ifta - South Dakota Department of Revenue(SD DOR) · Audits Notice of Intent to Audit ... according...

20

IFTA 2015 Procedures Manual To maintain one fuel license and one base jurisdiction location for each licensee. http://dor.sd.gov www.sdtruckinfo.com www.iftach.org

Transcript of ifta - South Dakota Department of Revenue(SD DOR) · Audits Notice of Intent to Audit ... according...

i f t a South Dakota

2015 Procedures Manual

to maintain one fuel license and one base jurisdiction location for each licensee.

http://dor.sd.govwww.sdtruckinfo.comwww.iftach.org

Taxpayer Bill of Rights

1. Youhavetherighttoconfidentiality.

2. YouhavetherighttotaxinformationthatiswritteninplainEnglish.

3. Youhavetherightofappeal.

4. Youhavetherighttocourteous,prompt,andaccurateanswerstoyourquestions.

5. Youhave the right to be certain that collection procedures or assessments are notinfluencedbyperformancegoalsorquotas.

6. Youhavetheright torelyonthewrittenadvicegiventoyoubytheDepartmentofRevenue.

7. YouhavetherighttobenotifiedbeforethedepartmentauditsyourrecordsunlesstheSecretaryofRevenuedeterminesthatadelaywilljeopardizethecollectionoftax.

8. Youhavetherighttoclearandconsistentpolicyregardingthedeadlinesforfilingtaxreturnsandmakingpayments.

9. Youhavetherighttoseekarefundofanytaxesyoubelieveyouhaveoverpaidwithinthelastthreeyears.

10. Youhavetherighttoaprocessrequiringthattheseizureofyourpropertyfortaxesbeapprovedbyapersonnolowerinauthoritythanthedivisiondirector.

11. Youhavetherighttoexpectthatagood-faithefforttocomplywithtaxlawswillbegivenconsiderationindisputedcases.

12. Youhavetherighttoataxcreditofinterestorpenaltiesthataredeterminedtohavebeeninappropriatelylevied.

13. Youhavetherighttotheremovalofalienonyourpropertywithin30daysafteryouhavepaidalltax,penaltyandinterestdue.

14. YouhavetherighttohavetheSouthDakotaDepartmentofRevenuecorrectthepublicrecord.

Table of Contents

IntroductionIFTAMemberJurisdictions ..............................................................................................................................................1

Key Terms: “Base Jurisdiction” and “Qualified Vehicle”Basic Terms .......................................................................................................................................................................2

LicensingRequirements ...................................................................................................................................................................3IFTACredentials ..............................................................................................................................................................3IFTATemporaryDecalPermit .........................................................................................................................................3Bonding ...........................................................................................................................................................................3LicenseRenewals .............................................................................................................................................................4 UnifiedCarrierRegistrationProgram(UCR) ...................................................................................................................5

Lease Agreements and Tax ResponsibilityIFTAArticlesofAgreementRegardingLeases ..............................................................................................................6

Record Keeping and Tax ReportingFuelReceipts ....................................................................................................................................................................7IndividualVehicleDistance/FuelReports........................................................................................................................7IFTA Tax Return .............................................................................................................................................................8

Penalties and License RevocationsPenalties ..........................................................................................................................................................................9CancellationProcedures ...................................................................................................................................................9

AuditsNoticeofIntenttoAudit ..................................................................................................................................................10CertificateofAssessment .................................................................................................................................................10AppealinganAuditAssessment .......................................................................................................................................10Notice of Hearing .............................................................................................................................................................10TheAdministrativeHearing .............................................................................................................................................10FindingsofFact,ConclusionsofLaw,andOrderoftheSecretaryofRevenue ...................................................................................................................................10NoticeofAppeal ..............................................................................................................................................................11Collections .......................................................................................................................................................................11NoticeofJeopardyAssessment ........................................................................................................................................11Notice of Tax Lien ............................................................................................................................................................11DistressWarrant ................................................................................................................................................................11License Revocations .........................................................................................................................................................11

AppendixDefinitions ........................................................................................................................................................................12Instructions for IFTA Tax Return ......................................................................................................................................12SampleIFTATaxReturn .................................................................................................................................................13SampleAgreementtoMaintainRecords ..........................................................................................................................14SamplePowerofAttorney ................................................................................................................................................15SampleIndividualFuelTripReport .................................................................................................................................15SampleAgreementtoFileReturnsinaTimelyManner....................................................................................................16

tatescollecttaxesonthemotorfuelusedwithintheirborderstobuildandmaintaintheroadsandhigh-

waysthatlinktheircommunitiestoeachotherandtherestofthenation.Asaninterstatemotorcarriertravel-inginSouthDakota,youpayyourshareofthesetaxesaccordingtotheprovisionsoftheInternationalFuelTaxAgreement (IFTA).This agreement, recognizedby58statesandprovinces,simplifiesthewayyoureportandpayfueltaxes,reducespaperworkandminimizescompli-ancerequirements.

Specifically,SouthDakota’sparticipationinIFTAmeansthat:

• AsinglefueltaxlicenseauthorizesyoutotravelinallIFTAmemberjurisdictions;

• Asingletaxreturnfulfillsyourreportingrequire-mentsforallmemberjurisdictions;

• Asinglestateusuallyperformsyourfueltaxaudit.

ThefollowingstatesandprovincesareIFTAmembers:

1

SD South Dakota NC NorthCarolinaAB Alberta ND NorthDakotaAL Alabama NE NebraskaAR Arkansas NL NewFoundland&LabradorAZ Arizona NH NewHampshireBC BritishColumbia NJ NewJerseyCA California NM NewMexicoCO Colorado NS NovaScotiaCT Connecticut NV NevadaDE Delaware NY NewYorkFL Florida OK OklahomaGA Georgia ON OntarioIA Iowa OR OregonID Idaho OH OhioIL Illinois PA PennsylvaniaIN Indiana PE PrinceEdwardIslandKS Kansas QC QuebecKY Kentucky RI RhodeIslandLA Louisiana SC SouthCarolinaMA Massachusetts SK SaskatchewanMB Manitoba TN TennesseeMDMaryland TX TexasME Maine UT UtahMNMinnesota VA VirginiaMOMissouri VT VermontMS Mississippi WA WashingtonMT Montana WI WisconsinMI Michigan WV WestVirginiaNB NewBrunswick WY Wyoming

ThismanualexplainstheIFTAoriginationandhowtheprocessoftaxdistributionamongthejurisdictionsworks.ItalsocontainsdetailedinformationonSouthDakota’sli-censingandbondingrequirements,leaseandtrippermits,recordkeepingandtaxreportingrequirements,penalties,andtheauditandappealprocess.

Yoursourceofinformation,forms,andassistanceaswellasthelocationtowhichyousendyourlicenseapplicationis:

Division of Motor VehiclesIFTA Section445 East Capitol AvenuePierre, SD 57501-3185Telephone: (605) 773-3314Fax: (605) 773-8416

http://dor.sd.govwww.sdtruckinfo.comwww.iftach.org

Introduction

S

wobasictermsshapetheworkingsofIFTA.Thefirstterm,“basejurisdiction,”establishesthejurisdiction

towhichacarrierwillmakefueltaxpayments.YourbasejurisdictionwillthendistributetheappropriateamountoftaxowedtoeachIFTAmemberjurisdictionforyou.SouthDakotawillbeyourbasejurisdictionif:

• Yourvehicle(s)areregisteredinSouthDakota,• Yourvehicle(s)’suseiscontrolledfromalocationinSouthDakota,

• Yourvehicle(s)’srecordsaremaintainedorcanbemadeavailableinSouthDakota,

• Atleastoneofyourvehicleslogssomemiles/kilometerswithinSouthDakota.

ThesecondtermdefinesthekindsofvehiclesthatqualifyforanIFTAlicense.These“qualified vehicles”arede-finedasmotorvehiclesused,designedormaintainedtotransportpeopleorpropertyandthat:

• Havetwoaxlesandagrossvehicleweightorregis-teredgrossvehicleweightexceeding26,000poundsor11,797kilograms;or

• Have three ormore axles, regardless of theweight;or

• Are used in combinationwhen such combinationexceedsagrossvehicleweightof26,000poundsor11,797kilograms.

Recreational vehicles are not consideredqualifiedve-hicles.

Ifyouhavemorethanonefleetoperatingoutofmorethanonejurisdiction,morethanonejurisdictioncouldqualifyasyourbasejurisdiction.Inthisinstance,thejurisdictionsinvolvedmayagreetodesignateonejurisdictionasyourbasejurisdiction.Thisdesignationmustbeapprovedinwritingbyeachaffectedjurisdiction.

