Homes for Californians in the New Century Challenges and Opportunities February 7, 2003 Presented by...

86

Homes for Homes for Californians in the Californians in the New Century New Century Challenges and Challenges and Opportunities Opportunities February 7, 2003 February 7, 2003 Presented by Henry Cisneros Presented by Henry Cisneros

-

Upload

helena-blake -

Category

Documents

-

view

215 -

download

1

Transcript of Homes for Californians in the New Century Challenges and Opportunities February 7, 2003 Presented by...

Homes for Homes for Californians in the Californians in the

New CenturyNew CenturyChallenges and Challenges and Opportunities Opportunities

February 7, 2003February 7, 2003

Presented by Henry Cisneros Presented by Henry Cisneros

Demographic Change in California

Population Distribution

Year TotalWhite /

Non-Latino LatinoAfrican

AmericanAmerican

IndianAsian-

American

1995262,82

0193,566 26,936 31,598 1,931 8,788

2000281,42

2194,553 35,306 34,658 2,476 10,243

2020 E

324,926

207,145 55,156 44,735 3,207 19,589

2050 E

403,686

212,990 98,228 59,239 4,405 37,589

Source: U.S. 2000 Census & U.S. Census Bureau Population Division, Population Projections of the U.S., Total Population by Race, Hispanic Origin, & Nativity

Population Projections for California

Year Department of Finance Census Bureau Preferred

1990 29,942 -

1995 32,063 31,589

1996 32,384 31,758

1997 32,957 31,925

1998 33,506 32,100

2000 34,653 34,441

2005 37,372 37,644

2010 39,958 41,373

2015 42,371 45,278

2020 45,449 49,285

2025 48,626 -

2030 51,869 -

2035 55,210 -

2040 58,731 -

Source: Public Policy Institute of California

In Thousands

California Population by Race / Ethnic Distribution

Source: Public Policy Institute of California

1995

Latino28%

Asian & Pacific

Islander10%

African American

7%American

Indian1%

White54%

DOF, 2025

Latino41%

Asian & Pacific

Islander15%

African American

6%

American Indian

1%

White37%

Population Projections by Race / Ethnicity

1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

White 17,180 17,422 17,731 17,902 17,969 18,123 18,216 18,222 18,141 18,005

Latino 9,101 10,689 12,301 13,964 15,643 17,778 20,085 22,547 25,199 28,091

Asian & Pacific Islander

3,338 3,999 4,684 5,314 5,815 6,474 7,128 7,786 8,441 9,092

African American

2,251 2,338 2,343 2,541 2,691 2,806 2,918 3,024 3,128 3,234

American Indian

193 206 222 237 253 266 279 290 300 309

Source: Public Policy Institute of California

In Thousands (DOF)

