HALF YEAR RESULTS PRESENTATION 2017

47

FULL YEAR RESULS PRESENTATION 2016 RESULTS FOR THE YEAR ENDED 30 NOVEMBER 2016 HALF YEAR RESULTS PRESENTATION 2017 RESULTS FOR THE SIX MONTHS ENDED 31 MAY 2017

Transcript of HALF YEAR RESULTS PRESENTATION 2017

FULL YEAR RESULS PRESENTATION 2016

RESULTS FOR THE YEAR ENDED 30 NOVEMBER 2016

HALF YEAR RESULTSPRESENTATION 2017

RESULTS FOR THE SIX MONTHS ENDED 31 MAY 2017

2

2017 Overview

• Encouraging first half performance with accelerated momentum in Q2

• Adjusted operating profit +26% to £19.3m (+5%* at constant currency and +8%* excluding innovation spend)

• GP up 2%* YoY and up 12% on a reported basis

• 80% of GP now generated outside UK&I (FY 2016: 75%)

• Contract GP up 8%* YoY against strong comparatives (+11%* YoY in H1 2016)

• Contract now accounts for 70% of Group GP (FY 2016: 67%)

• Permanent productivity improved by 8%* YoY, with GP down 10%* YoY

• USA our second largest region for the first time (22% of Group GP)

• Adjusted basic EPS up 29% YoY

• Net cash £5.2m (H1 2016: net debt £4.4m)

• Interim dividend maintained

* Growth is at constant currency

H1 2017 YTD Innovation spend £0.6m

3

FINANCIAL RESULTS

4

FINANCIAL HIGHLIGHTS

*Growth is at constant currency, on an adjusted basis

Note 1: Conversion ratio = operating profit expressed as a % of gross profit

Note 2: 2016 figures are adjusted for the impact of £2.3m of costs in relation to the restructuring of certain sales businesses and central support functions

As Reported Adjusted As Reported Adjusted Adjusted

HY 2017 HY 2016 HY 2016 Actual Growth CC Growth*

Revenue £521.0m £443.5m £443.5m +17% +7%

Contract gross profit £94.2m £79.7m £79.7m +18% +8%

Permanent gross profit £40.2m £40.1m £40.1m - -10%

Total gross profit £134.4m £119.8m £119.8m +12% +2%

Operating profit £19.3m £15.3m £13.0m +26% +5%

Conversion ratio 14.4% 12.8% 10.9% +1.6%pts +0.3%pts

Net finance expense (£0.2m) (£0.2m) (£0.2m)

Profit before tax £19.2m £15.1m £12.8m +27% +5%

Taxation (£5.0m) (£4.1m) (£3.5m)

Profit after tax £14.2m £11.0m £9.3m +29% +6%

Basic earnings per share 11.0p 8.6p 7.3p +29% +6%

Interim dividend per share 4.7p 4.7p 4.7p - -

Net cash £5.2m (£4.4m) (£4.4m)

5

BALANCE SHEET

Robust Balance Sheet

£50m revolving credit facility with HSBC and Citibank, which is committed to 2019

A seasonal reduction in net cash

30 May 30 November

2017 2016

Intangible assets £11.6m £11.6m

Property, plant & equipment £6.7m £7.1m

Investments £0.7m £0.7m

Deferred tax assets £2.7m £2.5m

Net working capital £51.2m £50.3m

Provisions (£5.3m) (£5.8m)

Net current tax liabilities (£2.5m) (£0.7m)

£65.1m £65.7m

Net cash £5.2m £10.0m

Net assets £70.3m £75.7m

6

CASH FLOW BRIDGE

Seasonal outflow of working capital, along with treasury share purchases, lead to a net cash outflow

YE 2016 Net

Cash

Operating

profit

Depn and

amort

Share

awards

Share

transactions

Exceptional

/ adjusted

items

Foreign

exchange

Treasury

shares

purchased

Capex &

Prepaid

investment

Taxes and

interest

Dividends Working

capital

HY 2017 net

cash

£10.0m

£19.3m£2.9m

£1.4m£0.1m

(£0.1m)

(£0.3m)

(£3.4m)

(£3.4m)

(£3.6m)

(£6.0m)

(£11.7m)

£5.2m

7

EARNINGS PER SHARE AND DIVIDENDS

Note 1: 2016 figures are adjusted for the impact of £2.3m of costs in relation to the restricting of certain sales businesses and central support function

Adjusted EPS up 29% and dividends maintained YoY

As Reported Adjusted As Reported Adjusted As Reported

HY 2017 HY 2016 HY 2016 Actual Growth Actual Growth

Profit after tax £14.2m £11.0m £9.3m +29% +53%

For basic EPS 128.7m 128.5m 128.5m - -

Dilutive impact of share plans 4.7m 5.0m 5.0m

Fully diluted EPS 133.4m 133.5m 133.5m - -

Basic 11.0p 8.6p 7.3p +29% +51%

Diluted 10.6p 8.2p 7.0p +29% +51%

DPS Interim Ordinary 4.7p 4.7p 4.7p - -

Weighted

average

number of

shares

EPS

8

FOREIGN EXCHANGE IMPACT

For HY 2017, currency movements versus Sterling provided a strong tailwind for the reported performance of the Group with the highest impact coming from Eurozone countries. The exchange rate

movements increased our HY 2017 reported GP and operating profit by circa £12.7m and £3.3m, respectively.