2

ImportantNotice-PleaseReadImplementation of South Dakota’s Dyed Diesel Fuel Inspection Program

Penalties apply to anyonewhouses tax-exempt(dyed)dieselfuelinalicensedmotorvehicleonSouthDakota roads andhighways. AuthorizedpersonneloftheDepartmentofRevenue,theIn-ternalRevenueService,andtheHighwayPatrolmaywithdrawfuelfromlicensedmotorvehicles,machinery, equipment and storage facilities insufficient quantities to test for compliancewiththelaw.

Penaltiesdifferforqualifiedvehicles(asdefinedunderIFTA)andnon-qualifiedvehicles.Personsusingdyedfuelinaqualifiedvehicle,suchassemi-trucks,aresubjecttothefollowingpenalties:

• $500forthefirstviolation• $1,000foreachsubsequentviolation

Persons using dyed fuel in vehicles other thanqualifiedvehicles,suchascarsorpickuptrucks,aresubjecttothefollowingpenalties:

• $250forthefirstviolation• $500foreachsubsequentviolationThefirstviolationofthedyedfuellawisaClass2misdemeanor;asubsequentviolationisaClass6felony.

Key Terms: “Base Jurisdiction” and “Qualified Vehicle”

T

RequirementsIf you are amotor carrierwhooperates a qualifiedvehicle(seeexplanationinprevioussection)inmorethanoneIFTAjurisdiction,itistoyouradvantagetoapplyforanIFTAlicense.

YoumayobtainanapplicationforanIFTAlicensefromtheSouthDakotaDivisionofMotorVehicles.Licensesareissuedforonecalendaryear,January1throughDe-cember31.Thedivisioncanissueyoualicenseonlyafterthefollowingrequirementshavebeenmet:

• Youhaveaccuratelycompletedalloftheformsinyourapplicationpacket,includingtheAgreementtoMaintainRecordsform;

• ThedivisionhasdeterminedthatSouthDakotaisyourbasejurisdiction;

• Youhavesentthedivisionthecorrectlicenseanddecalfees;

• Ifnecessary,youhavepostedanacceptablebond;(See“Bonding”)

• FeesfortheUnifiedCarrierRegistrationProgramhavebeenpaid.

IFTA CredentialsUpontheapprovalofyourapplication(approximately10daysafteryouhavemettheapplicationrequirementsabove), the divisionwill sendyouyour credentials,whichinclude:

• Youraccountnumber;• Twodecalsforeachqualifiedvehicleinyourfleet(thesemustbeplacedoneachlowerrearexteriorside of the cab).All IFTAdecals are numberedand assigned to a licensee’s accountwhen theyareissued.HighwayPatrolwillhaveaccesstothisinformationandbeabletoidentifyanydecalsthatarebeingutilizedillegally;

• A single cab card that youmust reproduce andcarryineachofyourqualifiedvehicles.Keeptheoriginalcabcardinyourplaceofbusiness.

Cab CardFailuretocarrythecabcardandproperlydisplaythedecalsmayresultincitationsandfines.

IFTA Temporary Decal Permit for New Ve-hiclesIfyouaddanewvehicletoyourfleet,youmayapplyfor a 30-day, temporary IFTAdecal for that vehicleprovidingyouhaveheldanIFTAlicensewithSouthDakota for one year and are in good standing.Youmustfollowupthisapplicationwithawrittenrequestandpaymentfortheactualdecal.Failuretofollowupisgroundsfordenialoffuturedecals.

Whenyourequestatemporarydecal,bereadytofur-nishboththeVINnumberandunitnumbersincethedecalsareissuedforspecificvehicles.ThetemporaryIFTAdecalwillbefaxedtoyouforretentioninyournewvehicleandwillbevalidonlyifyoucarrywithitacopyofyourcurrentIFTAlicensecabcard.

BondingInmost cases,youwillnotbe required to furnishasurety bondwhen applying for an IFTA license. Abond,however,isrequiredinthefollowinginstances:

• Youhaveahistoryofdelinquency in reportingorpayingtaxestotheStateofSouthDakota;

• Youaredelinquentinreportingorpayingtaxforanytwoconsecutivereportingperiodsduringa12-monthperiod;

• Youremitanon-sufficientfunds(NSF)checkfortaxpaymentanddonot issueavalidcheckwithin15daysofbeingnotifiedbytheDepartmentthatyouroriginalcheckdidnotclear.

TheDepartmentcurrentlyrequiresaminimumbondoff$1,000.00TheDepartmentwillnotacceptabondthat canbe terminatedon less than60days’ notice.Securitiesacceptedinclude:

Licensing

3

IFTA DECAL

• Acashbond,• Abondissuedbyacorporatesurety,or• AcertificateofdepositendorsedinfavoroftheSouthDakotaDepartmentofRevenue.(Thepayeeofthecertificateshallreceiveanyinterestpaidonthecer-tificate.)

License RenewalsEachSeptemberthedivisionwillautomaticallysendeveryIFTAlicenseholderarenewalnotice.Youwillbeaskedtoverifytheexistinglicenseinformationandorder the appropriate number of decals for the nextcalendaryear.

Your license will not be renewed, however, if you are delinquent in filing your tax returns or if you owe any taxes, owe on an audit, have a delinquent IRP account, or have not paid UCR fees.

If you Report or Travel only in South Dakota or File Zero Distance Returns for the Past 12 MonthsInordertoqualifyforlicensingundertheIFTAagree-ment,youmustoperate in twoormoremember ju-risdictions.OperationsinSouthDakotaonlywillnotallowyoutolicense.Inaddition,ifyoudonotreportanyoperationsfora12-monthperiod,youwillbecomeineligible to license. If youroperations changeandtraveloutsideofSouthDakotaoccursagain,contacttheDepartmentofRevenuetore-license.

Changes in OwnershipIfa licenseholdersellshisbusiness, thedepartmentmustbenotifiedimmediatelyinwriting.Theexistinglicensewillbecanceledandanewlicense issuedtothe new owner.

Temporary Fuel PermitsCarrierswhoareIFTAlicenseholdersmustproperlydisplay their decals and carry their cab cards in thevehiclesatalltimes.Ifforanyreasonacarrierdoesnotdisplaydecalsorhaveacabcard,thecarriermustpurchase a temporary fuel permit. InSouthDakotatemporaryfuelpermitscost$20andaregoodfor72hours or until a carrier leaves the state,whichevercomesfirst.

Mileageandtax-paidfuelpurchasedwhileoperatingunderatemporarypermitstillmustbeincludedonthequarterlytaxreturn.Inparticular,notethefollowingitems.(SeethesampleIFTAtaxreturnonpage12.)

• LineA: Add allmiles/kilometers accrued underthetemporaryfuelpermittototaldistancetraveled(necessarytocomputeaveragemiles/kilometerspergallon).

• LineB:Addallfuelpurchasedunderthetemporaryfuel permit to total fuel consumed (necessary tocomputeaveragemiles/kilometerspergallon).

• Column2:Includealldistancetraveledinthestateinwhichyoupurchasedthetemporaryfuelpermit.

• Column3: Donot include any distance traveledunderthetemporaryfuelpermit.

• Column5:Includeanyfuelyoupurchasedonatax-paidbasis.

Retainalltemporaryfuelpermitsinyourfilesforau-ditverification.Reviewthepermitsyousubmittobecertainthattheyarefuelpermits.Forexample,somejurisdictionshaveatonmileagepermit.

Ifyousubmittedthetonmileagepermitasafuelper-mit,yourclaimwouldbedisallowedandyouwouldbeassessedinterestforunder-reportingyourfueltaxliability.

he carrier operating a vehicle is always responsibleforthepaymentoffueltax,unlessaleaseagreementspecificallystatesotherwise.Forexample,ifacarrierleasingavehicleisstoppedbyalawenforcementof-ficer,andtheleaseagreementdoesnotshowthatthelessorisresponsibleforthepaymentoffueltax,thecarrierwill be held responsible. Similarly, a carrierwho is auditedby theDepartmentmust havedocu-mentationprovingthatthepaymentoffueltaxisthe

4

Unified Carrier Registration Program (UCR)

f you operate a truck or bus in interstate or inter-nationalcommercethereisanewfederal lawthat

appliestoyourbusiness.TheUnifiedCarrierRegistra-tion(UCR)Programrequiresindividualsandcompaniesthatoperatecommercialmotorvehiclesininterstateorinternational commerce to register their business andpayanannualfeebasedonthesizeoftheirfleet.Thislaw includes private carriers. It also includesFreightForwarders,BrokersandLeasingCompaniesthatmakearrangementsforthetransportationofcargoandgoodsininterstateorinternationalcommerce.

