How risk models are being revolutionised through new …/media/Files/News-and-Insight/Market... ·...

19

How risk models are being revolutionised through new data collection and analysis technology CUTTING THE CABLES CONNECTING THE WORLD p18 THE MEGACITIES SINKING INTO THE SEA p22 COLOMBIA: LATIN AMERICA’S NEW TIGER p24 WHY TORNADOES ARE TRICKY TO PREDICT p28 SUMMER 2014 WWW.lloyds.com INSIDE: BIG DATA SPECIAL REPORT p10

Transcript of How risk models are being revolutionised through new …/media/Files/News-and-Insight/Market... ·...

How risk models are being revolutionised through new data collection and analysis technology

CUTTING THE CABLES CONNECTING THE WORLD p18THE MEGACITIES SINKING INTO THE SEA p22COLOMBIA: LATIN AMERICA’S NEW TIGER p24WHY TORNADOES ARE TRICKY TO PREDICT p28

SUMMER 2014 WWW.lloyds.com

INSIDE: BIG DATA SPECIAL REPORT p10

01_LMM7_Cover_des5.indd 1 14/07/2014 12:16

Care has been taken to ensure accuracy of information, but neither Lloyd’s nor the publishers can accept responsibility for omissions or errors. Lloyd’s is regulated by the Financial Conduct Authority and the Prudential Regulation Authroity. © Lloyd’s 2014.

SUMMER 2014 www.lloyds.com

Published on behalf of Lloyd’s (www.lloyds.com) by Sunday (www.sundaypublishing.com)

If you would like to contribute to the next issue, please email [email protected]

COVER ILLUSTRATION BY SCOTT WOTHERSPOON

Colombia’s GDP has grown each year since 2004 by between 2% and 7% – a remarkable achievement

LATIN AMERICA’S NEW TIGER p24

02_LMM7_Opener_des1.indd 2 07/07/2014 16:14

03

WHEN GLOBAL MAINLINES GO DOWN

From earthquakes and � shing nets to ships’ anchors and sabotage, we explore the vulnerabilities of the vital sub-sea cables that keep our world connected.

22 THE SINKING CITIESJakarta, Dhaka, Venice… many of

the world’s great coastal cities are

subsiding at a signifi cant rate – in the

worst case, the falling ground levels

outstrip rising sea levels by ten to one.

The factors compounding the issue,

from groundwater extraction to shifting

tectonic plates, are diverse – and so are

the innovative solutions to address it.

24 LATIN AMERICA’S NEW TIGERPolitical stability, ambitious investments

in infrastructure, and strong GDP growth

have turned Colombia into an attractive

opportunity for foreign insurers.

TORNADOES: INSIDE THE VORTEX

� ey are the most violent of all theatmospheric storms, with an extraordinary capacity for damage. On average every year in the US, 1,200 twisters kill at least 60 people and incur economic losses of US$400m, making them almost as big a source of insurance claims as hurricanes. Unfortunately, though, they’re tricky to predict: the national average warning time is just 14 minutes…

COVER STORY: BIG DATA� e new tech that’s mining a treasure trove of valuable information; the analytics throwing up correlations between world events and commercial losses; and how risk models are being rede� ned.

Features

05 INTRODUCTIONWe welcome you to Market magazine

and tee up this issue’s top stories.

06 FORESIGHTNews from the market, including: the unique risks of insuring a deep-sea mining gold rush; what extracting minerals from space rocks means for the market; providing cover for major sporting events; and why climate change and its impact on the severity of catastrophes can be di� cult to account for in current models.

34 HERITAGE: HOME OF THE BRAVEA century ago, thousands of Lloyd’s

men marched off to war. Many would

not return. We commemorate their

extraordinary contribution.

35 MARKET UPDATEUpcoming events and Lloyd’s

international websites.

RegularsSUMMER 2014 www.lloyds.com

18

28

03_LMM7_Contents_des4.indd 3 10/07/2014 10:02

www.lloyds.com/marketintelligence

INSIGHT AND ANALYSIS YOU CAN TRUST. IT’S YOUR GLOBAL ADVANTAGE

MARKET INTELLIGENCE YOUR GLOBAL ADVANTAGE

04_Lloyds Ad.indd 1 12/11/2013 12:50

By 2016, it’s predicted that global Internet Protocol (IP) traffic will reach 1.3 zettabytes annually – or more than 115 million terabytes a month. And, if harnessed effectively, this glut of big data can revolutionise the way insurers manage risk – from supporting real-time decision-making to enabling more granular pricing.

In our Special Report (page 10), we explore the cutting-edge technologies helping to collect and analyse this titanic treasure trove of information, how the insights gleaned are being applied to major risk events, and the things firms need to think about when investing in data collection, conversion and storage.

We also unearth a few fascinating facts about submarine cables – and get to grips with the losses incurred when these crucial intercontinental conduits fail, either through natural or man-made intervention (page 18).

And we take a closer look at Latin America’s new tiger, Colombia (page 24). Once in state of near-civil war, on a continent beset by boom and bust cycles, the country has enjoyed remarkable growth, while the protectionist policies of the past have gradually been relaxed, creating new opportunities for foreign insurers.

Finally, we attempt to understand why tornadoes – the most violent of all the atmospheric storms – are almost impossible to predict, and whether models of the near future will ultimately widen the warning gap (page 28).

We hope you find this issue interesting. If you haven’t already done so, sign up to receive Market magazine or our newsletter at lloyds.com/marketmagazine

05

facebook.com/lloydslloyds.com

“As urban areas expand

and we see more suburban

sprawl, there will be

more tornado damage”

ILAN KELMAN, READER OF RISK, RESILIENCE AND GLOBAL HEALTH,

UNIVERSITY COLLEGE LONDON

@LloydsofLondon lloyds.com/linkedin

05_LMM7_Intro_des4.indd 4 11/07/2014 12:07

Beneath the oceans lie rich veins of raw materials. And as new firms gear up to mine these deep-sea deposits, insurers are starting to consider the risks

In April, Papua New Guinea gave the green light to Canadian mining company Nautilus to start the first ever deep-sea mining project. Nautilus intends to produce copper, gold, silver and zinc by using robotic machines to mine sulphide deposits in the seabed.With 70% of the globe covered by

ocean, some pundits are forecasting a sub-sea gold rush.

Nautilus says that despite the vastness of the Earth’s oceans, only a small percentage of the seas can be effectively mined. However, Shontel Norgate, Chief Financial Officer, says: “Seafloor mining has advantages over land-based mines, where high-grade and accessible deposits have been exhausted.”

A typical mine on land yields copper at a grade of about 0.6%, while typical grades of copper found along hydrothermal vents are at least ten times

higher. The Nautilus site in Papua New Guinea, Solwara 1, for example, has an average grade of 7.2%.

To date, the International Seabed Authority has granted 19 licences for deep-sea mining and a further five are pending. Consequently, the industry could produce as much as 5% of the world’s supply of rare earth elements – which are used in electronic devices such as smartphones and solar panels – by 2020, rising to 10% by 2030. Norgate says: “The fact that 30% of the world’s oil and gas is sourced offshore suggests

INTO THE DEEP

EMERGING RISKS

WORDS BY ROXANE MCMEEKENILLUSTRATIONS BY PATRICK GEORGE

06_LMM7_Foresight_des12.indd 5 10/07/2014 16:56

SOU

RCE:

‘IS

DEE

P-SE

A M

ININ

G W

OR

TH T

HE

RIS

K?’ I

NFO

GR

APH

IC

the potential of seafloor mining.” So what are the risks of deep-

sea mining? Firstly, there is the fact that it has never been done on a commercial scale. John Cooper is a Senior Partner, Energy and Marine, at Lloyd & Partners, the wholesale insurance broking arm of Jardine Lloyd Thompson. He says that, in fact, deep-sea mining will use many techniques the insurance market already understands. “Some risks will be straightforward to place, such as hull damage.” Others, like sub-sea robots, will be more difficult.

However, “thanks to the oil and gas industry, we are familiar with sub-sea robotics and there are some specialist underwriters out there for this risk”.

But what about the extreme depth at which sub-sea mining robots will operate? Solwara 1, for example, sits 1,600m below the surface. Norgate says: “The equipment is designed so that if something breaks, it can be hooked up to the vessel on the surface, which will have two large cranes. We will be able to do many repairs on board, where we’ll keep critical spare parts.”

The oil and gas industry will also provide a guide to insurance values for deep-sea mining, says Cooper. “The deeper you go, the more costly it is, because you need bigger and more specialist equipment. My guess would

be that vessels could be US$200m and above, and equipment in the tens of millions of dollars.”

From the point of view of liability insurance, Norgate argues that deep-sea mining is in fact relatively low risk. “The robots do all the work, so no-one goes to the seafloor. Our operatives are sitting comfortably in chairs on an air-conditioned ship.”

Environmental liability may be more complicated. Says Cooper: “Assessing the environmental impact of deep-sea mining will be tricky for underwriters. They are used to giving cover for seepage and pollution from wells being drilled, but mining could create alleged damage to seabeds, coral reefs and the sub-sea environment, and that will be harder for insurers to get their heads around because it’ll be difficult to prove and quantify.” Cooper concludes that the risk will probably prove uninsurable.

Regulation could also be problematic. Ian Coles, Global Head of Mining at law firm Mayer Brown, says: “Although the International Seabed Authority (ISA) was created in 1994 and has already granted licences, detailed legislation on how licensing will work – including who will benefit from mining activities – has yet to be worked out.” This will be complicated to resolve in both international waters as well as national areas. “State versus investor is always a hotly contested issue.”

Investors will want these issues sorted out before committing to the seafloor mining industry, says Coles. Whether and how soon the ISA takes decisive action, then, will determine the emerging seafloor mining industry’s ability to fulfil its potential. Once it does, the insurance market won’t find itself in totally unchartered waters.

