IFA/CIOT 18 th Cross Atlantic and European Tax Symposium BEPS and MNCs Lydia Challen – Allen &...

36

IFA/CIOT 18 th Cross Atlantic and European Tax Symposium BEPS and MNCs Lydia Challen – Allen & Overy Keith Brockman – Mars Anne Starck – HMRC Peter Adriaansen – Loyens & Loeff Jean Schaffner – Allen & Overy

-

Upload

sheena-booth -

Category

Documents

-

view

222 -

download

1

Transcript of IFA/CIOT 18 th Cross Atlantic and European Tax Symposium BEPS and MNCs Lydia Challen – Allen &...

IFA/CIOT 18th Cross Atlantic and European Tax Symposium

BEPS and MNCsLydia Challen – Allen & OveryKeith Brockman – MarsAnne Starck – HMRCPeter Adriaansen – Loyens & LoeffJean Schaffner – Allen & Overy

© Allen & Overy 2014

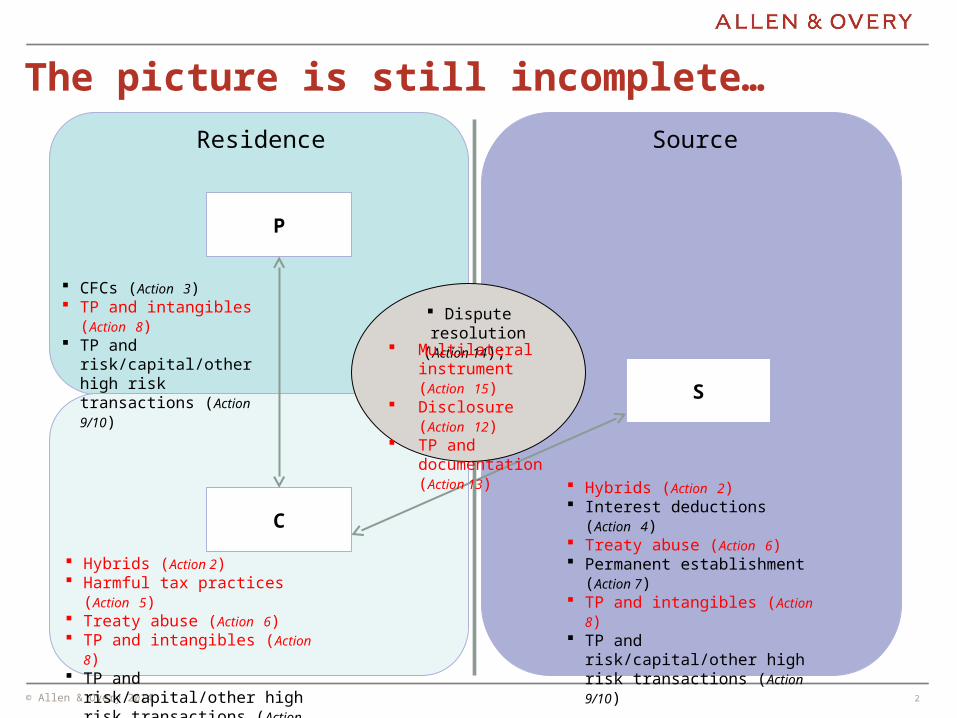

The picture is still incomplete…

2

Residence

P

C

S

Source

CFCs (Action 3) TP and intangibles (Action 8) TP and risk/capital/other

high risk transactions (Action

9/10)

Dispute resolution(Action 14);

Multilateral instrument (Action 15)

Disclosure (Action 12) TP and

documentation (Action 13)

Hybrids (Action 2) Harmful tax practices (Action 5) Treaty abuse (Action 6) TP and intangibles (Action 8) TP and risk/capital/other high

risk transactions (Action 9/10)

Hybrids (Action 2) Interest deductions (Action 4) Treaty abuse (Action 6) Permanent establishment (Action

7) TP and intangibles (Action 8) TP and risk/capital/other high

risk transactions (Action 9/10)

© Allen & Overy 2014

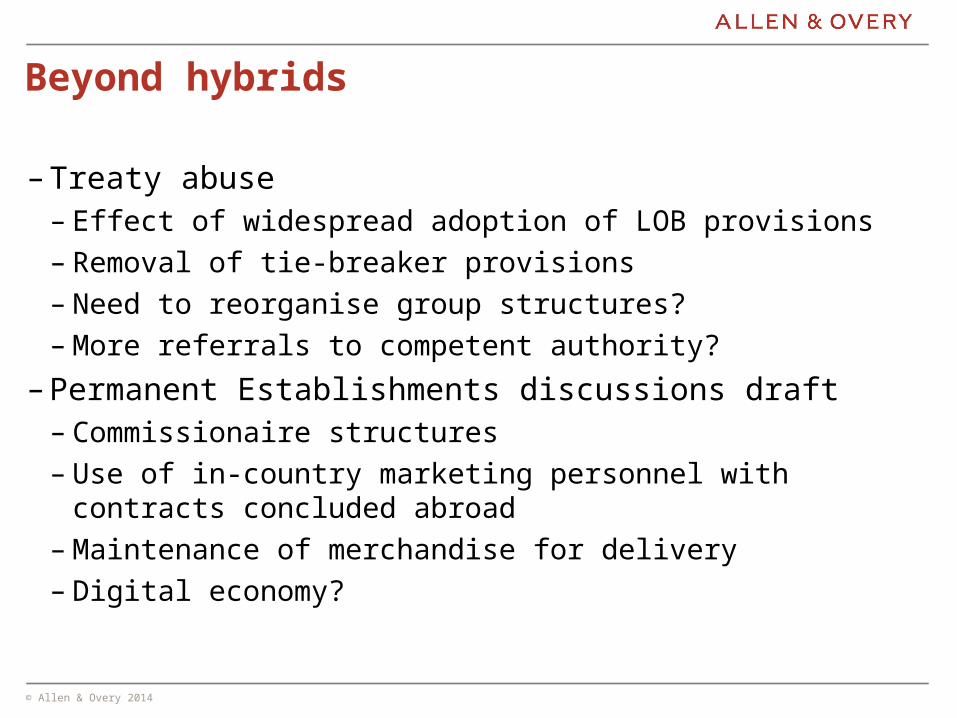

Beyond hybrids

– Treaty abuse– Effect of widespread adoption of LOB provisions

– Removal of tie-breaker provisions

– Need to reorganise group structures?