A“CommercialMotorVehicle”isdefinedasaself-pro-pelledvehicleusedonthehighwaysincommerceprinci-pallytotransportpassengersorcargo,ifthevehicle:

(a) has a gross vehicleweight of 10,001 pounds ormore;

(b)isdesignedtotransport11ormorepassengers(includ-ingthedriver);or

(c)isusedintransportinghazardousmaterialsinaquan-tityrequiringplacarding.

Thefeesunderthisprogramwillberequiredtobepaideachyearandmayvaryfromyeartoyear.Thecurrentfeesarelistedbelow.

The Fee Brackets for Motor Carriers are as follows:

Fleet Size (Include Trailers) Fee Per Company

Tier From To

1 0 2 ------------- $ 76.00 2 3 5 ------------- $ 227.00 3 6 20 ------------- $ 452.00 4 21 100 ------------- $ 1,576.00 5 101 1,000 ------------- $ 7,511.00 6 1,001 200,000 ------------- $ 73,346.00

Example: A motor carrier operating four tractors and nine straight trucks has a fleet size of thirteen (Tier 3) commercial motor vehicles and pays $452.00.

YoumayeitherapplyfortheUCRbycompletingaUCRapplicationandmailingtheappropriatefeetotheDepart-mentorregisteronlineatwww.ucr.in.govandfollowthestep-by-stepinstructions.Whenregisteringonline,pay-mentscanbemadeusingMasterCard,Discover,Visaore-Check.Creditcardpaymentsande-Checkpaymentscanonlybeprocessedifyouregisteronline.CreditcardscannotbeacceptediffilingapaperapplicationwiththeSouthDakotaDepartmentofRevenue.

The following feeswill be appliedwhen registering through theabovementionedwebsite.Pleasenotethatthecreditcardfeeisanestimatebutshouldbefairlyaccuratetowhatyouwillbechargedwhenpayingbycreditcard.

Example: A motor carrier operating four tractors and nine straight trucks has a fleet size of thirteen (Tier 3) commercial motor vehicles and pays by credit card owes $465.05. If the mo-tor carrier pays by e-Check, he will owe $456.00.

5

I

Tier Credit Card Fee

E-Check Fee

Debit Card Fee

Website Fee

1 $2.57 $1.00 $2.99 $3.002 $5.58 $1.00 $3.75 $3.003 $10.05 $1.00 $3.75 $3.004 $32.42 $1.00 $3.75 $3.005 $150.53 $1.00 $3.75 $3.006 $1,460.65 $1.00 $3.75 $3.00

responsibilityofanotherpartyorthecarriermusthavepaidthetax.

ThefollowingsixitemsquoteddirectlyfromtheIFTAArticlesofAgreementaddressthetaxresponsibilityoflessors,lessees,independentcontractorsandhouseholdgoodsagents.

1. Alessorwhoisregularlyengagedinthebusinessofleasingorrentingmotorvehicleswithoutdriversforcompensationtolicenseesorotherlesseesmaybedeemedtobethelicensee,andsuchlessormaybeissuedalicenseifanapplicationhasbeenproperlyfiledandapprovedbythebasejurisdiction.

2. Inthecaseofacarrierusingindependentcontractorsunder long-term leases (more than 30 days),the lessor and lesseewill begiven theoptionofdesignatingwhichpartywillreportandpayfuelusetax. If the lessee (carrier) assumes responsibilityforreportingandpayingmotorfueltaxes,thebasejurisdictionforpurposesofthisagreementshallbethebasejurisdictionofthelessee,regardlessofthejurisdictioninwhichthequalifiedmotorvehicleisregistered,forvehicleregistrationpurposesbythelessor.

3. In the case of a short-termmotor vehicle rental,by a lessor regularly engaged in the business ofleasing,orrentingmotorvehicleswithoutdrivers,forcompensationtolicenseesorotherlesseesof29daysorless,thelessorwillreportandpaythefueltaxunlessthefollowingtwoconditionsaremet:

a)Thelessorhasawrittenrentalcontractwhichdesignatedthelesseeasthepartyresponsibleforreportingandpayingthefuelusetax;and

b) Thelessorhasacopyofthelessee’sIFTAfueltaxlicensewhichisvalidforthetermoftherental.

4. Inthecaseofacarrierusingindependentcontractorsundershort-term/tripleaseof29daysorless,thetriplessorwillreportandpayallfueltaxes.

5. In the case of a household goods carrier usingindependent contractors, agents, or servicerepresentatives,underintermittentleases,thepartyliableforfueltaxshallbe:

a)Thelessee(carrier)whenthequalifiedmotorvehicle is being operated under the lessee’sjurisdictional operating authority. The basejurisdictionforpurposesofthisagreementshallbe thebase jurisdictionof the lessee (carrier),regardless of the jurisdiction in which thequalifiedmotorvehicleisregisteredforvehicleregistrationpurposesbythelessororlessee.

b) The lessor (independent contractor, agent,or service representative)when the qualifiedmotorvehicleisbeingoperatedunderthelessor’sjurisdictional operating authority. The basejurisdictionforpurposesofthisagreementshallbethebasejurisdictionofthelessor,regardlessofthejurisdictioninwhichthequalifiedmotorvehicle is registered for vehicle registrationpurposes.

6. Nomemberjurisdictionshallrequirethefilingofsuchleases,butyoumustmaketheleasesavailableuponrequestofanymemberjurisdiction.

Lease Agreements and Tax Responsibility

6

T

IFTAlicenseholdersmustmaintaindetailedrecordsandfilequarterlyreportsalongwiththeirfueltaxpayments.Recordsmust be retained for a periodof 4 years; thecurrenttaxyearplusthe3previousyears.Thisrecordkeeping and reporting responsibility consists of threeelements.

Fuel ReceiptsIn order for the licensee to obtain credit for tax-paidpurchases,areceipt,invoice,orcreditcardorautomated-vendor-generated invoice or transaction listingmustbe retainedby the licensee for eachpurchase of fuel.Separate totalsmust be compiled for gasoline, diesel,kerosene,gasohol,liquidpetroleumgasandCNG.Thefuelreceiptsmustcontain:

• Datethefuelwaspurchased;• Nameandaddressoftheseller;• Numberofgallonspurchased;• Typeoffuel;• Equipmentnumberofthevehicleusingthefuel;• Purchaser’sname(Whenthereisaleaseagreement,receiptswillbeacceptedinthenameofeitherthelesseeorthelessor.Theremust,however,bealegaldocumentconfirmingtheleaseagreement.);

• Pricepergallonortotalamountofsale.• Theamountoftaxpaid.SouthDakotadoesnotrequirecarrierstoreportgasolinepurchases,butmanyotherjurisdictionsdo.Specifically,thesurroundingjurisdictionsofMontana,NorthDakota,Minnesota,Iowa,andNebraskaallrequiregasolinere-porting.Whentravelingintogasolinereportingjurisdic-tions,purchaseenoughfueltooffsetthedistancetraveledwithintheirborders.

SinceSouthDakotadoesnotrequiregasolinereporting,thequarterlytaxreturnwillnotincludeanareaforreport-ingSouthDakotafuelpurchases.

Bulk StorageFuelpurchasedforbulkstoragemustbetotaledseparately.Carriersmustkeepallfueldeliveryticketsandinvoices.Inaddition,carriersmustrecordalldisbursementsandinventory reconciliation and distinguish between fuelplacedinqualifiedvehiclesandfuelusedforotherpur-poses.Manytaxpayersareclaimingallgallonsboughtinbulkduringthereportingperiodeveniftheyhavenotusedit.YoucanonlyreportthefuelonyourIFTAreturnifithasbeenpulledfrombulkstorageandplacedintoaqualifiedvehicleduringthefilingperiod.

Record Keeping and Tax Reporting

7

Over-the-Road PurchasesSimilarly,separatetotalsmustbekeptforanyover-the-road(OTR)purchases.Carriersmustkeepsalesreceipts,invoicesorcreditcard receipts. (These itemsmaybeonmicrofilm/microficheorotherelectronicdatastoragemedia.)

