Group 1 Final Presentation

53

Boeing Company Valuation Hannah Goldberg, Sean Ryan, Jake Varsano, Andrew Ruvkun, Ted Poatsy Tuck Bridge Program, Summer 2016

-

Upload

ted-poatsy -

Category

Documents

-

view

43 -

download

0

Transcript of Group 1 Final Presentation

Boeing Company ValuationHannah Goldberg, Sean Ryan, Jake Varsano, Andrew Ruvkun, Ted Poatsy

Tuck Bridge Program, Summer 2016

Why Boeing is currently overvalued

Aerospace industry poised for growth

Inability to meet market needs

Valuation

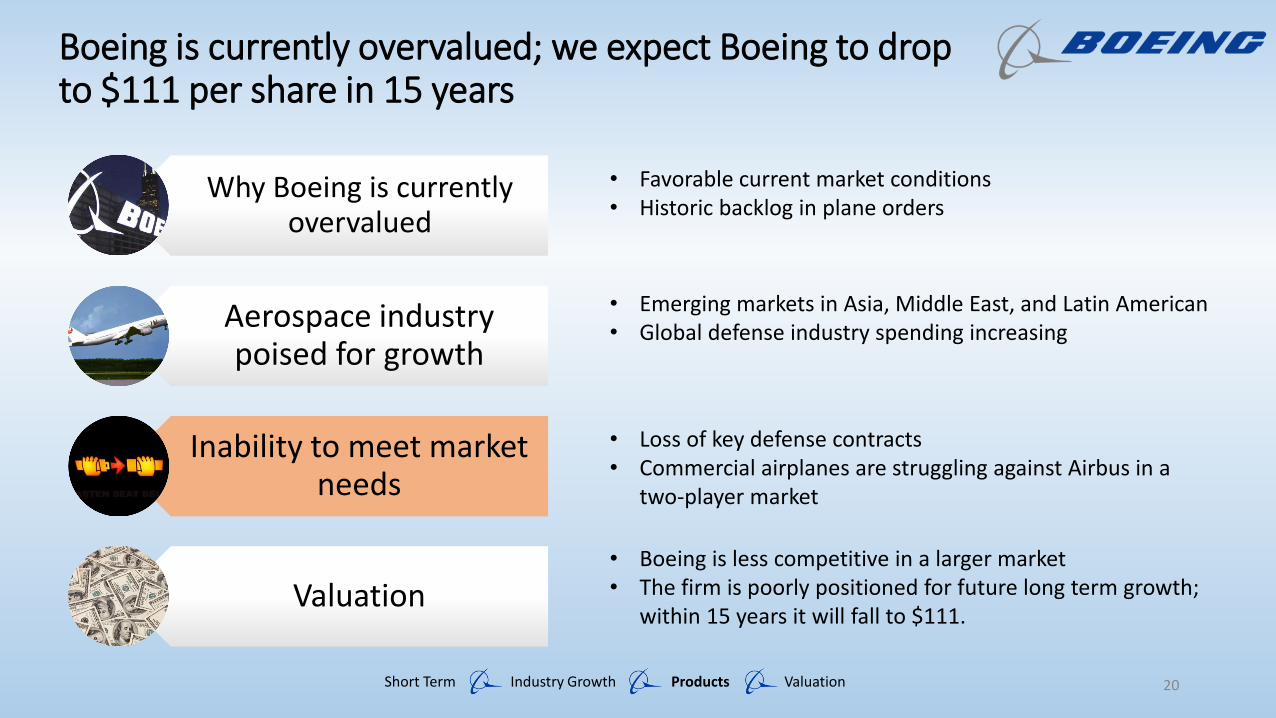

Boeing is currently overvalued; we expect Boeing to dropto $111 per share in 15 years

Short Term Industry Growth Products Valuation

• Favorable current market conditions• Historic backlog in plane orders

• Emerging markets in Asia, Middle East, and Latin American• Global defense industry spending increasing

• Loss of key defense contracts • Commercial airplanes are struggling against Airbus in a

two-player market

• Boeing is less competitive in a larger market• The firm is poorly positioned for future long term growth;

within 15 years it will fall to $111.

1

Why Boeing is currently overvalued

Aerospace industry poised for growth

Inability to meet market needs

Valuation

Boeing is currently overvalued; we expect Boeing to dropto $111 per share in 15 years

Short Term Industry Growth Products Valuation

• Favorable current market conditions• Historic backlog in plane orders

• Emerging markets in Asia, Middle East, and Latin American• Global defense industry spending increasing

• Loss of key defense contracts • Commercial airplanes are struggling against Airbus in a

two-player market

• Boeing is less competitive in a larger market• The firm is poorly positioned for future long term growth;

within 15 years it will fall to $111.

2

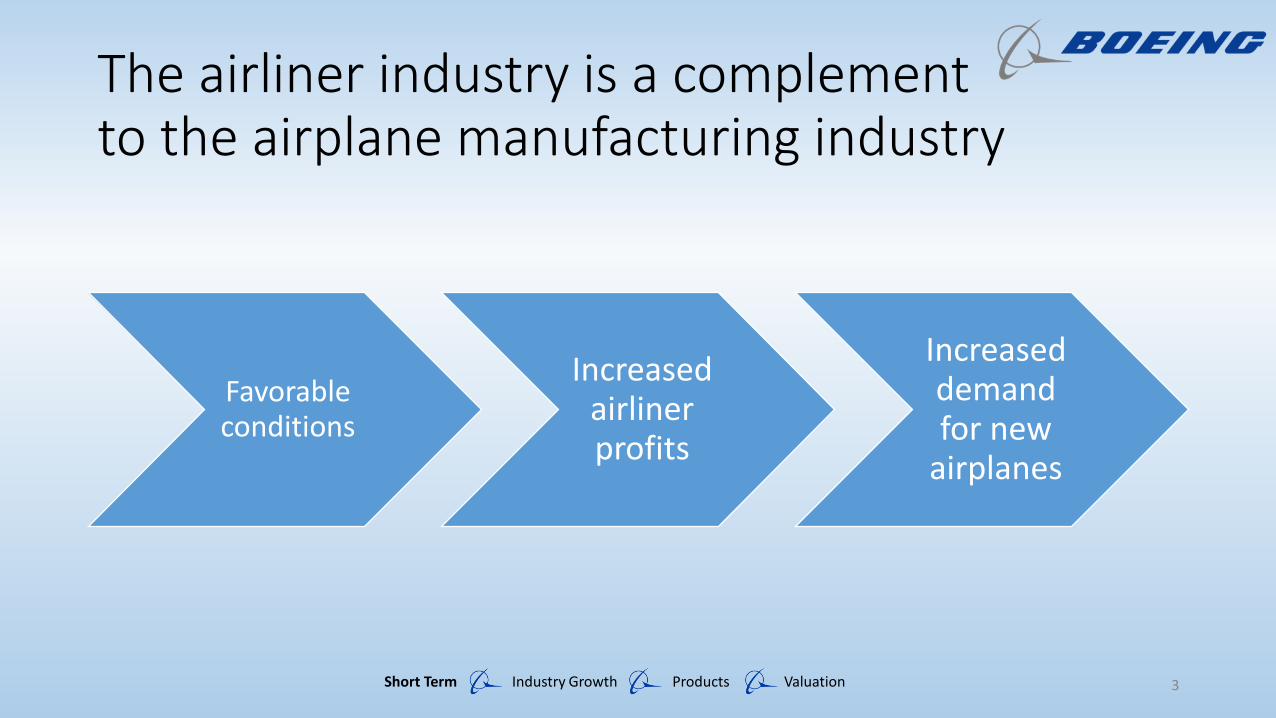

The airliner industry is a complementto the airplane manufacturing industry

Short Term Industry Growth Products Valuation

Favorable conditions

Increased airliner profits

Increased demand for new

airplanes

3

Overall airline industry growth driven by three factors

Short Term Industry Growth Products Valuation

Favorable Conditions

More demand for

air travel

Low Oil Costs

Low Interest

Rates

4

Overall airline industry growth driven by three factors

Short Term Industry Growth Products Valuation

Favorable Conditions

More demand for

air travel

Low Oil Costs

Low Interest

Rates

5

Airline passenger volume has increased due to globalization and recovery of global economy