– More referrals to competent authority?

– Permanent Establishments discussions draft– Commissionaire structures

– Use of in-country marketing personnel with contracts concluded abroad

– Maintenance of merchandise for delivery

– Digital economy?

© Allen & Overy 2014

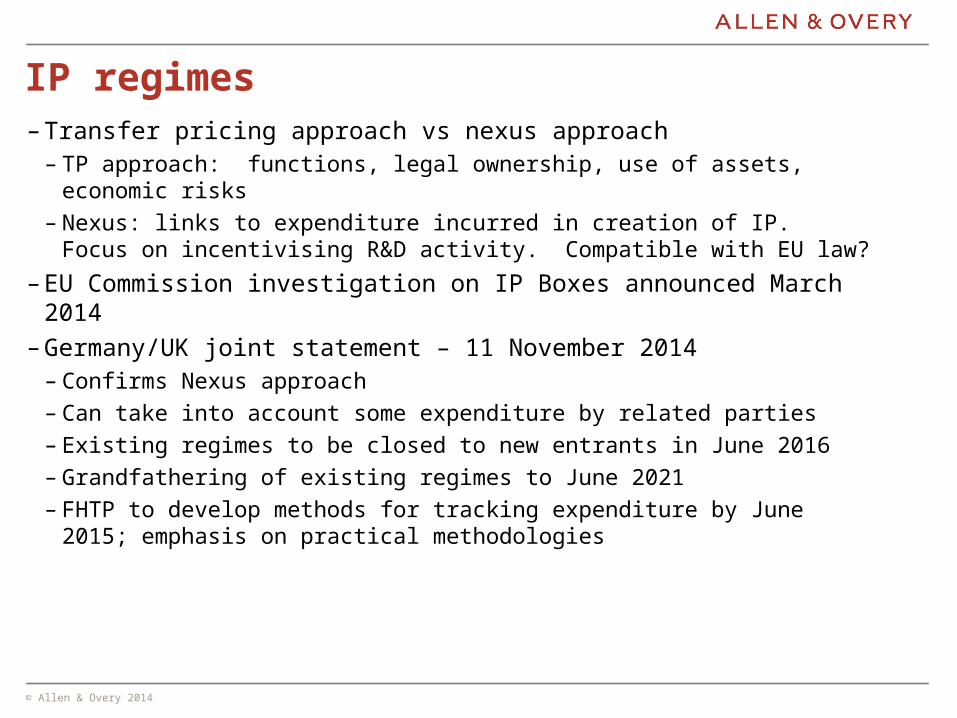

IP regimes– Transfer pricing approach vs nexus approach

– TP approach: functions, legal ownership, use of assets, economic risks– Nexus: links to expenditure incurred in creation of IP. Focus on

incentivising R&D activity. Compatible with EU law?

– EU Commission investigation on IP Boxes announced March 2014– Germany/UK joint statement – 11 November 2014

– Confirms Nexus approach– Can take into account some expenditure by related parties– Existing regimes to be closed to new entrants in June 2016– Grandfathering of existing regimes to June 2021– FHTP to develop methods for tracking expenditure by June 2015;

emphasis on practical methodologies

© Allen & Overy 2014

Looking to 2015 – will BEPS be eliminated?

– Respect for tax sovereignty – position of tax havens?– CFC rules– TP and risk/capital– Prospect of US reform?

