government of india india meteorlogical department ministry of earth sciences reference guide on

78

GOVERNMENT OF INDIA INDIA METEORLOGICAL DEPARTMENT MINISTRY OF EARTH SCIENCES REFERENCE GUIDE ON ADMINISTRATION, FINANCE & PROCUREMENT Office of the Director General of Meteorology Mausam Bhawan, Lodhi Road, New Delhi SEPTEMBER 2011

Transcript of government of india india meteorlogical department ministry of earth sciences reference guide on

GOVERNMENT OF INDIA INDIA METEORLOGICAL DEPARTMENT

MINISTRY OF EARTH SCIENCES

REFERENCE GUIDE ON

ADMINISTRATION, FINANCE & PROCUREMENT

Office of the Director General of MeteorologyMausam Bhawan,

Lodhi Road, New Delhi

SEPTEMBER 2011

Reference Guide on Administration, Finance & Procurement

ii

Edited by

Sh. Ram Prasad Lal

Compiled by

Shri Ramesh ChandShri V. K. Soni

Disclaimer: This is the compilation of presentations made during the training programme. However the relevant government rules may be kept in view. In case, if any instruction documented here is in conflict with GOI orders, the GOI orders will prevail. However this material can be used as a guiding material and cannot be quoted as reference document.

Reference Guide on Administration, Finance & Procurement

iii

FOREWORD

I am happy to note that the Budget & Planning Section of India Meteorological Department HQ is bringing out a Reference Guide on Administration, Finance & Procurement. This is first time that such a document has been prepared in India Meteorological Department.

2. Being a Scientific Department large number of Workshops, Symposia & Conferences were organized during past, covering diverse themes as sustainable development, Aviation Meteorology, Weather Forecasting, Tropical Storm and local service storm forecasting, Radar meteorology, risk management in Agriculture and Positional Astronomy etc. But few in house training were conducted during past on administration, procurement & stores. This was the weak area where continuous training is required in the department.

3. Needless to say that the driving force has been a constant endeavour to improve the services. The process has started by imparting various training to the Project Directors. Sensing the need of training in the field of administration, procurement & stores an orientation training programme for 3 days was conducted for Project Directors and officials dealing with Plan Projects during 02 May, 2011 to 04 May, 2011. On the basis of this training Budget & Planning Section at India Meteorological Department HQ, New Delhi took initiative to prepare a reference guide for guidance as per existing rules and regulation.

4. I congratulate the Budget & Planning Section for taking this initiative in preparing this document. I am sure that this reference guide will be useful for day to day administration, Procurement, Expenditure management, Policy decisions in the light of corresponding circumstances helping us to adjust the roadmap of future as per needs.

AVM (Dr.) Ajit TyagiDirector General of Meteorology

Reference Guide on Administration, Finance & Procurement

iv

Reference Guide on Administration, Finance & Procurement

v

PREFACE

It has been observed that Project Directors are facing problem in project formulation, procurement, expenditure management due to reason for not following the procedures properly regarding Administration, Finance & Procurement as per Government of India Guidelines issued under various rules & regulation. The reason behind this is the lack of training of IMD officers in related field. Therefore a one week orientation training programme for Project Directors and officials dealing with plan projects at RMCs was conduct from 02 May 2011 to 4 May 2011.

The manual on Administration, Finance and procurement have been prepared in conformity with the applicable directives contained in the new Government Financial Rules, 2005, Delegation of Financial Power Rules at present etc. Concerted efforts have been made to covers all major aspects of Budget and Planning, Procurement, finance and account management, project management, works, store management etc so that to introduce quality, competitions and execution in public administration. This is a compilation of presentation during the training programme.

This document has seven chapters.

1. Budget & Planning2. Procurement3. Finance & Account Management4. Project Management5. Works6. Store Management7. Miscellaneous issues

All chapters have been covered by concerned officers of this department. Chapter 2 deals with all aspects of procurement. Chapter 3 deals with finance and account management under which processing of bills by DDO and functioning of Cash and accounts sections in IMD have been broadly presented. Chapter 4 deals with project management guidelines for formulation appraisal and approval of Govt. Plan funded project schemes. Chapter 5 deals with guidelines for submission of works related proposal to DGM office by the field offices. Chapter 6 deals with store management and disposal. Chapter 7 deals on the medical rules and regulations as on date.

All IMD OFFICES are advised to follow the relevant government rules issued by government of India/ Ministry etc. In case of any reference material in the document is in conflict with Govt. of India orders, the government of India orders will prevail.

