Iglo Foods Holdings Limited/media/Investor Relations Documents/Annual report... · Net Sales of the...

77

Iglo Foods Holdings Limited Annual Report & Financial Statements 2014

Transcript of Iglo Foods Holdings Limited/media/Investor Relations Documents/Annual report... · Net Sales of the...

Iglo Foods Holdings Lim

ited Annual Report &

Financial Statements 2014

Iglo Foods Holdings Lim

ited Annual Report &

Financial Statements 2014

A fresh look at frozen

Iglo Foods Holdings LimitedAnnual Report & Financial Statements 2014

We create great tasting food to be enjoyed every day, at

every meal, by everybody. Our food is always delicious,

good for you and easy to prepare. Because our food is less

wasteful it helps people feel better about what they eat.

At Iglo our dream is to make mealtimes the best moments

of the day and everything we do is designed to inspire

more people to enjoy better meals together.

is to make B E T T E R M E A L S

T O G E T H E R

THE MISSION OF IGLO GROUP

Contents

GOVERNANCE

30 Board of Directors32 Strategic Report33 Directors’ Report34 Statement of Directors’

Responsibilities

BUSINESS OVERVIEW

01 Financial and operational highlights02 Our business at a glance04 Chairman’s Statement06 Chief Executive Officer’s Review08 Business Review16 Brand Reviews19 Corporate Social Responsibility22 Chief Financial Officer’s Review

FINANCIAL STATEMENTS

34 Independent Auditors’ Report to the Members of Iglo Foods Holdings Limited

36 Consolidated Income Statement36 Consolidated Statement of

Comprehensive Income37 Consolidated Statement

of Changes in Equity38 Consolidated Statement

of Financial Position39 Consolidated Statement

of Cash Flows40 Notes to the Financial Statements72 Glossary72 Other Information

2014 Highlights

Gross margin of the Iglo Group business increased by 1.8ppts to 35.3% (at constant currency exchange rates)

GROSS MARGIN 2014

2013

2012

2011

2010

33.5%35.3%

34.7%

33.2%34.4%1.8ppts

Net Sales of the Iglo Group business decreased by 1.9% to €1,469.5 million (at constant currency exchange rates)

NET SALES €m 2014

2013

2012

2011

2010

1,469.5 1,498.5

1,569.0 1,548.1

1,541.8 -1.9%

EBITDA before exceptional items decreased by 0.1% to €297.8 million (at constant currency exchange rates)

EBITDA €m 2014

2013

2012

2011

2010

298.0 297.8

342.1

304.1 325.3 -0.1%

Net Debt (excluding investor funded loan notes) decreased during the year as a result of the refinancing

NET DEBT €m 2014

2013

2012

2011

2010

1,514 1,414

1,629

1,559 1,410 -100m

Operating cash flow conversion of 90% was generated at reported exchange rates

OPERATING CASH FLOW CONVERSION

2014

2013

2012

2011

2010

97%90%

87%

127%106%

The reported average €/£ exchange rate for 2014 was 1.24. The constant currency results have been determined by translating the local currency denominated results for the year ended 31 December 2014 and for earlier comparative years to the 2014 budgeted €/£ exchange rate of 1.16.

Net Debt is defined as total bank and bond debt less cash and cash equivalents.

Decrease 2013-2014 Decrease 2013-2014

Increase 2013-2014

Decrease 2013-2014

Business highlights

• Launched three new innovation platforms - Inspirations, Steamfresh and Stir Your Senses

• Inspirations ranked as the UK’s best-selling new innovative FMCG launch in 2014 by Kantar

• Grew Net Sales in 8 out of 12 markets with a 5th successive quarter of growth in Italy

• Launched our Food of Life campaign with a new brand positioning, new packaging design, new advertising and omnichannels, plus digital focus, supported by A&P spend + 11% year-on-year

• Best-in-class models developed for digital engagement, Perfect Store shopper experience and portfolio mix management

• Launched our Forever Food Together CSR programme with particular focus on the role frozen can play in reducing food waste

Financial highlights

• Reported Net Sales broadly flat year-on-year; -1.9% in constant currency versus category trend of -0.5%, reflecting difficult market conditions in the UK and Germany

• Gross margin increase of 1.8% year-on-year to 35.3%

• Constant currency EBITDA broadly flat; 20.3% margin in line with our strategic target

• 4th successive year of negative working capital; operating cash conversion of 90%

• Net Debt reduced by €100m year-on-year; leverage reduced to 4.6x (2013: 5.0x)

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 1

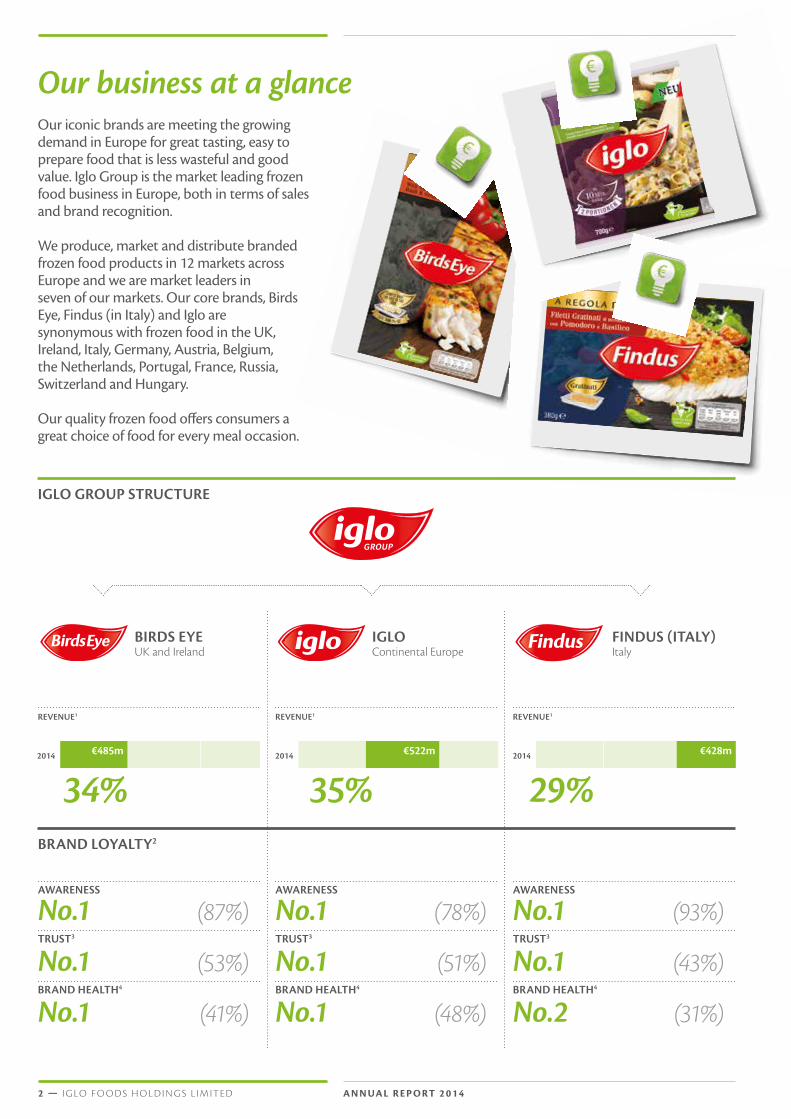

BRAND LOYALTY2

AWARENESS

No.1 (87%) AWARENESS

No.1 (78%) AWARENESS

No.1 (93%) TRUST3

No.1 (53%) TRUST3

No.1 (51%) TRUST3

No.1 (43%) BRAND HEALTH4

No.1 (41%) BRAND HEALTH4

No.1 (48%) BRAND HEALTH4

No.2 (31%)

IGLO GROUP STRUCTURE

Our business at a glanceOur iconic brands are meeting the growing demand in Europe for great tasting, easy to prepare food that is less wasteful and good value. Iglo Group is the market leading frozen food business in Europe, both in terms of sales and brand recognition.

