HLNG 2014 Q4 Presentation · LNG bonds GasLog Golar LNG Partners HLNG Teekay LNG 17 Note: Arctic...

23

Höegh LNG – The floating LNG services provider 3Q 2016 Presentation of financial results 17 November 2016

Transcript of HLNG 2014 Q4 Presentation · LNG bonds GasLog Golar LNG Partners HLNG Teekay LNG 17 Note: Arctic...

Höegh LNG – The floating LNG services provider

3Q 2016 Presentation of financial results

17 November 2016

Forward looking statements

2

This presentation contains forward-looking statements which reflects management’s current expectations, estimates and projections about

its operations. All statements, other than statements of historical facts, that address activities and events that will, should, could or may

occur in the future are forward-looking statements. Words such as “may,” “could,” “should,” “would,” “expect,” “plan,” “anticipate,” “intend,”

“forecast,” “believe,” “estimate,” “predict,” “propose,” “potential,” “continue” or the negative of these terms and similar expressions are

intended to identify such forward-looking statements. These statements are not guarantees of future performance and are subject to

certain risks, uncertainties and other factors, some of which are beyond our control and are difficult to predict. Therefore, actual outcomes

and results may differ materially from what is expressed or forecasted in such forward-looking statements. You should not place undue

reliance on these forward-looking statements, which speak only as of the date of this presentation. Unless legally required, Höegh LNG

undertakes no obligation to update publicly any forward-looking statements whether as a result of new information, future events or

otherwise.

Among the important factors that could cause actual results to differ materially from those in the forward-looking statements are: changes

in LNG transportation and regasification market trends; changes in the supply and demand for LNG; changes in trading patterns; changes

in applicable maintenance and regulatory standards; political events affecting production and consumption of LNG and Höegh LNG’s

ability to operate and control its vessels; change in the financial stability of clients of the Company; Höegh LNG’s ability to win upcoming

tenders and securing employment for the FSRUs on order; changes in Höegh LNG’s ability to convert LNG carriers to FSRUs including

the cost and time of completing such conversions; changes in Höegh LNG’s ability to complete and deliver projects awarded; increases in

the Company’s cost base; changes in the availability of vessels to purchase; failure by yards to comply with delivery schedules; changes

to vessels’ useful lives; changes in the ability of Höegh LNG to obtain additional financing, in particular, currently, in connection with the

turmoil in financial markets; the success in achieving commercial success for the projects being developed by the Company; changes in

applicable regulations and laws; and unpredictable or unknown factors herein also could have material adverse effects on forward-looking

statements.