SEAFLOOR MINING COULD PRODUCE 10% OF THE WORLD’S RARE EARTH ELEMENTS BY 2030

THE ESTIMATED VALUE OF GOLD IN THE SEABED IS TEN TIMES THE ENTIRE US GDP

AND THERE ARE MANY OTHER METALS THAT DEEP-SEA MINING OPERATIONS COULD YIELD…

SUB-SEA MINING SHOULD BOLSTER LOCAL ECONOMIES SIGNIFICANTLY

The rewards beneath the waves

US$

150T

RN:

ESTI

MA

TED

VA

LUE

OF

GO

LD IN

TH

E SE

AB

ED

US$

15.0

9TRN

: U

S G

ROSS

DO

MES

TIC

PRO

DU

CT

MA

NG

AN

ESE

US$

950M

NIC

KEL

US$

759M

CO

PPER

US$

259M

CO

BA

LTU

S$11

8M

DEE

P-SE

A M

ININ

G M

AY B

RIN

G

US$

60B

N IN

TO T

HE

UK

ECO

NO

MY

O

VER

30

YEA

RS

AN

AV

ERA

GE

OPE

RATI

ON

CO

ULD

Y

IELD

US$

20B

N O

VER

20

YEA

RS

TH

E PA

PUA

NEW

GU

INEA

PR

OJE

CT

CO

ULD

AD

D U

S$14

0M

TO T

HE

CO

UN

TRY

’S C

OFF

ERS

12According to the World Shipping Council, China now has 12 of the 20 largest container ports in the world. Find out more in our Market Intelligence Class Review at lloyds.com/ChinaMI

07

06_LMM7_Foresight_des12.indd 6 10/07/2014 10:04

High-profile billionaires are betting on asteroid mining turning into a trillion dollar business

Planetary Resources, a US start-up that plans to extract minerals from space rocks, is poised to launch its first spacecraft – for testing purposes only – this summer. The company, backed by Google’s billionaire founders, as well as Sir Richard Branson and director James Cameron, says asteroid mining will become a trillion-dollar industry.

The rationale is that there are over 1,500 asteroids that are as easy to reach as the Moon. “Asteroids contain useful resources such as platinum group metals, and in concentrations often ten to 100 times that of deposits on Earth,” says Chris Lewicki, President and Chief Engineer at Planetary Resources. “Landing unmanned craft on them and harvesting resources will allow us to cut

the costs of operating in space and make money by bringing materials home.”

Mining water could be particularly profitable. “The components of water – hydrogen and oxygen – are what we fuel rockets with. By extracting them from asteroids we could refuel rockets in space. The cost of getting a pint of water from Earth into space is US$15,000, so this would transform how we operate.”

What are the implications for Lloyd’s? With a mission to reach an asteroid and bring material back currently costing around US$1bn, huge losses are at stake. But Lewicki argues the risks are familiar: “We are using space craft and robots, which the US Government has done for 40 years.” The approach will also be more risk-averse: “Until now space has been a ‘failure is not an option’ environment, but we’ll use multiple, low-cost robotic craft to explore asteroids.” And asteroid mining will involve fewer unknowns than mining or drilling for oil and gas on Earth, “as asteroids floating around our solar system don’t change”.

Lewicki sees Lloyd’s as “the gold standard for insuring what we are doing”. However, he says that while Planetary Resources has cover for travelling into space, “mining in space will be a new risk and we may have to do it once or twice before anyone will insure us”.

EMERGING RISKS NEW RESEARCH

SPACE ROCKS

THE UNCERTAINTIES OF CLIMATE CHANGE

40%

19CMRise in global mean sea levels from 1901-2010

Increase in atmospheric CO2 concentrations since pre-industrial times

While the evidence for climate change is ‘conclusive’, risk models may not account for the phenomenon,says new Lloyd’s research

The Catastrophe Modelling and Climate Change report finds that while climate change trends can be built into models because historical data is fed into them, the trends are not necessarily reflected in the modelling output.

The report, which reviews the latest science, argues that there is a consensus that climate change is driven by human activity, but there is much less agreement on the nature and extent of the change. As a result: “Uncertainties associated with the estimation of both the extent to which climate change is occurring and the resulting change in catastrophe severities… and frequencies, means that the impact can be difficult to account for in risk models.”

THE COST OF GETTING A PINT OF WATER FROM EARTH INTO SPACE IS US$15,000

climate change: the science

DOWNLOAD LLOYD’S 2014 REPORT

CATASTROPHE MODELLING AND CLIMATE

CHANGE AT LLOYDS.COM/RISKINSIGHT

06_LMM7_Foresight_des12.indd 7 10/07/2014 16:57

Sport is big business, but for players and clubs it’s risky too…

The Brazilian Institute of Tourism forecast that visitors to the football World Cup would spend over US$11bn in the country, while FIFA reckoned on collecting US$4bn in revenues from the event – most of it from TV rights, and around a third from sponsorship and marketing.

Sport is undoubtedly big business, but it can also be risky business, not least for the competitors. And insurers play a big part in protecting clubs’ and players’ interests in the beautiful game’s biggest tournament.

FIFA, for instance, has an insurance programme that will compensate a club if one of its players is temporarily injured during an international appearance. The programme kicked off in 2012 after Dutch international Arjen Robben was put out of action for six months while representing his country. His club, Bayern Munich, had to continue paying the star

midfielder’s salary while he was in rehab. To put that in context, a player’s average wage at Manchester City, sport’s highest paying team, is US$5.3m a year, according to Sportingintelligence’s Global Sports Salaries Survey for 2014.

Lloyd’s insurers like Managing Agency Partners, meanwhile, can cover against disablement and medical expenses not covered by FIFA. Clubs can buy wage role protection too, while players, agents and sponsors with a valid insurable interest also offer purchase coverage.

Specialist underwriters, like Jonathan Thomas at Watkins Syndicate, can even cover specific body parts excluded by other insurers, such as a dodgy knee. “Sports professionals, especially those well into their career, with considerable commercial/sponsorship interests, make use of sports disability insurance. And if they can’t get full body insurance they often opt for buyback coverage to address an exclusion gap,” says Thomas.

CLASS OF BUSINESS

LLOYD’S CHAMPIONS DIVERSITY AND INCLUSION

As Lloyd’s develops its presence in existing markets, and as new high-growth territories open up, it needs a workforce that can quickly establish strong relationships with new clients, understand their needs, and work creatively with them. So a joint initiative between the Lloyd’s Market Association and the Corporation, called ‘Inclusion@Lloyd’s’ has recently launched to raise awareness and share best practice around diversity – and ensure the market is highly inclusive and delivers the talent and innovation required for continued success.

Managing agents and brokers are being asked to sign up to a charter and commit to leading and shaping the development of diversity and inclusion, both within their own organisations and across the broader market. They will benefit from access to useful information, tools, case studies and advice, and invitations to educational events. For details, visit lloyds.com/inclusion

LLOYD’S ASIA FORMS GENERAL AVIATION CONSORTIUM

The new Consortium will write General Aviation insurance and reinsurance risks based in Asia-Pacific and the Middle East. It will offer a comprehensive solution for General Aviation risks by providing 100% capacity for aircraft with up to 50 seats, and is led by Catlin Singapore, with the support of Amlin Singapore,Talbot Singapore and Argoglobal Underwriting Asia-Pacific. Says Bobby Heerasing, Chief Underwriting Officer of Catlin’s Asia-Pacific underwriting hub: “With the General Aviation Consortium, brokers and cedents can enjoy an enhanced and highly competitive product offering through a convenient single point of contact, combined with the benefit of Lloyd’s ‘A’ rated security.”

THINKING OUTSIDE THE PENALTY BOX

14 MINUTESThe national average warning time for tornadoes in the US – from the initial alert to the moment the funnel makes ground contact. Find out more on p30

09

06_LMM7_Foresight_des12.indd 8 10/07/2014 10:05

10_LMM7_Big Data_des12 (1).indd 9 10/07/2014 15:56

big data

WORDS BY EDWARD MURRAY

ILLUSTRATION BY STUDIO TONNE

HOW REAL-TIME ANALYSIS IS BEING APPLIED TO RISK EVENTS

WHAT INSURERS NEED TO THINK ABOUT WHEN IMPLEMENTING BIG DATA PROJECTS

THE NEW TECHNOLOGIES CAPTURING A GLUT OF USEFUL INFORMATION

in this issue’s Special Report we explore:

10_LMM7_Big Data_des12 (1).indd 10 10/07/2014 15:56

In 2008, the number of devices connected to the internet surpassed the 6.7 billion people living on the planet. Depending on who you believe there could be as many as one trillion devices connected to the internet by next year.

� e information recorded by these devices – the Internet of � ings – creates a titanic treasure trove of big data for insurers, and they’re pushing hard to analyse it e� ectively and apply the � ndings to their businesses.

As every aspect of life and business becomes digitised, so too does our ability to understand how individual events relate to each other and this will change the way we live.

Peter Hartwell, Senior Researcher at HP Labs, put it very powerfully when he said: “With a trillion sensors embedded in the environment – all connected by computing systems, software, and services – it will be possible to hear the heartbeat of the Earth, impacting human interaction with the globe as profoundly as the internet has revolutionised communication.”

CAPITALISE ON WHAT YOU’VE GOTMany insurers are already focused on extracting fresh insights from the vast amounts of data they currently hold, as the industry rushes to catch up with the rest of the world.

“� eir history has been to exploit their internal databases. � ey are maturing in their understanding of the old data they have and looking for value,” says George Marcotte, Managing Director, Financial Services Analytics for UK and Ireland at Accenture.

However, insurers seeking to put their � nger on the pulse of the Earth’s heartbeat and get an insight into the direct and indirect correlation between world events and commercial losses will probably need to make signi� cant investments in data collection, generation, conversion and storage.

SYNC WITH OTHER SOURCESIn the area of risk management alone, IT company Celent estimates that � nancial � rms will spend US$470m on big data projects this year, and predicts this will rise to US$730m by 2016.

� ese projects fall into four main areas: risk assessment and measurement, risk control and monitoring, risk reporting and governance, and front o� ce and risk operations. Drilling down further, they cover everything from risk

12 / BIG DATA

modelling and scenario analysis, to fraud detection, risk-based pricing and regulatory reporting.

Fraud detection is a big driver when it comes to big data investment in the insurance industry. � rough pan-industry initiatives such as the Claims and Underwriting Exchange and the My Licence project, the Driver and Vehicle Licensing Agency (DVLA) will open up its database to motor insurers so that all information given when someone applies for cover can be instantly cross-checked and forms pre-populated with accurate, up-to-date details of car and driver.

