Health Care Reform and Employers – 2015 Timothy R. Koski Alumni Appreciation Day April 30, 2015.

52

Health Care Reform and Employers – 2015 Timothy R. Koski Alumni Appreciation Day April 30, 2015

-

Upload

meagan-norman -

Category

Documents

-

view

215 -

download

0

Transcript of Health Care Reform and Employers – 2015 Timothy R. Koski Alumni Appreciation Day April 30, 2015.

Health Care Reform and Employers –2015

Timothy R. KoskiAlumni Appreciation Day

April 30, 2015

Disclaimer

• This is a summary of selected federal tax developments.• This outline is a summary of selected developments and is

not intended to provide legal, accounting, or other professional services, and is provided with the understanding that the author/presenter is not engaged in rendering legal, accounting, or other professional services.

• Due to the constantly changing nature of the subject, this outline should not be used as a resource for any tax or accounting opinion, or tax return position.

Outline of Discussion

• Status of ACA– The Health Care and Education

Reconciliation Act of 2010 (PL 111-152), amends the Patient Protection and Affordable Care Act of 2010 (PL 111-148)

• Employer Shared Responsibility

• Employer Reporting• Other Selected Issues

Status of ACA - Validity of Regulations Governing Premium Tax Credit

• King v. Burwell, 114 AFTR 2d 2014-5259 (CA-4, 7/22/2014), cert. granted 11/07/2014.– Supreme Court has agreed to settle a split between the Circuits

regarding the validity of the regulation authorizing the IRS to provide premium tax credits under the ACA for insurance purchased on federal Exchanges.• IRC §36B(b)(2)(A) refers to “the monthly premiums for .. qualified health plans

offered in the individual market … which were enrolled in through an Exchange established by the State” under §1311.

• Regulations issued under §36B provide that the premium tax credit isn’t just limited to State Exchanges, but also includes federally-facilitated Exchanges (Reg. 1.36B-1(k)).

Federal versus State Exchanges

Individual Shared Responsibility

• Beginning in 2014, individuals who aren’t otherwise exempt must purchase health insurance coverage that meets a minimum coverage standard (“minimum essential coverage”) or pay a penalty (“shared responsibility payment”).– Individuals can purchase insurance on the Exchange or from a private

provider outside the Exchange.– Premium tax credit is only available for insurance purchased through

the Exchange.

Individual Shared Responsibility

• Individuals and each family member must either:– Have minimum essential coverage;– Have exemption from minimal essential coverage;

or– Make a shared responsibility payment.• Penalty

Individual Shared Reasonability - Penalty

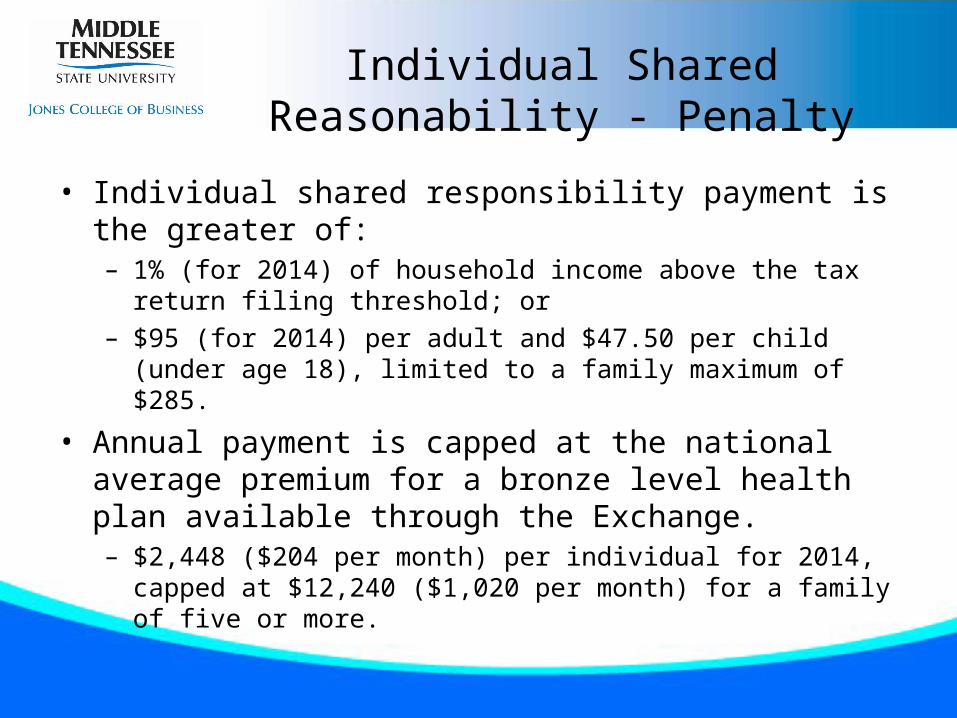

• Individual shared responsibility payment is the greater of:– 1% (for 2014) of household income above the tax return filing

threshold; or– $95 (for 2014) per adult and $47.50 per child (under age 18), limited

to a family maximum of $285.

• Annual payment is capped at the national average premium for a bronze level health plan available through the Exchange.– $2,448 ($204 per month) per individual for 2014, capped at $12,240

($1,020 per month) for a family of five or more.

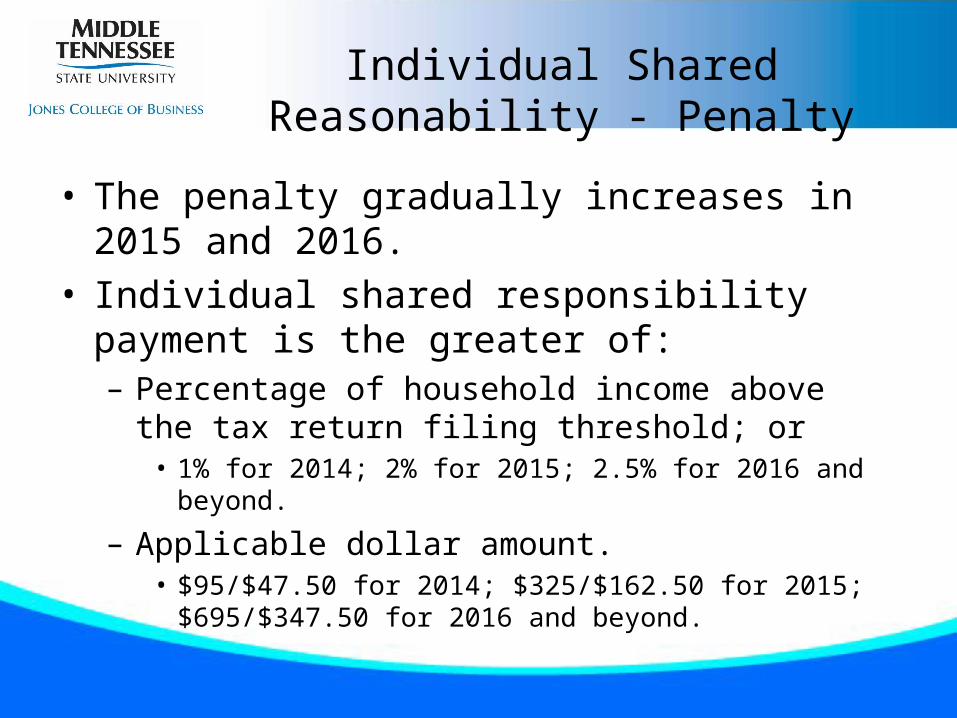

Individual Shared Reasonability - Penalty

• The penalty gradually increases in 2015 and 2016.• Individual shared responsibility payment is the

greater of:– Percentage of household income above the tax return

filing threshold; or • 1% for 2014; 2% for 2015; 2.5% for 2016 and beyond.

– Applicable dollar amount.• $95/$47.50 for 2014; $325/$162.50 for 2015; $695/$347.50 for

2016 and beyond.

Premium Tax Credit (PTC)

• A premium tax credit is available to assist individuals and families in purchasing health insurance.– Premium tax credit is available for health insurance

purchased through the Exchange.– Employer penalty only applies if employee purchases

health insurance through the Exchange and receives a subsidy (PTC).

PTC – Relationship to Poverty Level

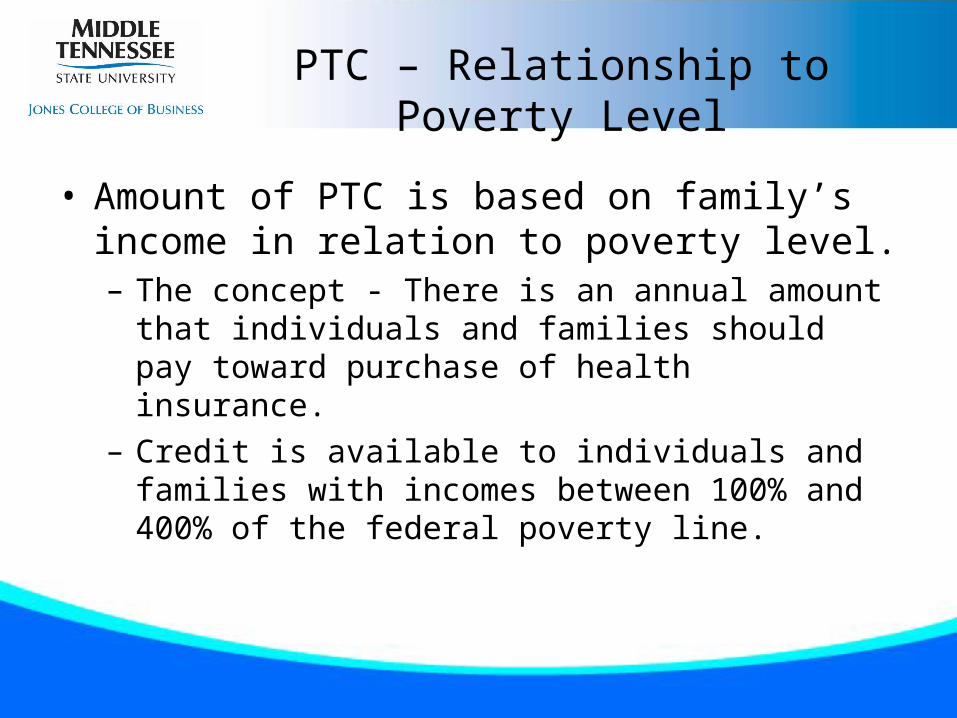

• Amount of PTC is based on family’s income in relation to poverty level. – The concept - There is an annual amount that individuals

and families should pay toward purchase of health insurance.