Reference Guide on Administration, Finance & Procurement

vi

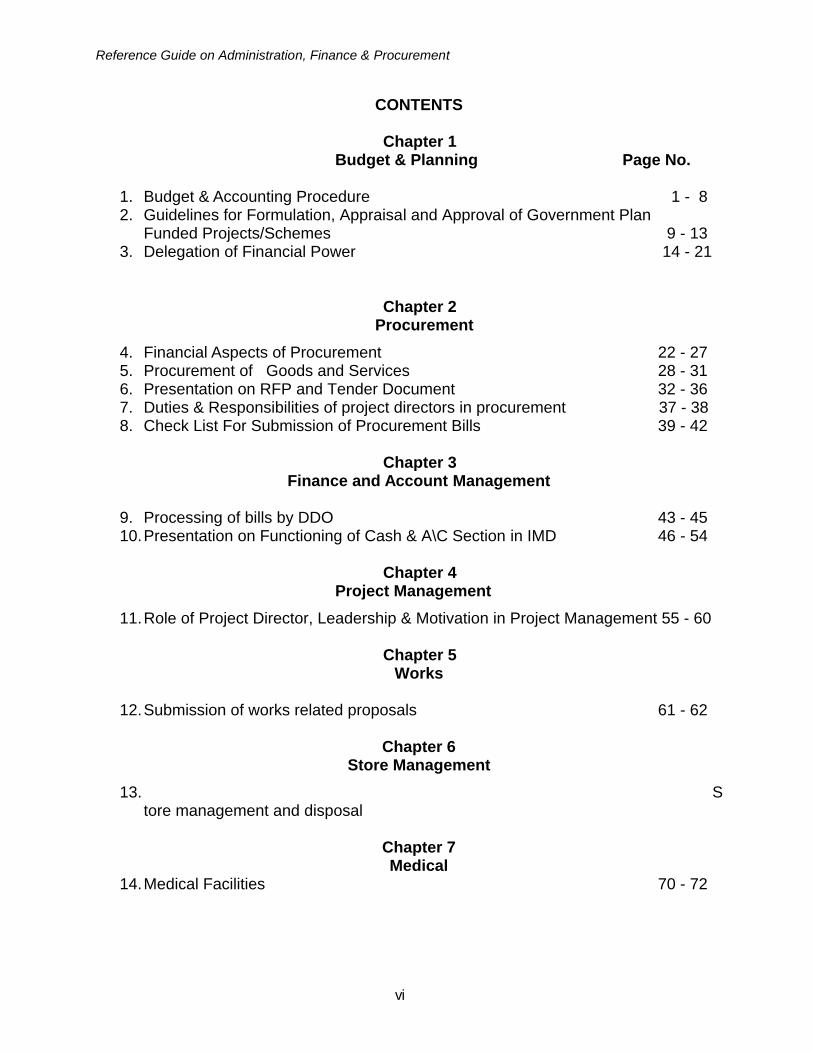

CONTENTS

Chapter 1Budget & Planning Page No.

1. Budget & Accounting Procedure 1 - 82. Guidelines for Formulation, Appraisal and Approval of Government Plan

Funded Projects/Schemes 9 - 133. Delegation of Financial Power 14 - 21

Chapter 2 Procurement

4. Financial Aspects of Procurement 22 - 275. Procurement of Goods and Services 28 - 316. Presentation on RFP and Tender Document 32 - 367. Duties & Responsibilities of project directors in procurement 37 - 388. Check List For Submission of Procurement Bills 39 - 42

Chapter 3Finance and Account Management

9. Processing of bills by DDO 43 - 4510.Presentation on Functioning of Cash & A\C Section in IMD 46 - 54

Chapter 4Project Management

11.Role of Project Director, Leadership & Motivation in Project Management 55 - 60

Chapter 5Works

12.Submission of works related proposals 61 - 62

Chapter 6Store Management

13. Store management and disposal

Chapter 7Medical

14.Medical Facilities 70 - 72

Reference Guide on Administration, Finance & Procurement

1

CHAPTER 1

BUDGET & PLANNING

A government budget is defined as a legal document that is passed by the legislature, and approved by the chief executive-or President. The two basic elements of any budget are the revenues and expenses. Unlike a pure economic budget,Government Budget is designed for optimal allocation of scarce resources taking into account larger sociopolitical considerations.

The main objective of Government financial management is to determine how well the financial and resource management responsibilities have been discharged. This is based amongst others, on a comparison of accomplishments against the fiscalpolicies and the time bound Government programmes. These fiscal policies and programmes determine the Budget of the Government, through which the amounts of revenue to be raised and the allocation of sums for the respective Governmentprogrammes and purposes are set. Budgeting therefore, involves determining for a future time period on what is to be done and achieved, the manner in which it is to be done and the resources required for the same. It requires the broad objectives of the Government to be broken down into detailed work plans for each programme and sub-programme, activity and projects for each unit of the Government organization.

Budget preparation in India is an iterative process between the Ministry of Finance/Planning Commission and the spending Ministries. It is a combination of top down approach with the Ministry of Finance and the Planning Commission issuingguidelines or communicating instructions to spending Ministries, and a bottom-up approach, wherein the spending Ministries present requests for budget allocation. Some of the salient features of Union Budget are as follows-

1. Budget is prepared on Cash Basis: Whatever is expected to be actually received or paid under proper sanction during a financial year (including arrears of the past years) should be budgeted in that year.

2. Rule of Lapse: All appropriations granted by the Parliament expire at the end of financial year and no deduction of unspent budget can be appropriated for meeting the demands in the next financial year. Thus, all unutilized funds within the year ‘lapse’ at the end of the financial year.

3. Realistic Estimation: It is essential that the provisions in the budget should be restricted to the amount required for actual expenditure. The Finance Ministry isinterested in seeing that the Departments do not obtain more/less money than what they really need. If a Department is allotted funds which it does not need, it will deprive some other Department from getting the required resources.

