ICP 17: Group-wide Supervision - 17: Group-wide Supervision ix Pretest Before studying this module...

68

ICP 17: Group-wide Supervision Basic-level Module A Core Curriculum for Insurance Supervisors

Transcript of ICP 17: Group-wide Supervision - 17: Group-wide Supervision ix Pretest Before studying this module...

ICP 17:Group-wide Supervision

Basic-level Module

A Core Curriculum for Insurance Supervisors

Copyright © 2006 International Association of Insurance Supervisors (IAIS).All rights reserved.

The material in this module is copyrighted. It may be used for training by competent organi-zations with permission. Please contact the IAIS to seek permission.

This module was prepared by Kathrin Schädlich. Dr. Schädlich has been manager of the Ac-counting and Solvency Department of the German Insurance Association since 1998. She is an expert on group supervision, solvency, and accounting. During the period of the trans-position of the European Community insurance group directive, she monitored and advised Germany’s supervisory authority.

The module was reviewed by Michael Hafeman and Ruud Pijpers. Michael Hafeman is an actuary and independent consultant on financial sector supervision and related issues. He has held senior positions in both private and public sector organizations in the financial services industry in Canada and the United States. Most recently, he was assistant superintendent of the specialist support sector at Canada’s Office of the Superintendent of Financial Institutions (OSFI) and served as a member of the Executive Committee and the Technical Committee of the International Association of Insurance Supervisors (IAIS) and as chair of its Solvency Subcommittee. Ruud Pijpers studied econometrics at the Erasmus University in Rotterdam, the Netherlands, where he also held a post as student-assistant, working in the field of and publishing on econometric modeling, optimal economic policy, and game theory. After work-ing in the United Kingdom and Brussels in education, the real estate sector, and investment consulting, he joined the supervisory authority in the Netherlands in 1994, where he has since been working in the fields of investments and derivatives, pensions, financial conglomerates and insurance groups, and insurer solvency assessment. He has represented the supervisory authority in a number of European and IAIS working groups.

iii

Contents

About the Core Curriculum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

Note to learner . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vii

Pretest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ix

A. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

B. An insurer as part of a group . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

C. Group-wide supervision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

D. Responsibilities for group-wide supervision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

E. Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

F. References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Appendix I. ICP 17 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Appendix II. Glossary of key terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Appendix III. Insurance group structure (case study) . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Appendix IV. Example of double and multiple gearing . . . . . . . . . . . . . . . . . . . . . . . . . 48

Appendix V. Examples of group structures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Appendix VII. Answer key . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Case StudiesCase Study 1. Baseline Scenario . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

FiguresFigure 1. Types of insurer risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Figure 2. Contagion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

v

About theCore Curriculum

A financially sound insurance sector contributes to economic growth and well-being by supporting the management of risk, allocation of resources, and mobilization of long-term savings. The insurance core principles (ICPs), developed by the International As-sociation of Insurance Supervisors (IAIS), are key international standards relevant for sound financial systems.

Effective implementation of the ICPs requires skilled and knowledgeable insurance supervisors. Recognizing this need, the World Bank and the IAIS partnered in 2002 to develop a “core curriculum” for insurance supervisors. The Core Curriculum Project, funded and supported by various sources, accelerates the learning process of both new and experienced supervisors. The ICPs provide the structure for the core curriculum, which consists of a set of modules that summarize the most relevant aspects of each topic, focus on the practical application of supervisory concepts, and cross-reference existing literature.

The core curriculum is designed to help those studying it to:

• Recognize the risks that arise from insurance operations• Know the techniques and tools used by private and public sector professionals• Identify, measure, and manage these risks• Operate effectively within a supervisory organization• Understand the ICPs and other IAIS principles, standards, and guidance• Recommend techniques and tools to help a particular jurisdiction observe the

ICPs and other IAIS principles, standards, and guidance• Identify the constraints and identify and prioritize supervisory techniques and

tools to best manage the existing risks in light of these constraints.

vii

Note to learner

Welcome to the ICP 17: Group-wide supervision module. This is a basic-level module on group-wide supervision that does not require specific prior knowledge of this topic. The module should be useful to either a new insurance supervisor or an experienced supervisor who has not dealt extensively with the topic or is simply seeking to refresh and update knowledge.

Start by reviewing the objectives, which will give you an idea of what a person will learn as a result of studying the module, and answer the questions in the pretest to help gauge prior knowledge of the topic. Then proceed to study the module either on an in-dependent, self-study basis or in the context of a seminar or workshop. The amount of time required to study the module on a self-study basis will vary, but it is best addressed over a short period of time, broken into sessions on chapters if desired.

To help you engage and involve yourself in the topic, we have interspersed the module with a number of hands-on activities for you to complete. These are intended to provide a checkpoint from time to time so that you can absorb and understand the material more readily. You are encouraged to complete each of these activities before proceeding with the next section of the module. An answer key in appendix VI sets out some of the points that you might consider when responding to the questions in each question set. You will also find question sets dealing with the local situation and related to practices in your jurisdiction. These are intended to help you apply the material in this module to your local circumstances. If you are working with others on this mod-ule, develop the answers through discussion and cooperative work methods. Since the responses will vary by jurisdiction, the answer key suggests where you might look for the answers.

Insurance Supervision Core Curriculum

viii

As a result of studying the material in this module, you will be able to do the fol-lowing:

1. State the definitions of an insurance group and a financial conglomerate (ac-cording to the IAIS Glossary of Terms) and explain why it is important that such terms be clearly defined in legislation

2. Explain how the fact that an insurer is part of a group can alter (a) its risk pro-file, (b) its financial position, (c) the role of its management, and (d) its business strategy

3. Explain why commercial, nonfinancial activities are often prohibited or severely restricted in an insurance group or a financial conglomerate

4. Describe the following approaches to supervision: (a) solo, (b) solo-plus, (c) consolidated, and (d) group comprehensive

5. Enumerate the following essential elements of group-wide supervisory over-sight and explain their importance: (a) group structure and interrelationships, (b) capital adequacy, (c) intragroup transactions and exposures, (d) reinsurance and risk concentration, and (e) internal control mechanisms and risk manage-ment processes

6. Prepare a map of a particular insurance group or financial conglomerate7. Describe the types of information required to conduct group-wide supervision,

beyond that required for solo supervision8. Illustrate how various jurisdictions have realigned their financial sector super-

visory responsibilities to facilitate the supervision of financial conglomerates9. Explain how supervisory authorities in different jurisdictions and financial sec-

tors might cooperate to achieve group-wide supervision, in particular with re-gard to (a) information sharing, (b) group-wide assessment, and (c) supervisory activities

10. Describe the role of a lead or coordinating supervisory authority11. Summarize the requirements of ICP 17.

ICP 17: Group-wide Supervision

ix

Pretest

Before studying this module on group-wide supervision, answer the following ques-tions. The questions are designed to help you gauge your existing knowledge of this topic. The answer key is presented in appendix VI at the end of this module.

For each of the following questions, circle the response that is correct or most relevant.

1. Solosupervision

a. Fullyservesthepurposesoffinancialsupervision

b.Referstosupervisionofasingleentity(thereforethedesignation“solo”).

2. Aninsurermustbelicensedbeforeitcanoperatewithinajurisdiction(seeICP6onlicensing).Thisrequirementrelatesto

a. Asingleentity

b.Aninsurancegrouporfinancialconglomerate.

3. Thosethatshouldbesubjecttoeffectiveinsurancesupervisionare

a. Exclusivelynational(domestic)insurersandinsurancegroups(excludingforeignentitiesandsubsidiaries)

b.Alsoinsurancegroupswithforeignentitiesandsubsidiaries.

Insurance Supervision Core Curriculum

x

4. Group-widesupervisionismainlyaimedat

a. Preventingthecreationofinsurancegroups

b.Preventingthecreationoffinancialconglomerates

c. Protectingconsumers

d.Protectingestablishedinsurersfromnewcompetitors.

5. Solosupervisionandgroup-widesupervision

a. Excludeeachotherinanycase

b.Cancomplementeachother.