Short Term Industry Growth Products Valuation

700

720

740

760

780

800

820

840

860

880

900

2009 2010 2011 2012 2013 2014 2015

Pas

sen

gers

(M

illio

ns)

Airline Passengers

Source: Boeing Company Data

6

Asia

North America

Latin America

Middle East

Africa

Current market outlook predicts worldwide passenger growth

AfricaLatin

AmericaMiddle

East EuropeNorth

America Asia

Asia 7.1% 7.2% 7.2% 5.1% 4.4% 6.2%

NorthAmerica

6.2% 4.9% 6.1% 3.0% 2.4%

Europe 4.7% 5.0% 5.4% 3.3%

Middle East

7.3% - 5.0%

Latin America

8.1% 6.6%

Africa 6.7%Source: Boeing Current Market Outlook 2015 - 2034

Traffic Route Growth Rates

Short Term Industry Growth Products Valuation 7

Overall airline industry growth driven by three factors

Short Term Industry Growth Products Valuation

Favorable Conditions

More demand for

air travel

Low Crude Oil Prices

Low Interest

Rates

8

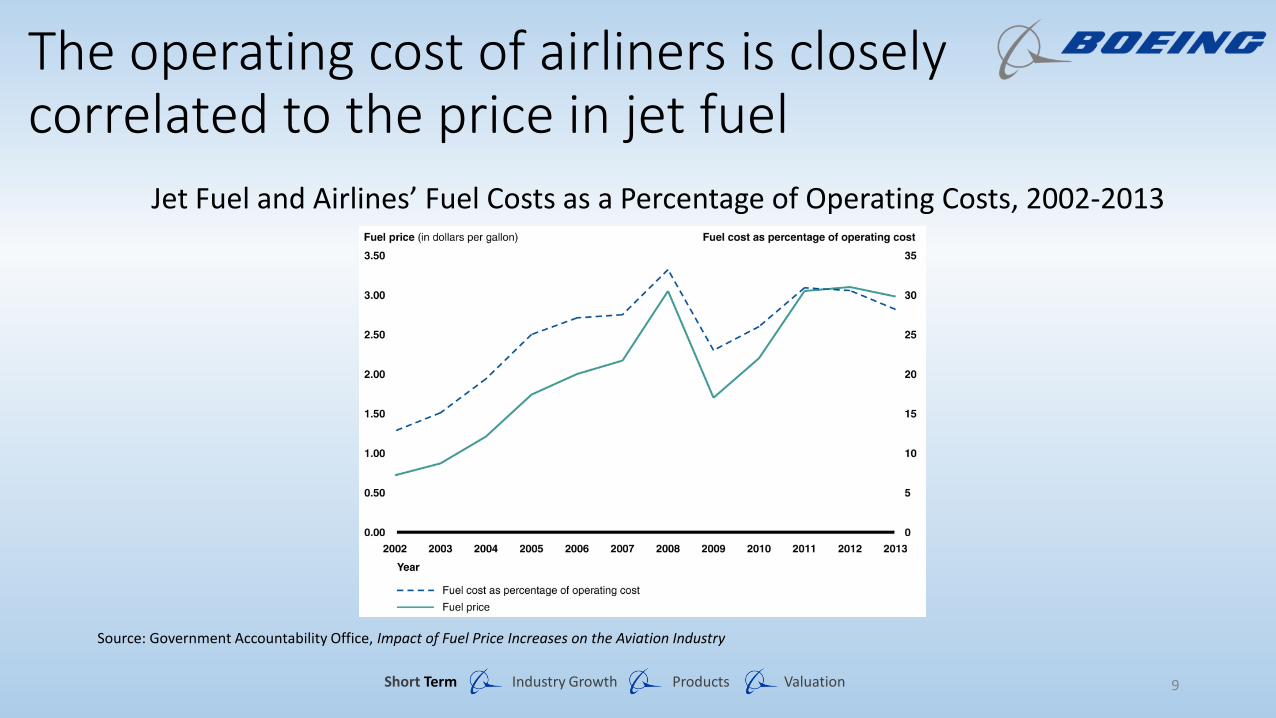

The operating cost of airliners is closely correlated to the price in jet fuel

Short Term Industry Growth Products Valuation

Source: Government Accountability Office, Impact of Fuel Price Increases on the Aviation Industry

Jet Fuel and Airlines’ Fuel Costs as a Percentage of Operating Costs, 2002-2013

9

Fall In Crude Oil has produced large profits for the airline industry

Short Term Industry Growth Products Valuation

Source: WTI

$-

$20

$40

$60

$80

$100

$120

2011 2012 2013 2014 2015 2016

Pri

ce

Crude Oil Price by QuartersHuge Profits Margins for Airliners

10

Overall airline industry growth driven by three factors

Short Term Industry Growth Products Valuation

Favorable Conditions

More demand for

air travel

Low Oil Costs

Low Interest

Rates

11

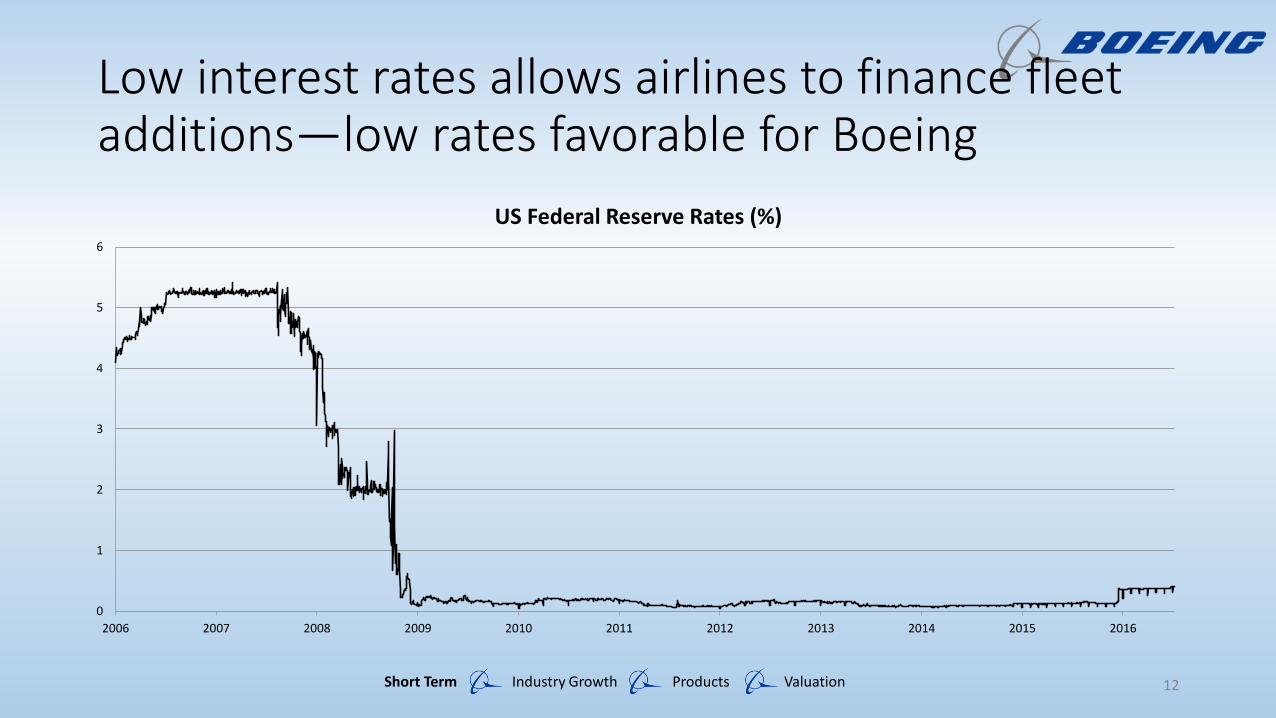

Low interest rates allows airlines to finance fleet additions—low rates favorable for Boeing

