IFRS 15 Revenue from contracts with customers - ICPAK · IFRS 15 –Revenue from contracts with...

68

IFRS 15 – Revenue from contracts with customers Presentation by: CPA Freda Mitambo Partner, Deloitte & Touche Uphold public interest

Transcript of IFRS 15 Revenue from contracts with customers - ICPAK · IFRS 15 –Revenue from contracts with...

IFRS 15 – Revenue from contracts with customers

Presentation by:CPA Freda Mitambo

Partner, Deloitte & Touche

Uphold public interest

Why IFRS 15 is important

2

What does it mean for clients?

• Revenue recognition principles will change

• P/L may vary to a certain extent

• IT Systems, Accounting Policies, Internal Processes and Controls may be subject to change

What do I need to know now?

• Key challenges

New estimates & judgments required

Retrospective application includes associated data gathering analysis

Change of systems, processes and internal controls

• Key advisory opportunities

• Training services, consulting on IT systems, tax planning and more

What is it?

• More detailed guidance on revenue recognition which involve significant judgments

• Effective on 1/1/2018 with retrospective application

What does it mean for auditors?

• Identify the key impacts on your clients

• Early discussion with clients on the key impacts and help your clients prepare for the changes

Clients

Ch

alle

ng

e/

Op

po

rtu

nity

Auditors

Key fa

cts

IFRS 15

3

The Time is Now!

1 January 2017

Date of initial application

1 January 2018

First annual financial statements in

accordance with IFRS 15

31 Dec 2018

4

STEP 1 Identify the contract with the customer

Five-step Model Framework

• Paragraph 9 lists the criteria which must all be met to qualify as a contract with a customer

• Entities will need to consider whether the contract should be combined with other contracts for accounting purposes

5

Step 1 – Identify the contract with a customer

A legally enforceable contract (incl. oral or implied) must meet all of the

following requirements:

A contract is outside the scope if:

Contracts are approved and the

parties are committed to perform.

Payment terms can be identified.

It is probable that the entity will

collect the consideration to

which it will be entitled.

Each party’s rights can be

identified.

Commercial substance.

The contract is wholly unperformed and Each party can unilaterally terminate the

contract without compensation

6

Five-step Model Framework

• An entity will typically identify all the distinct goods or services, or contract deliverables, which have been promised. They may be implicitly or explicitly promised in a contract –these are “performance obligations”

• A good or service promised is distinct, if the good or service is capable of being distinct and the promise to transfer the good or service is distinct within the context of the contract.

STEP 2 Identify the performance obligations in the contract

Identify all (incl. implicit) promised goods/services in the contract

Step 2: Identifying performance obligations

Is the good/service distinct?

Can the customer benefit from the good or service on

its own or together with other readily available

resources?

Is the good or service separately identifiable from

other promises in the contract?

Account for as a separate performance obligation

Combine two or more promised goods or services

YES NO

CAPABLE OF BEING

DISTINCT

DISTINCT IN CONTEXT

OF CONTRACT

Step 1 Step 2 Step 3 Step 4 Step 5

AND

7

8

Five-step Model Framework

• IFRS 15 typically bases revenue on the amount to which an entity expects to be entitled rather than the amount that it expects ultimately to collect (includes both fixed andvariable consideration)

• Variable consideration will only be included in the transaction price to the extent that an entity expects it to be “highly probable” that the resolution of the associated uncertainty would not result in a significant revenue reversal (the “constraint”)

STEP 3 Determine the transaction price

Transaction price

The transaction price would

not be reduced for the

effects of customer credit

risk.

Excluding credit risk

Variable considerationConsideration amount to which an entity

expects to be entitled in exchange for

transferring promised goods or services to

a customer.

Definition

The amount is fixed and not

contingent on the outcome of

future events.

Fixed consideration

• Consideration in a form other than

cash

• Shall be measured at FV

Non-cash consideration

Significant benefit of financing

• Estimated and

potentially constrained

• e.g., discounts, rebates,

refunds, etc.

Step 3: Determining the transaction priceStep 1 Step 2 Step 3 Step 4 Step 5

What is the transaction price? What does it include?

Consideration payable

to customers

• If identified, leads to adjustment in

transaction price.

• Practical expedient available.