We produce, market and distribute branded frozen food products in 12 markets across Europe and we are market leaders in seven of our markets. Our core brands, Birds Eye, Findus (in Italy) and Iglo are synonymous with frozen food in the UK, Ireland, Italy, Germany, Austria, Belgium, the Netherlands, Portugal, France, Russia, Switzerland and Hungary.

Our quality frozen food offers consumers a great choice of food for every meal occasion.

BIRDS EYEUK and Ireland

IGLO Continental Europe

FINDUS (ITALY)Italy

REVENUE1 REVENUE1 REVENUE1

2014 2014 2014€485m €522m €428m

34% 35% 29%

2 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

CLEAR NO. 1 IN EUROPEAN FROZEN FOOD5

Direct market access

Access via distribution

Not present

1

1

1

1

1

1

1

2

Iglo Group 9.2%

Oetker-Gruppe 4.2%

Findus Group 4.0%

Nestlé SA (incl. Wagner) 3.8%

McCain Foods Ltd 2.9%

STRONG LEADERSHIPMARKET SHARE %

2.2X

Source: Company information, Euromonitor, AC Nielsen, IRI, Ipsos.(1) Revenues are in constant currency for the year ended 31 December 2014. Relates to frozen food market. Iglo values shown are

results in Germany.(2) Relates to frozen food market.(3) December 2014 YTD average. Trust % based on questionnaire: thinking about the food brands shown here, please consider

each of the statements based on 5 of participants below and for each one please indicate which brands you think it applies to. You can indicate as many brands as you like for each statement. Which of these... is a brand I trust?

(4) Brand Health at December 2014. Source: Ipsos.(5) Relative position to No.2 branded competitor as per Nielsen and IRI data.

Net Sales growth in 8 out of 12

markets

8 out of 12

Fina

ncia

l sta

tem

ents

Gov

erna

nce

Busi

ness

ove

rvie

w

I G LO F O O DS H O L D I N G S L I M IT E D — 3

2014 was another tough year for the branded frozen food category in Europe. Difficult economic conditions, constrained shopping budgets and an evolving retail environment created challenges for our sector as a whole. They contributed to a disappointing decline in overall sales for Iglo.

However, our success in repositioning the company for growth, and the momentum we have started to build in a number of markets, strongly suggests that our strategy is starting to deliver some positive results.

This has been a year of change for our business, in which our people have responded very positively to the journey we are taking, and the immediate challenges that we face. In the pages of this report, you will read about the progress we’ve made in changing how our consumers relate to our brands, changing how we innovate and bring new products to market, and changing how we work together. We’ve evolved our culture to be more externally focused, ready to compete more effectively: not just in frozen, but whenever somebody decides which meal to prepare, and which food to put on the plate.

The 1.9% decline in sales on a constant currency basis suffered by Iglo as a whole reflects the challenging trading environment for branded frozen food across Europe. It also reflects the one-off benefit in the red meat category in the prior year, where many own-label competitor products were withdrawn from shelves in 2013 following the horsemeat scandal, but returned in 2014. Market conditions are expected to remain challenging in the near future, but the innovations that we are bringing to market will position us well to overcome these challenges. We improved our gross margin by 180 basis points during the year and maintained our EBITDA performance. The improved margin performance has been reinvested in the business through increased media spend behind the roll out of the new Food of Life campaign and the innovation launches.

Erhard Schoewel Chairman

We’ve evolved our culture to be more externally focused, ready to compete more effectively: not just in frozen, but whenever somebody decides which meal to prepare, and which food to put on the plate

A transformative yearCHAIRMAN’S STATEMENT

Frozen food over-trades by up to 200% online200%

4 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

We succeeded in growing Net Sales in 8 of the 12 markets where we operate. Our new innovation platforms emerged as our primary drivers of sales growth, and our more collaborative, cross-functional approach to operations has helped us to find new efficiencies and grow our margins.

In Italy, where we were able to launch our new branding and Better Meals Together strategy in the final quarter of 2013, we have now delivered five consecutive quarters of Net Sales growth. In markets such as Portugal, we’ve proved that innovation can grow sales even in tough economic conditions. In the Netherlands and Belgium, we’ve shown how a new approach to management can transform performance from negative to positive. Meanwhile, in the UK, we have continued to grow our share of online sales. As online shopping spreads across Europe over the next few years, the expertise that we have established bodes well for Iglo.

We have strengthened our management team to continue to drive our new vision forward – and the fact that 6 out of 15 senior management roles have been filled from within Iglo shows the strength of our talent pipeline. We’ve renewed our marketing function during the year, and embedded a new strategic framework for identifying opportunities and guiding innovation that gives us a clarity of purpose across all that we do.

We are committed to managing our portfolio effectively and we have done so by discontinuing lines that delivered sales but little profit. Measures such as this have had an additional negative impact on our sales during the year – but they position our business far more strongly for sustainable, profitable growth in the future.

We have continued to reduce Iglo’s net external debt whilst investing in the innovation that will drive growth over the coming years. Iglo remains extremely focused on cash generation and ended the year with negative working capital for the fourth successive year.

In July, we completed a refinancing of the Group’s Senior debt, replacing the existing facilities with two new tranches of Senior debt of €620 million and £400 million respectively. In addition, the Group issued a €500 million floating rate bond on the Luxembourg Stock Exchange. The maturity on all of the Group’s debt now extends to 2020 and the new debt arrangements are expected to deliver annual interest savings of around €14 million.

Market conditions will continue to be tough in 2015. However, the innovation platforms and new systems and processes that we have introduced are equipping Iglo well to deal with these challenges. We are building a nimbler, leaner and more competitive business. And the momentum that we have established behind our innovative new brand and products will continue to help mitigate the effects of the overall economic environment.

We succeeded in growing Net Sales in 8 of the 12 markets where we operate

Stir Your Senses allows home cooks to simply stir the ingredients to gradually unlock aromas, colours and tastes from around the world.

Our team in the Netherlands has set a new world record by creating the biggest fishfinger.

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 5

Elio Leoni Sceti Chief Executive Officer

Our mission is to make Better Meals Together, and between them, those three words capture every aspect of the journey our business is making

A fresh look at frozenCHIEF EXECUTIVE OFFICER’S REVIEW

Frozen food is 47% less likely to be wasted than fresh or chilled47%

Last year, one in ten of the meals prepared in European homes included some frozen food. But that’s only part of the story. For every one of these meals that included frozen food, there were another three when the person choosing the food thought about making frozen a part of the meal – but decided against it. The maths is simple – and it adds up to a huge opportunity for Iglo.

If we can persuade people to take a fresh look at frozen, to use it on those extra three occasions when it doesn’t yet make it onto the plate, then we can significantly grow the size of our business.

In the last financial year, we have taken our first steps towards persuading both consumers and our retail partners to take that fresh look at frozen. This has not grown the size of our business overnight. But it has given us unmistakable momentum in the markets where we’ve rolled out our new strategy. Our mission is to make Better Meals Together, and between them, those three words capture every aspect of the journey our business is making.

To make our food ‘Better’, we need to innovate – and innovate responsibly. We’ve done this by developing innovation platforms: new eating experiences that address the emotional needs around food that people in all of our markets share. We are inviting those people to prepare and enjoy our food in different ways – and we’ve promised them that the new recipes we develop will offer a healthier choice. Our results for this year show that innovation is now the fundamental driver of growth for our business.

To grow frozen’s share of the plate, we’re encouraging both consumers and retailers to think differently about the role it plays within ‘Meals’. We’re doing this through our new, European-wide advertising campaign, Food of Life, which elevates the role of our brand in people’s daily lives and evolves it from a functional choice to an emotional one. We’re doing it too through innovative digital marketing that presents our food in new contexts, and links it to other purchases to help show the range of occasions when frozen can make meals better. Our results show that this approach is working. We’ve grown our Net Sales in 8 out of 12 markets during the year.