Short Term Industry Growth Products Valuation

0

1

2

3

4

5

6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

US Federal Reserve Rates (%)

12

Massive backlog in plane orders secures near term outlook

• Currently 5762 total planes in the backlog

• Factoring a high 20% cancellation rate, order sheets still full until 2022

Short Term Industry Growth Products Valuation 13

Why Boeing is currently overvalued

Aerospace industry poised for growth

Inability to meet market needs

Valuation

Boeing is currently overvalued; we expect Boeing to dropto $111 per share in 15 years

Short Term Industry Growth Products Valuation

• Favorable current market conditions• Historic backlog in plane orders

• Emerging markets in Asia, Middle East, and Latin American• Global defense industry spending increasing

• Loss of key defense contracts • Commercial airplanes are struggling against Airbus in a

two-player market

• Boeing is less competitive in a larger market• The firm is poorly positioned for future long term growth;

within 15 years it will fall to $111.

14

Boeing is a leader in the commercial and defense aerospace industries

Commercial• 2015 Revenue: $66 billion

• 762 new orders

• Current backlog at 5,800 airplanes

• Program Models: 737, 747, 767, 777, 777X, 787

• Most popular model: 737 at 10,105 total orders

Defense• 2015 Revenue: $ 30.4 billion

• 186 aircraft orders

• 15,787 weapons system orders

• Program Models: F/A-18, F-17, CH-47 Chinook, AH-64 Apache, C-17 Globemaster III

• Most popular model: CH-47 Chinook at 41 deliveries

Short Term Industry Growth Products Valuation 15

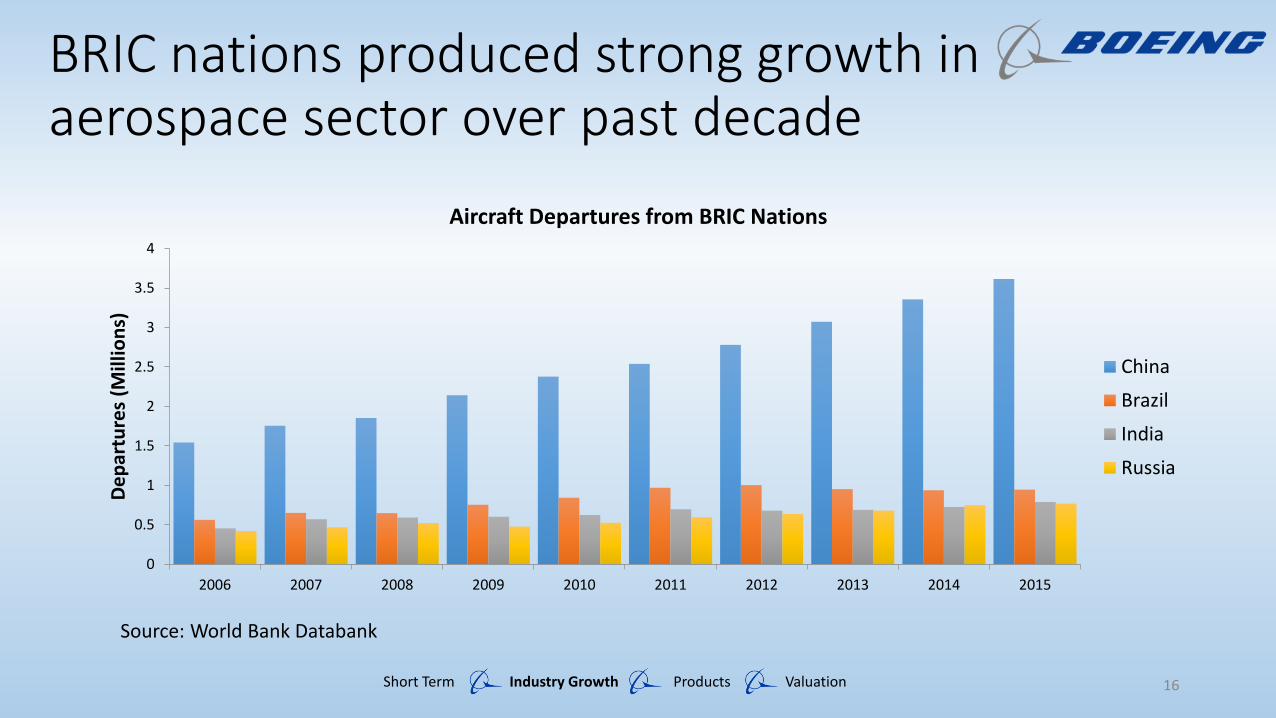

BRIC nations produced strong growth in aerospace sector over past decade

Short Term Industry Growth Products Valuation

Source: World Bank Databank

0

0.5

1

1.5

2

2.5

3

3.5

4

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

De

par

ture

s (M

illio

ns)

Aircraft Departures from BRIC Nations

China

Brazil

India

Russia

16

Global defense industry spending expected to grow

Short Term Industry Growth Products Valuation

220

230

240

250

260

270

280

290

300

2011 2012 2013 2014 2015 2016F 2017F 2018F 2019F 2020F

Rev

en

ue

(B

illio

ns)

Source: Deloitte, 2016 Global Aerospace and Defense Sector Outlook: Poised For a Rebound

Global Military Aerospace Manufacturing Revenue

17

United States defense spending is relatively stagnant

Short Term Industry Growth Products Valuation

400

450

500

550

600

650

700

750

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Spe

nd

ing

($ b

illio

n)

US Defense Budget

18

Boeing lost three major defense contracts

B-21, $55 billion

Short Term Industry Growth Products Valuation

Military Satellite, $83 million

F-35A, $1.5 trillion

T-X Trainer Program, undetermined

19

Why Boeing is currently overvalued

Aerospace industry poised for growth

Inability to meet market needs

Valuation

Boeing is currently overvalued; we expect Boeing to dropto $111 per share in 15 years

Short Term Industry Growth Products Valuation

• Favorable current market conditions• Historic backlog in plane orders

• Emerging markets in Asia, Middle East, and Latin American• Global defense industry spending increasing

• Loss of key defense contracts • Commercial airplanes are struggling against Airbus in a

two-player market

• Boeing is less competitive in a larger market• The firm is poorly positioned for future long term growth;

within 15 years it will fall to $111.

20

69% 14% 10% 8%TotalRevenue

(M)

Revenue per Segment (2015)

Commercial Aerospace

Boeing Capital(not visible <0.5%)

$66,048 $13,482 $7,751 $9,155

Source: Boeing SEC 10-K 2015 Annual Report

Defense Aerospace*

Commercial Aerospace earns 69% of Boeing’s total revenues

* Defense revenues are broken down into segments: BMA, GS&S, N&SS

Short Term Industry Growth Products Valuation

Boeing’s commercial revenue outpaces defense

Short Term Industry Growth Products Valuation 22

0

20

40

60

80

100

120

140

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Boeing Revenue Breakdown ($ Billion)

Defense Revenue Total Revenue

Airliners evaluate planes based on capacity, efficiency, and range

Capacity

Efficiency

RangeShort Term Industry Growth Products Valuation 23

Airbus meets airliners’ needs better than Boeing does

Narrow Body Wide Body

737 MAX 8 A320 neo 777-200 A350-800

Capacity(Passengers)

162 165 314 325

Efficiency(mpg/passenger)

103 105 86 98

Range(n mi)