Höegh LNG Holdings - Agenda for presentation of 3Q 2016 financial results

3

Sveinung J.S. Støhle

President & CEO

Highlights / Markets / Summary

Appendix

Steffen Føreid

CFO

Financials

Dedededw

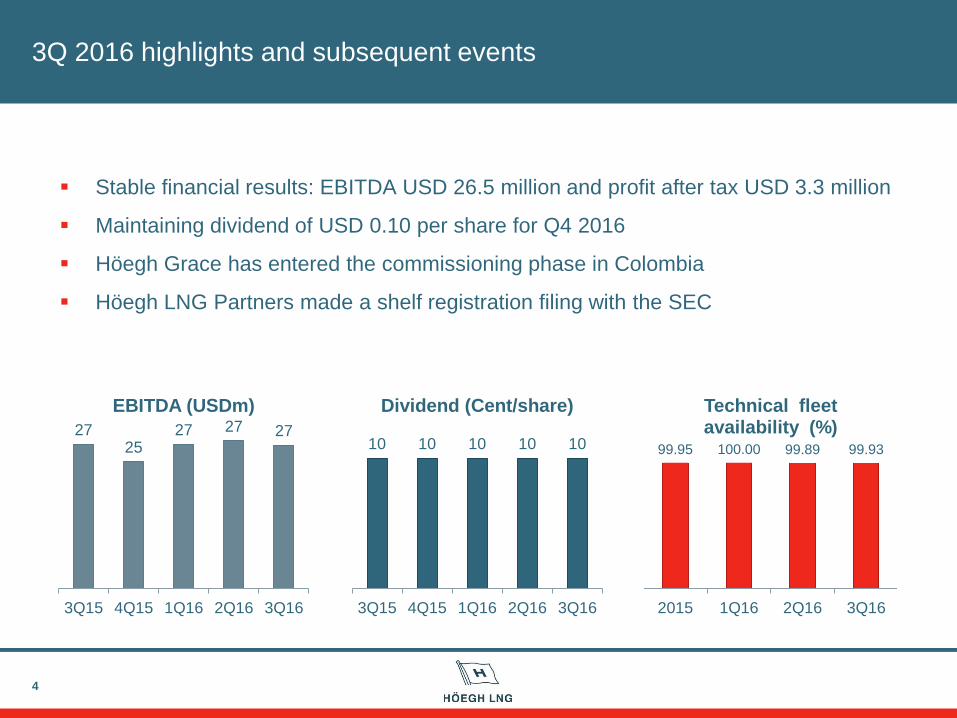

3Q 2016 highlights and subsequent events

Stable financial results: EBITDA USD 26.5 million and profit after tax USD 3.3 million

Maintaining dividend of USD 0.10 per share for Q4 2016

Höegh Grace has entered the commissioning phase in Colombia

Höegh LNG Partners made a shelf registration filing with the SEC

4

27 25

27 27 27

3Q15 4Q15 1Q16 2Q16 3Q16

EBITDA (USDm)

10 10 10 10 10

3Q15 4Q15 1Q16 2Q16 3Q16

Dividend (Cent/share)

99.95 100.00 99.89 99.93

2015 1Q16 2Q16 3Q16

Technical fleet availability (%)

Short/medium term focus

5

Operations

Project

execution

Commercial

Financial

To operate all FSRUs and LNGCs according to contract

Maintain ~100% technical fleet availability

Complete SPEC/Colombia commissioning for start-up early

December 2016

Construct and deliver FSRU#8 according to Penco LNG contract

Secure long-term contracts for:

FSRU#7 (March 2017 delivery)

FSRU Conversion project (end 2017 delivery)

Newbuilding Program ( 2019 1st delivery)

Refinance the first bond (HLNG01)

Secure debt financing for FSRU#8

Drop-down Höegh Grace to HMLP

Strategic initiatives

6

FSRU

newbuilding

tender

(FSRU#9+)

