ijcrb.webs.com F 2013 I JOURNAL F O CONTEMPORARY R …journal-archieves28.webs.com/211-231.pdf ·...

21

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 211 FEBRUARY 2013 VOL 4, NO 10 Assessment of Current and Future prospects of Activity Based Costing in the Textile Sector of Pakistan Danish Iqbal Godil Department of Management Sciences Bahria University – (Karachi Campus) Dr.Syed Shabib- ul- Hasan Department of Public Administration University of Karachi Abstract This study focuses on the costing system followed by textile sector in Pakistan and investigates the issues such as rate of adoption of ABC system by textile sector of Pakistan by classifying them as Implementers, Supports, Non implementers, Unawares, the reasons for non implementation and as to why management was motivated to implement ABC system in future was also analyzed. In order to accomplish these tasks firstly a questionnaire was developed and handed over to the finance and accounts staff of 60 textile companies out of which 42 responded. According to the findings of this study many companies of textile sectors have not implemented ABC system due to non active support of top management and time constraint. mindset of the organization, management is satisfied with current costing system, planning to implement it in future, lack of resources and high cost of system implementation etc. Keywords: ABC system, Textile Companies, Strong Active Support of Top Management.

Transcript of ijcrb.webs.com F 2013 I JOURNAL F O CONTEMPORARY R …journal-archieves28.webs.com/211-231.pdf ·...

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 211

FEBRUARY 2013

VOL 4, NO 10

Assessment of Current and Future prospects of Activity

Based Costing in the Textile Sector of Pakistan

Danish Iqbal Godil

Department of Management Sciences

Bahria University – (Karachi Campus)

Dr.Syed Shabib- ul- Hasan

Department of Public Administration

University of Karachi

Abstract

This study focuses on the costing system followed by textile sector in Pakistan and investigates

the issues such as rate of adoption of ABC system by textile sector of Pakistan by classifying

them as Implementers, Supports, Non implementers, Unawares, the reasons for non

implementation and as to why management was motivated to implement ABC system in future

was also analyzed. In order to accomplish these tasks firstly a questionnaire was developed and

handed over to the finance and accounts staff of 60 textile companies out of which 42 responded.

According to the findings of this study many companies of textile sectors have not implemented

ABC system due to non active support of top management and time constraint. mindset of the

organization, management is satisfied with current costing system, planning to implement it in

future, lack of resources and high cost of system implementation etc.

Keywords: ABC system, Textile Companies, Strong Active Support of Top Management.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 212

FEBRUARY 2013

VOL 4, NO 10

1. Introduction

With increasing worldwide competition in modern era, and due to the emergence of advance

manufacturing technologies (AMT), textile as well as other industries are adopting higher

production automation and product diversification. Cost allocation of production overhead is an

important factor in estimating total production cost and hence production overhead becomes an

important element in a product cost. Different methods such as Absorption costing, Variable

costing , Throughput costing , Standard costing and Activity based costing etc can be used for

overhead allocation purposes.

Under the traditional costing method volume based measures such as machine hours or labor are

utilized as cost driver for allocating production overhead cost. Such type of costing system was

suitable in those days where companies were manufacturing narrow range of products and direct

material and direct labor were considered as dominant factory costs. Overhead costs accounts to

small proportion of total production cost and the effect of distortion due to inappropriate

allocation was not significant. Justification of more sophisticated overhead allocation methods

was difficult due to high information processing costs.

In modern world era companies are producing wide range of products and hence direct labor

accounts to small proportion of total manufacturing overhead, whereas overhead costs becomes a

dominant part of total manufacturing cost. Holzer and Norreklit(1991) suggests that the demand

for more accurate product cost has increased due to the increased opportunity cost of having an

inappropriate costing information and decreased cost of operating more complicated cost

systems. So this accounts for the emergence of an alternative approach given by Cooper and

Kaplan, the ABC system. According to Hofstede (1980) and Brewer (1998) the increasing

significance of Asian countries in the world economy and the effect of their different national

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 213

FEBRUARY 2013

VOL 4, NO 10

customs on corporation management, both propose that more research on ABC in the Asian

environment is necessary.

Companies in Pakistani textile sector are following the usual costing system and are thus not able

to identify the cost behavior and cost of each product and are just relying on the overall

profitability of the company, so there is a need to switch to an another improved costing system.