3515 3500 5240 8100

Release Year 2017 2016 1998 2014

Short Term Industry Growth Products Valuation 24

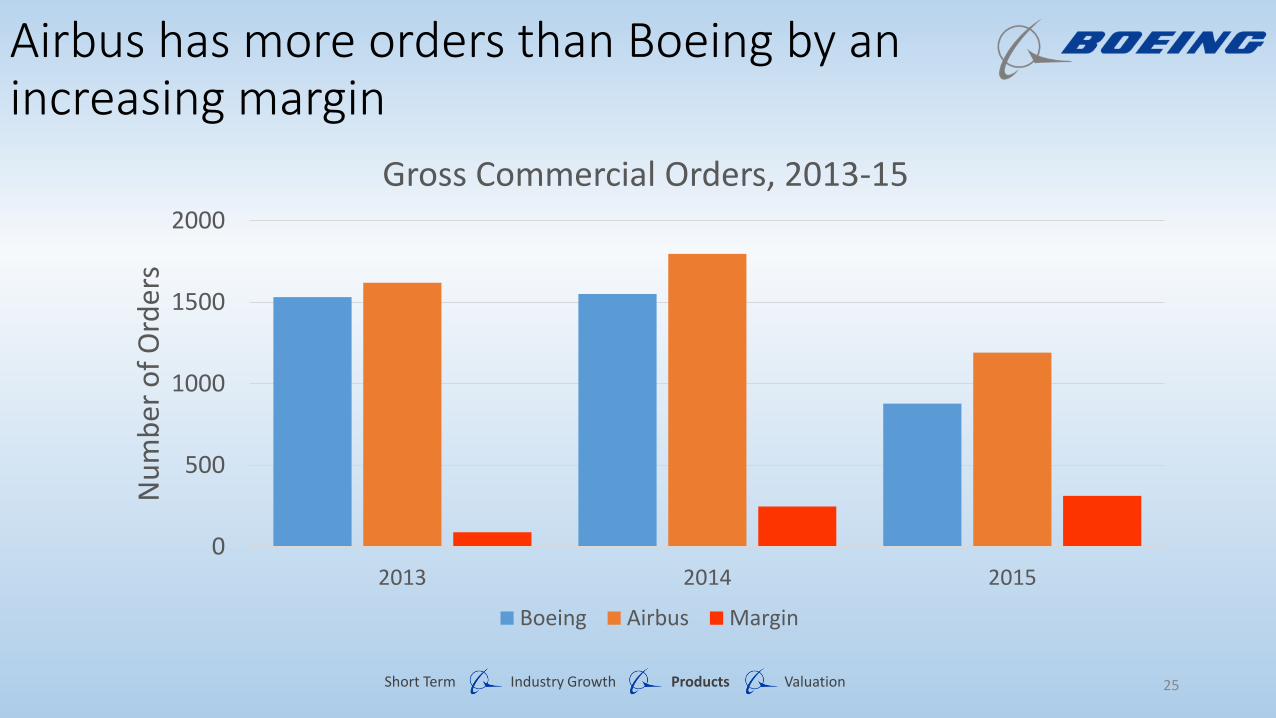

0

500

1000

1500

2000

2013 2014 2015

Nu

mb

er o

f O

rder

sGross Commercial Orders, 2013-15

Boeing Airbus Margin

Airbus has more orders than Boeing by an increasing margin

Short Term Industry Growth Products Valuation 25

Boeing has yet to pay $29 billion in production costs for 787 development

Short Term Industry Growth Products Valuation

-6000

-4000

-2000

0

2000

4000

6000

8000

2010 2011 2012 2013 2014 2015Mill

ion

s o

f D

olla

rs

Boeing Accounting Differences with 787

Earnings from operations using Program Accounting Earnings from operations using unit-cost Accounting

Source: Boeing Company Data, Bloomberg

26

Why Boeing is currently overvalued

Aerospace industry poised for growth

Inability to meet market needs

Valuation

Boeing is currently overvalued; we expect Boeing to dropto $111 per share in 15 years

Short Term Industry Growth Products Valuation

• Favorable current market conditions• Historic backlog in plane orders

• Emerging markets in Asia, Middle East, and Latin American• Global defense industry spending increasing

• Loss of key defense contracts • Commercial airplanes are struggling against Airbus in a

two-player market

• Boeing is less competitive in a larger market• The firm is poorly positioned for future long term growth;

within 15 years it will fall to $111.

27

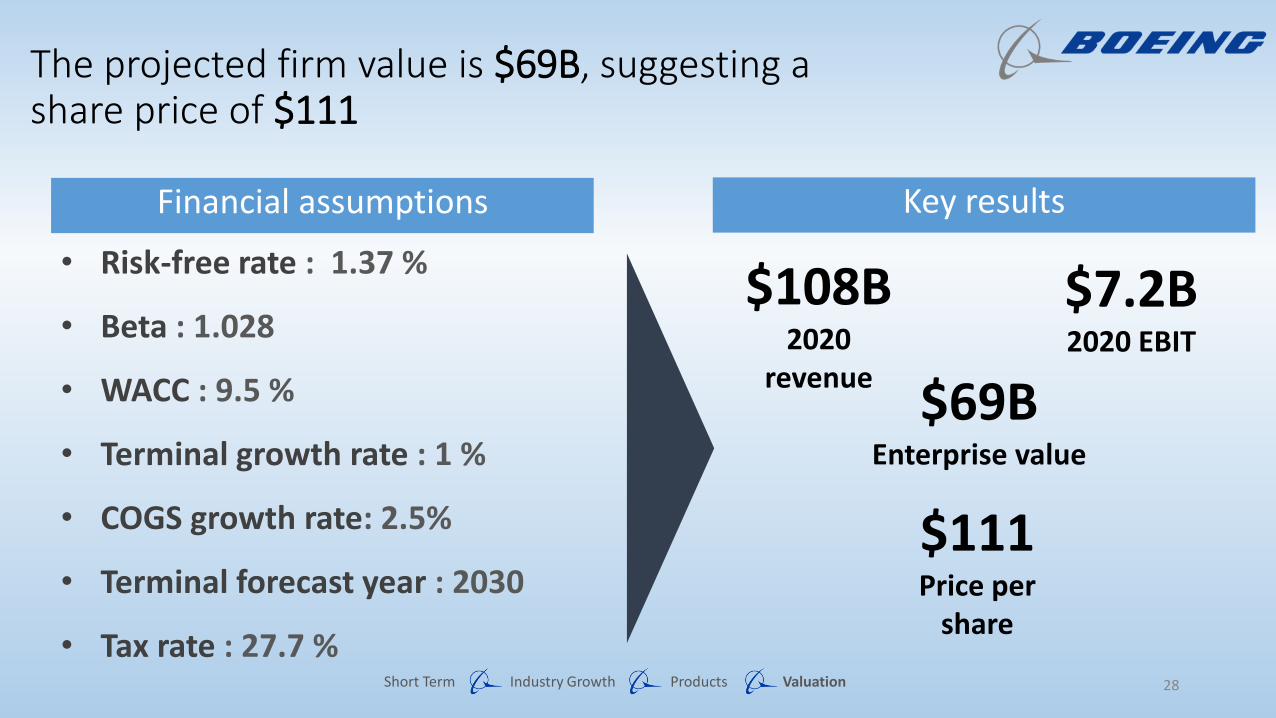

• Risk-free rate : 1.37 %

• Beta : 1.028

• WACC : 9.5 %

• Terminal growth rate : 1 %

• COGS growth rate: 2.5%

• Terminal forecast year : 2030

• Tax rate : 27.7 %

The projected firm value is $69B, suggesting a share price of $111

Financial assumptions Key results

$108B2020

revenue

$7.2B2020 EBIT

$69BEnterprise value

$111Price per

share

Short Term Industry Growth Products Valuation 28

Year 2015 2016 2017 2018 2019 2020 Terminal Value

Total Revenue 96,114 98,517 100,980 103,504 106,062 108,744

Cost of Goods Sold 82,088 84,140 86,243 88,398 90,608 92,873

EBIT 8,668 8,930 9,200 9,476 9,760 10,053

After-tax Income 6,267 6,456 6,651 6,851 7,057 7,268

(+) Depr. & Amort 1,833 1,851 1,870 1,889 1,907 1,927

(-) ∆ NWC 388 391 394 396 398

(-) CAPX 2,458 2,530 2,593 2,658 2,724

Free Cash Flows 4,980 4,673 4,386 4,116 3,863 46,788

Enterprise Value: $69 WACC: 9.5% Current Share Price: $127.17Estimated Share Price: $111