– Credit is available to individuals and families with incomes between 100% and 400% of the federal poverty line.

PTC – Requirements

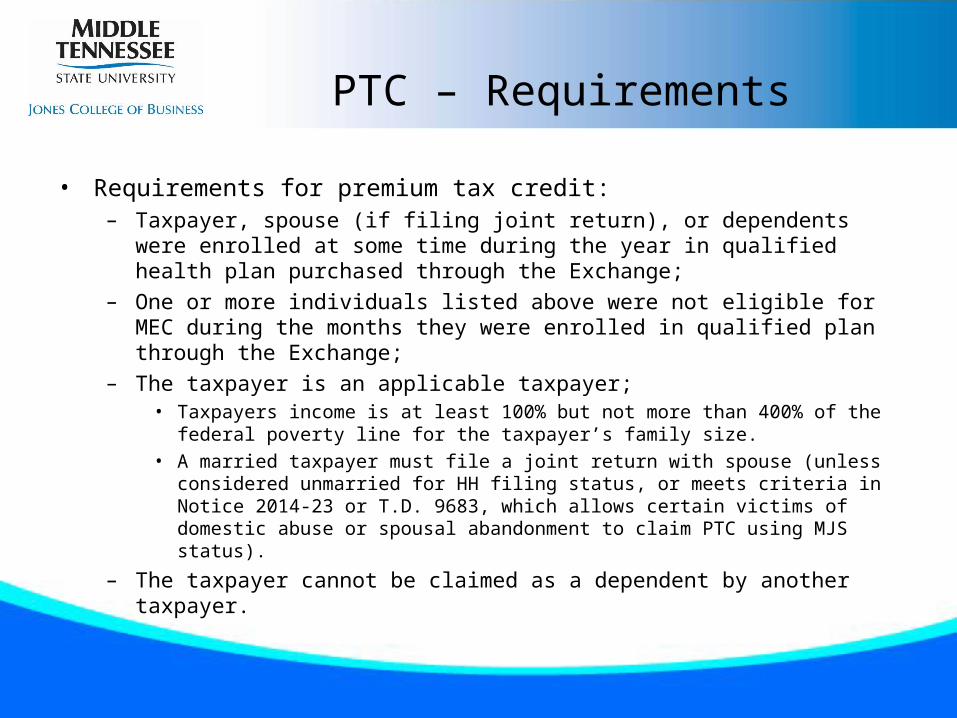

• Requirements for premium tax credit:– Taxpayer, spouse (if filing joint return), or dependents were enrolled at some time

during the year in qualified health plan purchased through the Exchange;– One or more individuals listed above were not eligible for MEC during the months they

were enrolled in qualified plan through the Exchange; – The taxpayer is an applicable taxpayer;

• Taxpayers income is at least 100% but not more than 400% of the federal poverty line for the taxpayer’s family size.

• A married taxpayer must file a joint return with spouse (unless considered unmarried for HH filing status, or meets criteria in Notice 2014-23 or T.D. 9683, which allows certain victims of domestic abuse or spousal abandonment to claim PTC using MJS status).

– The taxpayer cannot be claimed as a dependent by another taxpayer.

Premium Tax Credit

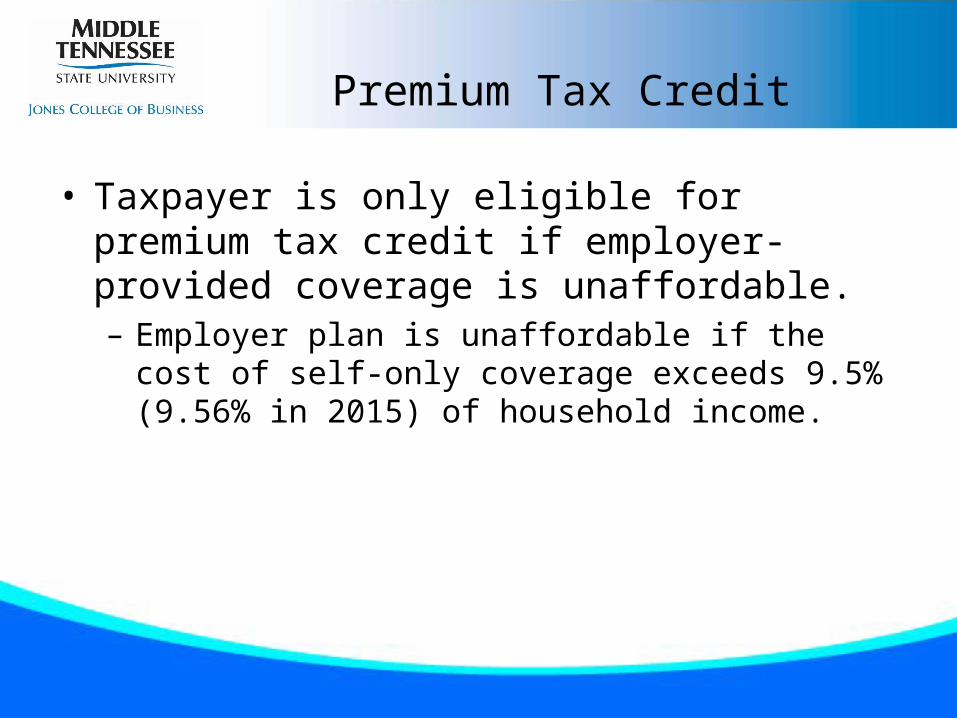

• Taxpayer is only eligible for premium tax credit if employer-provided coverage is unaffordable.– Employer plan is unaffordable if the cost of self-only

coverage exceeds 9.5% (9.56% in 2015) of household income.

Employer Shared Responsibility

• “Pay or Play”– Beginning in 2015, a nondeductible penalty tax

will be imposed on large employers that fail to provide minimum essential coverage.• Definition of large employer.• Calculation of penalty

– “Big” penalty– “Small” penalty

Employer Shared Responsibility

• Transition relief:– For 2015 only, large employer = 100 or more (instead of 50

or more) full-time equivalent employees.– For 2015 only, employers can look back to any six

consecutive months in determining whether they are “large employer.”

• Permanent relief:– No penalty for first three months of the year after meeting

definition of “large employer.”

Employer Shared Responsibility

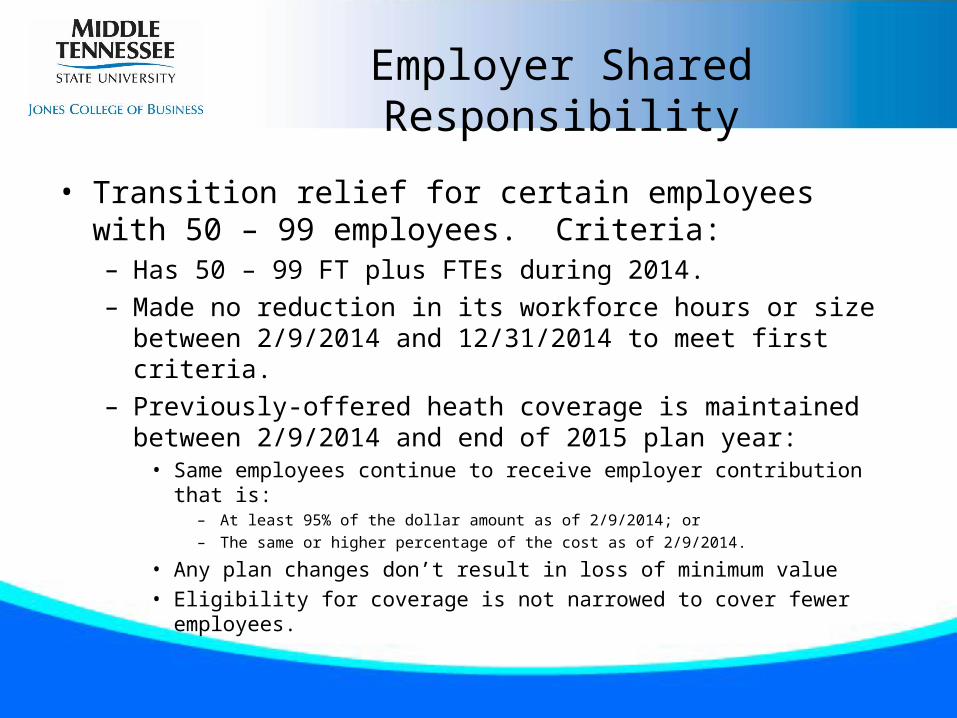

• Transition relief for certain employees with 50 – 99 employees. Criteria: – Has 50 – 99 FT plus FTEs during 2014.– Made no reduction in its workforce hours or size between 2/9/2014

and 12/31/2014 to meet first criteria.– Previously-offered heath coverage is maintained between 2/9/2014

and end of 2015 plan year:• Same employees continue to receive employer contribution that is:

– At least 95% of the dollar amount as of 2/9/2014; or– The same or higher percentage of the cost as of 2/9/2014.