Minority Populations Are Young

25.7%

32.1%35.0%

38.7%

White Non-Latino Asian-American African-American Latino

% of population under 20

Source: Market Segment Research; Population Report, Middle Series, 1996

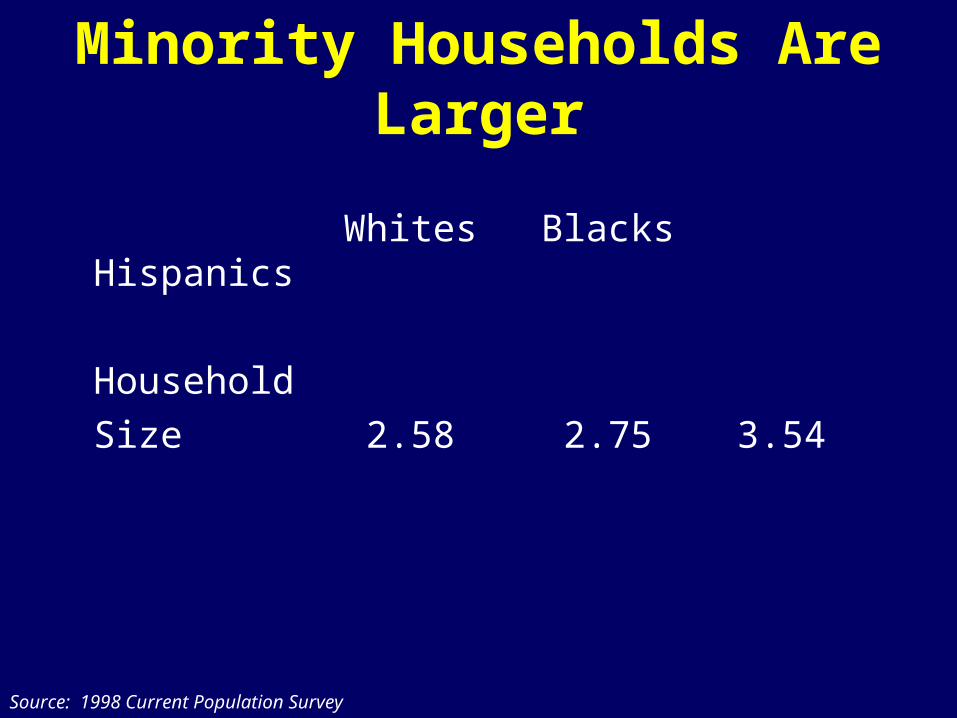

Minority Households Are Larger

Whites Blacks Hispanics

HouseholdSize 2.58 2.75 3.54

Source: 1998 Current Population Survey

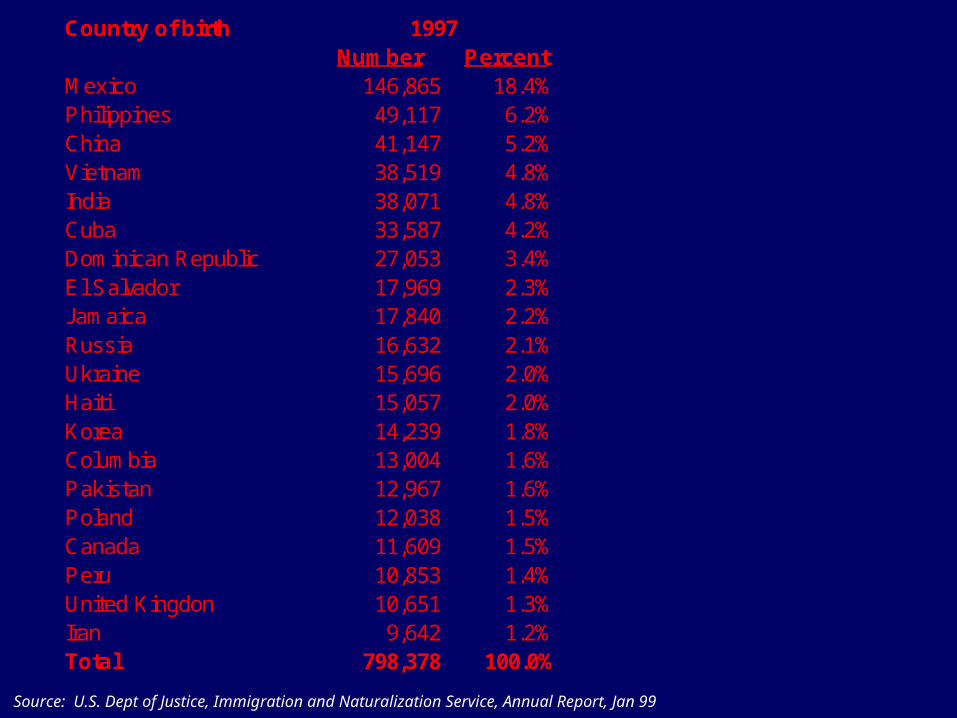

Country of birthNumber Percent

Mexico 146,865 18.4%Philippines 49,117 6.2%China 41,147 5.2%Vietnam 38,519 4.8%India 38,071 4.8%Cuba 33,587 4.2%Dominican Republic 27,053 3.4%El Salvador 17,969 2.3%Jamaica 17,840 2.2%Russia 16,632 2.1%Ukraine 15,696 2.0%Haiti 15,057 2.0%Korea 14,239 1.8%Columbia 13,004 1.6%Pakistan 12,967 1.6%Poland 12,038 1.5%Canada 11,609 1.5%Peru 10,853 1.4%United Kingdon 10,651 1.3%Iran 9,642 1.2%Total 798,378 100.0%

1997

Source: U.S. Dept of Justice, Immigration and Naturalization Service, Annual Report, Jan 99

Country of birthNumber Percent

Mexico 146,865 18.4%Philippines 49,117 6.2%China 41,147 5.2%Vietnam 38,519 4.8%India 38,071 4.8%Cuba 33,587 4.2%Dominican Republic 27,053 3.4%El Salvador 17,969 2.3%Jamaica 17,840 2.2%Russia 16,632 2.1%Ukraine 15,696 2.0%Haiti 15,057 2.0%Korea 14,239 1.8%Columbia 13,004 1.6%Pakistan 12,967 1.6%Poland 12,038 1.5%Canada 11,609 1.5%Peru 10,853 1.4%United Kingdon 10,651 1.3%Iran 9,642 1.2%Total 798,378 100.0%

1997

Source: U.S. Dept of Justice, Immigration and Naturalization Service, Annual Report, Jan 99

Over 249,000Over 249,000

--31%----31%--

come from come from

Spanish-Spanish-

speaking speaking

countriescountries

Country of birthNumber Percent

Mexico 146,865 18.4%Philippines 49,117 6.2%China 41,147 5.2%Vietnam 38,519 4.8%India 38,071 4.8%Cuba 33,587 4.2%Dominican Republic 27,053 3.4%El Salvador 17,969 2.3%Jamaica 17,840 2.2%Russia 16,632 2.1%Ukraine 15,696 2.0%Haiti 15,057 2.0%Korea 14,239 1.8%Columbia 13,004 1.6%Pakistan 12,967 1.6%Poland 12,038 1.5%Canada 11,609 1.5%Peru 10,853 1.4%United Kingdon 10,651 1.3%Iran 9,642 1.2%Total 798,378 100.0%

1997

Source: U.S. Dept of Justice, Immigration and Naturalization Service, Annual Report, Jan 99

Over 194,000Over 194,000

--24%----24%--

come from come from

AsianAsian

countriescountries

StatesNumber Percent Number Percent

Entire nation 798,378 11 Michigan 14,727 1.8%1 California 203,305 25.5% 12 Pennsylvania 14,553 1.8%2 New York 123,716 15.5% 13 Georgia 12,623 1.6%3 Florida 82,318 10.3% 14 Conecticut 9,528 1.2%4 Texas 57,897 7.3% 15 Arizona 8,632 1.1%5 New Jersey 41,184 5.2% 16 Minnesota 8,233 1.0%6 Illinois 38,128 4.8% 17 Ohio 8,189 1.0%7 Virginia 19,277 2.4% 18 Oregon 7,699 1.0%8 Maryland 19,090 2.4% 19 Colorado 7,506 0.9%9 Washington 18,656 2.3% 20 Hawaii 6,867 0.9%

10 Massachuestts 17,317 2.2% Total top 20 states 719,445 90.2%

1997 1997

Source: U.S. Dept of Justice, Immigration and Naturalization Service, Annual Report, Jan 99

Number Percent Number PercentAll Metropolitan Areas 798,378 13 Dallas, TX 11,061 1.4%

1 New York, NY 107,434 13.5% 14 Philadelphia, PA-NJ 10,858 1.4%2 Los Angeles-Long Beach, CA 62,314 7.8% 15 Newark, NJ 10,801 1.4%3 Miami, FL 45,707 5.7% 16 Seattle-Bellevue-Everett, WA 10,692 1.3%4 Chicago, IL 35,386 4.4% 17 Fort Lauderdale, FL 10,646 1.3%5 Washington, DC-MD-VA 31,444 3.9% 18 Detroit, MI 10,019 1.3%6 Orange County, CA 18,190 2.3% 19 Atlanta, GA 9,823 1.2%7 Houston, TX 17,439 2.2% 20 Bergan-Passaic, NJ 9,788 1.2%8 San Jose, CA 17,374 2.2% 21 Riverside-San Bernadino, CA 9,518 1.2%9 San Francisco, CA 16,892 2.1% 22 Nassau-Suffolk, NY 9,167 1.1%