© Allen & Overy 2014

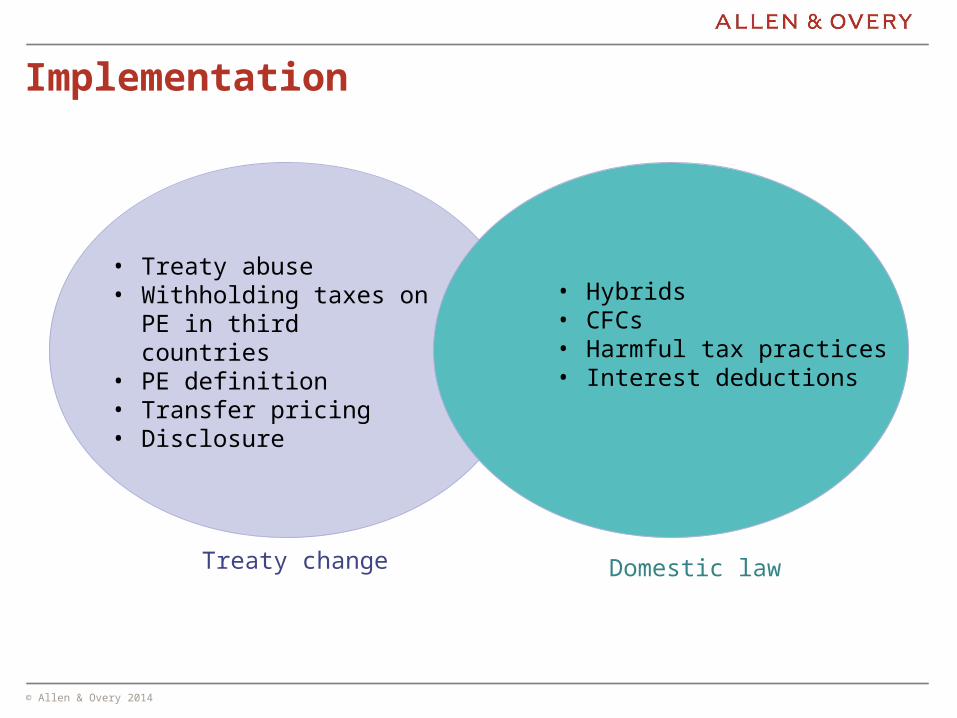

Implementation

• Treaty abuse• Withholding taxes on PE in

third countries• PE definition• Transfer pricing• Disclosure

• Hybrids• CFCs• Harmful tax practices• Interest deductions

Treaty change Domestic law

© Allen & Overy 2014

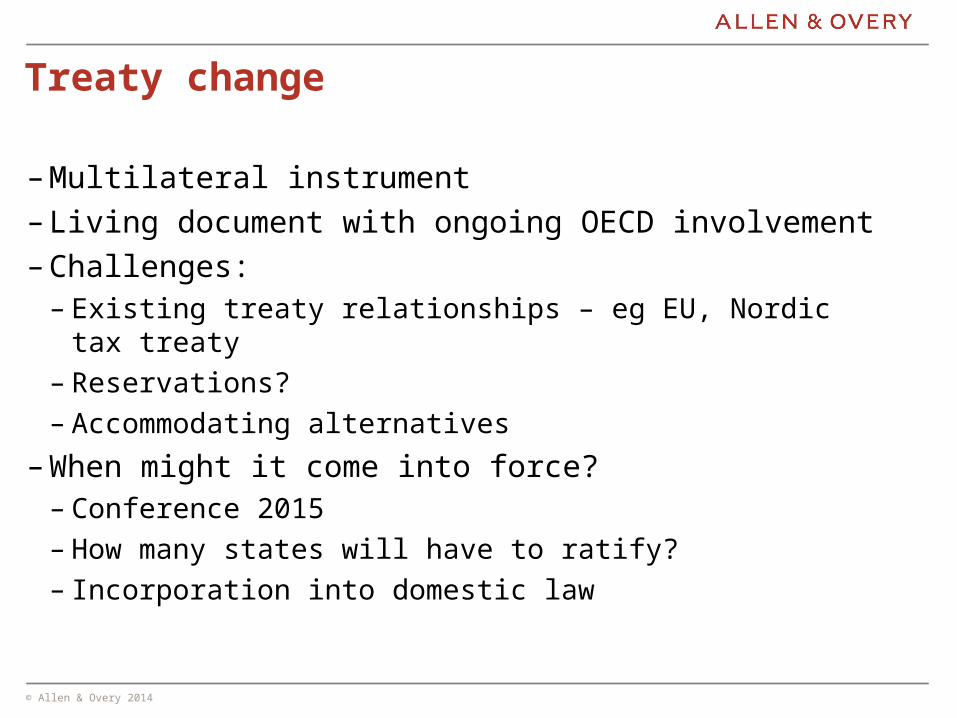

Treaty change

– Multilateral instrument– Living document with ongoing OECD involvement– Challenges:

– Existing treaty relationships – eg EU, Nordic tax treaty

– Reservations?

– Accommodating alternatives

– When might it come into force?– Conference 2015

– How many states will have to ratify?

– Incorporation into domestic law

© Allen & Overy 2014

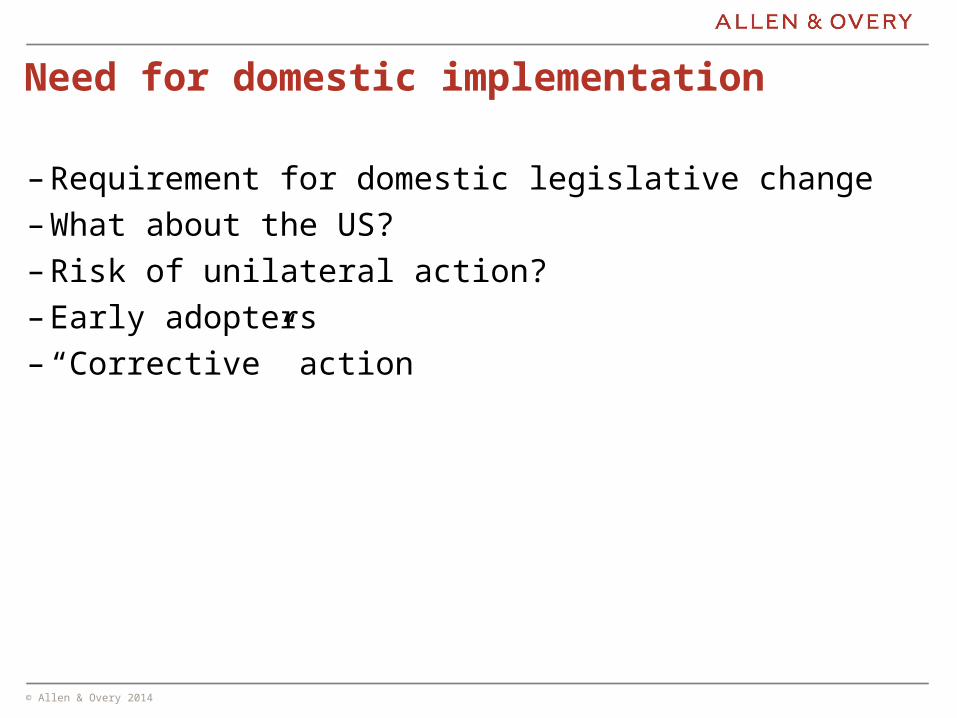

Need for domestic implementation

– Requirement for domestic legislative change– What about the US?– Risk of unilateral action?– Early adopters– “Corrective” action

9

OECD Guidance• It is essential that the new guidance in

Chapter V of the Guidelines, and particularly the new country-by-country (CbC) report, be implemented effectively and consistently.