Reduces transaction

price unless payment is

made for a distinct

good/service.

10

Five-step Model Framework

• After determining the transaction price at Step 3, Step 4 specifies how that transaction price is allocated between the different performance obligations identified in Step 2.

• Previously, IFRSs included very little in the way of requirements on this topic, whereas IFRS 15 is reasonably prescriptive.

STEP 4 Allocate the transaction price to the performance obligations

Determine standalone selling

price

• Estimate the price if unobservable

• Acceptable methods:> Adjusted market assessment approach >Expected cost plus a margin approach >Residual approach

Allocate the transaction price

• Allocate the transaction price to each performance obligation on a relative stand-alone selling price basis.

• Allocate discounts proportionally to all performance obligations unless certain criteria are met.

• Allocate variable consideration and changes in transaction price to all performance obligations unless two criteria are both met.

• Do not reallocate changes in standalone selling price after inception.

Step 4: Allocating the transaction price Step 1 Step 2 Step 3 Step 4 Step 5

Only allowed in limited circumstances

Maximize the

use of

observable

inputs and

apply

consistently

12

Five-step Model Framework

• The final step is to determine, for each performance obligation, when revenue should be recognized. This may be over time or at a point in time.

• Paragraph 35 outlines the criteria, of which one must be met, for revenue to be recognized over time.

STEP 5 Recognize revenue when (or as) each performance obligation is satisfied

Step 5: Recognizing revenue

The seller’s performance creates or

enhances an asset controlled by the

customer.

Performance satisfied over time = Revenue recognized over time

The seller does not create an asset that has

an alternative use to the seller and the seller has the right to be paid

for performance to date.

OR

Revenue recognized at a point in time

The customer simultaneously

receives and consumes the benefit of the

seller’s performance as the seller performs.

IF NOT

Step 1 Step 2 Step 3 Step 4 Step 5

OR

14

Audit Risk Assessment – Transition Versus Ongoing

Full retrospective

method

Modified retrospective

method

Risks relating to transition

Risks relating to on-going application

Modified Contracts

Completed contracts

Completed contracts with variable consideration

Transaction price allocated to remaining performance obligation

Practicalexpedientsfor:

Applies IFRS 15 retrospectively to all comparative periods presented. When chosen:

Full Retrospective Method

Prior yearcomparativesare restated

Practical Expedient:Modified contracts

Only contracts that are open at the date of initial application

Choose to apply the requirements to:

Modified Retrospective Method

All contracts at the date of initial application

OR

S3 17

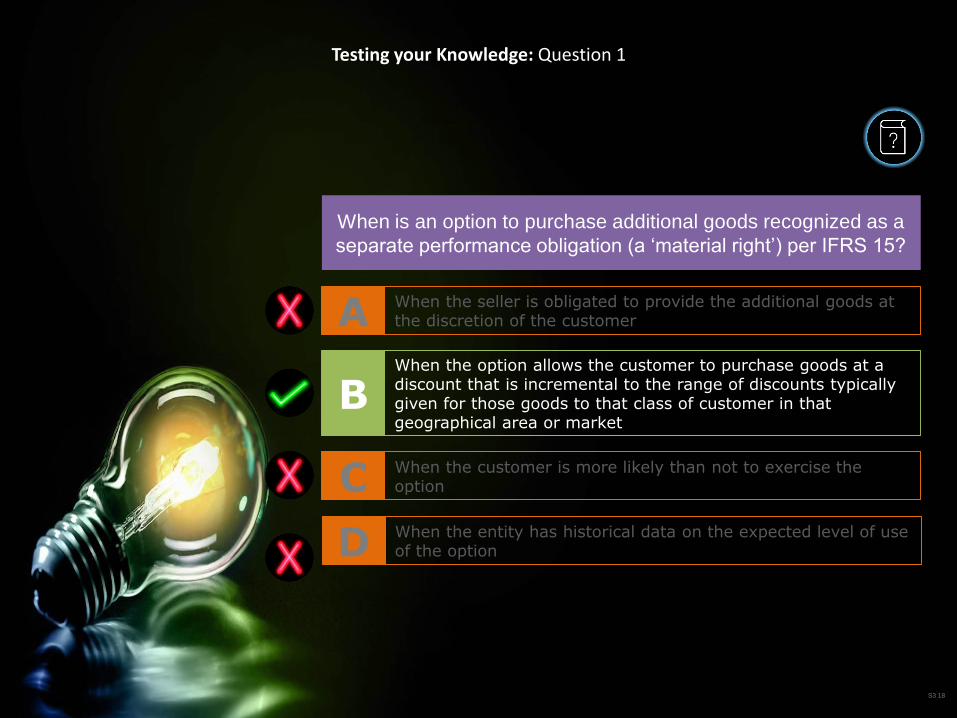

When is an option to purchase additional goods recognized as a separate performance obligation (a

‘material right’) per IFRS 15?

When the seller is obligated to provide the additional goods at the discretion of the customerAWhen the option allows the customer to purchase goods at a discount that is incremental to the range of discounts typically given for those goods to that class of customer in that geographical area or market

B

When the customer is more likely than not to exercise the optionCWhen the entity has historical data on the expected level of use of the

optionD

Testing your Knowledge: Question 1

S3 18

When the seller is obligated to provide the additional goods at the discretion of the customerAWhen the option allows the customer to purchase goods at a discount that is incremental to the range of discounts typically given for those goods to that class of customer in that geographical area or market

B

When the customer is more likely than not to exercise the optionCWhen the entity has historical data on the expected level of use of the optionD

Testing your Knowledge: Question 1

When is an option to purchase additional goods recognized as a

separate performance obligation (a ‘material right’) per IFRS 15?

S3 19

Which of the following criteria must be met to capitalize the costs of fulfilling a contract in accordance with IFRS

15 (assuming the costs are not within the scope of another standard)?

The costs relate directly to a specifically identifiable contractA

The costs generate or enhance resources that will be used in satisfying the contractB

The costs are expected to be recoveredC

The costs relate to satisfied performance obligations D

Testing your Knowledge: Question 2

Select all that apply

S3 20

Which of the following criteria must be met to capitalize the costs of fulfilling a contract in accordance with IFRS

15 (assuming the costs are not within the scope of another standard)?

The costs relate directly to a specifically identifiable contractA

The costs generate or enhance resources that will be used in satisfying the contractB

The costs are expected to be recoveredC

The costs relate to satisfied performance obligations D

Testing your Knowledge: Question 2

Select all that apply

S3 21

How does IFRS 15 deal with variability that is linked to

customer actions or choices?

If a contract gives a customer the option to purchase additional distinct goods or services, those goods or services are not treated as performance obligations.

Instead, consider whether customer option gives rise to a

material right. If it does, the material right itself (and not

underlying goods or services) should be treated as a

performance obligation.

Highlight - Case Study 1: Key Areas of Focus

S3 22

Background

Force manufactures and sells aircraft engines and parts.

Unlike its competitors, Force does not build its engines or

spare parts on a contract by contract basis. Force delivers

within a 30-day timeframe and therefore has aircraft

engines and spare parts on hand, ready for immediate

delivery. Force frequently sells spare parts separately from

the engines and vice versa.

FlyJet is a commercial airline which travels internationally.

Note: the below contract has been assessed as being

within the scope of IFRS 15 and the assessment has been

adequately documented in the audit file.

S3 23

Contract

Force has entered into a written contract with FlyJet to

sell:

10 aircraft engines for $12 million each (excl. sales

tax) and

20 specific aircraft engine spare parts (part XY002) for

$300,000 each (excl. sales tax)

The 10 engines will be delivered together before the

end of December 2018. The 20 spare parts will be

delivered together during January 2019.

The 20 spare parts are for future replacement

purposes, as and when needed. Additionally, in the

contract, FlyJet has the option to buy additional XY002

parts (beyond the 20) for the next 5 years. Other

engine spare parts can also be purchased by FlyJet,

however these would be purchased outside of this

contract. The purchase of the optional spare parts is at

the discretion of FlyJet, but Force is obligated to

provide these optional spare parts if requested.