6. Capitaladequacyrequirementsconcerningasingleentityshouldbe

a. Sensitivetothesize,complexity,andrisksofaninsurer’soperations,aswellastheaccountingrequirementsthatapplytotheinsurer

b.Aimedatenablingtheinsurancecompanyconcernedtoexpandinthefuture

c. Sufficienttoensurethattheinsurancecompanyconcernedwillbeabletomeetitscommitmentstowarditspolicyholdersevenifithassignificantinvestmentsinrelatedcompanies.

7. Group-widesupervision

a. Isrelevantforinsurancegroupsandfinancialconglomeratesoperatingonacross-borderbasisonly

b. Isrelevantforallinsurancegroupsandfinancialconglomerates.

8. Aninsurancecompany

a. Mayatthesametimebeamemberofbothaninsurancegroupandafinancialconglomerate

b.Maynotatthesametimebeamemberofbothaninsurancegroupandafinancialconglomerate.

9. Supervisorycooperationandinformationsharinga.Mayonlytakeplacewithinthesamedomesticjurisdictionforlegal

reasons

b.Arenecessaryalsointhesupervisionofinsurancegroupsandfinancialconglomeratesoperatingonacross-borderbasisandshouldthereforebeallowedbytheregulatoryframework.

ICP 17: Group-wide Supervision

xi

10.Aninsurancegroupcomprisesthreesupervisedinsurancecompanies.Allthreeinsurancecompaniesmeetthesolvencyrequirementsatthesololevel.Isitnecessaryfromthepointofviewofrisktoadoptagroupapproachaswell?a.Yes,becauseparticularsolvencyrisksmayariseasaresultofthegroup

structure

b.No,becausemeetingthesupervisoryrequirementsatthesololevelensuresthatthesolvencypositionofthegroupwillbeadequate.

1

ICP 17: Group-wide Supervision

Basic-level Module

A. Introduction

The Insurance Core Principles and Methodology includes seven principles under the heading of “ongoing supervision” (IAIS 2003b and 2005d). Among these is ICP 17 on group-wide supervision (see appendix I for the complete text):

The supervisory authority supervises its insurers on a solo and a group-wide basis.

Insurers may be part of a wider group, such as an insurance group or financial conglomerate. Group-wide supervision of a financial group refers to a supervisory ap-proach that considers the group structure, the constituent licensed entities, and all the interrelationships within that financial group (see IAIS 2000b). Solo-plus, consolidated, and group comprehensive supervision are the most well-known approaches within this general definition.

The IAIS framework and cornerstones are relevant for the formulation of regulato-ry financial requirements for all insurers, irrespective of the group context (IAIS 2005e, 2005h). The solvency regime should, of course, consider all risks arising from an insurer being part of a wider group and all transactions with and exposures to other companies within the group, both financial and nonfinancial. It should define solvency require-ments for insurers in a group context, both regarding the required level and suitable constituents of solvency. A major objective of the regime should be to avoid double or

Insurance Supervision Core Curriculum

�

multiple gearing and unsound intragroup creation of capital. The regime should further seek to eliminate any scope for regulatory arbitrage.

From the point of view of risk, the isolated consideration of a supervised company that is part of a group is not sufficient. Against the background of the risk-based regula-tory and supervisory approaches that are becoming increasingly prevalent, the follow-ing questions, in particular, arise for group-wide supervision:

• What risks may result from being part of a group? • How may these be addressed by or reflected in a range of quantitative and quali-

tative requirements, and to which legal entities do these requirements relate?• Which supervisory authority has which responsibilities, and which supervisory

instruments and enforcement powers are available, to see to it that these re-quirements are being met?

• To which entities may such instruments be addressed?

The solutions in specific jurisdictions mentioned in the text are meant to be ex-amples. They do not claim to be the “best practice” for all jurisdictions.

The IAIS Working Group on Analysis of Self-Assessment Questionnaires, with the assistance of the IAIS Secretariat, has prepared a report analyzing the results of the Insurance Core Principles (ICP) self-assessment exercise that was carried out between June 2004 and December 2005 (IAIS 2006d). The working group found that ICP 17 for group-wide supervision is one of the least observed principles and group-wide supervi-sion appears to be in the process of development.

European Union (EU) member states have quite similar supervisory regimes with regard to insurance groups and financial conglomerates, deriving from Directive 98/78/EC on the supplementary supervision of insurance undertakings in an insurance group and Directive 2002/87/EC on the supplementary supervision of credit institutions, in-surance undertakings, and investment firms in a financial conglomerate (see European Community 1998; 2002/2003). These are known as the insurance group directive and the financial conglomerate directive, respectively. As noted in the self-assessment report, the Helsinki Protocol (DT/NL/194/00) encourages and facilitates practical cooperation between the relevant authorities in the supervision of insurance groups (IAIS 2006b). The financial conglomerate directive was adopted in 2004, with domestic legislation in the member states being formulated afterward. Consequently, some EU respondents do not yet have practical experience in executing the legislation.

ICP 17: Group-wide Supervision

�

Imaginethefollowingscenario:Youworkforasupervisoryauthority.Youaresit-tingatyourdeskinyourofficeafterare-laxingweekend.Asyouletyourthoughtswanderandconsiderhowyoucanworkthroughthemountainofpapersonyourdesk,yourbossentersandwishesyouagoodmorningandasuccessfulstarttothenewweek.Youexchange(briefly,ofcourse)commentsaboutwhatyoudidover theweekend. And then your bossquicklycomestothereasonforhervisit.Shesaysthatsheknowsyouareinter-ested in new challenges and that shehasan interesting,verydemanding jobforyou.

Surely,youhavereadinthepapersandprobablydiscussedwithcolleaguesthe fact that the insurancegroup“FindYourBestWay”hasacquiredmoreinsur-ancecompanies.Yourbossshows youasheetofpaperonwhichshesketchedthestructureoftheinsurancegroupdur-ingherflight fromCanada to theNeth-erlands while on a business trip (seeappendix III). The sheet reflects her

current knowledge about the group’sstructure.Sheassumesthat thegroupwill continue toexpandandmightpos-siblyhaveitseyeonforeigncompetitorsandnicheinsurers.Shethinksthatthegroupmightacquireabank inorder tooptimizeitssaleschannelsandthatthesupervisory authority should prepareforthispossibledevelopmentaheadoftime. Group-wide supervision is neces-sary.Now, thequestion iswhatshouldbeconsideredforthegroup-widesuper-vision. Your boss would like for you toworkonthis issueandtouseallavail-ablesourcesofinformationasyoufamil-iarizeyourselfwiththematter.

Yourbossstressesthatyouareupto the job. She values you as a com-petent, communicative, and innovativepartner. Therefore, she suggests thatyoumeetforyourfirst jointbrainstorm-ingsessioninoneweek.

Thevariousremarksandexercisesincludedinthemoduleshouldhelpyoutopreparefortheupcomingbrainstorm-ingsession.

Case Study 1. Baseline Scenario

Exercises

1. Whichtermsdoyouassociatewiththetaskdescribedinthecasestudy?Createamind-map.*

2. YouknowthatyourbossisinvolvedwiththeIAISandwillexpectyoutoknowthetermsdefinedbytheIAIS.Therefore,reviewtheIAISglossary(IAIS2006b)andseewhetheryoufindthetermsyouhavejustputdowninyourmind-mapandhowthesetermsaredefined.Whichothertermsshouldyouaddtoyourmind-map?

*Mind-mapisapossibleresultofmind-mapping,acreativetechniqueforcollecting,structuring,andsummarizingideas.Itenablesindividualusers,professionals,andteamstocaptureideasandsort,structure,andpresent informationasaclearvisualmap(graphicorchart).Mind-mappinghelpstoexplainconcepts,findsolutions,andmakedecisions.Avarietyofmind-mappingsoftwareisavailableontheInternet,buthand-drivenmappingisalsopossible.

Insurance Supervision Core Curriculum

�

Before delving further into the topic of group-wide supervision, it is important to define some commonly used terms. The topic involves the terms mentioned in appen-dix II in particular.