To succeed, we need to take this journey ‘Together’, building a high-performance organisation that can deliver excellence in all areas, and compete effectively against all of the food choices that consumers have. During 2014 we strengthened our senior management team, with 6 out of 15 roles filled from within Iglo, and brought in important new skills in areas such as digital marketing. We’ve reinvigorated our values to help bring our organisation together and make it more competitive.

6 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

BETTER MEALS TOGETHER

INNOVATION

EXCELLENT EXECUTION

OUR BRAND

PEOPLE & CULTURE

INSPIRED BY CONSUMERS

ENABLED BY ONE

IGLO WAY

Our strategy rests on four growth pillars:

We are building a relevant brand, driven by consumer insight, which grows the frozen category and positions our solutions at the heart of meal occasions.

We will deliver big, bold innovation that challenges assumptions about frozen, introduces us to new meal occasions and enhances margins by adding value for consumers.

Our people and culture are driven by high-performance, with rewards aligned to our strategic goals and a structure that enables employees to focus on core areas of expertise.

We are organised around excellent execution, removing duplication, sharing best practice across markets and ensuring delegated decision-making and empowered accountability.

Persuading people to take a fresh look at frozen involves working together with other organisations as well. Our Forever Food Together Corporate Social Responsibility programme is helping to make this happen.

We’ve pioneered new ways of working that bring people together across our teams to deliver innovative solutions in innovative ways. By challenging ourselves we have been able to boost NPD and gross margin, and invest to maintain our EBITDA, whilst supporting our strategy and maintaining our commitment that all our food must be responsibly sourced and prepared.

Persuading people to take a fresh look at frozen involves working together with other organisations as well. Our Forever Food Together Corporate Social Responsibility programme is helping to make this happen. We know that frozen offers an inherently more sustainable choice that can dramatically reduce waste at all points in food’s journey to the plate. We know that it enables us to make more sustainable choices in food sourcing, and that it has a vital role to play in better managing our planet’s natural resources. We are committed to working with a range of partners to help raise awareness of these sustainability benefits.

Over the next few pages, we’ll take a closer look at the progress we have made in rolling out our new Better Meals Together strategy under the four organisational pillars of our business: Our Brand, Innovation, People and Culture, and Excellent Execution.

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 7

K E Y achievements

Our BrandBUSINESS REVIEW

This has been a transformative year for Iglo’s brand building and consumer connections. We have brought in proven leaders, rooted our brand strategy in the emotional relationship that people have with food, and launched a pan-European advertising campaign that brings this strategy to life effectively and efficiently across markets and media channels.

In April we welcomed Luca Miggiano as Iglo’s new Chief Marketing Officer. Luca has pioneered a powerful new approach to identifying the most relevant opportunities for Iglo. Under our new ‘Consumer Game Board’ framework, we analyse the occasion-based needs that people have around food, and identify those that Iglo can play a credible role in satisfying. This strategic approach confirms key elements of our position in the market: a provider of family and adult favourites, but not of snacks; a provider of authentic and natural food, rather than treats. And it has helped to unite all pillars of our business around a cohesive and consistent approach. Already, at the end of our first year of making Better Meals Together, consumers are beginning to have a clearer idea of what Iglo stands for.

Our advertising has played a big part in getting the message across. We rolled out our Food of Life advertising campaign across our markets, with more than 30 localised TV executions on air by the end of the year. In most markets, we complemented our TV campaign with other media including topical online video advertising that related our food to key moments such as the FIFA World Cup.

The values at the heart of our Better Meals Together strategy are reflected in everything we do when we communicate with our consumers. During 2014 we launched a new look and feel to our brand, including a new packaging design, created to boost on-shelf impact, product and brand recognition and consumer navigation of the category. We rolled this out in our four biggest markets in the second half of 2014 where it has been positively received and will continue to roll it out across our remaining markets in the first half of 2015.

When it comes to food, tasting is believing. Our Picture House pop-up restaurants brought the new experiences offered by innovative meal platforms like Inspirations and Steamfresh to life, and generated significant social media awareness in markets like the UK, by inviting consumers to upload pictures of their food. At the same time, we have launched an extensive sampling campaign targeted around retailers, to persuade shoppers to try our new Stir Your Senses meal experiences in a location where they can easily follow up by buying them.

• Renewal of our marketing expertise with key senior appointments

• A new strategic framework for planning and executing campaigns

• Launch of Food of Life advertising platform across all media channels in Europe

• Launched a new brand positioning across our markets, including a new packaging design

• Enhanced digital capability, including new appointments, resulting in initiatives such as Picture House pop-up restaurants to grow social media awareness

• Central role for Forever Food Together

• Net Sales growth in 8 out of 12 Iglo markets

8 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

Our TV advertising has played a big part in getting our message across. We rolled out our ‘Food of Life’ advertising campaign across our markets, with more than 30 localised executions on air by the end of the year.

We have launched an extensive sampling campaign, to persuade shoppers to try our new meal experiences.

Our Picture House pop-up restaurants brought the new experiences offered by innovative meal platforms and generated significant social media awareness to life.

We also began to move the sustainability benefits of frozen, and our Forever Food Together campaign, towards the centre of our brand story. Our Green Captain Forever Food Together icon now appears prominently on Iglo packaging – and provides consumers with a link to the Forever Food Together website, where they can find out more about the difference choosing our food can make.

The performance of our three brands, Findus Italy, Birds Eye and Iglo, correlates closely with the length of time for which our new brand strategy has been operating in their markets. In Italy, where we launched our new branding at the start of the year, we have seen consistent growth for Findus Italy, driven largely by new product lines. In the UK, while overall sales were held back by a declining market and a difficult customer environment, our new Birds Eye Inspirations platform (launched in the second quarter) has been ranked by Kantar as the best-selling new innovative FMCG product launched in 2014, reflecting the success of our focus on big initiatives. Our Iglo markets saw a full roll-out later in the year and while early sales of our Stir Your Senses product were encouraging, they were insufficient to return the business to growth.

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 9

K E Y achievements

InnovationBUSINESS REVIEW (cont.)

A close look at our results for 2014 confirms that innovation will be absolutely central to Iglo’s future success. In the markets where we grew sales, that growth was driven primarily by new products.

This is strong confirmation of our strategy, as it proves the appeal of the new concepts we are bringing to market. It is even more exciting in the slightly longer term, as it demonstrates how consumers are happy to take a fresh look at frozen when presented with the right recipes and for the right eating experiences; and it enables us to continue to reposition our business towards higher margin products that deliver a value consumers can recognise.

Our innovation platforms are families of products that introduce consumers to new concepts and experiences when it comes to how they prepare and enjoy their food. Steamfresh delivers crunchy steamed vegetables, side dishes and sauces that can be conveniently prepared in a microwave. Stir Your Senses immerses consumers in the textures and smells of stir-fry cooking to deliver a tasty meal that is quickly ready for the plate. Inspirations delivers premium experiences of fish and chicken through char-grilled flavours and finely balanced sauces.

These successful platforms are the first of many that have emerged from a research and development process that we have reorganised around consumers’ occasion-based needs. Our innovation pipeline has never been fuller than it is today, and this will provide us with the opportunity to continue growing both sales and margin.

Our approach to innovation is built around a commitment that the new products we launch will help consumers to make healthier meal choices. We work closely with our Nutrition Advisory Board, which includes leading European nutrition experts and academics, to make sure that our recipes are created capturing the latest, most informed nutrition advice. And we believe that the inherent nutrition credentials of the ingredients in our innovation platforms has been a big contributor to their success. This is because we focus on the foods that health advisors want people to eat more of like fish and vegetables, making it easier for consumers to achieve a tasty and balanced diet.

• Launch of new innovation platforms: Inspirations, Steamfresh and Stir Your Senses

• Expanded innovation pipeline, reorganised around meal occasions

• Nutrition Advisory Board expanded to strengthen relationships within the European diet and health community to fuel innovation

• Innovation-driven sales performance

1 0 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

Stir Your Senses immerses consumers in the textures and smells of stir-fry cooking to deliver a tasty meal that is quickly ready for the plate.

