-projects due to the reduced time available for their implementation. 57. Institutional Arrangements. The ULBs identified and designed the investment and TA programs, planned and managed implementation, and contributed funds to the sub-projects. The Project was implemented at the state level by a Municipal Strengthening Unit (MSU) under the Commissioner and Director of Municipal Administration (CDMA), which supported ULBs in preparing and managing sub-projects, including detailed design and supervision support. The MSU also coordinated training for the ULBs. APUFIDC and TUFIDC conducted fiduciary appraisal of sub-project proposals and ULBs, verified and disbursed funds, and collected repayments. Following the bifurcation, the reorganization and transferring of staff to Vijayawada (the interim capital of AP) and the creation of the parallel agencies in Telangana resulted in the need to hire and retrain staff and adapt to new working conditions.

58. Loan Utilization. The period leading up to and post bifurcation resulted in a loss of momentum in implementation, which affected overall progress and disbursement and compounded issues related to the significant depreciation of the rupee. See Efficiency for details.

IV. BANK PERFORMANCE, COMPLIANCE ISSUES, AND RISK TO DEVELOPMENT OUTCOME

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 20 of 57

A. QUALITY OF MONITORING AND EVALUATION (M&E) M&E Design

59. Results Framework. Three PDO indicators and 12 intermediate indicators comprised the RF. The PDO indicators evaluated the Project’s objectives, and intermediate indicators assessed the progress of the components and were measurable and time bound. Baselines, data/information sources, and responsible agencies for data collection and compilation were clearly defined. However, the framework nature of the Project meant that targets were difficult to determine at appraisal.

60. The Project was restructured twice with amendments to the RF. The two restructurings provided an opportunity to review and modify the RF. While some modifications were made by adding and dropping indicators, the review could have been more rigorous, especially in relation to end targets once sub-project activities and ULB participation rates were known. The PDO indicator measuring beneficiary satisfaction was modified to reflect the number of beneficiaries (for ease of measurement), and an additional PDO indicator was added to measure operational new systems as part of state-level and ULB capacity building. Intermediate indicators were modified to reflect the nature of project investments selected by the ULBs during implementation. However, the indicators could have been further refined and revised during the two restructurings. An indicator better calibrated to the sub-project investments (e.g., water supply coverage) would have provided more detail than the number of beneficiaries. The intermediate indicator related to the new capital city of AP was not applicable to the Project once the master plan was not funded under APTMDP and should have been dropped. Targets were not amended during the restructurings, which led to significant over achievement of some indicators, especially the intermediate indicators related to PDO Element 2. 61. The Project’s M&E system was designed to track project expenditures by ULBs, fund flows, and ULB and state administrative functions. The MSUs were responsible for overall project M&E based on reports from implementation agencies and their own analysis. Progress on ULBs’ investment sub-projects was reported monthly, which the CDMAs reviewed and compiled in the form of quarterly project reports for MAUD and the Bank.

