Growing Opportunity -...

47

AUSA Analyst Briefing Welcome Welcome Washington, D.C. October 10, 2006 Growing Opportunity

Transcript of Growing Opportunity -...

AUSAAnalyst Briefing

WelcomeWelcome

Washington, D.C.October 10, 2006

Growing Opportunity

Forward-Looking Information

Certain statements in today's discussion will be forward-looking statements. These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those contained in the statements.

Please see the full disclosure of risk factors and discussion at the end of this presentation.

Agenda•Bell Helicopter

– Mike RedenbaughChief Executive Officer, Bell Helicopter

•Textron Systems

– Dick MillmanPresident, Textron Systems

•Luncheon

•Booth Visit – At Your Leisure Booths 3213 & 3224, Hall C

1

Mike RedenbaughChief Executive Officer

Bell Helicopter

Analyst BriefingOctober 10, 2006

Growing Opportunity

2

Bell Helicopter… Clear Strategy to Become Premier

• Overview:

– Balanced Business/Becoming Premier

– Investing in Talent

– Growth Industry

• Commercial Products

• Military Products

• Customer Support Business

• Managing for Long-Term Growth

Strategic Focus…Key Levers of Value Creation

3

Bell HelicopterInvesting for Growth, Expanding Capacity

• Strong Commercial Aircraft Business

• High Growth in Military Programs

• Becoming the Premier Vertical-Lift Aircraft Manufacturer through Enterprise Management Initiatives

• Superior Product Line: Addressing Voice of the Customer in Quality, Value, Performance, Productivity, Reliability and Safety

• Expanding Customer Support Business

Mission: To Become the World’s Premier Vertical-Lift Aircraft Company

4

Spares

Overhaul & Repair

Technical Data

Support Equipment

Field Services

Training Systems

Depot Maintenance

Bell Helicopter’06 Forecast Revenues: $2.3B

Aircraft~ $925 Million

V-22 - Osprey

AH-1Z – Super Cobra

UH-1Y - Yankee

OH-58D - Kiowa

TH-67 – Trainer

ARH – Armed Recon

Eagle Eye - UAV

206

210

407

412

427

430

Support~ $375 Million

Spares

Huey II

Accessories/Completions

Repair & Overhaul

Rotor Blade Repair

Training Academy

Technical Support

U.S. MilitaryU.S. Military

Installed Base: 2,400 Installed Base: 10,200

Aircraft~ $490 Million

Support~ $510 Million

CommercialCommercial

56%44%

56%44%

Balanced Business...Complementing Each Other

5

Driving Execution –Leadership and Talent

EVP & CFOTony Viotto

EVP Integrated OperationsJohn Bean

EVP ProgramsMike Blake

Leadership / Organizational Design Essential Part of Strategy to Achieve Mission

CEOMike Redenbaugh

Talent Additions Last Three Years• Over 100 Industry Leaders• Over 1100 Engineering & Manufacturing Professionals