It is quite possible that, depending on the specifics of the jurisdiction concerned, the terms are defined differently in detail. For example, the definition of “insurance group” and “financial conglomerate” seem to follow two approaches: one is to define explicitly or provide criteria for “group” and “financial conglomerate” in domestic legislation, and the other is to define “related entity” or “person with the insurer” to extend the scope of supervision to such entities or persons. In both approaches, there is little commonality in the definitions across jurisdictions, except for EU member states (see IAIS 2006d). For example, the insurance group directive and the financial conglomerate directive use different approaches to defining the scope of group supervision (see section C). The insurance group directive starts at the entity and looks “outward” to related entities; it does not define an insurance group. The financial conglomerate directive looks more “top-down” and does define the scope of a financial conglomerate or group.

Some terms are used synonymously within this module, although their meaning can vary from one jurisdiction to another:

• Company / entity / enterprise / undertaking• Ownership / participation.

ICP 17: Group-wide Supervision

�

B. An insurer as part of a group

Insurance companies may be part of an insurance group or a financial conglomerate. Group membership can provide benefits to an insurer, but it also can pose risks. Su-pervisory authorities need to supervise in a manner that will ensure that such risks are being dealt with effectively.

Benefits and risks of group membership

The business model of an insurance group is based, among other things, on the spreading of risks among different markets, both with respect to different product lines and concerning different regional markets. It may be easier for an insurance group op-erating internationally to optimize capital and risks and to achieve economies of scale in its operations.

Similarly, groups have developed that offer services and products in different finan-cial sectors; these are the so-called financial conglomerates. Their primary business is financial, and their regulated entities engage in at least two of three activities: insurance, banking, and securities. Insurers and banks have engaged in many different forms of cooperation, in order to take advantage of the following:

• Changes in financial market structures• The diversification of financial products• Opportunities to develop new channels of distribution• The potential to reduce income volatility.

On the one hand, legislation often stipulates that separate activities need to be kept in different legal entities to reduce a possible spillover of risk. On the other hand, legis-lation allows the forming of groups. With the increasing size and scope of activities of a group, there is an increasing possibility to balance risk within the group.

Opportunities to increase market share in well-established and mature markets may be limited. Legal, political, cultural, or regulatory barriers sometimes hamper di-rect access to markets and influence the structure of international groups. Hence, to grow internationally, institutions may have to take a stake in existing companies and make use of well-established brands.

The structure of the financial sector and the significance of groups that are active in various sectors differ considerably from one country to another. Such groups may be insurance-dominated groups, bank-dominated financial groups, or more balanced in character. For example, in Germany, financial conglomerates are of greater importance in the insurance sector than in the banking sector. Despite their small number, they cover a considerable market share (see Deutsche Bundesbank 2005). In Europe, some of

Insurance Supervision Core Curriculum

�

the financial conglomerates are among the largest players on the financial markets and provide services across the globe.

The formation of groups can be broken down according to the foundation strate-gies applied, such as joint or individual establishment and takeover. Some large Europe-an insurers predominantly expand via acquisitions at home or abroad. A group strategy can provide a unified presence in the market and promote coordinated financial prod-ucts from the various sectors.

The membership of an insurer in a group can be a potential source of strength to the insurer (see IAIS 2003a). Diversification effects may exist that enhance the ability of the group—and ultimately that of the financial system overall—to withstand external shocks. For instance, different maturity structures in the balance sheet (for example, long-term bank assets contrasting with long-term insurance technical provisions) can reduce structural mismatches, and this can facilitate the asset and liability management of the conglomerates (see Deutsche Bundesbank 2005, p. 46).

Diversification of business areas and customer groups can result in financial con-glomerates having a more stable profitability profile than banking-only or insurance-only groups. Potential benefits of reducing risk through geographic diversification are another motivation for conglomeration. However, diversification effects are tempered by the fact that both banking and insurance revenue are, to some extent, dependent on exogenous factors such as bond yields, share prices, and indicators of business activity (see Deutsche Bundesbank 2005, p. 46).

Potential efficiency gains obtained through the use of economies of scale and scope can thus enhance the ability of financial conglomerates to bear risk.1 But the same fac-tors can result in a greater complexity of groups, reduced transparency, size-induced reduction in flexibility, and the opportunity for regulatory arbitrage. Thus the member-ship of an insurer in a group can also pose risks, particularly as a result of contagion (see Deutsche Bundesbank 2005; Freshfields Bruckhaus Deringer 2003; IAIS 2003a). Contagion is one of the most often cited challenges to group stability. It means that problems may spill over from one group entity to another. The formation of a financial conglomerate, moreover, also involves the risk that problems in one financial sector will spill over more quickly to other sectors, both within the conglomerate itself and throughout the financial system in general. Other factors to be considered include pos-sibly conflicting corporate cultures and common vulnerabilities of banks and insurers within a group in the event of unfavorable capital market developments.

If conglomerates were to face financial difficulties, these difficulties could seriously destabilize the financial system, particularly when the conglomerates hold a significant market share in several financial sectors and acquire increasing importance in the mar-ket owing to their size. Such instability could damage the interests of insurance policy-

1. Economies of scale primarily refer to efficiencies associated with supply-side changes, such as increasing or decreasing the scale of production, for a single type of product. Economies of scope refer to efficiencies associated with the distribution of different types of products. Economies of scope are one of the main reasons for marketing strategies such as product bundling and product lining.

ICP 17: Group-wide Supervision

7

holders, depositors, and investors (see European Community 2002/2003, recital clause 2 of the financial conglomerate directive).

The worldwide integration of economies and financial markets is increasing, and a sound and vibrant insurance and reinsurance industry is needed to sustain global eco-nomic growth (see Federal Reserve Board 2006). Thus effective group-wide supervision is necessary.

The need for group-wide supervision

Both economic and legal conditions lead to the creation of groups of companies and shape their business activities. These factors affect the risk profile of any group and hence the consideration of risks on the part of supervisory authorities.

With respect to group-wide supervision, historically, insurance laws have been de-signed for “ring fencing” the supervised entity and limiting impositions on the rest of the group, whether they be subsidiaries, siblings, or parents in the corporate structure (see IMF 2005, p. 138).

Jurisdictions have established so-called “firewalls” relating to the operations of sin-gle insurance companies to ensure that, for instance, the individual insurance company is not unduly impeded in its business activities but that the inappropriate outflow of resources to other companies is prevented. These include the prohibition or restriction of commercial, nonfinancial activities in an insurance company, which might otherwise affect its insurance activities negatively and compromise its ability to meet its commit-ments, both currently and in the future.

Such firewalls often extend to requiring that insurance companies specialize in either life or non-life insurance (see European Community 2002). Such firewalls are intended to ensure that the life insurance activities are distinct from the non-life insur-ance activities in order that the respective interests of life policyholders and non-life policyholders are not prejudiced and, in particular, that profits from life insurance ben-efit life policyholders.

Exercises

3. Listtheinsurancegroupsandfinancialconglomeratesthatcurrentlyexistinyourjurisdiction,whichshouldgiveyouageneralideaofwhetherornotgroup-widesupervisionisnecessary.

4. Brieflydescribepastdevelopmentsthathaveoccurredinyourmarket,whichmayhaveledtotheemergenceofinsurancegroupsandfinancialconglomerates.Ifnogroupsarecurrentlyoperatinginyourjurisdiction,aretherecurrentdevelopmentsthatmayleadtotheiremergenceinthefuture?

Insurance Supervision Core Curriculum

�

The position of an insurer as part of a group can alter its risk profile. Risk profile refers to an assessment of both the level of risk-taking activity and the quality of the existing risk management framework. Risks refer to the likelihood that expected or unexpected events will have a negative impact on the financial conglomerate (see Joint Forum 2001b, pp. 67–68). The conglomerate itself should be managing the risks, and the supervisory authority should develop a risk profile of the conglomerate based on its assessment of how well the conglomerate has done so. A conglomerate questionnaire has been prepared by the Joint Forum (2001b) as a tool for gathering such information. The regulatory requirements should be sensitive to risk.

Many categorizations of risk are available. The IAIS Solvency Subcommittee uses the International Actuarial Association (IAA) classification of risk and risk components in its work (see IAA 2004). Based on the work of the IAA, the risks faced by a typical insurance company can be categorized under five major headings (see figure 1).

• Underwriting risk is the specific insurance risk arising from the underwriting of insurance contracts, associated with both the perils covered and the processes followed in the conduct of the business.