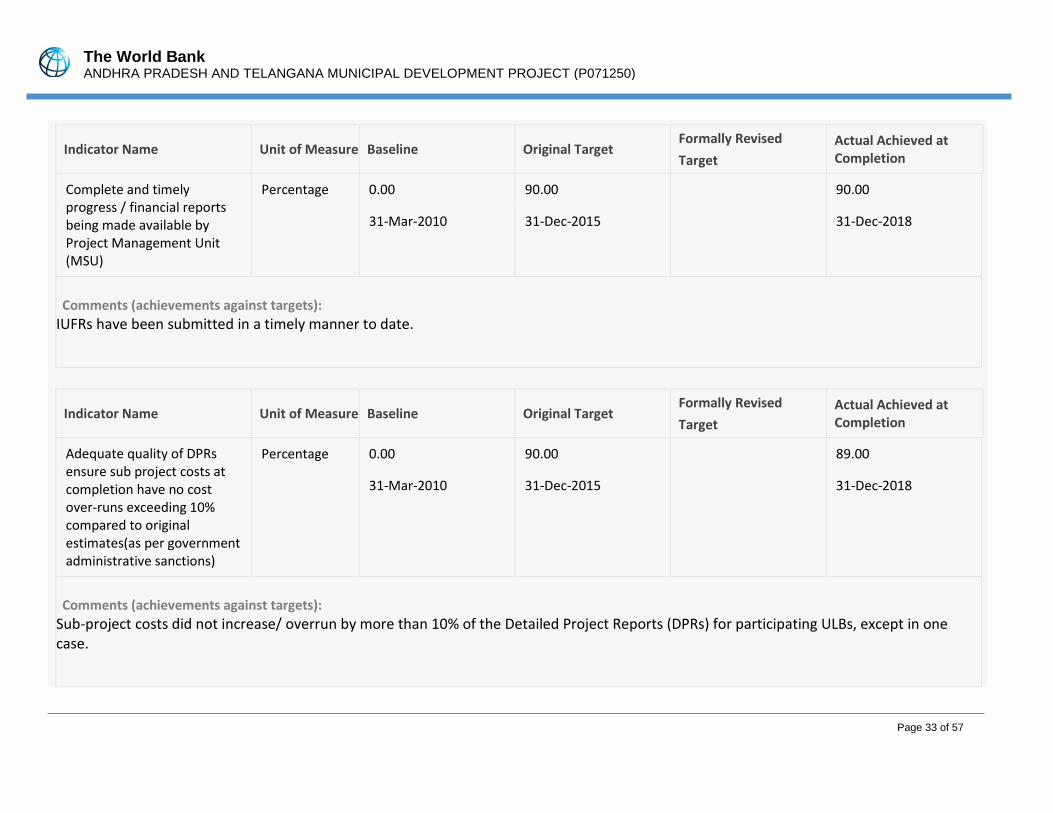

M&E Implementation 62. The M&E systems were implemented as per the original and updated designs. The MSUs and ULBs made a concerted effort to collect and track financial data on the infrastructure investments. ULBs were trained to collect and maintain data related to the sub-projects. All 14 ULBs provided individual sub-project progress reports, which included information related to selection of the sub-project, costing and payments, the reasons for time extensions, problems experienced, amount and type of ULB contribution, and the existence of a maintenance, business, and/or environmental management plan. “Complete and timely progress / financial reports being made available by Project Management Unit (MSU)” was an intermediate indicator that was fully achieved. M&E was consistently rated as Satisfactory in ISRs.

M&E Utilization 63. Utilization. The CDMAs organized regular meetings for ULBs to share their experiences. The Bank monitored and supported M&E implementation through the review of the CDMA reports and consultants, in addition to twice yearly missions. ULB and MSU reports were utilized by the PMUs, execution support agencies, and the Bank team to make corrections and improvements in the work program. This was especially relevant in the last year of implementation in order to identify sub-projects at risk of not being completed by project closing or in

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 21 of 57

danger of cost overruns. The intermediate indicator “Adequate quality of DPRs ensure sub project costs at completion have no cost over-runs exceeding 10% compared to original estimates” was achieved except for one ULB. 64. In AP, the e-governance team identified monitoring ULB performance and the lack of adequate information for informed decision-making as a critical challenge. The ERP system monitored performance indicators based on analysis of ULB data, alongside GIS maps which tracked and compared ULB performance.

Justification of Overall Rating of Quality of M&E: Modest.

B. ENVIRONMENTAL, SOCIAL, AND FIDUCIARY COMPLIANCE 65. Environmental and Social Safeguards. Due to the nature of the infrastructure investments and the project area, the Project was classified as Category A and triggered a number of Bank safeguard policies: OP/BP 4.01 (Environmental Assessment); OP/BP 4.36 (Forests); OP 4.09 (Pests); OP/BP 4.11 (Physical Cultural Resources); OP/BP 4.10 (Indigenous Peoples); and OP/BP 4.12 (Involuntary Resettlement). On the basis of the Social and Environmental Assessment, a Social and Environmental Assessment and Management Framework (SEAMF) was prepared, which was revised in 2015. The revised document incorporated the provisions of GoI’s 2014 “Right to Fair Compensation and Transparency in Land Acquisition and Rehabilitation and Resettlement Act.”