• Any plan changes don’t result in loss of minimum value• Eligibility for coverage is not narrowed to cover fewer employees.

Employer Shared Responsibility

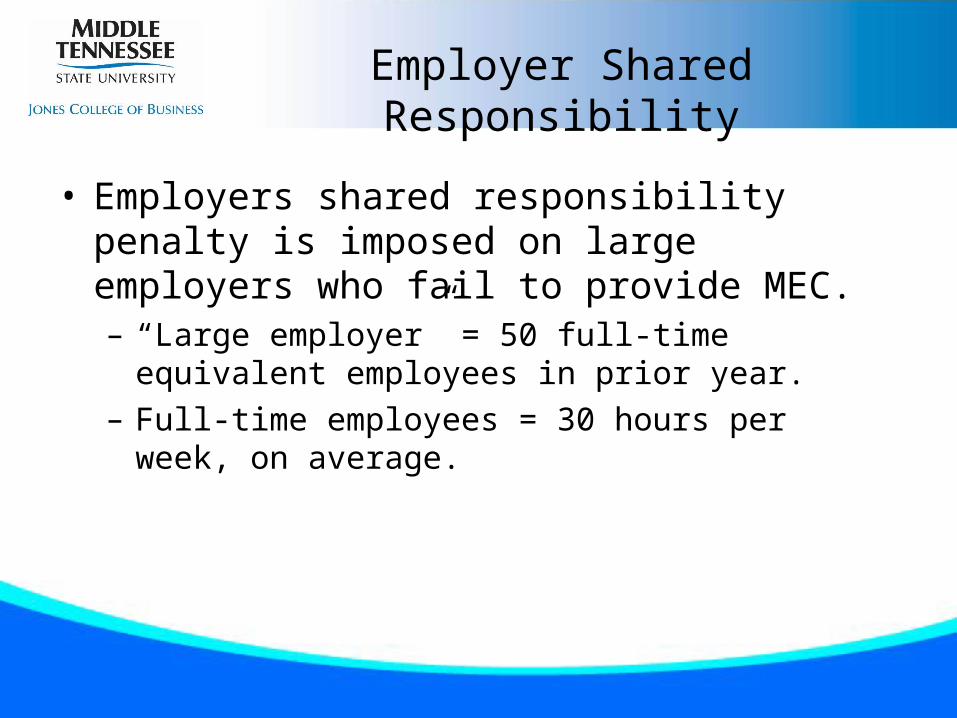

• Employers shared responsibility penalty is imposed on large employers who fail to provide MEC.– “Large employer” = 50 full-time equivalent employees in

prior year. – Full-time employees = 30 hours per week, on average.

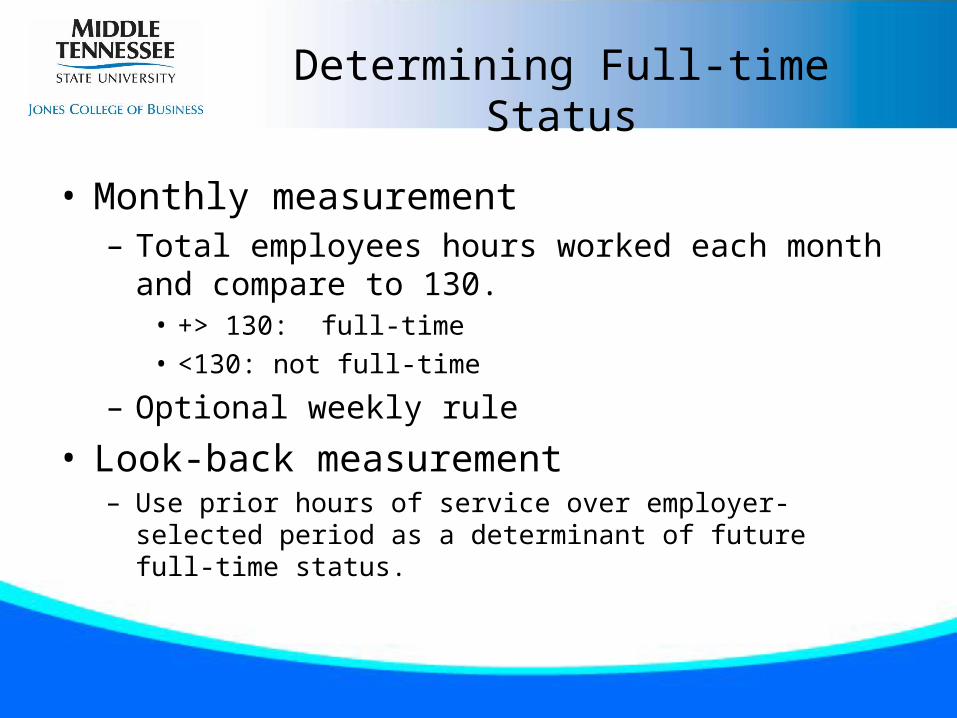

Determining Full-time Status

• Monthly measurement– Total employees hours worked each month and compare

to 130.• +> 130: full-time• <130: not full-time

– Optional weekly rule

• Look-back measurement– Use prior hours of service over employer-selected period as a

determinant of future full-time status.

Determining FTEs

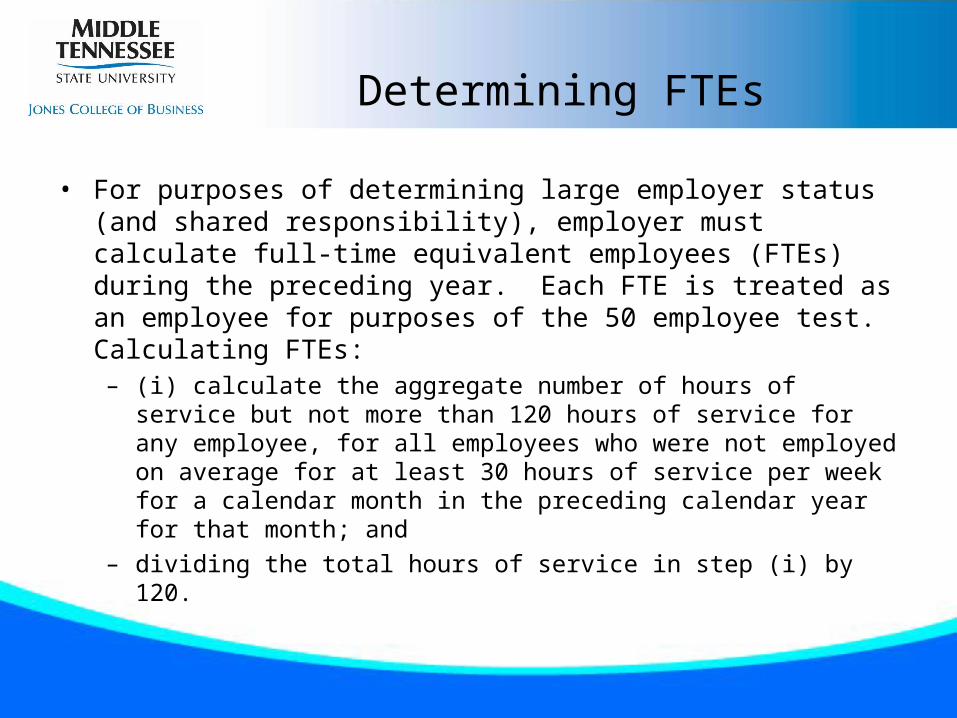

• For purposes of determining large employer status (and shared responsibility), employer must calculate full-time equivalent employees (FTEs) during the preceding year. Each FTE is treated as an employee for purposes of the 50 employee test. Calculating FTEs:– (i) calculate the aggregate number of hours of service but not more than 120

hours of service for any employee, for all employees who were not employed on average for at least 30 hours of service per week for a calendar month in the preceding calendar year for that month; and

– dividing the total hours of service in step (i) by 120.

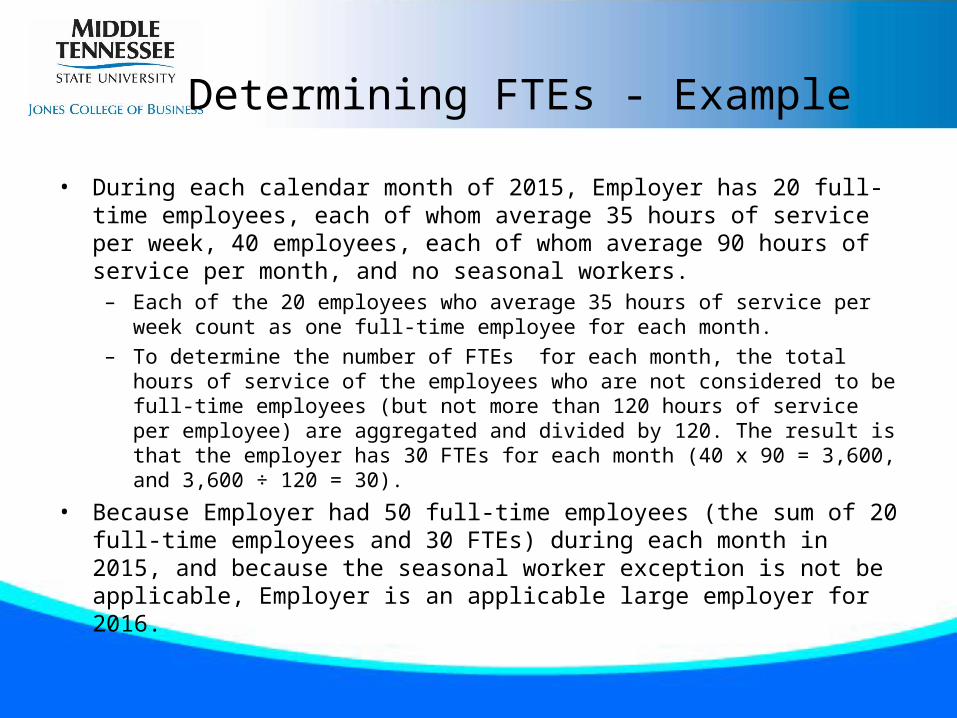

Determining FTEs - Example

• During each calendar month of 2015, Employer has 20 full-time employees, each of whom average 35 hours of service per week, 40 employees, each of whom average 90 hours of service per month, and no seasonal workers. – Each of the 20 employees who average 35 hours of service per week count as one full-

time employee for each month. – To determine the number of FTEs for each month, the total hours of service of the

employees who are not considered to be full-time employees (but not more than 120 hours of service per employee) are aggregated and divided by 120. The result is that the employer has 30 FTEs for each month (40 x 90 = 3,600, and 3,600 ÷ 120 = 30).