• Credit risk is the risk of default and change in the credit quality of the issuers of securities, counterparties (notably reinsurers), and intermediaries to whom an insurer has an exposure.

• Market risk is the risk arising from the level or volatility of the market prices of financial instruments.

• Operational risk is the risk of loss resulting from inadequate or failed internal processes, people, or systems or from external events.

Figure 1. Types of insurer risk

Underwriting risk Credit risk

Risks Liquidity risk

Market risk Operational risk

• Underwriting process risk• Pricing risk• Product design risk• Claims risk• Economc environment risk• Net retention risk• Policyholder behavior risk• Reserving risk

• Direct default risk• Downgrade or migration risk• Indirect credit or spread risk• Settlement risk• Sovereign risk• Concentration risk• Counterparty risk

• Interest rate risk• Equity and property risk• Currency risk• Basis risk• Reinvestment risk• Concentration risk• Asset-liability mismatch risk• Off-balance-sheet risk

All risks other thanunderwriting, credit,market, or liquidityrisks

Figu

re 1

. Typ

es o

f ins

urer

ris

k

ICP 17: Group-wide Supervision

�

• Liquidity risk is the exposure to loss in the event that insufficient liquid assets will be available to meet the cash-flow requirements of policyholder obligations as they fall due.

These types of risk have to take account of three key components of risk: volatility risk, uncertainty risk, and extreme event risk (Darlap and Mayr 2006).

The risk level of a group could be different from the simple sum of risks of all of its members individually. Certain risks, such as contagion risk, have essentially emerged with the appearance of financial groups. However, simple portfolio theory suggests a certain potential for diversification effects. Groups engaging in many different business lines or geographic areas may be able to reduce risk by pursuing diversification (Darlap and Mayr 2006). Modern group management foresees a flexible allocation of capital to different entities within a group, according to the risk attribution. Internal models are used, particularly by the larger groups, in risk and capital management. These models have to accommodate the specific situation of the group. Supervisory authorities need to be familiar with such management approaches and risk management techniques and be capable of assessing their effectiveness.

As noted in the IAIS paper on stress testing (IAIS 2003a), the effects of various risks in the context of insurance groups or financial conglomerates may include, but are not limited to, the following:

• The impact on the insurer if the parent no longer guarantees financial support or the insurer is unable to access additional capital or repatriate funds

• The effect on the insurer if a parent or affiliate within the group is impaired—for example, the impact on available funding sources, such as lines of credit, intra-group funding, or access to external capital

• The effect on the insurer if it is unable to sell or close a subsidiary in difficulty in a timely manner—for example, where the subsidiary shares the same brand, systems, and other infrastructure as the insurer

• The potential diversion of management time to group issues• The implicit support of group companies through the reallocation of group

overheads toward the insurance company• The pressure on the insurer to support other group members financially• The pressure on the insurer to comply with group requirements rather than the

firm’s own strategy—for example, with respect to investment mix

Exercise

5. Brieflyexplainhoweachoftheriskcategoriestowhichaninsurermaybesubject,asshowninfigure1,couldbeaffectedbytheinsurer’smembershipinagroup.

Insurance Supervision Core Curriculum

10

• The effect on the insurer of a high degree of dependence on group resources (for example, through intragroup outsourcing) to support the insurer’s critical operations

• The effect on the insurer of a downgrade in the rating of the group or other reputational issues.

These challenges for financial supervision may be strongly interrelated.An unregulated parent company and its unregulated subsidiaries may incur coun-

terparty and market risks similar to those faced by regulated group companies. If such risks materialize, they are likely to affect the financial position of the separate regulated entities of the group as well. Therefore, it is necessary to ensure that the entire group, in-cluding its unregulated parts, is adequately capitalized, not just the individual regulated companies in the group (see CEIOPS 2005a, p. 205).

Parent companies are often in a position to make significant decisions affecting the entire group, including regulated insurers. Therefore, regardless of their regulated status, it is desirable to subject parent companies to controls on effective shareholder control, fitness and propriety of the management, and effective internal control and risk management mechanisms.

Group-wide supervision is needed in order to respond to the risks to which an insurer may be subject as a result of its membership in a group.

ICP 17: Group-wide Supervision

11

C. Group-wide supervision

New supervisory tools have been developed in response to the growing trend in groups toward diversifying their activities across national borders and sectoral boundaries through ownership linkages. The creation of diversified financial groups raises addi-tional supervisory concerns, including contagion, conflicts of interest, lack of trans-parency, and regulatory arbitrage. Supervisory and regulatory arrangements are geared toward ensuring that risks are managed properly and that they do not threaten the safety and soundness of the financial system (see IMF 2005).

Among other things, the following aspects of membership of insurance companies in a group have to be considered:

• Typical risks may affect more than one company in a group• Risks may arise due to companies not subject to supervision• There may be diversification effects within a group• Group-specific forms of finance may exist• Funds may be moved around within a group• A (larger) group is often less transparent than an individual company.

Insurance supervision tends to focus, even more than banking supervision, on protecting the individual consumer (see Darlap and Mayr 2006). Group-wide supervi-sion typically seeks to protect insurance consumers in several ways:

• Improved information on groups (transparency monitoring)• Measures to prevent “double gearing” or “multiple gearing” (financing monitor-

ing)• Greater oversight of business transactions within the group (transaction moni-

toring) • Increased oversight of risk concentrations.

Each of these elements of supervision is discussed later in this section. However, there is now a common awareness of the key macroeconomic impor-

tance of stable and sound insurance markets and the close interrelationship between micro and macro prudential objectives.

Basic approaches to group-wide supervision

For a long time, supervisory law was based exclusively on companies operating alone in the market and not influenced by links of any kind with other companies. However, the close contractual and company-law-related links within groups have led to a reorienta-tion in this area.

Insurance Supervision Core Curriculum

1�

Within each jurisdiction, the legislation must address a fundamental issue: wheth-er financial supervision is to focus primarily on the individual company or on the group of companies as a whole. The approach taken in legislation will determine the basic ap-proach to group-wide supervision, which may be solo, solo-plus, consolidated, or group comprehensive (see IAIS 2000b and 2005f).

Solo supervision refers to the supervision of a licensed financial entity by the su-pervisor in the jurisdiction where the entity is incorporated, whereby the supervised entity is treated as a “stand-alone” entity. The solvency requirements are applied on a stand-alone basis.

Solo-plus supervision combines the solo supervision of all licensed financial entities with an assessment of the group context. It considers all the group relations that could have an impact on the financial position of the individual licensed entities, with special attention to capital adequacy, large exposures, intragroup transactions and positions, and so forth. In this case, the solvency requirements are applied to all relevant entities, taking into account group-related corrections, and—as a general check—to the group as a whole, on an aggregated basis.

Consolidated supervision focuses on the total of individual (whether licensed or not) entities of the entire group, consolidated at the level of the top holding company. In this case, the solvency requirements are applied to the net financial position of the group as a whole.

Group comprehensive supervision fully considers the constituent entities of a finan-cial group, the interrelationships within the group, both at the solo level and appropri-ate (sub) levels of aggregation, and the group as a total.

These approaches are only “concepts.” Supervisory practice is varied and more flu-id, sometimes combining aspects of more than one approach.

Historically, the orientation has been toward solo supervision. However, “pure” solo supervision has come under growing criticism. Supervision of groups, which are increasingly international, or at least consideration of the group associations of the in-dividual insurers is necessary. Within a group, solo supervision does not cover special links regarding risk, liability, and financing. Approaches to group-wide supervision are still evolving, but the trend is toward consolidated or group comprehensive supervi-sion.

A number of jurisdictions have established rules on supervision of insurance groups and financial conglomerates (see Half 2002). For example, in Europe supervi-sion is currently based on the “solo-plus” model. Solo solvency is based on one Euro-pean directive, while group solvency is based on another (European Community 1998). The responsibility for prudential supervision, including solvency, rests primarily with the home supervisory authority. Although other companies in a group, including those whose business is not insurance, are considered, the principle of individual supervision of insurance companies is maintained. The approach to the supervision of insurance groups is being reconsidered as part of the European Solvency II project, with a sub-stantial strengthening of group supervision expected.