Not much research work has been done on the assessment of ABC system in Pakistan

specifically with respect to Pakistani Textile sector. This study focuses on the costing system

followed by textile sector in Pakistan and incorporates a wide range of problems into one case

study such as rate of adoption of ABC costing by the textile sector of Pakistan by identifying the

implementers, supports, non implementers and unawares. Further the reason for non

implementation and why management is motivated to implement ABC system in future was also

analyzed.

1.1 Research Problem

ABC system is not very much popular in Pakistani manufacturing sector , specifically in the

textile sector as currently very few companies are following this system. Most of the prior

researches had been carried out among corporations in Western world while the practice of ABC

implementation and execution in other part of the world is often overlooked. Companies in

Pakistani textile sector are usually following the old conventional costing system or are not

following any appropriate costing system due to which they are not able to identify the cost

behavior and cost of each product.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 214

FEBRUARY 2013

VOL 4, NO 10

1.2 Research Objective

This study aims to determine the costing system followed by textile sector in Pakistan and

incorporates a wide range of problems into one case study such as,

To identify the adoption rate of ABC by textile sector of Pakistan by classifying it as

implementers supports, non implementers, unawares.

To identify the reasons for not implementing ABC.

To identify the reasons as to why management is motivated to implement ABC system in

future

2. Literature Review

2.1. Need of ABC system

According to Jensen and Meckling (1992), the main purposes of the managerial accounting are

to provide control by reducing conflict, to attach the policy to resources allocation and to aid the

company‟s internal coherence.

Cooper (1987) identified that the due to the increasing ratio of manufacturing overhead in

product cost, using direct labor hours or costs (volume-based allocation bases), results in

incorrect cost allocation. Cooper (1988) had further analyzed that due to increasing

diversification in volume of product, size and complexity the significance of cost distortion

under the traditional costing system has increased. Other studies also show same results (Turney,

1991; Cooper and Kaplan, 1991; Turney and Stratton, 1992).

Raffish (1991) surveyed production industries in the USA and identified that the proportion of

production overhead was around 30% to 50%, whereas direct material accounted to about 45%

to 55% in the product cost. Cost of direct labor was around 5% to 15% of product costs.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 215

FEBRUARY 2013

VOL 4, NO 10

Traditional costing system is one of the methods used to compute the cost of a product but this

system was suitable in those days where companies were manufacturing narrow range of

products and direct material and direct labor were considered as dominant factory costs.

In modern world era companies are producing wide range of products by using more complex

and automated systems, hence direct labor accounts to small proportion of total manufacturing

overhead whereas overhead costs becomes a dominant part of total manufacturing cost. Holzer

and Norreklit (1991) suggests that the demand for more accurate product cost has increased due

to the increased opportunity cost of having an inappropriate costing information and decreased

cost of operating more complicated cost system. So this accounts for the emergence of an

alternative approach given by Cooper and Kaplan, the ABC system. Need of accurate cost

information was one of the major reasons for adopting ABC. Other reasons include

modernization of current cost accounting system, correct allocation of indirect cost, proper

budgeting, cost control and reduction.

2.2. What is ABC system?

ABC identifies that the majority of costs are not fixed in long run and it tries to understand the

reasons due to which changes in cost occurs over the period. It allocates cost to each product or

service according to the time consumed or activity utilized etc. Thus this system works on the

basis of causality which results in improved computation of cost, aid in effective decision

making and serves as a yardstick for other management decisions.

C.B. Wessels a and F. Vermaas b (1998) concluded that ABC is useful as it enhances the

planning, decision making and control capabilities of management but it is a costly

management accounting system as high levels of details are necessary for its proper operation.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 216

FEBRUARY 2013

VOL 4, NO 10

Proper cost/benefit analysis needs to be done before implementing any management accounting

system.

ABC system is considered more useful as compared to traditional costing in, measuring product

cost, identifying profit and understanding cost drivers. Investment in advance manufacturing

technologies can be evaluated and its implementation may also results in better planning and

control of cost.

ABC system requires first to identify activities with in an organization in order to identify the

cost driver related to that activity. Cost pools are generated from which cost rates are determined

and charged to products accordingly.

According to Carsten (2001) selecting cost drivers is an important issue in implementing ABC

system as precision must be traded off against the complexity of the system. On one hand, a high

precision in allocating factory overhead costs often requires a large number of cost drivers while

on the other hand, a small number of cost drivers are necessary to attain acceptable level of cost

information and to make the ABC system easily understandable for management. So the selected

cost drivers also bear the cost of drivers which are not selected.