10 Oakland, CA 15,723 2.0% 23 Sacramento, CA 7,654 1.0%11 San Diego, CA 14,758 1.8% 24 Jersey City, NJ 7,529 0.9%12 Boston-Lawrence, MA 13,937 1.7% 25 Minneapolis-St. Paul, MN-WI 6,859 0.9%

1997 1997

Source: U.S. Dept of Justice, Immigration and Naturalization Service, Annual Report, Jan 99

Fact: Minority Families Have More Workers Per Household

25.6%

52.5%

13.5% 14.0%19.4%

15.3%

27.2%

U.S. BornLatino

Foreign-BornLatino

U.S. BornWhite

Foreign-BornWhite

African-American

U.S. BornAsian

Foreign-BornAsian

Households with Three or More Workers, 1990The Middle Class - 5 County Area

Source: Pepperdine University Institute for Public Policy “The Emerging Latino Middle Class” 1997

Growth of the Middle Class: 1989-1999

Source: U.S. Census Bureau

29.5% 32.3%

72.3%64.6%

Total Households

African American

Households

Hispanic Households

Asian Households

Middle Class Defined:

1989: $23,663 - $36,2011999: $33,001 - $52,174

Projected Owner Occupied Household Growth in Millions 2000 - 2010

African Asian/ Total Total American Hispanic Other

Minority

10.9 m. 1.8 m. 2.2 m. 1.0 m. 5.0 m.

Source: 1998 Current Population Survey

There Is Still a Significant Gap in the Rate of Home

Ownership74.4%

48.7% 48.8%

White Black Hispanic

Home Ownership Rate: 4th Quarter - 2001

Source: Department of Housing and Urban Development – Office of Policy Development & Research, US Housing Market Conditions, 4th Quarter 2001

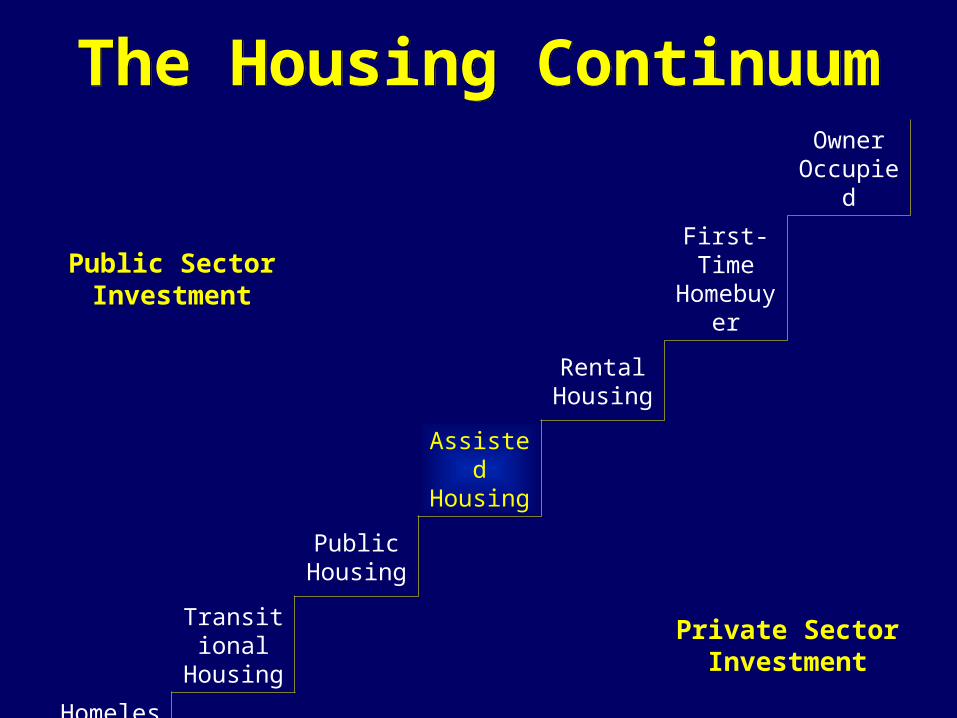

The Housing ContinuumThe Housing ContinuumOwner

Occupied

Public Sector Investment

First-Time Homebuyer

Rental Housing

Assisted Housing

Public Housing

Transitional Housing

Private Sector Investment

Homeless Shelter

The Housing ContinuumThe Housing ContinuumOwner

Occupied

Public Sector Investment

First-Time Homebuyer

Rental Housing

Assisted Housing

Public Housing

Transitional Housing

Private Sector Investment

Homeless Shelter

•More homeless facilities are needed and more beds at existing sites.

•Concerted efforts are required to bring homeless people in from the streets to safe, clean, and well-managed emergency shelters.

• Interventions must extend from street outreach to mental health and substance abuse programs.

•More homeless facilities are needed and more beds at existing sites.

•Concerted efforts are required to bring homeless people in from the streets to safe, clean, and well-managed emergency shelters.

• Interventions must extend from street outreach to mental health and substance abuse programs.

The Housing ContinuumThe Housing ContinuumOwner

Occupied

Public Sector Investment

First-Time Homebuyer

Rental Housing

Assisted Housing

Public Housing

Transitional Housing

Private Sector Investment

Homeless Shelter

More units are needed to provide decent apartments for persons with AIDS, persons with medical and emotional disabilities, and

mothers with children.

That means at least 150,000 units of suitable housing over ten

years, or 15,000 incremental units of supportive housing each

year.

More units are needed to provide decent apartments for persons with AIDS, persons with medical and emotional disabilities, and

mothers with children.

That means at least 150,000 units of suitable housing over ten

years, or 15,000 incremental units of supportive housing each

year.

The Housing ContinuumThe Housing ContinuumOwner

Occupied

Public Sector Investment

First-Time Homebuyer

Rental Housing

Assisted Housing

Public Housing

Transitional Housing

Private Sector Investment

Homeless Shelter

Continue large-scale renovation of deteriorated, overly dense public housing through full funding

of HOPE VI.