66. The Project team was thorough in preparing the safeguards documents. The SEAMF was developed into a Project Manager’s Manual (PMM) and a Manual for Urban Local Bodies (MULB). The manuals included a Social and Environmental Capacity-Building Action Plan (SECAP), and an Information and Consultation Strategy and Action Plan (ICS) to ensure that information was available to stakeholders throughout the project cycle and for obtaining stakeholder feedback. The PMM aided project managers to understand and supervise implementation of the SEAMF as well as manage information and communications for the Project. The MULB provided the ULBs with guidance for implementation.

67. Environmental and Social Safeguards Implementation. The Project’s safeguard documents were adopted by the successor states after the bifurcation of AP. Implementation of social safeguards was generally satisfactory, with minimal issues relating to land acquisition or implementation of the Tribal Development Plan. However, the delay in providing house ownership titles in one of the ULBs in AP resulted in downgrading of social safeguards management to “Moderately Unsatisfactory” in the final ISR. These ownership titles were provided shortly after project closing and demonstrated the ULBs’ continued commitment to the Project. Environmental safeguards were rated “Satisfactory” in the final ISR. The Project enabled the adoption of several good environmental management practices, including provisions for recycling backwash water in water treatment plants, monitoring of air and water quality, use of personal protective gear by workers, public notices on work periods and contact details of staff in-charge, systematic records on tree cutting and road restoration requirements, and the use of cautionary signage to restrict unauthorized access to work areas.

68. OP/BP 4.01 (Environmental Assessment). The Environmental Management Framework (EMF) developed during project preparation included a screening and appraisal process for sub-projects, institutional arrangements, and plans for capacity building and monitoring. Post-bifurcation, the EMF was revised and re-disclosed. An

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 22 of 57

environmental screening and assessment was undertaken for all sub-projects. The EMF was suitably responsive; when the scope of a sub-project was enhanced post-environmental screening and assessment, the environmental management plan was revised to reflect the changes.

69. OP/BP 4.11 (Physical Cultural Resources). A Physical and Cultural Resources Management Plan was prepared in consultation with the Department of Archaeology for the Malkajgiri sub-project (which required construction activity in the vicinity of a protected monument) and was implemented in an acceptable manner.

70. OP/BP 4.10 (Indigenous Peoples) and OP/BP 4.12 (Involuntary Resettlement). Land acquisition and resettlement impacts were addressed in compliance with the SEAMF by providing compensation as per agreed provisions and offering displaced families alternative housing with basic amenities and ownership rights. Two resettlement action plans in AP’s Guntur and Vizianagaram were prepared and implemented, as was a Tribal Development Plan for Telangana’s Manuguru. Land acquisition-related impacts in AP included the acquisition of 1.54 acres of private land (impacting 30 land owners) and the displacement of 32 informally-settled families. All basic infrastructure facilities proposed under the Tribal Development Plan were completed, except for the construction of boundary walls for the community centers for want of funds. The Project was endorsed by the tribal community and implementation was conducted in a culturally appropriate manner. The costs of implementation of land acquisition and resettlement in Guntur and Vizianagaram were US$307,840 (INR21.36 million) and US$27,380 (INR1.90 million) respectively, approximately 0.77 and 0.35 percent of the cost of the respective schemes. In Telangana, one acre of private land was acquired through the Land Acquisition Act and donation. The Telangana donor family was provided with regular employment in return for the land donation. Additional details can be found in Annex 6.

71. The Project made efforts to avoid the acquisition of private land by identifying vacant municipal property or annexing GoI-owned land. In addition to using ULB land, approximately 20 acres of land belonging to other government departments was used to meet sub-projects’ land requirements. The planned construction of a summer storage tank in Kakinada was abandoned due to complex land acquisition and livelihood issues. The proposed site consisted of 185 acres of land cultivated by three cooperative societies under lease arrangements from GoAP. The cooperative societies claimed rights over the land and appealed in court, which resulted in prolonged delays and the eventual abandonment of the scheme.

72. One of the key social development outcomes of the Project was the facilitation of resettlement assistance and the establishment of ownership rights for 32 families in Guntur. The Project provided housing with formal titles to the resettled families and provided support to extend basic amenities (e.g., internal roads, drains, and street lighting). In Manuguru, the Project improved access to key basic facilities and extended individual house connections for drinking water in two tribal villages.

