Govt. of NCT of Delhi - DelE Directorate of · PDF fileGovt. of NCT of Delhi ... April, 8 Drew...

24

Directorate of Education Govt. of NCT of Delhi Practice Test Material 2015-2016 Subject : Accountancy Class : XI Under the guidance of : Addl. DE (School/Exam)

Transcript of Govt. of NCT of Delhi - DelE Directorate of · PDF fileGovt. of NCT of Delhi ... April, 8 Drew...

Directorate of Education Govt. of NCT of Delhi

Practice Test Material 2015-2016

Subject : Accountancy Class : XI

Under the guidance of :

Addl. DE (School/Exam)

PRACTICE TEST-1

CLASS: XI

SUBJECT: ACCOUNTANCY

UNIT-1 : INTRODUCTION TO ACCOUNTING

Time : 50 minutes M.M. : 25

1. Define Accounting. 1

2. Define Book-keeping. 1

3. What do you mean by Management Accounting? 1

4. State any three features of Accounting. 3

5. Explain any three objectives of Accounting. 3

6. Explain any three advantages of Accounting. 3

7. Explain the following terms : 3

(i) Capital (ii) Voucher (iii) Goods

(i) (ii) (iii)

8. Differentiate between Book-keeping and accounting. 4

9. Explain the following terms :

(i) Assets (ii) Liabilities (iii) Drawings (iv) Purchases (v) Expenses

(vi) Trade Receivables 1x6=6

(i) (ii) (iii) (iv) (v)

(vi)

PRACTICE TEST-2

CLASS: XI

SUBJECT: ACCOUNTANCY

UNIT-1 : THEORY BASE OF ACCOUNTING

Time : 50 minutes M.M. : 25

1. Explain dual aspect concept. 1

2. What is going concern concept? 1

3. What do you mean by Revenue Recognition concept? 1

4. Explain verifiable objective concept. 1

5. „Capital is a liability for the business‟. Explain this statement with the principle applied. 3

6. Explain the following accounting conventions:

(i) Full Disclosure (ii) Consistency (iii) Materiality (iv) Conservatism 4

(i) (ii) (iii) (iv)

7. Explain the following : 4

(i) Accounting standards (ii) International Financial Reporting Standards

(i) (ii)

8. Describe the nature of Accounting standards. 5

9. Which financial statements are prepared under IFRS? 5

PRACTICE TEST-3

CLASS: XI

SUBJECT: ACCOUNTANCY

THEORY BASE OF ACCOUNTING

Time : 50 minutes M.M. : 25

1. Which accounting assumption assumes that a business enterprise will not be liquidated in the near future? 1

2. Under which accounting principle, quality of human resources with the enterprise is not recorded in the books of account? 1

3. „Closing stock is valued at lower of cost or market price.‟ Which accounting principle is applied in this statement? 1

4. Under which accounting principle an asset is recorded at cost, even if the market price is more or less? 1

5. How does the matching principle apply to depreciation? 3

6. “One of the accounting assumption helps in better understanding of accounting information and makes it comparable with that of previous years.” Identify and explain the implied assumption in above statement. 3

7. Explain the following terms : 4

a) Accounting standards

b) International Financial Reporting Standards (IFRS) 1½x2=3

8. Explain any three objectives of accounting standards. 3

9. Distinguish between cash basis of accounting and accrual basis of accounting on any three basis. 3

10. Explain the following with suitable example / implication in accounting:

a) Accounting Entity Principle

b) Materiality Principle

c) Accounting Period Principle

d) Dual Aspect Principle 1½x4=6

PRACTICE TEST-4

CLASS: XI

SUBJECT: ACCOUNTANCY

UNIT-3 : RECORDING OF TRANSACTIONS

Time : 50 minutes M.M. : 25

1. Define Journal. 1

2. Draw a format of Purchase Book. 1

3. Define cash book. 1

4. Explain the rules of debit and credit for traditional classification of accounts. 3

5. From the following information, prepare an accounting equation:

i) Mr. Anil started business with cash Rs. 1,00,000

ii) Purchased goods for cash Rs. 20,000 and on credit for Rs. 25,000

iii) Sold goods for cash Rs. 40,000 (costing Rs. 30,000)

iv) Wages paid Rs. 4,000 and outstanding wages Rs. 5,000 3

6. Prepare Accounting vouchers for following transactions: 3

i) Bought goods for cash vide cash memo No. 183 10,000

ii) Sold goods for cash vide cash memo No. 114 8,000

iii) Purchased computer for office use from Ms. Ashoka Traders 25,000

7. Prepare purchase book for the following transactions of Ajay Traders: 3

i) Purchased from Naresh and Co.

40 chairs @ Rs. 200 each

50 tables @ Rs. 300 each

Less : 20% trade discount

ii) Purchased from Gopal Dass & Co.

20 sofa-sets @ Rs. 15,000 each

iii) Purchased from Sunil Pvt. Ltd. for cash

10 double beds @ Rs. 8,000 each

Less 15% trade discount

iv) Purchased from Gupta Traders

5 computer sets for office use

@ 10,000 each

Less 25% trade discount

v) Purchased from Ram Kumar & Co.

25 Almirah @ Rs. 2,000 each 3

8. Journalise the following transactions in the books of Ms. Alam Traders:

2015

April, 4 Salaries due to Manager Rs. 10,000

April, 6 Insurance premium paid in advance for next year Rs. 12,500

April, 7 Goods worth Rs.4,000 were used by the proprietor for his domestic use

April, 10 Purchased goods from Ramesh Rs.10,000

April, 13 Bills receivable accepted by Vijay (a customer) Rs. 6,000

April, 16 Additional capital introduced by Alam Rs. 18,000.