S3 24

Contract

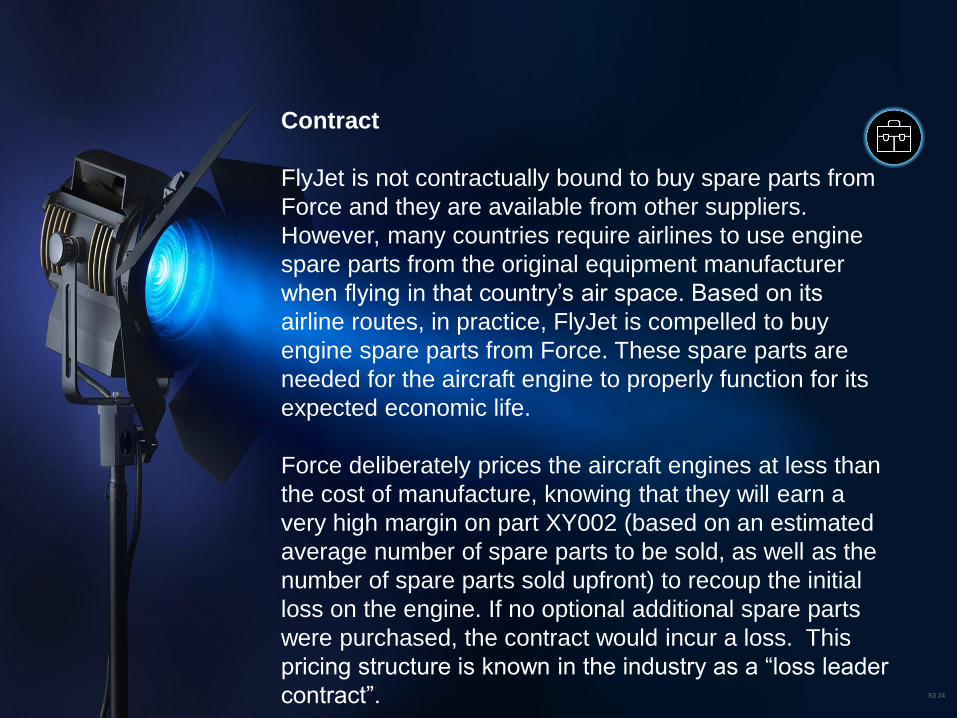

FlyJet is not contractually bound to buy spare parts from

Force and they are available from other suppliers.

However, many countries require airlines to use engine

spare parts from the original equipment manufacturer

when flying in that country’s air space. Based on its

airline routes, in practice, FlyJet is compelled to buy

engine spare parts from Force. These spare parts are

needed for the aircraft engine to properly function for its

expected economic life.

Force deliberately prices the aircraft engines at less than

the cost of manufacture, knowing that they will earn a

very high margin on part XY002 (based on an estimated

average number of spare parts to be sold, as well as the

number of spare parts sold upfront) to recoup the initial

loss on the engine. If no optional additional spare parts

were purchased, the contract would incur a loss. This

pricing structure is known in the industry as a “loss leader

contract”.

S3 25

Contract

The standalone price of the aircraft engine is $20

million each. When Force sells the aircraft engines

by themselves (without the spare parts), the aircraft

engines are sold at a profit. The spare parts are not

sold at a discount to their standalone selling price.

Force estimates that a total of 75 optional spare parts

will be purchased by FlyJet and that the profits on the

spare part sales will more than compensate for the

discount on the selling price of the aircraft engines.

This is based on Force’s historical statistical

evidence of selling a large number of spare parts.

S3 26

Highlight - Case Study 1: Guide 1 Background

Force contracts with FlyJet to sell

• 10 aircraft engines for $12 million each

• 20 spare parts for $300,000 each

• FlyJet option to purchase additional specific spare parts

• Loss leader contract – aircraft engines priced at less than the cost of manufacture, in anticipation of spare parts securing profits

• Estimated sale of 75 optional spare parts over 5 years

S3 27

Highlight - Case Study 1: Guide 1 Solutions

STEP 2 Identify the performance obligations in the contract

STEP 3 Determine the transaction price

STEP 4 Allocate the transaction price to the performance obligations

S3 28

Highlight - Case Study 1: Step 2

Is the good or service distinct within the context

of the contract?

IFRS 15.10 - A contract is an agreement between two or more parties that creates

enforceable rights and obligations

REMINDER

Is the good or service capable of being distinct?