• Because Employer had 50 full-time employees (the sum of 20 full-time employees and 30 FTEs) during each month in 2015, and because the seasonal worker exception is not be applicable, Employer is an applicable large employer for 2016.

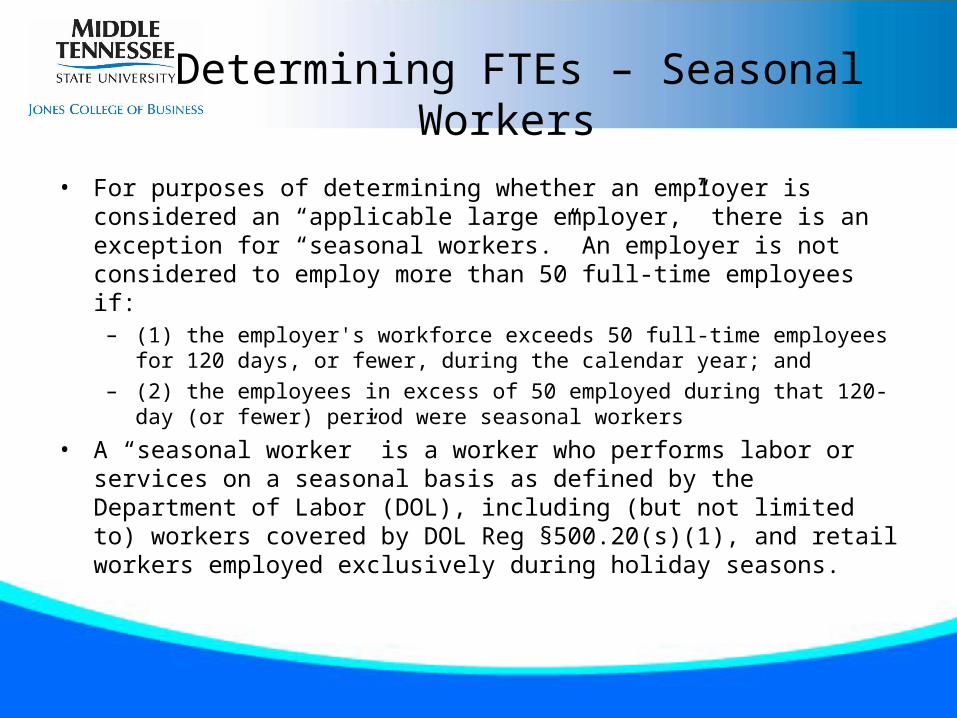

Determining FTEs – Seasonal Workers

• For purposes of determining whether an employer is considered an “applicable large employer,” there is an exception for “seasonal workers.” An employer is not considered to employ more than 50 full-time employees if:– (1) the employer's workforce exceeds 50 full-time employees for 120 days, or fewer,

during the calendar year; and – (2) the employees in excess of 50 employed during that 120-day (or fewer) period were

seasonal workers

• A “seasonal worker” is a worker who performs labor or services on a seasonal basis as defined by the Department of Labor (DOL), including (but not limited to) workers covered by DOL Reg §500.20(s)(1), and retail workers employed exclusively during holiday seasons.

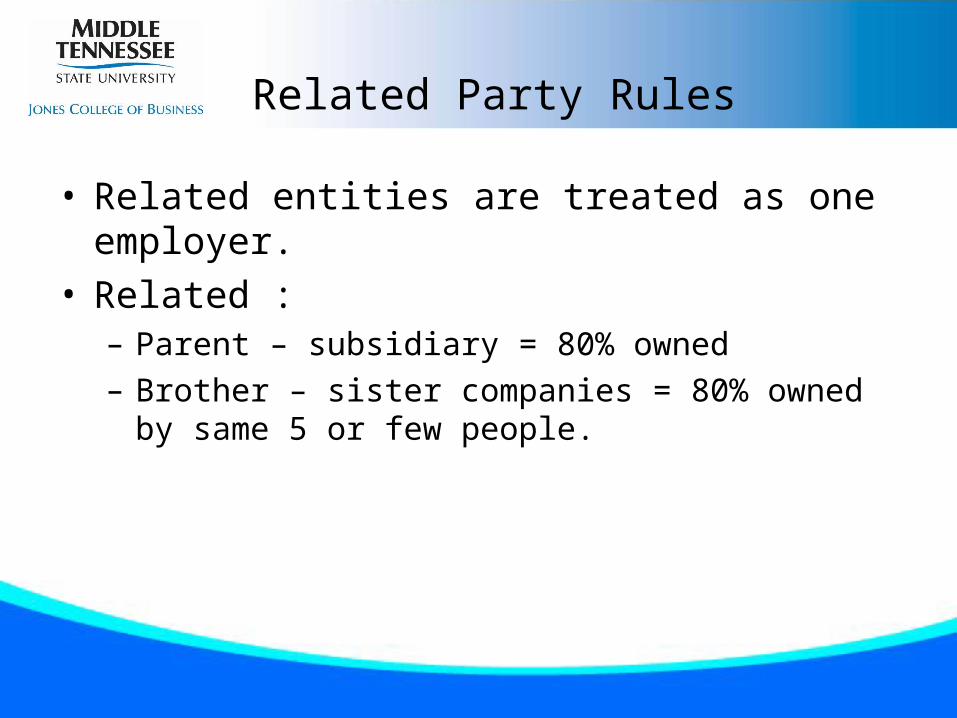

Related Party Rules

• Related entities are treated as one employer.• Related :– Parent – subsidiary = 80% owned– Brother – sister companies = 80% owned by same 5 or few

people.

Employer Shared Responsibility

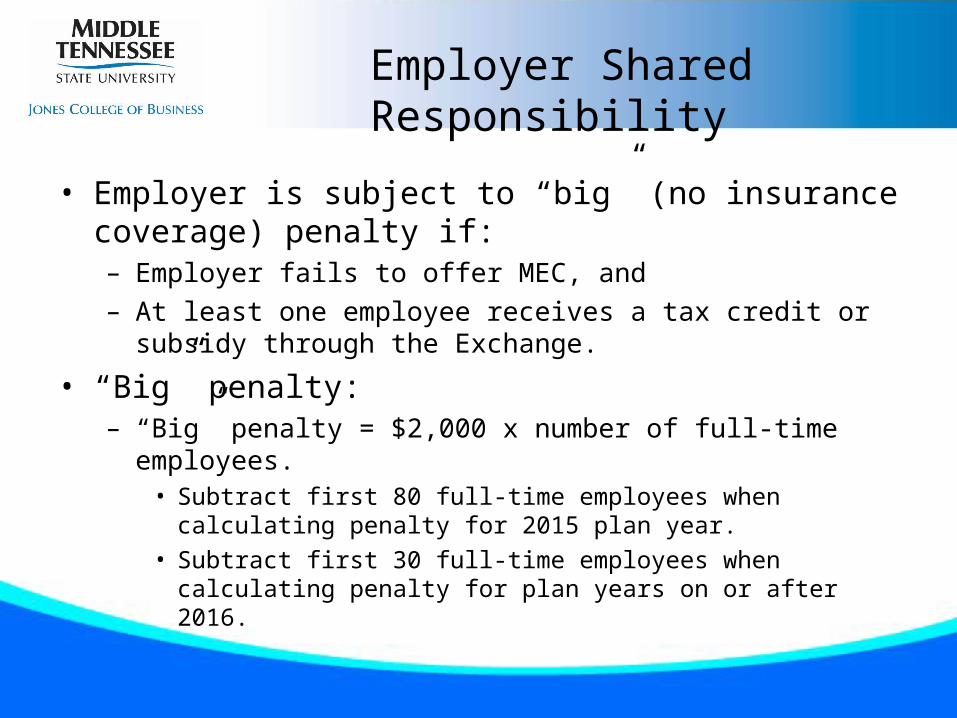

• Employer is subject to “big” (no insurance coverage) penalty if:– Employer fails to offer MEC, and– At least one employee receives a tax credit or subsidy through the

Exchange.

• “Big” penalty:– “Big” penalty = $2,000 x number of full-time employees.

• Subtract first 80 full-time employees when calculating penalty for 2015 plan year.

• Subtract first 30 full-time employees when calculating penalty for plan years on or after 2016.

Employer Shared Responsibility

• Employer has 3,080 FTE employees, offers no health insurance coverage to employees, and at least 1 employee receives subsidy from Exchange. – Penalty in 2015 = $6,000,000 {(3,280 – 80) x $2,000 = $6,000,000}.– Penalty in 2016 and beyond = $6,500,000 {(3,280 – 30) x $2,000 =

$6,500,000.