(Millions)

Less competitive products will decrease Boeing’s share price to $111 despite a growing industry

27Short Term Industry Growth Products Valuation

Sensitivity Analysis

0.00% 0.25% 0.50% 0.75% 1.00% 1.25% 1.50% 1.75% 2.00%

8.00% $ 122 $ 125 $ 128 $ 131 $ 134 $ 138 $ 142 $ 146 $ 150

8.25% $ 119 $ 121 $ 124 $ 127 $ 130 $ 133 $ 136 $ 140 $ 144

8.50% $ 115 $ 117 $ 120 $ 123 $ 125 $ 128 $ 132 $ 135 $ 139

8.75% $ 112 $ 114 $ 116 $ 119 $ 121 $ 124 $ 127 $ 130 $ 134

9.00% $ 109 $ 111 $ 113 $ 115 $ 118 $ 120 $ 123 $ 126 $ 129

9.25% $ 106 $ 108 $ 110 $ 112 $ 114 $ 117 $ 119 $ 122 $ 125

9.50% $ 103 $ 105 $ 107 $ 109 $ 111 $ 113 $ 115 $ 118 $ 121

9.75% $ 101 $ 102 $ 104 $ 106 $ 108 $ 110 $ 112 $ 114 $ 117

10.00% $ 98 $ 100 $ 101 $ 103 $ 105 $ 107 $ 109 $ 111 $ 113

10.25% $ 96 $ 97 $ 99 $ 100 $ 102 $ 104 $ 106 $ 108 $ 110

10.50% $ 93 $ 95 $ 96 $ 98 $ 99 $ 101 $ 103 $ 105 $ 107

10.75% $ 91 $ 93 $ 94 $ 95 $ 97 $ 98 $ 100 $ 102 $ 104

11.00% $ 89 $ 90 $ 92 $ 93 $ 94 $ 96 $ 98 $ 99 $ 101

Short Term Industry Growth Products Valuation 30

Terminal Growth Rate

WACC

Why Boeing is currently overvalued

Aerospace industry poised for growth

Inability to meet market needs

Valuation

Boeing is currently overvalued; we expect Boeing to dropto $111 per share in 15 years

Short Term Industry Growth Products Valuation

• Favorable current market conditions• Historic backlog in plane orders

• Emerging markets in Asia, Middle East, and Latin American• Global defense industry spending increasing

• Loss of key defense contracts • Commercial airplanes are struggling against Airbus in a

two-player market

• Boeing is less competitive in a larger market• The firm is poorly positioned for future long term growth;

within 15 years it will fall to $111.

31

Index of the Appendix

Short Term Industry Growth Products Valuation 32

Brexit36 Brexit’s impact on Boeing (USD/GBP)37 S&P 1500 (Airlines) vs. NYSE BA

Traffic Growth34 Global traffic increase by market35 South Asian market leads in traffic growth45- China Air Traffic50- Comm. Air LT Growth

Exchange Rates and Commodity Prices41 Monthly Exchange Rates 2011-201642 Price of Aluminum43 Titanium Historic Costs44 Indexed Costs of All Raw Materials

Financial Data39- Historical Stock Price51- Expanded FCF52- Beta and WACC

Market Competition46- Wide Body Market47- Narrow Body Market48- Single Aisle Market

Fleet Growth33 Growth, replacement, retained

Misc.38- Average Ticket Price40- Boeing Backlog49- Comm. Air Deliveries

Older airplanes replaced with more efficient,newer generation models as airlines refinance

Short Term Industry Growth Products Valuation

Air

pla

nes

Source: Boeing Current Market Outlook

Short Term Industry Growth Products Valuation

Global traffic increase by market

Source: Boeing Current Market Outlook

South Asian market leads in traffic growth

Short Term Industry Growth Products Valuation

Source: Boring Current Market Outlook

Short Term Industry Growth Products Valuation

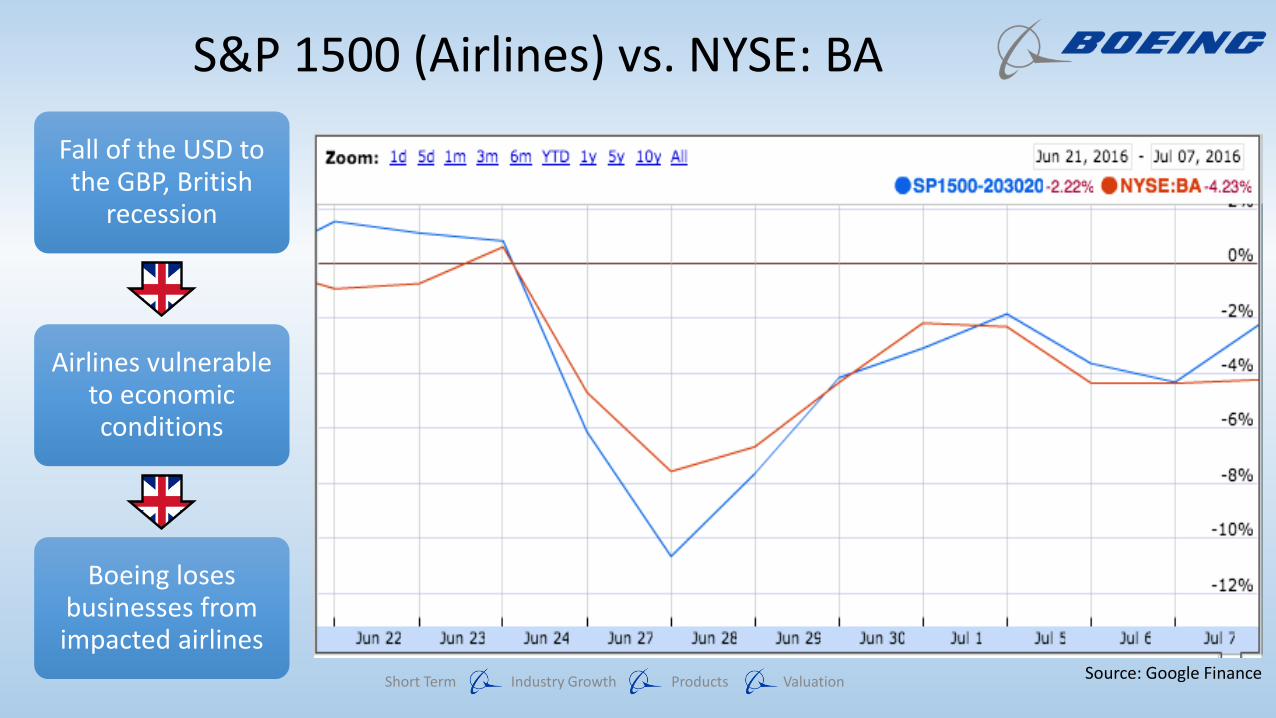

Brexit’s impact on Boeing

Fall of the USD to the GBP, British

recession

Airlines vulnerable to economic conditions

Boeing loses businesses from impacted airlines

June 23, 2016 Brexit

Source: XE.com

Short Term Industry Growth Products Valuation

Fall of the USD to the GBP, British

recession

Airlines vulnerable to economic conditions

Boeing loses businesses from impacted airlines

S&P 1500 (Airlines) vs. NYSE: BA

Source: Google Finance

Average Plane Ticket Price

Short Term Industry Growth Products Valuation 38

500

550

600

650

700

750

800

850

2009 2010 2011 2012 2013 2014* 2015*

Pri

ce in

U.S

. D

olla

rs

Year

Average Global Airfare Price

Historical Stock Price, 1980-present

Short Term Industry Growth Products Valuation 39

Boeing backlog

• Firms pay 1% of the order total when they place an order• Costs increase as delivery date nears