Average Closing Average Closing Average Closing

EUR € 1.18 1.15 1.32 1.31 +10.7% +12.8%

USD $ 1.25 1.29 1.45 1.46 +13.4% +12.0%

Gross

Profit

Operating

Profit

Gross

Profit

Operating

Profit

EUR € £698k £208k £591k £191k

USD $ £297k £78k £220k £9k

Six months ended Six months ended YoY Exchange

31 May 2017 31 May 2016 Rate Movement

Six months ended Six months ended

31 May 2017 31 May 2016

Impact of a 1% change

9

OPERATING REVIEW

10

2017 PRIORITIES

* Growth is at constant currency

Progress

Strategic investment inContract

• Record contract runners at half-year end

• Fourteenth consecutive quarter of GP growth

• Contract now 70% of GP (FY 2016: 67%)

• Contract represents 64% of sales headcount (FY 2016: 63%), our highest ever

Drive recovery in Permanent productivity

• Successful focus on improving productivity, up 8%* YoY

• Restructure of Permanent business operating model to focus on higher yielding markets and lower

cost delivery

Broaden capabilities in high growth US markets

• GP up 16%* YoY with Contract up 17%* and Permanent up 14%*

• Double digit growth achieved across all sectors except Banking & Finance

• Our second largest region, representing 22% of our Group GP

Accelerate sector diversification in key STEM growth markets

• Strong performances from Life Sciences, Energy, Engineering and ICT (predominantly Continental

Europe)

• Exciting ICT opportunities outside UK and Europe

Build scale and critical mass in global network

• Growth driven by increased returns from existing locations

• New office opened in Vienna

Focus on costs and efficiencies to improve operational gearing

• On going review of support infrastructure and tight control of costs

• Improving productivity per sales head (Contract and Permanent), up 9%* YoY

DIVISION

DIVERSIFICATION

GEOGRAPHICAL

DIVERSIFICATION

SECTOR

DIVERSIFICATION

70%

30%

Cont

Perm

67%

33%

Cont

Perm

20%

51%

22%

7%

25%

49%

20%

6%

UK&IC EuropeUSAAPAC & ME

44%

15%

9%

9%

21%

2%

45%

16%

8%

9%

21%

1%

ICT

Banking & Finance

Energy

Engineering

Life Sciences

Other

11

BUSINESS PROFILE

HY 2017 HY 2017 HY 2017

FY 2016FY 2016FY 2016

12

CONTRACT / PERMANENT GROSS PROFIT ANALYSIS

HY 2017

FY 2016

Continued focus on growth in Contract across all regions and sectors

DIVISION GEOGRAPHY SECTOR

70%

30%

Cont

Perm

79%70% 68%

53%

21%30% 32%

47%

UK&I C Europe USA APAC & ME

Cont Perm

74%

55%

92%

72%64%

26%

45%

8%

28%36%

ICT Banking &

Finance

Energy Engineering Life Sciences

Cont Perm

67%

33%

Cont

Perm

77%66% 67%

39%

23%34% 33%

61%

UK&I C Europe USA APAC & ME

Cont Perm

73%

52%

92%

65% 60%

27%

48%

8%

35% 40%

ICT Banking &

Finance

Energy Engineering Life Sciences

Cont Perm

CONTRACT

RUNNERS

GROSS

PROFIT PER

DAY RATE

4,157 4,359 4,692 5,1225,791

7,5738,412

9,078 9,249

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 HY17

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 HY17

13

KEY PERFORMANCE INDICATORS: CONTRACT

* Growth is at constant currency

Note 1: All numbers are period end

Note 2: Contractors are those on placement with one of the Group’s clients at the end of

the relevant period

Note 3: The average gross profit per day per contractor is calculated by taking the period

end Total Runner Weekly Gross Profit position, divided by the period end number of

active contractors, divided by 5 (assuming a 5 day working week)

Contract margin %

HY 2017 19.6%HY 2016 19.8%

+5% vs

FY09

+8% vs

FY10

+9% vs

FY11

+13% vs

FY12

+31% vs

FY13

+11% vs

FY14

+8% vs

FY15

-1%* vs

FY09

+4%* vs

FY10

-2%* vs

FY11

-5%* vs

FY12

0%* vs

FY13

+3%* vs

FY14

-1%* vs

FY15

Contract runners up 81% vs 2012

+2% vs

FY16

+12% vs

HY16

-3%* vs

FY16

-3%* vs

HY16

14

CONTRACT RUNNERS – COMPARISON TO PRIOR YEARS

A record number of runners, with a strong seasonal recovery

Note 1: Growth in 2014 was largely driven by strong penetration of a buoyant Energy market

112%

131%

111%

108%103%

90%

95%

100%

105%

110%

115%

120%

125%

130%

135%

November December January February March April May June July August September October November

2013 2014 2015 2016 2017

PERMANENT

PLACEMENT

VOLUMES

PERMANENT

AVERAGE FEE

6,0606,551

7,434 7,343

6,429 6,601 6,4085,731

2,443

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 HY17

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 HY17

15

KEY PERFORMANCE INDICATORS: PERMANENT

* Growth is at constant currency

Note 1: 2013 data is based on a normalised 52 week period

Note 2: 2014 data is adjusted due to timing of period ends (an additional 45 placements in

Germany)

Note 3: The average permanent placement fee is calculated using the total placement

fees for the relevant period, divided by the number of placements for the period

Note 4: This analysis excludes retained business

+8% vs

FY09

+13% vs

FY10

-1% vs

FY11

-12% vs

FY12

+3% vs

FY13

-3% vs

FY14

+1%* vs

FY09

+6%* vs

FY10

+4%* vs

FY11

0%* vs

FY12

+1%* vs

FY13

+3%* vs

FY14

+1%* vs

FY15

Placement volumes down 16% YoY

Average fee up 3%* YoY

Permanent focus is on productivity and moving up the food chain.The decrease is broadly in line with the 17% decrease in Permanent average headcount.