ICP 17: Group-wide Supervision

1�

Compared with the insurance group directive, the financial conglomerate directive took a notable step toward more extensive group supervision (European Community 2002/2003). The principal reason for the financial conglomerate directive was the need to face the accelerating pace of consolidation in the financial industry and the inten-sification of links between financial markets (see Gruson 2004). Laws and regulations dealing with different financial sectors were not able to deal with these developments, and such laws have traditionally adopted different approaches, with different definitions of capital, types of risks, and capital requirements. Under the financial conglomerate di-rective, solvency requirements and admissible capital depend on the solvency rules for each of the sectors. The financial conglomerate directive does not replace the existing consolidated or supplementary supervision of groups that operate in one sector of the financial industry; rather it introduces supplementary supervision of the regulated enti-ties in groups that straddle more than one financial sector. It requires the cooperation of supervisory authorities of different sectors and jurisdictions to make a group-wide prudential assessment.

Many countries have responded to the blurring of the boundaries between sectors by creating an integrated supervisory authority.

Groups subject to supervision

A further particularity of group supervision is that, although groups typically consist of various legally separate entities, the group as a whole might not be a legal entity. Thus it is important that there be clear legal rules on what constitutes an insurance group and a financial conglomerate. Such rules enable companies to know what rules they need to follow (are they an insurance group, a financial group, or something else) and to help supervisory authorities achieve clarity on who is responsible for what aspects of a group’s supervision.

Corporate legal structure refers to the legal framework of a group’s organization of the various entities that make up the group. Such entities may include insurance companies and their subsidiaries, banks and their subsidiaries, and unsupervised or unregulated entities.

The financial conglomerate directive describes the following structures for finan-cial conglomerates, which are possible under European law:

Exercises

6. Dosupervisoryrulesforinsurancegroupsexistinyourcountry?Ifso,whichoftheapproachesintroducedhereisfollowed?

7. Dosupervisoryrulesforfinancialconglomeratesexistinyourcountry?Ifso,whichoftheapproachesintroducedhereisfollowed?

Insurance Supervision Core Curriculum

1�

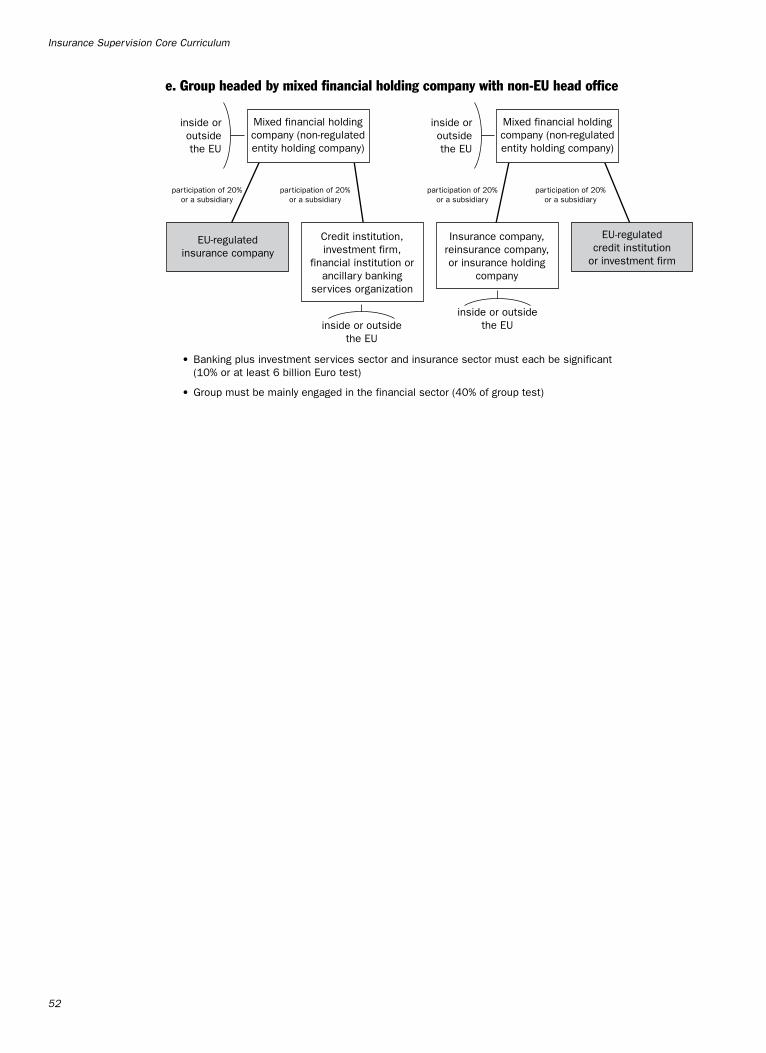

• Group headed by an EU-regulated entity• Group headed by a mixed financial holding company with EU-headed office• Horizontal financial conglomerate• Group headed by a non-EU-regulated entity• Group headed by a mixed financial holding company with non-EU head office.

Gruson (2004) includes examples of these group structures, which are reproduced in appendix V.

The financial conglomerate directive defines a financial conglomerate as a group of enterprises consisting of a parent company, its subsidiaries, and those enterprises in which either the parent or one of the subsidiaries has a stake. Groups of enterprises that are united to form a horizontal group are also covered by this definition. The group must contain at least one insurer and one company from the banking or investment sec-tors. One of these enterprises must be subject to supervision. If there is no supervised enterprise at the top, the group may be regarded as a financial conglomerate only if it is active mainly in the financial sector.

Moreover, for a group to be classified as a financial conglomerate, the enterprises must have considerable aggregated and consolidated operations in both the insurance and the banking or investment services sectors; in other words, they must be sufficient-ly cross-sectoral in character, as measured by balance sheet total and solvency require-ments. Moreover, considerable cross-sectoral activity must be assumed to exist if the enterprise’s balance sheet in the smallest sector amounts to at least €6 billion.

It is the responsibility of the national supervisory authorities to determine whether a group that is active in multiple sectors is a financial conglomerate. In parallel to the national procedures for determining which groups are financial conglomerates, nation-al supervisors are in the process of coordinating, at the European level, the identifica-tion of financial conglomerates (see European Commission 2006a, 2006b).

Elements of group-wide supervision

Group-wide supervision should not be limited to financial indicators such as capital adequacy and risk concentration; it also should consider the management structure, fit and proper testing, and legal issues. As in solo supervision, group supervision should have both quantitative and qualitative elements.

Exercise

8. Whathastobedealtwithbylawtoenableinsurancecompanies,insurancegroups,andfinancialconglomeratestoknowwhichrulesareapplicable?

ICP 17: Group-wide Supervision

1�

Transparency of group sTrucTure and inTerrelaTionships

The position of an insurer as part of a group can alter the role of its management. How-ever, depending on the size, international character, and interconnections, group struc-tures may not be transparent and therefore may be difficult to understand. For example, there may be:

• Unclear company or group structures• Quickly changing company or group structures• Outsourcing abroad• Outsourcing to entities that are not regulated.

The management structure of most groups falls into one of three categories (or a combination thereof): corporate legal (legal entity basis), business line (product or ser-vice basis), or geographic (region, country, or municipality).

Transparency is important to supervisory authorities. In fact, only if group struc-tures and interconnections are known is it possible to be aware of risks and to react adequately to them at the supervisory level. ICP 17, essential criterion g, states that the supervisory authority should be able to deny or withdraw the license when the organi-zational or group structure hinders effective supervision.

The IAIS Guidance Paper on Combating the Misuse of Insurers for Illicit Purposes includes comments on the need for transparency in general (IAIS 2005c):

• Insurers should only be part of a group if its structure is sufficiently transparent. The insurer or parent company of the group should explain how the group is set up. The group structure needs to have a sound business reason and purpose.

• If the insurer is part of a group, the supervisor should identify which persons (natural or legal) take part in or have an influence on the decisionmaking of the insurer, including major shareholders, significant owners, the parent company, other group-associated companies, and the board or management of those com-panies.