73. Fiduciary. The Project’s overall financial management system was rated as Moderately Satisfactory in the final ISR. Accounting and reporting in both states, as well as internal audits, were mostly on time. External audits were normally delayed, but there are currently no outstanding reports. There was an issue in both states with utilization certificates being submitted as and when funds were required, instead of monthly as recommended. This delayed the accounting process and was repeatedly highlighted in Project mission packages. Additionally, in

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 23 of 57

Telangana, ULBs reported unpaid bills and requested transfer of funds from TUFIDC for making payments to contractors. Multiple mission packages requested GoT to release funds to ULBs, as these delays affected project implementation.

74. The MSUs maintained adequate records to support the Project’s expenditures incurred by the States. The Project disbursed both sub-grants and sub-loans to the ULBs through APUFIDC and TUFIDC, which the Bank reimbursed. Both states had some issues with ULBs making less-than-agreed contributions to sub-projects; while these did not impact disbursement, they did affect the overall financial closure of contracted packages.

75. Procurement. The overall procurement performance was rated as Moderately Satisfactory in the final ISR. The procurement process generally complied with World Bank procurement rules and procedures. The ULBs and state agencies demonstrated growing capacity for conducting procurement activities, including procurement planning and the bidding process. The procurement process generally worked well, especially for the IT firms selected for Components A and B. However, there were some delays in procurements that could then not be taken up, such as water meter contracts in some of the ULBs.

C. BANK PERFORMANCE

Quality at Entry 76. The World Bank team incorporated relevant lessons from previous AP and local governance service delivery projects in the design of the Project. When project approval was delayed after the 2005 negotiations, the design was updated to reflect current GoI, GoAP, and Bank priorities. The Project addressed the issues highlighted by national programs, state policies, and Bank strategic documents. Risks were correctly identified and appropriately mitigated. The Project’s framework design was deliberately flexible to allow the selection of ULBs and sub-projects based on the agreed criteria and ULB priorities. The Bank ensured that a team of specialists was mobilized to address all relevant project issues, including technical aspects, social and environmental safeguards, and M&E. Economic and financial analysis, appropriate for a framework project, was also carried out. See Key Factors During Preparation.

77. Project design focused adequately on fiduciary and safeguards requirements. Financial management and procurement arrangements were well designed and addressed the principal risks identified by the capacity and risk assessments. Appropriate environmental and social safeguard policies were triggered, and the SEAMF followed Bank requirements. Safeguards documentation was especially thorough, including MULBs and ICS, and helped ensure ULBs understood their roles and responsibilities and how to disseminate information to stakeholders. Training related to safeguards, procurement, and project management began during project preparation.

78. The Project was designed as a framework and was thus only partially ready for implementation at the time of approval. The selection of the participating ULBs and the sub-projects began after project approval. Consequently, the first two years of implementation were dedicated to the selection of participating cities and sub-projects, the signing of MoUs, and recruitment of consultants to provide technical support to the ULBs.

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 24 of 57

Quality of Supervision 79. The Project was thoroughly supervised by the Bank’s task team throughout the implementation period. The Bank produced 19 ISRs during the Project. Most missions comprised joint field visits with GoAP/GoT teams and core World Bank team members and were effective in identifying and addressing implementation issues. Supervision and midterm review documentation, including Aide Memoires, management letters, and ISRs, were thorough and appropriately candid and included clear action items to expedite sub-project implementation and address any fiduciary and safeguards issues. The Project benefitted from excellent team continuity as the co-TTL remained for the entire duration. The core team was all based in-country.

80. Restructurings were completed in a timely manner to reflect project needs. The Bank provided needed support during the bifurcation. The team restructured the Project in April 2015 after it was determined how to split the loan in consultation with GoI and the CMU. Throughout the bifurcation process, the Bank team continued to conduct missions, hold field-based reviews, and provide ULB-level training. The second restructuring ensured the Project’s main activities could be completed.

81. M&E design updates and utilization could have been more rigorous, including amending the RF during the restructurings to better reflect sub-project investments and outcomes. Targets, especially related to PDO Element 2, were conservatively estimated at appraisal and should have been revised once the momentum of implementation increased.