• The international nature of tax planning means that unilateral and uncoordinated actions by countries will not suffice and may actually make things worse

10

Potential for Inconsistency

• Confidentiality / Public availability

• Early unilateral legislation & non-conformity

• TP exceptions to the “arm’s length principle”

• Exchange of information: Liberal definition / use

• LOB derivative benefits provision

• Subjective General Anti-Avoidance Rules (GAAR)-“Principal Purpose” vs. LOB & Domestic vs. Treaty

11

Potential for Inconsistency

• TP CbC: Formulary apportionment vs: Functions, assets and risks analysis

• TP rules as a substitute for CFC rules

• Global consensus: US Foreign Tax Credit (FTC)

• Arbitration provisions: Adopt “Best Practices” at audit level and provide avenues for resolution (MAP inefficiencies, timeliness)

• CbC rules: Timing / OECD + domestic legislation

12

TP Documentation: What next?

• Pre-BEPS

• BEPS incentivized unilateral legislation

• BEPS Guidelines / Consistent domestic legislation

• Post-BEPS + domestic legislation

13

GAAR: What next?

• Domestic and / or treaty legislation

• Increased subjectivity & uncertainty

• Additional documentation: material transactions

• Additional likelihood of double taxation

• Monitoring adherence to GAAR standard

14

CbC Reporting: What next?

• Preparation of outline per OECD Guidelines

• Prepare Q & A’s for audit

• Provide supplementary information

• Supplement with TP Master File and / or Local File

The BEPS Action Plan

• The action plan calls for 15 actions organised around the following three main pillars:

• The coherence of corporate tax at the international level

• A re-alignment of tax and substance

• Transparency, coupled with certainty and predictability.

Actions 11 - 14 Transparency and Certainty

• Greater transparency for tax administrations and more certainty for business:

• Establish methodologies to collect and analyse data on BEPS and the actions to address it (Action11)

• Require taxpayers to disclose their aggressive tax planning arrangements (Action 12)

• Re-examine transfer pricing documentation (Action 13)

• Make dispute resolution mechanisms more effective (Action 14).

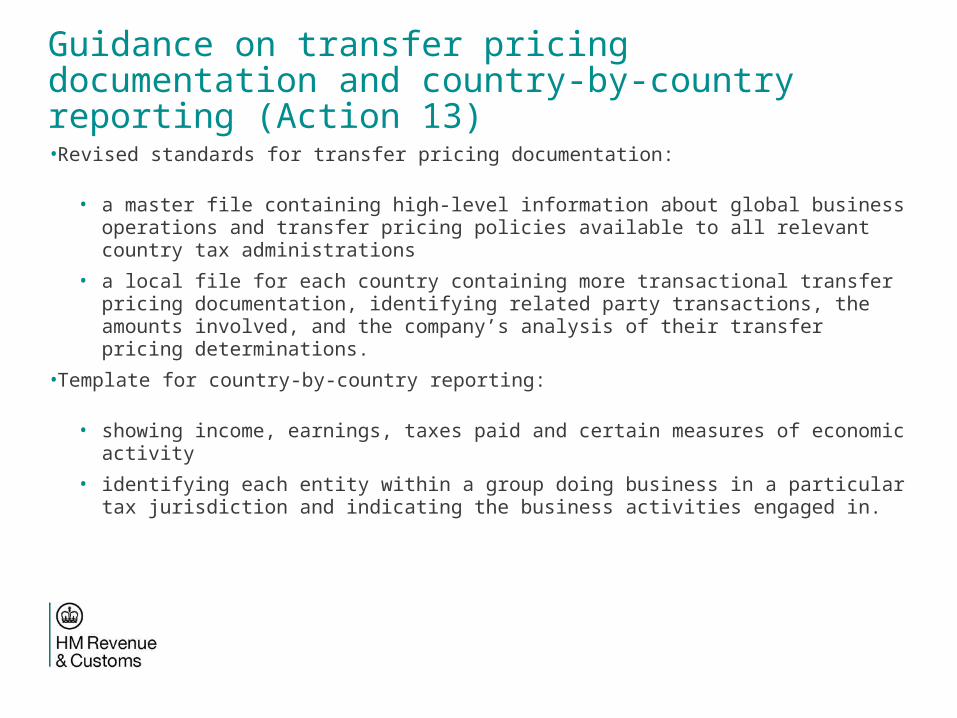

Guidance on transfer pricing documentation and country-by-country reporting (Action 13)

•Revised standards for transfer pricing documentation:

• a master file containing high-level information about global business operations and transfer pricing policies available to all relevant country tax administrations

• a local file for each country containing more transactional transfer pricing documentation, identifying related party transactions, the amounts involved, and the company’s analysis of their transfer pricing determinations.

•Template for country-by-country reporting:

• showing income, earnings, taxes paid and certain measures of economic activity

• identifying each entity within a group doing business in a particular tax jurisdiction and indicating the business activities engaged in.