4. Budget to be on Gross/Net Basis: Budget is prepared both on the gross basis and net basis. The gross figures of receipts and expenditure of the Government are reflected separately for voting by Parliament and the Departments/Ministries are normally not permitted to utilize the receipts or deduct expenditure in their budget proposals. Net basis of budgeting is done in case of some Grants e.g. Defence

Reference Guide on Administration, Finance & Procurement

2

Ordnance Factories, and Department of Posts wherein the departmental receipts are allowed to be utilized and outlays on gross as well as net basis are reflected.

5. Form of Estimates to Correspond to Accounts: It is essential that the form in the budget estimates correspond to that of Government accounts as it is from theseaccounts, that the performance of the Government is judged and the estimation forsubsequent year made. If these are prepared in different forms, financial control will also become difficult.

6. Estimates to be on Departmental Basis: Each Department prepares estimates for receipts and expenditure separately. Generally one Demand or Grant is allocated in respect of each Ministry/Department. In case of certain large Departments/Ministriesmore than one Demands for Grants is allocated in terms of General Financial Rules.

The Budget is presented to the Parliament in such form as the Finance Ministry may decide after considering the suggestions, if any, made by the Estimates Committee. Broadly the Budget documents depict information relating to receipts andexpenditure for three years i.e.-

i. Through Budget Estimates (BE) of receipts and expenditure in respect of Budget year(current financial year);

ii. For the year preceding the Budget year (current year) through Revised Estimates(RE); andiii. Actuals of the second year proceeding the Budget year.Budget thus sets forth the receipts and the expenditure of the Government for three

consecutive years.

BUDGET MANUAL OF THE GOVERNMENT OF INDIA

Budget Division of Department of Economic Affairs, Ministry of Finance, brought out a Budget Manual in September 2010. The Budget related instructions and guidelines were till now available in the form of executive instructions and guidelines etc. including the annual Budget Circulars. These, however, did not cover many facets of the Budget making process. There was, therefore, a felt need for a comprehensive Manual to bring together the entire Budget related features and activities

The Budget Manual is a comprehensive document which captures the content of the Union Budget as well as the procedures and activities connected with the preparation of the Annual Budget. The processes and guidelines have been simplified and put in a logical sequence for easy comprehension. The Annexes have been added wherever required for providing a more holistic perspective on related matters. This Manual unravels the detailed processes involved in the entire gamut of Budget preparation. It isalso expected to bring about greater transparency on the subject.

This Manual provides deeper understanding to the officials of Ministries/Departments of their roles and responsibilities with respect to preparation of documents and statements included in the Budget. It is expected to serve as a guidebook for uniform administration of the Budgeting procedures and practices in the Government of India including the line Ministries and Departments.

Reference Guide on Administration, Finance & Procurement

3

PLANNING PROCESS:

Planning Commission plays an important role in the budgetary process and the public finances of the country. The Planning Commission, besides formulating and monitoring development Plans, advises the Union Government regarding the desirable transfer of resources to the States, essential for development outlays. PlanningCommission not only prepares the Plans but through the years over its annual scrutiny, at the time of considering the annual Plan, of overall position of resources and their application, it has played an important role every year in formulation of the Budgets of the Centre and the States.

The Planning Commission holds extensive discussions with the Central Government and the States, which submit in advance their own estimates of resources and expenditure for the Plan period. Planning Commission prepares the Five Year Plans taking into account the resources that would be available and the needs for development. (The Five Year Plans are approved by the National Development Council). The discussions in the Planning Commission with the Government takes place at two levels, viz. (i) officials interest and (ii) between Ministers and Planning Commission.

Thereafter, the Planning Commission finalizes the draft Five Year Plan for the country, which is placed before the National Development Council. After approval by the Council, the Plan is placed before the Parliament. Within the framework of the Five Year Plan, each year’s Plan (Annual Plan) is separately considered and finalized through procedures as mentioned at (i) and (ii) above. The size of the Annual Plans of the Centre and the States are finalized on the basis of these discussions. The Centre’s contribution in the shape of loan and grant for a State’s Annual Plan is also determined.The Annual Plans of the Centre and the State are recast within the ceilings fixed in these discussions and the necessary budget provisions made as per the Annual Plan thus finalized.

The Planning Commission prescribe each year the form and the manner in which proposals are required to be submitted to them for determining the Plan allocations for the ensuing year. The Financial Adviser in each Ministry / Department of the CentralGovernment will accordingly call for requisite data from the estimating authorities, public sector and other enterprises under the control of the Ministry / Department, etc. The approved Plan allocations will be communicated by the Planning Commission to theCentral Ministries / Departments, indicating the total Plan outlay approved for each scheme / organization and the extent to which it is to be met from extrabudgetaryresources and from provisions in the Demands for Grants.

Based upon the Gross Budgetary Support (GBS) package for the Plan schemes conveyed to the Planning Commission by the Ministry of Finance for that particular year, decisions on the allocation to various Ministries and Departments is conveyed to the concerned Ministries/Departments and the Ministry of Finance, Budget Division for inclusion in the Budget for the ensuing financial year.