• The supervisor should remain aware of changes in the formal and informal con-trol structure of the group. It should especially be vigilant for a gradual increase of the interest in or control of the insurer (“creeping control”). For this pur-pose, the supervisor could check, for example, the register of shareholders, the minutes of the board and shareholders meetings of the insurer, as well as other relevant documentation, such as the listing of acquisitions and participations by the insurer. The same could be done for the parent company, if the supervisor has legal authority to do so.

The supervisory authority must obtain and analyze information about the group structure and interrelationships. This could be based on both offsite collection of infor-

Insurance Supervision Core Curriculum

1�

mation and onsite inspections. A group mapping exercise should be undertaken that delineates the group structure and identifies the supervisory authorities involved. The Conglomerate Questionnaire discusses various types of information that can be useful in this regard (Joint Forum 2001b).

Such information should include an organizational chart or other descriptive ma-terial that depicts the following:

• The supervised entity and any material holding companies, subsidiaries, or af-filiates, with indications of which legal entities take or bear substantial risk

• The organizational structure of the business lines, with the supervised entity’s place in the structure and the location of relevant business line management

• The supervisors of any material holding companies, subsidiaries, or affiliates.

The Conglomerate Questionnaire also suggests that the following information be obtained and discusses the relevance of such information to the supervisory authority’s understanding of a group:

• A chart depicting the management structure of the conglomerate, descriptions of the responsibilities of different types of managers (legal entity, corporate, and business line) within the conglomerate, the relationship among managers, and important types of interaction

• A description of the roles and responsibilities of the conglomerate’s board of directors, the composition of the board, and the roles, responsibilities, and com-position of the board of the supervised legal entity

• The level and distribution of capital among the material legal entities of the con-glomerate, the conglomerate’s approach to capital allocation on an economic and a regulatory basis, and whether the conglomerate is in compliance with its capital requirements in all regulated legal entities

• Financial information on the supervised entity and its ultimate holding com-pany, if applicable, including balance sheets (as of the most recent fiscal quarter and financial year-end), income statements (for the most recent year-to-date period and financial year-end), and consolidated balance sheets and income statements, where available.

A well-managed group should be able to provide such information quite readily!

capiTal adequacy

Insurer solvency and capital adequacy take a central position in risk management by insurers and in insurance supervision (see IAIS 2006c). Insurers and insurance groups must have capital commensurate with the level of risks inherent in their activities. Reg-

ICP 17: Group-wide Supervision

17

ulation and supervision should specifically address the distribution of capital within the group.

The apparent capital of a group of companies can be inflated through techniques referred to as “double gearing,” “multiple gearing,” “excessive gearing,” or “pyramid of credit.” Regulatory gaps or inconsistencies across both countries and industry sectors might enable institutions to overstate their “true” capital by counting it twice (double gearing) or several times (multiple gearing); see Darlap and Mayr (2006). Double or multiple gearing describes situations where companies are using shared capital as a buffer against risk occurring in separate entities. Thus a company is able to expand its business activity, without holding additional capital, by acquiring shares in a subsidiary company. Alternatively, an insurance company may purchase shares in a bank as a con-dition for receiving a loan. In these cases, both institutions are leveraging their exposure to risk. Regulatory and supervisory measures aimed at preventing and countering the effects of double or multiple gearing and artificial intragroup creation of capital are an important aspect of group-wide supervision.

The following transactions may result in double gearing or multiple gearing:

• Self-financing of the participating interest• Passing on of newly raised equity capital (transmission effect)• Transformation of loan capital of the parent company into equity capital of the

subsidiary (or subsidiaries)• Financing of the participating interest by the subsidiary.

Since a parent company can often exercise dominant influence on other group members, including the possibility of restructuring the capital of the subsidiaries, there is an unquestionable need to ensure that the same capital of the subsidiaries is not used artificially within a group to cover risks simultaneously in several group companies (see CEIOPS 2005a). The IAIS Principles on Capital Adequacy and Solvency states that capital adequacy and solvency regimes have to address double gearing and other issues that arise as a result of membership in a group, considering the following factors (IAIS 2002a):

• Capital adequacy and solvency regimes for insurers that are part of a group also should take a group-wide view. When considering insurance companies that are part of a group, it is important to avoid double gearing of capital.

• Consideration should be given to the capacity for intragroup funding. • For an insurance group, the treatment of transactions between members of the

same group should be considered as part of a capital adequacy and solvency regime.

• In addition, insurance supervisors should consider reputation and contagion risks that may arise as a result of problems in an associated company.

Insurance Supervision Core Curriculum

1�

The Joint Forum (1999) has proposed five principles for the assessment of capital adequacy within financial conglomerates, which are outlined below. The paper also dis-cusses relevant issues that supervisory authorities should consider when applying these principles.

• Acceptable capital adequacy measurement techniques should be designed to de-tect and provide for situations of double or multiple gearing—in other words, where the same capital is used simultaneously as a buffer against risk in two or more legal entities.

• Acceptable capital adequacy measurement techniques should be designed to detect and provide for situations where a parent issues debt and passes the pro-ceeds downstream in the form of equity, which can result in excessive leverage.

• Acceptable capital adequacy measurement techniques should be designed to include a mechanism to detect and provide for the effects of double, multiple, or excessive gearing through unregulated intermediate holding companies that have participations in dependents or affiliates engaged in financial activities.

• Acceptable capital adequacy measurement techniques should be designed to in-clude a mechanism to address the risks being accepted by unregulated entities within a financial conglomerate that are carrying out activities similar to the activities of entities regulated for solvency purposes (such as leasing, factoring, and reinsurance).

• Acceptable capital adequacy measurement techniques should be designed to address the issue of participations in regulated dependents (and in specific un-regulated dependents) and to ensure that the treatment of minority and major-ity interests is prudentially sound.

Appendix IV provides an example of double and multiple gearing within a finan-cial conglomerate.

ICP 17: Group-wide Supervision

1�

inTragroup TransacTions and exposures

The position of an insurer as part of a group can alter its business strategy. Regulatory inconsistency provokes shifts in activity between jurisdictions and institutions (for ex-ample, from a bank to an insurance company) when the requirements are lower in one than in the other for the same risk (see Darlap and Mayr 2006).

An insurer that is part of a group can be subject to intragroup exposures and con-tagion. According to the Study on Financial Conglomerates and Legal Firewalls (Fresh-fields Bruckhaus Deringer 2003), the risk of contagion may arise if two entities have a legal or factual connection with one another. Contagion risk (or domino or spillover effect) means the risk that adversity, or even a crisis, experienced by one company may spread to other companies in the group. For example, the reputation of an insurer may

Exercise

9. Thecasestudyoutlinedbelowdescribesasituationofdoublegearingbasedonparticipation.Considerthecasestudyandanswerthesequestions.Whatcouldconcernyouasasupervisorinthiscase?Howwouldthesolvencymarginhavetobeestablishedinthecaseofrisk-basedgroup-widesupervision?

Insurance Company B

Insurance Company A(100% Parent Company of Company B)

Assets

Participation in BDiv. assets

Solvency requirement: 95Available solvency: 100

50950

Liabilities

CapitalDiv. liabilities

100%

100900

Insurance Company B(100% Subsidiary of Company A)