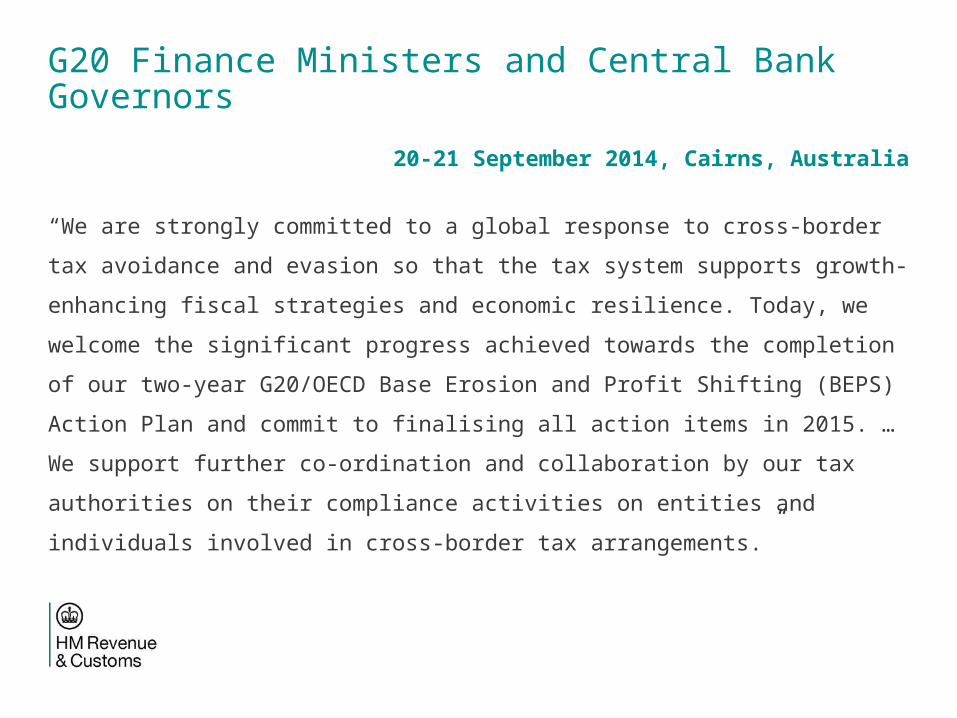

G20 Finance Ministers and Central Bank Governors

20-21 September 2014, Cairns, Australia

“We are strongly committed to a global response to cross-border tax avoidance

and evasion so that the tax system supports growth-enhancing fiscal strategies

and economic resilience. Today, we welcome the significant progress achieved

towards the completion of our two-year G20/OECD Base Erosion and Profit

Shifting (BEPS) Action Plan and commit to finalising all action items in 2015. …

We support further co-ordination and collaboration by our tax authorities on their

compliance activities on entities and individuals involved in cross-border tax

arrangements.”

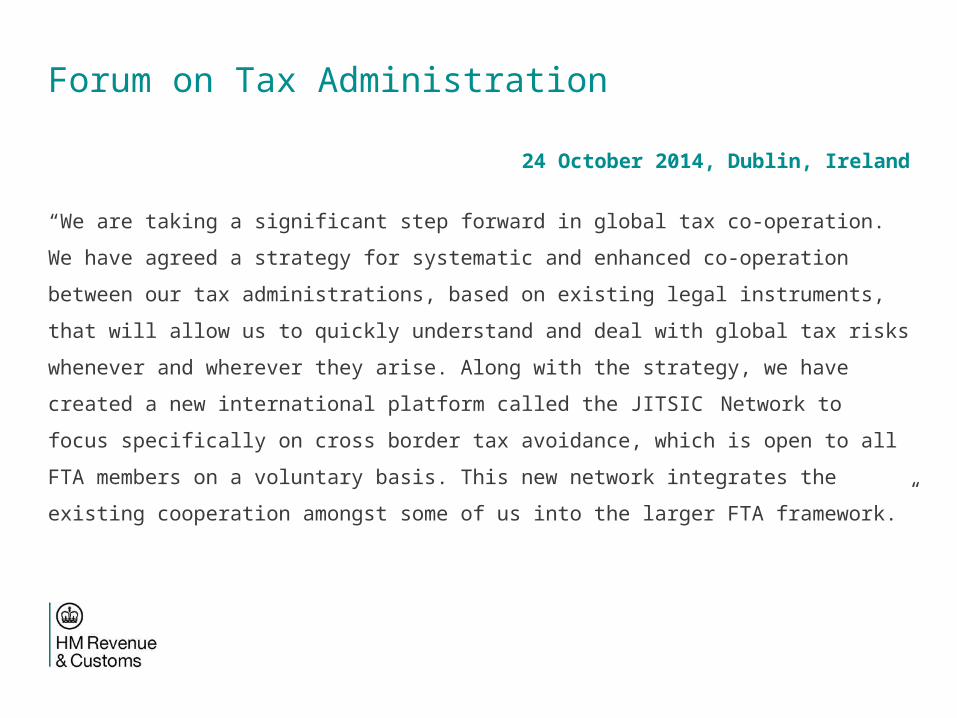

Forum on Tax Administration

24 October 2014, Dublin, Ireland

“We are taking a significant step forward in global tax co-operation. We have

agreed a strategy for systematic and enhanced co-operation between our tax

administrations, based on existing legal instruments, that will allow us to quickly

understand and deal with global tax risks whenever and wherever they arise.

Along with the strategy, we have created a new international platform called the

JITSIC Network to focus specifically on cross border tax avoidance, which is

open to all FTA members on a voluntary basis. This new network integrates the

existing cooperation amongst some of us into the larger FTA framework.”