April, 18 Goods returned to Ramesh Rs. 2,000

April, 25 Interest on capital Rs. 3,000 4

9. Enter the following transactions in Triple column cash book of Mr. Abrar: 6

2015 Rs.

April, 1 Cash in hand 20,000

Cash at Bank 28,000

April, 2 Deposited into bank 5,000

April, 5 Bought goods for cash 4,000

April, 8 Drew from bank for office use 3,000

April, 10 Wages paid to workers 1,000

April, 12 Goods sold to Ram and received through cheque 4,000

April, 15 Cheque received from Ram deposited into bank --

April, 18 Paid salaries by cheque 6,000

April, 20 Paid rent 6,000

April, 23 Bank charges 100

April, 28 Received from Md. Dilshad and 1,900

allowed him discount 100

April, 29 Paid to Mr. Lal and 1,800

Discount allowed by him 50

April, 30 Sundry expenses paid 250

April, 30 Dividend received through cheque 1,200

PRACTICE TEST-5

CLASS: XI

SUBJECT: ACCOUNTANCY

PREPARATION OF LEDGER

Time : 50 minutes M.M. : 25

1. Define Ledger. 1

2. Show the format of ledger account. 1

3. What do you mean by posting? 1

4. Folio of which book is shown in Journal? 1

5. Distinguish between journal and ledger. 3

6. Write any four advantages of ledger. 4

7. What do you mean by balancing of accounts? Explain. 4

8. Enter the following transactions in Sales Book and post them into ledger: 5

2015

July, 4 Sold goods to „Garima & Co.‟ on credit for Rs. 1,00,000 at 5% trade discount

July 14 Sold goods for cash to Mohan Rs. 16,000

July 22 Sold goods to Anil of the list price of Rs. 1,30,000 at trade discount of 10%

9. On April 15, 2015, cash received from „Deepak & Co.‟ is Rs. 61,000 and discount allowed to them Rs. 1,000. Pass Journal entry and post it into ledger. 5

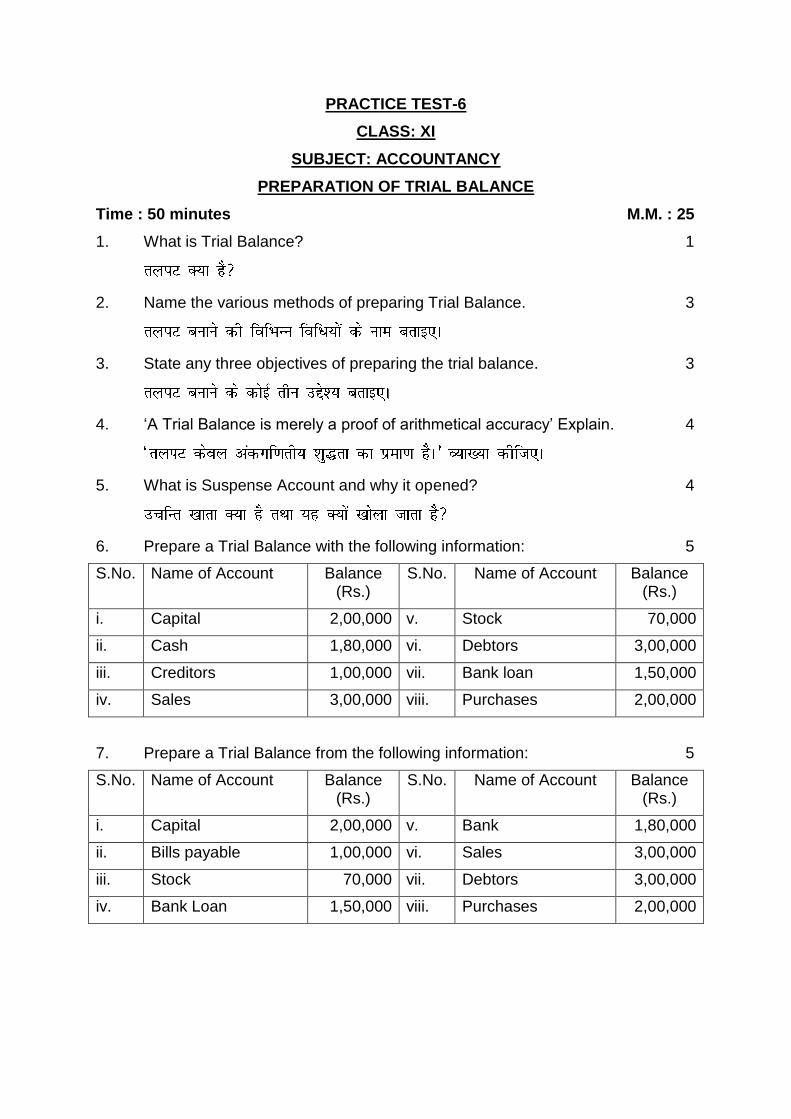

PRACTICE TEST-6

CLASS: XI

SUBJECT: ACCOUNTANCY

PREPARATION OF TRIAL BALANCE

Time : 50 minutes M.M. : 25

1. What is Trial Balance? 1

2. Name the various methods of preparing Trial Balance. 3

3. State any three objectives of preparing the trial balance. 3

4. „A Trial Balance is merely a proof of arithmetical accuracy‟ Explain. 4

5. What is Suspense Account and why it opened? 4

6. Prepare a Trial Balance with the following information: 5

S.No. Name of Account Balance (Rs.)

S.No. Name of Account Balance (Rs.)

i. Capital 2,00,000 v. Stock 70,000

ii. Cash 1,80,000 vi. Debtors 3,00,000

iii. Creditors 1,00,000 vii. Bank loan 1,50,000

iv. Sales 3,00,000 viii. Purchases 2,00,000

7. Prepare a Trial Balance from the following information: 5

S.No. Name of Account Balance (Rs.)

S.No. Name of Account Balance (Rs.)

i. Capital 2,00,000 v. Bank 1,80,000

ii. Bills payable 1,00,000 vi. Sales 3,00,000

iii. Stock 70,000 vii. Debtors 3,00,000

iv. Bank Loan 1,50,000 viii. Purchases 2,00,000

PRACTICE TEST-7

CLASS: XI

SUBJECT: ACCOUNTANCY

PREPARATION OF BANK RECONCILIATION STATEMENT

Time : 50 minutes M.M. : 25

1. What is Bank Reconciliation Statement? 1

2. What is bank overdraft? 1

3. Mention the main purpose of bank reconciliation statement. 1

4. State any two causes of difference in cash book and pass book balance. 1

5. Explain the need of bank reconciliation statement. 3

6. Name any four items which are to be added in the Debit Balance of Cash Book while preparing bank reconciliation statement. 1

7. Explain the following: 4

i. Cheques sent to the bank for collection but dishonoured.

ii. Direct payment made by the bank on behalf of customer

i.

ii.