6

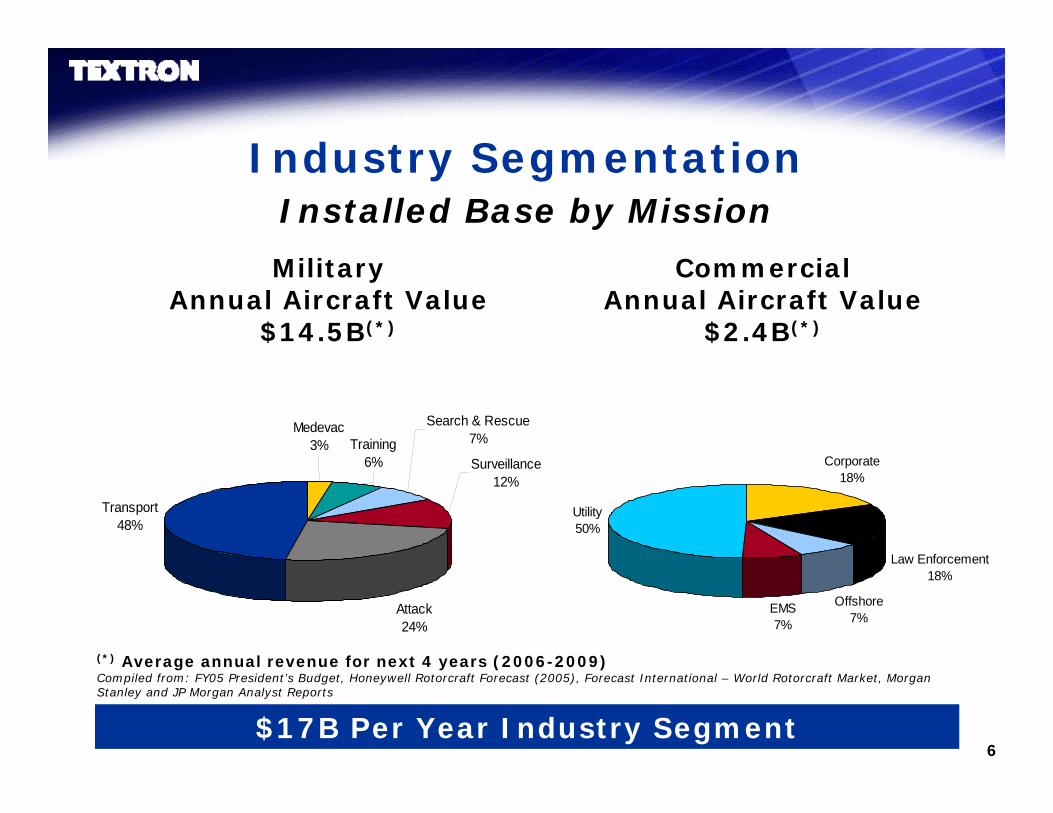

Search & Rescue7%

Surveillance12%

Transport48%

Training6%

Medevac3%

Attack24%

Industry Segmentation

Corporate18%

Law Enforcement18%

Offshore7%

EMS7%

Utility50%

Installed Base by Mission

(*) Average annual revenue for next 4 years (2006-2009)Compiled from: FY05 President’s Budget, Honeywell Rotorcraft Forecast (2005), Forecast International – World Rotorcraft Market, Morgan Stanley and JP Morgan Analyst Reports

CommercialAnnual Aircraft Value

$2.4B(*)

MilitaryAnnual Aircraft Value

$14.5B(*)

$17B Per Year Industry Segment

7

Rotorcraft Industry -Strong Growth Outlook

Global War On Terrorism • DOD Rotorcraft Spend Increasing From 4.8% To 6.4% Of Procurement

Budget: FY05 To FY11

• Flight Hours Have Increased 2-4x Previous Levels

• Rotorcraft Survivability Essential To DOD

Homeland SecurityIncreasing Border Protection: Domestic And International

Offshore/Utility Segments80% Of Fleet: 20 Years Or Older

Regulatory/Insurance/Safety Issues Driving Fleet Replacement

High Oil Prices Driving Offshore Exploration

EMS & National Disaster EffortsAsia Tsunami Disaster; Pakistan Earthquake Relief

Hurricane Katrina / Rita / Wilma

Growing International DemandAsia-Pacific Significant Opportunity

Industry Growth Continues Across the Board

8

Bell Helicopter… Clear Strategy to Become Premier

• Overview:

– Balanced Business/Becoming Premier

– Investing in Talent

– Growth Industry

• Commercial Products

• Military Products

• Customer Support Business

• Managing for Long-Term Growth

Strategic Focus…Key Levers of Value Creation

9

Aircraft

609

412407206B3/L4

429

417

427

430

210

Support

SparesRepair &OverhaulAircraft CompletionsRefurbishmentTraining SystemsField ServicesTechnical DataSupport Equipment

Commercial Business Products & Support Services

Commercial Business Growing

10

Rotorcraft MissionsCorporate EMS

Law Enforcement

Disaster Relief

Offshore

Utility

Helicopters Perform a Wide Variety of Missions Every Day

11

New Introduction from Bell

• Making Our Best-Selling Long-Light Single Even Better • Improved Engine

– 15% Increase In SHP, 5% Lower SFC, 50% Higher TBO

• Integrated Avionics– Modern Avionics Suite Reduces Workload, Improves Safety

• First Delivery – 2009

Bell 417 Light Single

Over 100 Orders

12

New Introduction from Bell

• “First-ever” Technologies from Bell’s Modular Affordable Product Line (MAPL)

– Unprecedented Cabin and Cockpit Features

– New High Performance Rotor Technology

• First Delivery – 2008/2009

Bell 429 Global Ranger Light Twin

Over 175 Orders

13

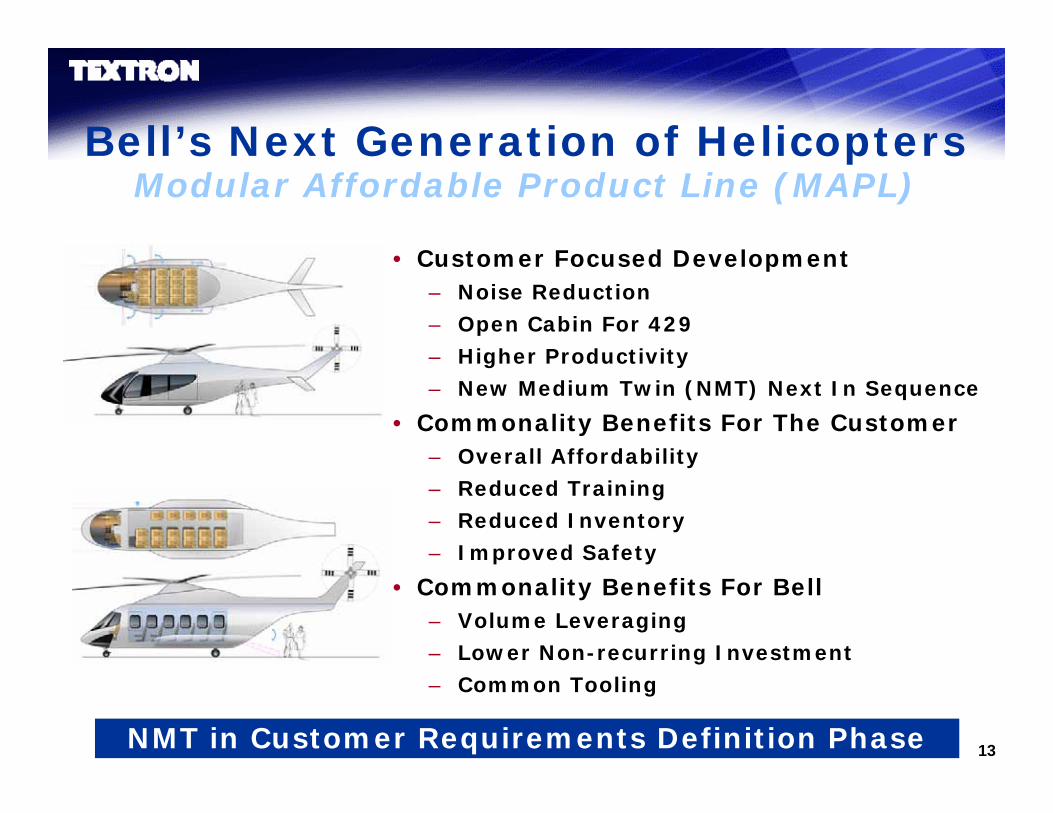

Bell’s Next Generation of HelicoptersModular Affordable Product Line (MAPL)