Theserecordsmustalwaysidentifythevehiclebyunitnumberorlicenseplatenumber,sinceIFTAlicensehold-ersmayonly report fuelpurchasesmade forqualifiedvehiclesthattheyoperate.Altered receipts or those with erasures will not be accepted for tax-paid credit.

Individual Vehicle Distance/Fuel ReportsTheIndividualVehicleDistance/FuelReport(IVDFR)isthebasicdistance-reportingdocument(Samplep.14).AllIVDFRsmustinclude:

• Datesoftrip(startingandending);• Triporiginanddestination;• Routesoftravelincludinghighwaynumbers;• Totaldistancetraveledwithineachjurisdiction;• Totaltripdistance(includingallvehiclemovementwhether loaded, empty, deadhead, or bobtail dis-tance);

• Unit number or vehicle identification number forpowerunitsandtrailers;

• Beginning and ending odometer readings (or hubmeter);

• Registrant’sname;• Driver’sidentification(name,number,signature)Thefollowinginformationishelpful,butnotmandatory: •Odometerreadingatjurisdictionalbordercrossing.

SouthDakotaencouragestheuseofnewtechnologyandmostcosteffectivemethodsofaccumulating totalandin-jurisdiction distances that accurately reflect actualrouteoftravel.Ifacarrierinstalls/implementssystem(s)thatprovidesaccurate(life-to-date)distancedatawith-outdriverinput,carriermayrequestawaiverofeitherodometerreadingsorroutesoftravel,notboth.Arequestforawaiverofareportingrequirementmustbeinwrit-ing.SouthDakotawillconductaninspectionofinternalcontrolproceduresandfullytestthecarriersdistanceandfuelaccountingsystem.Avalidwaiverofeitherroutesoftravelorodometers(notboth)willbearthesignatureofanauthorizedSouthDakotaofficial.Thewaiverisvalidforthreeyears-unlessthereisamaterialchangeininternalcontrolsormethodsofaccumulatingkeydataelementsnecessarytocompletequarterlyreturns.

Record Keeping and Tax Reporting (cont.)

8

IFTA Tax ReturnThetwoprecedingelements,fuelreceiptsandIVDFR’s,arethebasisforthethirdelement,thequarterlyIFTATaxReturn.Thedivisionwillsendyouthetaxreturnformatleast30daysbeforethetaxreturnduedate.Your tax return must be postmarked no later than midnight on the last day of the month following the close of a reporting period.IfthelastdayofthemonthfallsonaSundayorlegalholiday,thenextbusinessdaywillbeconsideredthefinalfilingdate.

The returnmust show total distance traveled, all fuelconsumed,andtotaltaxpaidgallonsbyqualifiedvehiclesduringthequarteraswellasthedistancetraveledandfuelconsumedineachIFTAjurisdiction.Iffuelisnotpur-chasedduringthequarter,theaveragemiles/kilometerspergallonfromthepreviousquarterisused.Youmustsubmitataxreturnforeachtaxreportingperiod,evenifnotaxablefuelwasused.Ifyoudonotreceiveataxreturn,youmustsubmitawrittenreportsettingforthalloftherequiredinformation.Thisreportwillbeacceptedinlieuoftheprescribedform.Failure to receive the authorized form does not relieve you from the obliga-tion of submitting a return.

MeasurementsLicenseesbasedinSouthDakotaarerequiredtoreportinU.S.measurements.When you calculate your fueltax,usethefollowingfactorsandcomputetothenearestone-tenthofacent:

Oneliter =.2642gallons Onegallon =3.785liters Onemile =1.6093kilometers Onekilometer =.62137milesWhenyoureportfuelsthatcannotbemeasuredinlitersorgallons,suchascompressednaturalgas,reportthefuelattheconversionfactorusedbythejurisdictioninwhichthefuelwasused.

Tax-Exempt MilesIFTAmemberjurisdictionsdifferintheirdefinitionoftax-exemptmiles/kilometers.Beforeyoureporttax-exemptmiles/kilometersonyourtaxreturn.Informationonju-risdiction’sexplanationsoftaxexemptmiles/kilometerscanbeviewedatwww.iftach.org.Fuelusedforoff-roadagriculturaloroff-roadcommercialpurposes inSouthDakotaisnolongerexemptfromtaxandisnotsubjecttorefundortaxexemptreporting.

Annual ReportingIfyourdistanceinallIFTAmemberjurisdictionsother than South Dakotatotalslessthan5,000milesduring

acalendaryear,youmaychoosetoreportonanannualbasis.Youmusthaveaone-yearfilinghistoryundertheIFTAprogramtobeeligibleforthisexception.

Ifyouwishtoreportannually,youmustpetitiontheDivi-sionofMotorVehiclespriortofilingyourfirstquartertaxreturn.Requestsforannualfilingsubmittedafterthefirstquarterwillnotgointoeffectuntilthenextlicenseyear.Whenthedivisionreceivesyourrequest, itwillnotifytheothermemberIFTAjurisdictionsoftherequest.Ifanyjurisdictionobjectstoyourrequest,therequestwillbedenied.Youwillreceivewrittennotificationthattheannualfilingprivilege has beengranted to you.Oncenotified,youwillberesponsibleforfilingfourseparatetaxreturnsattheendoftheyear.

Refunds and CreditsWhenyoufileyourtaxreturn,applyanyoverpaymentoffueltaxespaidinonejurisdictiontothetaxesowedtoanotherIFTAjurisdiction.Forexample,ifyouunderpaidfueltaxesinMinnesotaby$100andoverpaidtaxesinMontanaby$50,remitthenettaxof$50alongwithyourIFTAreturn.Ifyoushowanettaxcreditof$25ormoreonataxreturn,SouthDakotawillprocessandissuearefundbeforetheendofthenextreportingperiod.

A refundwill not bemade, however, if there are anytaxliabilitiesoutstanding,includingauditassessments,penaltiesorinterest.Similarly,refundswillbewithheldif a licenseholder’s payment of fuel tax to any IFTAjurisdictionisdelinquent.

Asacost-savingmeasure,thedepartmentwillnottakeactiononcreditsoramountsduethatareunder$5.00,un-lessalicenseholdermakesawrittenrequest.Thesesmallbalanceswillbeheldinthelicenseholder’saccount.

IFTArequirestheassessmentofcostlypenaltiesforfail-uretofileareturn,forfilingalatereturnorforunderpay-mentoftaxesdue.Thesepenaltiesincluded:

• Afeeof$50or10percentof thenet tax liability,whicheverisgreater;and

• ForafleetbasedinaU.S.jurisdiction,interestshallbesetatanannualrateoftwo(2)percentagepointsabove the underpayment rate established underSection6621(a)(2) of the InternalRevenueCode,adjustedon an annual basis on January1of eachyear.Interestshallaccruemonthlyat1/12thisannualrate.

• Interestwillbecalculatedfromthedatethetaxbe-comesdueandisassessedforeachmonthorfractionthereofuntilpaid.

Penalties and License Revocations

9

oavoidpenaltyforlatefiling,yourtaxreturnmustbepostmarkedno later thanmidnighton the lastdayofthemonthfollowingthecloseofareporting

period.IfthelastdayofthemonthfallsonaSunday,orlegalholiday,thenextbusinessdaywillbeconsideredthefinalfilingdate.

Iffilinganonlinereturn,theretunmustbefiledonthesystembytheduedatetobeconsideredontime.

Ifareturnishanddelivered,itwillbeconsideredfiledandreceivedonthedateitwasdeliveredtoanemployeeoftheSouthDakotaDepartmentofRevenue.

FailuretofileareturnorremittaxonatimelybasisisaClass1misdemeanorforthefirstviolation.AsubsequentviolationisalsoaClass1misdemeanor.

Procedures Taken by the Department for Failure to File or Pay It is imperative that all tax returns and payments areremittedasrequired.DonotignoreanynoticessenttoyouregardingyourIFTAlicense.Manytaxpayersbelievethatbecausetheyarepayingthetaxatthepump,thattheimportanceoffiling their IFTA tax return isminimal.Failuretofileareturnwillhaveserioustaxconsequencesagainstthelicenseholder.Ifthedepartmenthastogen-erateajeopardyassessmentbasedonanestimateduetofailuretofile,yourtaxliabilitycanamounttothousandsof dollars, as the assessment generatedwill not allowcreditfortaxpaidpurchases.Thefollowingprocedureswillbetakenagainstanylicenseholderwhofailstofileareturnorpayanamountdue.