Conversion

HLNG has received very competitive terms reflecting

current shipyard orderbooks

Given the strong FSRU market, HLNG is considering to

opportunistically improve its leading position in the

FSRU market

The FSRU Conversion Project is on schedule with all

major components; (i) selection of engineering provider,

(ii) ordering of critical equipment, (iii) selection of

conversion yard, (iv) purchase of LNGC, for a planned

completion end 2017

Höegh Grace/Colombia update

7

Project on

schedule

Start-up is

a value

generating

trigger

Received commissioning cargo

Entered the commissioning phase

Commercial start-up of 20-year

contract early December

Increasing EBITDA by

approximately USD 40 million

Next planned drop-down to HMLP

Strategic

rationale

for SPEC

LNG needed to meet increasing

demand for electricity in Colombia

Ensures security of supply during

periods of drought

Back-up for

hydro

New gas fired

generation

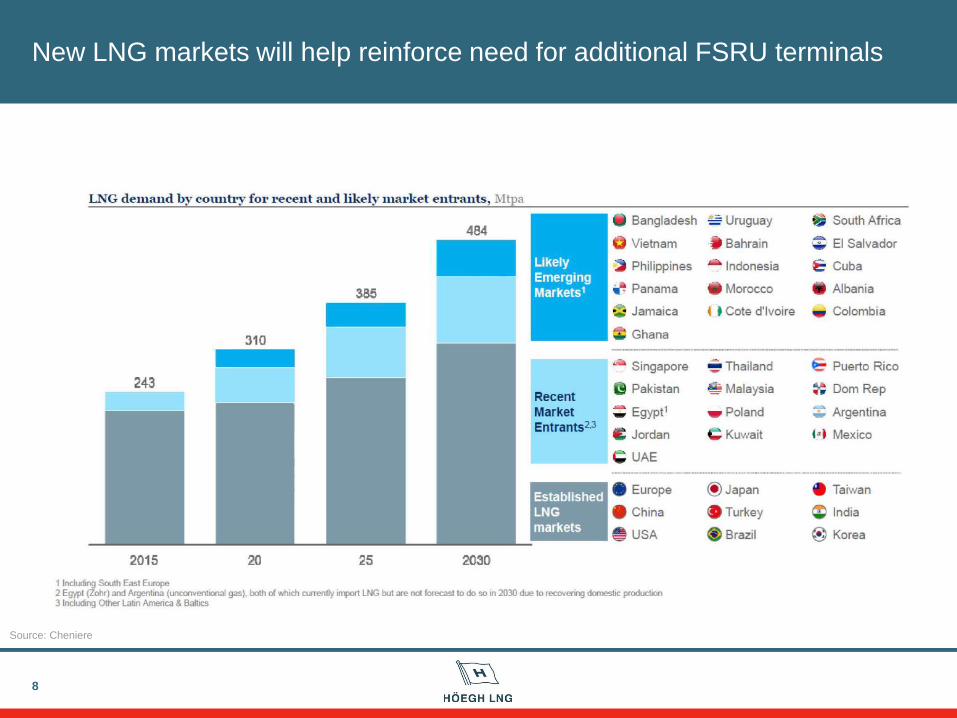

New LNG markets will help reinforce need for additional FSRU terminals

8

Source: Cheniere

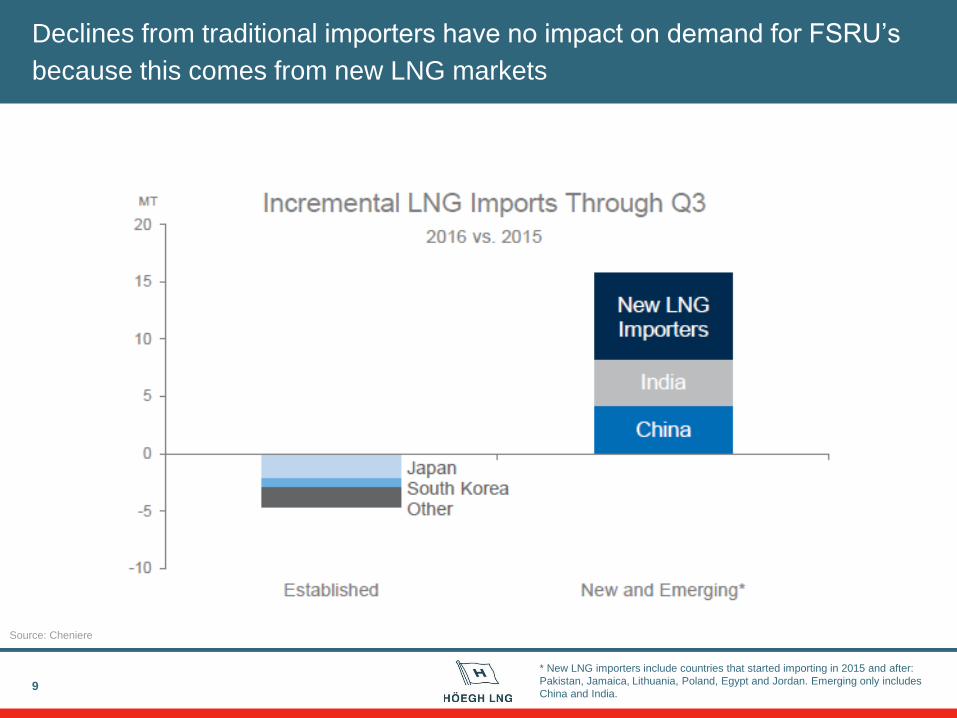

Declines from traditional importers have no impact on demand for FSRU’s

because this comes from new LNG markets

9

Source: Cheniere

* New LNG importers include countries that started importing in 2015 and after:

Pakistan, Jamaica, Lithuania, Poland, Egypt and Jordan. Emerging only includes

China and India.