0 500 1000 1500 2000 2500 3000 3500

737- 800A

777F

737-700

767-300F

737-900ER

787-9

777-300ER

787-10

777X

787-8

737-800

737 MAX

Backlog Breakdown By Model

Series1

Short Term Industry Growth Products Valuation 40

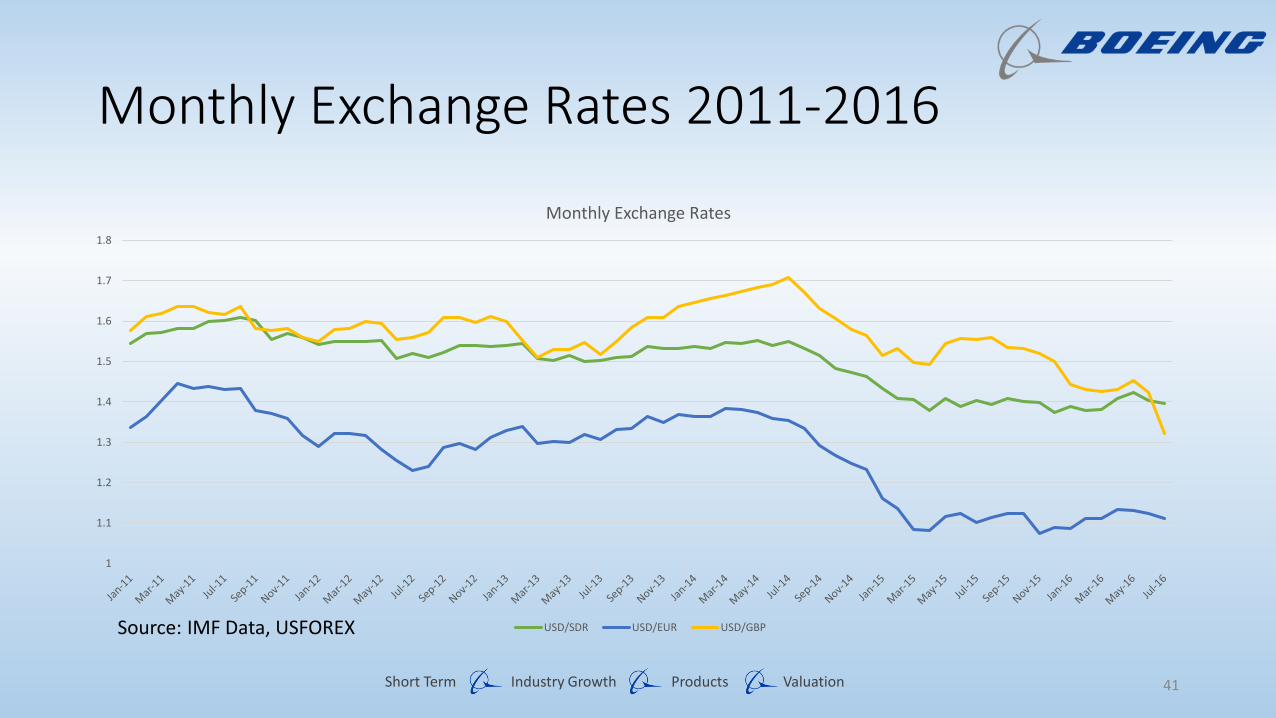

Monthly Exchange Rates 2011-2016

Short Term Industry Growth Products Valuation

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

Monthly Exchange Rates

USD/SDR USD/EUR USD/GBPSource: IMF Data, USFOREX

41

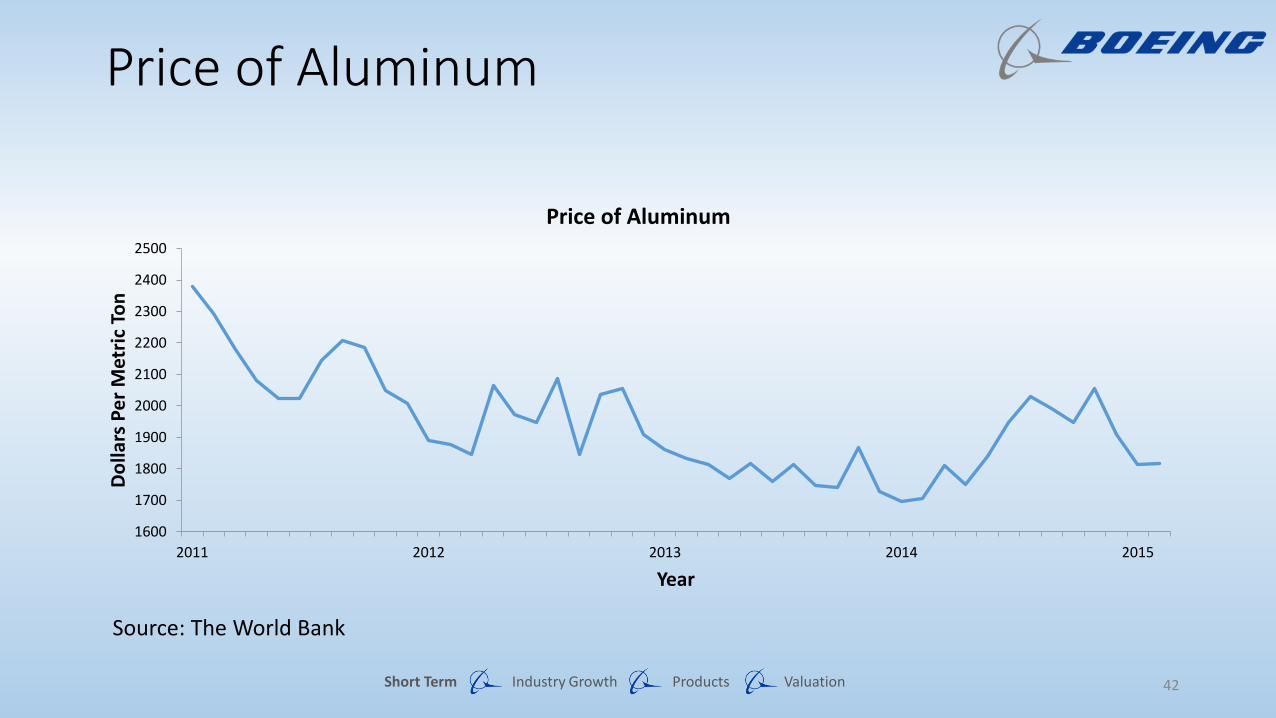

Price of Aluminum

Short Term Industry Growth Products Valuation

Source: The World Bank

1600

1700

1800

1900

2000

2100

2200

2300

2400

2500

2011 2012 2013 2014 2015

Do

llars

Pe

r M

etri

c To

n

Year

Price of Aluminum

42

Titanium Historic Price

Short Term Industry Growth Products Valuation

Source: United States Geologic Survey

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

2011 2012 2013 2014 2015

Price of Titanium (dollars per metric ton)