Employer Shared Responsibility

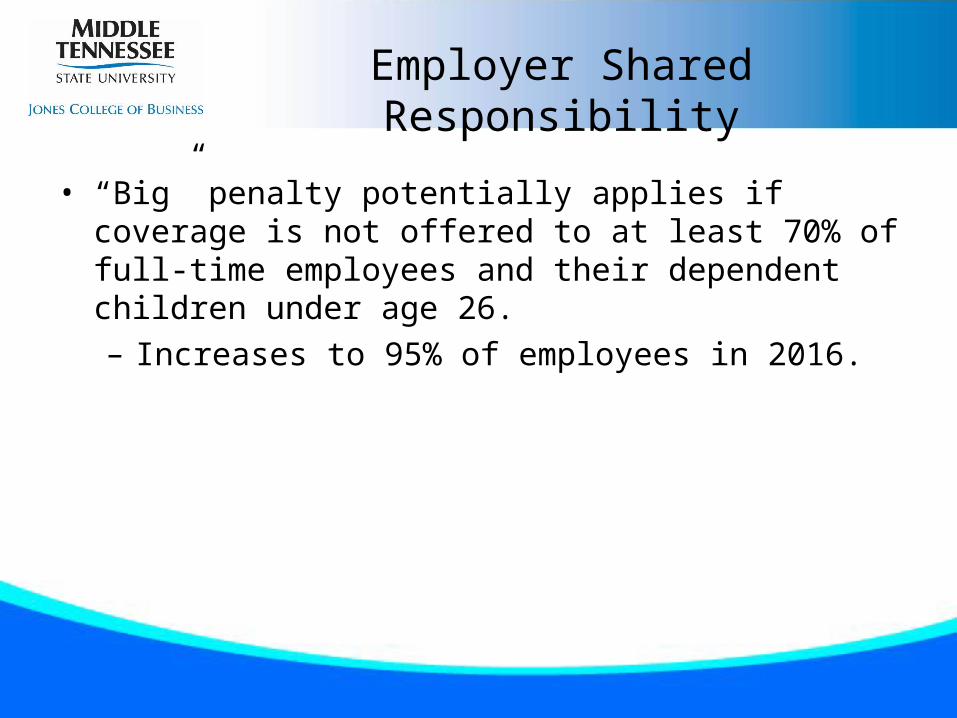

• “Big” penalty potentially applies if coverage is not offered to at least 70% of full-time employees and their dependent children under age 26.– Increases to 95% of employees in 2016.

Employer Shared Responsibility

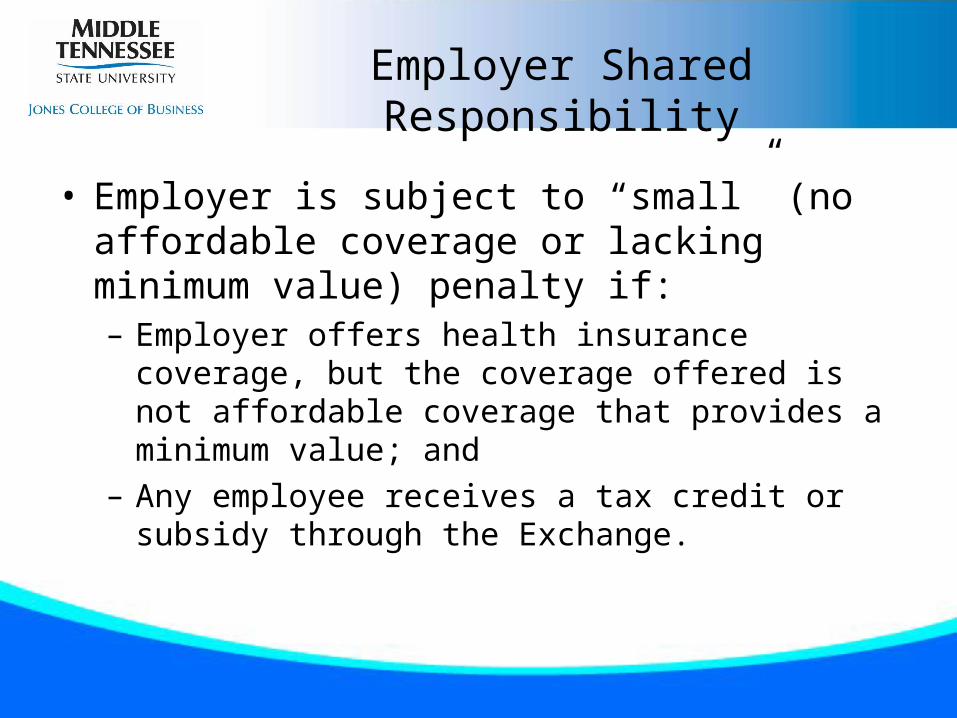

• Employer is subject to “small” (no affordable coverage or lacking minimum value) penalty if:– Employer offers health insurance coverage, but the

coverage offered is not affordable coverage that provides a minimum value; and

– Any employee receives a tax credit or subsidy through the Exchange.

Employer Shared Responsibility

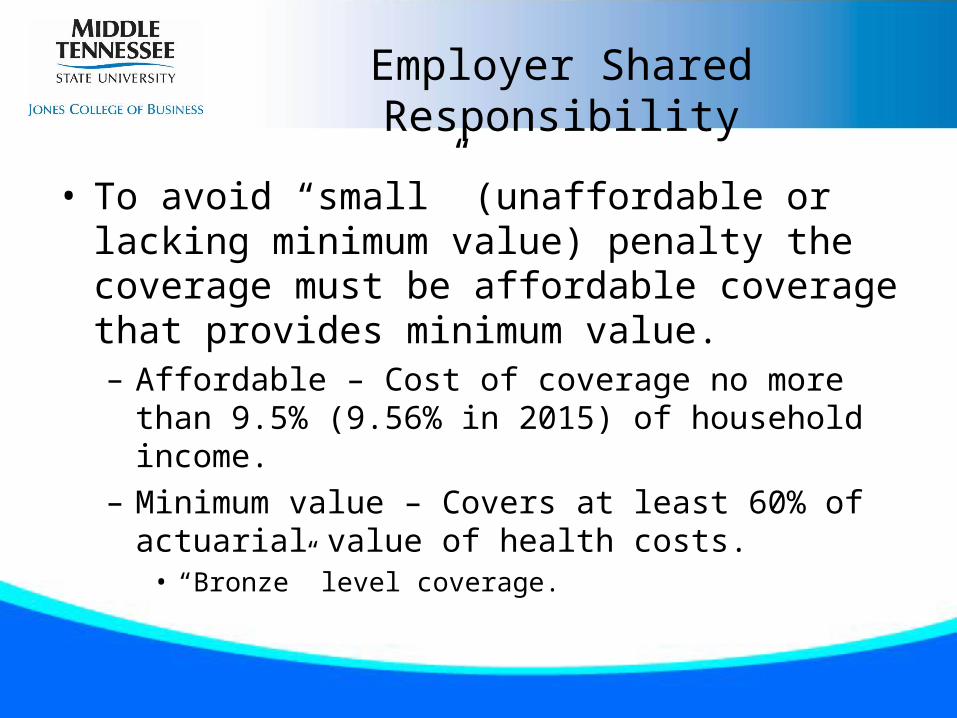

• To avoid “small” (unaffordable or lacking minimum value) penalty the coverage must be affordable coverage that provides minimum value.– Affordable – Cost of coverage no more than 9.5% (9.56%

in 2015) of household income.– Minimum value – Covers at least 60% of actuarial value of

health costs.• “Bronze” level coverage.

Employer Shared Responsibility

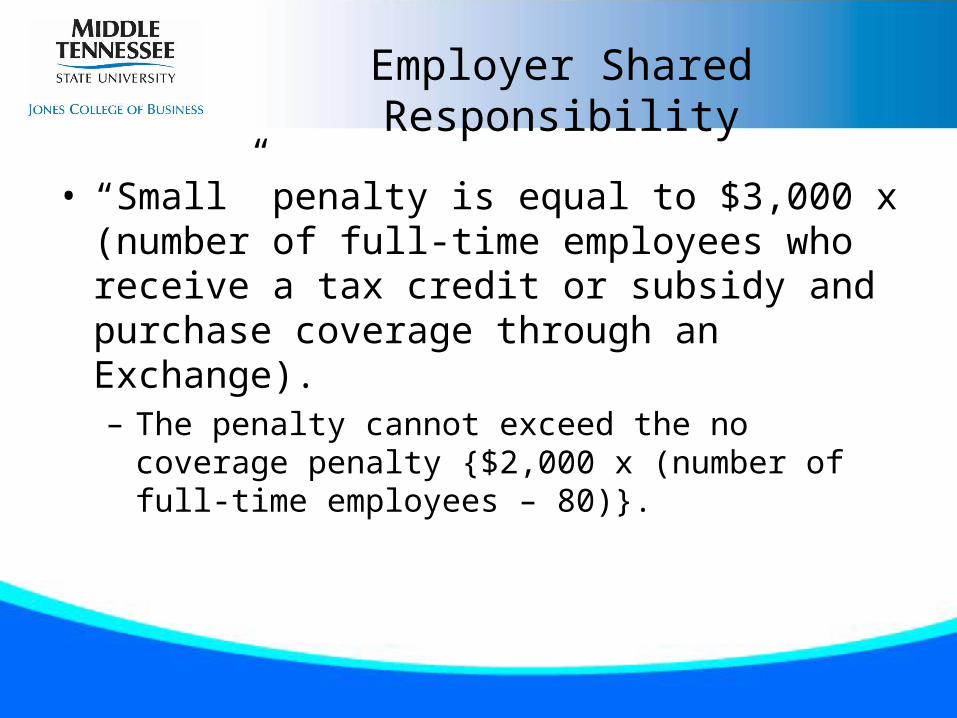

• “Small” penalty is equal to $3,000 x (number of full-time employees who receive a tax credit or subsidy and purchase coverage through an Exchange).– The penalty cannot exceed the no coverage penalty

{$2,000 x (number of full-time employees – 80)}.