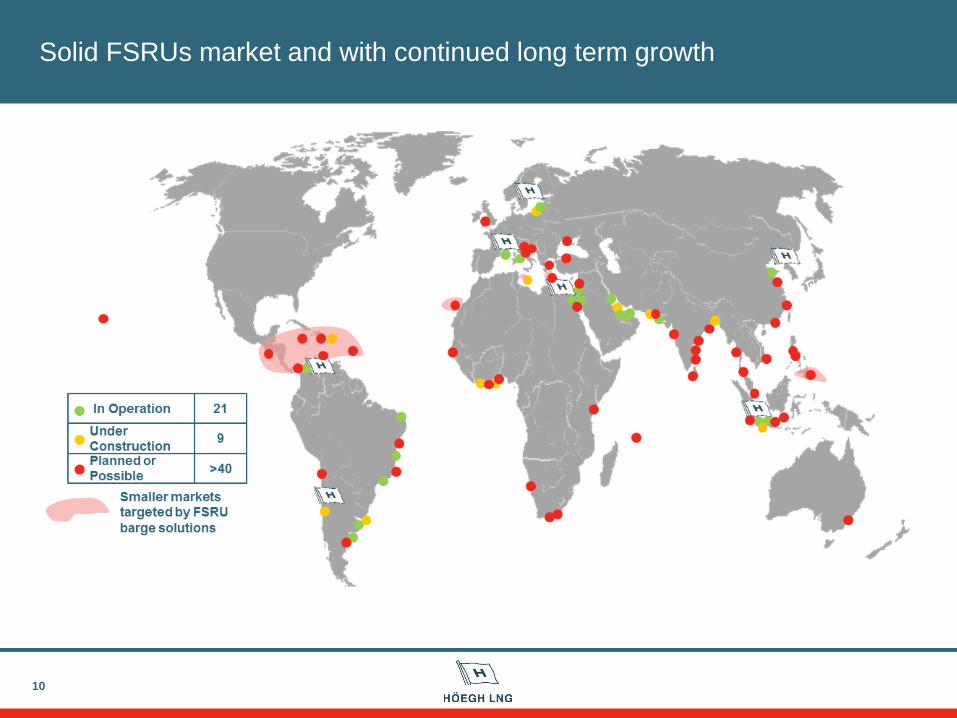

Solid FSRUs market and with continued long term growth

10

Stable competitive landscape

2011 2012 2013 2014 2015 2016

BW Gas

Excelerate

Golar LNG

11

Long-term FSRU contract award1

1 Do not include cancelled projects, contract renewals and sublets.

12

Höegh Grace in operation for commercial start in Colombia early December

Very competitive terms received for next round of FSRU newbuilding order(s)