8. On July 31, 2015, the cash book of „Kavita Enterprises‟ showed a debit balance of Rs. 1,56,000. On comparing the cash book with the pass book, the following discrepancies were noted:

i. Cheques issued for Rs. 42,000 but of them one cheque for Rs. 10,000 was encashed on August 4, 2015 and another cheque for Rs. 7,000 has not yet been presented.

ii. A cheque of Rs. 8,000 credited in the pass book on July 26, 2015 being dishonoured is debited again in the pass boon on August 2,

2015. There was no entry in the cash book about dishonour of cheque until August 10, 2015.

iii. Cheque for Rs. 16,000 were deposited in bank but of these cheques for Rs. 4,000 were not recorded in the cash book.

iv. Amount wrongly credited by bank Rs. 13,000.

v. Payment side of cash book has been overcast by Rs. 400.

Prepare Bank Reconciliation statement. 5

9. On July 31, 2015, the Pass Book of „Verma & Co.‟ showed a debit balance of Rs. 64,000. Prepare a Bank Reconciliation Statement with the following information:

i. Cheques issued of Rs. 10,000 on July 27, 2015 but this was not presented for payment whereas this was recorded twice in the cash book.

ii. A cheque of Rs. 3,000 issued on July 28, 2015 was taken in cash column.

iii. Cheques deposited into bank for Rs. 27,000 but of these cheques for Rs. 14,000 were cleared in August, 2015.

iv. On July 29, 2015 a customer deposited Rs. 10,000 directly into the bank account but it was entered only in the pass book.

v. Receipt column of cash book has been under cast by Rs. 2,000.

PRACTICE TEST-8

CLASS: XI

SUBJECT: ACCOUNTANCY

DEPRECIATION, PROVISION AND RESERVE

Time : 50 minutes M.M. : 25

1. Define Depreciation. 1

2. What do you mean by scrap value of the Asset? 1

3. Define provision. 1

4. Give any three differences between provision and reserve. 3

5. What are the main causes of Depreciation? 3

6. What are the differences between straight line method and written down value method of charging depreciation? 3

7. What are the main objectives of providing depreciation? 3

8. On 1st April, 2012 ABC Transport Co. purchased a bus for Rs. 40,00,000. On 1st October, 2013, this bus was involved in an accident and was completely destroyed and Rs. 26,50,000 were received by a cheque from the insurance company in full settlement on 1st January, 2014. On the same date (i.e., 1st January, 2014) another bus was purchased by the company for Rs. 45,00,000.

The company charges depreciation @ 20% per annum under the written drown value method. Prepare the bus account for 3 years when the books are closed on 31st March every year. 4

9. On 1st April, 2012, X Ltd. purchased a machinery for Rs. 24,00,000. On 1st October, 2014 a part of machinery purchased on 1st April, 2012 for Rs. 2,00,000 was sold for Rs. 1,10,000 and a new machinery at the cost of Rs. 4,50,000 was purchased and installed on the same date. The company has adopted the method of providing 10% p.a. depreciation on the diminishing balance of the machinery. Show the machinery account, provision for depreciation account and machinery disposal account for 3 years.

The company closes its books on 31st March. 6

Commission 2,400

Sundry Debtors 9,140

Cash in hand 80

Cash at Bank 1,300

Wages 30,000

Salaries 2,800

Purchases 42,700

Sales 96,000

Bills receivable 1,440

Bills payable 1,120

Sundry creditors 10,400

Return inwards 1,860

Provision for doubtful debts 500

Drawings 1,400

Return outwards 1,100

Rent 1,200

Factory lighting & heating 160

Insurance 1,260

General Expenses 200

Bad Debts 500

Discount 1,300 740

Total 1,17,860 1,17,860

The following adjustments are to be made :

i. Stock on March 31, 2015 Rs. 10,400.

ii. Three months factory lighting and heating due but not paid Rs. 60.

iii. 5% depreciation to be written off on furniture.

iv. Write off further bad debts Rs. 140.

v. Provision for doubtful debts to be increased to Rs. 600 and provision for discount on debtors @ 2% to be made.