Joining up multiple sources of data can also have signi� cant bene� ts when handling claims, as was seen in the recent prolonged severe ¢ ooding in parts of the UK. Insurers were able to use digital terrain data from Ordnance Survey and Google to predict how inland and coastal ¢ ooding might develop and monitor its spread, alerting claims teams and loss adjusters as well as spotting potentially fraudulent claims that fell outside the a� ected areas.

DO IT THE WAL-MART WAYOne thing underwriters may � nd di� cult to come to terms with though – say Kenneth Cukier and Viktor Mayer-Schönberger, authors of Big Data – is the lack of immediate connection between di� erent databases: “Society will need to shed some of its obsessions for causality in exchange for simple correlations: not knowing why, but only what.”

A simple example of the breakthroughs that can be made once such inhibitions are abandoned comes from Wal-Mart. � ey reviewed years’ worth of till receipts, matched that data against a wide range of other databases, and noticed surprising correlations between hurricane warnings and the types of food people purchased. It didn’t matter that they couldn’t explain why that happened – they had extracted vital sales intelligence and now change the stock in the shops as soon as hurricane warnings are issued.

10_LMM7_Big Data_des12 (1).indd 11 10/07/2014 15:59

13

REMOTE SENSORSNetworks of physical objects that contain embedded technology capable of communicating with the outside environment will provide real-time data on everything from cars to medical implants.

Airliner easyJet has said it will install a prognostic tool in all of its aircraft, which can feed back live updates to operations and engineering staff on the ground – enabling them to begin investigating an issue while a plane is still in the air and ensure the right resources or parts are available when the fl ight lands. These measures should improve effi ciency and operational performance, and reduce delays – and generate valuable information on effective risk management for aircraft fl eets the world over, allowing insurers to refi ne the covers they write.

Elsewhere, sensors embedded in refrigeration units for transport monitor their internal temperature and send alerts when it rises. This lets operators take action and prevent cargoes, including everything from seafood to medical vaccines, from being written off.

UNMANNED AERIAL VEHICLES (UAVs)With no need for manpower, their ability to cover long distances at high altitudes, and to stay airborne for 30-plus hours, the data gathering capabilities of UAVs makes the business of surveillance a lot less risky and more economically viable.

The Australian government is a recent convert. Its new fl eet of Triton UAVs can cruise at 20,000 metres, sweeping a distance greater than Sydney to London with a 360-degree radar. A costly investment maybe – however, more than 80% of China’s oil is imported through the Indian Ocean on Australia’s West Coast. Japan, India and South Korea also depend on this route. And with Somali piracy costing US$5.3bn-US$5.5bn in 2011, with US$635m in insurance claims, the price tag suddenly gets put into context.

Beyond security, commercial UAVs are being used to gather data from aerial surveys of crops to improve yields and farming methods, remotely inspect oil pipelines, and provide detailed data to create 3D mapping.

SATELLITESA satellite’s ability to gather serious detail from great distances is exciting and frightening at the same time. Currently the highest detailed satellite data available has a magnitude of 50cm to a pixel, which means cars and houses are easily identifi able.

In April this year, the European Space Agency’s Copernicus Earth Observation project fl eet of Sentinel-1A satellites took to the skies. It’s aim is to collect data for the earth’s big problems, including natural and manmade disasters that cost the European economy €15bn a year. Offering global coverage day and night to a ground resolution of 5 x 20 metres, the fl eet has already provided imagery of the recent Bosnia-Herzegovina fl oods. In combination with geospatial insight, the data and imagery gathered helped government and relief agencies get a clear picture of the situation and create damage assessment maps, allowing insurers to estimate fl ood damage and assess exposure.

Commercial UAVs are being used to gather data from aerial surveys of crops to improve yields, and to remotely inspect oil pipelines

CUTTING-EDGE DATA GATHERING TECHNOLOGY IS REVOLUTIONISING THE WAY INDUSTRIES OPERATE

collecting data

10_LMM7_Big Data_des12 (1).indd 12 10/07/2014 15:59

14 / BIG DATA

SOME OF THE BIGGEST WINS FOR INSURERS WILL COME FROM HARNESSING THE POWER OF BIG DATA AND APPLYING IT TO NATURAL OR MAN-MADE EVENTS THAT CAUSE CRIPPLING LOSSES

Deploying data

Google Crisis Map

WHAT IS IT: First used in 2012, Google Crisis Map layered data about the size, shape, speed and direction of Superstorm Sandy onto an interactive map. It also overlaid traffic data, evacuation routes, flood zones and shelter locations, and updated the map in real time.

HOW IS IT BEING USED: Google has launched a similar initiative for the 2014 US wildfire season. And recently, it has partnered with the Colombian Institute of Hydrology, Meteorology and Environmental Studies and the National Unit for Disaster Risk Management to provide people with access to useful information before, during and after a natural disaster, such as a tropical storm or earthquake.

IMPLICATIONS: The data comes into its own when responding to property claims after an event, especially when linked to satellite images of storm and flood damage. Insurers can get a very good idea of the scale of the damage, the losses and the on-the-ground response required.

Willis Oil Spill Model

WHAT IS IT: A big data model to help clients understand potential losses from oil drilling operations.

HOW IS IT BEING USED: After the Gulf of Mexico oil spill, Willis worked with the State of Florida to help it understand if it should permit drilling off its coast. It began to build an oil spill model to estimate the frequency, severity and cost of oil spills. Gathering data from sources such as the US Government and the US Geological Survey, the broker now has a tool that can be used for projects around the world. Phil Ellis, Chief Executive Officer of Willis Global Solutions, comments: “We can adjust its application depending on the basic geology, the regulatory framework, the kinds of companies that are there, and the drilling history.”

IMPLICATIONS: The model allows underwriters to more accurately define the extent of exposures associated with particular exploration and drilling projects throughout the world – and lets them draw up the most appropriate wordings for specific risks and price the business from a more informed position.

10_LMM7_Big Data_des12 (1).indd 13 10/07/2014 16:00

15

FROM TERROR ATTACKS TO PANDEMICS, BIG DATA IS HELPING TO REFINE THREAT MODELS

pandemic modelling has moved beyond the losses that insurers would bear from the life market: “What models are increasingly focused on is the business interruption and macro-economic impact that a pandemic can have. They are looking at things such as companies going out of business, trade credit insurance, contingent business interruption losses and all of that secondary activity that could be fairly crippling. A pandemic would also have an impact on an insurer’s investment portfolio on the back of the downturn in the stock market that would occur. That is perhaps more significant in terms of balance sheet impact than the claims themselves.”

Again, big data has an important part to play in modelling the changes that a pandemic would create in investment markets, and being able to monitor and understand the way investment decisions are made, when people are massing into crowded trades and where asset bubbles are starting to rise.

Forewarned is forearmed, and as big data gets better at delivering these insights, insurers and the policyholders they cover will get a better understanding of where losses might occur and how to avoid them.

pandemics Transmissibility and virulence are the two key factors in modelling a pandemic, and big data is providing new insights into both of these.

In regard to transmissibility, it is difficult to locate the first person that a pathogen has infected and then track every other person they have passed it on to. Without an accurate understanding of the total number of people a pathogen has infected, it is almost impossible to effectively estimate just how deadly it is.

However, big data is making it easier to tackle these problems. “What we’re hoping,” says Dr Andrew Coburn, Senior Vice President at RMS, “is that with big data we will get a much better idea of infection rates. One experiment that has been very interesting is Google Flu, which essentially tracks search terms. People who feel ill type in ‘flu symptoms’, or such like, and they’ve found that the wave of search terms is highly correlated with the outbreak of flu.”

The earlier insurers can get an indication of a developing pandemic, the faster they can provide advice to insureds around everything from the drugs that hospitals will need to order and the resources local authorities will require, to what businesses and individuals can do to avoid infection.

In addition, Coburn says the focus for

modelling data

THREAT #1

PredPol

WHAT IS IT: PredPol helps to put police officers in the right place at the right time, giving them the best chance of preventing crime. The technology is broadly similar to that used to predict the aftershocks following a major earthquake. Once a crime has been committed, it attempts to anticipate where the next one will happen. HOW IS IT BEING USED: Deployed by the Los Angeles Police Department, PredPol has analysed data on 13 million arrests dating back over 80 years. In the Foothill Division where it was first implemented, crimes were down 13% in the four months following the rollout – compared to an increase of 0.4% in the rest of the city.

IMPLICATIONS: A reduction in crime has implications in many different lines of business, from property and motor to medical and travel. Potentially, it could be very useful if insurers could persuade police authorities to share the data so they can overlay it on their existing underwriting information to get a more accurate picture of theft and fraud risks in an area.

10_LMM7_Big Data_des12 (1).indd 14 10/07/2014 16:00

terrorist attacksTerrorist attacks present a number of major problems for insurers, particularly in regard to probabilistic modelling and risk accumulation. The good news is that terrorist risk modelling has become a lot more sophisticated in the last decade, and big data has played a significant part in this evolution.

A recent white paper from RMS reveals that its models for terror attacks are plugged into simulations of over 90,000 possible large-scale attacks against 9,800 different targets worldwide, with 35 potential methods of attack – ranging from improvised explosive devices to biological and nuclear attacks.

Explaining how the RMS models work, Chris Folkman, Director, Model Project Management at RMS, says they rely on understanding where terrorist plots take place; how often they take place; how successful they are and what the counter terrorism capabilities are within a given region.

“That basically gets us to the number of successful attacks that can be expected in a particular place each year and we use that as the starting point for the probability of an attack.”

Looking beyond probability calculations, the other major problem for insurers is the localised nature of most terrorism events. The World Trade Centre was situated on a 16-acre site and yet the losses ran to tens of

The models help insurers find hotspots of exposure. They can use them to quantify a worst-case scenario attack at a location of interestCHRIS FOLKMAN, DIRECTOR, MODEL PROJECT MANAGEMENT, RMS

billions of dollars. “That means two things,” says Folkman. “First, it is very difficult to diversify because the risk is concentrated and it is often in urban areas where there is a lot of insurable exposure. Second, it is important that the data that goes into the model in terms of the location is accurate – preferably to building level.”