Summary

Maintaining dividend payment of USD 0.1 per share for 4Q 2016

Continued steady operating performance – EBITDA of USD 26.5 million

Höegh LNG Holdings - Agenda for presentation of 3Q 2016 financial results

13

Sveinung J.S. Støhle

President & CEO

Highlights / Markets / Summary

Appendix

Steffen Føreid

CFO

Financials

Dedededw

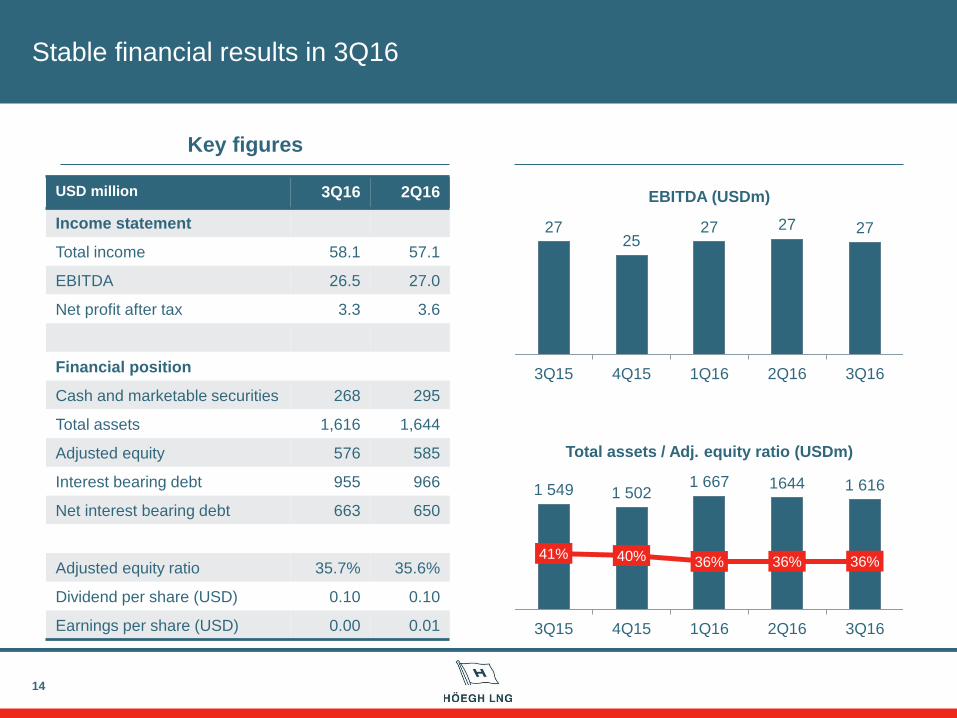

Stable financial results in 3Q16

14

USD million 3Q16 2Q16

Income statement

Total income 58.1 57.1

EBITDA 26.5 27.0

Net profit after tax 3.3 3.6

Financial position

Cash and marketable securities 268 295

Total assets 1,616 1,644

Adjusted equity 576 585

Interest bearing debt 955 966

Net interest bearing debt 663 650

Adjusted equity ratio 35.7% 35.6%

Dividend per share (USD) 0.10 0.10

Earnings per share (USD) 0.00 0.01

Key figures

27 25

27 27 27

3Q15 4Q15 1Q16 2Q16 3Q16

EBITDA (USDm)

1 549 1 502 1 667 1644 1 616

41% 40% 36% 36% 36%

3Q15 4Q15 1Q16 2Q16 3Q16

Total assets / Adj. equity ratio (USDm)

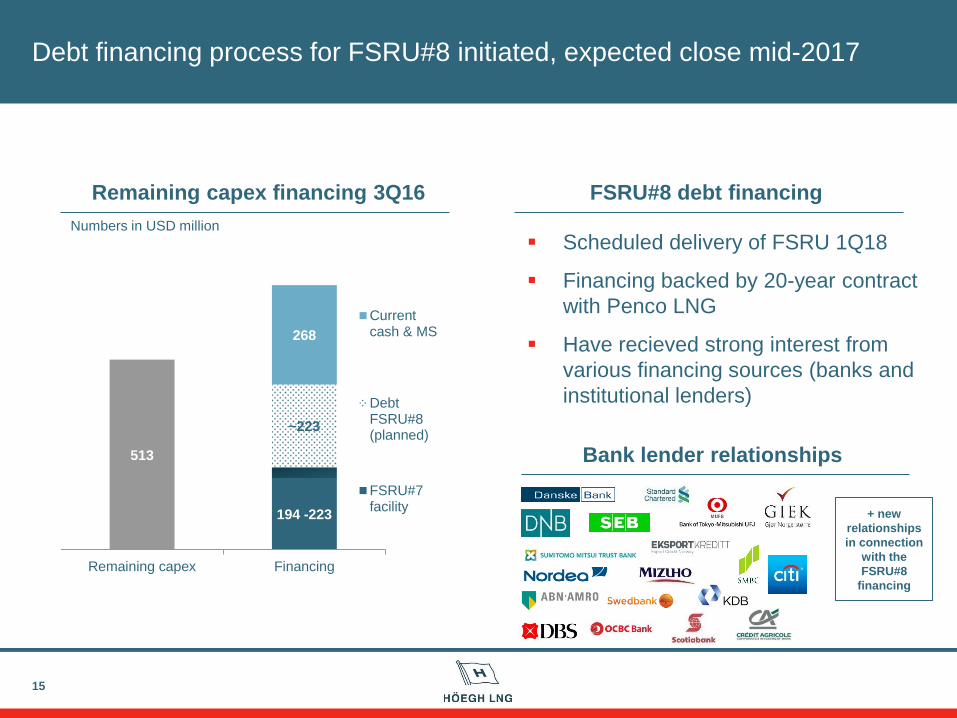

Debt financing process for FSRU#8 initiated, expected close mid-2017

15

513

194 -223

~223

268

Remaining capex Financing

Currentcash & MS

DebtFSRU#8(planned)

FSRU#7facility

FSRU#8 debt financing

Numbers in USD million

Scheduled delivery of FSRU 1Q18

Financing backed by 20-year contract

with Penco LNG

Have recieved strong interest from

various financing sources (banks and

institutional lenders)

Remaining capex financing 3Q16

Bank lender relationships

+ new

relationships

in connection

with the

FSRU#8

financing

HMLP unit price up 26% LTM

16

+26%

+6%

-4%

0

50

100

150

200

250

300

350

400

0

2

4

6

8

10

12

14

16

18

20

No

v-1

5

De

c-1

5

De

c-1

5

Ja

n-1

6

Feb

-16

Feb

-16

Ma

r-1

6

Ap

r-1

6

Ma

y-1

6

Ma

y-1

6

Ju

n-1

6

Ju

l-1

6

Ju

l-1

6

Au

g-1

6

Se

p-1

6

Se

p-1

6

Oct-

16

No

v-1

6

Volume (000’) USD HMLP unit price development

HMLP volume HMLP

Alerian MLP index (rebased) S&P500 (rebased)