© Allen & Overy 2014

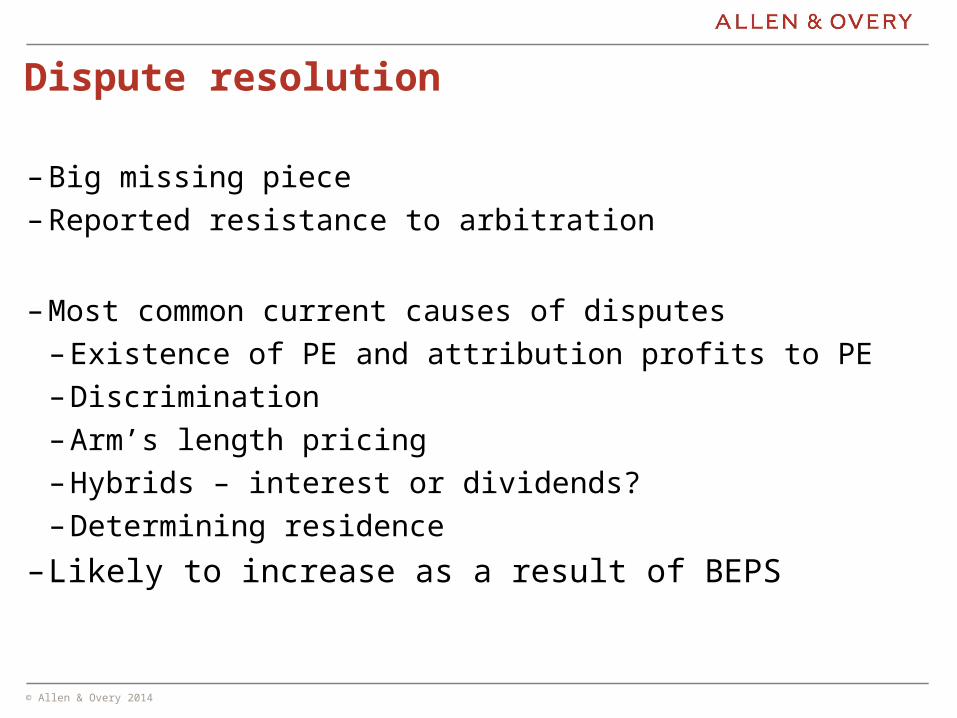

Dispute resolution

– Big missing piece– Reported resistance to arbitration

– Most common current causes of disputes– Existence of PE and attribution profits to PE– Discrimination– Arm’s length pricing– Hybrids – interest or dividends?– Determining residence

–Likely to increase as a result of BEPS

© Allen & Overy 2014

Mutual agreement procedure vs arbitration

– Mutual agreement procedure– Not litigation/limited arbitration

– ‘Discussion’ process between competent authorities– With a view to reaching agreement– Limited taxpayer participation

– Activating the process

– Mandatory binding arbitration in OECD model since 2008– Only 17% actual treaties

– Triggering the process– Resolving the issues not the case

– Supports but does not replace mutual agreement procedure

21

© Allen & Overy 2014

Mutual agreement procedure

– Statistics– Growing case load– Increasing duration

– Why do taxpayers fail?– Agreement reached in 90% of cases – is this success?– Providing insufficient information– Domestic law dispute– Time limits lapse– Taxpayer guilty of avoidance, evasion, fraud

