IFRS Revenue Recognition

20

Revenue Recognition under IFRS PwC

-

Upload

mohsin-jamal -

Category

Documents

-

view

157 -

download

5

Transcript of IFRS Revenue Recognition

Revenue Recognition under IFRS

PwC

8 November 2005Page 2AGiG

PricewaterhouseCoopers

Session Outline

• IAS 18 – key concepts

• IAS 18 – frequent issues

• Multiple elements revenue arrangements

• Principal – agent relationships

Revenue recognition under IFRS

8 November 2005Page 3AGiG

PricewaterhouseCoopers

Scope of IAS 18

Sale of goods

Rendering of services

Interest, royalties and dividends

Revenue arising from:

Revenue recognition under IFRS

8 November 2005Page 4AGiG

PricewaterhouseCoopers

Outside of scope

Lease agreement

Dividends arising from investments accounted for under the Equity method

Insurance contracts of insurance entities

Changes in the FV of financial assets and liabilities on their disposal

Changes in the value of other current assets

Initial recognition from changes in the FV of biological assets related to the agricultural industry

Initial recognition of agricultural produce

Extraction of mineral ores

Revenue recognition under IFRS

8 November 2005Page 5AGiG

PricewaterhouseCoopers

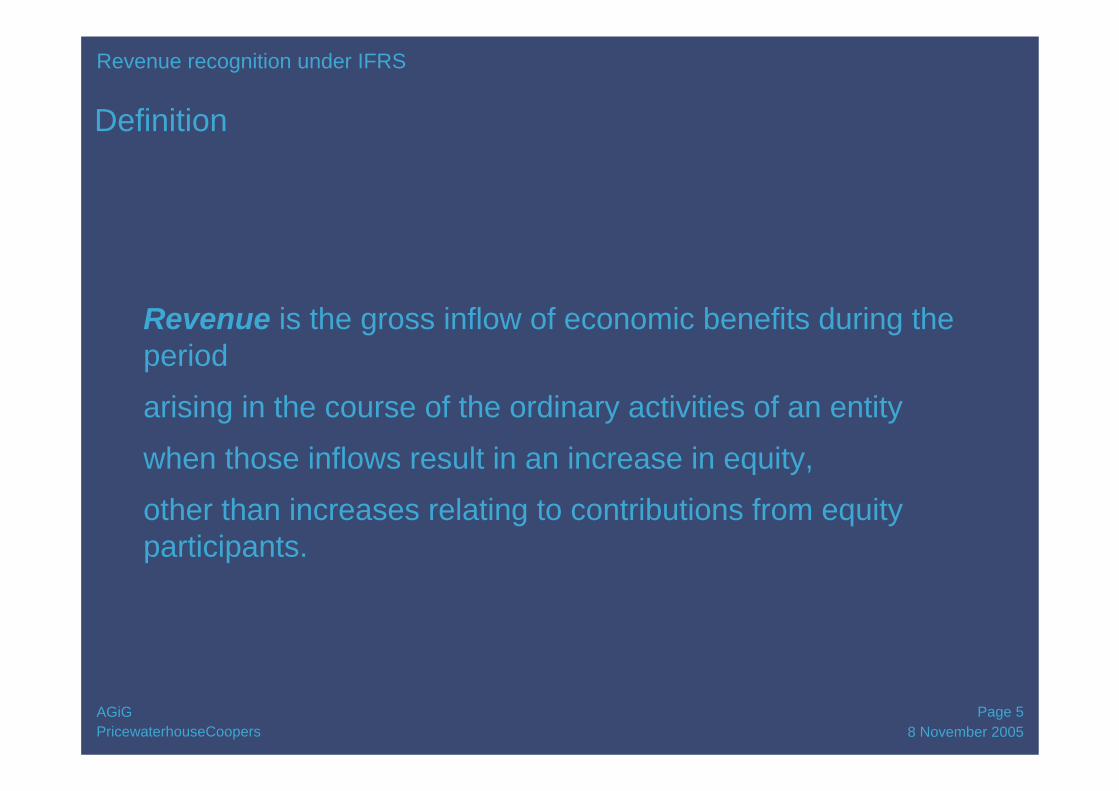

Definition

Revenue is the gross inflow of economic benefits during the period

arising in the course of the ordinary activities of an entity

when those inflows result in an increase in equity,

other than increases relating to contributions from equity participants.