82. The Project could not utilize about one-third of the loan. Cancellations were discussed and explicitly mentioned in mission packages as early as the Mid Term Review in 2013, but GoI and the state governments decided to leave the loan amount unchanged.

Justification of Overall Rating of Bank Performance: Moderately Satisfactory D. RISK TO DEVELOPMENT OUTCOME

83. The future sustainability of the completed sub-projects must be carefully monitored. Potential issues related to the maintenance of physical infrastructure, institutional capacity at the local level, and continuation of community engagement must be supervised. Key aspects of sustainability include:

a. Completion of remaining Project works. GoAP and GoT have made provisions to complete sub-projects that were not completed by the loan closing date, as well as scale them up using state, GoI, SCM, and/or AMRUT funds. However, asset management will be critical and closely linked to financial sustainability and institutional capacity. Incomplete sub-projects are in the Telangana ULBs which had limited implementation time, and all will be completed by June 30, 2019. Additional works (e.g., incorporating metering in Badvel and Kakinada) will scale up APTMDP’s investments. b. Financial Sustainability. ULBs will receive water-supply related revenues that directly support O&M. As of May 2019, collection efficiency is very low in some ULBs, and there is potential for generating much higher revenues based on the existing tariffs. GoAP/GoT and CDMAs should also work with ULBs to introduce revised water tariffs to fully cover O&M costs (e.g., Badvel has recently raised tariffs as a result of the Project). These efforts will reduce the need for ULBs to provide O&M subsidies for water supply operations. c. Institutional Capacity. The Project provided significant training to both state and ULB officials, which has resulted considerable capacity building. However, routine rotation and reassignment of

The World Bank ANDHRA PRADESH AND TELANGANA MUNICIPAL DEVELOPMENT PROJECT (P071250)

Page 25 of 57

personnel is an ongoing occurrence, and provision must be made for training the replacement staff. d. Community Engagement. Residents’ associations were actively involved in resolving issues during Project implementation but have no formal role in O&M moving forward. Institutionalizing roles and responsibilities for the community post-implementation will ensure continued stakeholder engagement and ownership of the investments.

84. Links to National Programs. The continuation of the national SCM and AMRUT missions until 2021 (and possibly beyond) has enormous potential to expand APTMDP investments. Kakinada in AP is currently implementing water supply metering under SCM. There are also discussions of mapping the city’s pipeline network, digitizing it, and linking it to a data platform in order to monitor the water supply network. Vizianagaram, Guntur, and Anantapur have used AMRUT funds to extend APTMDP works or to introduce smart metering.

V. LESSONS AND RECOMMENDATIONS 85. Capacity building of local governments is an ongoing activity and must be targeted to the selected ULBs’ priorities. Bank-supported urban development projects in other Indian states have operated primarily through state-level financial intermediaries to channel investment financing and facilitate ULB capital market access. APMDP chose to anchor the project in CDMA and focus on improving ULB capacity, including for service provision. This has prepared these ULBs for more sophisticated financing models in the future. Future projects should consider whether such a focused approach would be suitable in the specific local circumstances. 86. The Bank must set realistic conditions for Board presentation. In 2005, the condition for presenting the APMDP loan to the Executive Directors for approval - the repeal of the Urban Land Ceiling Act - delayed the approval of the loan by nearly three years. As a result, the loan for the Project had to be re-negotiated and the GoI requirement of 30 percent pipeline had to be reestablished. The impact of such conditions for Board presentation of loans should be carefully considered a priori.

87. Framework projects require the RF to be refined and updated. Projects approved under a framework approach are unable to design an M&E system that adequately captures project results, as the participating ULBs and/or the details of the specific infrastructure investments are not known at appraisal. The RF should be carefully monitored and modified during restructurings to better capture the results of the identified investments. 88. The Bank should consider funding of focused, complementary TA packages for ULBs. Most state-level urban projects in India, including APTMDP, have TA components that are formulated statewide for comprehensive studies. Consequently, the contracts are large and are implemented across a range of ULBs to enable cross-learning and coordination. However, as was the case in this Project, progress of implementation is uneven when there are a large number of ULBs. An alternative would be to work with a selected number of ULBs on a demand driven / pilot basis and mainstream initiatives subsequently through dissemination and a follow-on project.