The RMS models can calculate exposure in relation to not only the property risks, but also those associated with lines of business involving human exposure – including life insurance, workers’ compensation and personal accident.

For insurers, this sort of modelling brings a number of benefits. Says Folkman: “The models help insurers find hotspots of exposure. They can use them to quantify a worst-case scenario attack at a location of interest. And they can use them to create underwriting rules, and at a corporate level to create risk appetite guidelines.”

THREAT #2

16 / BIG DATA

10_LMM7_Big Data_des12 (1).indd 15 10/07/2014 16:00

17

THE SCOPE FOR USING BIG DATA TO UNLOCK NEW BUSINESS IS HUGE. BUT FIRST, YOU HAVE TO MANAGE THE IMPLEMENTATION. WE TALK TO TONY BOOBIER, BUSINESS ANALYTICS INSURANCE LEADER FOR EUROPE, IBM

MARKET: How infl uential is big data in the world of insurance?TONY BOOBIER: There are a lot of projects wrapped up under the big data banner. Whether insurers are looking at risk, customer analytics, or operational analytics, the big data agenda is all-pervasive. To date, the applications have been limited predominantly to the personal lines market. One area that has experienced signifi cant change is user-based insurance in the motor sector. But we’re now seeing big data pervade in the commercial lines market too, and many of its specialised areas. Data

talking data

is coming from space satellites, UAVs and devices embedded in everything from cars to cargo ships. And all of this information is being used to generate insight into the risks insurers underwrite. MARKET: How should insurers implement big data projects?TB: We think of implementation in terms of three core components. The fi rst is the challenge presented by the data and how you get a solid information infrastructure. Then there are the skills and software solutions you need, and how you embed these tools into your organisation. Third is the issue of culture. Businesses that adopt a big data and analytics agenda need to have a fact-driven leadership. The board does not need to be technologically savvy, but it does need to provide leadership to ensure a data-driven culture. MARKET: How important is data accuracy?TB: There’s a misconception that every piece of data needs to be irreproachable to be able to extract useful insight. We recommend that fi rms fi rst identify the outcomes they’re looking for and then work backwards to prioritise what data cleansing and organisation is required. If you do it the other way around and try and get all of the data spot on, it can feel like you’re trying to tame a tidal wave.

In an environment where so much data is unstructured, you’re never going to get it perfect. We tend to look at the world through UK or European glasses. But as insurers focus on growth markets like Asia or Latin America, the quality of information we’ve traditionally had is not quite as good. There needs to be some pragmatism.

10_LMM7_Big Data_des12 (1).indd 16 10/07/2014 16:00

18 / INFOGRAPHICWORDS BY HELEN YATESILLUSTRATIONS BY THE DESIGN SURGERY

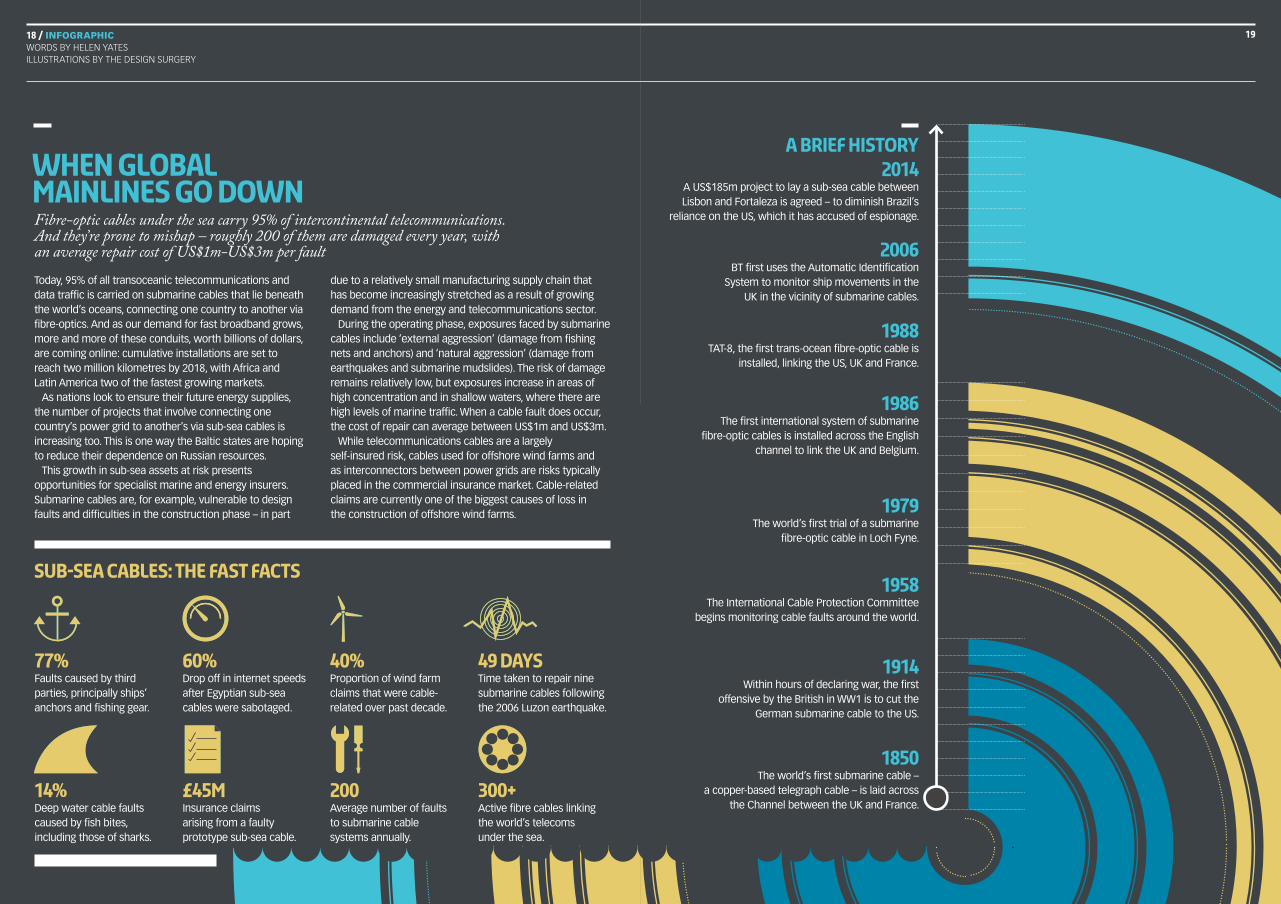

when global mainlines go downFibre-optic cables under the sea carry 95% of intercontinental telecommunications. And they’re prone to mishap – roughly 200 of them are damaged every year, with an average repair cost of US$1m-US$3m per faultToday, 95% of all transoceanic telecommunications and data traffic is carried on submarine cables that lie beneath the world’s oceans, connecting one country to another via fibre-optics. And as our demand for fast broadband grows, more and more of these conduits, worth billions of dollars, are coming online: cumulative installations are set to reach two million kilometres by 2018, with Africa and Latin America two of the fastest growing markets.

As nations look to ensure their future energy supplies, the number of projects that involve connecting one country’s power grid to another’s via sub-sea cables is increasing too. This is one way the Baltic states are hoping to reduce their dependence on Russian resources.

This growth in sub-sea assets at risk presents opportunities for specialist marine and energy insurers. Submarine cables are, for example, vulnerable to design faults and difficulties in the construction phase – in part

due to a relatively small manufacturing supply chain that has become increasingly stretched as a result of growing demand from the energy and telecommunications sector.

During the operating phase, exposures faced by submarine cables include ‘external aggression’ (damage from fishing nets and anchors) and ‘natural aggression’ (damage from earthquakes and submarine mudslides). The risk of damage remains relatively low, but exposures increase in areas of high concentration and in shallow waters, where there are high levels of marine traffic. When a cable fault does occur, the cost of repair can average between US$1m and US$3m.

While telecommunications cables are a largely self-insured risk, cables used for offshore wind farms and as interconnectors between power grids are risks typically placed in the commercial insurance market. Cable-related claims are currently one of the biggest causes of loss in the construction of offshore wind farms.

77% Faults caused by third parties, principally ships’ anchors and fishing gear.

40% Proportion of wind farm claims that were cable-related over past decade.

60% Drop off in internet speeds after Egyptian sub-sea cables were sabotaged.

49 daysTime taken to repair nine submarine cables following the 2006 Luzon earthquake.

14% Deep water cable faults caused by fish bites, including those of sharks.

200Average number of faults to submarine cable systems annually.

£45m Insurance claims arising from a faulty prototype sub-sea cable.

300+Active fibre cables linking the world’s telecoms under the sea.

sub-sea cables: the fast facts

18_LMM7_Sub_Cabs_des4.indd 17 14/07/2014 12:18

19

1850The world’s first submarine cable –

a copper-based telegraph cable – is laid across the Channel between the UK and France.

1914Within hours of declaring war, the first

offensive by the British in WW1 is to cut the German submarine cable to the US.

1958The International Cable Protection Committee

begins monitoring cable faults around the world.

1979The world’s first trial of a submarine

fibre-optic cable in Loch Fyne.

1986The first international system of submarine

fibre-optic cables is installed across the English channel to link the UK and Belgium.

1988TAT-8, the first trans-ocean fibre-optic cable is

installed, linking the US, UK and France.

2006BT first uses the Automatic Identification

System to monitor ship movements in the UK in the vicinity of submarine cables.