ABC system uses cost drivers at unit, product, batch and facility level to allocate cost as

compared to conventional costing system which just uses unit level characteristics of goods.

2.3. ABC system around the Globe:-

According to Innes and Mitchell (1991) the adoption rate is about 10% in UK, while as per

Armitage and Nicholson (1993) it was 14% in Canada during the same period. According to

Green and Amenkhienan (1992) adoption rate in US companies were more than UK. Later Groot

(1999) investigated and showed that it was 17.7% in US while as per Frey and Gordon (1999) it

was 24.4%. As per Chenhall and Langfield-Smith (1998) and Brown et al., (2001) investigation

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 217

FEBRUARY 2013

VOL 4, NO 10

adoption rate in Australia ranges from less than 12% to 56%.Research conducted by Bescos et

al.,( 2001) in Canada and by Joshi ( 2001) in India showed that the ABC adoption rate is 23.1 %

and 20% percent, respectively. Finally, according to Bescos et al., (2001) investigation in Japan

showed that about 7% of the companies have adopted it, but interest showed that adoption rate

can increase up to 34.5%.

Cohen, Venieris and Kaimenaki (2005) surveyed and collected evidences regarding ABC

implementation and suggested that though there has been an increasing rate of awareness of

ABC over the past decade, but the overall implementation rate is low. They conducted an

empirical research on 88 Greek companies that belongs to manufacturing, services and retail

sector. They indentified four categories with regard to ABC. (adopters, supporters, deniers and

unawares). They also investigated the reasons that influence the companies decision of changing

their existing cost accounting system even after encountering many problems in ABC

implementation such as doubt of management regarding the effectiveness of new system and

inadequate resources etc.

Research findings suggest that companies have not adopted ABC due to high implementation

cost, lack of support from management and companies‟ satisfaction with their existing system.

Companies had also considered its future adoption to improve cost control, to use it as superior

performance measures, to conduct more accurate analysis of customer profitability and for more

refined decision making etc.

Researchers were also surprised to find that senior accountants of some largest Greek companies

were unaware about ABC system and its philosophy.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 218

FEBRUARY 2013

VOL 4, NO 10

2.4. Application of ABC system in different industries

According to Messner (2009) for the public sector, ABC is an alternative to improve the

inefficiencies of conventional system and also to build up their responsibility level as the

generated information can help the business to explain, defend and take responsibility for what

have been done.

Rong, Thomas, Wen-Ying and Chao-Hsin (2009) discussed the case of implementation of ABC

in a textile company. They analyzed the reasons as to why the ABC was not implemented and

not reached to the action phase. According to them the main reasons of failure were the lack of

management support, IT support, education and training. However lack of performance based

incentives, lack of MIS staff and improper inventory management were also some of the reasons

that contributed towards the postponement of ABC implementation. Companies management

was focused more on efficiency advancement and brand name and did not considered altering the

performance plan associated with ABC implementation.

Nachtmann and Hani Al-Rifai (2010) has analyzed the application of ABC system in AC

manufacturing industry and found out that about 55% of their production overhead were related

with material handling activities and hence traditional costing system would distort the cost

results. So ABC system was implemented which also indicated that overhead is not consumed by

product on volume basis as represented by their existing system (Traditional costing). The

analysis of ABC indicated that out of 7 products 3 are in loss at current market price. Much of

the ABC system depends upon the quality and amount of available data. The overhead rates used

by ABC would not be appropriate if there is a major change in product or process and hence they

need to be updated. Further, ABC system required to be updated if new product line is added or

subtracted. Spreadsheet was used for ABC as it can be efficiently updated.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 219

FEBRUARY 2013

VOL 4, NO 10

Suthummanon, Ratanamanee, Boonyanuwat and Saritprit (2011) have studied the application of

ABC on a furniture factory and stated that it helps management to spot expensive and

unprofitable products. This information is important from management point of view as it will

help in the reduction and elimination of non value added activities of such manufactured

products by applying additional industrial engineering methods. They further analyzed that as

ABC system is labor intensive and time consuming process its success depends upon the

complete participation of every part of the organization. Management who identifies the need for

implementing the system may be hesitant of the changes brought by ABC and may oppose the

same. Hence in these situations important improvement opportunities may be missed. Therefore

consideration needs to be given to such resistance.

3. Research Methodology

In order to accomplish these tasks a questionnaire was developed and handed over to the finance

and accounts staff of the different textile companies. They were asked to reply to the

questionnaire on their perceptions, experiences and understanding. Telephonic and personal

Interviews were also conducted The questionnaire was send to about 60 textile companies out of

which 42 responded, which accounts to 70% response rate.