If,foranyreason,youfail,neglectorrefusetofileataxreturnwhendue,anon-filernoticewillbesenttoyourequestingthattheappropriatereturnbefiled.If,after30days,thereturnstillhasnotbeenfiled,ajeopardyas-sessmentbasedonthebestinformationavailablewillbegenerated.Thejeopardyassessmentwillprovideyouwith60 daysinwhichtoeitherfiletheapplicablereturnandpayanytax,penalty,interestdueorrequestahearingtocontest the assessment. Failure to take action within the 60 day period will result in the jeopardy assessment becoming your amount due and no further recourse can be taken to object to the assessment nor can you later file the applicable delinquent return to reverse the assessment.

If you have not satisfied a tax delinquency or filed awrittenappealrequestwithin60daysofthedateofno-tification,ataxlienwillbegenerated,alongwithaletterofrevocation.Youwillbeprovided30daystopayyour

T assessmentpriortorevocationofyourlicense.Youhavetherighttosubmitawrittenrequestforahearingcon-testingtherevocationofyourlicense.Afterthis30-dayperiod,adistresswarrantwillbeissuedandyourlicensewill be canceled.Onceyour license is canceled, yourIFTAlicenseandalldecalsbecomeinvalid.Operationinmemberjurisdictionsisillegalandcauseforenforce-ment action.

Thesameprocedureswilltakeplaceifyoufailtopayalltax,penaltyorinterestdueagainstyourlicense.Thejeopardyassessmentthatwillbeissuedwillbebasedontheactualamountduefromyourtaxreturnfilingratherthananassessmentbasedonthedepartment’sestimationoftax,penaltyandinterestdue.

IFTA allows for a grace period into the last day of February of each year. Because of this grace period, a tax return must be filed for the first quarter of a year if you have not submitted a written letter of cancella-tion to the department to cancel your IFTA license at the end of any given tax year.

Once the department has canceled your license, youwillberequiredtopostabondinordertoreinstateyourlicense.Therearenoexceptionstothisrequirement.

Asnotedearlier,theDepartmentmayalsorevokeyourIFTAlicenseifyoudonotcomplywithrecordkeepingrequirements.

Cancellation ProceduresIf you cancel your InternationalRegistrationProgramaccount (the agreement underwhich interstatemotorcarriersarelicensed),youmayalsoberequiredtocancelyourIFTAaccount.YoumustreturnyourIFTAlicense,removetheIFTAdecalfromthecab,andfilethetaxre-turncontainingdistanceandfuelinformationuptoandincludingyourlastdayofoperation.ContacttheDepart-mentifyouhaveanyquestionsconcerningcancellationofyourIFTAlicense. To cancel your license properly, your request must be made in writing and sent to the Department of Revenue, Division of Motor Vehicles.

Audits

heDepartmentofRevenue routinely audits IFTAlicenseholdersrequiredtopayfueltaxes.Thepur-

poseofanauditistoensurelicenseholderscomplywiththetermsoftheIFTA/IRP.TheauditverifiestheaccuracyofthereportedjurisdictionaldistanceandfuelgallonsonthequarterlyIFTATaxreturnsbyreviewingtherequiredsourceandsummarydocumentslistedontheRecordKeep-ingandTaxReportingsectionofthismanual.

Notice of Intent to AuditTheauditprocessbeginswhenthedepartmentmailsaNoticeofIntenttoAudittothelicenseholder.Licenseholdersarenormallynotifiedatleast30daysbeforetheauditdate(unless thedepartmentsecretarydeterminesthatadelaywouldjeopardizethecollectionoftax).Ontheopeningdayoftheauditthelicenseholdershouldprovidetheauditorwithallrecordssupportingdistancetraveledandfuelconsumed.Ifthelicenseholderfailstopresentdocumentationtotheauditorwithin60daysofthebeginningoftheaudit,theauditormaydisallowthedistanceandfuel,resultinginanassessmentofadditionaltaxesandinterest.Alicenseholder’sfailuretoproviderecordsforauditpurposeswillcausethestatuteoflimita-tionstobesuspendeduntilsuchrecordsareprovided.Ifthelicenseholder’srecordsarenotcompleteenoughtoascertainanaccuratedistributionofjurisdictionalfueltaxes,theauditormayestimatejurisdictionalfueltaxesfortheperiodunderauditusingthefollowingguidelines:• Alicenseholder’spriorexperienceoracomparisonwithsimilaroperations;or

• Anacceptable industry standardAMPG foropera-tions.

Ifalicenseholder’soperationalrecordsarenotlocatedinSouthDakotaand itbecomesnecessary fordepartmentauditorstotraveltowheresuchrecordsaremaintained,thedepartmentwillbillthelicenseholdertheperdiemandtravelexpensesincurredbytheauditor(s)toconducttheaudit.Certificate of AssessmentAfterreviewingthelicenseholder’srecords,aCertificateofAssessmentwillbeissued.Thecertificateshowsthetypeandamountoftaxorfeesdue,ifany,andthereasonsforanyassessment.Thelicenseholderhas60daysfromthedateofthecertificatetotakethefollowingaction:• Paytheassessment,includingaccruedinterest,or• Requestahearing(inwriting)beforetheSecretary

of Revenue.

Appealing an Audit AssessmentArequestforahearingisthelicenseholder’sonlywayof contesting an audit assessment. If a license holderdecidestoappealtheassessment,heorshemustsubmit

aRequestforHearingwithinthe60-daytimelimitation.Therequest,submittedinletterform,mustspecificallyidentify the issuesbeingcontested. If itdoesnot, theadministrativehearingcouldbedenied.

Therequestforhearingmuststate:• Theportionoftheassessmentbeingcontested,and• Themistakeoffactorerroroflawthelicenseholderbelievesresultedinaninvalidassessment.

Onceaproperrequestforhearinghasbeenfiled,themat-terbecomesacontestedcaseandfallswithinthescopeoftheAdministrativeProceduresAct(SDCL1-26).ThedepartmentschedulesthematterforhearingandservesthelicenseholderwithaNoticeofHearing.

Notice of HearingThenoticeofhearinginformsthelicenseholderofthetimeandplaceofhearing,thenameandaddressofthehearingexaminer,andsetsforththeissuestobeconsid-ered.Thenoticeofhearingmustbeservedonthelicenseholderatleast10dayspriortothehearing,toallowtimefor“discoveryproceedings,”whichmayincludeapre-hearingconferenceinvolvingthedepartment’sattorney,thelicenseholderandhisorherrepresentative,andthehearing examiner.

The Administrative HearingTheadministrativehearingisconductedaccordingtotheprovisionsof theAdministrativeProceduresAct (SDCL1-26).The licenseholdermaybe representedbyanat-torney.Essentially,thelicenseholderisaplaintiffinacivilmat-ter.Consequently,heorshemustprovethattheassess-mentisinvalidbecauseitisbasedonamistakeoffactorerroroflaw.Inmostcases,theadministrativehearingisthelicenseholder’sonlyopportunitytopresenttestimonyandevidence.Attheconclusionofthehearing,thehearingexaminermay request briefs on the legal issues. Following thesubmission of briefs, the hearing examiner prepares proposedfindingsoffactandconclusionsoflawforthesecretarytoconsider.

Findings of Fact, Conclusions of Law, and Order of the Secretary of RevenueThe secretarymay adopt the proposals of the hearingexamineror,afterreviewingtherecord,maysubmithisorherownfindings,conclusions,anddecision.Copiesofthefindingsoffact,theconclusionsoflaw,andtheorderaresenttothelicenseholder.Ifthelicenseholderisorderedtopayadditionalfeesand/or taxanddesires toappeal thedecision to thecircuitcourt, he or she must:

10

T

• Paytheamountsorderedtobepaid,or• Fileabondwiththedepartmenttoinsurepayment.TheSouthDakotaSupremeCourthasruledthatifpay-mentisnotmadeorabondposted,thecircuitcourtcannothearanappeal.

Notice of AppealAfterthelicenseholderhaspaidthefeesand/ortaxorfiledabond,theappealtothecircuitcourtisgovernedbytheAdministrativeProceduresAct.Thelicenseholdermustservehisorhernoticeofappealuponthedepartmentandfileit,alongwithproofofservice,withtheclerkofcourtsoftheappropriatecounty.Thisnoticeofappealmustbefiledwithin30daysofthedatetheSecretaryofRevenueserves the licenseholdernoticeofhisorherdecision.Whenthecourthearstheappeal,itwillbaseitsreviewofthedepartmentsecretary’sdecisionupontheadministrativerecord.Withregardtothequestionsoffact,thesecretary’sfindingswillbeupheldunless“clearlyerroneous.”Ques-tionsoflawarefullyreviewablebythecourt.The decision of the circuit courtmay be appealed totheSouthDakotaSupremeCourt. Thesupremecourtwillreviewthesecretary’sdecisionontherecord,underthe same standardsof reviewemployedby the circuitcourt.