Revenue recognition under IFRS

8 November 2005Page 6AGiG

PricewaterhouseCoopers

Appendix to IAS 18

‘Bill and hold’ salesGoods shipped subject to conditionsLay away – delivery occurs after final paymentSale and repurchase agreementsAgency transactionsInstalment salesServicing feesAdvertising commissionsFinancial service feesMembership feesLicense fees and royalties

Revenue recognition under IFRS

8 November 2005Page 7AGiG

PricewaterhouseCoopers

Sale of goods

Significant risks and rewards transferred

No continuing managerial involvement / effective control

Revenue can be measured reliably

Probable that economic benefits will flow to the entity

Costs can be measured reliably

Sale has occurred

Recognise revenue

Revenue recognition under IFRS

8 November 2005Page 8AGiG

PricewaterhouseCoopers

Rendering services

Percentage of completion method

Reliable estimate of outcome

Outcome not estimable

Recognised expected loss immediately

Recognise revenue according to stage of completion

Recognise revenue to extent of recoverable costs

Revenue recognition under IFRS

8 November 2005Page 9AGiG

PricewaterhouseCoopers

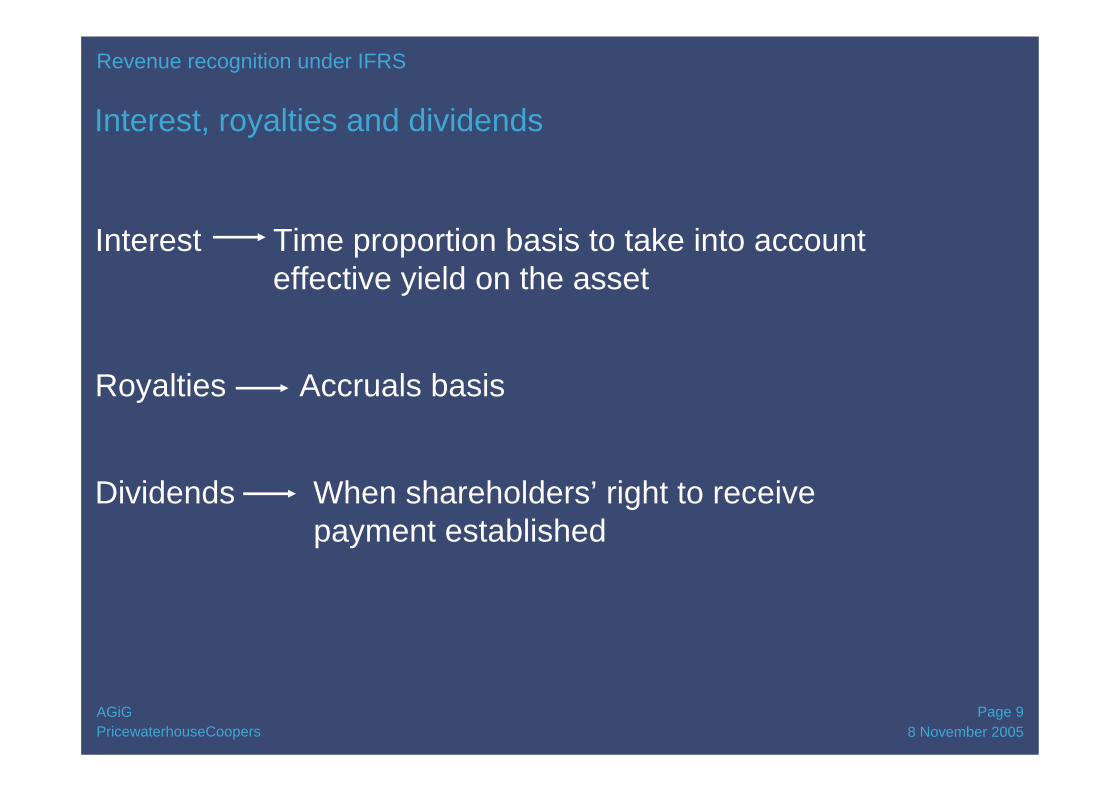

Interest, royalties and dividends

Interest Time proportion basis to take into account effective yield on the asset

Royalties Accruals basis

Dividends When shareholders’ right to receive payment established

Revenue recognition under IFRS

8 November 2005Page 10AGiG

PricewaterhouseCoopers

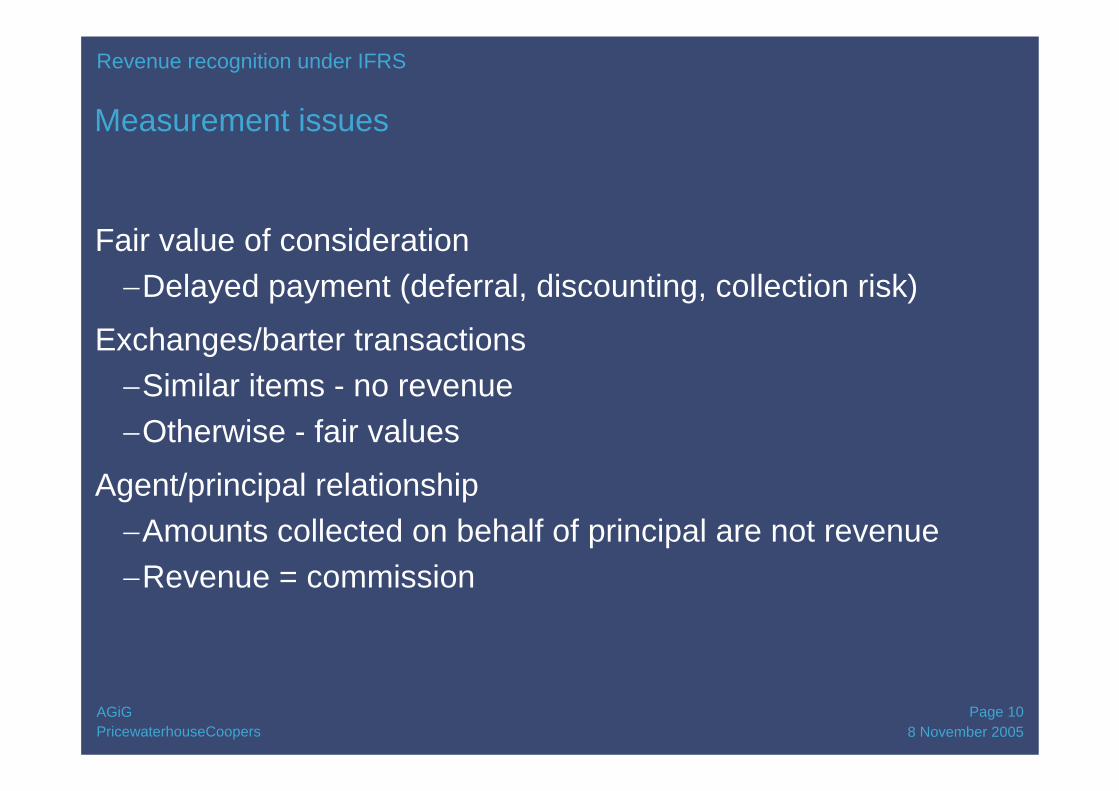

Measurement issues

Fair value of consideration−Delayed payment (deferral, discounting, collection risk)

Exchanges/barter transactions−Similar items - no revenue−Otherwise - fair values

Agent/principal relationship−Amounts collected on behalf of principal are not revenue−Revenue = commission

Revenue recognition under IFRS

8 November 2005Page 11AGiG

PricewaterhouseCoopers