• Customer Focused Development– Noise Reduction– Open Cabin For 429– Higher Productivity– New Medium Twin (NMT) Next In Sequence

• Commonality Benefits For The Customer– Overall Affordability– Reduced Training– Reduced Inventory– Improved Safety

• Commonality Benefits For Bell– Volume Leveraging– Lower Non-recurring Investment– Common Tooling

$10BOpportunity

NMT in Customer Requirements Definition Phase

14

Leveraging Tiltrotor into Commercial Markets

• First Flight March ‘03, Airplane Mode Flight July ‘05• Reached 304 kts Airspeed & 25,000’ April ‘06• Exploring Potential Military Applications

25,000’ Flight Ops April 2006

BA609

A/C #2 Ground Test

Progressing Toward FAA Certification

15

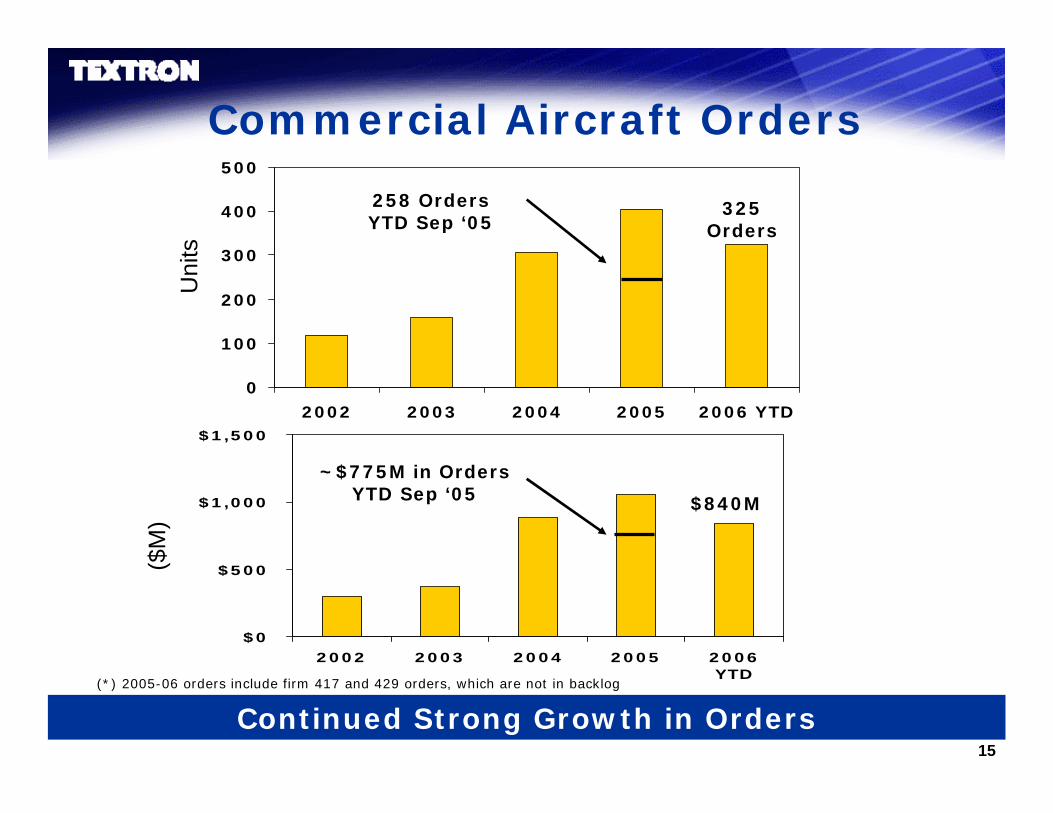

Commercial Aircraft Orders

0

100

200

300

400

500

2002 2003 2004 2005 2006 YTD

Uni

ts

$0

$500

$1,000

$1,500

2002 2003 2004 2005 2006YTD

($M

)

Continued Strong Growth in Orders(*) 2005-06 orders include firm 417 and 429 orders, which are not in backlog

258 Orders YTD Sep ‘05

325 Orders

~$775M in Orders YTD Sep ‘05 $840M

16

Bell Helicopter… Clear Strategy to Become Premier

• Overview:

– Balanced Business/Becoming Premier

– Investing in Talent

– Growth Industry

• Commercial Products

• Military Products

• Customer Support Business

• Managing for Long-Term Growth

Strategic Focus…Key Levers of Value Creation

17

Aircraft Support

SparesOverhaul & RepairTechnical DataSupport EquipmentField ServicesTraining SystemsDepot Maintenance