2014A US$185m project to lay a sub-sea cable between Lisbon and Fortaleza is agreed – to diminish Brazil’s

reliance on the US, which it has accused of espionage.

a brief history

18_LMM7_Sub_Cabs_des4.indd 18 14/07/2014 12:18

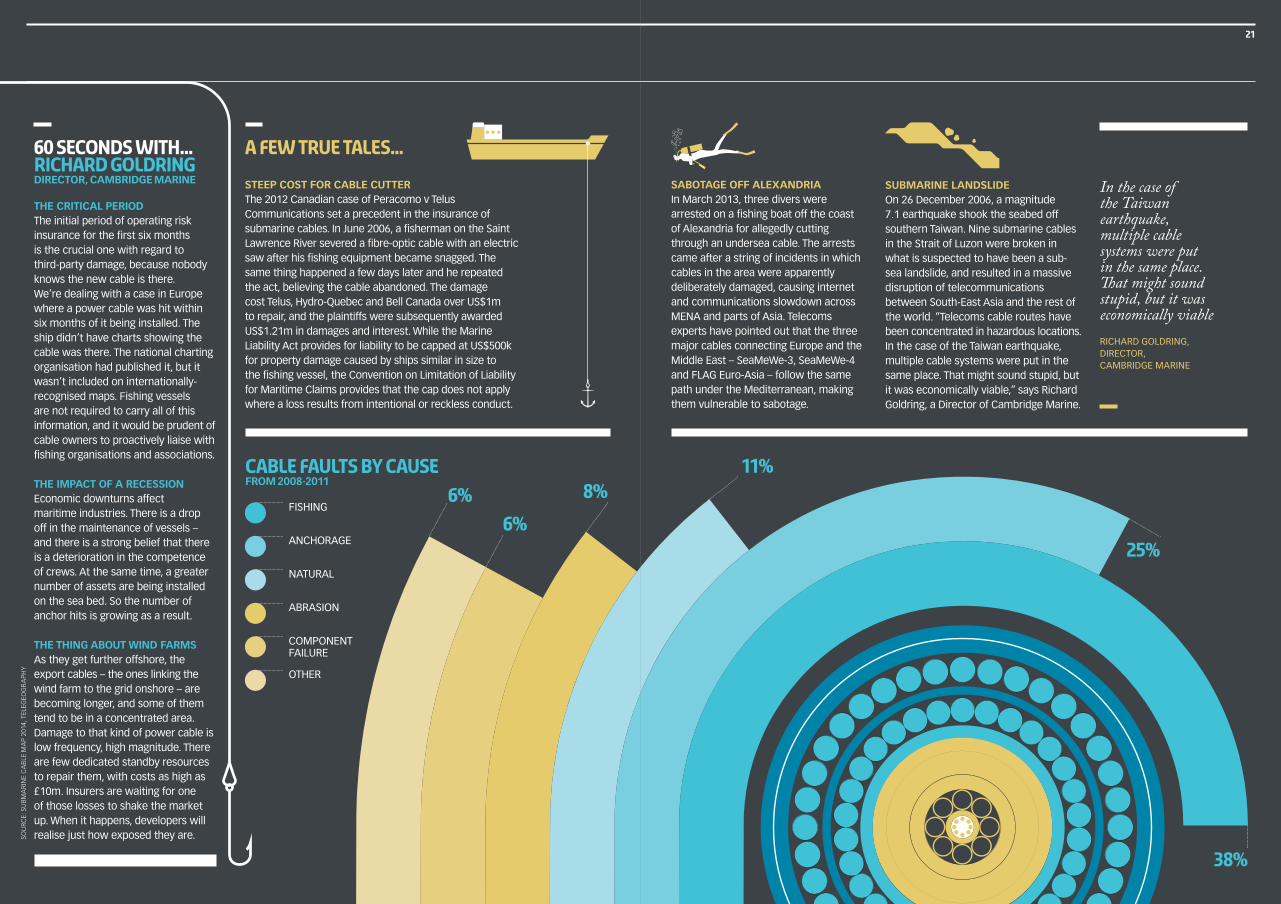

STEEP COST FOR CABLE CUTTER The 2012 Canadian case of Peracomo v Telus Communications set a precedent in the insurance of submarine cables. In June 2006, a fisherman on the Saint Lawrence River severed a fibre-optic cable with an electric saw after his fishing equipment became snagged. The same thing happened a few days later and he repeated the act, believing the cable abandoned. The damage cost Telus, Hydro-Quebec and Bell Canada over US$1m to repair, and the plaintiffs were subsequently awarded US$1.21m in damages and interest. While the Marine Liability Act provides for liability to be capped at US$500k for property damage caused by ships similar in size to the fishing vessel, the Convention on Limitation of Liability for Maritime Claims provides that the cap does not apply where a loss results from intentional or reckless conduct.

a few true tales…

cable faults by causeFROM 2008-2011

THE CRITICAL PERIODThe initial period of operating risk insurance for the first six months is the crucial one with regard to third-party damage, because nobody knows the new cable is there. We’re dealing with a case in Europe where a power cable was hit within six months of it being installed. The ship didn’t have charts showing the cable was there. The national charting organisation had published it, but it wasn’t included on internationally-recognised maps. Fishing vessels are not required to carry all of this information, and it would be prudent of cable owners to proactively liaise with fishing organisations and associations.

THE IMPACT OF A RECESSIONEconomic downturns affect maritime industries. There is a drop off in the maintenance of vessels – and there is a strong belief that there is a deterioration in the competence of crews. At the same time, a greater number of assets are being installed on the sea bed. So the number of anchor hits is growing as a result.

THE THING ABOUT WIND FARMSAs they get further offshore, the export cables – the ones linking the wind farm to the grid onshore – are becoming longer, and some of them tend to be in a concentrated area. Damage to that kind of power cable is low frequency, high magnitude. There are few dedicated standby resources to repair them, with costs as high as £10m. Insurers are waiting for one of those losses to shake the market up. When it happens, developers will realise just how exposed they are.

60 seconds with… Richard GoldringDIRECTOR, CAMBRIDGE MARINE

FISHING

ANCHORAGE

NATURAL

ABRASION

COMPONENT FAILURE

OTHER

6%

6%

8%

SOU

RCE:

SU

BM

AR

INE

CA

BLE

MA

P 20

14, T

ELEG

EOG

RA

PHY

18_LMM7_Sub_Cabs_des3 (1).indd 19 10/07/2014 16:02

21

SABOTAGE OFF ALEXANDRIA In March 2013, three divers were arrested on a fishing boat off the coast of Alexandria for allegedly cutting through an undersea cable. The arrests came after a string of incidents in which cables in the area were apparently deliberately damaged, causing internet and communications slowdown across MENA and parts of Asia. Telecoms experts have pointed out that the three major cables connecting Europe and the Middle East – SeaMeWe-3, SeaMeWe-4 and FLAG Euro-Asia – follow the same path under the Mediterranean, making them vulnerable to sabotage.

SUBMARINE LANDSLIDE On 26 December 2006, a magnitude 7.1 earthquake shook the seabed off southern Taiwan. Nine submarine cables in the Strait of Luzon were broken in what is suspected to have been a sub-sea landslide, and resulted in a massive disruption of telecommunications between South-East Asia and the rest of the world. “Telecoms cable routes have been concentrated in hazardous locations. In the case of the Taiwan earthquake, multiple cable systems were put in the same place. That might sound stupid, but it was economically viable,” says Richard Goldring, a Director of Cambridge Marine.

In the case of the Taiwan earthquake, multiple cable systems were put in the same place. That might sound stupid, but it was economically viableRICHARD GOLDRING, DIRECTOR, CAMBRIDGE MARINE

11%

25%

38%

18_LMM7_Sub_Cabs_des3 (1).indd 20 10/07/2014 16:02

Insurers of large property portfolios in the world’s great coastal cities will have factored the effects

of climate change into their catastrophe models – including rising sea levels and more frequent

storm surges. But what’s often missed is that many of these cities are sinking faster than the water is

rising. In some, subsidence outstrips sea level rise by a factor of ten to one.

Together with sea water inundation and flood damage, this can have disastrous consequences for the

built environment – and property and business interruption insurers. The surge that overwhelmed New

Orleans following Hurricane Katrina, and the subsequent cascading collapse of critical infrastructure,

offered a glimpse of the sort of scenario underwriters fear. “We’re going down and the sea is coming

up,” confirms Gilles Erkens, of the Deltares Research Institute in Utrecht. “Potential losses could run

into hundreds of millions of dollars every year.”

The causes are varied. Foremost is large-scale

groundwater extraction for drinking water and

industrial processes – although elsewhere, like

Los Angeles, it is oil and gas extraction that is to

blame. Some urban areas are also constructed

on multiple layers of soft soil, which compacts

when built on – one of the problems facing

New Orleans, for instance, and a feature of

megacities that spring up on river deltas, such

as Guangzhou in south west China.

One of the most severely affected cities was

Tokyo, which grew rapidly in the middle of the

last century and sunk over four metres as a result

– until drastic remedial measures were put in

place in the 1970s to restrict the extraction of

groundwater. Since then the subsidence has

stabilised. But from Jakarta and Dhaka to

Venice, the risks are still all too real…

As sea levels rise, ground levels in coastal megacities are also

falling – with potentially disastrous implications for insurers

22 / SUBSIDENCE

The sinking cities

WORDS BY DAVID WORSFOLD ILLUSTRATIONS BY DENIS CARRIER

We’re going down and the sea is coming up. Potential losses could run into hundred of millions of dollars every yearGILLES ERKENS,

DELTARES RESEARCH

INSTITUTE, UTRECHT

22_LMM7_Subsidence_des6.indd 21 10/07/2014 10:11

23

Insurers of large property portfolios in the world’s great coastal cities will have factored the effects

of climate change into their catastrophe models – including rising sea levels and more frequent

storm surges. But what’s often missed is that many of these cities are sinking faster than the water is

rising. In some, subsidence outstrips sea level rise by a factor of ten to one.

Together with sea water inundation and flood damage, this can have disastrous consequences for the

built environment – and property and business interruption insurers. The surge that overwhelmed New

Orleans following Hurricane Katrina, and the subsequent cascading collapse of critical infrastructure,

offered a glimpse of the sort of scenario underwriters fear. “We’re going down and the sea is coming

up,” confirms Gilles Erkens, of the Deltares Research Institute in Utrecht. “Potential losses could run

into hundreds of millions of dollars every year.”

The causes are varied. Foremost is large-scale

groundwater extraction for drinking water and

industrial processes – although elsewhere, like

Los Angeles, it is oil and gas extraction that is to

blame. Some urban areas are also constructed

on multiple layers of soft soil, which compacts

when built on – one of the problems facing

New Orleans, for instance, and a feature of

megacities that spring up on river deltas, such

as Guangzhou in south west China.