43

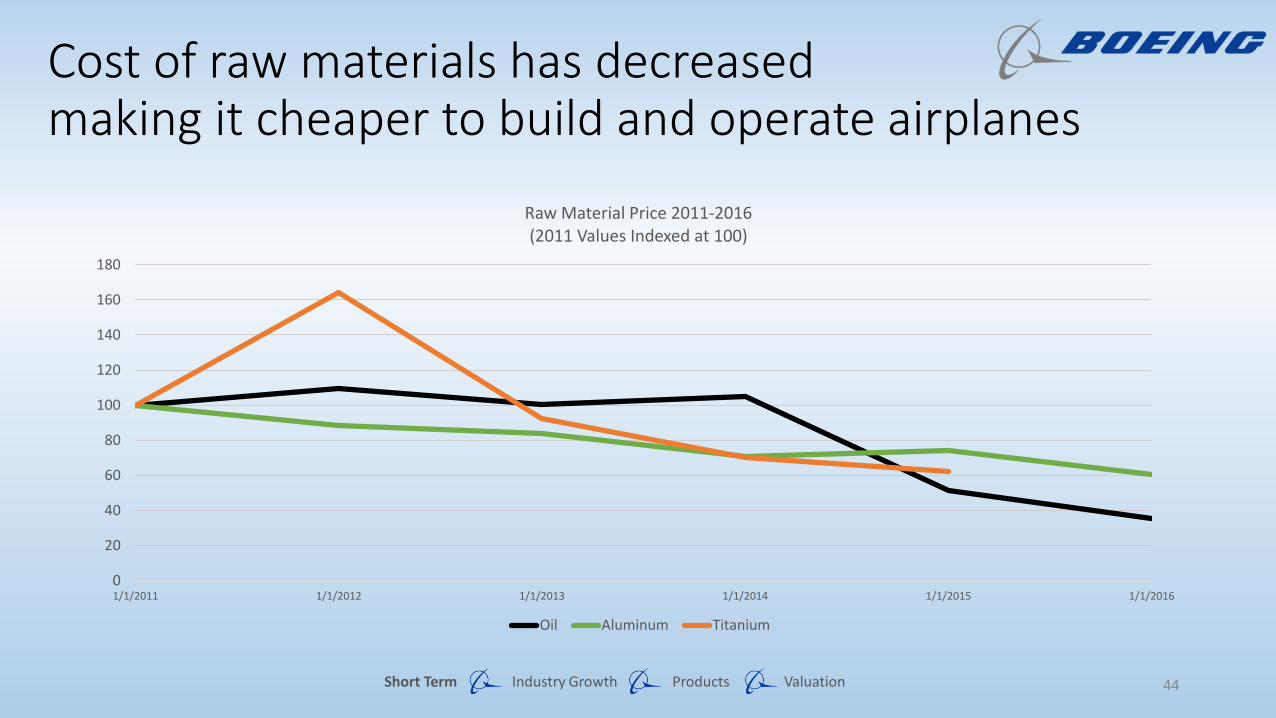

Cost of raw materials has decreased making it cheaper to build and operate airplanes

Short Term Industry Growth Products Valuation

0

20

40

60

80

100

120

140

160

180

1/1/2011 1/1/2012 1/1/2013 1/1/2014 1/1/2015 1/1/2016

Raw Material Price 2011-2016 (2011 Values Indexed at 100)

Oil Aluminum Titanium

44

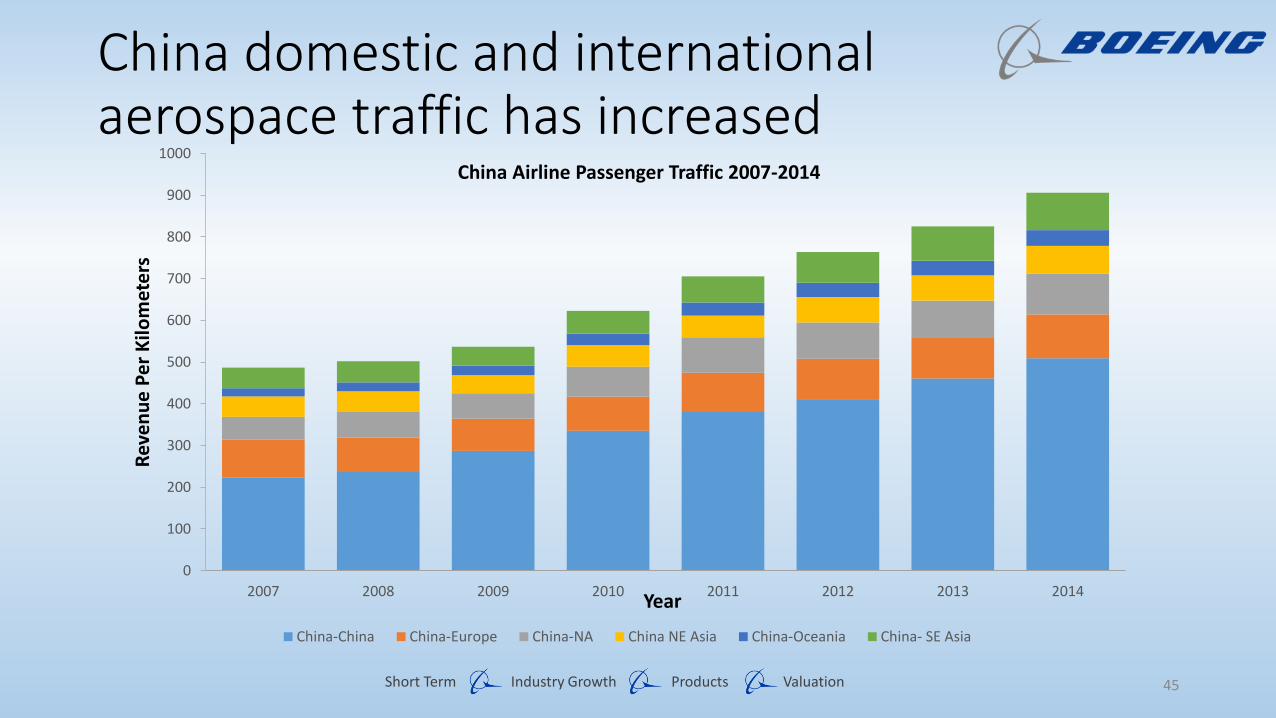

China domestic and international aerospace traffic has increased

Short Term Industry Growth Products Valuation

0

100

200

300

400

500

600

700

800

900

1000

2007 2008 2009 2010 2011 2012 2013 2014

Rev

en

ue

Pe

r K

ilom

ete

rs

Year

China Airline Passenger Traffic 2007-2014

China-China China-Europe China-NA China NE Asia China-Oceania China- SE Asia

45

Wide-body passenger airplanes products in production or use

Short Term Industry Growth Products Valuation

Large Medium Small

Boeing 747-8 Boeing 777, 777X Boeing 767, 787-8, -9

Airbus A380 Boeing 787-10 Airbus A330-200, -300, -800, -900

Airbus A350-1000 Airbus A350-800, -900

Illyushin IL-96

Source: Boeing, Current Market Outlook 2014- 2034

46

Boeing’s narrow-body models dominate its backlogs

Short Term Industry Growth Products Valuation

76.85%

12.79%

8.61%

1.37%

0.38%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

737 Family

787 Family

777 Family

767 Family

747 Family

Backlog Breakdown by Product Line

Source: Boeing Company Data

47

Single Aisle Passenger Airplanes Products in Production or Use

Single Aisle Regional Jets

Boeing 737-600, -700, -800, -900ER

AVIC ARJ-900 Antonov An-148, -158 AVIC ARJ-700

Boeing 737-MAX7, MAX8, MAX9 Bombardier CRJ-1000 Bombardier CS100, CS300

Bombardier CRJ

Airbus A318, A319, A320, A321 Embraer 190, 195 Comac C919

Embraer 170, 175 Mitsubishi MRJ

Airbus A319neo, A320neo, A321neo

Tupolev TU-204, TU-214 Sukhoi Superjet 100

Source: Boeing, Current Market Outlook 2014- 2034

Short Term Industry Growth Products Valuation 48

Commercial aerospace deliveries will increase

Short Term Industry Growth Products Valuation

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

2011 2012 2013 2014 2015 2016F 2017F 2018F 2019F 2020F

Nu

mb

er

of

Air

craf

ts

Year

Commercial Aerospace Deliveries

Source: Deloitte, 2016 Global Aerospace and Defense Sector Outlook: Poised For a Rebound