Employer Shared Responsibility

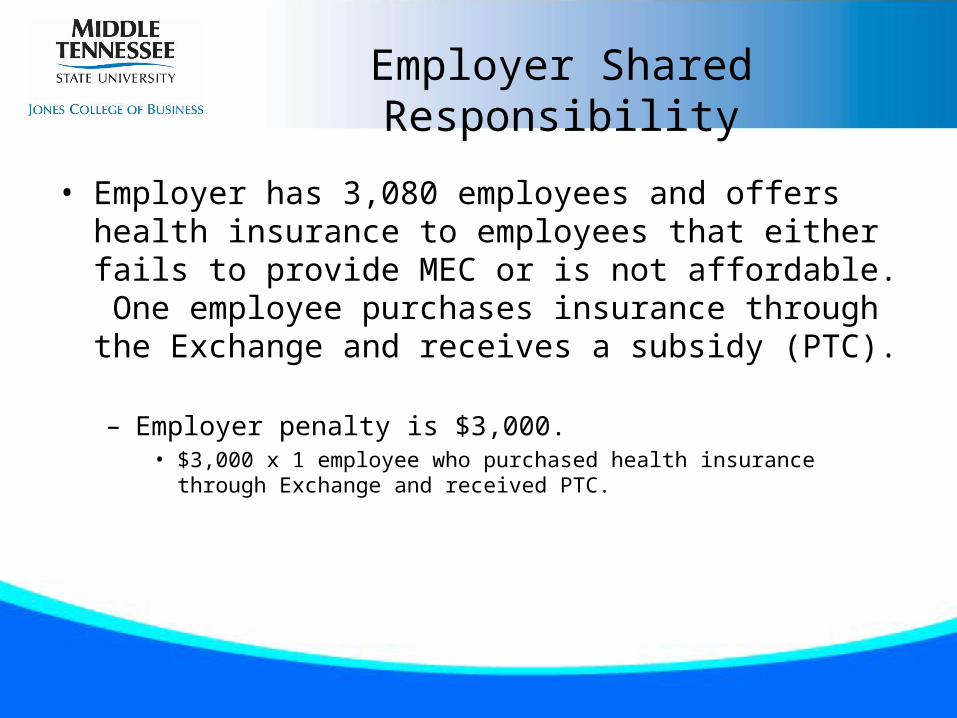

• Employer has 3,080 employees and offers health insurance to employees that either fails to provide MEC or is not affordable. One employee purchases insurance through the Exchange and receives a subsidy (PTC). – Employer penalty is $3,000.

• $3,000 x 1 employee who purchased health insurance through Exchange and received PTC.

Tiers of Coverage

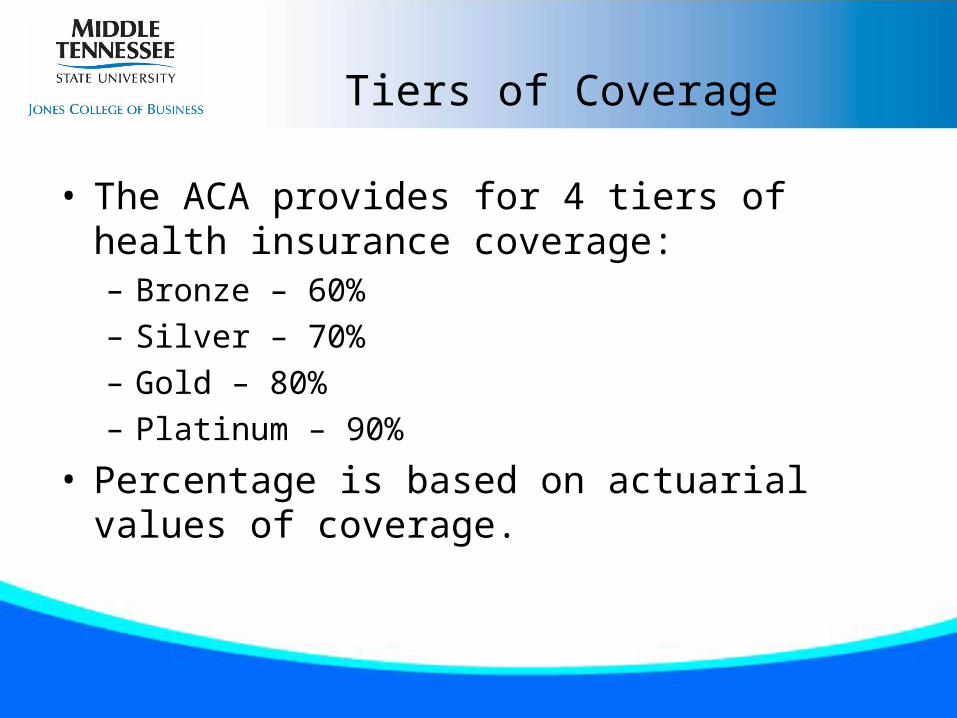

• The ACA provides for 4 tiers of health insurance coverage:– Bronze – 60%– Silver – 70%– Gold – 80%– Platinum – 90%

• Percentage is based on actuarial values of coverage.

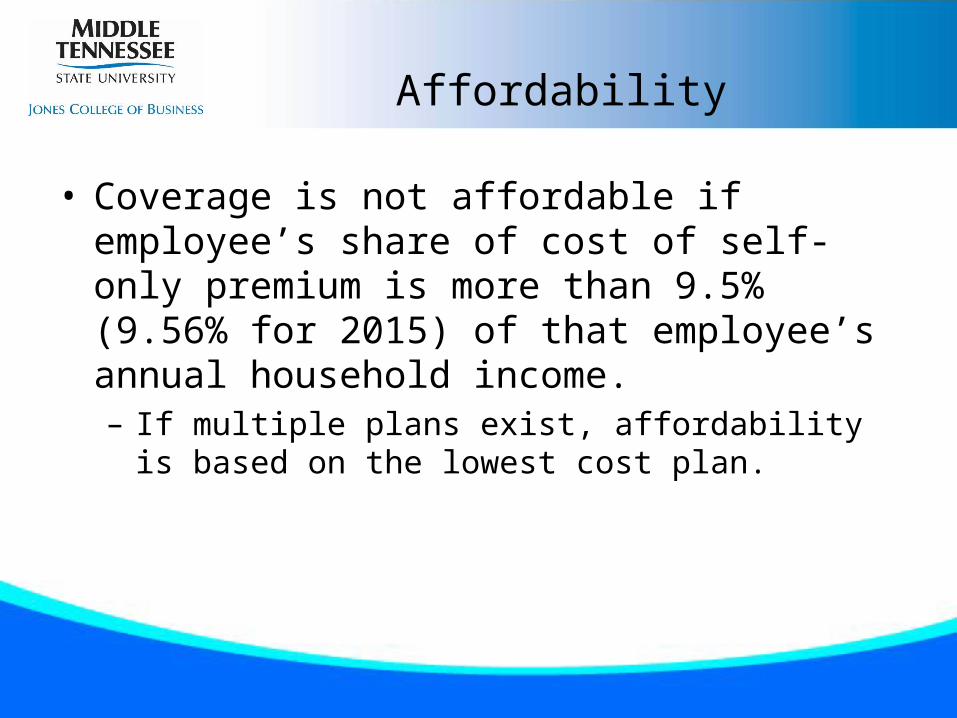

Affordability

• Coverage is not affordable if employee’s share of cost of self-only premium is more than 9.5% (9.56% for 2015) of that employee’s annual household income.– If multiple plans exist, affordability is based on the lowest

cost plan.

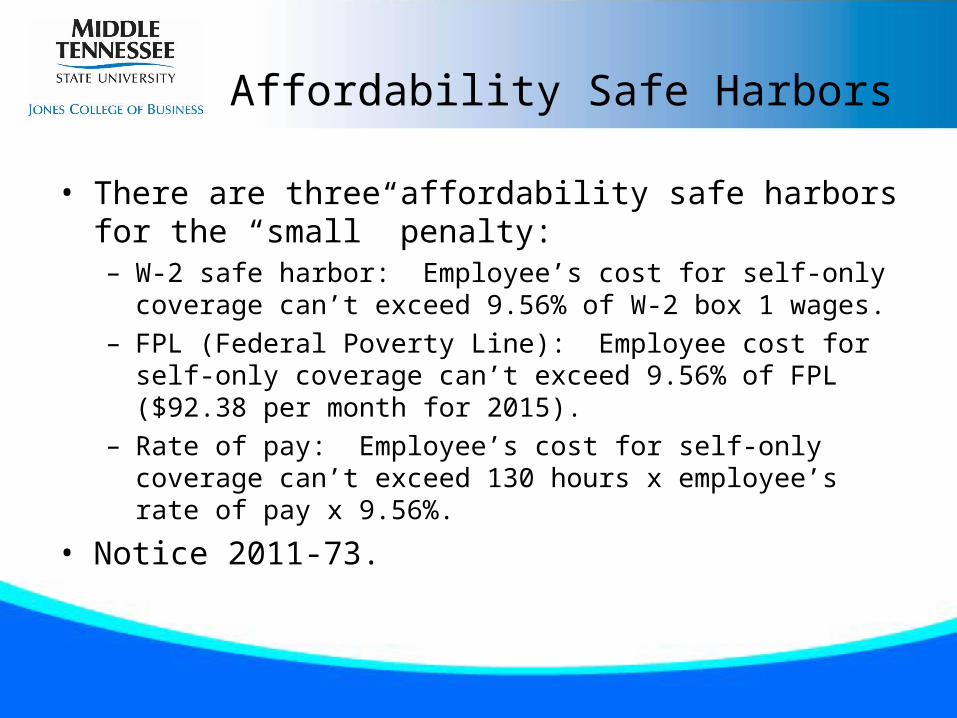

Affordability Safe Harbors

• There are three affordability safe harbors for the “small” penalty:– W-2 safe harbor: Employee’s cost for self-only coverage can’t exceed

9.56% of W-2 box 1 wages. – FPL (Federal Poverty Line): Employee cost for self-only coverage can’t

exceed 9.56% of FPL ($92.38 per month for 2015).– Rate of pay: Employee’s cost for self-only coverage can’t exceed 130

hours x employee’s rate of pay x 9.56%.