Initially the response rate was very low. To increase the response rate accounts and finance staff

members were phoned, requesting them to complete the questionnaire. The telephonic interviews

resulted with an interesting feedback as to why the accounts and finance employees had not

replied to the initial e-mail sent. Following are some of the reasons:

They don‟t have any idea about ABC system.

They were busy with the monthly reporting.

The questionnaire was too much lengthy.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 220

FEBRUARY 2013

VOL 4, NO 10

The required information in the survey was too sensitive for the company.

Their company‟s SOP does not allow leaking such information.

They are not in practice of participating or completing in such type of surveys

3.1. Questionnaire Design

This study aims at determining the costing system followed by textile sector in Pakistan and

incorporates a wide range of problems into one case study such as it aims

To identify the adoption rate of ABC by textile sector of Pakistan by classifying it as

Implementers, Supports, Non implementers, Unawares.

To identify the reasons for not implementing ABC.

To identify the reasons as to why management is motivated to implement ABC system in

future

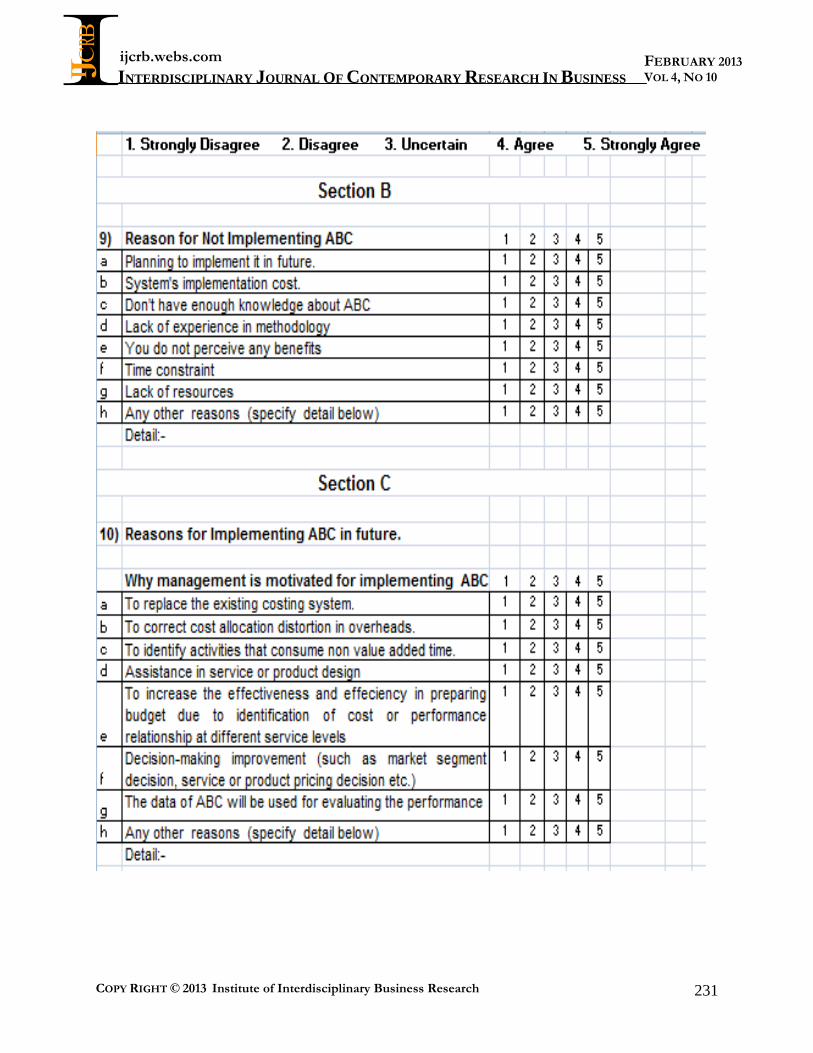

The questionnaire consists of three sections namely A, B, and C which were designed to gain

some general and specific idea of respondents and they also represent 3 objectives of this

research.

Most of the questions were close ended as the close ended questions have guided replies that

may encourage the participants to have more interest in answering the questions. Key questions

were based on Likert-type scale. Factors influencing the reasons for not implementing ABC and

as to why management was motivated to implement ABC system in future were scored on a five-

point numerical scale from 1 represents = strongly disagree to 5 represents = strongly agree.