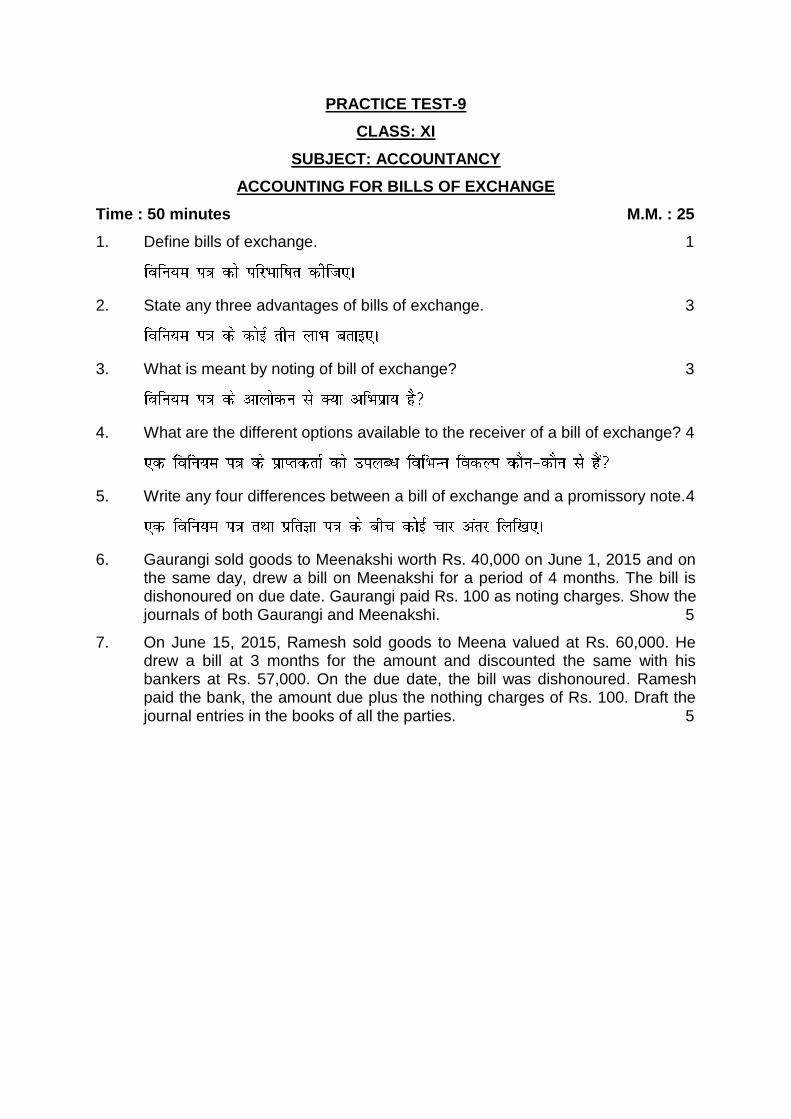

PRACTICE TEST-9

CLASS: XI

SUBJECT: ACCOUNTANCY

ACCOUNTING FOR BILLS OF EXCHANGE

Time : 50 minutes M.M. : 25

1. Define bills of exchange. 1

2. State any three advantages of bills of exchange. 3

3. What is meant by noting of bill of exchange? 3

4. What are the different options available to the receiver of a bill of exchange? 4

5. Write any four differences between a bill of exchange and a promissory note.4

6. Gaurangi sold goods to Meenakshi worth Rs. 40,000 on June 1, 2015 and on the same day, drew a bill on Meenakshi for a period of 4 months. The bill is dishonoured on due date. Gaurangi paid Rs. 100 as noting charges. Show the journals of both Gaurangi and Meenakshi. 5

7. On June 15, 2015, Ramesh sold goods to Meena valued at Rs. 60,000. He drew a bill at 3 months for the amount and discounted the same with his bankers at Rs. 57,000. On the due date, the bill was dishonoured. Ramesh paid the bank, the amount due plus the nothing charges of Rs. 100. Draft the journal entries in the books of all the parties. 5

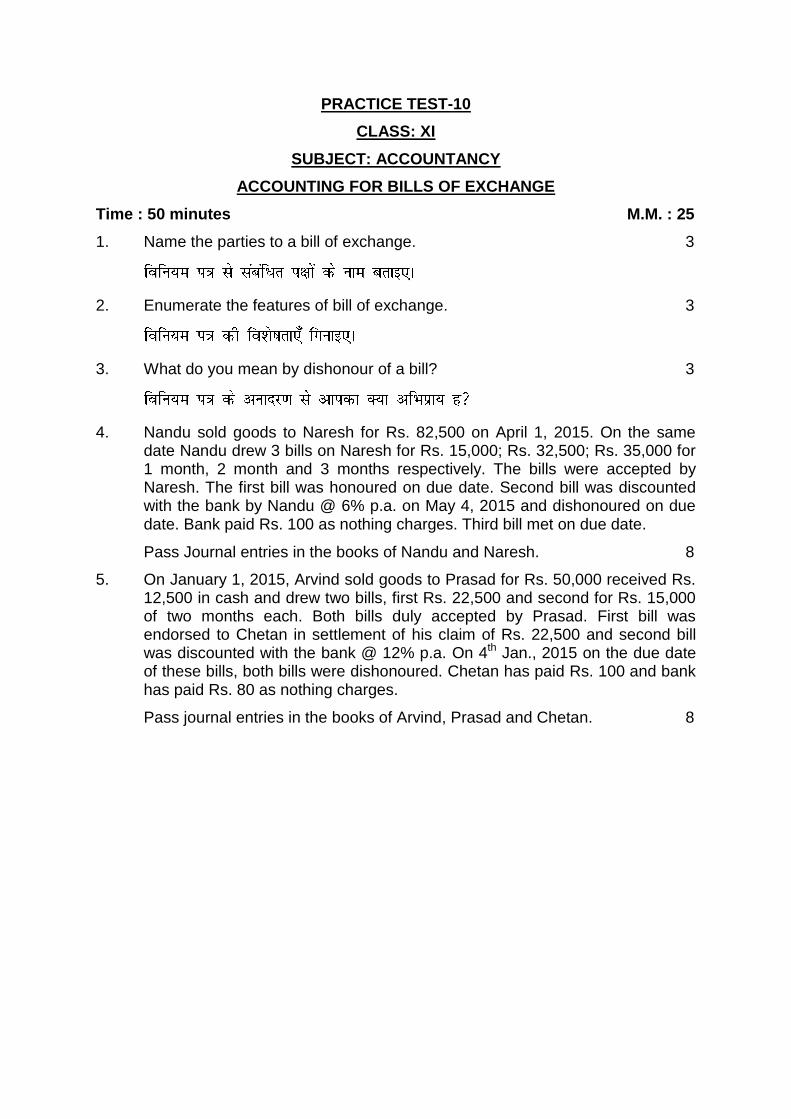

PRACTICE TEST-10

CLASS: XI

SUBJECT: ACCOUNTANCY

ACCOUNTING FOR BILLS OF EXCHANGE

Time : 50 minutes M.M. : 25

1. Name the parties to a bill of exchange. 3

2. Enumerate the features of bill of exchange. 3

3. What do you mean by dishonour of a bill? 3

4. Nandu sold goods to Naresh for Rs. 82,500 on April 1, 2015. On the same date Nandu drew 3 bills on Naresh for Rs. 15,000; Rs. 32,500; Rs. 35,000 for 1 month, 2 month and 3 months respectively. The bills were accepted by Naresh. The first bill was honoured on due date. Second bill was discounted with the bank by Nandu @ 6% p.a. on May 4, 2015 and dishonoured on due date. Bank paid Rs. 100 as nothing charges. Third bill met on due date.