CollectionsIfalicenseholderfailstopayfees,taxes,penaltiesandinterest,thedepartmentmaybeginacivilsuitagainstthelicenseholderforrecoveryofthedebt.Ifsuccessful,thedepartmentbecomesajudgmentcreditorandcanusethenormalcollectionproceduresopentosuchacreditor.

Notice of Jeopardy AssessmentInsomecases, theDepartmentmaybypass the formalauditprocedureindeterminingiffeesand/ortaxesaredue.IftheSecretaryofRevenuefindsthattheassessmentorcollectionofanytaxisjeopardizedbythedelay,hemayimmediatelymakeanassessmentoftheestimatedtax,penaltyor interestanddemandpayment from thelicenseholder.Thus,whenconfrontedwithanuncoop-erativelicenseholderwhofailstofilerequiredreturnsorreportstaxabletransactions,thesecretarymayestimatetheamountsduebaseduponavailablerecordsorsourcesandissuetheNoticeofJeopardyAssessment.IfalicenseholderfailstopaytheamountsnotedinthejeopardyassessmentandisaresidentofSouthDakota,thedepartmentwillfileappropriateliensandrequesttheissuanceofdistresswarrants.

Notice of Tax LienAnyfee,tax,penaltyorinterestduefromalicenseholderresultsinanautomaticlienonhisorherrealorpersonal

property.Topreservethestate’slienpriorityagainstothercreditors,theDepartmentfilesaNoticeofTaxLienwiththeregisterofdeedsofthecountyinwhichthelicenseholder’spropertyislocated.

Distress WarrantIfthelicenseholderstillfailstomakepayment,thedepart-mentrequeststhecountytreasurertoissueadistresswar-ranttothecountysheriff.Thedistresswarrantdirectsthesherifftoproceedtocollectthedelinquentfeesand/ortaxesbyseizingandsellingthelicenseholder’sproperty.

License RevocationsIftheholderofanIFTAlicensefailstopayfeesand/ortaxes ina timelyfashion, the licensemayberevoked.TheDepartmentwillgivethelicenseholderpriornoticeandanopportunitytobeheardbeforehisorherlicenseissuspendedorrevoked.Ahearingexaminerconductstherevocationhearing.TheDepartmentpresentsevidencetoprovethefailuretopayfeesand/ortaxes.Thelicenseholderthensubmitshisorherevidenceortestimonytoshowcompliancewiththelicensingregulations.Followingthehearing,theexam-inerpreparesminutesandadecisionfortheSecretaryofRevenuetoconsider.Thesecretarywillthenissuehisorherorder,whichmayincludeanassessmentofadditionaltaxes,penaltyandinterest.Thedepartmentandthelicenseholderhavetherightofjudicialreviewofthesecretary’sorder.Theprocedureforjudicialreviewisessentiallythesameasthatdescribedintheprevioussectiononauditappeals.

Declaratory RulingsIfalicenseholderbelievesthatanerrorhasbeenmadeindetermininghisorherliability,heorshemayasktheSecretaryofRevenuetorenderaformalopinionregardingtheapplicationorinterpretationofalicensingregulation.ThisisaccordingtospecificrulesandproceduressetforthinSDCL1-26-15.Alicenseholderwhowantsadeclaratoryrulingfromthedepartmentsecretarymustsubmitaverifiedpetition.Thepetitionmustpresentthespecificquestiononwhichheorsheisrequestingarulingandthefactualbasisforthequestion.Typically,thepetitionwillincludearequestforarefundoffeesand/ortaxes.Ifthesecretarydeterminesthatadditionalfactsorinformationareneeded,heorshemaycallforahearingonthepetition.Thesecretarymustnotifythelicenseholderofthehearingatleast10dayspriortothehearingdate.Thesecretarymaydeclinetorenderadecisionifheorshedeterminesthatarulingwillnotsettlethecontroversy.Ifarulingismade,thesecretarywillincludefindingsoffactandconclusionsoflaw.Thesecretary’srulingissubjecttoappealtothecourts.11

Appendix

12

Theappealisthesameasanappealofanyotheragencydecisioninacontestedcase.Base Jurisdiction or Base State:Themember jurisdic-tionwherequalifiedmotorvehiclesarebasedforvehicleregistrationpurposesand;

1. Wheretheoperationalcontrolandoperationalrecordsofthelicensee’squalifiedmotorvehiclesaremain-tainedorcanbemadeavailable,and;

2. Where some travel is accrued by qualifiedmotorvehicleswithinthefleet.Thecommissionersoftwoormoreaffectedjurisdictionsmayallowapersontoconsolidateseveralfleetswhichwouldotherwisebebasedintwoormorejurisdictions.

In-Jurisdiction Distance or In-State Distance: Thetotalnumberofmilesorkilometersoperatedbyaregistrant’s/licensee’s qualifiedmotor vehicleswithin a jurisdiction.In-jurisdictionmiles or kilometers do not include thoseoperatedonafueltaxtrippermitorthoseexemptedfrom

Instructions for States with Surcharge TaxesThestateslistedinthechartbelowhavesurchargetaxesthatareallcalculatedinthesamemanner.Twolineswillappearforeachsurchargetaxstate.Thefirstlinewillalwaysbere-cordedasthetaxratethatisassessedatthepump.Thesecondlineisforthesurchargetax.Thistax,whichiscollectedbasedonthetaxablegallonsshownonthepreviousline(column4),isonlycollectedonthisreturn.DonotaddthesurchargetaxlineaspartofyourtotalIFTAmiles/kilometersbecauseyouwillreportthisonthepreviousline.

AnnotationsColumn 1 - EachjurisdictionthatisanIFTAmemberforthereportingperiodwillbeprintedinColumn1.

Column 2 - Show the total distance traveled in eachjurisdictioninColumn2.

Column 3 -Show totaldistance traveled forwhich fueltax is due.Deduct distance that a jurisdiction considersnon-taxable,suchasoff-roaddistanceanddistancetraveledundertemporaryfuelpermits.SeePages15-18forfulllistof exemptions. Note: Toll road miles/kilometers are taxable.

Column 4 - DividetotaltaxabledistanceinColumn3byaveragemiles/kilometerspergallon,LineCabove.

Column 5 - Listthegallons,byjurisdiction,onwhichfueltaxhasbeenpaid.Note:Fuelpurchasedinsomejurisdic-tionsmaynothavethetaxassessedatthetimeofpurchase.Seeinstructionsthataccompanyquarterlytaxreturns.

Column 7 - ThetaxratefortheapplicablefueltypewillbeprintedinColumn7.

Column 9 - ThecorrectinterestrateforthecurrentyearwillbeprintedinColumn9.Interestiscalculatedonlyifreturnisfiledafterduedate.

Total of Column 10 - Computethe“amountdue”or“credit”foreachjurisdictionandthendeterminethe“amountdue”or“credit”foralljurisdictionscombined.

Qualified Motor Vehicle:Amotorvehicleused,designed,ormaintained for transportation of persons or propertyand:

1. Having two axles and a gross vehicleweight orregistered gross vehicleweight exceeding 26,000poundsor11,797kilograms;or

2. Havingthreeormoreaxlesregardlessofweight;or

3. Is used in combinationwhen theweight of suchcombination exceeds 26,000 pounds or 11,797kilogramsgrossvehicleweight.

“Qualifiedmotor vehicle” does not include recreationalvehicles.

Revocation: Thewithdrawal of license and privilegesgrantedtothelicenseebythelicensingjurisdiction.

Total Distance:Allmilesorkilometerstraveledduringthereportingperiodbyeveryqualifiedvehicleinthelicensee’sfleet,regardlessofwhetherthemiles/kilometersareconsid-

Instructions For IFTA Tax Return

Definitions

Total Due - Showthenetamountdueorthecredit.Ifacreditofmorethan$25isdue,arefundwillbeissuedpriortotheendofthenextquarter.

Line A -ShowthetotalofallentriesinColumn2here.“TotalMiles”meansdistancetraveledduringthereportingperiodbyeveryqualifiedvehicleinyourfleet,regardlessofwhetherthedistanceconsideredtaxableornon-taxablebyajurisdiction.