Assets

Div. assets

Solvency requirement: 70Available solvency: 80

900

Liabilities

CapitalDiv. liabilities

80820

Insurance Company A

Insurance Supervision Core Curriculum

�0

Figure 2. Contagion

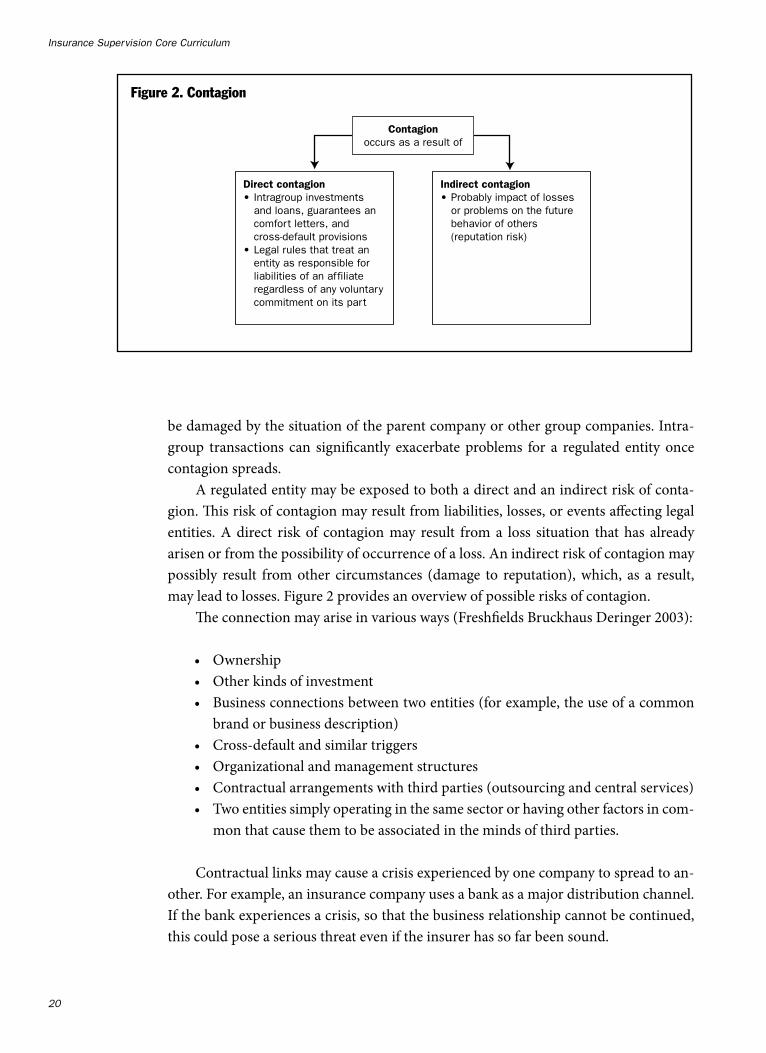

be damaged by the situation of the parent company or other group companies. Intra-group transactions can significantly exacerbate problems for a regulated entity once contagion spreads.

A regulated entity may be exposed to both a direct and an indirect risk of conta-gion. This risk of contagion may result from liabilities, losses, or events affecting legal entities. A direct risk of contagion may result from a loss situation that has already arisen or from the possibility of occurrence of a loss. An indirect risk of contagion may possibly result from other circumstances (damage to reputation), which, as a result, may lead to losses. Figure 2 provides an overview of possible risks of contagion.

The connection may arise in various ways (Freshfields Bruckhaus Deringer 2003):

• Ownership• Other kinds of investment• Business connections between two entities (for example, the use of a common

brand or business description)• Cross-default and similar triggers• Organizational and management structures• Contractual arrangements with third parties (outsourcing and central services)• Two entities simply operating in the same sector or having other factors in com-

mon that cause them to be associated in the minds of third parties.

Contractual links may cause a crisis experienced by one company to spread to an-other. For example, an insurance company uses a bank as a major distribution channel. If the bank experiences a crisis, so that the business relationship cannot be continued, this could pose a serious threat even if the insurer has so far been sound.

Figure 2. Contagion

Direct contagion• Intragroup investments and loans, guarantees an comfort letters, and cross-default provisions• Legal rules that treat an entity as responsible for liabilities of an affiliate regardless of any voluntary commitment on its part

Indirect contagion• Probably impact of losses or problems on the future behavior of others (reputation risk)

Contagionoccurs as a result of

ICP 17: Group-wide Supervision

�1

The risk of so-called psychological contagion arises if market participants assume that the crisis experienced by one company will have significant negative effects on another company. In this respect, it may not make any difference whether there is a close economic or legal link between the companies. The financial services sector, in particular, depends on the confidence of customers and is therefore prone to this type of risk. A decrease in confidence may lead to a loss of business, lower creditworthiness, and so forth.

A risk of contagion may also arise if market participants expect that a company will provide financial support to other companies in the group, even if there is no legal obligation to do so. A group itself may, for example, decide to provide support to protect the value of a common brand name. In fact, if an ailing company is not able to overcome the crisis despite the assistance rendered, it is unlikely that the funds transferred can be recovered, which may cause trouble for the company rendering assistance.

Supervisory authorities have to ensure that the transactions between entities in the same insurance group and financial conglomerate are appropriate. Supervision of intragroup transactions is an important element of group-wide supervision. The IAIS (2005c) proposes that the following aspects concerning business relationships and transactions with related and third parties be kept in mind:

• The supervisor should identify, possibly on the basis of the work of the external auditor, whether there are related parties. Parties are considered to be related (a) if one party has the ability either to control the other party or to exercise significant influence over it in making financial and operating decisions or (b) if the parties are within a group structure, even if one party does not exercise controlling powers or significant influence over the other. A party that is not a related party is considered to be a third party.

• Transactions with related parties can consist of a transfer of resources or obliga-tions between related parties, regardless of whether a price is charged. Business relationships and transactions with related or third parties, in which a member of the board or manager has an interest, should be held and performed at arm’s length. As appropriate, the non-executive directors or supervisory board, inter-nal audit function, and compliance function should verify if this is the case.

• If a board member or manager holds a position in, or has an interest in, a busi-ness partner of the insurer, his or her involvement in any transaction with that business partner should be controlled or, if necessary, prohibited. For example, if a senior financial officer of the insurer is also an asset manager with an affili-ated bank, he should not have the sole responsibility or authority to carry out investment transactions for the insurer.

• The internal control system of the insurer should be adequately set up and func-tioning with respect to transactions with related or third parties. Agreements, including side letters, of long duration or great importance to the insurer should be monitored for conflicts of interest.

Insurance Supervision Core Curriculum

��

Supervisory authorities need to understand the nature and volume of intragroup transactions and exposures. Supervision of intragroup transactions and exposures could, for instance, be organized as follows:

• Insurers, or the group, are required to report significant intragroup transactions and exposures to the supervisory authority at least annually

• Quantitative limits and qualitative requirements are established to define what must be reported

• If it appears that the solvency of the insurer is or may be jeopardized, the su-pervisory authority takes appropriate measures at the level of the insurer or at holding level, as appropriate.

reinsurance and risk concenTraTion

Insurance companies face a number of risks in their business activities and should have policies and procedures in place to manage them. One common risk management tech-nique is to reinsure some risks with other insurers. If the reinsurance company con-cerned is an external company, the potential risk of the reinsurer failing to fulfill its commitments in the event of a claim must be examined from a prudential point of view. If the reinsurance company belongs to the same group as the insurer, there is the fur-ther risk that the reinsurance cover has been contracted under conditions that are not usual between arm’s-length parties. Therefore, in the case of an intragroup reinsurance contract, it is particularly important to consider whether an economic risk transfer has really occurred and on what conditions. This is all the more true when the intragroup reinsurer is subject to no solvency requirements at all or is subject to weak requirements compared with the direct insurer seeking reinsurance. Therefore, the supervisory au-thority must clarify the risk situation around the intragroup reinsurance.

Exercises

10.Onthebasisofthegroupstructuresallowedinyourjurisdiction,howcancontagionriskarise?

11.Considerthebaselinescenario(presentedinappendixIII),inwhichInsuranceCompanyAshowsapropertywithabookvalueof100aspartofitsassets.CompanyAsellsthispropertytoCompanyBatacurrentvalueof150.Asastaffmemberofthesupervisoryauthoritythatsupervisesthesetwoinsurers,doyouhavetodealwiththistransaction?Ifso,how?

12.Describetheinformationyouhavetogatherinordertoassesstherisksthatmayarisefromintragroupandrelated-entitytransactions.

ICP 17: Group-wide Supervision

��

From a prudential point of view, it may well be appropriate for insurance compa-nies to seek reinsurance cover. The individual insurance company examines which part of the risks accepted it is capable of bearing itself and cedes any risk exceeding this part to a reinsurer that has more capacity to cover such risks. This is true also in the case of an intragroup reinsurer that accepts risks from other group companies in order to make them bearable both for the individual company and for the group by means of appropriate risk-policy measures. These measures include reinsurance contracts with companies outside the group so that risks that were reinsured within the group end up with external reinsurance companies. In relation to the prudential evaluation of such retrocessions, the credit risk must be assessed by the same standards as are applied to reinsurance that is placed directly with an arm’s-length party.