49

Commercial airline industry is forecasted tosee consistent growth in the next 15 years

Short Term Industry Growth Products Valuation

0

100

200

300

400

Commercial Industry Growth, 2015-33 ($ Billions)

United States Asia Consolidated Total

50

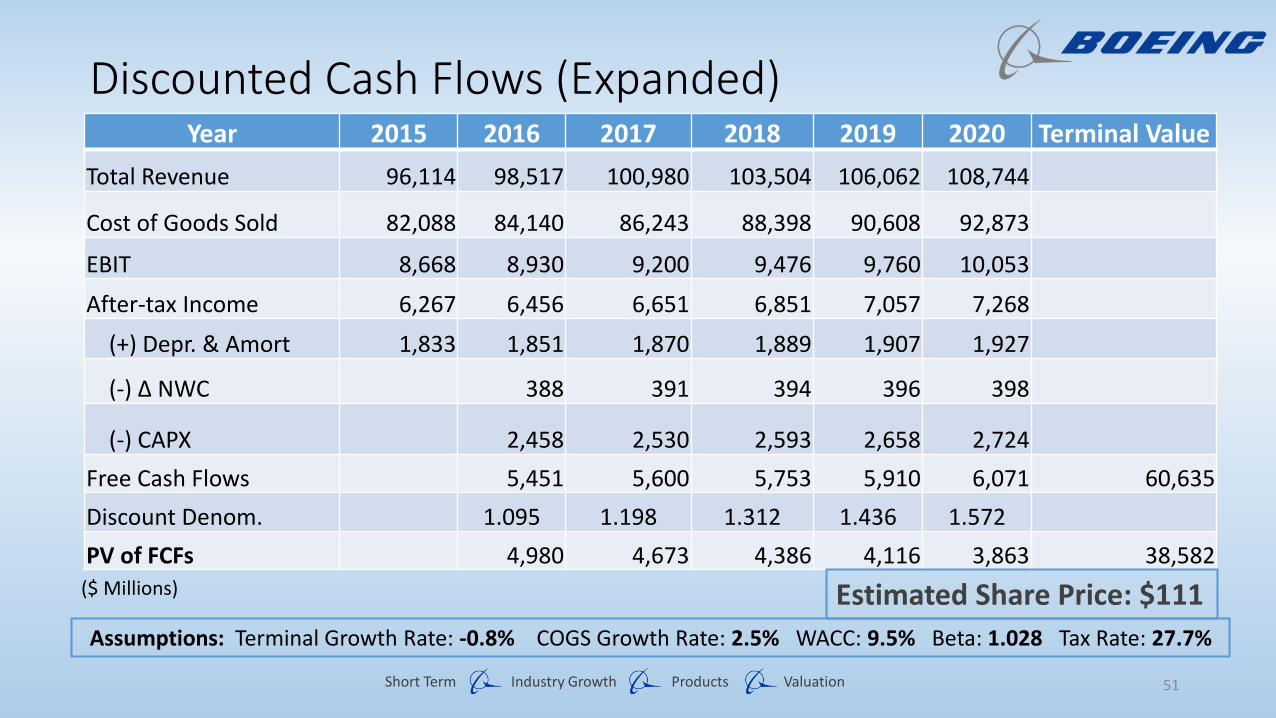

Discounted Cash Flows (Expanded)Year 2015 2016 2017 2018 2019 2020 Terminal Value

Total Revenue 96,114 98,517 100,980 103,504 106,062 108,744

Cost of Goods Sold 82,088 84,140 86,243 88,398 90,608 92,873

EBIT 8,668 8,930 9,200 9,476 9,760 10,053

After-tax Income 6,267 6,456 6,651 6,851 7,057 7,268

(+) Depr. & Amort 1,833 1,851 1,870 1,889 1,907 1,927

(-) ∆ NWC 388 391 394 396 398

(-) CAPX 2,458 2,530 2,593 2,658 2,724

Free Cash Flows 5,451 5,600 5,753 5,910 6,071 60,635

Discount Denom. 1.095 1.198 1.312 1.436 1.572

PV of FCFs 4,980 4,673 4,386 4,116 3,863 38,582

Assumptions: Terminal Growth Rate: -0.8% COGS Growth Rate: 2.5% WACC: 9.5% Beta: 1.028 Tax Rate: 27.7%

($ Millions) Estimated Share Price: $111

Short Term Industry Growth Products Valuation 51

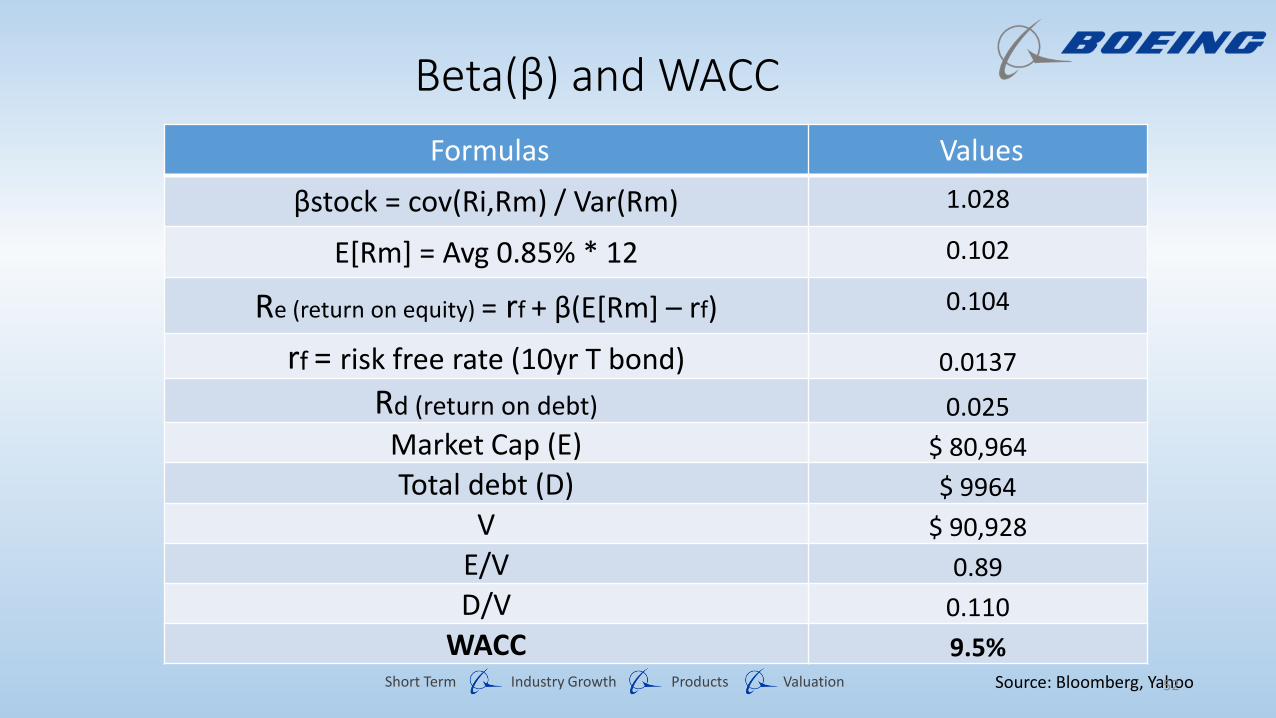

Beta(β) and WACC

Formulas Values

βstock = cov(Ri,Rm) / Var(Rm) 1.028

E[Rm] = Avg 0.85% * 12 0.102

Re (return on equity) = rf + β(E[Rm] – rf) 0.104

rf = risk free rate (10yr T bond) 0.0137

Rd (return on debt) 0.025

Market Cap (E) $ 80,964

Total debt (D) $ 9964

V $ 90,928

E/V 0.89

D/V 0.110

WACC 9.5%Source: Bloomberg, YahooShort Term Industry Growth Products Valuation 52