Reduce concentrations of poverty by creating smaller-scaled mixed-income developments matched to Section 8 and other programs, to

open housing opportunities in neighborhoods with stronger

economic prospects.

Continue large-scale renovation of deteriorated, overly dense public housing through full funding

of HOPE VI.

Reduce concentrations of poverty by creating smaller-scaled mixed-income developments matched to Section 8 and other programs, to

open housing opportunities in neighborhoods with stronger

economic prospects.

Horner NeighborhoodHorner NeighborhoodHorner NeighborhoodHorner Neighborhood

Old

New

Atlanta, Georgia: Perry Atlanta, Georgia: Perry HomesHomes

Atlanta, Georgia: Centennial Atlanta, Georgia: Centennial PlacePlace

Harbor PointHarbor PointHarbor PointHarbor Point

Norfolk: Diggs TownNorfolk: Diggs TownNorfolk: Diggs TownNorfolk: Diggs Town

The Housing ContinuumThe Housing ContinuumOwner

Occupied

Public Sector Investment

First-Time Homebuyer

Rental Housing

Assisted Housing

Public Housing

Transitional Housing

Private Sector Investment

Homeless Shelter

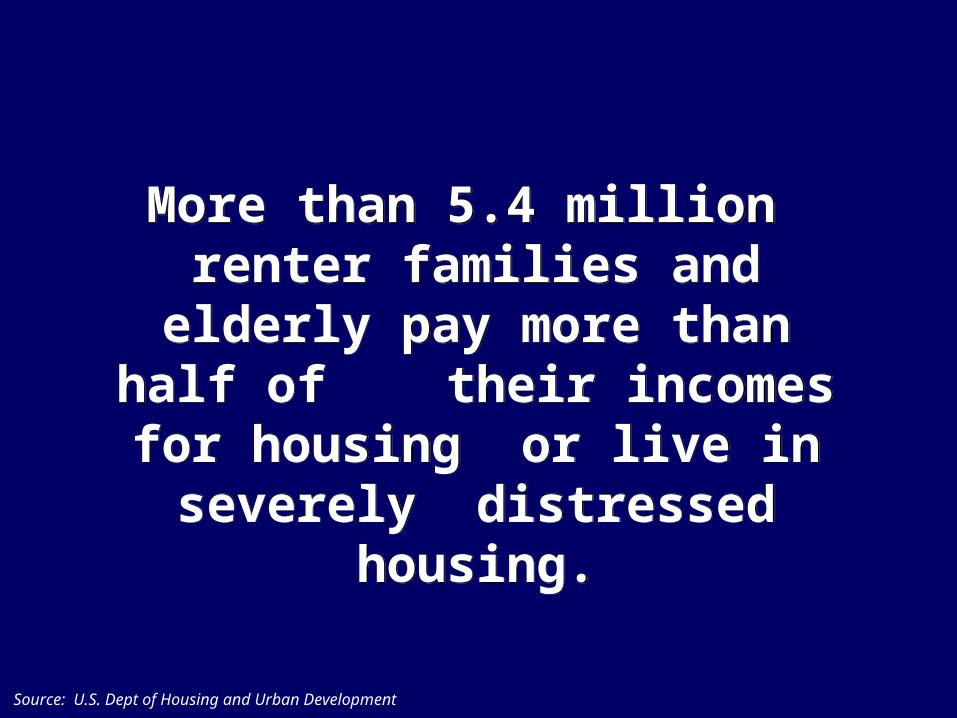

More than 5.4 million renter families and

elderly pay more than half of their incomes for

housing or live in severely distressed

housing.

More than 5.4 million renter families and

elderly pay more than half of their incomes for

housing or live in severely distressed

housing.

Source: U.S. Dept of Housing and Urban Development

57% of all renters – or 20 million households – earn less than $30,000 annually.

For them, affordable rent is $750/month or less.

Median asking rent for a new apartment is $920/month.

57% of all renters – or 20 million households – earn less than $30,000 annually.

For them, affordable rent is $750/month or less.

Median asking rent for a new apartment is $920/month.

In order to build units for the 6.4 million households with severe affordability problems, provide

capital subsidies for the production of units for occupancy

by extremely low-income households.

To preserve the current stock of subsidized rental housing, enact exit tax relief via a preservation

tax incentive to transfer properties to preservation entities.

In order to build units for the 6.4 million households with severe affordability problems, provide

capital subsidies for the production of units for occupancy

by extremely low-income households.

To preserve the current stock of subsidized rental housing, enact exit tax relief via a preservation

tax incentive to transfer properties to preservation entities.

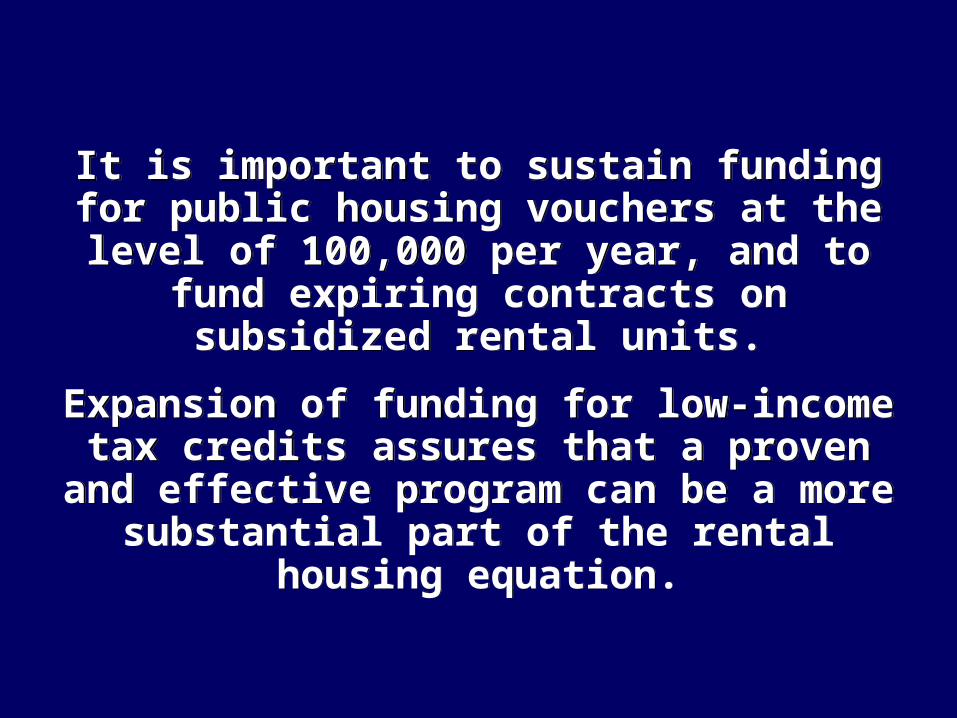

It is important to sustain funding for public housing vouchers at the level of 100,000 per year, and to