Issues arise frequently in practice

• Revenue recognition issues are contentious in practice

• Business transactions are getting more complex

• IAS 11 and 18 have not changed significantly

• IASB has undertaken a project jointly with FASB; discussion paper is expected to be issued in Q3 2006

Revenue recognition under IFRS

8 November 2005Page 12AGiG

PricewaterhouseCoopers

Multiple-element revenue arrangements• Limited guidance – IAS 18 para 13:

• Identify components of one transaction to reflect substance

• Combine two transactions if their commercial effect cannot be understood otherwise

• Key issues • Which is the applicable standard?• Can the arrangement be divided into separately

identifiable components?• How should total consideration be allocated to the

separately identifiable components?• How should revenue be recognised for an arrangement

that is accounted for as a whole?

Revenue recognition under IFRS

8 November 2005Page 13AGiG

PricewaterhouseCoopers

Multiple-element revenue arrangementsExample - IT Platform

An IT company is developing a specialised IT platform for a customer.Work commenced 1 January 2005. At 31 December 2005, the hardware (which the IT company also sells separately) has been installed and the software is 50% completed. The IT company does not anticipate any problem with the software development, which should take another 6 months to complete. The customer has the right to return the hardware if the software does not work according to the customer’s specifications.

The contract as a whole is approximately 70% completed based on the costs incurred, which is a reliable measure of the services performed. Costs incurred to date and costs to complete can be measured reliably for the hardware and software separately and in total. The hardware and software account for 30% and 70% of thetotal consideration respectively.