Inspirations delivers premium experiences of fish and chicken through char-grilled flavours and finely balanced sauces.

Steamfresh delivers crunchy steamed vegetables, side dishes and sauces that can be conveniently prepared in a microwave.

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 1 1

K E Y achievements

People and CultureBUSINESS REVIEW (cont.)

In 2014 we made great strides in aligning our internal culture, and the way we manage our people, around our new strategy for growth.

We sharpened our PACE values to place a greater emphasis on the behaviours that will enable us to compete to win in the broader food market. ‘Performance’ now embodies the concept of “fighting to win”, through harnessing the collective energy of the entire organisation to beat the competition. Our value of ‘Achievement’ now drives harder the concept of personal accountability. While ‘Collaboration’ continues to underscore the ability of the entire organisation and its component parts to work effectively, we are also actively encouraging constructive challenge. This involves the giving and receiving of views with a positive mind-set to help ensure we deliver the best outcome in everything we do. Finally, we are more focused than ever on driving ‘Energy’ and excitement around the huge growth opportunity available to Iglo.

We moved pro-actively to embed these updated values across our business, particularly in the way that we manage our people and reward their performance. We developed a new bonus scheme with improved line-of-sight metrics, which allow us to reward colleagues who have taken ownership for their areas of responsibility and delivered results.

We launched a new recognition scheme, the Iglo Growth Achievement Awards, which include awards for Brand Equity, Innovation, People and Culture and Excellent Execution, reflecting the four organisational pillars of our business. We have also launched further awards around our commitment to Forever Food Together. In 2014 we had more than 400 nominations for these awards.

At the same time, our ‘150 Ideas’ initiative, which we launched last year, has involved all employees in building an innovation pipeline for Iglo. Several ideas generated by the programme are now in development.

• Launched meal occasion based Category Organisation model and recruited new expertise, including digital marketing

• PACE (Performance, Achievement, Collaboration, Energy) internal values refreshed with a new outward focus

• Successfully implemented a new bonus scheme, aligned to group strategy

• Highest ever cultural index score of 60.4 in ‘What’s Cooking?’ survey

• 6 out of 15 new Executive Leadership Team appointments filled through internal applications

• Iglo & Me people portal launched to drive internal engagement and external employer branding

1 2 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

The Iglo and Me people portal launched this year is designed to help our people plan their career progression at Iglo, with transparent information on roles, responsibilities, requirements and rewards.

The Iglo Growth Achievement Awards recognise exceptional individual and team performances.

We sharpened our PACE values to help focus on the behaviours which will drive business results.

The ‘What’s Cooking’ culture survey recorded our highest ever score.

We also launched a new Iglo & Me people portal, which is designed to connect with and engage colleagues across the company. It’s about writing the Iglo story together and equipping everyone with the right tools to develop their career with Iglo.

Developments such as these have helped to improve our employee engagement scores, with our cultural index score moving up 2.4 points to reach 60.4, the highest ever level. The annual engagement survey that generates these metrics has itself been rebranded in line with our group strategy, and is now known as the ‘What’s Cooking?’ Survey.

Where organisational changes have been required to improve efficiencies and support our innovation programme, we have succeeded in implementing significant change, especially in our factories, in a socially responsible manner through our constructive industrial relations with local works councils and unions. By seeking to manage these changes in partnership, we have avoided any significant disruption and achieved considerable operational savings.

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 1 3

K E Y achievements

Excellent ExecutionBUSINESS REVIEW (cont.)

Our strategy cannot succeed without excellent execution. The progress that we have made in several key areas this year shows how that principle is becoming embedded across Iglo.

We have pioneered a new, cross-functional way of working that supports our innovation platforms with an equally innovative approach to planning and managing our supply chains. Our operations team has come together with our research (R&D) and marketing departments to realign the way that we develop and execute the Better Meals Together strategy that we are delivering for our consumers. As a result, we have been able to deliver bigger and better product innovation and increase productivity, whilst reducing waste and redesigning our business around a commitment to responsible sourcing and preparation. The net result is that, even with increases in our A&P investment during the year, we have been able to keep our high EBITDA margin impact, whilst continually improving the quality of our products, as reflected in further decreases in our already low number of consumer complaints.

We have invested in increasing productivity across our supply chain through an approach of integrated end-to-end supply chain management, which is already delivering impressive results. All of our factories are well invested, in particular, our Lowestoft factory in the UK and our Bremerhaven factory in Germany, both of which have executed on our strong new product pipeline with pioneering automated solutions that will deliver future innovation. Both have also delivered fantastic returns in quality and efficiency. At the same time, we have been able to leverage long-term planning with our core warehousing and distribution partners to improve our distribution costs. Our strategic sourcing toolkit is enabling better strategic supplier relationship management and ensuring effective ways of working across the supply chain, from source to plate.

We have been decisive in re-orienting our business around high-margin products and in pulling back from categories that deliver sales but little positive benefit to the bottom line. This has impacted on our sales figures in the short term, but this focus on our sustainable core business is a key enabler of the efficient and effective cross-functional ways of working that are helping to embed executional excellence across our business.

• Cross-functional working supports innovation more effectively

• Portfolio management re-orientates business around high-margin products

• Quality by design programme drives quality and consumer feedback

• 180 basis point growth in gross margin

• Rolled out the Perfect Store format to 11.2% of our target larger stores across nine key markets

• Double digit online sales growth and share up through increased visibility

The Perfect Store format has been rolled out to 606 stores across Europe606

1 4 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

Our Lowestoft factory in the UK has executed on our strong new product pipeline with pioneering automated solutions and also delivered fantastic results in quality and efficiency.

Our Perfect Store programme is improving the atmosphere and orientation of the frozen food aisles in-store.

Improving shopper experience of the frozen category, both in-store and online, is key to successfully redefining the role that our food plays in meal occasions and persuading consumers to take a fresh look at frozen.

Our Perfect Store programme, where we work closely with our retail customers to improve the atmosphere and orientation of the frozen food aisles in-store, has delivered some real successes, particularly in Belgium and Germany, where we have seen sales in stores participating in the programme increase by up to 8% compared to non-participating stores. Our focus for 2015 is to build on this momentum and continue to roll out the programme across Europe, revitalising the frozen aisles and growing the category.

Online grocery sales will be a key driver of future growth for frozen, where we are finding that consumers spend proportionately more on frozen goods when food is bought online. For some retailers we are finding that this can be more than twice as much. Excellent execution is enabling us to grow in line with the market in the UK, where a market survey in 2014 suggested that we are the second most popular online grocery brand by sales value. We have done this by taking a Category Management approach to the channel, with a focus on Brilliant Basics execution and ensuring that our on-site presence is as shopper-focused as possible. Our aim is to deliver a win for all concerned, increasing basket size for the retailer whilst bringing our brand proposition to life in the online space.

Our aim is to deliver a win for all concerned, increasing basket size for the retailer whilst bringing our brand proposition to life in the online space.

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 1 5

Birds EyeBRAND REVIEW

Andrew Weston-Webb Managing Director, Birds Eye UK & Ireland

Conditions have been challenging for the UK grocery market, and for branded frozen food in particular. As the year progressed, shoppers increasingly turned to discounters and established retailers sought to fight that trend with greater focus on pricing and own-label products at the short-term expense of brands.

For Birds Eye, these challenging conditions were exacerbated by extended negotiations with one medium-sized retailer and our decision to discontinue legacy meals that delivered sales but weakened brand image and contributed little profit.

Against this backdrop our Birds Eye brand experienced a 4.6% decline in sales on a constant currency basis during the year.

Another factor impacting sales in the year-on-year comparison was the one-off impact of the horsemeat scandal in the previous year, when many own-label competitors in the burger category disappeared from shelves. Birds Eye products, which remained on shelf throughout the crisis, consequently delivered significantly higher sales than in a normal year.