HMLP units key figures1:

Last close (15 Nov): USD 18.75

Market cap: USD 493 million

52 week high: USD 19.23

52 week low: USD 12.55

Current distribution: 0.4125 USD/unit

Current dividend yield: 8.8%

Höegh LNG ownership: 58%

HMLP has filed a shelf registration

Allows HMLP to issue new equity at

short notice with limited documentation

1 As of close 15.11.16

Preparations made for refinancing of HLNG01 maturing 2017

0

100

200

300

400

500

600

700

0 1 2 3 4 5

Ind

ica

tive

cre

dit

sp

rea

d (

bp

s)

Years to maturity

LNG bonds

GasLog

Golar LNG Partners

HLNG

Teekay LNG

17

Note: Arctic Securities indicative prices, as of 16 Nov 2016

Source: Arctic Securities

Bond Maturity Years to

maturity

Rank Coupon Currency Indicative price Indicative

spread

HLNG01 03.10.2017 0.88 Sr unsecured NIBOR3M+600 NOK 103.5 202

HLNG02 05.06.2020 3.56 Sr Unsecured LIBOR3M+500 USD 100.0 500

18

Debt financing process for FSRU#8 initiated

Preparing for dropdown of Höegh Grace to HMLP

Summary

Stable financial performance

Preparations made for refinancing of NOK 750m bond

19

Q&A session Call-in details:

Norway +47 23 50 01 87

United Kingdom +44 (0)20 3364 5726

United States +1 719-325-2340

Participant passcode: 201425

Höegh LNG Holdings - Agenda for presentation of 3Q 2016 financial results

20

Sveinung J.S. Støhle

President & CEO

Highlights / Markets / Summary

Appendix

Steffen Føreid

CFO

Financials

Dedededw

Income Statement – Joint Ventures according to equity method

21

USD million 3Q2016 2Q2016 1Q2016 4Q2015 3Q2015

Freight revenues 53.6 52.3 51.1 51.3 54.1

Management and other income 1.0 1.5 1.0 3.9 1.4

Share of results from investments in joint ventures 3.5 3.3 3.3 3.5 2.8

TOTAL INCOME 58.1 57.1 55.4 58.7 58.3

Charterhire expenses (8.9) (8.8) (8.8) (8.9) (8.9)

Bunker expenses (0.2) (0.1) (0.0) (1.8) (0.1)

Operating expenses (12.1) (11.7) (9.3) (10.0) (11.5)

Project administrative expenses (2.9) (2.9) (3.0) (3.2) (2.3)

Group administrative expenses (5.2) (4.8) (4.8) (4.1) (4.8)

Business development expenses (2.3) (1.8) (2.9) (6.0) (4.2)

EBITDA 26.5 27.0 26.6 24.6 26.6

Depreciation (9.2) (9.2) (7.3) (6.9) (6.9)

Reversal of impairment (impairment) - - - (37.0) -

EBIT 17.3 17.8 19.3 (19.3) 19.7

Interest income 0.3 0.4 0.5 0.4 0.4

Interest expenses (14.3) (14.6) (12.9) (12.6) (12.6)

Other financial items 1.1 0.4 0.2 (0.4) (5.4)