Pass Journal entries in the books of Nandu and Naresh. 8

5. On January 1, 2015, Arvind sold goods to Prasad for Rs. 50,000 received Rs. 12,500 in cash and drew two bills, first Rs. 22,500 and second for Rs. 15,000 of two months each. Both bills duly accepted by Prasad. First bill was endorsed to Chetan in settlement of his claim of Rs. 22,500 and second bill was discounted with the bank @ 12% p.a. On 4th Jan., 2015 on the due date of these bills, both bills were dishonoured. Chetan has paid Rs. 100 and bank has paid Rs. 80 as nothing charges.

Pass journal entries in the books of Arvind, Prasad and Chetan. 8

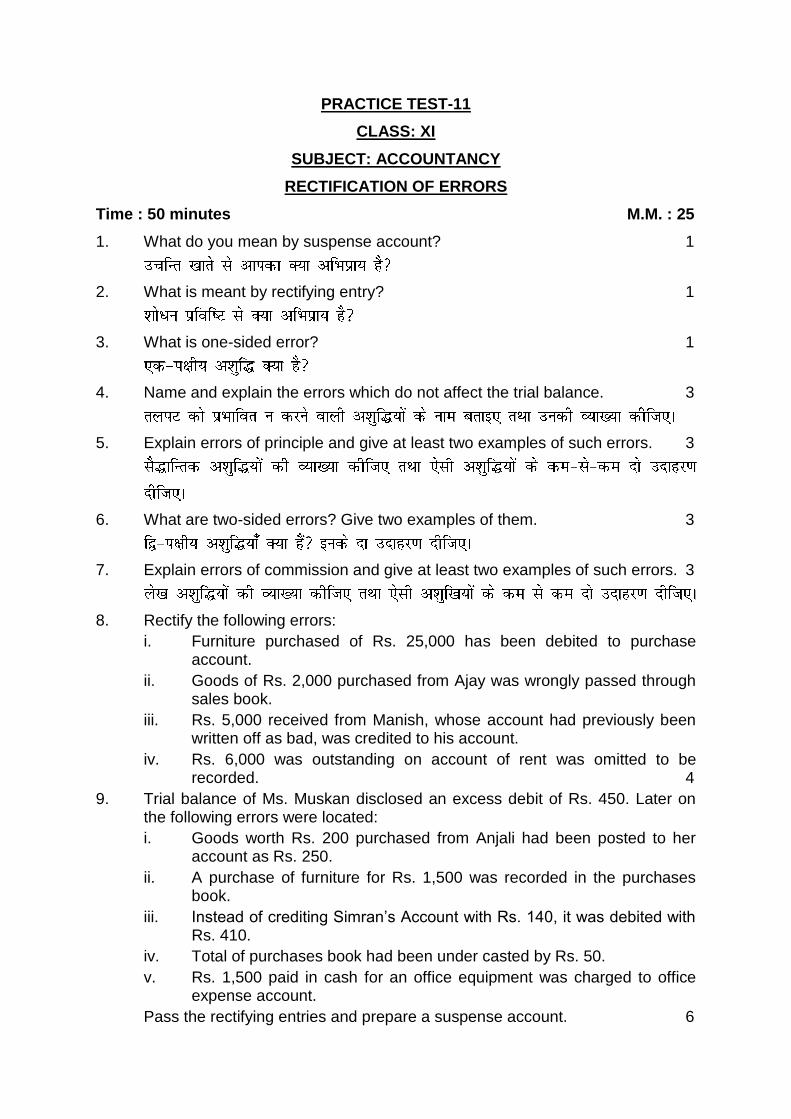

PRACTICE TEST-11

CLASS: XI

SUBJECT: ACCOUNTANCY

RECTIFICATION OF ERRORS

Time : 50 minutes M.M. : 25

1. What do you mean by suspense account? 1

2. What is meant by rectifying entry? 1

3. What is one-sided error? 1

4. Name and explain the errors which do not affect the trial balance. 3

5. Explain errors of principle and give at least two examples of such errors. 3

6. What are two-sided errors? Give two examples of them. 3

7. Explain errors of commission and give at least two examples of such errors. 3

8. Rectify the following errors:

i. Furniture purchased of Rs. 25,000 has been debited to purchase account.

ii. Goods of Rs. 2,000 purchased from Ajay was wrongly passed through sales book.

iii. Rs. 5,000 received from Manish, whose account had previously been written off as bad, was credited to his account.

iv. Rs. 6,000 was outstanding on account of rent was omitted to be recorded. 4

9. Trial balance of Ms. Muskan disclosed an excess debit of Rs. 450. Later on the following errors were located:

i. Goods worth Rs. 200 purchased from Anjali had been posted to her account as Rs. 250.

ii. A purchase of furniture for Rs. 1,500 was recorded in the purchases book.

iii. Instead of crediting Simran‟s Account with Rs. 140, it was debited with Rs. 410.

iv. Total of purchases book had been under casted by Rs. 50.

v. Rs. 1,500 paid in cash for an office equipment was charged to office expense account.