Installed Base: 2,400

V-22Osprey

AH-1Z/ UH-1YSuperCobra/Huey

OH-58DKiowa Warrior

TH-67Creek II

USCGEagle Eye

VH-71Marine One

Government BusinessProducts & Support Services

ARH-70ABell 407/417

USAFCSAR-X Potential

Balanced Business...Complementing Each Other

18

V-22 Program

360 AircraftCombat AssaultAssault SupportExternal Load

Operations

Marine Corps

50 AircraftSpecial Operations

Insertion/ExtractionWMD Warfare

Air Force

48 AircraftCombat SAR

Fleet LogisticsSpecial WarfareAerial Tanker

Navy

$19BProgram

Twice the Speed . . . Five Times the Range

VV--22 22 ISIS Transformational CapabilityTransformational Capability

19

0

5

10

15

20

25

30

35

40

'06 '07 '08 '09 '10 '11

New Aircraft

Modifications

V-22 Current Ramp-up Schedule

Un

it P

rod

uct

ion

133 total units ’06 –’11: +1 Net V-22Note: Reflects Proposed DOD FY07 and Long-Range Budgets – Subject to Change

20

‘05-06 V-22 Milestones

• OPEVAL – Resounding Success• Full Rate Production Decision September 2005• Submitted Proposal for Multi-Year Procurement

Sep 2006• Star of Farnborough Airshow

V-22 Production 2 Units Ahead of Schedule

21

Tiltrotor Future Opportunities

• Air Force Special Operations Command (AFSOC)– 27 Additional V-22 Aircraft

• Future V-22 Variants:– USN - Airborne Early Warning: 75 Aircraft– UK, Japan, Israel Tiltrotor Variants

• Army Tiltrotor Variants– 25-75 Potential Tiltrotor Aircraft– SOF Task Force 160th, CH-47 and

UH-60 Replacement Opportunities

• Joint Heavy Lift Quad Tiltrotor: 250-300 Aircraft Potential

Tiltrotor Future is Growing

22

UH-1Y100 Units

AH-1Z180 Units

H-1 Upgrade ProgramLow Cost/High Performance

• 84% commonality between Y & Z

• Low Rate Initial Production Underway

• Operational Evaluation Underway

• Delivering 4 Aircraft in 2006

• Next DOD Review Late October

$5.6BProgram

Another Significant Growth Opportunity

23

0

5

10

15

20

'06 '07 '08 '09 '10

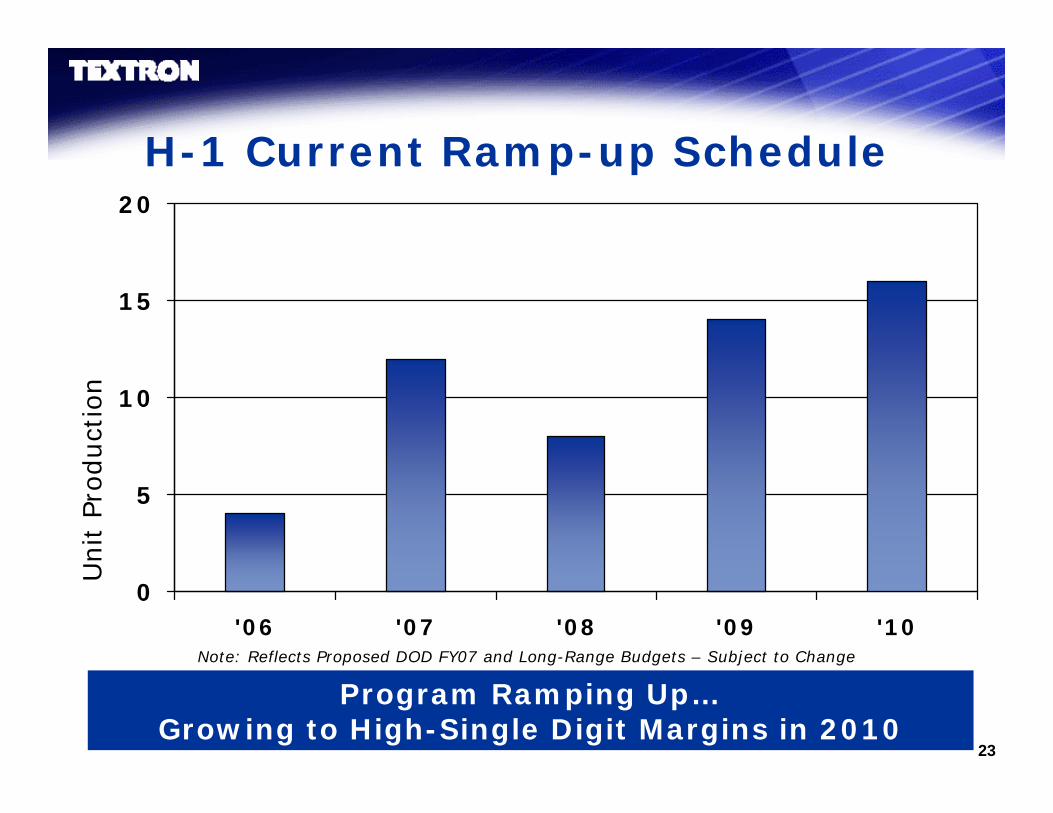

H-1 Current Ramp-up Schedule

Unit P

roduct

ion

Program Ramping Up…Growing to High-Single Digit Margins in 2010

Note: Reflects Proposed DOD FY07 and Long-Range Budgets – Subject to Change

24

14 Aircraft, 8 Y’s & 6 Z’s, on Production Line

H-1 Upgrade Program

25

$3.0BTotal Bell

Potential

• Militarized Commercial Derivative Of 407/417• 368 Units @ $5.5 M Per Aircraft• Delivery Over 6 Years, Beginning In 2007• Significant Future Foreign Military Potential