Identify material(explicit and implicit)

promised goods and services

S3 29

Highlight - Case Study 1: Step 2

Is the good or service distinct within the context

of the contract?

• 10 aircraft engines are

capable of being distinct and

distinct within context of

contract; and

• 20 spare parts are capable of

being distinct and distinct

within context of contract.

Is the good or service capable of being distinct?

Identify material(explicit and implicit)

promised goods and services

S3 30

Highlight - Case Study 1: Step 3

IFRS 15.10 defines a contract as an agreement

between two or more parties that creates enforceable

rights and obligations

Optional additional spare parts are not sold at discount to their stand-alone selling price. There is no material right to

customer and option will not be accounted for as a performance obligation

Force’s assessment of optional additional spare parts as a separate performance obligation is incorrect

S3 31

Highlight - Case Study 1: Step 3

Optional goods or services that are distinct:

•Exclude from performance obligations

•Exclude associated amounts payable from transaction price

•Assess whether material right

Variable goods or services that are not distinct:

• Include within performance obligation of which they form

part

• Treat variable amounts payable by customer as variable

consideration

S3 32

Highlight - Case Study 1: Step 3

The transaction price should only include amounts (including variable amounts)

to which the entity has rights under the present contract.

The transaction price is therefore $126 million:

• 10 aircraft engines at $12 million each• 20 spare parts at $300,000 each

S3 33

Highlight - Case Study 1: Loss Incurred on Aircraft Engines

An entity should recognize as expenses when incurred costs that relate to satisfied performance obligations (or partially satisfied performance obligations) in the contract

REMINDER

Full costs for sale of 10 aircraft engines and 20 spare parts should therefore

be expensed upon sale

S3 34

Highlight - Case Study 1: Step 2

Should the optional additional spare parts expected to be sold be included within the

performance obligations under the contract?

Is the option to purchase the spare parts a material right?

S3 35

Highlight - Case Study 1: Step 3

Should the estimated sales of the optional spare parts be included in the transaction

price as management proposes?

If the estimated sales relating to the optional spare parts are not included as performance

obligations in the original contract, how should the loss incurred on the aircraft

engines be treated? Could this be capitalized or is it required to be expensed?

Expensed

S3 36

Engines

Spare parts

Total stand-alone selling price

Engines

Spare parts

Transaction price

Allocation of the transaction price to the performance obligations

$200 million

$6 million

$206 million

$122.3 million

$3.7 million

$126 million

Highlight - Case Study 1: Step 4

37

Factors to Consider

© 2017. For information, contact Deloitte Touche Tohmatsu Limited. S3 37

Degree of judgment /

objectivity in accounting

process

Accounting and reporting complexities

Complexity / simplicity of

related calculations

Degree of complexity or

judgment

The complexity of transactions

Size and composition

of the ABCOTD

Volume of activity,

complexity, and whether homogenous

Nature of the ABCOTD

Effect of quantitative

and qualitative

factors

Economic, accounting,

or other developments

Exposure to losses

Changes from the

prior period

Susceptibility to

misstatement due to error

or fraud

Transactions outside of

normal course of business

Risk of fraudExistence of Related Party Transactions

Possibility of Significant Contingent liabilities

Degree of automation /

Manual intervention

Degree of complexity and

judgment

Nature and composition of the

ABCOTD

Economic, internal and historic

factors

Audit Considerations

Factors to consider when identifying and assessing RoMMs

Evaluate the client’s risk assessment

Management estimates

IFRS 16 - Leases

Uphold public interest

•

Lessor accounting largely unchanged

One single

measurement

model

Determination of

whether a

contract contains

or is a lease

Two main changes are…

Lessor

and

Lessee

Lessee

What is the impact of IFRS 16 on clients?

Introduction

1 Jan 20191 Jan 2018

December year-ends:

Retrospective application

with restatement

Disclosure – reasonably estimable information (up to effective date)

December year-ends:

Effective date

Entities can elect to apply full retrospective approach or a ‘modified’ retrospective approach (with no restatement of comparatives)

31 Dec 2016

Introduction

Timeline to transition

PRACTICAL EXPEDIENT

Early adoption may

be permitted

Permits both lessees and lessors not to reassess whether a contract is, or contains a lease at the date of initial application.