-11% vs

FY15

-16% vs

HY16

+1%* vs

FY16

+3%* vs

HY16

16

GEOGRAPHICAL GROSS PROFIT ANALYSIS

* Growth is at constant currency

GEOGRAPHICAL

DIVERSIFICATION

ASIA PACIFIC &

MIDDLE EAST

GROSS PROFIT

GROWTH /

(DECLINE) BY

REGION*

HY 2017 HY 2016

HY 2017 FY 2016

(16%)

8%12%

5%

16%

(4%)

UK&I

Benelux

France

Germany

USA

APAC & ME

(5%)

15%

7%

22%

6%

(15%)

20%

19%

5%27%

22%

7%UK&I

Benelux

France

Germany

USA

APAC & ME

25%

17%

5%27%

20%

6%

34%

43%

23%

Australia

Asia

Middle East

32%

48%

20%

17

SECTOR GROSS PROFIT ANALYSIS

* Growth is at constant currency

SECTORAL

DIVERSIFICATION

GROSS PROFIT

GROWTH /

(DECLINE) BY

SECTOR*

HY 2017 HY 2016

HY 2017 FY 2016

1%

(5%)

7%

1%

6%

9%

ICT

Banking & Finance

Energy

Engineering

Life Sciences

Other

18%

(5%)

(31%)

10%12% 11%

44%

15%

9%

9%

21%

ICT

Banking &

FinanceEnergy

Engineering

Life

SciencesOther

45%

16%

8%

9%

21%

1%2%

18

INNOVATION

• Helps to future-proof the company and generate new revenue streams

• Innovation system & governance structure set up

• Invested $2m in three third party start-ups:

• Contractor platform targeting healthcare recruitment and other large vertical markets• Bot messaging platform• HR tech / recruitment incubator

• Currently rolling out a new video CV platform for candidates

• Talent platform to go live in Q3, addressing Permanent & Contract requirements

• Expect to spend circa £2m on Innovation operating expenses this year (H1: £0.6m)

• We will provide a deeper dive into our Innovation agenda at the Capital Markets Day on 15 November 2017

19

OUTLOOK

• Encouraged by the improvement in momentum across the business in the period

• Continuing to build further momentum in the more resilient Contract market • 70% of Group GP (2012: 50%)• 64% of sales headcount (2012: 44%)• 81% increase in Contract runners since 2012

• Ongoing focus on productivity in Permanent

• FX tailwind expected to be less material from H2

• Heightened level of political and economic uncertainty expected to remain a feature

• Sectorally and geographically diverse and agile, with 80% of Group GP generated outside of the UK

* Growth is at constant currency

20

FINANCIAL CALENDAR

201715 September Q3 Interim Management Statement

2 November Ex-dividend date for 2017 interim dividend

15 November Capital markets day

30 November 2017 Financial Year end

8 December 2017 Interim dividend paid

15 December Trading update for the year ended 30 November 2017

201829 January Annual results for the year ended 30 November 2017

21

SUPPLEMENTARY MATERIAL

22

GROSS PROFIT PERFORMANCE BY REGION

Note 1: GP Growth is at constant currency

Contract GP up 8%* YoY against strong prior year comparatives (H1 2016 up 11%* YoY)

