IDC Predictions 2015 Digital Transformation in the...

18

IDC Predictions 2015 Digital Transformation in the Enterprise: Opportunity and Disruption Steven Frantzen Senior Vice President, EMEA Region January 2015

Transcript of IDC Predictions 2015 Digital Transformation in the...

IDC Predictions 2015

Digital Transformation in the Enterprise: Opportunity and Disruption

Steven Frantzen

Senior Vice President, EMEA Region

January 2015

© IDC Visit us at IDC.com and follow us on Twitter: @IDC_EMEA

The ‘New World’ Versus the ‘Old World’

‘Incoming Airbus A320 on December 8th was making an afternoon approach at

Heathrow when, with the plane at 700 feet, the pilot spotted what appeared to be a

quadcopter close by’

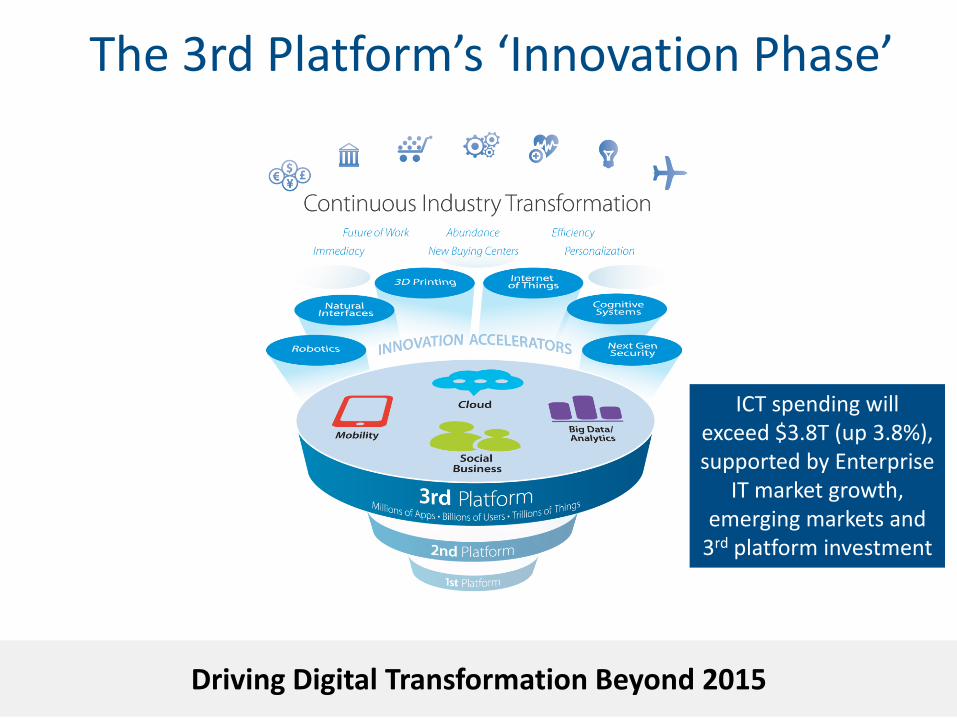

The 3rd Platform’s ‘Innovation Phase’

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 3Driving Digital Transformation Beyond 2015

ICT spending will exceed $3.8T (up 3.8%), supported by Enterprise

IT market growth, emerging markets and

3rd platform investment

European ICT Market & GDP Expectations, 2015

© IDC Visit us at IDC.com and follow us on Twitter: @IDC_EMEA

Greece

Ireland

Portugal

Finland

Austria

Denmark

Norway

Switzerland

Belgium

Sweden

Netherlands

Spain

Italy

France

UK

Germany

-3,0%

-2,5%

-2,0%

-1,5%

-1,0%

-0,5%

0,0%

0,5%

1,0%

1,5%

2,0%

0,0% 0,5% 1,0% 1,5% 2,0% 2,5% 3,0% 3,5%

2015 GDP Forecast

20

15

IC

T F

ore

ca

st

Gro

wth

Source: European Blackbook, Q3 2014, EIU, October 2014

4

Mobility Predominates

Smartphones and Tablets will generate 40% of all IT growth worldwide in 2015

Wireless data will be the biggest ($536B) and fastest-growing Telecom Services sector

Mobile application download growth will slow, but hit 150 billion

Dynamic enterprise mobile application development

Broader uptake of enterprise mobility

What percentage of your employees will be using smartphones in 12 months?

Using

56.6%

Not

using

43.4%

Source: IDC European Enterprise

Mobility Survey, H2 2014 | N = 920

CIOs to focus on supporting an agile architecture to support legacy and next-

generation mobile applications

5

By 2016, 65% of global competitive strategies will require real-time IT-as-a–

Service (ITaaS), and 80% of CIOs will deliver a new enterprise architectural framework

Cloud Services in Transition

Public cloud services sales will near $70B The “greater cloud market” – including public, private

clouds, and enabling IT and services – will hit $118B

IaaS competition will intensify, further consolidation

PaaS wars will expand, with number of apps in leading marketplaces doubling

“Strange bedfellow” partnerships multiply

6

Big Data & Analytics Migrate & Integrate

Big data & analytics market will reach $125 billion

Rich media analytics will at least triple Video, Audio, and Image analytics and search:

expanding use cases in many industries

Data as a Service proliferates

IoT will be the next critical focus for data/ analytics services

The “Year of Cognitive/Machine Learning”