• Notice 2011-73.

Minimum Value

• Minimum value can be calculated in one of three ways: – HHS calculator – Safe harbor checklist– Actuarial certification

Information Reporting

• New IRC §§6055 and 6056 impose information reporting requirements on providers of minimum essential coverage and large employers.– The effective date of the information reporting requirements added

by the ACA were delayed to 2015 (Notice 2013-45).• Information reporting was optional for 2014.

– Final regulations issued for calendar years beginning after December 31, 2014.

Information Reporting by Health Coverage Providers - §6055

• Any person who provides MEC to an individual must report to the IRS and furnish statements to individuals. Persons required to file information returns include:– Health insurance issuers, or carriers, for insured coverage;– Plan sponsors of self-insured group health plan coverage (even if less

than 50 employees); and– The executive department or agency of a governmental unit that

provides coverage under a government-sponsored program.

• Forms 1095-B and 1094-B

Information Reporting by Employers - §6056

• Applicable large employers that are subject to employer shared responsibility provisions are required to comply with information reporting under §6056.

• Applicable large employer = An employer that employed an average of at least 50 full-time employees on business days during the preceding calendar year.– Full-time employee includes employee who worked on average at

least 30 hours per week and any full-time equivalent employees.

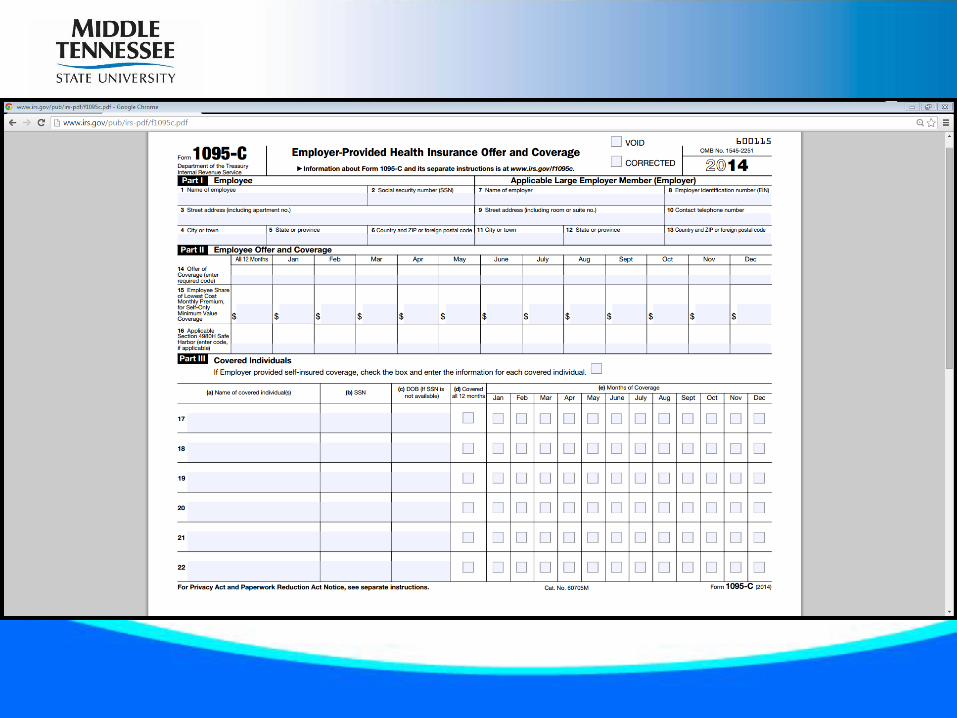

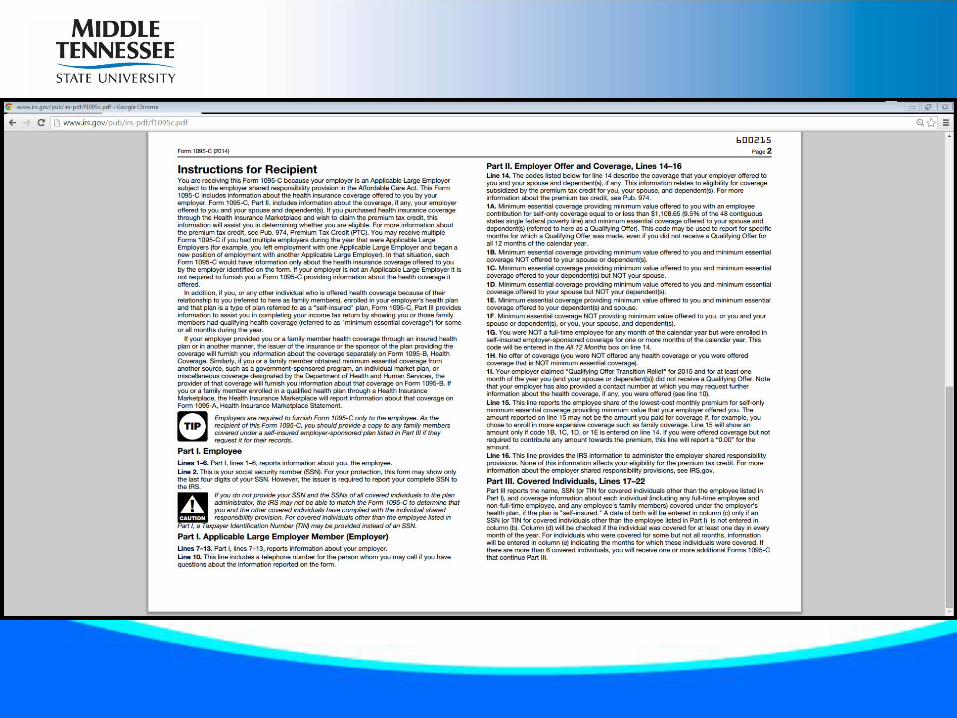

• Forms 1095-C and 1094-C

Methods of Reporting

• General method• Optional simplified alternative methods– Simplified reporting based on certification of

qualifying offer– Option to report without separate identification of

full-time employees (98% offers)

General Reporting

• Each applicable large employer may satisfy requirements to file a §6056 return by filing a Form 1094-C and, for each full-time employee, a Form 1095-C, or other forms the IRS may designate.

Simplified Reporting – Alternative 1

• If employer certifies that it made a “qualifying offer” of health insurance coverage to all full-time employees for all months during the year, it may report simplified information to the IRS and in the employee statement. Qualifying offer:– Employer offered minimum value (60% bronze level) coverage.– Required employee contribution for the employee-only (single)

coverage was no more than 9.5% (9.56% for 2015) of FPL.– Minimum essential coverage was offered to employees’ spouses and

dependents.

• 2015 transition rule – Simplified reporting allowed if qualifying offer made to 95% of full-time employees and their spouses and dependents.

Simplified Reporting – Alternative 2

• Simplified reporting alternative 2 (98% rule) allows employers to report to the IRS without identifying or specifying number of full-time employees. To qualify for this method employer must certify that: – It offered coverage to at least 98% of full-time employees; – Coverage offered was minimum value (60% bronze level)

coverage; and – Coverage was affordable.

Notice 2013-54

• Employer payment plans (employer offers to reimburse employees for the purchase of individual market policy instead of providing company health insurance) does not comply with health care reform.– Potential excise tax penalty of $100/day per employee

(§4980D)

Notice 2013-54 - Employer Payment Plans

• Employer payment plans are group health pans that will fail to comply with the market reforms that apply to group health under the ACA.– Notice 2013-54 refers to a group health plan under which an employer

reimburses an employee for some or all of the premium expenses incurred for an individual health insurance policy or directly pays a premium for an individual health insurance policy covering the employee, such as arrangements described in Rev. Rul. 61-146.

– Applies to all employers – both small employers and applicable large employers (ALEs).

– Market reforms do not apply to group health plans that have fewer than 2 employees or that provide “excepted benefits.”