Pass the rectifying entries and prepare a suspense account. 6

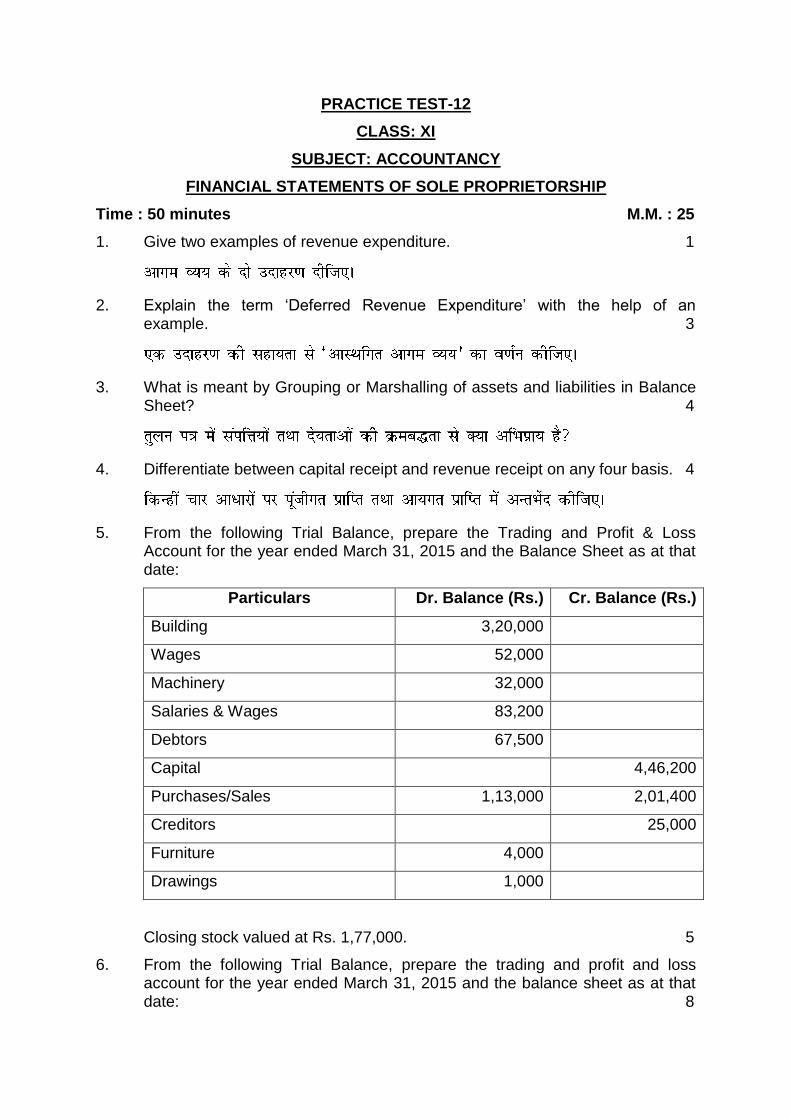

PRACTICE TEST-12

CLASS: XI

SUBJECT: ACCOUNTANCY

FINANCIAL STATEMENTS OF SOLE PROPRIETORSHIP

Time : 50 minutes M.M. : 25

1. Give two examples of revenue expenditure. 1

2. Explain the term „Deferred Revenue Expenditure‟ with the help of an example. 3

3. What is meant by Grouping or Marshalling of assets and liabilities in Balance Sheet? 4

4. Differentiate between capital receipt and revenue receipt on any four basis. 4

5. From the following Trial Balance, prepare the Trading and Profit & Loss Account for the year ended March 31, 2015 and the Balance Sheet as at that date:

Particulars Dr. Balance (Rs.) Cr. Balance (Rs.)

Building 3,20,000

Wages 52,000

Machinery 32,000

Salaries & Wages 83,200

Debtors 67,500

Capital 4,46,200

Purchases/Sales 1,13,000 2,01,400

Creditors 25,000

Furniture 4,000

Drawings 1,000

Closing stock valued at Rs. 1,77,000. 5

6. From the following Trial Balance, prepare the trading and profit and loss account for the year ended March 31, 2015 and the balance sheet as at that date: 8

Particulars Dr. Balance (Rs.) Cr. Balance (Rs.)

Capital 2,50,000

Plant & Machinery 50,000

Land & Building 60,000

Sales 4,50,000

Furniture & Other equipments 25,000

Trade Expenses 15,000

Cash at Bank 1,25,000

Wages & Salaries 30,000

Repairs 5,000

Purchases 3,00,000

Opening stock 1,00,000

Sundry Debtors/Sundry Creditors 50,000 60,000

Purchases Return 5,000

Rent 6,000

Discount 4,000

Drawings 5,000

Bills Receivable/Bills Payable 20,000 15,000

Bad Debts 2,000

Interest 5,000

The stock on March 31, 2015 was valued at Rs. 70,000.

PRACTICE TEST-13

CLASS: XI

SUBJECT: ACCOUNTANCY

FINANCIAL STATEMENTS OF SOLE PROPRIETORSHIP

(WITH ADJUSTMENTS)

Time : 50 minutes M.M. : 25

1. What do you understand by adjustment entry? 1

2. What is provision for doubtful debts? 3

3. Explain the following: 4

i) Contingent liability

ii. Unearned income

i)

ii.

4. What is the use of financial statements for potential investors? 4

5. Give journal entries for the following adjustments in financial statements: 5

i) Salaries Rs. 10,000 are outstanding

ii) Rs. 8,000 for rent have been received in advance

iii) Interest on capital Rs. 3,000

iv) Write off Rs. 4,000 as further bad debts

v) Insurance amounting to Rs. 2,000 is paid in advance

6. From the following trial balance, prepare trading and profit and loss account for the year ended March 31, 2015 and a balance sheet as at that date: 8

Particulars Dr. Balance (Rs.) Cr. Balance (Rs.)