PROFIT (LOSS) BEFORE TAX 4.4 4.0 7.1 (32.0) 2.1

Taxes (1.1) (0.5) (0.8) (1.0) 0.4

NET PROFIT (LOSS) 3.3 3.5 6.3 (33.0) 2.5

-

Financial position- Joint Ventures according to equity method

22

USD million 30.09.2016 30.06.2016 31.03.2016 31.12.2015 30.09.2015

Licences, design and other intangibles 0 0 0 0 37

Newbuildings under construction and vessels 1 245 1 247 1 225 1 033 1 036

Shareholder loans to joint ventures 9 10 13 14 15

Mark-to-market on hedging instruments 0 0 0 3 0

Other assets 71 73 66 71 55

Restricted cash (non-current) 23 20 20 20 17

Current cash and marketable securities 268 294 343 344 371

Asset held for sale 0 0 0 18 18

TOTAL ASSETS 1 616 1 644 1 667 1 503 1 549

Total equity 442 434 456 492 510

Investments in joint ventures 76 85 83 74 90

Interest bearing debt 955 966 979 787 801

Mark-to-market on hedging instruments 72 86 76 68 74

Other liabilities 71 72 73 83 74

TOTAL EQUITY AND LIABILITIES 1 616 1 643 1 667 1 503 1 549

Total equity adjusted for hedging reserves 576 585 592 598 642

Equity ratio adjusted for hedging reserves 36 % 36 % 36 % 40 % 41 %

Net interest bearing debt 663 650 616 423 413

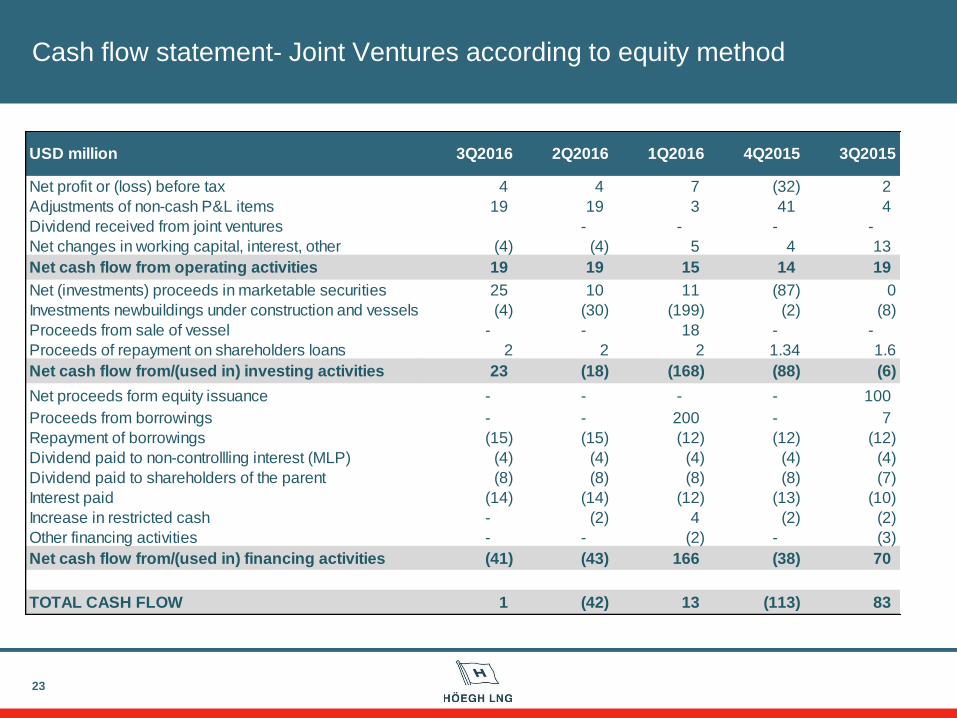

Cash flow statement- Joint Ventures according to equity method

23

USD million 3Q2016 2Q2016 1Q2016 4Q2015 3Q2015

Net profit or (loss) before tax 4 4 7 (32) 2

Adjustments of non-cash P&L items 19 19 3 41 4

Dividend received from joint ventures - - - -

Net changes in working capital, interest, other (4) (4) 5 4 13

Net cash flow from operating activities 19 19 15 14 19

Net (investments) proceeds in marketable securities 25 10 11 (87) 0

Investments newbuildings under construction and vessels (4) (30) (199) (2) (8)

Proceeds from sale of vessel - - 18 - -

Proceeds of repayment on shareholders loans 2 2 2 1.34 1.6

Net cash flow from/(used in) investing activities 23 (18) (168) (88) (6)

Net proceeds form equity issuance - - - - 100

Proceeds from borrowings - - 200 - 7

Repayment of borrowings (15) (15) (12) (12) (12)

Dividend paid to non-controllling interest (MLP) (4) (4) (4) (4) (4)

Dividend paid to shareholders of the parent (8) (8) (8) (8) (7)

Interest paid (14) (14) (12) (13) (10)

Increase in restricted cash - (2) 4 (2) (2)

Other financing activities - - (2) - (3)

Net cash flow from/(used in) financing activities (41) (43) 166 (38) 70

TOTAL CASH FLOW 1 (42) 13 (113) 83