22

© Allen & Overy 2014

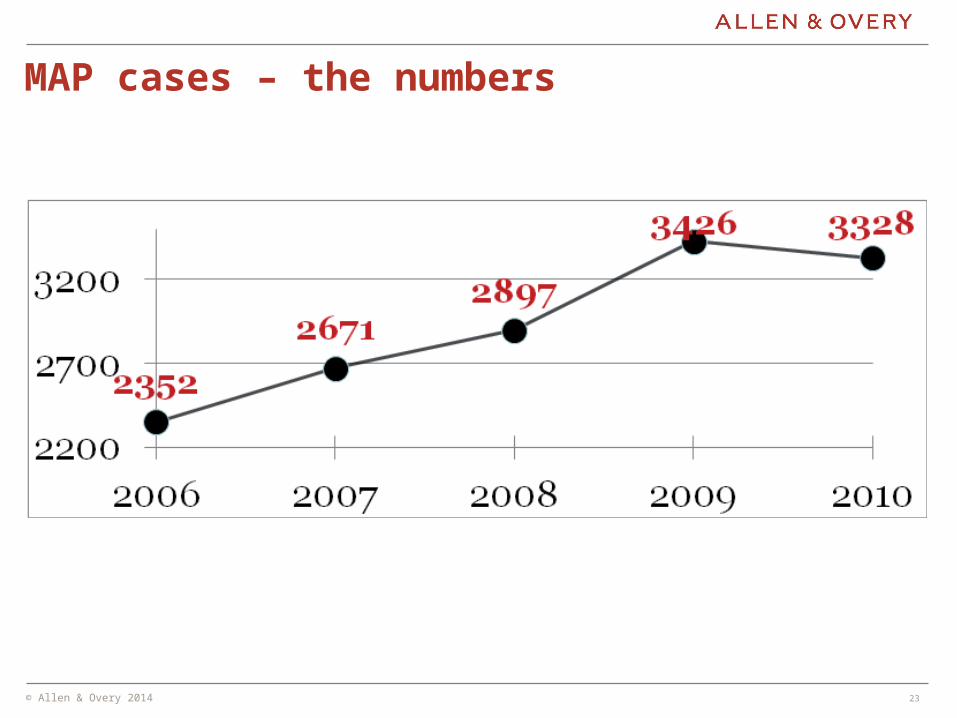

MAP cases – the numbers

23

© Allen & Overy 2014

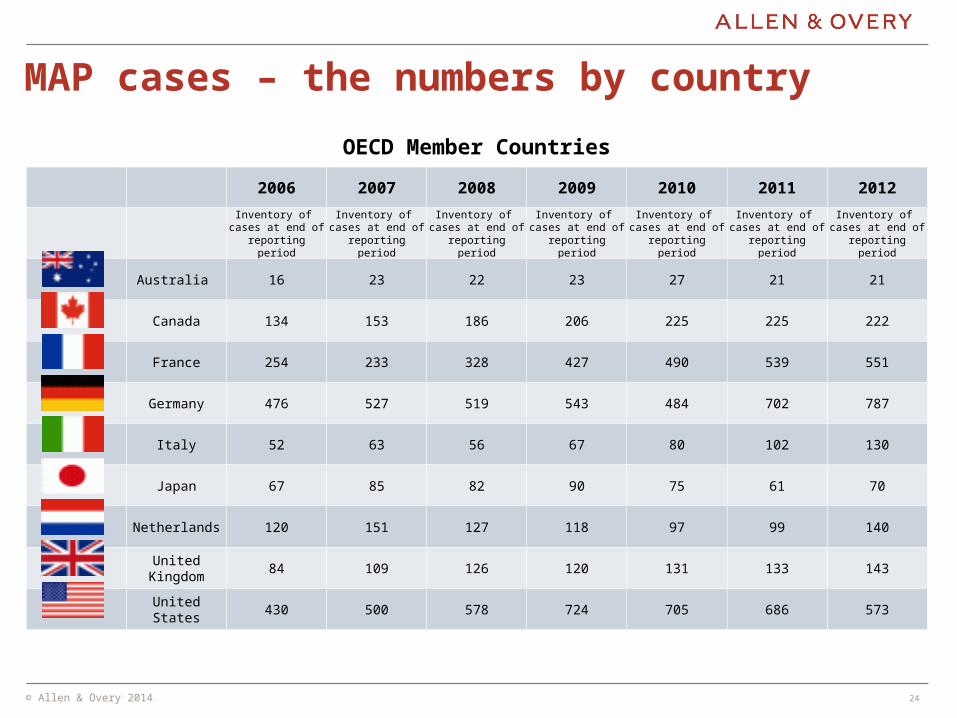

MAP cases – the numbers by country

OECD Member Countries

2006 2007 2008 2009 2010 2011 2012

Inventory of

cases at end of reporting period

Inventory of cases at end of reporting period

Inventory of cases at end of reporting period

Inventory of cases at end of reporting period

Inventory of cases at end of reporting period

Inventory of cases at end of reporting period

Inventory of cases at end of reporting period

Australia 16 23 22 23 27 21 21

Canada 134 153 186 206 225 225 222

France 254 233 328 427 490 539 551

Germany 476 527 519 543 484 702 787

Italy 52 63 56 67 80 102 130

Japan 67 85 82 90 75 61 70

Netherlands 120 151 127 118 97 99 140

United Kingdom 84 109 126 120 131 133 143

United States 430 500 578 724 705 686 573

24

© Allen & Overy 2014

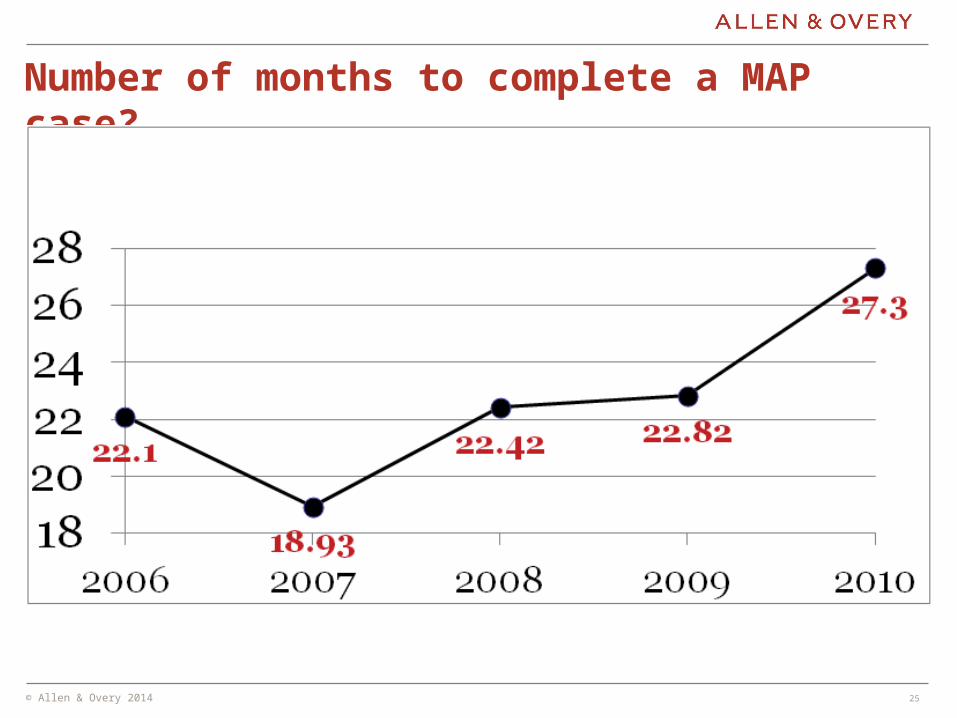

Number of months to complete a MAP case?

25

The Netherlands – general view on BEPS

• BEPS is mostly a source country problem and international cooperation is the only solution

• An increase of international transparency and exchange of information is essential for this

• The Netherlands supports the ‘holistic’ approach

• Nonetheless, The Netherlands has already taken some domestic measures

• Before taking any further measures, the Netherlands will await the further guidance expected 2015

• On a separate note: the Netherlands is not an advocate of harmonization of EU corporate tax systems by means of a common consolidated corporate tax base (CCCTB)

26

Renewed regulations on Dutch minimum substance requirements

• Decree on Dutch minimum substance requirements for DVL (dienstverleningslichaam) and information provision effective as per 1 January 2014. By exchanging information, the Netherlands provides the concerning treaty partner state with a fair possibility to make a well-informed decision whether or not to grant treaty benefits to the DVL

• Codification of existing minimum substance requirements for stronger enforcement and for exchange of information with foreign tax authorities

• Updated regulations on APA’s, ATR’s and relating substance requirements – published on 12 June 2014

• Exchange of information • DVLs that do not meet substance requirements but apply tax treaties and/or EU I&R Directive;• APAs for stand alone structures

• Extension substance rules to holdings - if ATR desired

• Extension substance rules to other categories (e.g. non-resident taxation)

27

Sanctions non-compliance regulations

• Non-, inadequate or late provision of information: fine

• Spontaneous exchange of information to source country in respect of interest, royalty, rent or lease amounts for which treaty or EU I&R directive protection has or may be claimed

• Exchange of information on APA’s:

- Only for stand-alone structures (i.e. in the absence of other activities in the Netherlands) - For new APA’s only