GP Growth YoY YTD 17 Sales FTE HC (SL1-SL5) Growth YoY

Cont Perm Total Cont / Perm Mix Cont Perm Total

Q1 17 -13% -37% -19% Q1 17 -12% -27% -18%

Q2 17 -14% -11% -14% Q2 17 -15% -22% -17%

HY17 -14% -25% -16% HY17 -14% -24% -17%

Q1 17 +17% -11% +7% Q1 17 +15% -9% +5%

Q2 17 +15% -8% +7% Q2 17 +20% -9% +8%

HY17 +16% -9% +7% HY17 +17% -9% +6%

Q1 17 +11% +16% +12% Q1 17 -17% -28% -21%

Q2 17 +23% +13% +20% Q2 17 -19% -17% -18%

HY17 +17% +14% +16% HY17 -18% -23% -20%

Q1 17 +11% -30% -14% Q1 17 -4% -22% -17%

Q2 17 +54% -22% +5% Q2 17 -12% -19% -17%

HY17 +31% -26% -4% HY17 -8% -21% -17%

Q1 17 +7% -14% - Q1 17 -1% -18% -8%

Q2 17 +9% -6% +4% Q2 17 - -15% -6%

HY17 +8% -10% +2% HY17 - -17% -7%

Cont79%

Perm21%

Cont68%

Perm32%

Cont53%

Perm47%

UK&I

USA

APAC & MENA

20% of

Group

22% of

Group

7% of

group

Cont70%

Perm30%

GROUP

Cont70%

Perm30%

C Europe51% of

group

23

GROSS PROFIT PERFORMANCE BY SECTOR

Note 1: GP Growth is at constant currency

Growth across all sectors with the exception of Banking and Finance

GP Growth YoY YTD 17 Sales FTE HC (SL1-SL5) Growth YoY

Cont Perm Total Cont / Perm Mix Cont Perm Total

Q1 17 +7% -10% +2% Q1 17 - -14% -5%

Q2 17 +3% -6% +1% Q2 17 - -14% -5%

HY17 +5% -8% +1% HY17 +0% -14% -5%

Q1 17 -5% -12% -8% Q1 17 -1% -20% -11%

Q2 17 +3% -6% -1% Q2 17 -9% -18% -14%

HY17 -1% -9% -5% HY17 -5% -19% -13%

Q1 17 +22% -34% -1% Q1 17 +6% -28% -10%

Q2 17 +14% -17% +3% Q2 17 +15% -17% +1%

HY17 +17% -26% +1% HY17 +10% -23% -5%

Q1 17 +17% -13% +4% Q1 17 +3% -17% -7%

Q2 17 +12% - +7% Q2 17 +2% -9% -3%

HY17 +15% -7% +6% HY17 +3% -13% -5%

Q1 17 +7% -14% - Q1 17 -1% -18% -8%

Q2 17 +9% -6% +4% Q2 17 - -15% -6%

HY17 +8% -10% +2% HY17 - -17% -7%

Cont74%

Perm26%

Cont72%

Perm28%

Cont64%

Perm36%

ICT

ENGINEERING

LIFE SCIENCES

44% of

Group

9% of

Group

21% of

group

Cont70%

Perm30%

GROUP

Cont55%

Perm45%

BANKING &

FINANCE15% of

group

24

GROSS PROFIT PERFORMANCE BY REGION 2016

Note 1: GP Growth is at constant currency

GP Growth YoY YTD 16 Sales FTE HC (SL1-SL5) Growth YoY

Cont Perm Total Cont / Perm Mix Cont Perm Total

Q1 16 -1% +2% - Q1 16 +5% -10% -1%

Q2 16 - -31% -9% Q2 16 +9% -15% -

HY16 -1% -17% -5% HY16 +7% -12% -1%

Q1 16 +17% +25% +20% Q1 16 +14% +1% +8%

Q2 16 +20% +8% +16% Q2 16 +13% +4% +9%

HY16 +19% +16% +18% HY16 +13% +3% +9%

Q1 16 +20% +2% +14% Q1 16 +61% -1% +32%

Q2 16 +10% -15% - Q2 16 +53% -18% +20%

HY16 +15% -8% +6% HY16 +57% -9% +26%

Q1 16 +3% -21% -13% Q1 16 -4% -24% -19%

Q2 16 +3% -27% -18% Q2 16 +6% -15% -9%

HY16 +3% -24% -15% HY16 +1% -20% -14%

Q1 16 +11% +9% +10% Q1 16 +16% -6% +6%

Q2 16 +10% -12% +2% Q2 16 +17% -7% +6%

HY16 +11% -2% +6% HY16 +17% -7% +6%

Cont76%

Perm24%

Cont67%

Perm33%

Cont39%Perm

61%

UK&I

USA

APAC & MENA

27% of

Group

19% of

Group

6% of

group

Cont67%

Perm33%

GROUP

Cont65%

Perm35%

C Europe48% of

group

25

GROSS PROFIT PERFORMANCE BY SECTOR 2016

Note 1: GP Growth is at constant currency

GP Growth YoY YTD 16 Sales FTE HC (SL1-SL5) Growth YoY

Cont Perm Total Cont / Perm Mix Cont Perm Total

Q1 16 +21% +17% +20% Q1 16 +24% +13% +20%

Q2 16 +20% +6% +15% Q2 16 +23% +9% +18%

HY16 +20% +11% +18% HY16 +24% +11% +19%

Q1 16 +12% - +6% Q1 16 +11% -5% +1%

Q2 16 -3% -24% -14% Q2 16 +14% -3% +4%

HY16 +4% -14% -5% HY16 +12% -4% +3%

Q1 16 - +77% +21% Q1 16 +6% - +3%

Q2 16 +7% -10% +1% Q2 16 +10% -13% -1%

HY16 +4% +22% +10% HY16 +8% -6% +1%

Q1 16 +9% +35% +19% Q1 16 +38% +19% +28%

Q2 16 +11% +1% +7% Q2 16 +34% +6% +19%

HY16 +10% +16% +12% HY16 +36% +13% +23%

Q1 16 +11% +9% +10% Q1 16 +16% -6% +6%

Q2 16 +10% -12% +2% Q2 16 +17% -7% +6%

HY16 +11% -2% +6% HY16 +17% -7% +6%

Cont72%

Perm28%

Cont63%

Perm37%

Cont59%Perm

41%

ICT

ENGINEERING

LIFE SCIENCES

45% of

Group

9% of

Group

20% of

group

Cont67%

Perm33%

GROUP

Cont53%

Perm47%

BANKING &

FINANCE16% of

group

26

UK&I TRADING METRICS

Note 1: Growth is at constant currency

Note 2: Office count includes corporate function offices

20% of Group

GP

HY GROSS PROFIT GROWTH YoY

Q1 Q2 H1 MAY 17 8

Contract -13% -14% -14% MAY 16 13

YoY -5

Permanent -37% -11% -25%

NOV 16 10

Total -19% -14% -16% vs Year End -2

OFFICES

DIVISION MIX SECTOR MIX HY 2017 SECTOR MIX FY 2016

Outside HY 2017; inside FY 2016

77%

23%

79%

21%

Cont

Perm59%

14%

12%

11%

2% ICT

Banking &

FinanceEnergy

Engineering

Life Sciences

Other

60%15%

3%

10%

10%

2%

UK

Ireland

2%

27

UK&I TRADING METRICS