Why now?

Introduction

Client impact and changes

KEY CLIENT ADVICE

Systems

Processes

Controls

Metrics

Key accounting focus areas

IFRS 16 versus IAS 17

T

e

x

t

Focus on

lessees

Definition of

a lease

Measuring the

lease liability

All leases now on the

statement of financial

position

IFRS 16 versus IAS 17Identification of a lease

IFRS 16 changesIFRS 16 retains

Definition of a lease Application of the definition

A contract, or part of a contract, that

conveys the right to use an asset for

a period of time in exchange for

consideration.

Concept of control is introduced

Identifying a lease may require significant judgment

Definition of a leaseIFRS 16 versus IAS 17

Is it a lease?

Identified asset Right to control the use of

identified asset

and

Right to obtain substantially all economic benefits from use

Right to direct the use

whether the customer has the right to control the use of an identified asset for a period of time.

IFRS 16 versus IAS 17Expected impact

Treatment under IAS 17

Expected conclusion under IFRS 16

Contracts that are or contain a lease

Generally, the same

Significant judgment was applied

Possibly different

IFRS 16 versus IAS 17

This is dummy text it is

not here to be read.

This is dummy text it is

not here to be read.

This is dummy text it is

not here to be read.

This is dummy text it is

not here to be read.

1This is dummy

text it is not here

to be read. This is

dummy text it is

not here to be

read. This is

dummy text it is

not here to be

read.

2Leases

recognized on

statement of

financial position

Service contracts

recognized on

income statement

Operating lease

and service

component both

recognized on

income statement

IFRS

16

IAS

17

Non-lease

component

Identified and accounted for separately

from the lease component

Separating components

PRACTICAL EXPEDIENT

KEY CLIENT ADVICE

IFRS 16 versus IAS 17

Income statement

EBITDA XXXDepreciation XXXFinance cost XXX

Profit before tax XXX

Statement of Financial Position

Lease assets XXX

Lease liabilities XXX

Income statement

Lease payments XXX

EBITDA XXX

Profit before tax XXX

Statement of Financial Position

IAS 17 IFRS 16

Obligation to

make lease

payments

Right to use

underlying leased

asset

Depreciation on

lease assets and

finance cost of

lease liability

Single measurement model

Off-balance sheet

IFRS 16 versus IAS 17

Total assets

Total liabilities

• Significant impact on entities with material off-balance sheet leases.

• Impact on net assets

42,000

44,000

46,000

48,000

50,000

52,000

54,000

56,000

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5

Statement of Profit or Loss and OCI

IFRS 16 IAS 17

Finance costs

Operating costs

EBITDA

• Expenses are weighted towards at start of lease term and decrease as the lease matures (straight-line depreciation).

• EBITDA increases regardless of the entity’s lease portfolio.

IFRS 16 versus IAS 17• Areas of judgment

Most significant areas of judgment

Present value of

expected payments at

end of lease

Lease

liabilityPresent value of

lease rentals

Present value of future lease payments

Discount rate • Rate implicit in the lease• Incremental borrowing rate

Lease term

Non-cancellable term of the lease +periods covered by an option to extend and the option to terminate the leases

These concepts have

not changed

IFRS 16 versus IAS 17

The rate of interest that causes the PV of the lease payments and the

unguaranteed residual value to equal the sum of the FV of the

underlying asset and any initial direct costs of the lessor.

The interest

rate implicit in

the lease

Use the lessee’s incremental

borrowing rate.

If the implicit interest rate

cannot be determined…

Determining the discount rate

Revised discount rateAs a result of re-measurement of lease

liability

Discount rate at commencement

date

JUDGMENT

© 2017. For information, contact Deloitte Touche Tohmatsu Limited.

IFRS 16 versus IAS 17

JUDGMENT

Change in assessment of

option to purchase

Events to

remeasurement

Change in lease term

Changes in future lease payments

Change in residual value guarantee

• Re-measuring the lease liability

A lessee shall determine the revised discount rate and shall remeasure the lease liability by

discounting the revised lease payments

NO LONGER possible to compute a lease amortization schedule and simply roll that schedule

forward

Transition options

IFRS 16 versus IAS 17

A Apply a single discount rate to a portfolio of leases

Leases ending within 12 months of the date of initial application

Use hindsight in determining the lease term

Cumulative catch-up approachFor leases previously identified as operating leases

Lessees and lessors are permitted to grandfather assessments regarding whether a

contract existing at the date of initial application contains a lease.