fund expiring contracts on subsidized rental units.

Expansion of funding for low-income tax credits assures that a proven and effective program can be a

more substantial part of the rental housing equation.

It is important to sustain funding for public housing vouchers at the level of 100,000 per year, and to

fund expiring contracts on subsidized rental units.

Expansion of funding for low-income tax credits assures that a proven and effective program can be a

more substantial part of the rental housing equation.

Specialized rental housing, such as the Senior 202

Program, warrants expansion.

The national network of highly capable non-profit housing providers is an essential extension of

Federal capability to address specific demographic needs.

Specialized rental housing, such as the Senior 202

Program, warrants expansion.

The national network of highly capable non-profit housing providers is an essential extension of

Federal capability to address specific demographic needs.

The Housing ContinuumThe Housing ContinuumOwner

Occupied

Public Sector Investment

First-Time Homebuyer

Rental Housing

Assisted Housing

Public Housing

Transitional Housing

Private Sector Investment

Homeless Shelter

Affordability Pressures Are Mounting as the Moderate-Income

Rental Supply Plummets

Source: HUD tabulations of the American Housing Survey, prepared for the Millennial Housing Commission Report

Change in Affordable Units 1985-99, in Millions

Note: HUD income limits are adjusted for inflation and real income growth for both 1985 and 1999.

Under 30% of AMI

30-50% of AMI

50-60% of AMI

60-80% of AMI

80-100% of AMI

100-120% of AMI

Over 120% of AMI

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

ExtremelyLow

Very Low Low HighModerate

A family with one full-time worker earning the

minimum wage cannot afford the local fair-market

rent for a two-bedroom apartment anywhere in the

country.

A family with one full-time worker earning the

minimum wage cannot afford the local fair-market

rent for a two-bedroom apartment anywhere in the

country.

In 24 states, households with

two full-time minimum wage earners lack the

income to cover fair-market rents on such a unit without

exceeding the “30% of income” threshold which

defines affordability.

In 24 states, households with

two full-time minimum wage earners lack the

income to cover fair-market rents on such a unit without

exceeding the “30% of income” threshold which

defines affordability.

Multifamily construction slowed in the 1990s despite

a population increase.

1970s – 5 million units

1990s – 2.5 million units

Multifamily construction slowed in the 1990s despite

a population increase.

1970s – 5 million units

1990s – 2.5 million units

Attract private capital to the production of mixed-

income, multi-family rental housing through state bond programs.

Attract private capital to the production of mixed-

income, multi-family rental housing through state bond programs.

The Housing ContinuumThe Housing ContinuumOwner

Occupied

Public Sector Investment

First-Time Homebuyer

Rental Housing

Assisted Housing

Public Housing

Transitional Housing

Private Sector Investment

Homeless Shelter

Allocate a flexible new tax credit to stimulate

the production of affordable units for

homeownership.

Allocate a flexible new tax credit to stimulate

the production of affordable units for

homeownership.

The Housing ContinuumThe Housing ContinuumOwner

Occupied

Public Sector Investment

First-Time Homebuyer

Rental Housing

Assisted Housing

Public Housing

Transitional Housing

Private Sector Investment

Homeless Shelter

Projected Homeownership Rate: 2000 - 2010

2000 2010Projected Change

U.S. Total 66.4 % 69.1 % + 2.7 %

African American

46.2 % 51.1 % + 4.9 %

Hispanic 44.5 % 49.1 % + 4.6 %

Asian 52.6 % 55.9 % + 3.3 %

Source: U.S. 2000 Census

Fannie Mae and Freddie Mac have set homeownership goals

for target populations.

Fannie Mae and Freddie Mac have set homeownership goals

for target populations.

• Minorities• New Immigrants• Female heads of household• Young households• Families in redevelopment areas• Families in rural areas

For example, Fannie Mae’s American Dream Commitment targets:

For example, Fannie Mae’s American Dream Commitment targets:

AFFORDABILITY

AND HOMEOWNERSHIP

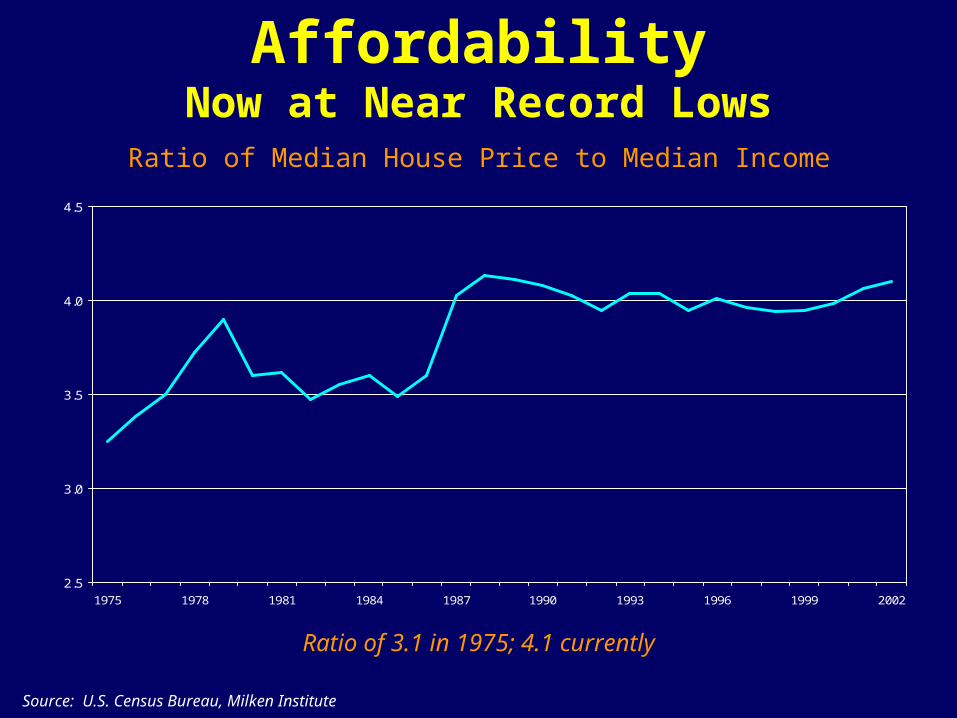

AffordabilityNow at Near Record Lows

2.5

3.0

3.5

4.0

4.5

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002

Source: U.S. Census Bureau, Milken Institute

Ratio of Median House Price to Median Income

Ratio of 3.1 in 1975; 4.1 currently

Affordability: Three Dimensions

• Mortgage Interest Rates

• Income

• Home Prices

Mortgage Interest Rates

The decline from 8.05% in June, 2000 to 6.5% currently gives the median income household an 18% increase in its purchasing power.

Source: Federal Housing Finance Board (Bloomberg)

0

2

4

6

8

10

12

14

16

18

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002

National Average 30 Year Conventional Fixed Rate Home Mortgage

Household Income

Over the last 25 years, incomes have increased steadily.

0

50

100

150

200

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002

Median Household Income

Source: U.S. Census Bureau, Milken Institute.

Thousa

nds

of

$

Household Income vs. Home Prices

But in that time period, incomes have grown slower than home prices. Median home prices increased at an average annual rate of 5.9 percent.

When home prices rise faster than incomes, affordability suffers.

0

50

100

150

200

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002

Median House Price Median Household Income

Source: U.S. Census Bureau, Milken Institute.

Thousa

nds

of

$

Home Prices

The price of homes is a function of supply and demand: the problems of producing homes constrain the supply of new housing units.

Source: U.S. Census Bureau

500

1,000

1,500

2,000

2,500

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002New

Pri

vate

ly O

wned H

ousi

ng U

nit

s (I

n T

housa

nds)

Recommended Ratio:Recommended Ratio:1 new housing unit

for every 1.5 jobs created

In Fact:In Fact:California: 1 to 3.6Los Angeles: 1 to 5San Jose: 1 to 7.8

Affordability of Housing by Minorities

Median home price, June 2002:$182,600

Source: Bloomberg, U.S. Census Bureau, Milken Institute

How much Home can the median

household income support?

10th Percentil

e30th

Percentile50th

Percentile70th

Percentile90th

Percentile

U.S. Average $ 49,438 $ 122,912 $ 205,521 $ 318,894 $ 687,091

African Americans

$ 30,954 $ 83,182 $ 147,345 $ 231,385 $ 479,081

Hispanics $ 43,665 $ 100,638 $ 161,977 $ 244,771 $ 477,752

Home Price is calculated assuming a 20% down payment on a 30 Year Fixed Rate Mortgage with payments equal to 30% of gross annual household.

CityOccupatio

nAverage Income

Median Home Price

Qualifying Income

Downtown Los

AngelesTeacher $ 38,570 $ 333,250 $ 111,083

Yorba Linda

(Orange County)

Firefighter $ 42,300 $ 338,500 $ 112,883

Palo AltoPolice

Detective$ 62,230 $ 815,000 $ 270,667

San JoseRegistered

Nurse$ 56,650 $ 430,000 $ 143,333

Home Prices are Beyond the Reach of California’s Middle-

Class

Home Prices are Beyond the Reach of California’s Middle-

Class

Affordability

• Land Cost

• Public Role

• Fiscal Issues

• Financial Institutions

• Gentrification

• Homebuyers Assistance

• Local Government Homeownership Priorities

Work with local governments who declare homeownership a priority

to review land use policies and fiscal structure for middle class

and entry level affordability.

Consider incentives to encourage states and local governments to create housing trust funds with their own funds and with private

resources, in order to supplement Federal programs for

homeownership.

Work with local governments who declare homeownership a priority

to review land use policies and fiscal structure for middle class

and entry level affordability.

Consider incentives to encourage states and local governments to create housing trust funds with their own funds and with private

resources, in order to supplement Federal programs for

homeownership.