Amid these tough market conditions, our new innovation platforms and Food of Life brand campaign have received a positive response from the market, with Inspirations chicken and char-grilled fish leading the way. Kantar has ranked the Inspirations launch as the best-selling new FMCG product launched in 2014, and the range has already delivered retail sales value of €60 million.

The decision to discontinue legacy meals, which impacted sales in the short term, will enable more profitable growth in the future, particularly with the launch of our premium Stir Your Senses ready meals in the first quarter of 2015.

We invested in our online capability with great success, delivering significant growth. Birds Eye is now the second biggest brand in the UK for online grocery sales after Coca-Cola, and as shoppers increasingly choose to buy groceries online, this channel’s importance to our business will continue to grow. We are building constructive working relationships with our retailers in the online space, pioneering innovative combo deals that position our food in new lifestyle contexts whilst growing basket size. We also launched a new consumer website which better reflects the needs and expectations of our consumers in an increasingly digital world.

In Ireland we grew our share of a declining market by 1.7%, by combining effective new promotional tactics with innovation and brand investment. This provides us with a strong blueprint for the current UK environment that we intend to roll out in the coming year.

Whilst the outlook for 2015 will remain challenging, the strong performances of our product launches in 2014 have paved the way for new innovation platforms in the year ahead. We expect to grow our share in key adult meals categories to introduce the Birds Eye brand into new households and to attract new consumers to the category. We intend to continue to build a strong foundation for retail customer partnerships that can succeed amid the current, difficult trading conditions.

Kantar has ranked the Inspirations launch as the best-selling new FMCG product launched in 2014, and the range has already delivered retail sales value of €60m.

1 6 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

IgloBRAND REVIEW

Achim Eichenlaub Managing Director, Iglo Markets

The European retail market has been challenging throughout 2014, and frozen food has not been immune from this. Net sales for the Iglo markets as a whole declined 2.8% year-on-year, driven largely by a poor performance in Germany where protracted negotiations with two large supermarket chains resulted in lower promotional support of Iglo products for a period.

Following a change in management in Germany, performance improved slightly in the second half, and the Group anticipates a further improvement in 2015 as the full strategy implementation starts to take effect.

Outside Germany, a combination of decisive management changes, as well as a focus on adult meal categories, delivered strong growth in a promising series of performances. After splitting the management of the Iglo businesses in Belgium and the Netherlands, we experienced a return to sales growth in the former and in the latter succeeded in increasing sales by 8.2%. In Portugal, we innovated successfully, adding adult portions to our fish finger and chicken nugget ranges and increasing our media spend; the result was a strong 8.7% increase in sales. In Russia, we remain the key market leader in value-added fish products, growing that market as whole by 20% in the last year.

In France, we refocused our portfolio to raise our visibility and sharpen our effectiveness, moving away from legacy products that make little positive impact on the bottom line. While this initially meant a decline in top-line sales, this approach stands us in good stead for the year ahead. Sales also declined in Austria but we performed in line with the market as a whole. Following a geographic review of our business, we have decided to cease marketing our products in Romania, Slovakia and Turkey where the frozen category is small in terms of the overall grocery market.

Our Better Meals Together strategy only rolled out in our Iglo markets in the final quarter of the year. The strong performance of our first innovation platform – Stir Your Senses – suggests that the prospects for our other innovation platforms, such as Steamfresh and Burger, will act as a significant boost for 2015.

2014 saw a significant increase in gross margin of 2.4% across our Iglo markets. This positions the brand well for 2015 and reflects strong growth across several of our European markets.

Our outlook for 2015 is a cautiously positive one. The increasingly deflationary environment in Europe and its impact on consumer spending will remain risk factors. However, the successful conclusion of our negotiations with retail customers in Germany will remove a significant drag on performance for that market and we expect our strong innovation pipeline to help offset the challenging retail environment across Europe. The strong performance of our first innovation

platform – Stir Your Senses – suggests that the prospects for our other innovation platforms, such as Steamfresh and Burger, will act as a significant boost for 2015.

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 1 7

Daniel Pagnoni Managing Director, Findus Italy

In Italy, Iglo has delivered 5 consecutive quarters of growth5

Findus Italy was one of very few FMCG companies to post an increase in sales during 2014, despite market conditions that remained extremely challenging. Of the top 15 FMCG businesses in the country, all but four experienced a decline in sales*. In this context, our success in overcoming constrained shopping budgets and increased own-label competition is very encouraging.

Our Findus brand has now posted five consecutive quarters of growth in top line sales. This performance has been driven by the execution of our Better Meals Together strategy, which we launched in Italy in the final quarter of 2013, making it the first of our markets to roll out the approach. Our strategy is focused on delivering innovation and investing in marketing to support our core portfolio and innovation launches.

The Findus Italy performance also stems from a strongly energised working culture, following the reorganisation of the business during the previous year, and a relentless focus on excellence in execution across our business functions.

We succeeded in distributing innovative new products effectively and efficiently across the market. Our strong sales performance was backed by the Food of Life advertising campaign and a powerful media plan, which doubled our market awareness with the same level of spend. Fish recipes, seafood and our new poultry and burger lines were key drivers of growth over the year, with innovative products targeted at adults accounting for much of our sales growth. Our total poultry sales grew by 42%, driven by the launch of the Inspirations platform, and we gained more than 100 basis points of share in the fish category where Findus Italy sales grew by 4% against category growth of just 1%.

We improved our net working capital position dramatically whilst developing an efficient approach to logistics and improving our stock planning to lower the amount of capital tied up on shelves.

Looking ahead to 2015, there is no doubt that market conditions will remain challenging. However, over the next year, we have plans to further extend and simplify our commitment to innovation and the new product lines that have driven growth in 2014. At the same time we plan to unlock further opportunities by applying the same innovative approach to re-energising the Sofficini and Quattro Salti product lines.

The successful launch of innovative products has been a key driver of the Italian business’ growth during 2014 and, with a strong innovation pipeline extending this to new categories throughout 2015, Findus Italy is well placed for growth in a challenging retail environment.

Fish recipes, seafood and our new poultry and burger lines were key drivers of growth over the year, with innovative products targeted at adults accounting for much of our sales growth.

Findus ItalyBRAND REVIEW

*Source: Company Information, IRI

1 8 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

Forever Food TogetherCORPORATE SOCIAL RESPONSIBILITY

Forever Food Together is Iglo’s Corporate Social Responsibility programme which is an integral part of our strategy.

It captures our vision of the role that frozen food, and we, can play in tackling fundamental challenges for society. It also reflects the trust that people have in our brands, and the recognition that with it comes an on going responsibility. We do this through always providing fully traceable, safe, top-quality food, and through doing so in a responsible way that ensures our food will be available forever.

The Forever Food Together programme is built around three goals, or promises to our consumers that set stretching targets for our business over the next five years.

• Goal 1: By 2020, we will educate consumers across Europe about the unique advantages of freezing and frozen food and help tackle food waste

• Goal 2: By 2020, 100% of our innovation will help consumers make healthier meal choices

• Goal 3: By 2020, 100% of our food products will be responsibly sourced and prepared

During 2014, we raised the profile of our Forever Food Together programme, both internally and externally. We have embedded it more deeply within our culture, values and operations and we have made it a fundamental part of our brand positioning.

Frozen offers a more sustainable food choice that can dramatically cut food waste because it inherently extends shelf-life. It enables us to maximise our food resources across the supply chain and into the home, whilst helping household budgets go further. Consumers can plan and shop more efficiently as well.

The sustainable benefits of frozen are thus naturally aligned with our Better Meals Together strategy.

SHARING OUR VISION OF FOREVER FOOD TOGETHER2014 marked the external launch of Forever Food Together at a high-profile event held at the Shard in London, which Baroness Scott chaired, where a panel discussed the difference that freezing and frozen food can make in reducing food waste.

Internally, our Forever Food Together roadshow reached out to more than 620 colleagues at 17 of our key locations across Europe. The roadshows helped embed the principles of Forever Food Together across all areas of our business.