Reference Guide on Administration, Finance & Procurement

4

STRUCTURE OF GOVERNMENT ACCOUNTS

In accordance with Constitutional requirements Government accounts are maintained in the following three categories:

Part I Consolidated FundPart II Contingency FundPart III Public Account

CONSOLIDATED FUND OF INDIA (Part-I):

Under Article 266(1) of the Constitution of India, all revenues received by the Government of India, all loans raised by the Government by issue of treasury bills, loans or Ways and Means advances and all moneys received by the Government inrepayment of loans shall form one consolidated fund to be titled the " Consolidated Fund of India". Divisions Under Consolidated Fund of India-

Revenue Account, Capital Account and Debt,Loans & Advances: Expenditure and Receipts Therein:

The Consolidated Fund of India has the following two divisionsRevenue AccountCapital Account

Revenue Account- Expenditure/Receipts: The Revenue Account deals with theproceeds of taxation and other receipts classed as Revenue and expenditure met there from.

Capital Account-Expenditure/Receipts: The Capital Account deals with expenditureincurred with the purpose of either increasing the concrete assets of durable nature or of reducing recurring liabilities. It is logical otherwise to meet Capital expenditure from borrowed funds, the liabilities in respect of which are spread over a number of years, as the benefits arising from Capital expenditure flow over a period of years. CapitalAccount also includes various types of Capital Receipts. The Capital Account comprises of the following sections:

a. The section ‘Receipt heads (Capital Account)’ deals with receipts of a Capitalnature which cannot be applied as a set off to Capital Expenditure;

b. The section ‘Expenditure heads (Capital Account)’ deals with expenditure incurredwith the object either of increasing concrete assets of a material and permanent character or of reducing recurring liabilities. It also includes receipts of a Capital nature intended to be applied as set off to Capital expenditure; and

c. The sections ‘Public Debt’ and ‘Loans and Advances’, comprise of loans raised and their re-payments such as internal debt, external debt and their recoveries.

For Budgeting purposes, the distinction between Revenue expenditure and Capital expenditure is of crucial importance, for which uniform principles are followed both at the Centre and in the States. The Capital account also includes loans raised by Government and their repayments and loans and advances paid by the Government and their recoveries.

Reference Guide on Administration, Finance & Procurement

5

ACCOUNTING SYSTEM:

The Government Accounts have necessarily to comply with the budgetary structure of the country. Since budgets in India are on an annual basis, governmental transactions are also finalised in the accounts on an annual basis. However, theGovernment Accounts of each financial year are kept open for a certain period in the following year for adjusting transactions which took place in the previous financial year.

The government accounts in India are kept on a cash basis. Therefore, only actual receipts and payments during the financial year are taken into account with no outstanding liabilities or accrued income included. All cash appropriations lapse at theclose of the financial year.

SIX TIER ACCOUNTING CLASSIFICATION AND WHAT EACH TIER SIGNIFIES:

The Budget of Government is linked to the accounts and Government transactions accounted for under the Consolidated Fund, Contingency Fund and the Public Account of India.

CLASSIFICATION SYSTEM:

Each Division in the Consolidated Fund and the Public Accounts is divided into sectors, which may in some cases be further divided into sub-sectors and then into the six tiers of accounting classification. The number of classification in the Detailed Demands for Grants are not allowed to go beyond the standard six tiers indicated as under-

1. Major Head- 4 digits (Function);2. Sub-Major Head- 2 digits (Sub-Function);3. Minor Head- 3 digits (Programme);4. Sub-Head- 2 digits (Scheme);5. Detailed Head- 2 digits (Sub-Scheme); and6. Object Head- 2 digits (Object Head or Primary Units of Appropriation)

LIST OF MAJOR AND MINOR HEADS OF ACCOUNTS:

Based on the classification into Revenue and Capital divisions, the transactions are grouped into sectors which are further sub-divided into sub-sectors and Major Heads of account. The major heads normally indicate within each sector/sub-sector thebroad functions of a particular department of Government.

In the four digit codes allotted to the major heads, the first digit indicates whether the major head is a Receipt head/ Revenue expenditure head/ Capital expenditure head or a Loan head. The last three digits are the same for corresponding major heads in Revenue receipts section/Revenue expenditure section/Capital receipts/expenditure section and Loans and Advances section. The Receipt Major

Reference Guide on Administration, Finance & Procurement

6

heads are assigned the block 0020 to 1999, Expenditure Major Heads on Revenueaccounts from 2011 to 3999, Expenditure Major heads on Capital accounts from 4001 to 5999 while all Capital receipts are classified under Major head 4000. Major heads under Public debt is from 6001 to 6004 and those under loans and advances/inter-statesettlement and Contingency Fund from 6001 to 8000 and the Major heads under Public Account from 8001 to 8999. In the loan section Major heads have been opened with reference to functions and purposes instead of the beneficiaries.

The Sub Major heads are opened under a Major Head to record those transactions which are of a distinct nature and of sufficient importance to be recorded exclusively, but at the same time allied to the function of the Major Head.

The Major and Sub-Major heads are subdivided into Minor heads. The minor heads correspond to programmes or broad groups of programmes. It is output oriented rather than organization or input oriented. The classification upto the Minor Head level are prescribed by the Controller General of Accounts in consultation with the C&AG and is common to the Central and State Governments.The complete list of Major and Minor Heads of Account along with the Correction Slips therein are available at the website of the Controller General of Accounts (CGA) at cga.nic.in.

Sub Head/Detailed Head/Object Head

Sub Head represents schemes, the detailed head represents Sub-Schemeswhile the Object Head represents the objects/items (e.g. Pay, DA, HRA, Rewards, Gratuity, etc.) on which the expenditure is incurred. Each of these levels has been allotted a two digit code. Wherever it is not feasible to break up the objects of expenditure into such details, the codes provided for aggregates of certain items may be used instead for computer processing.