* Excluding retained business

1 At constant currency

Cont Perm Total YoY vs Year End

YoY -16% -19% -17% -6% -6%

YoY -14% -24% -17% -5% -4% Below +2% +1% Below

YoY

vs FY

16

vs

Group

PERMANENT

SALES HEADCOUNT PROFIT PER DAY RATE1 PLACEMENT FEE*1

Cont Perm Total YoY

vs Year

End

vs

Group

CONTRACT GROSS

vs Year

End -8% -4% -7%

AVERAGE

-29%

PERIOD END CONTRACT PERMANENT

SALES HEADCOUNT RUNNERS PLACEMENTS*

YoY

495

159

336

HY 17

Cont Perm Total

503

160

343

HY 17

Cont Perm Total

2,663

2,680

2,515

FY

16

HY

16

HY

17

751

534

HY

16

HY

17

FY

16

HY

16

HY

17

FY

16

HY

16

HY

17

28

BENELUX TRADING METRICS

Note 1: Growth is at constant currency

Note 2: Office count includes corporate function offices

19% of Group

GP

HY GROSS PROFIT GROWTH YoY

Q1 Q2 H1 MAY 17 6

Contract +16% +19% +18% MAY 16 7

YoY -1

Permanent -18% -18% -18%

NOV 16 6

Total +6% +10% +8% vs Year End 0

OFFICES

DIVISION MIX SECTOR MIX HY 2017 SECTOR MIX FY 2016

Outside HY 2017; inside FY 2016

74%

26%

79%

21%

Cont

Perm 50%

13%

12%

11%

7%7%

ICT

Banking &

FinanceEnergy

Engineering

Life Sciences

Other

50%

13%

11%

12%

6%8%

Bel Lux

Neth

29

BENELUX TRADING METRICS

* Excluding retained business

1 At constant currency

Cont Perm Total YoY vs Year End

YoY +25% -23% +8% +26% +6%

YoY +20% -22% +5% -3% -2% Below +5% +3% Below

-22%

PERIOD END CONTRACT PERMANENT

SALES HEADCOUNT RUNNERS PLACEMENTS*

YoY

vs Year

End +16% -15% +6%

AVERAGE

YoY

vs FY

16

vs

Group

PERMANENT

SALES HEADCOUNT PROFIT PER DAY RATE1 PLACEMENT FEE*1

Cont Perm Total YoY

vs Year

End

vs

Group

CONTRACT GROSS

397

99

298

HY 17

Cont Perm Total

384

100

285

HY 17

Cont Perm Total

1,970

1,657

2,084

FY

16

HY

16

HY

17

526

411

HY

16

HY

17

FY

16

HY

16

HY

17

FY

16

HY

16

HY

17

30

GERMANY TRADING METRICS

Note 1: Growth is at constant currency

Note 2: Office count includes corporate function offices

27% of Group

GP

HY GROSS PROFIT GROWTH YoY

Q1 Q2 H1 MAY 17 8

Contract +16% +10% +13% MAY 16 8

YoY 0

Permanent -7% -5% -6%

NOV 16 8

Total +6% +4% +5% vs Year End 0

DIVISION MIX SECTOR MIX HY 2017 SECTOR MIX FY 2016

OFFICES

Outside HY 2017; inside FY 2016

60%

40%

62%

38%Cont

Perm57%

6%

3%

14%

20%

ICT

Banking &

FinanceEnergy

Engineering

Life Sciences

Other

52%

7%4%

14%

23%

Germany

Switz

31

GERMANY TRADING METRICS

* Excluding retained business

1 At constant currency

Cont Perm Total YoY vs Year End

YoY +15% +3% +9% +12% +0%

YoY +11% -2% +5% -2% -1% Above -2% -2% Below

CONTRACT PERMANENT

SALES HEADCOUNT RUNNERS PLACEMENTS*

vs Year

End +6% +3% +5%

PERIOD END

vs

Group

AVERAGE CONTRACT GROSS PERMANENT

SALES HEADCOUNT PROFIT PER DAY RATE1 PLACEMENT FEE*1

Cont Perm Total YoY

vs Year

End YoY

vs FY

16

vs

Group

YoY

-10%

585

255

330

HY 17

Cont Perm Total

558

245

313

HY 17

Cont Perm Total

1,971

1,755

1,974

FY

16

HY

16

HY

17

869

786

HY

16

HY

17

FY

16

HY

16

HY

17

FY

16

HY

16

HY

17

32

FRANCE TRADING METRICS

Note 1: Growth is at constant currency

Note 2: Office count includes corporate function offices

5% of Group

GP

HY GROSS PROFIT GROWTH YoY

Q1 Q2 H1 MAY 17 2

Contract +21% +20% +21% MAY 16 1

YoY 1

Permanent -16% +5% -7%

NOV 16 1

Total +9% +16% +12% vs Year End 1

Outside HY 2017; inside FY 2016

DIVISION MIX SECTOR MIX HY 2017 SECTOR MIX FY 2016

OFFICES

72%

28%

76%

24%

Cont

Perm 49%

21%

9%

4%

17%

ICT

Banking &

FinanceEnergy

Engineering

Life Sciences

Other

50%

19%

8%

7%

16%

France

33

FRANCE TRADING METRICS

* Excluding retained business

1 At constant currency

Cont Perm Total YoY vs Year End

YoY +45% -13% +25% +19% +1%

YoY +35% -15% +17% +5% +5% Below +9% +5% Below

CONTRACT PERMANENT

SALES HEADCOUNT RUNNERS PLACEMENTS*

vs Year

End +23% -9% +13%

PERIOD END

vs

Group

AVERAGE CONTRACT GROSS PERMANENT

SALES HEADCOUNT PROFIT PER DAY RATE1 PLACEMENT FEE*1

Cont Perm Total YoY

vs Year

End YoY

vs FY

16

vs

Group

YoY

-35%

129

32

97

HY 17

Cont Perm Total

118

32

86

HY 17

Cont Perm Total

631

536

640

FY

16

HY

16

HY

17

139

91

HY

16

HY

17

FY

16

HY

16

HY

17

FY

16

HY

16

HY

17

34

USA TRADING METRICS

Note 1: Growth is at constant currency

Note 2: Office count includes corporate function offices

22% of Group

GP

HY GROSS PROFIT GROWTH YoY

Q1 Q2 H1 MAY 17 8

Contract +11% +23% +17% MAY 16 8