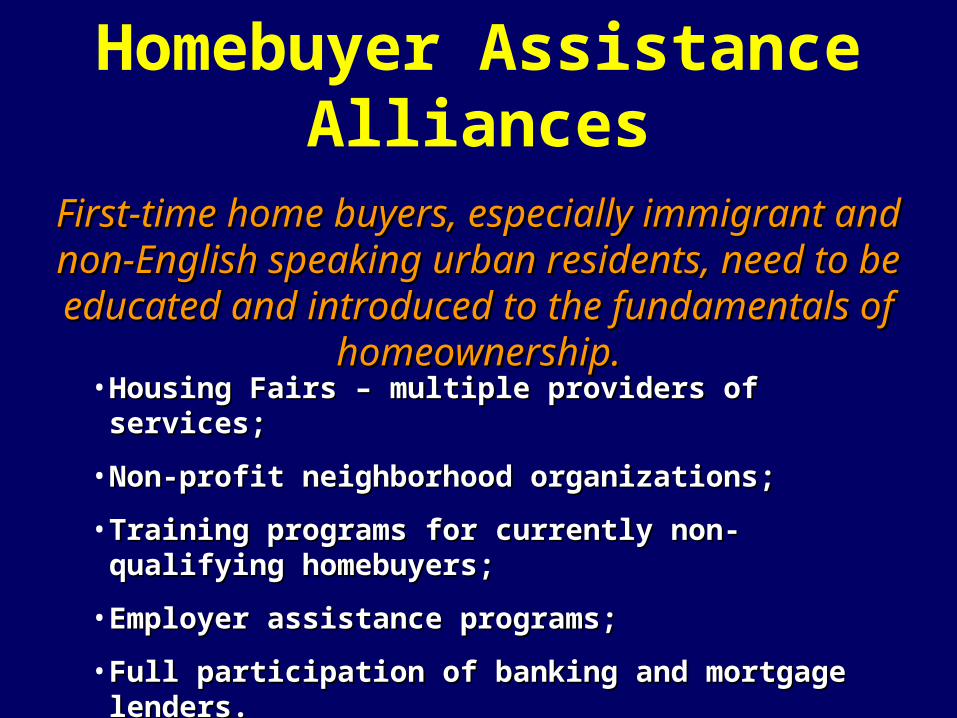

First-time home buyers, especially immigrant and non-First-time home buyers, especially immigrant and non-English speaking urban residents, need to be educated English speaking urban residents, need to be educated and introduced to the fundamentals of homeownership.and introduced to the fundamentals of homeownership.

• Housing Fairs – multiple providers of services;Housing Fairs – multiple providers of services;

• Non-profit neighborhood organizations;Non-profit neighborhood organizations;

• Training programs for currently non-qualifying homebuyers;Training programs for currently non-qualifying homebuyers;

• Employer assistance programs;Employer assistance programs;

• Full participation of banking and mortgage lenders.Full participation of banking and mortgage lenders.

Homebuyer Assistance Alliances

•Professional & Business Groups

•In Cooperation With Employers as Employee Benefits

•Immigrant Self-help Advocacy Groups

•Community-based Organizations

•Church Communities

•Person-to-person Explanations

Homebuyer Assistance Alliances

Targeted Mortgage Products

• First-time Homebuyer Mortgage Assistance• Down Payment Assistance;• Zero Down-Payment with Fannie Mae and KB Mortgage

Company for Teachers, Nurses, Policemen, & Firefighters;• “1% down-payment” and low-interest loans sponsored by

Fannie Mae or other financial institutions;• Bond financing to create low interest loans for

moderately-low income families.• New ACV initiated and targeted products …

SPECIAL LOAN PROGRAMSSPECIAL LOAN PROGRAMS::

The Key to Affordable Urban Home The Key to Affordable Urban Home OwnershipOwnership

The Key to Affordable Urban Home The Key to Affordable Urban Home OwnershipOwnership

An Exclusive Financing Option Through Fannie Mae & KB Mortgage Company

- Firefighters

- Healthcare Professionals

- Teachers

- Police Officers

• Zero Down

• Zero Closing Cost

• Targets:

Targeted Mortgage Products

Targeted Mortgage Products

URBAN PROGRESS

AND HOMEOWNERSHIP

Homeownership

•Traditional Infill Approach

•Large Sites:– Military Facilities, i.e., Mather AFB

– Brownfields

– Large tracts,

KB Home at Mather AFBSacramento, CA

1,716 – 4,028 sq. ft.$239,500 – $344,000

Urban RealitiesUrban Realities

• Land cost can be substantially higher than regional suburban alternatives; land configuration and previous uses increase costs

• Smaller & difficult to develop sitesSmaller & difficult to develop sites

• Costs and entitlement processes dictate more expensive and/or higher density products

•Social conditions can be as complex as the physical sites

•Older, poorer and more diverse educational institutions

Urban RealitiesUrban Realities

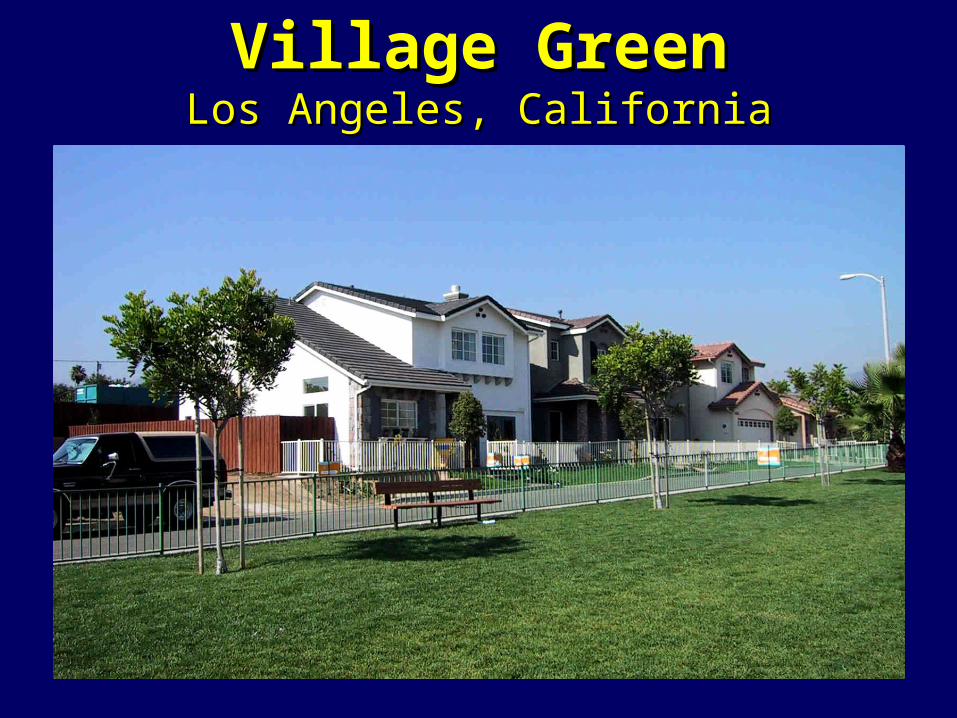

Yet, More American Homeowners Are Seeking

Central Locations

Yet, More American Homeowners Are Seeking

Central Locations• To Avoid Congestion, Traffic, and Long Commutes

• To Enjoy a Metropolitan Lifestyle With Downtown Amenities

• To Be Near Employment Centers

• To Be Near Familiar Neighborhoods and Close to Family and Community Roots

• To Participate in Civic Involvements and Greater Citizen Interactions

• To Have a Distinctive “Village Within the City” Experience with New Home Comforts and Technologies