One of the most severely affected cities was

Tokyo, which grew rapidly in the middle of the

last century and sunk over four metres as a result

– until drastic remedial measures were put in

place in the 1970s to restrict the extraction of

groundwater. Since then the subsidence has

stabilised. But from Jakarta and Dhaka to

Venice, the risks are still all too real…

JAKARTA, INDONESIA

Jakarta is subsiding faster than any

other megacity. The northern part has

sunk by nearly four metres in the last

35 years, mainly due to groundwater

extraction as the population has

mushroomed and former agricultural

land has been taken over by massive

residential and industrial developments.

Across the city as a whole, Jakarta

is sinking five to ten centimetres a year.

The subsidence has severely damaged

buildings and infrastructure, increased

flooding in densely populated areas,

destroyed local groundwater systems

and increased seawater intrusion. This

has started to threaten key commercial

districts of the city, where many major

Asian, American and European

companies are based. It is here that

the largest insurance exposures will be

concentrated, and one of the reasons

the authorities are now taking action.

To help cope with the threat, the

Dutch Government is giving $4m for a

feasibility study to build a dyke (levee)

around Jakarta Bay, drawing on its

experience of protecting its own coastal

cities, such as Rotterdam. In January

this year, the Indonesian Government

also agreed to build two new dams and

a 1.2 km flood relief tunnel. Plus, there

are plans to expand the reservoirs that

serve the conurbation of 28 million

people that surrounds Jakarta, so that

new restrictions can be imposed on the

extraction of groundwater for both

domestic and industrial use.

DHAKA, BANGLADESH

Dhaka is dropping 15mm a year, as

the impact of slowly shifting tectonic

plates coincides with the effects of

massive water extraction. “When we

extract groundwater, the empty spaces

in the sponge-like soil are filled with air

until they get recharged with rainwater

again,” says Professor Syed Humayun

Akhter, of Dhaka University. But the

concreting over of the surface prevents

this happening – this vacuum might be

filled with brackish seawater, turning

the area into a saline land, and leading

to the desertification of some areas.

One big challenge facing authorities

is that, due to endemic surface and

river water pollution from industrial

and household waste, 83% of Dhaka’s

water comes from cleaner underground

sources. “Nowhere in the world

do authorities depend fully on

groundwater,” says urban expert,

Professor Nazrul Islam. Without major remedial measures

to reduce this reliance and scale back

extraction programmes, the OECD

estimates that by 2070 over 11 million

people in Dhaka will be exposed to

flood risk on a scale that could bring the

city to a standstill for months or force

abandonment of some districts – further

magnifying potential insured losses, as

no restoration would be contemplated.

Currently, there are proposals to build

a dyke along the eastern side of the city

and improve the drainage by dredging

badly silted canals.

VENICE, ITALY

Venice sunk about 120mm in the

20th century due to natural and human

causes. In addition, the sea level rose

about 110mm. A range of measures –

such as restrictions on groundwater

extraction – were introduced to

stabilise the problem. But recent

satellite mapping suggests these

may not be enough, as the city is still

subsiding by one to two millimetres a

year. The causes are two-fold.

First, the Adriatic plate, on which

Venice sits, is slowly sliding beneath the

Apennine Mountains and causing the

city and its environs to drop steadily.

The area is also tilting by a millimetre

or two eastward every year. The second

cause is the restoration of its historic

buildings: “When some people restore

their buildings, they load them and

they can go down significantly by

up to five millimetres in a year,”

Pietro Teatini, a researcher from the

University of Padova, told the BBC.

Coupled with the threat of rising sea

levels, estimated to be between three

and ten millimetres a year, this

persistent fall in ground level could

prove a perfect storm for insurers.

And, unless there’s better co-operation

between property owners, authorities

and commercial interests, it will hit

Venice in the next decade, says the

University of Padova’s research team.

Currently, a multi-billion dollar project

to build new barriers that can be raised

in the face of high tides is underway.

22_LMM7_Subsidence_des6.indd 22 10/07/2014 10:12

25

Once besieged by organised crime, left-wing insurgency and right-wing paramilitaries – and in a state of near-civil war, with many parts of the country outside of the government’s control – Colombia has emerged as a bright spot in Latin America. Former President Álvaro Uribe Vélez, who came to power in 2002, put a big dent in the security risk, and the recently re-elected incumbent – President Juan Manuel Santos Calderón – is now trying to hammer out a final peace agreement with the guerrillas, ending the violence for good.

This political stability has had a big impact on Colombia’s economic and social development, with unprecedented growth in infrastructure in particular. According to AM Best’s 2014 report, The State of Insurance Regulation in Latin America, the government plans to award 25 highway projects at a cost of around US$21bn, increase port investments by 20% to nearly US$500m, and upgrade four airports this year. Infrastructure investments are expected to be between 3%-6% of GDP by 2016, versus the current 1.5% level.

“Despite the tough times, Colombia has experienced only two years of economic contraction – a remarkable achievement in a continent beset by boom and bust cycles,” says Gabriel Anguiano, who heads up Lloyd’s international market development in Latin America. In fact, the World Bank reports that Colombia’s GDP has grown each year since 2004 by between 2% and 7%. It describes Colombia as “upper middle income”, with robust spending, and predicts growth to stay above 4% each year.

In non-life insurance, the outlook is even rosier. Written premium is expected to increase from US$4.3bn in 2012 to US$6.1bn in 2017, recording a projected compound annual growth rate of 8.2%.

And the insurance regulator – the financial superintendent – is keen to bring Colombia’s economy into line with more open markets. Working with the insurance trade association, Fasecolda, it is veering away from protectionist law for local firms to rules based on solvency and competency, allowing any firm that can meet the standards to compete freely.

FOREIGN CAPITAL WELCOMEReinsurance is different. There has never been a monopoly and global players have always been present – there are no local Colombian reinsurers. Foreign reinsurers only have to renew their licences each year and meet credit rating standards. In key lines, the solvency regime imposed on insurance companies means the maximum net retention admissible is 10% of the net equity, meaning lines with catastrophic exposure such as earthquake and surety require a lot of reinsurance support.

Humberto Cabrera, CEO of broker Aon Benfield in Colombia, which was originally established as an Alexander Howden operation 22 years ago, explains: “Until July 2013, domestic exposures could not be covered by insurance written outside Colombia. However, the situation has since changed and now only compulsory insurance and government risks are exclusively

Sustained economic growth and the introduction of open market policies are creating new opportunities for foreign insurers to diversify their interests in Colombia

WORDS BY CHRIS WHEAL ILLUSTRATIONS BY ANGUS GREIG

24 / COLOMBIA

reserved for locally established companies. Foreign capital has always been welcomed and no restrictions on ownership apply. Along with Miami, Colombia is becoming a hub for international players interested in Latin America.”

Lloyd’s eyes Colombia as an opportunity and, as of April 2014, it is authorised to write marine, aviation and transport insurance from Colombia – covering international maritime transport, international commercial aviation, and space launch and transportation (including satellite) risks.

Lloyd’s Anguiano has already been providing syndicates in London with market information and insight. “Last year, Lloyd’s held a ‘Colombia Insurance Day’ and in April this year managing agents visited Colombia. The work to raise awareness cuts both ways, educating the Colombian insurance market about the modern Lloyd’s,” he says. Anguiano and Lloyd’s International Regulatory Affairs team are also working with the financial superintendent to get approval for a Lloyd’s representative office.

At present, Liberty Specialty Markets is the only Lloyd’s firm on the ground in Colombia. Its representative office opened in May 2012. Jose Ospina is the manager. “Countries in Latin and Central America, including

Colombia, are traditionally European in the form in which they arrange their reinsurance. This means that in Latin America everyone is trying to have long-term relationships through proportional treaties, but at the moment these have some restrictions. The new reinsurers are trying to push through important changes to proportional treaties. We are developing a mainly non-proportional reinsurance treaty and facultative reinsurance business,” he says.

A DEARTH OF ACCURATE DATAOne problem is the amount of information used to calculate risk. The regulator’s financial changes take into account the fact that the information available is not the

same as insurers/reinsurers would get in Europe or in the US. There is a question over the accuracy of the data, which means foreign players tend to be cautious in the market.

But Ospina flags up how Colombia opens doors to the rest of the region too. “Colombia is a hub. There are 13 reinsurers’ offices to attend in the region and access to other countries is easy, as plenty of airlines enable you to do your business across the whole region. If you decide to go to Mexico, Lima or Buenos Aires tomorrow, you can find five or six flights from Bogotá.”

Colombia also has a reputation for highly trained and skilled insurance professionals. Ospina is President of the Colombian Reinsurers Association / ACTER, which is developing educational training and programs to ensure the new generation of insurers continue to have the appropriate technical skills. “I am 45 years old and may be viewed as something of a dinosaur. You will find a lot of ‘dinosaurs’ who learned 25 years ago when the academic training was very good. Now a lot of young people are coming into the industry and into the ACTER academic committee. On this committee, there are some experienced individuals from Aon Benfield, XL Re, Munich Re, and from some of the insurance companies. They are trying to develop the best technical knowledge in universities,” he says.

THE MYTH OF THE FAST BUCKWith all this good news comes a warning: it’s probably not possible to launch in Colombia and make a quick buck. The 13 registered international reinsurers are operating in what is currently an overcrowded market. Property is the main focus. The impact of La Niña and flooding brought renewed demand and there have been seismic activity claims too, but the small proportion of the insured market – perhaps just 10% of a catastrophe’s total cost – means price corrections don’t happen fast. New entrants

Lloyd’s has maybe 100 products not sold in this market, but the problem is how to develop the culture to create demand for them

26 / COLOMBIA

JOSE OSPINA, MANAGER, LIBERTY SPECIALTY MARKETS COLOMBIA

24_LMM7_Colombia_des7.indd 25 10/07/2014 10:13

In some cases, the insurers are trying to produce parametric covers, but these are not the solution – they are only a cat solution. We need to cover all the exposures with frequency in the claims expected, but it is necessary to develop a role for the Government to cover the excess so that insurers and reinsurers can cover what the Government wants insured,” Ospina says.

But he believes Lloyd’s has something special to offer Colombia. “There is an opportunity for non-traditional exposures. Lloyd’s has maybe 100 products not sold in this market, but the problem is how to develop the culture to create demand for them. You need to approach the decision-makers and provide added value to make a difference to the Government and to companies. If you don’t do that, you are just another player and you won’t make money.”