Some questions of section A were comprised of Yes or No options and also on a on a five-point

numerical scale, from 1 represents = not at all satisfied to 5 represents = highly satisfied.

Questions included in section A were devised to get the idea of size of the company, costing

system followed by them and their satisfaction level with their current costing system if other

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 221

FEBRUARY 2013

VOL 4, NO 10

than ABC system. Section B was aimed to identify the reasons for not implementing ABC,

whereas section C identifies the perceptions of the employees regarding the reasons as to why

management is motivated to implement ABC system in future.

4. Data Analysis and Results

4.1. Data Analysis Techniques

For this study, along with the mean values, graphs and tables are also used to answer the research

questions. The most significant outcomes are discussed briefly.

4.2. Discussion of the results

Following graphs shows the result of section „A‟ which consists of 8 questions in which general

idea of size of the company, the satisfaction level of employees with the current costing system

followed by them and the adoption rate of ABC system by textile sector of Pakistan was

analyzed.

Figure 1 shows the size of companies in term of annual sales turnover. It is evident from Figure 1

that out of 42 respondents companies 32 companies which accounts to 76% have annual sales

turnover of greater than 299 million. Only 5 companies (12%) out of 42 companies are currently

following ABC system whereas 37 (88%) are not currently following this system as shown

figure 2. One reason for this is that, accountants of 13 (31%) companies even don‟t have any

idea of ABC system which is evident from Figure 3.

Figure 4 clearly depicts that most of the companies i.e. 28 (67%) are still following the old

conventional (Absorption) costing system, followed by standard costing which is used by

7companies (17%).

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 222

FEBRUARY 2013

VOL 4, NO 10

Figure 5 shows the adoption rate of ABC system which is classified under the head of non

implementer (43%), Unawares (31%), Supporters (14%) and implementers (12%).

All mean values in Table 1 are significant that is greater than 3 which shows that respondents are

satisfied with their current costing system (other than ABC system) and thinks that their current

costing system is successful in capturing correct cost information in gaining insight about

manufacturing performance.

In Section B of questionnaire, reasons for not implementing ABC were inquired from

respondents. It is evident from the results of Table 2.above that system implementation cost

mean value (3.17) and time constraint (mean value 3.46) are the two main reasons for not

implementing ABC system. Some other reasons which were mentioned by respondents are:-

Mindset of the organization

Satisfied with current costing system

Non qualified accountants

Lack of management support.

However 6 textile companies are planning to implement ABC system in future for which all

reasons mentioned in table 3 seems to be significant. It means that they are all agreeing on the

reasons mention in table 3 due to which management is motivated to implement ABC system in

future. Two reasons i.e. to correct cost allocation distortion in overheads (mean value 4.17) and

to identify activities that consumes non value added time mean value (4.17) are the most

significant ones.

5. Implications

Companies in Pakistani textile sector are following old conventional costing system due to which

appropriate cost of each product and their cost behavior can not be identified. So these

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 223

FEBRUARY 2013

VOL 4, NO 10

companies are just relying on the overall profitability of the company. Management should

change their mindset and switch to another improved costing system i.e. ABC system in order to

compute the true cost of product.

Strong active support of management is vital in the successful implementation of any system.

Dedication is also one of the most important factors. Top management should not only provide

all the means of implementation and required resources but also provide active support to

employees for the successful implementation of ABC system.

Hiring of well qualified professional accountants is also very much important for those

companies who are trying to implement ABC system in future.

6. Future Research

The research indicates that some companies are in planning phase of their ABC implementation.

Future research on implementation process and pros and cons of ABC can be done with respect

to textile sector of Pakistan. Case study approach can be used so that the comparison of product

cost can be done under two costing systems i.e. Traditional and ABC system.

Further same type of research can be done on other manufacturing retail and service sectors so

that the general idea of Pakistani environment regarding ABC system can be obtained.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 224

FEBRUARY 2013

VOL 4, NO 10

References

Armitage H.M. and Nicholson, R. (1993), “Activity based costing: a survey of Canadian

practice”, No. 3, Society of Management Accountants of Canada.

Brewer, P.C. (1998), “National culture and activity-based costing systems: a note”, Management

Accounting Research, Vol. 9, June, pp. 241-60.

Bescos, P., Cauvin, E., Gosselin, M. and Yoshikawa, T. (2001), “The implementation of ABCM

in Canada, France and Japan: a cross-national study”, paper presented at the 24th Annual

Congress of the European Accounting Association, Athens, 18-20 April.