Revenue recognition under IFRS

8 November 2005Page 14AGiG

PricewaterhouseCoopers

Multiple-element revenue arrangementsExample - IT Platform

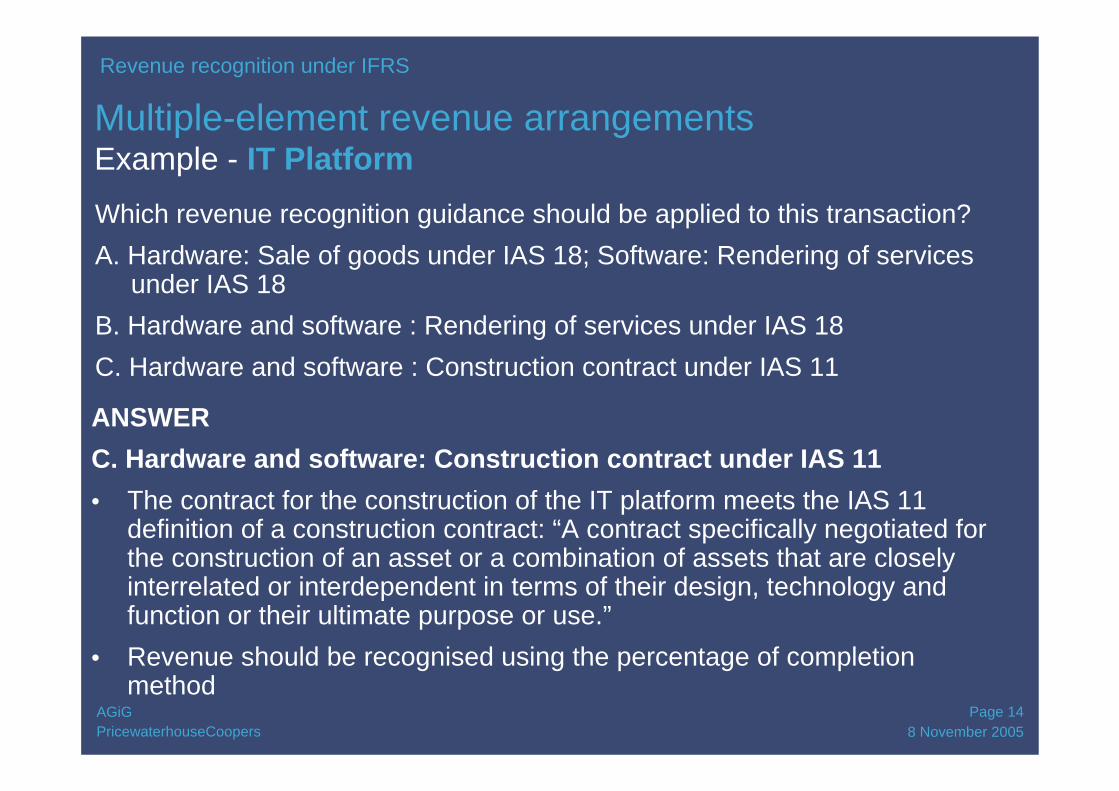

ANSWERC. Hardware and software: Construction contract under IAS 11• The contract for the construction of the IT platform meets the IAS 11

definition of a construction contract: “A contract specifically negotiated for the construction of an asset or a combination of assets that are closely interrelated or interdependent in terms of their design, technology and function or their ultimate purpose or use.”

• Revenue should be recognised using the percentage of completion method

Revenue recognition under IFRS

Which revenue recognition guidance should be applied to this transaction?A. Hardware: Sale of goods under IAS 18; Software: Rendering of services

under IAS 18B. Hardware and software : Rendering of services under IAS 18C. Hardware and software : Construction contract under IAS 11

8 November 2005Page 15AGiG

PricewaterhouseCoopers

Multiple-element revenue arrangementsKey points

• The applicable standard should be used

• Identify the key features of the transaction

• In assessing a transaction, consider:

Contractual terms

Other facts and circumstances

Revenue recognition under IFRS

8 November 2005Page 16AGiG

PricewaterhouseCoopers

Principal – agent relationships

Key indicators for principal (i.e. gross revenue reporting)

• Responsible for fulfilling orders by customers *

• Assumes general inventory risk *

• Flexibility in establishing prices

• Adds significant value

• Discretion in choosing suppliers

• Determines product or service specifications

• Assumes physical inventory loss risk and credit risk

• Margin earned is not fixed

US GAAP: * = strong indicators; IFRS: no order of priority – case by case

Revenue recognition under IFRS

8 November 2005Page 17AGiG

PricewaterhouseCoopers

A software company is required, for legislative reasons, to sell its proprietary software through a distributor. Customers order from the distributor, who then orders the necessary product from the software companyThe software company delivers the product directly to the customer.