For example, where it is not possible to indicate Pay, DA, HRA, CCA etc. separately, the code for salaries may be used for representing the aggregate of these items. The Object Heads have been prescribed under Government of India’s Ordersbelow Rule 8 of Delegation of Financial Power Rules. The power to amend or modify these object heads and to open new Object Heads rest with Department of Expenditure of Ministry of Finance on the advice of the Comptroller and Auditor General of India.The Budget Heads exhibited in estimates of receipts and expenditure framed by the Government or in any appropriation order should conform to the prescribed rules of classification in accordance with Rule 74 of the General Financial Rules.

IMPORTANCE OF OBSERVING CORRECTNESS IN CLASSIFICATION CO-RELATING TRANSACTIONS AS CLASSIFIED IN THE BUDGET/ACCOUNTS WITH THE FUNCTIONS: Keeping in view the form of accounts prescribed under the Constitutional provisions under the advice of C&AG, the Detailed Demands for Grants presented by the Ministries to Parliament, should also adopt the same six tier numericcodification pattern.

Reference Guide on Administration, Finance & Procurement

7

FLOW OF GOVERNMENT ACCOUNTS

The Civil Account Manual contains detailed instructions and procedures relating to payments made by PAOs, CDDOs of Civil Ministries/ Departments of Central Government and accounting, compilation, consolidation of annual account etc. These instructions cover most of the facets thereof and include standard forms of various accounts registers/ records/returns to be maintained and/or submitted by such offices.

Reference Guide on Administration, Finance & Procurement

8

PREPARATION OF ANNUAL ACCOUNTS

STATEMENT OF BUDGET ESTIMATES (FINAL):

After the pre-Budget meetings are over, and the approved ceilings for expenditure, as finalised in these meetings, are communicated including ceilings for Plan and Non-Plan expenditure (The Revenue and Capital expenditure break up is finalized within the concerned Ministries/Departments by the Financial Advisers) the Financial Advisers are required to prepare the Statement of Budget Estimates (Final)

NOTES ON DEMANDS: The Notes on Demands for Grants appear in Expenditure Budget Volume-2. These are intended to depict a brief summation of the budget allocations as appearing in the Expenditure Budget Volume-2. Hence, these arerequired to be brief, to the point and should be linked to the item for which the Budget allocations have been reflected. Further and more elaborate detailing on schemes can be made in the Expenditure Budget Volume-1.

Reference Guide on Administration, Finance & Procurement

9

GUIDELINES FOR FORMULATION, APPRAISAL AND APPROVAL OF PLAN SCHEMES FORMULATION

Presentation by Ram Prasad Lal Director ( Budget & Planning)

GFR Rule 78 describes the procedure for Plan or Non plan Expenditure : Plan expenditure representing expenditure on Plan outlays approved for each scheme or organisation by the Planning Commission and indicating the extent to which such outlays are met out of budgetary provisions shall be shown distinctly from the other (Non-Plan) expenditure in the accounts as well as in the Budget documents.

In pursuance of the need felt by the Government to reform investment approval and implementation procedures, the Government had set up a Committee in September, 2001 to examine the existing procedures and suggest measures to simplify and expedite the process. The Committee divided its task in two parts, Part-I concentrating on issues that arise from the conceptualization of the project to the stage of investment approval, and Part-II covering all implementation and operational issues starting from the stage of investment approval till the commissioning of the project.

Rigorous project formulation and appraisal have a major bearing on the relevance and impact of projects as well as on their timely implementation. The Committee has identified indifferent quality of project formulation and appraisal as major factors which contribute to bottlenecks at the implementation stage and consequential time and cost over-runs. Failure to identify constraints in the availability of land, inadequate environmental impact analysis and lack of consultation with stakeholders at the time of project formulation can retard the implementation and impact of the project at a later stage. Additional time and effort spent at the project formulation and appraisal stage would be time well-spent and result in qualitative improvement in terms of ultimate project impact.

After having considered the matter carefully, the following guidelines are laid down for formulation and appraisal of Government funded plan schemes/projects, covering all sectors and Departments.

Guidelines for Formulation, Appraisal and Approval of Government Plan Funded Projects/Schemes

Government have prescribed, from time to time, procedures/mechanisms fortaking up public investment/expenditure programmes that are viable from the socioeconomic point of view, avoid thin spreading of resources and/or multiplicity ofimplementation structures and channels and facilitate simple, speedy, efficient andstreamlined decision making. With the commencement of the XII Plan period, Guidelines on the subject will be issued afresh, so as to rationalize the Scheme of delegation further, align it more closely with the rapidly changing economic environment, empower Ministries/Departments further for undertaking investment

Reference Guide on Administration, Finance & Procurement

10

programmes and make the entire procedure more responsive and resilient in ensuring timely and well-informed decision making.

FEASIBILITY REPORT (FR) The FR should focus on analysis of the existing situation, nature and magnitude

of the problems to be addressed, need and justification for the project in the context of national priorities, alternative strategies, initial environmental and social impact analysis, preliminary site investigations, stake holder commitment and risk factors.

The FR should establish whether the project is conceptually sound and feasible and enable a decision to be taken regarding inclusion in the Plan and preparation of a DPR.