In addition, Lloyd’s syndicates realise they have to build foundations for long-term development in the Colombian market, including prompt settlement of valid claims. Says Ospina: “There’s no point opening an office and someone saying, ‘Lloyd’s is here, I am here’. You will spend three years waiting for the business to come in and it won’t.”

FOR THE LATEST MARKET INTELLIGENCE ON COLOMBIA

VISIT: LLOYDS.COM/COLOMBIAMI

27

competing on price will only find themselves with the same risks and not enough premium, says Ospina.

“What you have is commercial pricing, not technical pricing. The risk for Lloyd’s syndicates is that they will have a lot of expenses and the average claim cost could be high. Additionally, substantial growth should be viewed with caution as it is difficult to achieve profitably in the current market,” he says.

There are opportunities. Aon Benfield’s Cabrera says: “The future resides very much in growth in the personal lines sector – driven by demand from the country’s growing middle class – and also in specialty lines around the growing areas of the economy, mainly infrastructure, agriculture and natural resources.” Insurance is currently not sold to the mass market, only to the wealthy.

Ospina says, for example, he only has insurance for his home and car because the bank lending him the money makes insurance compulsory. The growth potential if the ‘direct’ insurance market expands is huge. “When you check the GDP in every country in Latin America, except for Brazil, the share of GDP for insurance is only 1%-1.3%. Insurance is expensive for the average person in our countries,” he says.

THE AGRICULTURE OPPORTUNITYOspina thinks the biggest opportunity is in agricultural insurance. That means talks must take place between the Government and private sector insurers and reinsurers to create a market. South American politics tends to mean a new president sweeps a broom through the civil servants too, breaking the point of contact and wiping out the experience, making those practical discussions harder.

“The Colombian Government has a big fund to provide some subsidy for insurance in the agriculture sector, but the insurers selling agricultural insurance are not providing the levels of cover and protection the government is expecting.

24_LMM7_Colombia_des7.indd 26 10/07/2014 10:13

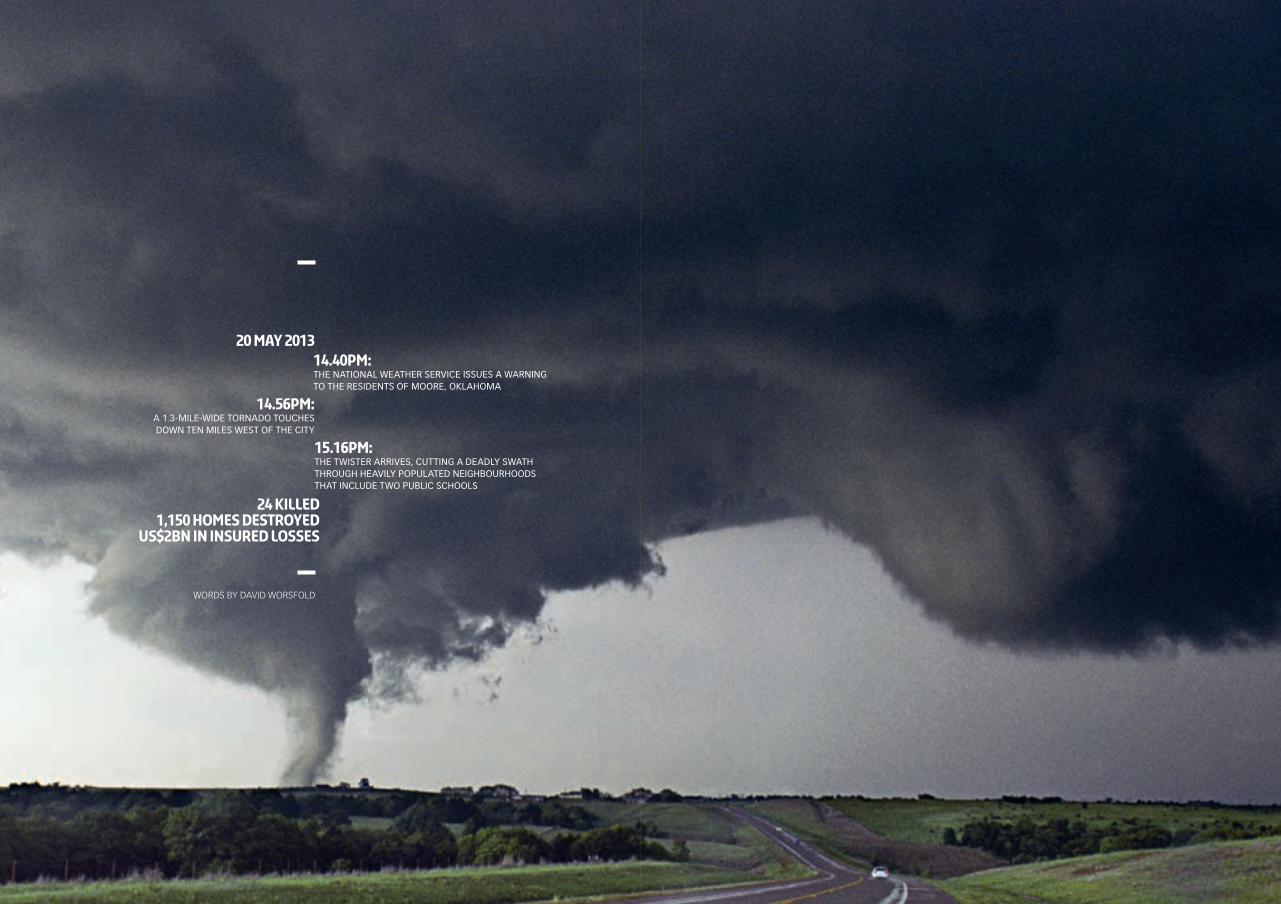

WORDS BY DAVID WORSFOLD

20 May 2013

24 killed 1,150 homes destroyed

US$2bn in insured losses

15.16pm: THE TWISTER ARRIVES, CUTTING A DEADLY SWATH THROUGH HEAVILY POPULATED NEIGHBOURHOODS THAT INCLUDE TWO PUBLIC SCHOOLS

14.56pm: A 1.3-MILE-WIDE TORNADO TOUCHES DOWN TEN MILES WEST OF THE CITY

14.40pm: THE NATIONAL WEATHER SERVICE ISSUES A WARNING TO THE RESIDENTS OF MOORE, OKLAHOMA

28_ LMM7_Tornadoes_des11.indd 27 10/07/2014 13:08 28_ LMM7_Tornadoes_des11.indd 28 10/07/2014 13:08

� e Moore tornado was just one of 76 that hit ten US states that month – and the country’s costliest natural disaster last year. And yet 2013 pales next to the destruction wrought by the 1,600 tornadoes that ripped across the US in 2011 – the worst year ever for this type of catastrophe. More than 550 people died, with estimated damages of US$28bn.

Such tragic consequences are unusual. � e average number of fatalities has steadily declined since 1925 and, before Moore, only one of the 25 deadliest twisters occurred in the last 58 years. � at said, annual � gures for the US – where three-quarters of the world’s tornadoes arise – are nevertheless remarkable.

On average 1,200 tornadoes take 60 lives, injure 1,500 and hemorrhage at least US$400m from the economy every year. And, according to the US Insurance Information Institute (III), 36% of all annual natural disaster-related claims payouts are o� the back of tornado strikes. Oklahoma (US$9.8bn) is second only to Texas as the state (US$16.9bn) with the costliest payouts resulting from thunderstorms, tornadoes and hail for the years 2000-2013.

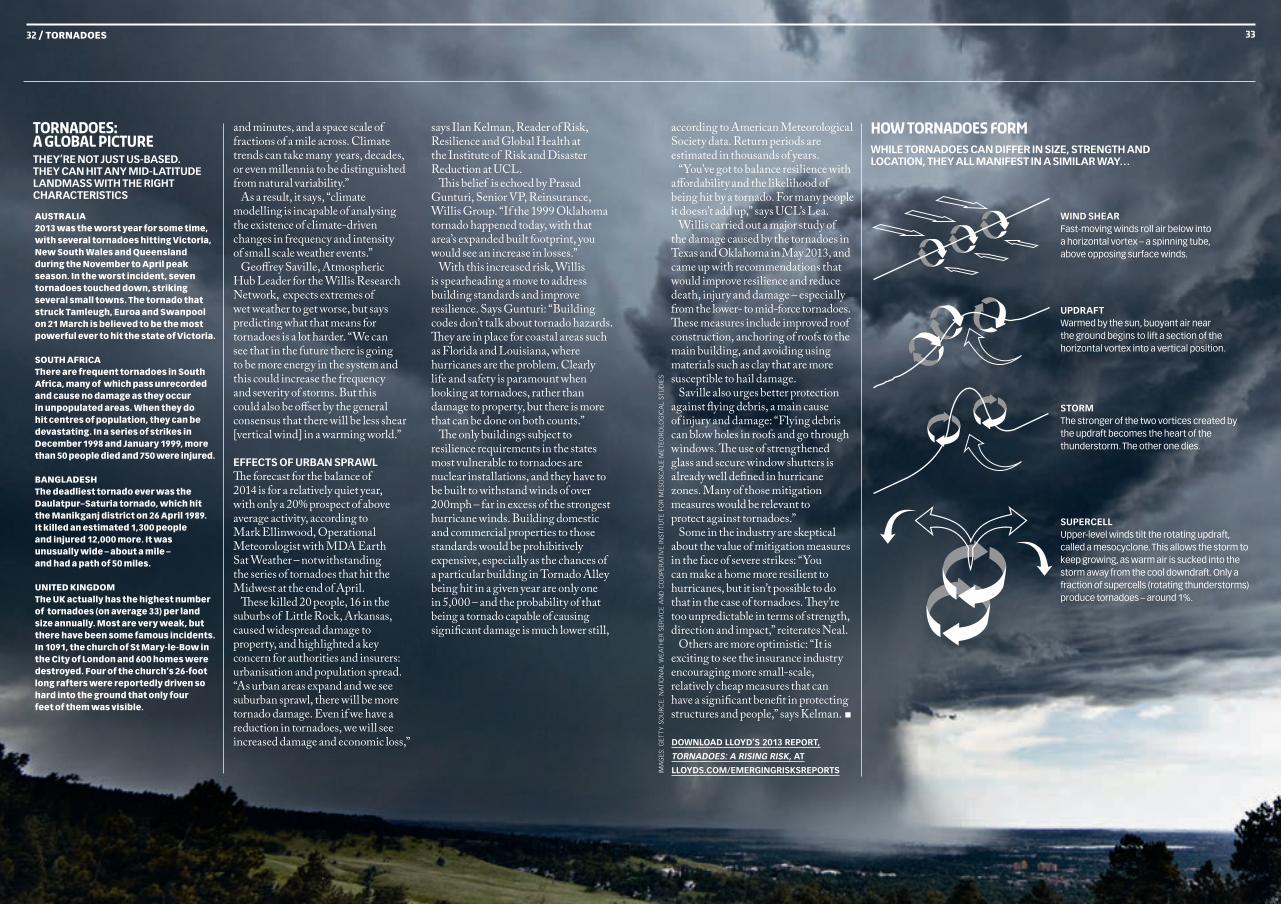

ISSUES OF UNPREDICTABILITYWith their penchant for widescale devastation, tornadoes have the dubious accolade of being the most

violent of all atmospheric storms. When they do form – most frequently in late spring and early summer, with May historically the peak month – they sweep across the Great Plains, along the notorious Tornado Alley, bringing winds of more than 200mph. A top-rated twister that struck Oklahoma in 1999 registered winds in excess of 300mph – the strongest ever recorded on earth.