Capital 8,000

Plant and Furniture 10,000

Furniture & Fittings 520

Stock on April 1, 2014 9,600

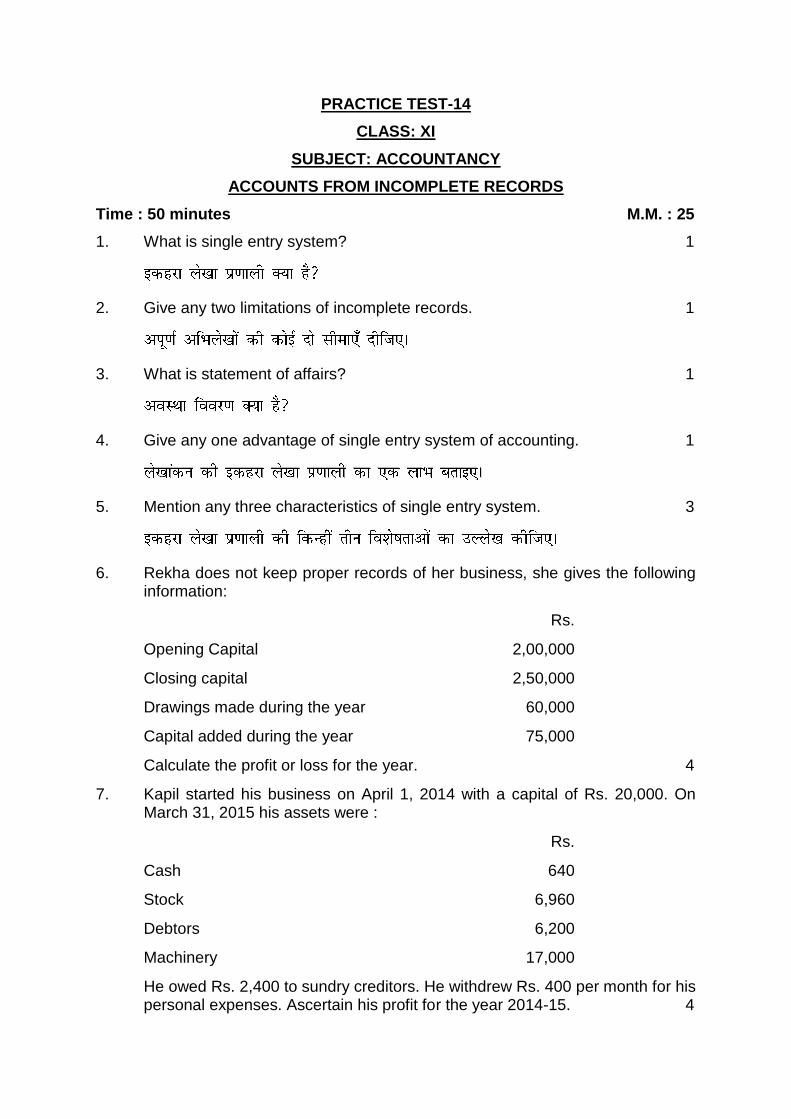

PRACTICE TEST-14

CLASS: XI

SUBJECT: ACCOUNTANCY

ACCOUNTS FROM INCOMPLETE RECORDS

Time : 50 minutes M.M. : 25

1. What is single entry system? 1

2. Give any two limitations of incomplete records. 1

3. What is statement of affairs? 1

4. Give any one advantage of single entry system of accounting. 1

5. Mention any three characteristics of single entry system. 3

6. Rekha does not keep proper records of her business, she gives the following information:

Rs.

Opening Capital 2,00,000

Closing capital 2,50,000

Drawings made during the year 60,000

Capital added during the year 75,000

Calculate the profit or loss for the year. 4

7. Kapil started his business on April 1, 2014 with a capital of Rs. 20,000. On March 31, 2015 his assets were :

Rs.

Cash 640

Stock 6,960

Debtors 6,200

Machinery 17,000

He owed Rs. 2,400 to sundry creditors. He withdrew Rs. 400 per month for his personal expenses. Ascertain his profit for the year 2014-15. 4

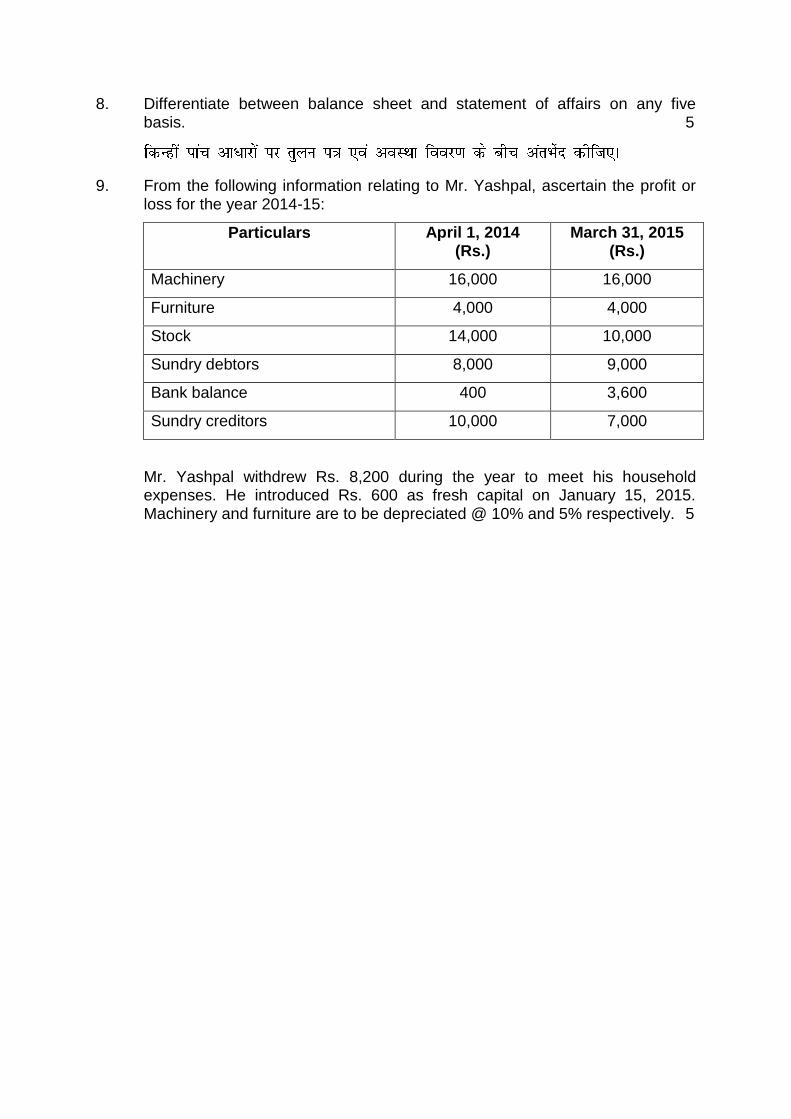

8. Differentiate between balance sheet and statement of affairs on any five basis. 5

9. From the following information relating to Mr. Yashpal, ascertain the profit or loss for the year 2014-15:

Particulars April 1, 2014 (Rs.)

March 31, 2015 (Rs.)