Village GreenVillage GreenLos Angeles, CaliforniaLos Angeles, California

Targeted Consumers Want

Location and Convenience

Targeted Consumers Want

Location and Convenience • Young Professionals

• Empty nesters and retirees• First-time homeowners with

young families• Immigrants• Minority homeowners• Working families• Multigenerational

households

Many City & County Governments Have

Established the Construction of Homes in Central Areas as a Priority

Many City & County Governments Have

Established the Construction of Homes in Central Areas as a Priority

GOVERNMENTS CAN BE HELPFUL:• Identifying Sites in Priority Areas

• Helping Assemble Complex Sites

• Assuring the Adequacy of Needed Utilities, Transportation, and Other Public Infrastructure

• Working to Meet Local “Affordability” Objectives

• Expediting the Approval and Entitlement Process

• Working with Neighborhood and Community Leaders

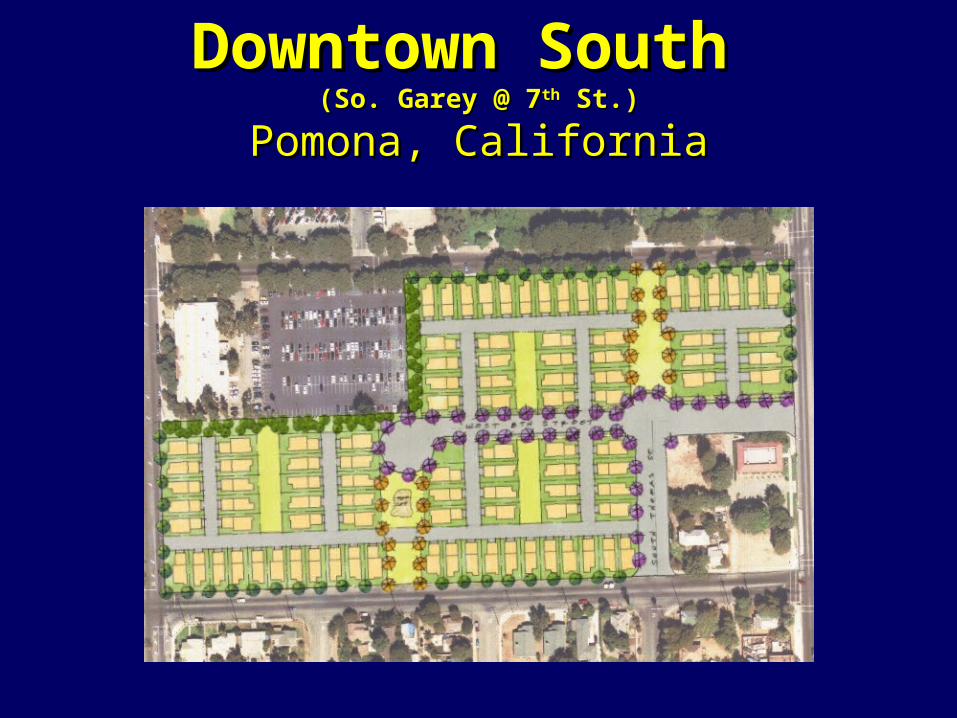

Downtown South Downtown South (So. Garey @ 7(So. Garey @ 7thth St.) St.)

Pomona, CaliforniaPomona, California

Downtown South Downtown South (So. Garey @ 7(So. Garey @ 7thth St.) St.)

Pomona, CaliforniaPomona, California

Downtown South Downtown South (So. Garey @ 7(So. Garey @ 7thth St.) St.)

Pomona, CaliforniaPomona, California

• School districtsSchool districts• Neighborhood leadersNeighborhood leaders• Local businessLocal business• PolicePolice• Community collegesCommunity colleges• Corporate partners – i.e. telecom/digitalCorporate partners – i.e. telecom/digital• Financial institutions - make Financial institutions - make

homeownership a realityhomeownership a reality

Strategic Partnerships:Strategic Partnerships:The Key to Urban The Key to Urban

ProjectsProjects

Expand the concept of empowerment or enterprise zones to create “homeownership zones.”

Encourage local governments to Encourage local governments to assemble sites, clean up assemble sites, clean up

brownfields, create land banks, brownfields, create land banks, rehabilitate properties, reconstruct rehabilitate properties, reconstruct infrastructure, and prepare land for infrastructure, and prepare land for

large-scale infill neighborhoods.large-scale infill neighborhoods.

Expand the concept of empowerment or enterprise zones to create “homeownership zones.”

Encourage local governments to Encourage local governments to assemble sites, clean up assemble sites, clean up

brownfields, create land banks, brownfields, create land banks, rehabilitate properties, reconstruct rehabilitate properties, reconstruct infrastructure, and prepare land for infrastructure, and prepare land for

large-scale infill neighborhoods.large-scale infill neighborhoods.

1. The availability of quality, affordable rental units is important to creating a pipeline of future homeowners:

1. The availability of quality, affordable rental units is important to creating a pipeline of future homeowners:

Concluding Points

- Preserve and expand the subsidized stock

- Expand the availability of affordable market units

- Preserve and expand the subsidized stock

- Expand the availability of affordable market units

2. In order to enhance affordability, it is critical to expand the supply of affordable for-sale homes:

2. In order to enhance affordability, it is critical to expand the supply of affordable for-sale homes:- National Policy: Homeownership

Tax Credits

- Local Governments: Identify and assist in assembly of sites

- Private Builders: Target median price and below

- National Policy: Homeownership Tax Credits

- Local Governments: Identify and assist in assembly of sites

- Private Builders: Target median price and below

3. Mortgage products must be addressed to high growth homeownership markets:

3. Mortgage products must be addressed to high growth homeownership markets:

- Effective outreach to minority populations

- Design of targeted financial products

- Give core business priority to the new demographics of homeownership

- Effective outreach to minority populations

- Design of targeted financial products

- Give core business priority to the new demographics of homeownership