Bell Armed Reconnaissance Helicopter

First Flight July 20First Flight July 20thth 20062006

26

0

10

20

30

40

50

60

'06 '07 '08 '09 '10

ARH-70A Current Ramp-up Schedule

Unit P

roduct

ion

System Design & Development

Growing to High Single Digit Margins in 2010Growing to High Single Digit Margins in 2010Note: Reflects Proposed DOD FY07 and Long-Range Budgets – Subject to Change

27

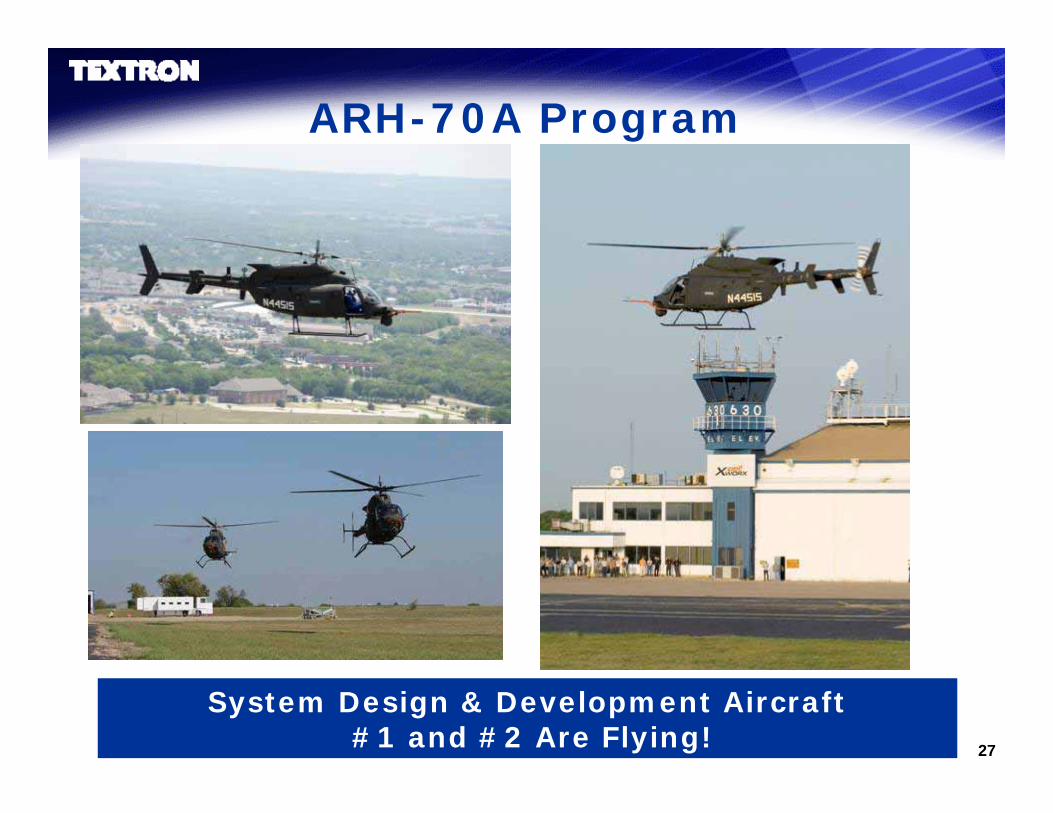

SDD #4

SDD #3

System Design & Development Aircraft#1 and #2 Are Flying!

ARH-70A Program

28

U.S. Presidential HelicopterVH-71• Initial Contract - Systems Development &

Demonstration Phase

– Lockheed Lead; Bell; AgustaWestland

– Total Initial Contract: $1.7 Billion

– Bell: ~$160 Million

– 2005-2010

• Total Program Potential:

– 23 Units

– $6 Billion

$750MTotal BellPotential

Bell Proud Partner in President’s Helicopter

29

Country Description Product Value Contract Timing

India Light Recon 407 ~$550M 2007

Saudi Arabia Min of Interior 412EP ~$300M 2007

Taiwan Attack AH-1Z ~$850M 2008Utility UH-1Y $1B+ 2008

BrazilColumbia Upgrades Huey II $100M+ 2006-2007EcuadorArgentina

UK/Japan Transport V-22 ~$1.2B+ 2011

Poland Utility 429 ~$150M 2007

Malaysia Attack/Utility AH-1Z/UH-1Y $400M+ TBD

International / Military Opportunities

Plus Significant Long-Term V-22 and ARH Opportunities

30

Bell Helicopter… Clear Strategy to Become Premier

• Overview:

– Balanced Business/Becoming Premier

– Investing in Talent

– Growth Industry

• Commercial Products

• Military Products

• Customer Support Business

• Managing for Long-Term Growth

Strategic Focus…Key Levers of Value Creation

31

Customer Support BusinessAttractive Returns, Good Growth

CompletionsCompletions PartsParts ServicesServices

Acquisitions:

• Edwards and Associates• Carbide Technology• Acadian Composites• U.S. Helicopter

Strategy:

• Expand Support & Service Business For Bell Fleet

• Extend Selectively Into Non-Bell Fleet

#1 in Product Support 12th Consecutive Year…Pro Pilot Magazine

32

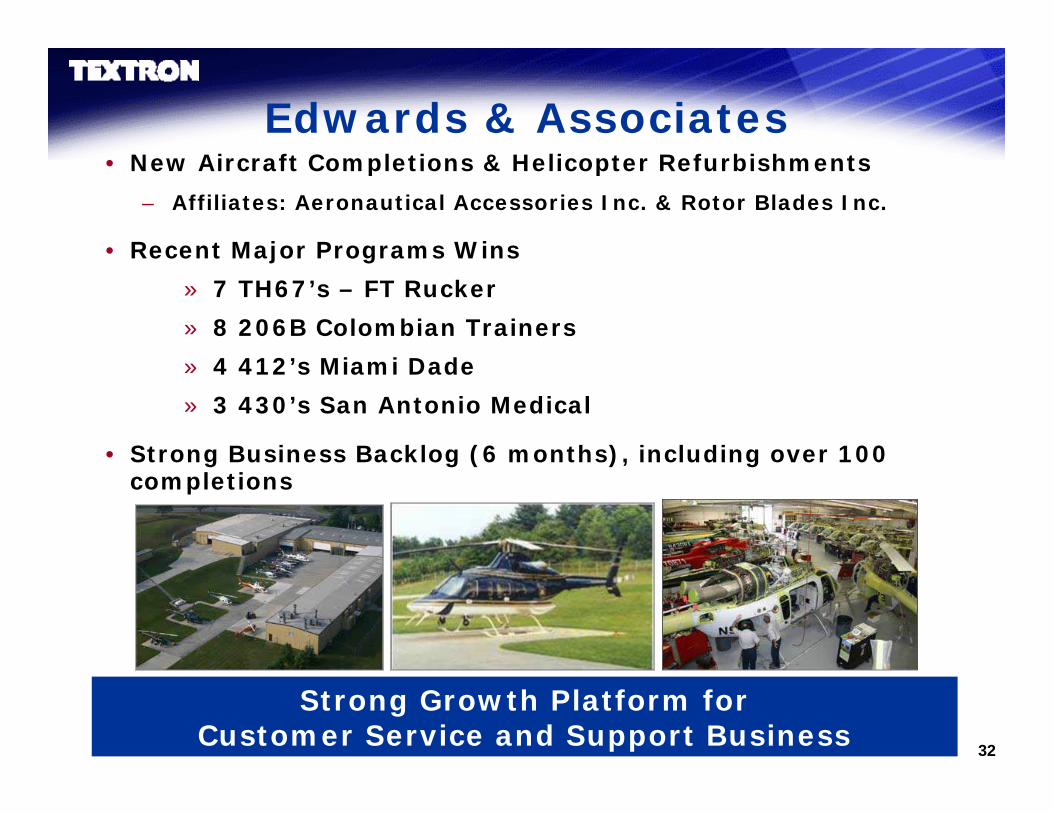

Edwards & Associates• New Aircraft Completions & Helicopter Refurbishments

– Affiliates: Aeronautical Accessories Inc. & Rotor Blades Inc.

• Recent Major Programs Wins

» 7 TH67’s – FT Rucker

» 8 206B Colombian Trainers

» 4 412’s Miami Dade

» 3 430’s San Antonio Medical

• Strong Business Backlog (6 months), including over 100 completions

Strong Growth Platform for Customer Service and Support Business

33

BellAero• Government Maintenance & Logistics Services

– Product Expertise: Huey, Huey II, TH-1H, UH-1N, Cobra, OH-58 – US Helicopter – Depot Support– BellAero Support Services – Field Support

• Recent Major Program Wins– USA OH-58 Reset (72 units per year)– DoS UH-1N SLEP Program, Huey II Remanufacture Program– USAF TH-1H Trainer Program– USMC H-1 Logistics Support