Adjust the right of use asset by the amount of provision for onerous leases

Exclude initial direct costs

Full retrospective approachNo reliefs available

IFRS 16 transition implications

22

Impacts on client’s environment and audit risk assessment

IFRS 16 transition implications

Impact client’s

environmentKey accounting

focus areas

Impacts the audit risk

assessment

An effective risk assessment requires a deep understanding of the entity, its environment and its internal control.

Client’s decisions

Determining ROMMs

IFRS 16 transition implications

1

2

3

Degree of complexity and judgment

Nature and composition of the Account Balances, Classes of

Transactions and Disclosures

Economic, internal and historic factors

To assess ROMMs auditors need to understand our clients, their environment, internal

controls and their lease transaction process

Understanding the client’s selection and application of accounting policies

IFRS 16 transition implications

Processes Systems

MetricsControls

Process changes may

be required to capture

the data necessary to

comply with accounting

and disclosure

requirements

Changes to systems

and processes will result

in clients’ revisiting their

existing internal controls

to determine whether

they are still adequate

Lessees may need to

consider implementing a

contract management

module for leases

This could impact debt

covenants, tax balances

and an entity’s ability to

pay dividends

Impact on processes

IFRS 16 transition implications

Business

strategies

may change2Update

policies and

manuals3

Time and

effort to

gather data1

Education to

ensure policies

and procedures

are applied

consistently4

Update

policies and

manuals3

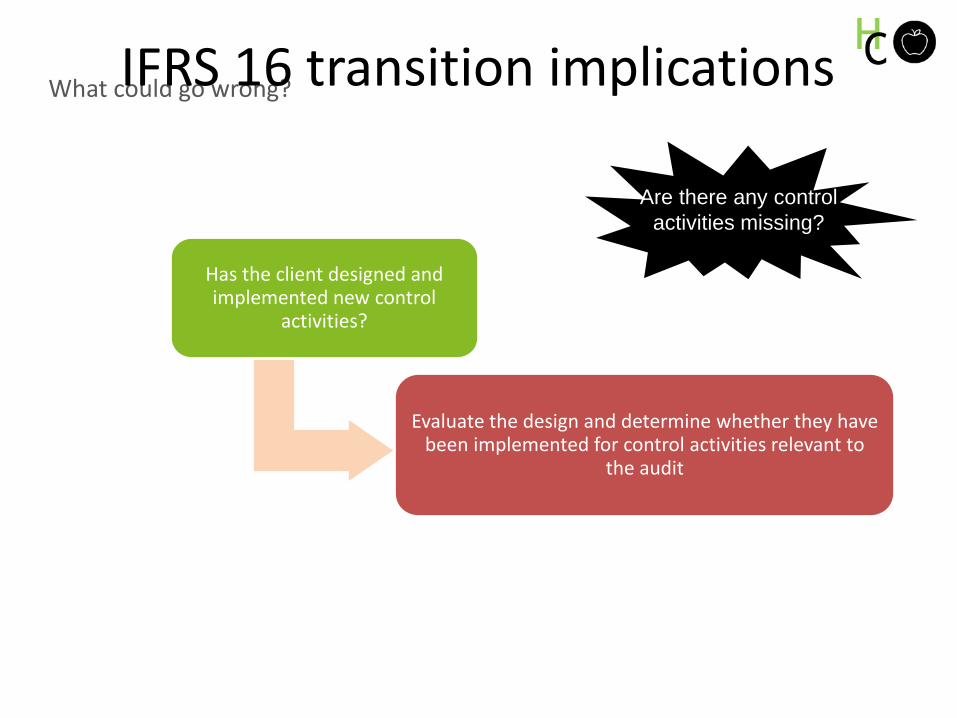

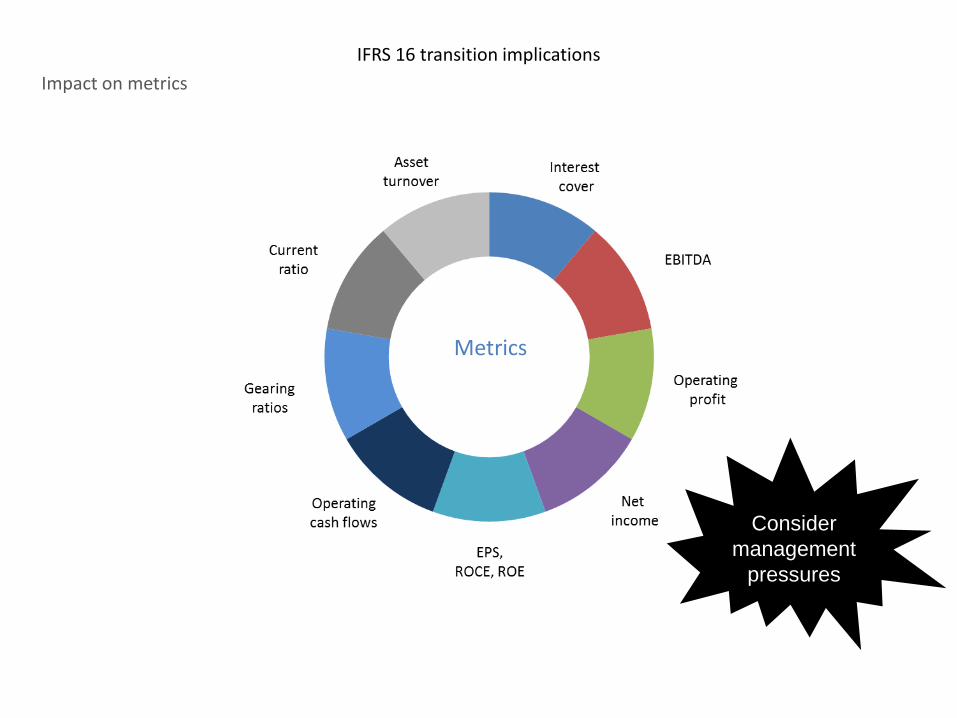

What could go wrong?

IFRS 16 transition implications

Not all lease

contracts are

captured and

recorded

(on-going

application) 1

A re-

measurement in

variable lease

payments is not

recorded2

Incorrectly

measuring the

lease term3

IFRS 16 has more data requirements for calculation and disclosure purposes. Clients need to assess adequacy of current systems.