YoY 0

Permanent +16% +13% +14%

NOV 16 8

Total +12% +20% +16% vs Year End 0

DIVISION MIX SECTOR MIX HY 2017 SECTOR MIX FY 2016

OFFICES

Outside HY 2017; inside FY 2016

67%

33%

68%

32%

Cont

Perm

14%

23%

14%

48%

ICT

Banking &

FinanceEnergy

Engineering

Life Sciences

Other

15%

25%

11%

49%

USA

35

USA TRADING METRICS

Cont Perm Total YoY vs Year End

YoY -15% -13% -14% +23% +14%

YoY -18% -23% -20% -10% -12% Above -5% -10% Above

YoY

vs FY

16

vs

GroupCont Perm Total YoY

vs Year

End

vs

Group

AVERAGE CONTRACT GROSS PERMANENT

SALES HEADCOUNT PROFIT PER DAY RATE1 PLACEMENT FEE*1

YoY

+22%

vs Year

End -4% -1% -3%

PERIOD END CONTRACT PERMANENT

SALES HEADCOUNT RUNNERS PLACEMENTS*

299

97

202

HY 17

Cont Perm Total

300

97

203

HY 17

Cont Perm Total

1,363

1,262

1,549

FY

16

HY

16

HY

17

321

392

HY

16

HY

17

FY

16

HY

16

HY

17

FY

16

HY

16

HY

17

* Excluding retained business

1 At constant currency

HY GROSS PROFIT GROWTH YoY

Q1 Q2 H1 MAY 17 6

Contract +11% +54% +31% MAY 16 6

YoY 0

Permanent -30% -22% -26%

NOV 16 6

Total -14% +5% -4% vs Year End 0

Outside HY 2017; inside FY 2016

DIVISION MIX SECTOR MIX HY 2017 SECTOR MIX FY 2016

OFFICES

39%

61%53%

47%Cont

Perm

29%

37%

21%

13%

ICT

Banking &

FinanceEnergy

Engineering

Life Sciences

Other

29%

36%

17%

2% 16%

Australia

Singapore

Japan

Hong Kong

MENA

2%1%

1%1%

2%

36

ASIA PACIFIC & MIDDLE EAST TRADING METRICS

Note 1: Growth is at constant currency

Note 2: Office count includes corporate function offices

7% of Group

GP

37

ASIA PACIFIC & MIDDLE EAST TRADING METRICS

Cont Perm Total YoY vs Year End

YoY -9% -21% -17% +25% +1%

YoY -8% -21% -17% -7% -5% Below -3% -2% Above

YoY

vs FY

16

vs

GroupCont Perm Total YoY

vs Year

End

vs

Group

AVERAGE CONTRACT GROSS PERMANENT

SALES HEADCOUNT PROFIT PER DAY RATE1 PLACEMENT FEE*1

YoY

-25%

vs Year

End +5% -5% -1%

PERIOD END CONTRACT PERMANENT

SALES HEADCOUNT RUNNERS PLACEMENTS*

161

99

62

HY 17

Cont Perm Total

159

101

58

HY 17

Cont Perm Total

480

391

487

FY

16

HY

16

HY

17

305

229

HY

16

HY

17

FY

16

HY

16

HY

17

FY

16

HY

16

HY

17

* Excluding retained business

1 At constant currency

38

SECTOR GROSS PROFIT ANALYSISICT BY REGION BANKING & FINANCE BY REGION

GROUP BY SECTOR

ENGINEERING BY REGION LIFE SCIENCES BY REGION

ALL CHARTS: Outside HY 2017; Inside FY 2016

45%

16%

8%

9%

21%

44%

15%

9%

9%

21%

2%

ICT

Banking & Finance

Energy

Engineering

Life Sciences

Other

33%

19%6%

32%

6%27%

21%

6%

35%

7%4%

23%

14%

6%11%

31%

15%

19%

15%

7%

11%

33%

15%

12%5%

29%

45%

5%

10%

6%

4%

26%

50%

4%

27%

23%

44%

28%

23%

2%

44%

2%

UK&I Benelux France DACH USA APAC & ME

39

ENERGY - GROUP

* Growth is at constant currency

Note 1: Mix by division, region and stream is based on gross profit

An improved performance in Energy with GP up 7%* YoY, driven by onshore fracking

Cont Perm Total

Q1 17 -10% +1% -8%

Q2 17 +29% -35% +23%

HY 17 +9% -15% +7%

Cont Perm Total

Q1 17 -13% -48% -17%

Q2 17 -6% +2% -6%

HY 17 -9% -32% -12%

% of Group Gross Profit YoY Growth Contract Runners

Average Sales Headcount YoY Growth

Outside HY 2017; Inside FY 2016

Mix by Region Mix by Stream Mix by Division

Outside HY 2017; Inside FY 2016 Outside HY 2017; Inside FY 2016 Outside HY 2017; Inside FY 2016

8%

9%

92%

8%

92%

8%

Cont

Perm

10%

46%29%

15%

5%

42%

37%

16% UK&I

C Europe

USA

APAC & ME

24%

15%

40%

21%29%

20%20%

31%

Upstream

Midstream

Downstream

Power &

Renewables

1,0

78

1,0

34

92

0

96

4

1,0

06

1,0

46

1,1

16

1,3

42

Q3

2015

Q4

2015

Q1

2016

Q2

2016

Q3

2016

Q4

2016

Q1

2017

Q2

2017

FY GP £213.6m £167.8m £162.4m £189.5m £199.5m £192.8m £218.2m £235.7m £258.7m

GROSS

PROFIT

CONTRACT

GROSS

MARGIN

£99.7m £91.6m £72.5m £87.3m £97.1m £91.6m £100.8m £110.5m £119.8m £134.4m

£113.9m£76.2m

£89.8m£102.2m £102.4m £101.2m

£117.4m£125.2m

£138.9m

£0m

£50m

£100m

£150m

£200m

£250m

£300m

2008 2009 2010 2011 2012 2013 2014 2015 2016 HY 2017

H1 H2

21.5% 22.1% 21.6% 21.4% 21.5%20.2% 20.0% 19.8% 19.9% 19.6%

2008 2009 2010 2011 2012 2013 2014 2015 2016 HY 2017

40

HISTORICAL GROSS PROFIT & GROSS MARGIN

Note 1: 2013 data is based on a normalised 52 week period

Our strongest HY performance for GP

Contract gross margin % remained relatively flat despite difficult trading conditions