• Strong Business Backlog, increased over 300% in last year

Strong Growth Platform for Customer Service and Support Business

34

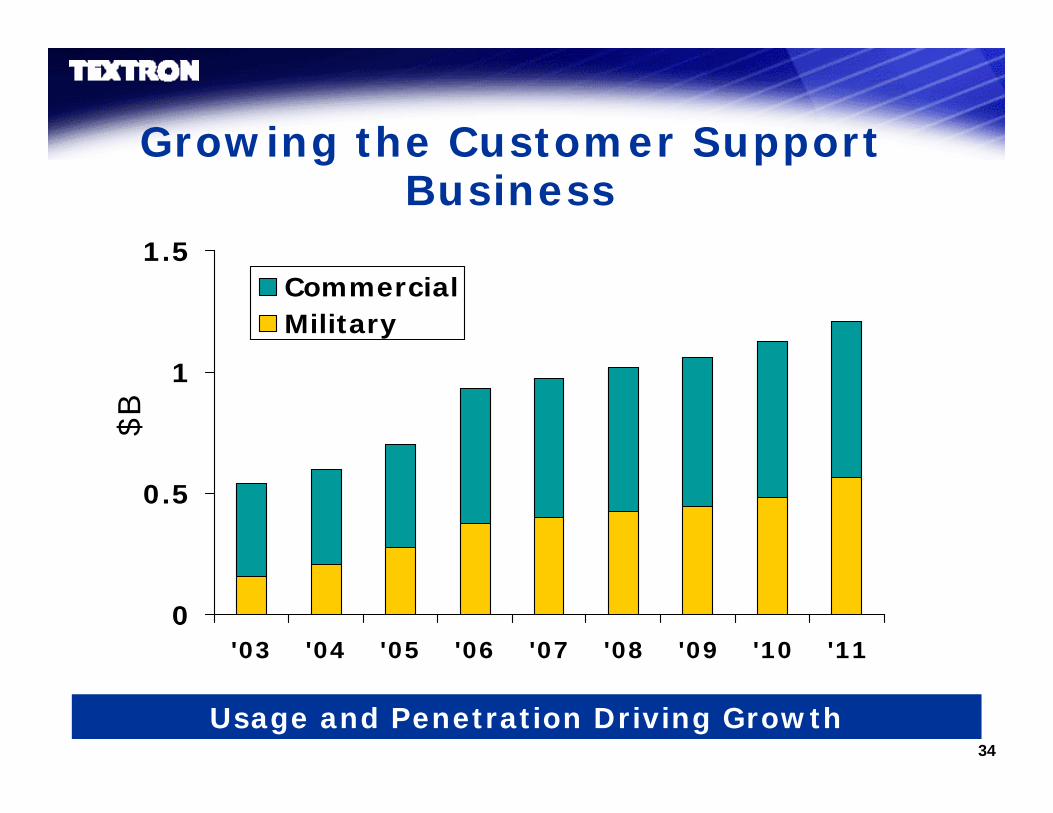

Growing the Customer Support Business

Usage and Penetration Driving Growth

0

0.5

1

1.5

'03 '04 '05 '06 '07 '08 '09 '10 '11

CommercialMilitary

$B

35

Bell Helicopter… Clear Strategy to Become Premier

• Overview:

– Balanced Business/Becoming Premier

– Investing in Talent

– Growth Industry

• Commercial Products

• Military Products

• Customer Support Business

• Managing for Long-Term Growth

Strategic Focus…Key Levers of Value Creation

36

0

4,000

0 250 500 750 1,000

Revenue ($M)

Cumulative Capital Spend ($M)

SustainmentStrategy

GrowthStrategy

2000

2001 2002

2003

2004 2005

20062007

2008

2009

2010

• From 2000 through 2003 spent less than $200M in Capital

• From 2004 through 2007 expect to spend ~$500M on growth

Growth Plan InvestmentProgress to Date

Capital Investment Accelerates, Followed by Revenue Growth

37

Path to The Premier Vertical-Lift Aircraft Manufacturer

Investing ~$40M Annually to Improve Systems

• Systems Modernization Investments:

– Program Management Execution (EVMS)

– Procurement, MRP, Financials, Billing (SAP)

– Manufacturing Execution System (Visiprise)

– Product Data Management (Enovia)

– Computer-Aided Design (CATIA V5)

– Warehouse Automation (EPIC)

38

Operations Transformation Program

Production Throughput and Productivity

Operations Strategy

Organizational Capabilities

Overhead Reduction

Supplier and Material Optimization

Engineering Effectiveness

Materials Management

– Align Leadership and Build Accountable Performance Culture

Capital Productivity

– Re-Evaluate Core/Context and Outsource Major Non-Core Items

– Enhance SIOP to Synchronize Supply with Customer Demand

– Value Stream Map Entire Product Flow and Launch Accelerators

– Align Capital Spending Program with Streamlined Product Strategy

– Reduce Manufacturing Overhead to Industry-leading Level

– Prioritize Engineering to Support Procurement and Production

– Reduce Through Design-to-Cost/Supplier Negotiation and Consolidate/ Globalize Supply Base

– Streamline Model Customization Offerings Impacting ProductionProduct Optimization

Path to The Premier Vertical Lift Manufacturer

39

FO

RT W

OR

TH

Advance Composite Center: Drive Systems Center: Rotor Systems & Assembly Center:

AM

AR

ILLO

MIR

AB

EL

Bell Capital Projects (2006-2010)

TE

NN

ES

SE

E

ALA

BA

MA

•Property Plant & Equipment (30%) - Process Line / 5 – Axis Mills CNC / Tape Lay and Fiber Placement Machines /Tooling / Bonding Press “L”

•Facility Expansion (15%) - Training Building / Test Stands / Office Refurb

•IT (15%) – Enterprise Resource Program, Product Data Manager and Business Process Updates

•Amarillo (10%) - Building Expansion / Flight Hangar / 3rd Floor Expansion

•Mirabel (10%) – Building Expansion / Warehouse Extension

•Tennessee (Edwards- 10%) - New Facility for Customizing

•Alabama (Bell Aero/U.S Helicopter - 10%) – Building/ Hangar Expansion

Investing for Growth & Expanding Capacity

40

Bell Product Lifecycle Profitability412 Example

~20X Multiplier on Initial Investment Over 25 Years

-25

0

25

50

75

100

125

1-5 6-10 11-15 16-20 20-25 25-30

Years Since Program Inception

Avera

ge A

nn

ual G

ross

P

rofi

t ($

M)