Machinery 16,000 16,000

Furniture 4,000 4,000

Stock 14,000 10,000

Sundry debtors 8,000 9,000

Bank balance 400 3,600

Sundry creditors 10,000 7,000

Mr. Yashpal withdrew Rs. 8,200 during the year to meet his household expenses. He introduced Rs. 600 as fresh capital on January 15, 2015. Machinery and furniture are to be depreciated @ 10% and 5% respectively. 5

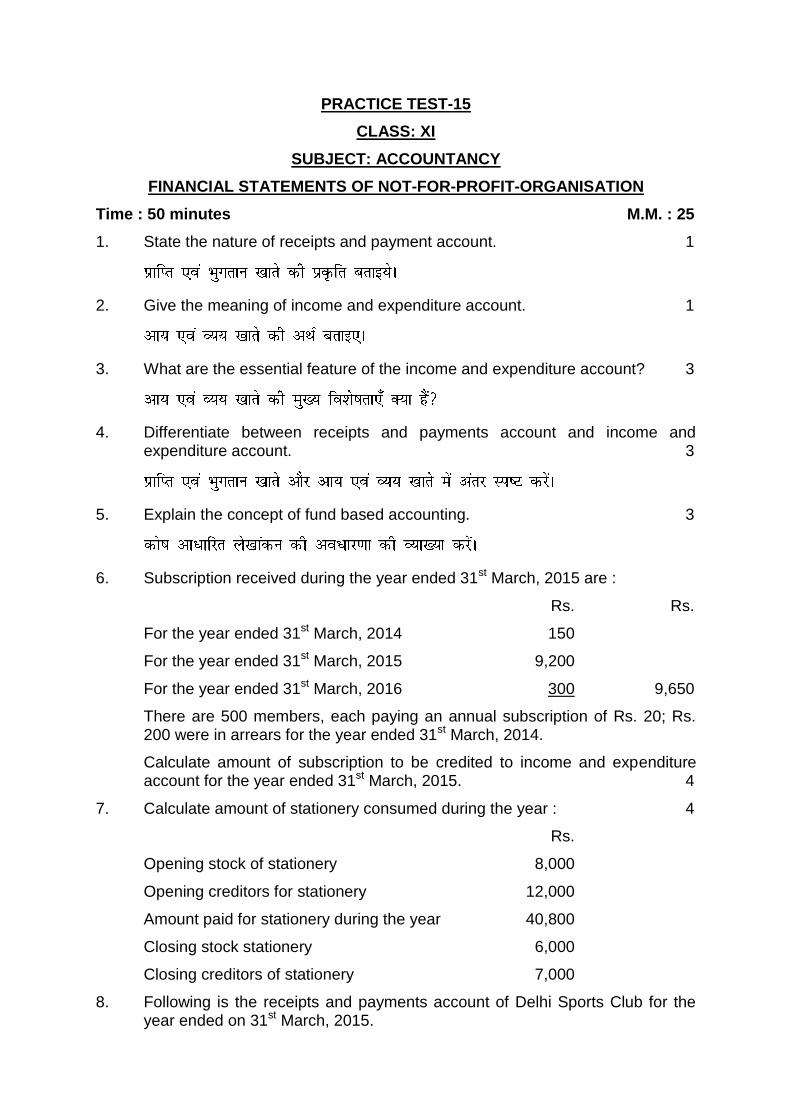

PRACTICE TEST-15

CLASS: XI

SUBJECT: ACCOUNTANCY

FINANCIAL STATEMENTS OF NOT-FOR-PROFIT-ORGANISATION

Time : 50 minutes M.M. : 25

1. State the nature of receipts and payment account. 1

2. Give the meaning of income and expenditure account. 1

3. What are the essential feature of the income and expenditure account? 3

4. Differentiate between receipts and payments account and income and expenditure account. 3

5. Explain the concept of fund based accounting. 3

6. Subscription received during the year ended 31st March, 2015 are :

Rs. Rs.

For the year ended 31st March, 2014 150

For the year ended 31st March, 2015 9,200

For the year ended 31st March, 2016 300 9,650

There are 500 members, each paying an annual subscription of Rs. 20; Rs. 200 were in arrears for the year ended 31st March, 2014.

Calculate amount of subscription to be credited to income and expenditure account for the year ended 31st March, 2015. 4

7. Calculate amount of stationery consumed during the year : 4

Rs.

Opening stock of stationery 8,000

Opening creditors for stationery 12,000

Amount paid for stationery during the year 40,800

Closing stock stationery 6,000

Closing creditors of stationery 7,000

8. Following is the receipts and payments account of Delhi Sports Club for the year ended on 31st March, 2015.

Receipts and payments account for the year ended on 31st March, 2015

Receipts Rs. Payments Rs.

To Balance B/d 18,000 By Salaries and Wages 15,000

To Subscriptions: By Office Expenses 5,000

2014 6,000 By Sports Equipments 12,000

2015 29,000 By Electricity Expenses 14,000

2016 5,000 40,000 By Travelling Expenses 6,000

To Donations 7,000 By Sundry Expenses 8,000

To Entrance Fees 15,000 By Balance c/d 20,000

80,000 80,000

Additional Information:

a) Outstanding subscription for 2014 was Rs. 8,000.

b) Outstanding salaries and wages Rs.6,000.

c) Depreciate sports equipment by 20%

Prepare Income and Expenditure Account for the year 2014-15 of the club from the above particulars. 6

PRACTICE TEST-16

CLASS: XI

SUBJECT: ACCOUNTANCY

COVERED : COMPUTERS IN ACCOUNTING

Time : 50 minutes M.M. : 25

1. A computer cannot function without the operating software. Give one reason in support of your answer. 1

2. What do you understand by grouping of accounts? 1

3. Write the name of any two utility software. 1

4. Explain the components of computer system. 3

5. Explain any three capabilities of a computer system. 3

6. Explain any three limitations of computer system. 3

7. Explain accounting information system (AIS) as a part of management information system (MIS). 3

8. „Computerised accounting is much better than manual accounting‟. Justify this statement by giving a comparison of manual accounting and computerised accounting. 4

9. Write short note on the following:

i) Readymade software

ii) Customised software

iii) Tailor-made software 2x3=6

i)

ii)

iii)