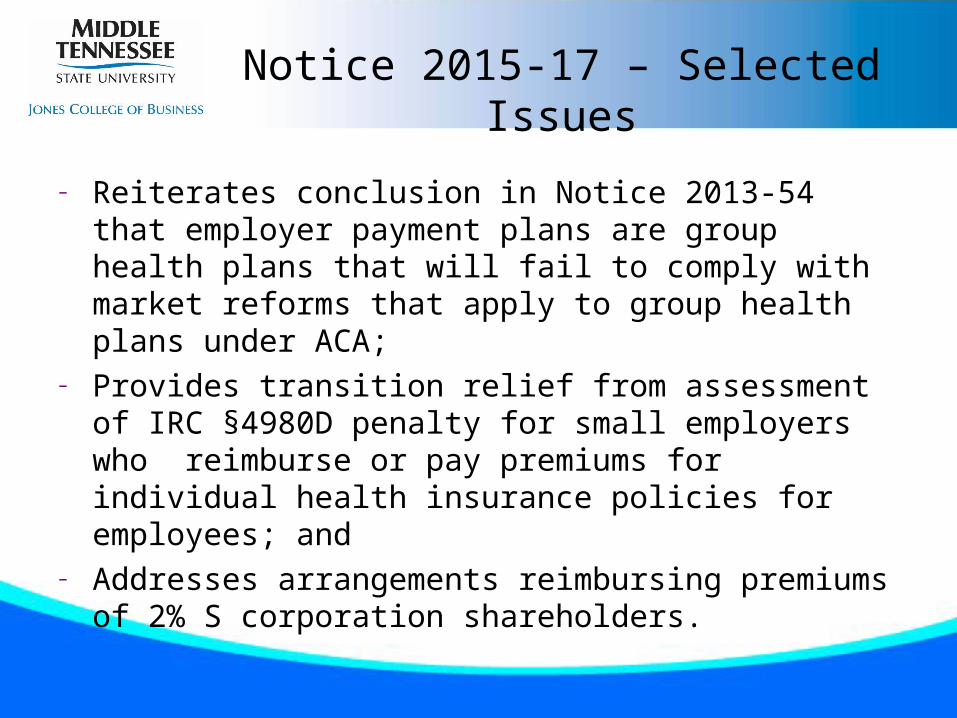

Notice 2015-17 – Selected Issues

– Reiterates conclusion in Notice 2013-54 that employer payment plans are group health plans that will fail to comply with market reforms that apply to group health plans under ACA;

– Provides transition relief from assessment of IRC §4980D penalty for small employers who reimburse or pay premiums for individual health insurance policies for employees; and

– Addresses arrangements reimbursing premiums of 2% S corporation shareholders.

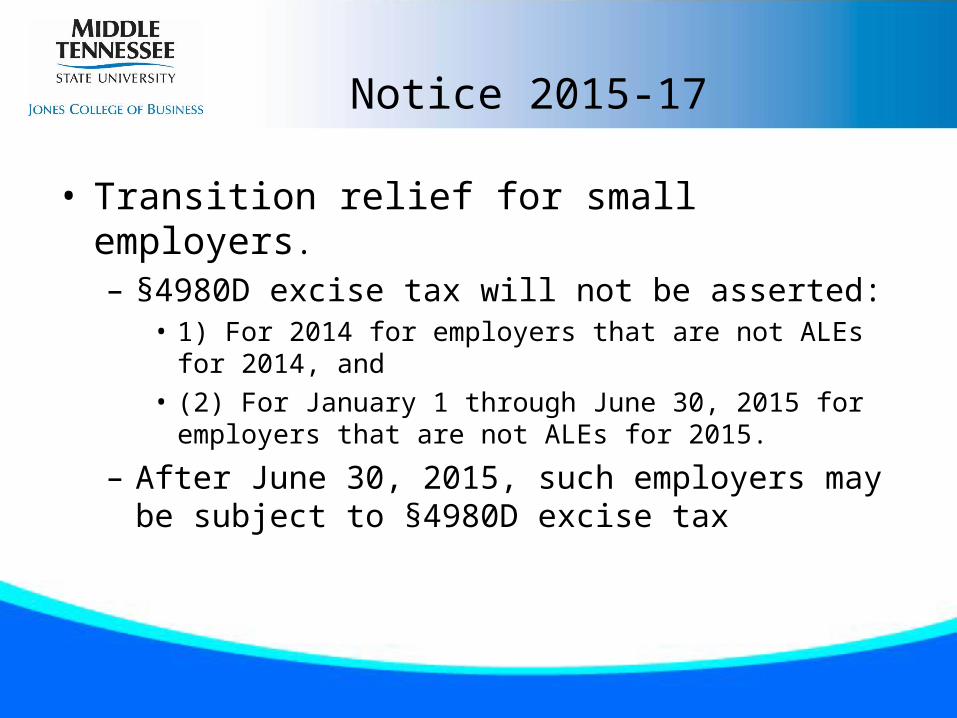

Notice 2015-17

• Transition relief for small employers.– §4980D excise tax will not be asserted:

• 1) For 2014 for employers that are not ALEs for 2014, and• (2) For January 1 through June 30, 2015 for employers that are not

ALEs for 2015.

– After June 30, 2015, such employers may be subject to §4980D excise tax

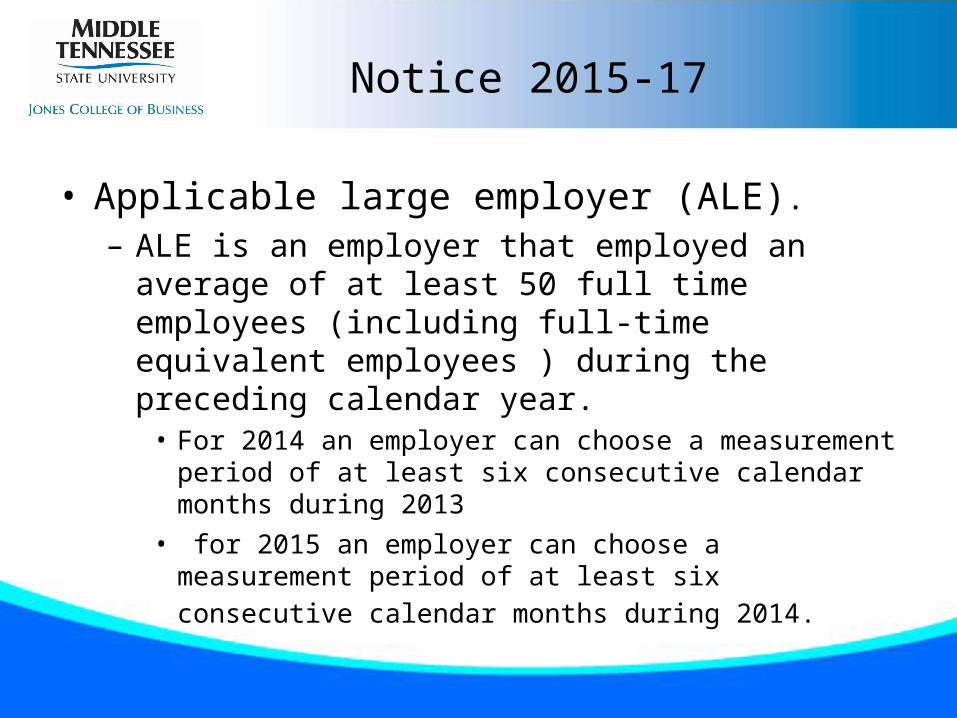

Notice 2015-17

• Applicable large employer (ALE).– ALE is an employer that employed an average of at least

50 full time employees (including full-time equivalent employees ) during the preceding calendar year.• For 2014 an employer can choose a measurement period of at

least six consecutive calendar months during 2013• for 2015 an employer can choose a measurement period of at

least six consecutive calendar months during 2014.

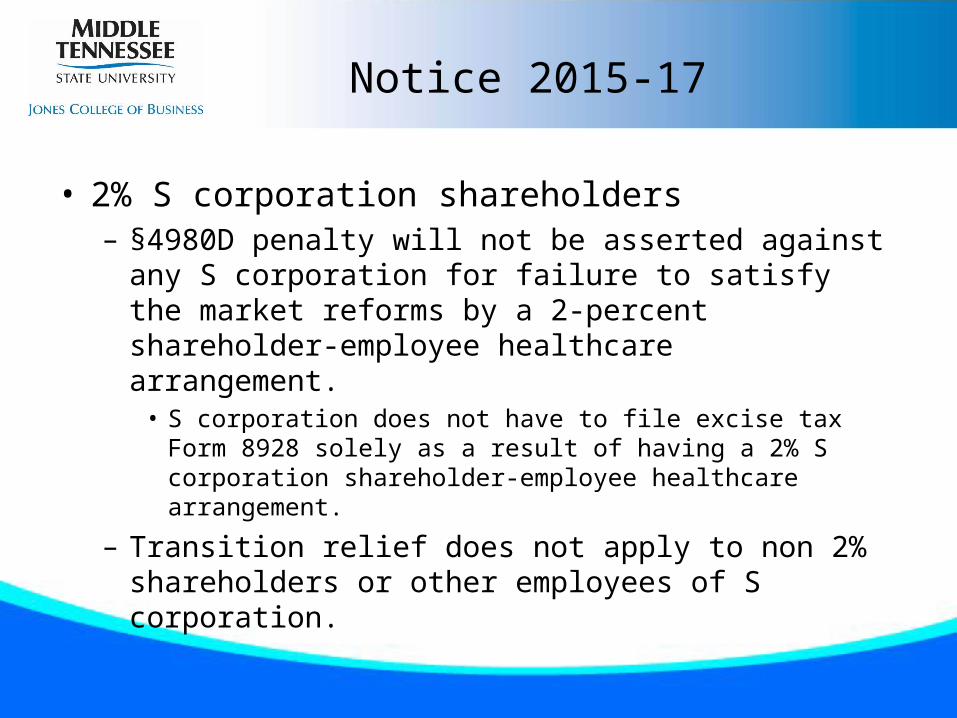

Notice 2015-17

• 2% S corporation shareholders– §4980D penalty will not be asserted against any S

corporation for failure to satisfy the market reforms by a 2-percent shareholder-employee healthcare arrangement. • S corporation does not have to file excise tax Form 8928 solely as

a result of having a 2% S corporation shareholder-employee healthcare arrangement.

– Transition relief does not apply to non 2% shareholders or other employees of S corporation.

Notice 2015-17

• If employer increases an employee’s compensation, but does not condition the payment of the additional compensation on the purchase of health coverage (or otherwise endorses a particular policy, form, or issuer of health insurance), the arrangement is not an employer health plan.

Notice 2015-17

• An arrangement whereby employer reimburses an employee’s substantiated premiums for non-employer sponsored hospital and medical insurance (excluded from income under IRC §106), is a group health plan subject to ACA market reforms.– Arrangement is subject to ACA market reforms whether employer

treats the money as pre-tax or post-tax to the employee.

Future Developments

• Your guess is as good as mine?