The FR should present a rough estimate of the project cost. Consultation with stakeholders should be held to ensure involvement of stakeholders in the project concept and design.

IN- PRINCIPLE APPROVAL OF PLANNING COMMISSION

The Administrative Ministry should send the FR to the Planning Commission for ‘in-principle’ approval, to enable the project/scheme to be included in the Plan of the Ministry/Department.

The Administrative Ministry should prepare the DPR for the project/scheme after obtaining ‘in-principle’ approval of the Planning Commission.

The various stakeholders in the project should continue to be associated while preparing the DPR.

The services of Experts/professional bodies may be hired for preparation of the DPR, if considered necessary.

PREPARATION OF DPR & EVALUATION

The DPR must address all issues related to the justification, financing and implementation of the project/scheme.

The Terms of Reference (TOR) for preparation of the DPR should cover all aspects of the generic DPR structure.

Evaluation arrangements for the project, whether concurrent, midterm and/or post-project, should be spelt out in the DPR.

It may be noted that continuation of projects/schemes from one Plan period to another will not be permissible without an independent, in depth evaluation.

GENERIC STRUCTURE OF THE DPR

Context/background Problems to be addressed Project Objectives Target beneficiaries Project strategy

Reference Guide on Administration, Finance & Procurement

11

Legal Framework Environmental impact assessment On-going initiatives Technology issues Management arrangements

1. Means of Finance and Project Budget: This section should focus on means of finance, evaluation of options, project budget, cost estimates and phasing of expenditure.

2. Time frame: This section should indicate the proposed ‘Zero’ date for commencement and also provide a PERT/CPM chart, wherever relevant.

3. Risk analysis 4. Evaluation: This section should focus on lessons learnt from evaluation of similar

projects implemented in the past. 5. Success criteria: Success criteria for each Deliverable / Output of the project

should also be specified in measurable terms to assess achievement against proximate goals.

6. Financial and economic analysis 7. Sustainability: Issues relating to sustainability, including stakeholder commitment,

operation and maintenance of assets after project completion, and other related issues should be addressed in this section.

CONTINUATION OF ON-GOING SCHEMES FROM XI TO XII PLAN

At the beginning of each Five Year Plan detailed guidelines are issued by Ministry of Finance after the advise and consultation with Planning Commission of India. The guidelines for 12th Five Year Plan are yet to be notified. Based on instructions of 11th

Five Year Plan following procedures are likely to be followed during 12th Five Year Plan.

For continuation of the Schemes in the XII Plan, the Schemes are subjected to evaluation through an independent, impartial and reputed agency and the evaluation reports put through a rigorous scrutiny with regard to performance in the XI Plan and recommendations with regard to the following:

Whether the Scheme needs to be continued in XI Plan or dissolved forthwith; In case it is to be continued, then:

o Need for improvements;o Phasing of Expenditure in the XI Plan for each component of the Scheme;o Setting of physical and financial milestones/targets for the XII Plan for

each component.o The administrative Ministry can approve the continuance of the scheme

for the XII Plan period, if and only if:o (a) No major change in the content or parameters of the scheme is

proposed; any change in basic parameters, ( e.g., change in objectives, quantum, pattern and extent of subsidy, user fee, delivery mechanism, population coverage / beneficiary definition, eligibility conditions /criteria).

Reference Guide on Administration, Finance & Procurement

12

o (b) The projected requirement of funds for implementing the Scheme over the Plan period is within the outlay approved by Planning Commission;

CONDITION FOR EXERCISING DELEGATION OF FINANCIAL POWERS

The delegation of financial powers contained in this OM will be exercised only where necessary/requisite funds are available in the Annual Plan and the Five Year Plan outlay as per the Phasing of the Project/Scheme. The powers will continue to be governed by procedural and other instructions issued by Government from time to time, e.g., General Economy Instructions.

INSTITUTIONAL STRUCTURE FOR APPRAISAL OF PLAN SCHEMES

Standing Finance Committee (SFC) (25.0 to < 100 .00 Cr)

ChairpersonSecretary of the Administrative Ministry/DepartmentMember Financial Advisor of the Administrative Ministry/Department Joint Secretary in Charge of the Subject Division Representative of the Planning Commission, Department of Expenditure and

any otherMinistry/Department that the Secretary/Financial Advisor may suggest can also be invited, asper requirement.

INSTITUTIONAL STRUCTURE FOR APPRAISAL OF PLAN SCHEMES / PROJECTS

Expenditure Finance Committee (EFC) (100.00 to < 300.00 Cr)

For proposals costing less than Rs 300 Crore

Secretary of the Administrative Ministry/Department ChairmanSecretary (Planning Commission) or his representative MemberSecretary (Department of Expenditure) or his representative MemberFinancial Advisor of the administrative Ministry/Department Member - Secretary

For proposals costing Rs 300 Crore and above

Secretary (Department of Expenditure) ChairmanSecretary (Planning Commission) or his representative MemberSecretary of the Administrative Ministry MemberFinancial Advisor of the administrative Ministry/Department Member - Secretary

Reference Guide on Administration, Finance & Procurement

13

APPROVAL LIMITS FOR ORIGINAL COST ESTIMATES

Reference Guide on Administration, Finance & Procurement

14

Delegation of Financial Power to Director General of Meteorology

Presentation by Ramesh Chand Director(Budget)