We also established a network of Forever Food Together Ambassadors from every level of the business across all Iglo sites. Our Ambassadors operate with the central CSR team and act as a CSR compass locally, ensuring a two-way flow of information, passing on progress reports, requesting local support when required and offering up new ideas and initiatives to drive the programme.

The Green Captain icon became the public face of our Forever Food Together programme, appearing as a CSR brand icon on all new Iglo packaging with a clear message summarising our three goals in the local language of each market. Our Green Captain points consumers to our Forever Food Together websites, which explain our commitments and our vision of frozen as a more sustainable food choice.

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 1 9

Forever Food TogetherCORPORATE SOCIAL RESPONSIBILITY (cont.)

PROGRESS AGAINST OUR THREE GOALSThe three goals of our Forever Food Together programme provide us with a clear framework for measuring our progress. We made significant advances towards all three goals during 2014.

Goal 2: 100% of our innovation will help consumers make healthier meal choicesThe world faces an obesity epidemic that proves how challenging it can be for consumers to make healthier eating choices. Our response is to innovate responsibly, offering consumers recipes that are easy and convenient to prepare, and provide a simple route to a balanced diet. Our goal is for 100% of our innovation to help consumers make healthy meal choices by 2020.

Iglo Group’s Nutrition Advisory Board brings together independent experts such as leading nutritionists and academics, to help guide our innovation progress and inform our future plans.

During 2014, we worked with the Board to implement our Forever Food Together Nutrient Profiling Tool which embeds nutrition guidelines at the heart of our Research & Development (R&D), and will track progress towards our goal.

Of all new products launched by Iglo in 2014, 80% met the criteria for offering a healthier food choice that are laid down in the Nutrient Profiling Tool. This represents significant progress towards our goal of 100% of our new products meeting these criteria by 2020.

Goal 1: We will educate consumers across Europe about the unique advantages of freezing and frozen food, and help tackle food wasteMore than a third of the food that the world produces is wasted and EU food waste alone is predicted to reach 126 million tonnes by 2020. The first goal of our Forever Food Together programme is our response to this fundamental societal challenge.

Frozen, our method of food preservation, reduces the possibility of food waste at all points in food’s journey to the plate. Freezing food extends its shelf life and enables it to be transported easily, reducing waste in the supply chain. Up to now though, less has been known for certain about the impact of freezing on use of food within the home.

During 2014, new research was published that sheds light on this area and the findings are significant in the drive towards creating more sustainable food consumption. We commissioned Sheffield Hallam University in the UK to independently investigate how the behaviour of families buying frozen food differed from those buying the equivalent fresh or chilled food products. The study, which was peer reviewed and published in the British Food Journal, showed that, when eating frozen food, domestic food waste was reduced by 47%.

These findings formed the centrepiece in our external launch of the Forever Food Together programme, and will help us to mobilise a broader range of stakeholders around the benefits of frozen food. They demonstrate the role which frozen can play in using our planet’s resources more efficiently and provide a firm foundation for raising awareness. At the Forever Food Together launch, we committed to undertake and support further research in other countries to understand the beneficial impacts of frozen.

Through our Green Captain icon and our supporting Forever Food Together websites, we are getting the word out direct to consumers about the sustainability benefits of frozen. At the same time we are using the Hallam University research to build momentum behind a cross-industry campaign that can take awareness of the importance of freezing food, and reducing waste, to the next level.

At our launch event, we also committed to leveraging the benefits of frozen as extensively as possible within our own supply chains. For key iconic product lines such as fish fingers, peas and spinach and vegetables, we will work with our supply chain partners to demonstrate that 100% of the food resources that pass into our supply chain are used. We have set ourselves the ambitious target of achieving this by 2020, and further demonstrating the unique benefits that quick freezing as a method of food preservation can have on food waste.

Goal 3: 100% of our food products will be responsibly sourced and preparedEstablishing resilient, transparent and certified food supply chains is essential for frozen to fulfil its potential as a sustainable force. Goal 3 of our Forever Food Together programme reflects our commitment to responsible food sourcing through certification, and also our commitment to providing the quality and transparency that consumers expect from Iglo brands.

Under Goal 3, we adopt recognisable, credible global standards for raw materials sourcing, design, production and distribution, and we work to establish such standards where they do not already exist. This has involved taking a long-term leadership position in pioneering the certification of sustainable fisheries in partnership with the Marine Stewardship Council. This has led to Iglo selling more MSC-certified fish in more countries than any other food company in Europe. Our peas and spinach are grown in partnership and meet GlobalGAP, ISO14001 and LEAF standards.

2 0 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

We are confident that frozen food has a pivotal role to play in developing more sustainable food consumption solutions for consumers and society. At the heart of our programme is our belief that we are at our most effective when we are able to bring together policymakers, civil society, suppliers and food manufacturers, retailers and consumers and align these efforts with our brand valuesOur approach, Forever Food Together for a sustainable future, reflects this

During 2014, we made important progress with our Goal 3 targets.

Goal 3 status

Independent Verification 2006 2014 Group

2020 Target

Wild Capture Fisheries Marine Stewardship Council 48% 90% >90%

Agricultural Crops & Vegetables GlobalGAP DE & IT & LEAF in UK N/A 100% 100%

Palm Oil Certified Segregated RSPO (highest Standard)

none 90% 100%

Carbon Emissions & Energy N/A -18% -30%

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 2 1

Despite difficult trading conditions the Group continued to execute its new strategy through investment in marketing and innovation which has improved gross margin and delivered stable EBITDA, as well as another year of strong cash generation with closing Net Debt at 4.6x EBITDA

Improved margins and continued strong cash flowCHIEF FINANCIAL OFFICER’S REVIEW

Paul Kenyon Chief Financial Officer

OUR PERFORMANCEThe Group’s sales performance this year was disappointing, declining in constant currency terms by 1.9% year-on-year. However, Gross Profit and Margin both grew year-on-year as a result of improved mix management, margin-accretive innovation launches and a continued focus on operational cost efficiency. The Group’s EBITDA before exceptional items margin, at 20%, remains at the top end of industry norms.

The business continued to deliver a strong performance in cash management, ending the year with negative working capital for the fourth successive year. This was driven by continued high levels of cash generation by the business, with an operating cash flow conversion percentage of 90% before exceptional items. At the year end, the Net Debt/EBITDA ratio was 4.6x.

TRADING RESULTSTrading results to EBITDA before exceptional items are presented using constant currency exchange rates.

Constant currency results have been determined by translating the local currency denominated results for the year ended 31 December 2014 and for earlier comparative years to the 2014 budgeted €/£ exchange rate of 1.16. This represents a change in methodology to the constant currency results displayed in previous annual reports, which will not be comparable. The change has been made to align the constant currency results with those reported internally to the Chief Operating Decision Maker.

Net SalesTotal Net Sales decreased by 1.9% year-on-year to €1,469.5 million. The European food market has been challenging in 2014, and frozen food has not been immune to this with the defined frozen food market declining by 0.5% during that year. Two of the Group’s key markets saw declines in market size in the year, and against that background it is encouraging that the Group’s Italian business has delivered five successive quarters of Net Sales growth. This performance was driven by the execution of our new strategy through investment in marketing to support the core product lines and our innovation pipeline. In the UK market, the impact of the market decline has been compounded by extended negotiations with a medium-sized retailer which led to a reduction in the assortment listed, a decline in the legacy portfolio of meals and one-off gains of burger listings in 2013 following the horsemeat scandal. However, this decline has been offset to some extent by the successful launch of the Inspirations and Steamfresh platforms. In Germany, a slightly improved performance was seen in the second half of the year following the conclusion of some extended customer negotiations and the launch of the Stir Your Senses platform. Overall, Net Sales growth has been achieved in 8 out of 12 markets.

Gross MarginGross Margin improved this year, increasing by 1.8 ppts to 35.3%. The increase was primarily due to a favourable product mix driven by margin accretive innovation and supply chain continuous improvement.