Not only a “solo” insurer but also an insurer as part of a group can be exposed to risk concentration. As discussed in section B, insurance groups and financial con-glomerates often develop in a quest to increase not only the scale but also the scope of operations and to benefit from a decrease in volatility. Even so, the supervisory author-ity has to ensure that the concentration of risk at the group level is also appropriate, taking into account possible contagion effects. Risk concentration refers to an exposure with the potential to produce losses large enough to threaten a financial institution’s health or ability to maintain its core operations. Risk concentrations can also arise in a group’s assets, liabilities, or off-balance-sheet items through the execution or process-ing of transactions (either products or services) or through a combination of exposures across these broad categories. The potential for loss reflects the size of the position and the extent of loss given a particular adverse circumstance. Risk concentrations can take many forms, including exposures to the following:

• Individual counterparties• Groups of individual counterparties or related entities• Counterparties in specific geographic locations• Industry sectors• Specific products• Service providers, such as back-office services• Natural disasters or catastrophes.

In identifying risks, supervisory authorities have to take into account the ways in which large losses can develop in a group as a result of risk concentration and possible contagion.

inTernal conTrol mechanisms and risk managemenT processes

It is, first of all, clearly the responsibility of the insurer itself to manage its risks, value its obligations, and procure and hold sufficient capital. Insurers face many kinds of risks

Insurance Supervision Core Curriculum

��

and use a variety of tools to manage them. It is the role of the regulatory regime and the supervisory authority to see that this management responsibility is met and to ensure accountability (see IAIS 2006c).

Because groups may operate as integrated entities and manage risks on a global ba-sis, their operations typically employ centralized risk management systems and internal control processes; the degree of centralization varies, however. One of the major chal-lenges facing financial conglomerates is integrating the management of risk across the various sectors. Risk management was in former times focused on sector-specific risks. But it was necessary to introduce integrated risk management in order to manage the group. Integrated risk management systems cut across organizational structures and separately regulated entities.

Supervisory authorities should review the centralized risk management and con-trol techniques, as well as other relevant intraorganizational factors, in order to under-stand fully the exposures of the whole organization and their effect on the supervised entities. For example, the financial conglomerate directive requires that appropriate risk management and adequate internal control methods be in place at the conglomerate level, including a proper business organization and proper accounting procedures. Ar-ticle 9 sets out more specific requirements for internal control mechanisms and risk management processes, as follows. Appropriate risk management includes the follow-ing elements:

• Sound governance and management• Approval and regular review of strategies and policies concerning all risks in-

curred by the appropriate governing body at the conglomerate level• Adequate capital adequacy policies anticipating the effects of the business strat-

egy on the risk profile and capital requirements• Adequate procedures ensuring that the risk monitoring systems are properly

integrated into the organization• Measures ensuring that the systems implemented in those enterprises subject

to supplementary supervision are consistent so that all risks can be measured, monitored, and controlled at the level of the financial conglomerate

Proper internal control mechanisms include the following elements:

• Adequate mechanisms regarding capital adequacy (to identify and quantify all material risks and to relate own funds appropriately to risks).

• Sound reporting and accounting procedures (to identify, measure, monitor, and control the intragroup transactions and the risk concentration).

The task of a supervisory authority is to verify that a group has appropriate risk management, internal control systems, and reporting systems and that it is able to pro-

ICP 17: Group-wide Supervision

��

vide all information that the supervisory authority may require in an adequate and timely manner.

The Conglomerate Questionnaire describes various types of information on risk management that may be helpful:

• The conglomerate’s broad business strategy and view of its principal risks. For each principal risk, this includes a description of the approach to measuring, managing, and controlling that risk, the organization of risk management per-sonnel and their reporting lines, limit structures or other risk control mecha-nisms in the regulated entity, and, where relevant, the role of stress testing or contingency planning in managing risk at the business line, legal entity, or group-wide level

• Policies and procedures of the conglomerate, addressing the introduction of new products or business lines

• The approach to managing the liquidity and funding profile of the supervised entity, including liquidity of the material assets, nature and stability of the en-tity’s current funding sources, and availability of alternative funding; large pay-ables, including securities payables, aggregate insurance claims payments, and out-of-the-money over-the-counter derivative and foreign exchange contracts; and other significant needs for cash and securities associated with exchange activities or clearing and settlement as well as the conglomerate’s approach to managing significant clearing and settlement arrangements through or for other firms.

managemenT suiTabiliTy

The challenges of managing a merger of diverse firms and the operation of the result-ing conglomerate are substantial. The operation of a financial conglomerate requires the ability to integrate the financial activities, research and development investments, pricing decisions, compensation practices, cost containment activities, and cultures of a large and diverse organization. Before any steps toward conglomeration are taken, each potential participant in such a merger should judge whether this set of skills exists in the managerial team.

The persons involved in performing key functions for an insurer, such as its direc-tors, senior managers, auditors, and actuaries, must be suitable to fulfill their roles (see ICP 7 on suitability of persons). The supervisory authority should apply “fit and proper” standards with regard to the board and management and should maintain regular con-tact to evaluate on an ongoing basis their integrity and competence to fulfill their duties (see IAIS 2000a, 2005g, and 2006c). Suitability means that these persons have not only the appropriate competence, experience, and qualifications needed to perform the du-

Insurance Supervision Core Curriculum

��

ties of their position but also the integrity to do so in a manner that will not jeopardize the interests of policyholders.

Senior managers of a group generally have been tested for suitability (fit and proper). It is important to extend the requirement of fitness and propriety to the board of holding companies, which may exert considerable influence on companies in the group. For example, the financial conglomerate directive requires the member states to provide that persons who effectively direct the business of a mixed financial holding company must be of sufficiently good repute and have sufficient experience to perform their duties.

ICP 17: Group-wide Supervision

�7

D. Responsibilities for group-wide supervision

The supervision of insurance groups and financial conglomerates often involves super-visory authorities from different financial sectors and jurisdictions (domestic/foreign). The development of such groups has rightly prompted deeper links between insurance supervisors and supervisors in other sectors.

Tasks for the supervision of the group and its constituent parts should be set out in legislation. To the extent that they are not prescribed in legislation, the supervisors in-volved should agree on the tasks. Such agreements are sometimes evidenced by formal cooperation agreements between the various supervisory authorities. As stated in ICP 17, essential criterion c, the supervisory responsibilities of each authority should be well defined and leave no supervisory gaps. Supervisory powers should mirror supervisory responsibilities and rest on a firm legal basis.

In Europe, for example, there are differences between the approaches taken to in-surance groups under the insurance group directive and to financial conglomerates un-der the financial conglomerate directive. The differences in approach are related directly to differences in the supervisory perspectives in the banking and insurance sectors. In fact, whereas a top-down supervision approach has been implemented in the banking sector (meaning that the supervisors address mainly the ultimate parent of the financial group), a bottom-up approach has been implemented in the insurance sector (meaning that the supervisors focus mainly on the individual insurer according to the solo-plus principle). Consequently, the development of a more harmonized approach between the two methods of supplementary supervision, at the level of the insurance group and at the level of the financial conglomerate, must take these different perspectives into account (see CEIOPS 2005b).

In view of the need for increased cooperation among supervisory authorities, and considering the involvement of authorities from different sectors and different jurisdic-tions, the financial conglomerate directive foresees the appointment of a coordinator, identifies which authorities should be involved in supplementary supervision at the level of the financial conglomerate, and provides enforcement measures for the coordi-nator with respect to a mixed financial holding company.

As to the internal organization of supervision, there are two main types of su-pervisory authorities—that is, integrated supervisory authorities responsible for the insurance, banking, and securities sectors and independent supervisory authorities re-sponsible for insurance only (and possibly pensions). The internal structure used by an integrated supervisory authority for dealing with groups or financial conglomerates may differ from jurisdiction to jurisdiction. Some have a specialized division for group supervision, and others charge sector-specific divisions with supervisory responsibility for the respective parts of a group, with appropriate coordination. Separate supervisory authorities may strive to achieve effective coordination by formulating a collaboration protocol, which governs exchange of information and cooperation between the author-ities within the jurisdiction, or by holding regular meetings among the authorities (see IAIS 2006d).

Insurance Supervision Core Curriculum

��

The need for supervisory cooperation