Delegation of Financial Power to DG, IMD

In exercise of the powers vested in Secretary, MoES under Delegation of Financial Power Rules and in terms of Rule 13(2) of DFPR, Secretary, MoES in partial modification to the earlier OM NO.GW-50000/SFS dated 28th Nov.,2008 on the subject, hereby enhances the financial power to the Director General of Meteorology, IMD to Rs.5 crores for all the items (24 items) of expenditure mentioned therein except for following, where approval of Ministry would be necessary:

Any case of resultant single tender (i.e. single tender or effective single tender after Technical Evaluation) or

Any order not placed on OEM or Any order to foreign principals where their Indian Agents are not

registered/enlisted with DGS & D or Holding any international Conferences/Workshops/Meetings/Seminars etc or Entering into any international agreement or contract for technical collaboration &

consultancy services or Entering into any national agreement or contract for technical collaboration &

consultancy services whose total value exceeds Rs.2.00 crores or Write-of-looses or Re-appropriation of funds from one budget head to another.

The delegated powers shall be subject to the following Concurrence of Finance Officer (FO) shall be obtained in all the cases covered

under delegated powers of DGM. The Director General of Meteorology shall be responsible for ensuring that the

delegated powers are subject to the observance of the procedure and restriction laid down in the General Financial Rules, Delegation of Financial powers Rules and other orders issued by the Ministry of Finance , Central vigilance commission or other ministries from time to time.

All orders with regard to ban on creation of posts, ban on filling of vacancies etc. issued by the Government will be applicable. Clearance from concerned ministries, like Ministry of Works and Housing, Department of Economics Affairs etc. will have to be obtained as hitherto.

*For cases covered under delegated powers of DGM, if Fo does not agree with theproposal or if FO is on long leave/tour then such cases may be sent to Controller of Accounts, MoES for consideration/concurrence whose office is stationed in IMD complex.

Reference Guide on Administration, Finance & Procurement

15

*Since the powers of JS&FA shall be exercised by the Finance Officer, therefore, instead of the diary number of JS&FA, the sanction orders would carry the diary number of the F.O.

Item Covered Under OM NO.GW-50000/SFS dated 28th Nov.,2008 Bicycle Electric Gas & Water Charges Fixture & Furniture (Purchase & Repair) Freight & Demurrage Hire of office Furniture fan etc Land (Acquired from/ through state Govt.) Legal Charges Motor Vehicles-Maintenance upkeep & repair. Municipal Rate & Taxes

Power to sanction works including Petty Works & Repair Postal & Telegraph Charges Printing & Binding Publication Rent – ordinary office accommodation*

o Where the accommodation is entirely utilized for the officeo Where the accommodation is used partly as office and partly as residenceo For residential and other purposes

Repairs and removal of machinery (Where the expenditure is not of a capital nature)*

Staff paid from contingencies i) Purchase of stationary stores* ii) Local purchase of petty stationary stores iii) Local purchase of rubber stamps and office seals Stores* Stores required for the works Other stores i.e. stores required for the working of an establishment, instruments,

equipments and apparatus Supply of uniforms, badges and other articles of clothing etc. and washing

allowance Telephone charges Computers (including personal computers)* Hire and maintenance of computers of all kinds* Power to incur miscellaneous expenditure Sanction of schemes* Administrative approval and expenditure sanction to Capital works and Major