Brown, D., Booth, P. and Giacobbe, F. (2001), “Organizational influences, ownership, and the

adoption of activity based costing in Australian firms”, Working Paper No. 46, School of

Accounting, University of Technology, Sydney, June.

Carsten Homburg (2001) “A note on optimal cost driver selection in ABC Management

Accounting Research” vol. 12, pp. 197–205

C. B. Wessels & H. F. Vermaas (1998) “A management accounting system in sawmilling using

activity based costing techniques” The Southern African Forestry Journal, 183:1, pp. 31-35

Chenhall, R. and Langfield-Smith, K. (1998), “Adoption and benefits of management accounting

practices: an Australian study”, Management Accounting Research, vol. 9, pp. 1-19.

Cohen S, Venieris G, Kaimenaki E, (2005),"ABC: adopters, supporters, deniers and unawares",

Managerial Auditing Journal, vol. 20 Iss: 9 pp. 981 – 1000

Cooper, R. (1987), “Does your company need a new cost system?” Journal of Cost

Management,Spring, pp. 45-9.

Cooper, R. (1988), “The rise of activity-based costing – part one: what is an activity-based cost

system?” Journal of Cost Management, Summer, pp. 45-54.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 225

FEBRUARY 2013

VOL 4, NO 10

Cooper, R. and Kaplan, R.S. (1991), The Design of Cost Management System, Prentice-Hall,

Englewood Cliffs, NJ.

Frey, K. and Gordon, L.A. (1999), “ABC, strategy and business unit performance”, International

Journal of Applied Quality Management, vol. 2 No. 1, pp. 1-23.

Green, F.B. and Amenkhienan, F.E. (1992), “Accounting innovations: a cross-sectional survey of

manufacturing firms”, Journal of Cost Management, vol. 6, pp. 58-64.

Groot, T.L.C.M. (1999), “Activity based costing in US and Dutch food companies”, Advances in

Management Accounting, vol. 7, pp. 47-63.

Hofstede, G. (1980), “Culture‟s Consequences: International Differences in Work-Related

Values” Sage, Newbury Park, CA.

Holzer; H.P. and Norreklit, H., (1991), “Some Thoughts on Cost Accounting Developments in

the United States” Management Accenting search, (Academic Press, U.K.).

Innes, J. and Mitchell, F. (1991), “Activity based costing a survey of CIMA members”,

Management Accounting, October, pp. 28-30.

Jensen, M.C., and Meckling, W.H. (1992), “Specific and General Knowledge and Organizational

Structure” Contract Economics, ed. Lars Werin and Hans Wijkander in Jensen, M.C., 1988.

Foundations of Organizational Strategy, Harvard University Press.

Joshi, P.L. (2001), “The international diffusion of new management accounting practices: the

case of India”, Journal of International Accounting, Auditing and Taxation, vol. 10 No. 1,

pp. 85-109.

Messner, M. (2009), “The limits of accountability. Accounting, Organizations and Society” vol.

34 pp. 918-938.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 226

FEBRUARY 2013

VOL 4, NO 10

Nachtmann H. & Hani Al-Rifai (2004), “An Application of activity based costing in the air

conditioner manufacturing industry” The Engineering Economist: A Journal Devoted to the

Problems of Capital Investment, 49:3, pp. 221-236

Ness,Joseph A.and Thomas G.Cucuzza, (1995), “Taping the potential of ABC” Harward

Business Review,vol.73, Issue.4, July-August

Raffish, N and Turney, P (1991). “Glossary of Activity-Based Management”, Cost

Management Journal, Fall, pp. 53-63.

Suthummanon S., Ratanamanee W., Nirachara B.& Saritprit P. (2011), “Applying Activity-

Based Costing (ABC) to a Parawood Furniture Factory” The Engineering Economist: A

Journal Devoted to the Problems of Capital Investment, 56:1, pp.80-93

Turney, P.B.B. (1992), “What an activity-based cost model look like?” Journal of Cost

Management, Winter, pp. 54-60.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 227

FEBRUARY 2013

VOL 4, NO 10

Annexure

Figure I

Figure II

Figure III

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 228

FEBRUARY 2013

VOL 4, NO 10

Figure IV

Figure V

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 229

FEBRUARY 2013

VOL 4, NO 10

Table 1

Table 11

Table III

1. Significance of Study

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 230

FEBRUARY 2013

VOL 4, NO 10

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 231

FEBRUARY 2013

VOL 4, NO 10