28

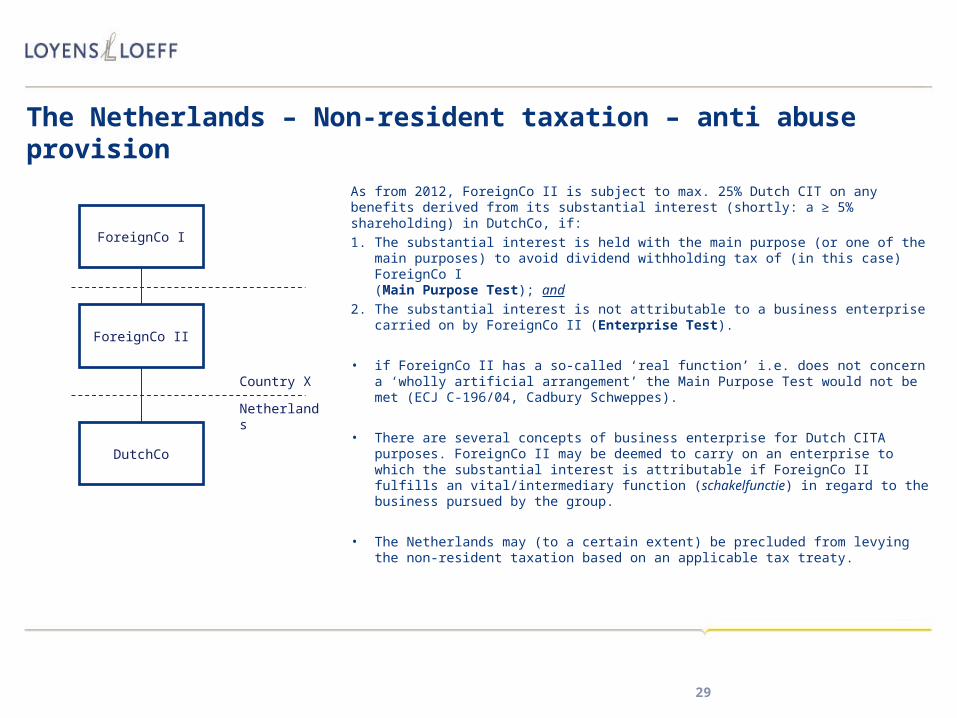

The Netherlands – Non-resident taxation – anti abuse provision

29

As from 2012, ForeignCo II is subject to max. 25% Dutch CIT on any benefits derived from its substantial interest (shortly: a ≥ 5% shareholding) in DutchCo, if:

1. The substantial interest is held with the main purpose (or one of the main purposes) to avoid dividend withholding tax of (in this case) ForeignCo I(Main Purpose Test); and

2. The substantial interest is not attributable to a business enterprise carried on by ForeignCo II (Enterprise Test).

• if ForeignCo II has a so-called ‘real function’ i.e. does not concern a ‘wholly artificial arrangement’ the Main Purpose Test would not be met (ECJ C-196/04, Cadbury Schweppes).

• There are several concepts of business enterprise for Dutch CITA purposes. ForeignCo II may be deemed to carry on an enterprise to which the substantial interest is attributable if ForeignCo II fulfills an vital/intermediary function (schakelfunctie) in regard to the business pursued by the group.

• The Netherlands may (to a certain extent) be precluded from levying the non-resident taxation based on an applicable tax treaty.

Netherlands

DutchCo

ForeignCo I

ForeignCo II

Country X

Conclusions

• Netherlands codified minimum substance requirements as per 1 January 2014

• Netherlands tries to make system ‘more robust’

• Netherlands focuses on exchange of information

• Allow source country to make own analysis

• Further steps: international cooperation is the only solution

30

State Aid – Starbucks

31

11 June 2014

EC press release regarding the opening of in-depth state aid investigations regardingApple (Ireland), Fiat Finance & Trade (Luxembourg) and Starbucks (the Netherlands).

30 September 2014

EC published its opening decisions regarding Apple and Fiat Finance & Trade

11 November 2014

EC published its opening decision regarding Starbucks

© Allen & Overy 2014

State aid

1. Context

– aid granted via public resources,

– which distorts competition

– by favouring certain undertakings or good

32

© Allen & Overy 2014 33

2. Examples

FFT

Lack of cooperation of Luxembourg, indirect method of transfer pricing determination

22 anticipated decisions presented, representative of the rulings practice, on an anonymous basis, but reference to « FFT » (with, in the initial file, a ruling request, TP report and tax administration reply)Discussion on the methodology and assets funds exposed to risks, on the comparables and the return on equity (parallell with Starbucks)Comparison between the financial sectors and the automotive sectorNo precisions regarding the deduction for the counterpartsNo precisions regarding the linking with accountsLink to case law pending against EU Commission (T-258/14): request to provide a complete list of anticipating decisions made in 2010, 2011 and 2012:

Right of defense Principle of proportionality No link to precise facts (no relevance of information sought) Direct tax is competence of member states

© Allen & Overy 2014 34

3. Examples

Amazon

Luxco paid royalties to SCS (non taxable in Luxembourg in the absence of commercial activity)

• Excessive reduction of the base, any result that differs from the full market competition price and lowers the tax base can be considered a State aid

• No TP report provided• Limitation of the taxable result of Luxco, without consideration of its turnover• Global context (royalties received by Luxco)• Taking into account the respective functions of Luxco and of SCS• Duration of the ruling (in fact)• More favorable treatment than other tax payers in the same situation

Code of conduct group has validated on 27 May 2011 the Luxembourg TP Circulars on intragroup financing

© Allen & Overy 2014

4. Market perception

−Rulings are acceptable if they interpret the law

−Regulations on rulings and TP (methodology and documentation)

−No base erosion

© Allen & Overy 2014 36

Questions?

These are presentation slides only. The information within these slides does not constitute definitive advice and should not be used as the basis for giving definitive advice without checking the primary sources.

Allen & Overy means Allen & Overy LLP and/or its affiliated undertakings. The term partner is used to refer to a member of Allen & Overy LLP or an employee or consultant with equivalent standing and qualifications or an individual with equivalent status in one of Allen & Overy LLP’s affiliated undertakings.