Must ensure there is adequate time to allow for testing to avoid any last minute unforeseen problems

May be circumstances that further complicate IT system requirements

Systems need to be

able to store and

update the data on

an ongoing basis

Involvement of

IT specialists

Impact on systems

IFRS 16 transition implications

What could go wrong?

IFRS 16 transition implications

Assessing

susceptibility to

misstatement

We need to determine if clients have processes to identify risks as a result of adopting IFRS 16 and whether appropriate controls are in place.

Auditors

Impact on controls

IFRS 16 transition implications

What could go wrong?IFRS 16 transition implications

Has the client designed and implemented new control

activities?

Evaluate the design and determine whether they have been implemented for control activities relevant to

the audit

Are there any control

activities missing?

IFRS 16 transition implications

Impact on metrics

Metrics

Consider

management

pressures

IFRS 16 transition implications

What could go wrong?

IFRS 16

IAS 17

EBITDA

Management bias?

What areas

impacted?

IFRS 16 transition implications

Other considerations on transition

ROMMs may be a one-time risk on

transition

First time recognition may pose highest risk

Do not underestimate the time and

resources involved

10 Key questions for management

Getting your client ready

3

4

5

2

1

8

9

10

7

6

Do you know what discount rates you will be using for your different leases?

Do you know which transition reliefs are available, and whether you will apply any of them?

Have you considered whether your leasing strategy requires revision?

Have you considered the impact of the changes on financial results and position?

Are systems and processes capable of monitoring leases and keeping track of the required ongoing assessments?

How will you communicate the impact to affected stakeholders?

Have you considered the potential use of IFRS 16’s recognition exemptions and practical expedients?

Have you planned when you will consider the tax impacts?

Do you know which of the entity’s contracts are, or contain, a lease?

Are your systems and processes capturing all the required information?

Questions?