Line B -ShowtotalfuelconsumedduringreportingperiodbyeveryqualifiedvehicleincludedinyourentryforA.

State

Indiana

Kentucky

Virginia

Tax

I1

K1

V1

Surcharge

I2

K2

V2

13

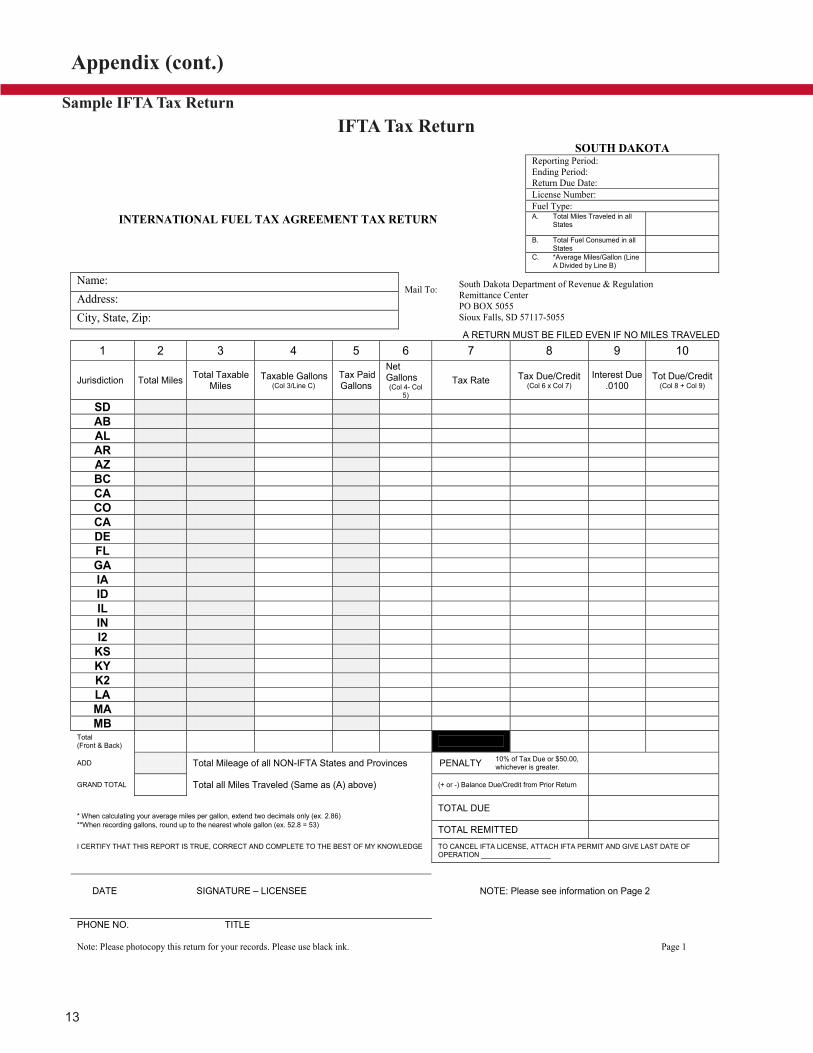

IFTA Tax ReturnSample IFTA Tax Return

Appendix (cont.)

SOUTH DAKOTA ReportingPeriod:EndingPeriod:ReturnDueDate:License Number: FuelType:A. Total Miles Traveled in all

States INTERNATIONAL FUEL TAX AGREEMENT TAX RETURN B. Total Fuel Consumed in all

States C. *Average Miles/Gallon (Line

A Divided by Line B)

Name: Address:City,State,Zip:

MailTo: SouthDakotaDepartmentofRevenue&RegulationRemittance Center POBOX5055SiouxFalls,SD57117-5055

A RETURN MUST BE FILED EVEN IF NO MILES TRAVELED

1 2 3 4 5 6 7 8 9 10

Jurisdiction Total Miles Total Taxable Miles

Taxable Gallons (Col 3/Line C)

Tax PaidGallons

NetGallons(Col 4- Col

5)

Tax Rate Tax Due/Credit (Col 6 x Col 7)

Interest Due.0100

Tot Due/Credit (Col 8 + Col 9)

SD

AB AL AR AZ BC CA CO CA DE FL GA IA ID IL IN I2

KS KY K2 LA MA MB

Total (Front & Back)

ADD Total Mileage of all NON-IFTA States and Provinces PENALTY 10% of Tax Due or $50.00, whichever is greater.

GRAND TOTAL Total all Miles Traveled (Same as (A) above) (+ or -) Balance Due/Credit from Prior Return

* When calculating your average miles per gallon, extend two decimals only (ex. 2.86) TOTAL DUE

**When recording gallons, round up to the nearest whole gallon (ex. 52.8 = 53) TOTAL REMITTED

I CERTIFY THAT THIS REPORT IS TRUE, CORRECT AND COMPLETE TO THE BEST OF MY KNOWLEDGE TO CANCEL IFTA LICENSE, ATTACH IFTA PERMIT AND GIVE LAST DATE OF OPERATION __________________

DATE SIGNATURE – LICENSEE NOTE: Please see information on Page 2

PHONE NO. TITLE

Note:Pleasephotocopythisreturnforyourrecords.Pleaseuseblackink. Page1

AGREEMENT TO MAINTAIN RECORDS IN ACCORDANCE WITH THE INTERNATIONAL FUEL TAX AGREEMENT AND THE INTERNATIONALREGISTRATION PLAN’S RECORD KEEPING REQUIREMENTS

Everylicenseeshallmaintainadequaterecordsofoperation.ThelicenseeshallpreservetherecordsforIRPforthethreemileagereportingperiods(July1throughJune30)whichimmediatelyprecedethecurrentlicenseyear,alongwiththecurrentlicenseyear.ThelicenseeshallpreservetherecordsforIFTAforaperiodoffouryearsfromtheduedateofthereturn.

SouthDakotarequiresthatrecordsbemadeavailabletothedepartmentforaudituponrequest.Intheeventthelicenseefailstomakeacceptablerecordsavailablefortheaudit,thedepartmentmaymakeassessmentsandpenaltiesfortheperiodunderauditandmaysuspendorcancellicenseprivileges.

DOCUMENTS TO BE MAINTAINED The following paragraphs briefly describe the documents required. Detailed record keeping

information and requirements are included in the South Dakota Procedures Manuals.

Eachtripmustbesupportedbyadriver’stripsheet,driver’slogorotherdocumentcompletedbythedriverthatincludesthefollowinginformation:1)Dateoftrip(beginningandending);2)Triporiginanddestination;3)Routes(highwaynumbers)traveled;4)Mileagebyjurisdiction;5)Totaltripmiles;6)Vehicleequipmentnumberoridentificationnumber(forpowerunitandtrailer);7)Odometerreadings;8)Drivernameandsignature;9)Bothtaxableandnon-taxableusageoffuel;10)Milestraveledfortaxableandnon-taxableuse;11)Mileagerecapsforeachvehicleforeachjurisdictioninwhichthevehicleoperated.Eachlicenseeshallmaintainacompleterecordoffuelpurchasedorreceived,includingretailandbulkstorageusedintheconductofitsbusiness.Thefuelrecordsshallcontain,butarenotlimitedto:

a. Thedateofeachreceiptoffuel;b. Thenameandaddressofthepersonfromwhompurchasedorreceived;c. Thenumberofgallonsreceived;d. Thetypeoffuel;e. Thevehicleorequipmentintowhichthefuelwasplaced;f. Allinformationforthereconciliationofbulkstorage;g. Bothtaxableandnon-taxableusageoffuel;h. Milestraveledfortaxableandnon-taxableuse;i. Mileagerecapsforeachvehicleforeachjurisdictioninwhichthevehicleoperated.

Mileageandfuelrecordedonthedriver’stripsheetorthedriver’slogshallbesummarizedmonthlybyequipmentnumbershowingthetotalnumberofmilesoperatedineachjurisdictioncoveringtheapplicablemileagereportingperiodandthefuelpurchasedineachjurisdiction.

Fromthemonthlysummaries,thelicenseeshallprepareayearlyrecapshowingthetotalfleetmilesandfuel,brokendownbymonthforeachjurisdiction,coveringtheapplicablereportingperiod.