FY OP

ADJUSTED

OPERATING

PROFIT

before

exceptional

items

CONVERSION

RATIO

adjusted

operating

profit before

exceptional

items as a %

of gross profit

£24.4m

£11.0m £7.1m £11.0m £9.1m £6.7m £8.4m£14.1m £15.3m £19.3m

£32.4m

£7.0m £14.1m

£19.0m£16.0m

£14.3m£21.4m

£27.4m £26.0m

£0m

£10m

£20m

£30m

£40m

£50m

£60m

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

H1 H2

23

.8%

11

.8%

9.6

%

12

.2%

9.2

%

7.1

%

8.3

%

12

.8%

12

.8%

14

.4%

25

.9%

10

.5%

12

.8%

15

.3%

12

.2%

10

.9%

13

.7%

17

.6%

16

.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

HY FY

£56.8m £18.0m £21.2m £30.0m £25.1m £21.0m £29.8m £41.5m £41.3m

41

HISTORICAL OPERATING PROFIT & CONVERSION RATIO

Note 1: Includes data for IT Job Board up to 2011

Note 2: 2013 data is based on a normalised 52 week period

Note 3: 2013, 2014 and 2015 are before exceptional items

Note 4: 2015 figures were adjusted for the impact of £3.1m of costs in relation to restructuring Energy business and the impairment of IT assets

Note 5: 2016 figures are adjusted for the impact of £3.5m of costs in relation to the restricting of certain sales businesses and central support function

42

HEADCOUNT

Note 1: Headcount is now based on full time equivalent heads. This is a change from prior years.

Note 2: Sales heads include consultants and sales management

May 09 Nov 09 May 10 Nov 10 May 11 Nov 11 May 12 Nov 12 May 13 Nov 13 May 14 Nov 14 May 15 Nov 15 May 16 Nov 16 May 17

Period End

Total Heads1,511 1,461 1,638 1,719 1,865 2,109 2,100 2,021 2,125 2,232 2,484 2,483 2,571 2,752 2,712 2,590 2,642

Period End

Sales Heads1,111 1,051 1,181 1,204 1,351 1,610 1,620 1,568 1,667 1,797 2,015 2,016 2,051 2,185 2,142 2,044 2,064

524 459 474 484 519 564 507 459 477 497 538 541 553 579 550 490 457

587592

707 720832

1,046 1,1131,109

1,1901,300

1,477 1,475 1,4981,606 1,592

1,554 1,607

May 09 Nov 09 May 10 Nov 10 May 11 Nov 11 May 12 Nov 12 May 13 Nov 13 May 14 Nov 14 May 15 Nov 15 May 16 Nov 16 May-17

UK Sales Heads Int'l Sales Heads

43

SALES HEADCOUNT

Note 1: Headcount is now based on full time equivalent heads

Note 2: Sales heads include consultants and sales management

May 09 Nov 09 May 10 Nov 10 May 11 Nov 11 May 12 Nov 12 May 13 Nov 13 May 14 Nov 14 May 15 Nov 15 May 16 Nov 16 May 17

Period End

Sales Heads1,111 1,051 1,181 1,204 1,351 1,610 1,620 1,568 1,667 1,797 2,015 2,016 2,051 2,185 2,142 2,044 2,064

461 436 481 458 529623 646 683

824 8941,009 1,067 1,124

1,270 1,299 1,280 1,324

650615

700 746

822

987 974 885

843903

1,006 949927

915 843764 740

May 09 Nov 09 May 10 Nov 10 May 11 Nov 11 May 12 Nov 12 May 13 Nov 13 May 14 Nov 14 May 15 Nov 15 May 16 Nov 16 May 17

Contract Sales Heads Permanent Sales Heads

44

CASH FLOW

Note 1: Cash conversion ratio is calculated as net cash generated from operations less capital expenditure, stated as a % of operating profit before exceptional items / adjustments, and is a

measure of the Group’s ability to convert profit into cash

Note 2: 2016 figures are adjusted for the impact of £2.3m of costs in relation to the restricting of certain sales businesses and central support function

Seasonal working capital outflow

Purchased to settle share-based payments

Strong cash conversion

As Reported Adjusted As Reported

HY 2017 HY 2016 HY 2016

Operating profit before exceptional items £19.3m £15.3m £13.0m

Depreciation, amortisation and impairments £2.9m £2.8m £2.8m

Share awards charge and other non cash items £1.4m £1.7m £1.7m

Increase in receivables (£2.7m) (£1.9m) (£1.9m)

Decrease in payables and provisions (£9.0m) (£13.4m) (£11.8m)

Net cash generated from operations £11.9m £4.5m £3.8m

Taxation paid (£3.4m) (£2.4m) (£2.4m)

Capital expenditure (£2.6m) (£4.0m) (£4.0m)

Prepaid investment (£0.8m) - -

Net finance expense (£0.2m) (£0.2m) (£0.2m)

Dividends paid (£6.0m) (£6.0m) (£6.0m)