By 2018, 30% of CIOs of global organizations will have rolled out a pan-enterprise data

and analytics strategy

7

IoT Will Begin to Affect Everything

IoT spending will exceed $1.7 trillion in 2015, up 14%

30 billion things connected by 2020

IoT will be the killer app for digital transformation

0% 20% 40% 60% 80% 100%

Gov't/Edu

Healthcare

Prof Svcs/Transport

Process Manu

Retail/Wholesale

Util/Oil & Gas

Telecom/Media

Discrete Manu

Finance

TOTAL

Already adopted Plan in next 12 months

No adoption plans Not Familiar

Q: Considering the Internet of Things (IoT) solutions and M2M communication, are you familiar, do you adopt or are you planning to adopt them? (%Share for Europe)

Source: IDC European Vertical Market Survey, October

2014, n=1,628

8

CIOs need to get closer to the network, become enablers for business partners

and review partnerships

Other Innovation Accelerators

Move to 3rd Platform-optimized Security

Security - a top 3 business priority for 70% of CEOs of global enterprises

15% of mobile devices will be accessed biometrically (over 50% by 2020)

More encryption of regulated data

EU Data Protection legislation impact

Threat intelligence as a service on the horizon

3D Printing

By 2020, more than 10% of consumer products will be available through “produce on demand” via 3D printing

2015 spending will surge 27%, to $3.4B

9

More Technology Fuelled Digital Disruption!

Disruption, re-invention, and continuous transformation become the norm

1/3 of market share leaders in every industry will be disrupted by 3rd

Platform competitors

The number of Industry Platforms/Communities will double in 2015

Numerous 3rd Platform-driven disruptions accelerate

10

Digital Transformation of the Customer

© IDC Visit us at IDC.com and follow us on Twitter: @IDC

Educated Customers Mobile Customers

Brand Discussions in Social Networks

New Service Channels

Traditional

Digital Marketing

Channels

Oceans of Customer Data

11

IT-enabled Services

Transforming Business Processes

IT-enabled Business Processes

Automating Business Processes

IT-enabled Products

Creating IT-enabled Products

© IDC Visit us at IDC.com and follow us on Twitter: @IDC

Digital Transformation of Processes, Services and Products

12

Distribution & ServicesSmart Utilities

Domino’s Pizza sold £104 million of pizza via its mobile platform in the UK and Ireland alone

Digital Transformation of the Enterprise & Industries

‘In the next five years, robotics, wearable technology and cognitive computing will start to be commonplace in retail’

Mike McNamara, CIO Tesco

Healthcare

Data Driven + Securely Managed 13

Beyond Business - Transforming Cities and Public Services

14 14

© IDC Visit us at IDC.com and follow us on Twitter: @IDC

Digital Transformation Implications – Leadership

15

Angela ArendtsCEO Burberry

(now Apple Retail)

Vivek BadrinathCMO/CIO

Accor Group

Stan SugarmanCDO

Gruner & Jahr

with John Douglas (CTO)

The Common Denominator: ‘Executive Sponsor’ for Digital Transformation

Operational

excellenceInnovation in products

company functions

processes and

business models

Product and

process

improvement

Competitive

necessity

Medium term

competitiveness

Long term

competitiveness

(IDC European IT Executive Survey, April 2014, n=1,310)

Improvement & Innovation

16

50% of European organizations have created a new group focused on innovation

Transforming to a Business Innovation IT Organization

Source: IDC, Enterprise IT Transformation Maturity Model, May 2014

Managed

Business Innovation

Effective partnership between business and IT around 3rd Platform implementations allows organization to outpace competitors through the use of 3rd Platform

Opportunistic

2nd Platform IT

Uncoordinated efforts between business and IT around 3rd Platform implementations; limited progress toward 3rd Platform adoption

Ad Hoc

Core IT

No effort between business and IT to coordinate or incorporate 3rd Platform technology

Repeatable

3rd Platform IT

Coordinated efforts between business and IT around 3rd Platform implementation allow organization to keep pace with peers in 3rd Platform adoption

Optimized

Business Transformation

Highly orchestrated interaction between business and IT around 3rd Platform implementations, enabling a world-class organization with lasting competitive advantage driven by 3rd Platform transformation and an organization that has embraced it.

Opportunisticc

2nd Platform IT

Uncoordinated efforts between business and IT around 3rd Platform implementations; limited progress toward 3rd Platform adoption

Managed

Business Innovation

Effective partnership between business and IT around 3rd Platform implementations allows organization to outpace competitors through the use of 3rd Platform

Ad Hoc

Core IT

No effort between business and IT to coordinate or incorporate 3rd Platform technology

Repeatable

3rd Platform IT

Coordinated efforts between business and IT around 3rd Platform implementation allow organization to keep pace with peers in 3rd Platform adoption

Optimized

Business Transformation

Highly orchestrated interaction between business and IT around 3rd Platform implementations, enabling a world-class organization with lasting competitive advantage driven by 3rd Platform transformation and an organization that has embraced it.

55% of European organizations have gone through a major IT re-organization in the last 12 months (IDC European IT Executive Survey, April 2014, n=1,310)

17

Beyond 2015

15

18

Digital transformation and disruption are

inevitable in most industries

‘Every organization must become a

technology/digital company in the new

marketplace’

3rd platform technologies and innovation

accelerators bring clear benefits to customers,

employees and companies – but not without

challenges

They change the nature and role of IT and

innovation – becoming the realm of all C-level

execs

Leverage IT organization as a partner in business

innovation

Move beyond a defensive posture – explore the

possibilities

Work with partners who understand the

challenges and opportunities

"If you went to bed last night as an industrial

company, you're going to wake up today as a

software and analytics company.”

CEO of GE - Jeff Immelt