System Design & Development

Product Prime

Ramp-Up

41

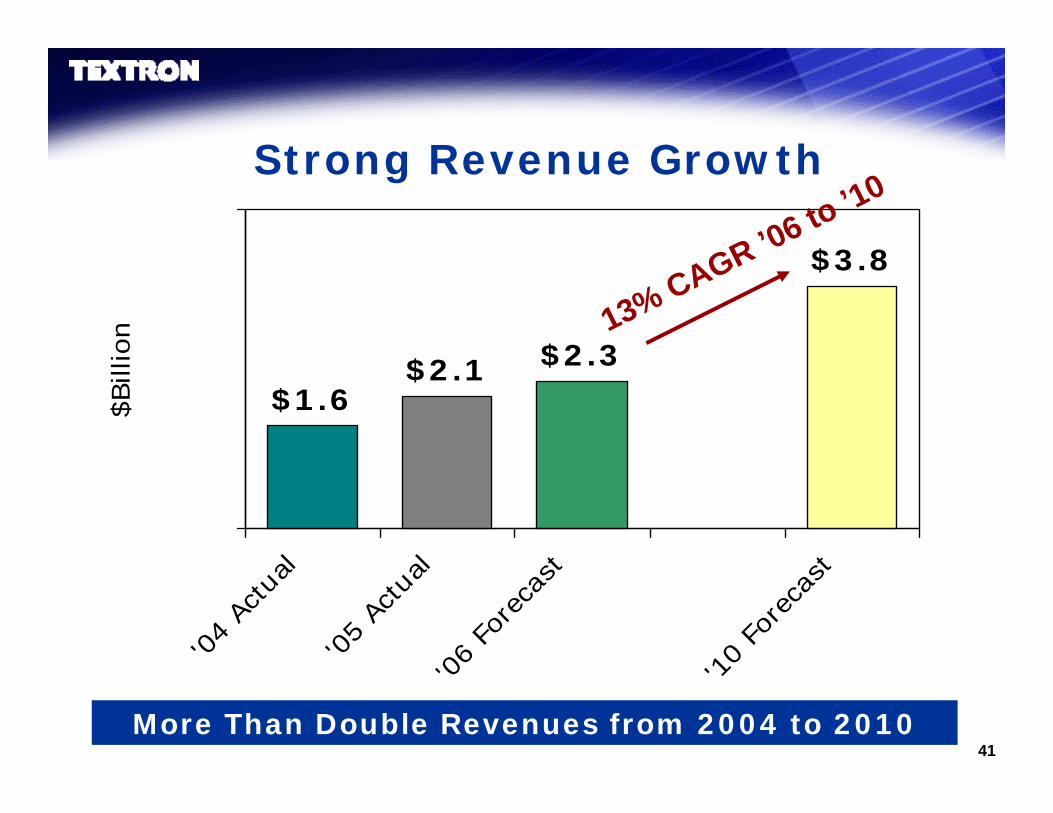

Strong Revenue Growth

$1.6$2.1 $2.3

$3.8

-

5.0

'04

Actu

al

'05

Actu

al'0

6 Fo

reca

st

'10

Fore

cast

$Bill

ion 13% CAGR ’06 to ’10

More Than Double Revenues from 2004 to 2010

42

Bell HelicopterInvesting for Growth, Expanding Capacity

Double 2004 Revenues & NOP by 2010…ROIC in High Teens

• Strong Commercial Aircraft Business

• High Growth in Military Programs

• Becoming the Premier Vertical-Lift Aircraft Manufacturer through Enterprise Management Initiatives

• Superior Product Line: Addressing Voice of the Customer in Quality, Value, Performance, Productivity, Reliability and Safety

• Expanding Customer Support Business

Certain statements in this report and other oral and written statements made by Textron from time to time are forward-looking statements, including those that discuss strategies, goals, outlook or other non-historical matters; or project revenues, income, returns or other financial measures. These forward-looking statements speak only as of the date on which they are made, and we undertake no obligation to update or revise any forward-looking statements. These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those contained in the statements, including the following: [a] changes in worldwide economic and political conditions that impact interest and foreign exchange rates; [b] the interruption of production at Textron facilities or Textron’s customers or suppliers; [c] Textron's ability to perform as anticipated and to control costs under contracts with the U.S. Government; [d] the U.S. Government's ability to unilaterally modify or terminate its contracts with Textron for the Government's convenience or for Textron's failure to perform, to change applicable procurement and accounting policies, and, under certain circumstances, to suspend or debar Textron as a contractor eligible to receive future contract awards; [e] changes in national or international funding priorities and government policies on the export and import of military and commercial products; [f] the adequacy of cost estimates for various customer care programs including servicing warranties; [g] the ability to control costs and successful implementation of various cost reduction programs; [h] the timing of certifications of new aircraft products; [i] the occurrence of slowdowns or downturns in customer markets in which Textron products are sold or supplied or where Textron Financial offers financing; [j] changes in aircraft delivery schedules or cancellation of orders; [k] the impact of changes in tax legislation; [l] the extent to which Textron is able to pass raw material price increases through to customers or offset such price increases by reducing other costs; [m] Textron’s ability to offset, through cost reductions, pricing pressure brought by original equipment manufacturer customers; [n] Textron's ability to realize full value of receivables and investments in securities; [o] the availability and cost of insurance; [p] increases in pension expenses related to lower than expected asset performance or changes in discount rates; [q] Textron Financial’s ability to maintain portfolio credit quality; [r] Textron Financial’s access to debt financing at competitive rates; [s] uncertainty in estimating contingent liabilities and establishing reserves to address such contingencies; [t] performance of acquisitions; [u] the efficacy of research and development investments to develop new products; [v] bankruptcy or other financial problems at major suppliers or customers that could cause disruptions in Textron’s supply chain or difficulty in collecting amounts owed by such customers; and [w] Textron’s ability to execute planned dispositions.

Forward-looking Information

AUSAAnalyst Briefing

Thank YouThank You

Washington, D.C.October 10, 2006

Growing Opportunity