Treasury shares purchased (£3.4m) (£4.6m) (£4.6m)

Tracker shares and share option related transactions £0.1m £0.6m £0.6m

FX movement (£0.3m) £2.8m £2.8m

Movement in net (debt) / cash (£4.7m) (£9.3m) (£10.0m)

Cash outflow from previously recognised exceptional items (£0.1m) (£0.6m) (£0.6m)

Cash outflow from 2015 and 2016 restructuring - (£0.7m) -

Movement in net (debt) / cash after adjustments (£4.8m) (£10.6m) (£10.6m)

Cash conversion ratio 48% 3% (2%)

79%

6%

2%6%

7%

Payroll Property Advertising IT & Professional Other

16%

84%

Support Services Sales

45

COST BASE ANALYSIS

Note 1: Based on costs for FY 2016

The Group has maintained its flexible cost base

Cost Base

Payroll Costs

46

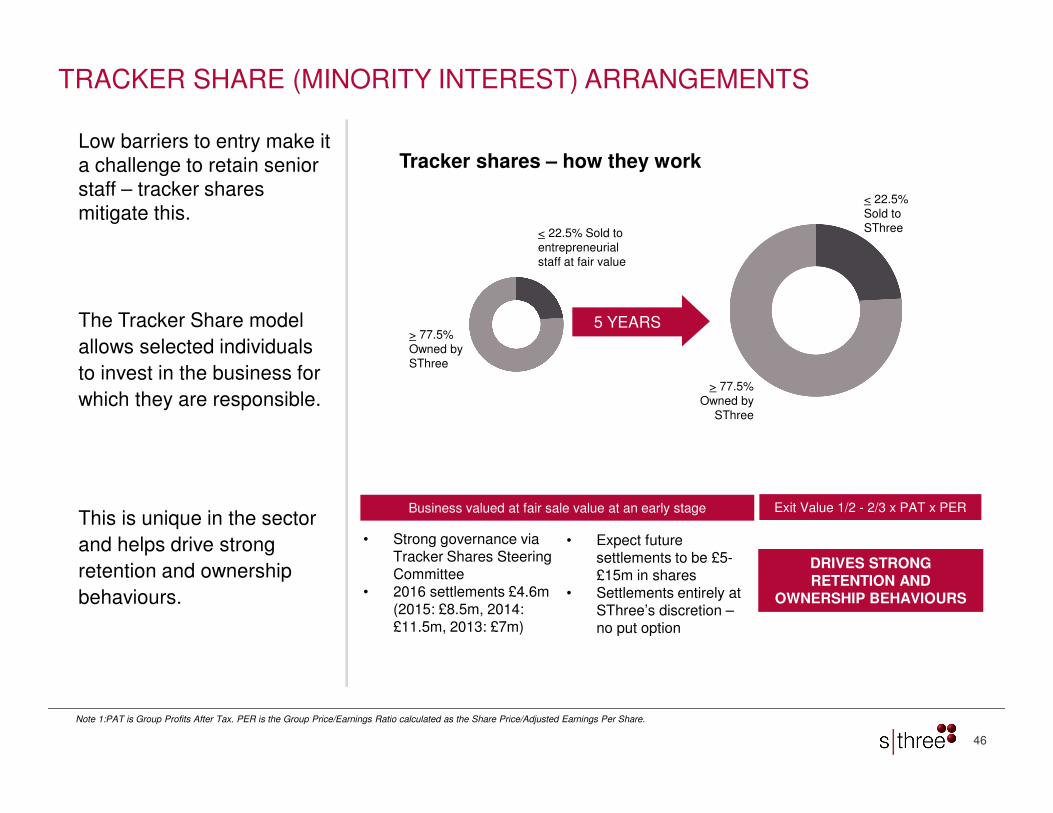

TRACKER SHARE (MINORITY INTEREST) ARRANGEMENTS

Low barriers to entry make it a challenge to retain senior staff – tracker shares mitigate this.

The Tracker Share model

allows selected individuals

to invest in the business for

which they are responsible.

This is unique in the sector

and helps drive strong

retention and ownership

behaviours.

Tracker shares – how they work

> 77.5% Owned by SThree

< 22.5% Sold toentrepreneurialstaff at fair value

< 22.5% Sold toSThree

> 77.5% Owned by

SThree

5 YEARS

• Strong governance via Tracker Shares Steering Committee

• 2016 settlements £4.6m (2015: £8.5m, 2014: £11.5m, 2013: £7m)

• Expect future settlements to be £5-£15m in shares

• Settlements entirely at SThree’s discretion –no put option

DRIVES STRONG RETENTION AND

OWNERSHIP BEHAVIOURS

Exit Value 1/2 - 2/3 x PAT x PERBusiness valued at fair sale value at an early stage

Note 1:PAT is Group Profits After Tax. PER is the Group Price/Earnings Ratio calculated as the Share Price/Adjusted Earnings Per Share.

47

39 OFFICES IN 16 COUNTRIES

BELGIUMAntwerpBrussels

FRANCEParisLyon

GERMANYBerlinDüsseldorfFrankfurtMunichHamburgStuttgart

AUSTRIAVienna

LUXEMOURGLuxembourg City

NETHERLANDSAmsterdamRotterdam

SWITZERLANDZurich

USAAustinBostonChicagoHoustonMinneapolisNew YorkSan DiegoSan Francisco

UAEDubai

HONG KONGHong Kong

MALAYSIAKuala Lumpur

SINGAPORESingapore

AUSTRALIASydney

JAPANTokyo

UKBristolBirminghamGlasgowLondonLeedsManchester

IRELANDDublin

Note 1: Austria office opened 1st June 2017