DECLARATION

TheundersignedagreestomaintainrecordsinaccordancewithInternationalFuelTaxAgreementandtheInternationalRegistrationPlanfromtheoriginaldateoflicensinguntilsuchtimeastheIRPorIFTAaccountisnolongeractiveandthelicenseiscancelled.

(PrintedName)–AuthorizedCompanyRep–(Signature) Title

LicenseBusinessName AccountNumber Date

PR/IF 306 – 8/10

445 East Capitol Ave Pierre, SD 57501-3185

Sample Agreement to Maintain Records

14

Appendix (cont.)

Sample Power of Attorney

Sample Individual Vehicle Distance Fuel Report15

A C C O U N T I N G O R R E P O R T I N G F I R M A U T H O R I Z A T I O N F O R M / R E S P O N S I B L E P A R T Y

SouthDakotaDepartmentofRevenue DivisionofMotorVehicles 445EastCapitolAvenue

Pierre,SouthDakota57501-3100

PLEASEFILLOUTTHISFORMIFYOUHAVEANACCOUNTINGFIRMORREPORTINGSERVICECOMPILEYOURAPPLICA-TIONSANDRETURNFORYOU

Licensee’sarerequiredtofilereturns/applicationandpaytaxes/feesasitisowed.TheyarealsorequiredtoacceptandrespondtovarioustypesofofficialcommunicationswiththeDepartmentofRevenue. IfalicenseeprefersanAccountingorReportingfirmtofulfilltheseresponsibilities,thisauthorizationformistobecompleted.Thisisaprivilegeextendedtothelicenseewhichrequiresspecialhandlingbythedepartment,therefore,suchactionwillnotbeconsideredunlessthisformisproperlycompletedandplacedonfilewiththedepartment.However,thecompletionofthisformdoesnotrelievethelicenseeofthelegalobligationsassociatedwithaparticularlicense.Thelicenseeisultimatelyresponsibleforthepaymentofthetax/feeaswallasallactsandomissionsofthestatedAccountingorReportingfirm.

POWER OF ATTORNEY

KNOWALLMENBYTHESEPRESENT,thattheundersignedprincipalandlicenseehasmadeandappointed,anddoesherebymakeandappoint(FirmsName)_______________________________________________________

oragentsoremployees,withtheofficesat(MailingAddress)_________________________________________

_______________________________________________(PhoneNumber)_____________________________ toactasAttorney-in-Factfortheundersigned,whomakesthisappointmenteitherpersonallyorinanauthorizedrepresentativecapacityonbehalfofaprincipalpartnership,corporation,orotherentity;thispowerofattorneyshallbelimitedtothefollowingspecificpurposesinvolvingtheSouthDakotalicense(s)indicated:

Toprepare,signandfileapplicationswiththeDepartmentofRevenue. Toprepare,signandfilewiththeDepartmentofRevenueperiodictaxreturnsorreportsasrequiredbySouthDakotalaw. TocollectrefundsowedtotheprincipalbytheStateofSouthDakota. Totakelegalnoticeofalldelinquencies,cancellationlistingsandofficialmailingspreparedandsentbytheDepartmentofRevenue. Totakelegalnoticeofalltaxrate/feechanges. Topreserveallrecordsrequiredtobekeptbytheprincipalforthestatutoryperiodoftime. TorespondtocommunicationswhensuchresponsesarerequestedbytheDepartmentofRevenue. TotakelegalnoticeofallNoticesofIntenttoAudit. TopresenttoofficialsoftheDepartmentofRevenueallrecordsrequestedtobeinspected. TocooperateandassistallofficialsoftheDepartmentofRevenuewhiletheyareconductingallaudits. TotakelegalnoticeofallCertificatesofAssessment.

ThisPowerofAttorneyshallbeeffectiveuponreceiptthereofbytheDepartmentofRevenueandshallcontinueuntilcancelledbyfilingwiththedepartmentaninstrumentproperlyexecutedandrecitingsuchcancellation.

IN WITNESS WHEREOF,theundersignedhascausedthesepresenttobeexecuted,forbenefitoftheprincipalnamedbelow.

Pleasecheckthefollowinglicensesthatyouholdorareapplyingfor:

Tax License(s) Tax License(s) Numbers if Previously Assigned

_____InStateSupplier _________________________________________________ _____OutofStateSupplier _________________________________________________ _ _ _ _ _Importer _________________________________________________ _ _ _ _ _Exporter _________________________________________________ _____Blender _________________________________________________ _____Marketer _________________________________________________ _____LPGVendor _________________________________________________ _____CNGVendor _________________________________________________ _____LPGUser _________________________________________________ _____HighwayContractor _________________________________________________ _____IFTAAccount_________________________________________________ _____ProrateAccount _________________________________________________

Accounting or Reporting Firm By: Principle and Licensee By:

___________________________________________ ____________________________________ C o m p a n yName CompanyName

___________________________________________ ____________________________________ S igna tu re o fOwner/LegalRep./Title SignatureofOwner/LegalRep./Title

___________________________________________ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ FederalIDNumber FederalIDNumber

___________________________________________ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ Address-Mailing Address-Mailing

___________________________________________ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ City/State/Zip City/State/Zip

____________________________________________ ____________________________________ PhoneNumber PhoneNumber Indicate your preference for mailing address for IRP billings, licenses, and all other IRP material: Reporting Service_____ Licensee_____ Stateof______________________________) : ss. Countyof___________________________)

Onthis__________dayof______________,beforetheundersigned,aNotaryPublicfortheStateof

(month/year)

_______________________________________personallyappeared__________________________________knowntobethepersonwhosenameissubscribedtothewithininstrument,andacknowledgetomethat__heexecutedthesameincapacityasshown.

INWITNESSWHEREOF,Ihavesetmyhandandsealthis_____________dayof____________________,thiscertificateabovewritten (month/year) _________________________________________ NotaryPublic

DEPARTMENT OF REVENUE DIVISION OF MOTOR VEHICLES - IFTA

IF-10/12 445EastCaptitolAve;Pierre,SD57501

AGREEMENT TO FILE RETURNS IN A TIMELY MANNER

Thequarterlyreturnandpaymentshallbedueonthelastdayofthemonthfollowing quarter’s end. If the last day of the month falls on a Sunday or a holiday, thereturnandpaymentshallbedueonthenextworkingday.

Ifthereturnisnotfiledontime,thefollowingcollectionactivitybegins:1. AThirtyDayNoticeismailedinformingthelicenseethereturnhasnot

beenreceived.2. Ifthereturnisstilldelinquent,aJeopardyAssessmentisissuedafter30days

havepassedfromissuanceoftheThirtyDayNotice.3. If the return isstilldelinquentor payment infullon theJeopardy

Assessment is not made, a Tax Lien is filedafter 0 days havepassedfromthe issuance oftheJeopardyAssessment. Once a Tax Lien is filed, thelicense becomes suspended. A Tax Lien affectsyourcreditrating.

4. If the return still isn’t filed or payment in full on the Tax Lien is not made, aDistressWarrantisfiledafter30dayshavepassedfromthefilingoftheTaxLien.TheDistressWarrantgivestheCountySheriffauthoritytoseizefundsfrompersonalcheckingandsavingaccountstosatisfyamountowed.

Tobere-instatedafteranaccounthasbeensuspended,thefollowingisrequired:1. A$1,000cashbondwillberequiredtobefiledwiththeDepartmentof

Revenue.2. Anewapplicationwillneedtobecompletedaccompaniedby$10

reinstatement fee.3. Newdecalswillneedtobeorderedaccompaniedbyrequireddecalfees.4. AnewAgreementtoMaintainRecordsisrequired.5. AnewPowerofAttorneyisrequired.6. AnewAgreementtoFileReturnsisrequired.

(PrintedName)–AuthorizedCompanyRep–(Signature) Title

___________________ ________________ _______________License Business Name Account Number Date

16

State(SDCL20-13)andFederal(titleVIoftheCivilRightsActof1964,theRehabilitationActof1983asamended,andtheAmericanswithDisabilitiesActof1990)lawsrequirethattheDepartmentofRevenueprovideservicestoallpersonswithoutregardtorace,color,creed,religion,sex,disability,ancestry,ornationalorigin.

PrintedonRecycledPaper.The2015IFTAProceduresManualiswrittenanddesignedtomakelicensinginformationaccessibletothegeneralpublic.

Revised 2014

South Dakota Department of Revenue

IFTA445 E. Capitol Avenue | Pierre, South Dakota 57501-3185

Phone: (605) 773-3314 | Fax: (605) 773-8416 | http://dor.sd.gov | [email protected]