2 2 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

EBITDA excluding exceptional itemsEBITDA before exceptional items remained broadly flat, as the improved margin performance was reinvested in the business through increased media spend behind the roll out of the new Food of Life campaign and the innovation launches. Investments were also directed towards improving the Group’s marketing capability and increasing research & development capacity.

Results at reported and constant currency Table 1: Reported currency€m 2014 2013 Movement %Revenue (Net Sales) 1,500.9 1,505.8 (4.9) (0.3)Gross Profit1 531.3 502.2 29.1 5.8Gross Margin 35.4% 33.4% 2.0EBITDA before exceptional items 306.2 300.1 6.1 2.0Exceptional items (52.9) (83.8)Depreciation (24.8) (23.4)Amortisation (5.6) (4.5)Operating profit 222.9 188.4

Table 2: Constant currency€m 2014 2013 Movement %Revenue (Net Sales) 1,469.5 1,498.5 (29.0) (1.9)Gross Profit 519.2 501.5 17.7 3.5Gross Margin 35.3% 33.5% 1.8EBITDA before exceptional items 297.8 298.0 (0.2) (0.1)

Exceptional itemsExceptional items during the year were €52.9 million (2013: €83.8 million).

The Group has incurred charges of €17.4 million in relation to a strategic review of the Group’s operations and other items (2013: €11.2 million). This includes costs incurred as a result of the decision to cease marketing its products in Romania, Slovakia and Turkey in November 2014, amounts in relation to tax matters from previous accounting periods and costs related to the implementation of the Better Meals Together strategy.

The Group incurred charges of €16.7 million (2013: €13.8 million) related to management incentive schemes. The majority of these costs have been accrued during the year, but are not due for payment until the associated performance conditions are met.

The Group has incurred restructuring costs of €11.6 million (2013: €10.5 million) in the year, principally in our German factories. Restructuring has been implemented as part of a strategy to deliver further operational efficiencies.

€5.5 million has been charged in relation to a fire in August 2014 in the Group’s Italian production facility which produces Findus branded stock for sale in Italy. The charge includes the cost of stock damaged by the fire, the impairment of property as well as ongoing incremental costs incurred as a result of the disruption to operations. The Group has insurance policies in place covering the stock, property and loss of earnings for which claims are currently in process. The proceeds of these claims cannot be recognised until the recoverable amount is judged to be virtually certain. As at 31 December 2014, losses of €8.7 million have been incurred, which has been offset by receipts from the insurers of €3.2 million.

€1.7 million has been incurred in the year (2013: €20.9 million) principally due to a further payment of registration tax related to the acquisition of Findus Italy. The Group is appealing the rulings and has elected to pay the assessed taxes in order to avoid incurring penalties and interest.

In 2013, €27.4 million was charged as a result of the decision to fully provide for the value of goodwill in the Belgium business.

The tax impact on the exceptional items amounts to €7.8 million (2013: €10.4 million).1 Stated after cost of sales of €912.6 million (2013: €939.3 million) and distribution costs of €57.0 million (2013: €64.3 million).

The reported average €/£ exchange rate for 2014 was 1.24. The constant currency results have been determined by translating the local currency denominated results for the year ended 31 December 2014 and for earlier comparative years to the 2014 budgeted €/£ exchange rate of 1.16.

Net Debt is defined as total bank and bond debt less cash and cash equivalents.

Gross margin of the Iglo Group business increased by 1.8ppts to 35.3% (at constant currency exchange rates)

GROSS MARGIN 2014

2013

2012

2011

2010

33.5%35.3%

34.7%

33.2%34.4%34.7%33.5%35.3%

33.2%1.8pptsIncrease 2013-2014

Decrease 2013-2014

Net Sales of the Iglo Group business decreased by 1.9% to €1,469.5 million (at constant currency exchange rates)

NET SALES €m 2014

2013

2012

2011

2010

1,469.5 1,498.5

1,569.0 1,548.1

1,541.8 -1.9%

Decrease 2013-2014

EBITDA before exceptional items decreased by 0.1% to €297.8 million (at constant currency exchange rates)

EBITDA €m 2014

2013

2012

2011

2010

298.0 297.8

342.1

304.1 325.3 -0.1%

Decrease 2013-2014

Net Debt (excluding investor funded loan notes) decreased during the year as a result of the refinancing

NET DEBT €m 2014

2013

2012

2011

2010

1,514 1,414

1,629

1,559 1,410 -100m

Operating cash flow conversion of 90% was generated at reported exchange rates

OPERATING CASH FLOW CONVERSION

2014

2013

2012

2011

2010

97%90%

87%

127%106%

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 2 3

Finance costsGroup net finance costs were €290.2 million (2013: €227.6 million).

Of the total costs for the year, €87.4 million (2013: €95.7 million) related to interest on bank loans and €129.8 million (2013: €116.7 million) to interest on investor loan notes.

On 17 July 2014, the Group completed a refinancing of its Senior debt with a syndicate of banks. All Senior debt was repaid and replaced with new Senior Euro debt of €620.0 million and Senior GBP debt of £400.0 million, which are both repayable on 30 June 2020. In addition to this, €500.0 million has been raised through the issuance of a floating rate bond issue on the Luxembourg Stock Exchange, with a repayment date of 15 June 2020. The refinancing has allowed the Group to access additional investors and is expected to deliver annual interest savings of around €14 million.

The current year charge also includes a one-off charge of €37.9 million linked to the refinancing in July 2014 of which €34.5 million relates to the write-off of deferred borrowing costs relating to the previous senior debt. The current year charge also includes a loss of €15.6 million (2013: €5.0 million gain) of exchange differences arising on re-translation of financial assets and liabilities and a charge of €7.5 million (2013: €11.8 million) for the amortisation of deferred borrowing costs.

TaxationThe tax expense for the year was €41.8 million (2013: €2.0 million).

This charge is split between a current tax expense of €27.5 million (2013: €16.6 million) and a net deferred tax charge of €14.3 million (2013: credit of €14.6 million).

The current tax charge is higher by €10.9 million due to an increase in taxable profits in 2014 compared to 2013. This is due to a year-on-year reduction in tax deductible costs and other temporary timing differences.

The increase in the deferred tax charge of €28.9 million is driven by significant credits to the P&L in 2013. In 2013, there was a credit of €14.6 million due to a change in deferred tax rates from 23% to 20%. A further credit of €8.3 million was recognised in 2013 as a result of an adjustment to the calculation of deferred tax on intangibles. In 2014, a charge of €7.8 million was incurred following an impairment to our deferred tax assets. This was as a result of matters under discussion with the local tax authorities.

Loss after taxOverall, the Group made a loss after tax of €109.1 million (2013: €41.2 million).

LIQUIDITYIn total, there was a net decrease in cash and cash equivalents of €97.9 million (2013: increase of €101.5 million) leaving a net cash balance of €219.2 million at 31 December 2014 (2013: €317.1 million). The net repayment of loan principal of €236.9 million (2013: €nil) is the key driver behind this decrease in cash.

Operating cash flows Table 3: Operating cash flows€m 2014 2013EBITDA before exceptional items 306.2 300.1Loss on disposal of fixed assets 0.2 –(Increase)/decrease in working capital (0.4) 20.4Decrease in employee benefits provision and other non-cash movements (4.3) (1.8)Cash generated from operations 301.7 318.7

Tax paid (17.1) (30.1)Cash flows related to exceptional items (17.2) (51.3)Net cash from operating activities 267.4 237.3

At an operating level the Group remains highly cash generative.

During the year to 31 December 2014 net cash inflows from operating activities, before exceptional items, was €301.7 million (2013: €318.7 million) and operating cash flow conversion was 90% (2013: 97%).

CHIEF FINANCIAL OFFICER’S REVIEW (cont.)

2 4 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

Operating cash flow conversion 2014 90%2013 97%2012 87%2011 106%2010 127%

Working capitalWe continue to maintain very low levels of working capital, achieving negative working capital for the fourth year in a row at 31 December 2014.