The distributor makes a fixed percentage margin on each sale, but bears the credit risk associated with the sale of the software.The software company determines the sales price, but allows the distributor at its discretion to grant discounts based on an approved discount table.Upon shipment to the customer, the software customer bills the distributor taking into consideration any discounts that were agreed between customer and distributor in order to maintain the distributor’s fixed margin.

Revenue recognition under IFRS

The software sells for 120 per unit. The distributor’s fixed percentage margin is 10%. For ease of administration, the software company and the distributor net settle any amounts owed between parties under the contract.

Principal – agent relationshipsExample - Software company and its distributor

8 November 2005Page 18AGiG

PricewaterhouseCoopers

How much revenue should be recognised by the following companies for each unit of software sold?A. Software company = 120; Distributor = 12

B. Software company = 108; Distributor = 12

C. Software company = 108; Distributor = 120

ANSWERA. Revenue for Software company = 120; Revenue for Distributor = 12

for each unit of software sold.

Revenue recognition under IFRS

Principal – agent relationshipsExample - Software company and its distributor

• Credit risk alone is not sufficient to overcome other indicators that software company is the principal in the relationship

• The distributor is acting as an agent for the software company for the sale of the software units.

8 November 2005Page 19AGiG

PricewaterhouseCoopers

No order of priority for the indicators

Depends on facts and circumstances

Cash received may not be equal to revenue

Principal – agent relationshipsKey points

Revenue recognition under IFRS

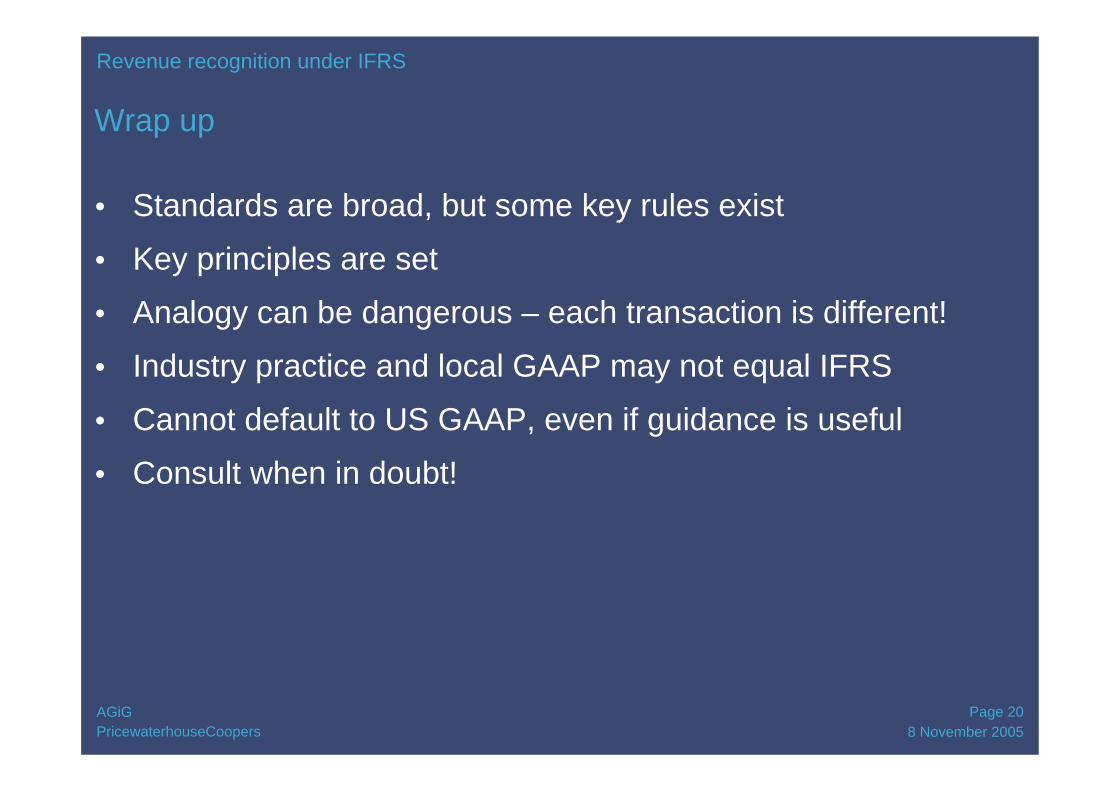

8 November 2005Page 20AGiG

PricewaterhouseCoopers

Wrap up

• Standards are broad, but some key rules exist

• Key principles are set

• Analogy can be dangerous – each transaction is different!

• Industry practice and local GAAP may not equal IFRS

• Cannot default to US GAAP, even if guidance is useful

• Consult when in doubt!

Revenue recognition under IFRS