Beyond their raw, terrifying power, though, it’s tornadoes’ � ckle nature that gives them their extraordinary capacity for damage – and makes them such a headache for insurers.

� is unpredictability is evidenced by the narrow preparation window a� orded to the residents of Moore: just 36 minutes from the initial alert to annihilation. Sixteen, if you lived in neighbouring Newcastle and stopped the clock the moment the funnel made ground contact – which is roughly two minutes better than the national average warning time.

But what makes tornadoes so inscrutable? Firstly, understanding tornado formation is not an exact science. Experts know that twisters in Tornado Alley are borne out of warm, wet air from the Gulf of Mexico crashing into cold, dry air descending from the Rocky Mountains, creating the right conditions for the massive rotating columns of air called ‘supercells’ – the grand thunderstorms below which tornadoes can form. But they don’t know which of these will actually spawn tornadoes and which won’t. Statistically, only 1% of thunderstorms produce tornadoes.

Another problem is that tornadoes are often very localised and dynamic,

changing direction quite suddenly. � e friction caused by blades of grass can be a determining factor.“� ey have narrow, varied paths and, as we have seen, they can be quite catastrophic over small areas as well as larger regions,” says Kirsten Orwig, Specialist in Atmospheric Perils, Swiss Re America. “You have to make a lot of assumptions when modelling the potential impact, and the predictions can be uncertain as a result.”

Even within the track of a tornado, the destruction can be randomly distributed. Inside a mile-wide circulation, you can have miniature tornadoes – or suction vortices – spinning around, each boasting powerful winds on small timescales.

“Sometimes we see claims where just one or two houses in a block are completely destroyed, while others are almost untouched,” says Randy Neal, Senior Vice President (VP) at VeriClaim.

WIDENING THE WARNING GAPAll of this makes modelling losses from tornadoes tricky. And the fact that usable data is either absent – a dearth of information on temperature and moisture in the air above the surface has been blamed for the lack of understanding of what generates a tornado – or of mixed quality, doesn’t help. Says Orwig: “� e raw historical data is not very reliable, especially before 1990, when the Doppler Radar network was installed. After 1990 the data is better, but it is very di ̈ cult to determine long-term trends with only

30 / TORNADOES

28_ LMM7_Tornadoes_des11.indd 29 10/07/2014 13:08

According to the US Insurance Information Institute, most domestic and commercial property insurance policies cover damage by tornadoes, even in Tornado Alley. In the most vulnerable areas, however, the excesses can be quite high.

Tornadoes are typically accompanied by lightning, heavy hailstorms and fl ash fl ooding. So, on top of the obvious catastrophic property damage caused by tornadoes, motor and agriculture insurers also face large claims.

On average, one-fi fth of the annual losses from tornado-related weather incidents in the US are incurred on motor policies, as wind, hail and fl ash fl oods are covered as standard on comprehensive policies.

Cover for fi re and lightning is standard – although in the most strike-prone regions of Tornado Alley, hail is often treated as a named peril and limited to agreed values rather than full replacement cost, because of the frequency of occurrence.

Flood cover is usually excluded, but homeowners and small businesses can access cover under the National Flood Insurance Program, administered by the Federal Emergency Management Agency. This is under review following the passing of the Homeowner Flood Insurance Affordability Act of 2014.

Agriculture policies are split between multi-peril crop insurance (MPCI), for a farm’s overall crop yield, and hail insurance policies for specifi c fi elds or crops. Annual average losses under MCPI policies from 2001-10 were US$325m, with a further US$310m incurred on specifi c crop hail insurance policies.

20 years of accurate information.” It’s hoped that new data collection

methods will, in the future, throw up terabytes of game-changing nuggets. A research team from Oklahoma State University is, for example, developing drone swarms that will � y into storms to collect their vital statistics – from pressure and temperature, to humidity and wind speeds – and help isolate tornadoes’ unique ‘� ngerprint’.

And high-performance computing power will help crunch that data. � e National Oceanic and Atmospheric Administration is implementing Warn-On-Forecast, a prediction system that uses high-resolution models coupled with radar, satellite, and other storm-scale weather data to anticipate where a tornado will land with greater accuracy. It is hoped this will ultimately increase warning lead times to up to an hour, saving lives and property.

Meanwhile, humanitarian e� orts are already being bolstered by cutting-edge tools. Following the Moore tornado strike, aid organisation Team Rubicon used military-grade tech loaded onto Android smartphones to provide critical knowledge about and support in damaged areas in real-time, by dynamically distributing information to a central database.

TRENDS IN TORNADO ACTIVITYFor now, though, given the uncertainty over the quality of historic data, predictions are shrouded in caution. Most experts agree that, despite the huge losses in 2011 and 2013, and focusing only on the most intense events, the trend from the 1960s onwards seems to be very � at. “Many of the major incidents can be explained by natural climatic variations such as Paci� c oscillations and El Niño, which we know a� ects the intensity of thunderstorms and where they have the most impact,” says Dr Adam Lea, Research Fellow at the Department of Space and Climate Physics, University College London (UCL).

Experts are equally cautious when it comes to linking climate change with potential increases in tornado activity.According to Lloyd’s 2013 report, Tornadoes: A Rising Risk: “Tornadoes occur on the timescale of seconds

31

You can make a home more resilient to hurricanes, but it isn’t possible to do that in the case of tornadoes. � ey’re too unpredictable in terms of strength, direction and impactRANDY NEAL, SENIOR VICE PRESIDENT, VERICLAIM

breaking down the billWHAT’S COVERED AS STANDARD, WHAT ISN’T, AND WHY…

28_ LMM7_Tornadoes_des11.indd 30 10/07/2014 13:08

and minutes, and a space scale of fractions of a mile across. Climate trends can take many years, decades, or even millennia to be distinguished from natural variability.”

As a result, it says, “climate modelling is incapable of analysing the existence of climate-driven changes in frequency and intensity of small scale weather events.”

Geo� rey Saville, Atmospheric Hub Leader for the Willis Research Network, expects extremes of wet weather to get worse, but says predicting what that means for tornadoes is a lot harder. “We can see that in the future there is going to be more energy in the system and this could increase the frequency and severity of storms. But this could also be o� set by the general consensus that there will be less shear [vertical wind] in a warming world.”

EFFECTS OF URBAN SPRAWL� e forecast for the balance of 2014 is for a relatively quiet year, with only a 20% prospect of above average activity, according to Mark Ellinwood, Operational Meteorologist with MDA Earth Sat Weather – notwithstanding the series of tornadoes that hit the Midwest at the end of April.

� ese killed 20 people, 16 in the suburbs of Little Rock, Arkansas, caused widespread damage to property, and highlighted a key concern for authorities and insurers: urbanisation and population spread. “As urban areas expand and we see suburban sprawl, there will be more tornado damage. Even if we have a reduction in tornadoes, we will see increased damage and economic loss,”

says Ilan Kelman, Reader of Risk, Resilience and Global Health at the Institute of Risk and Disaster Reduction at UCL.

� is belief is echoed by Prasad Gunturi, Senior VP, Reinsurance, Willis Group. “If the 1999 Oklahoma tornado happened today, with that area’s expanded built footprint, you would see an increase in losses.”

With this increased risk, Willis is spearheading a move to address building standards and improve resilience. Says Gunturi: “Building codes don’t talk about tornado hazards. � ey are in place for coastal areas such as Florida and Louisiana, where hurricanes are the problem. Clearly life and safety is paramount when looking at tornadoes, rather than damage to property, but there is more that can be done on both counts.”

� e only buildings subject to resilience requirements in the states most vulnerable to tornadoes are nuclear installations, and they have to be built to withstand winds of over 200mph – far in excess of the strongest hurricane winds. Building domestic and commercial properties to those standards would be prohibitively expensive, especially as the chances of a particular building in Tornado Alley being hit in a given year are only one in 5,000 – and the probability of that being a tornado capable of causing signi£ cant damage is much lower still,

32 / TORNADOES

AUSTRALIA2013 was the worst year for some time, with several tornadoes hitting Victoria, New South Wales and Queensland during the November to April peak season. In the worst incident, seven tornadoes touched down, striking several small towns. The tornado that struck Tamleugh, Euroa and Swanpool on 21 March is believed to be the most powerful ever to hit the state of Victoria.

SOUTH AFRICAThere are frequent tornadoes in South Africa, many of which pass unrecorded and cause no damage as they occur in unpopulated areas. When they do hit centres of population, they can be devastating. In a series of strikes in December 1998 and January 1999, more than 50 people died and 750 were injured.

BANGLADESHThe deadliest tornado ever was the Daulatpur–Saturia tornado, which hit the Manikganj district on 26 April 1989. It killed an estimated 1,300 people and injured 12,000 more. It was unusually wide – about a mile – and had a path of 50 miles.