Table 4: Working capital analysis€m 2014 2013 Movement Inventory 229.1 221.8 Receivables 49.4 57.6 Payables (313.9) (304.5)Working capital (35.4) (25.1) (10.3)FX and non-trading items 10.7 Increase in working capital 0.4

Other cash flowsTax payments of €17.1 million were lower than the prior year payments of €30.1 million. This is partly due to the timing of payments, as the lower current tax expense in 2013 compared to 2012 meant that year-on-year tax payments reduced. In addition, a tax refund was received in 2014 following an overpayment in 2013.

Cash flows relating to exceptional items of €17.2 million relate primarily to payment for restructuring projects.

Investing cash flows Table 5: Investing cash flows€m 2014 2013 Capital expenditure & other expenditure (26.3) (28.3)Investing cash flows (26.3) (28.3)

€26.3 million was reinvested into capital expenditure, mainly involving upgrading of capacity and improving quality across our production facilities.

Financing cash flows Table 6: Financing cash flows€m 2014 2013 Proceeds from new loans* 1,624.1 0.4Repayment of loan principal* (1,861.0) –Payment of refinancing fees (15.9) (7.0)Interest related payments (91.4) (100.1)Financing cash flows (344.2) (106.7)

*Net repayment of loan principal of €236.9 million (2013: €0.4 million net proceeds from new loans).

On 17 July 2014, the Group completed a refinancing of its Senior debt with a syndicate of banks. All Senior debt as at the balance sheet date was repaid and replaced with new Senior Euro debt of €620 million and Senior GBP debt of £400 million, which are repayable on June 30, 2020. In addition to this, €500 million has been raised through the issuance of a floating rate bond issue on the Luxembourg Stock Exchange, with a repayment date of June 15, 2020. Both the new Senior debt and the bond issue are secured with equal ranking against certain assets of the Group. The refinancing has allowed the Group to access additional investors and is expected to deliver annual interest savings of around €14 million.

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 2 5

Borrowings Table 7: Debt structure

€m

Bank debt & Bond

debt

Cash and cash

equivalents

Investor Loan

Notes TotalBalance at December 2013 1,831.4 (317.1) 1,149.0 2,663.3Cash generated by business – 103.1 – 103.1Capitalised interest – – 129.8 129.8Net repayment of loan principal (236.9) – – (236.9)Movements due to foreign exchange 39.1 (5.2) – 33.9Total 1,633.6 (219.2) 1,278.8 2,693.2

At the end of December 2014, total bank and bond debt was €1,633.6 million compared to €1,831.4 million at the end of December 2013.

In addition to the bank debt shown above, the Group also has access to a revolving credit facility of €80 million, expiring in December 2019. This is available to finance working capital requirements and for general corporate purposes. Currently, €4.0 million is utilised for letters of credit, overdrafts, customer bonds and bank guarantees.

At the end of December 2014, Net Debt was €1,414.4 million compared to €1,514.4 million at the end of December 2013. Net Debt is defined as total bank and bond debt plus cash and cash equivalents.

Further detail on the Group’s borrowings is set out in note 17 of the financial statements.

FINANCIAL POSITIONGoodwill & other intangible assetsWe review the carrying value of our goodwill and brands on an annual basis. Our review does not indicate any impairment in the current year, but the headroom on the calculation is relatively low for the operations in Italy. Italy has experienced consistent sales growth in the year on the back of increased investment into A&P and new product launches. The headroom has increased in the year although this has mainly been driven by the reduction in WACC. As such, there is still a risk that changes in the market could impact the carrying value of goodwill and brands so that they fall short of that determined by value in use, leading to possible impairment.

See note 11 for further details on intangible assets.

Other liabilities: pensionsThe net pension liabilities relate mainly to obligations in Germany of €114.8 million (2013: €62.1 million) and Italy €5.7 million (2013: €5.4 million). The increase in the liability is driven by a decrease in the discount rate used to calculate the liability at 31 December 2014. This has been most prominent in Germany where the discount rate applied to the defined benefit pension plan has reduced from 3.9% at 31 December 2013 to 2.0% as at December 2014 following a fall in interest rates in the Eurozone and reductions in market yields on long-dated corporate bonds.

See note 19 for further details on employee benefits.

CHIEF FINANCIAL OFFICER’S REVIEW (cont.)

2 6 — I G LO F O O DS H O L D I N G S L I M IT E D A N N UA L R E P O RT 2 0 1 4

Manufacturing and logistics

Our manufacturing and distribution facilities could be disrupted and/or damaged for reasons beyond our control, such as extremes of weather, fire, supplies of material or services, systems failure, workforce actions or environmental issues.

Any significant manufacturing or logistical disruptions could affect our ability to make and sell products which could cause revenues to decline. This is in addition to the risk of cash outflows for asset replacement and the risk to employee safety.

There is an ongoing programme of efficiency improvement initiatives across our production facilities and operations and we have a business continuity planning process in place. All risks of physical property loss or damage and resultant loss of gross profit and increased cost of working are covered by insurance subject to insurable limits.

Technical services quality assurance

As we manufacture food products, any quality failure could impact the health of our consumers and the reputation of the brands.

Product quality is challenged via third parties including customers, consumers, NGOs, local authorities and Port authorities amongst others.

Our sourcing and production standards and quality processes are designed to avoid such issues arising. A quality failure could lead to the delisting of products, a product recall, impairment of stock and a loss of standard accreditation. Weak public relations may damage our brand image leading to a decline in sales.

Our sourcing and production standards and quality processes are designed to avoid such issues arising.

The Consumer Services function contracts a service from a third party digital media communications agency to monitor social media sites for communications related to the Group brands and products. The information is fed back to management to form an appropriate response.

Information technology

We depend on accurate, timely information and numerical data from key software applications to aid day-to-day operations and decision-making.

Any disruption caused by failings in these systems, of underlying equipment or of communication networks, could delay or otherwise impact day-to-day operations or decision-making, or cause financial losses.

Preventative measures are taken by a third party service provider to ensure data security is kept up-to-date and applied throughout the Group.

We have contingency plans in place for such situations, including manual workarounds, offsite systems backups and options for working offsite or from alternative locations. A crisis management protocol is in place for business interruption issues as part of the service level agreement.

Competition and consumer marketing

The frozen food industry is highly competitive.

We compete with other multinational corporations which are focused on special segments of the frozen food market in which both we and they operate, and with retailers who promote their “own labels”.

Furthermore, consumer tastes are susceptible to change. If we are unable to respond successfully to rapid changes in demand or consumer preferences, our sales or margins could be adversely affected.

Monthly management accounts are produced which are reviewed by the Board. These accounts allow performance to be assessed in both absolute and relative market terms and are used by the Board to make decisions.

Legal & regulatory risk management

Employees either make or receive acts of bribery in course of their duties.

A breach of legislation could lead to large fines for the Group and directors.

A code of conduct has been created and issued to employees. Employees are frequently reminded of their responsibilities and are asked to confirm agreement with the code on an annual basis.

Legal & regulatory contractual risk management

Employees enter purchasing arrangements without an approved contract in place.

The Group has controls in place to pre-approve significant contracts for goods and services.

Our Procurement function is aware of the importance of issuing approved Group terms at various point of the sale process, and employees are made aware of the Group policy that guides all supplier contracts and negotiations.

NON FINANCIAL RISK FACTORSOur business and the financial results of our operations could be materially affected by any or all of the following risks that we continue to manage actively:

Busi

ness

ove

rvie

wG

over

nanc

eFi

nanc

ial s

tate

men

ts

I G LO F O O DS H O L D I N G S L I M IT E D — 2 7

Project management and innovation

Failure to deliver new products.

In a competitive market the business must constantly drive forward with business innovation. Effective project management processes are critical to delivering this innovation.

The project management process is driven through regular reviews with cross-functional participation to robustly challenge projects and its deliverables, and to bring issues and risks to the table for addressing. The reviews allow targets and delivery expectations to be monitored and realigned.