Works*

Reference Guide on Administration, Finance & Procurement

16

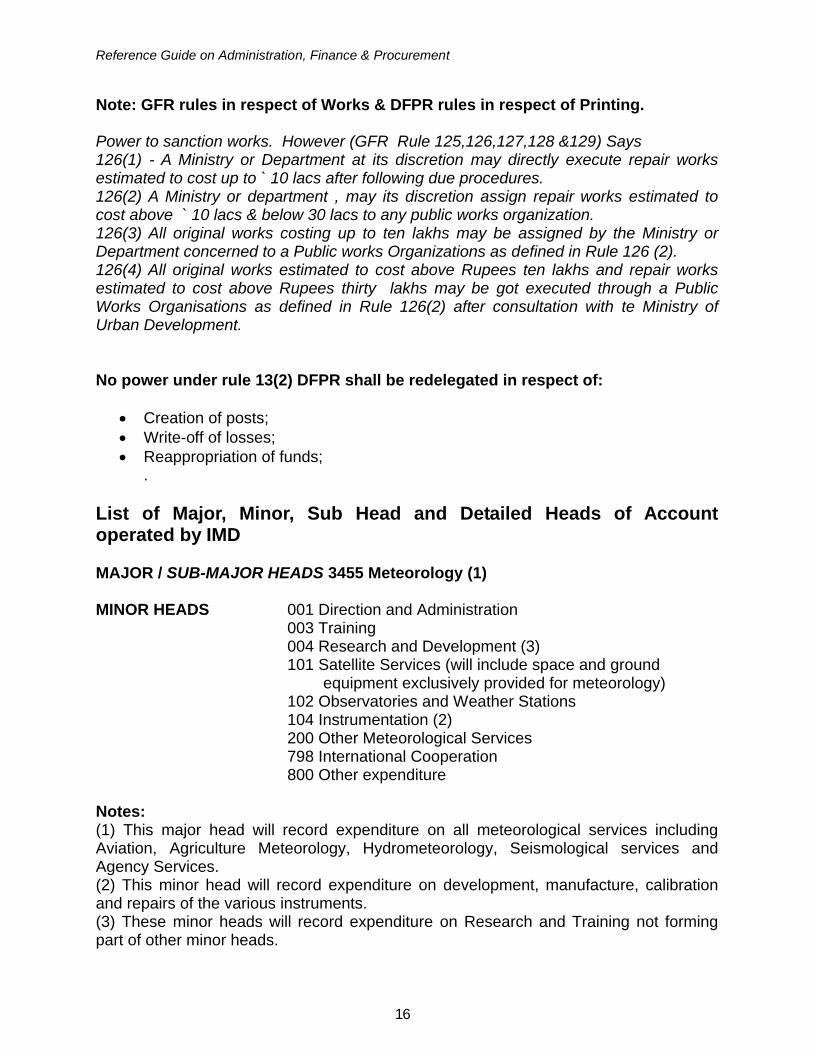

Note: GFR rules in respect of Works & DFPR rules in respect of Printing.

Power to sanction works. However (GFR Rule 125,126,127,128 &129) Says126(1) - A Ministry or Department at its discretion may directly execute repair works estimated to cost up to ` 10 lacs after following due procedures.126(2) A Ministry or department , may its discretion assign repair works estimated to cost above ` 10 lacs & below 30 lacs to any public works organization.126(3) All original works costing up to ten lakhs may be assigned by the Ministry or Department concerned to a Public works Organizations as defined in Rule 126 (2).126(4) All original works estimated to cost above Rupees ten lakhs and repair works estimated to cost above Rupees thirty lakhs may be got executed through a Public Works Organisations as defined in Rule 126(2) after consultation with te Ministry of Urban Development.

No power under rule 13(2) DFPR shall be redelegated in respect of:

Creation of posts; Write-off of losses; Reappropriation of funds;

.

List of Major, Minor, Sub Head and Detailed Heads of Account operated by IMD

MAJOR / SUB-MAJOR HEADS 3455 Meteorology (1)

MINOR HEADS 001 Direction and Administration003 Training004 Research and Development (3)101 Satellite Services (will include space and ground

equipment exclusively provided for meteorology)102 Observatories and Weather Stations104 Instrumentation (2)200 Other Meteorological Services798 International Cooperation800 Other expenditure

Notes:(1) This major head will record expenditure on all meteorological services includingAviation, Agriculture Meteorology, Hydrometeorology, Seismological services andAgency Services.(2) This minor head will record expenditure on development, manufacture, calibrationand repairs of the various instruments.(3) These minor heads will record expenditure on Research and Training not formingpart of other minor heads.

Reference Guide on Administration, Finance & Procurement

17

MAJOR / SUB-MAJOR HEADS - 5455 Capital Outlay on Meteorology

MINOR HEADS (Programmes)001 Direction and Administration003 Training101 Satellite Services102 Observatories and Weather Stations200 Other Meteorological Services800 Other expenditure

SUB HEAD / DETAILED HEAD

Director General of Meteorology Training R & D Services Space Meteorology Observatory Services Operation & Maintenance Meteorological Services Agromet Advisory Services Aviation Meteorology Airborne Platforms & FDP World Meteorological

Organization

International Seismological Centre

Externally Aided Projects World Bank Aided Projects Departmental Canteen Seismic Hazard and Risk

Evaluation Modernization of IMD Common Wealth Games &

Dedicated Weather Channel

The object heads under Revenue -3455 Meteorology

01 Salaries02 Wages03 OTA06 Medical Treatment11 DTE12 FTE13 Office Expenses 14 Rent Rates and Taxes16 Publication17 BCTT21 Supplies & Material

24 POL26 Advertisement & Publicity27 Minor Works28 Professional Services30 Other Contractual Services31 Grant-in-Aid32 Contributions33 Subsidies34 Stipend50 Other Charges70 Deduct Recoveries

The object heads under Capital-5455 Capital Outlay on Meteorology

51 Motor Vehicle52 Machinery & Equipments53 Major Works

Reference Guide on Administration, Finance & Procurement

18

List of Existing Object Head in IMD as on 1st January 2011

S.No.

Object Heads

Code Definition Description

1 Salaries 01 Salaries, Sumptuary Allowance

Salaries – Will include pay, allowances in all forms of personnel including honoraria and leave encashment except travel expenses (other than leave travel concession). This object classification will also be utilized for recording expenditure on emoluments and allowances of Heads of States and other high dignitaries including sumptuary allowance)

2 Wages 02 Wages Wages – Will include wages of laborers and of staff at present paid out of contingencies

3 Overtime Allowance

03 Overtime Allowance

Overtime Allowance – Is the amount paid to a Non-Gazetted Government servant for performing official duties beyond office hours in addition to his working hours.

4 * Medical Treatment

06 Medical Treatment

Medical Treatment – Will include amount paid towards medical reimbursement to Government Servants/ Pensioners.

5 Domestic Travel Expenses

11 Travel expenses, conveyance Allowance

Domestic Travel Expenses – Will cover all expenses on account of travel on duty in India including conveyance and fixed travelling allowances but excluding leave travel concessions which would be part of salaries. This will also include TA/DA to non-official members on account of travel in India.

Reference Guide on Administration, Finance & Procurement

19

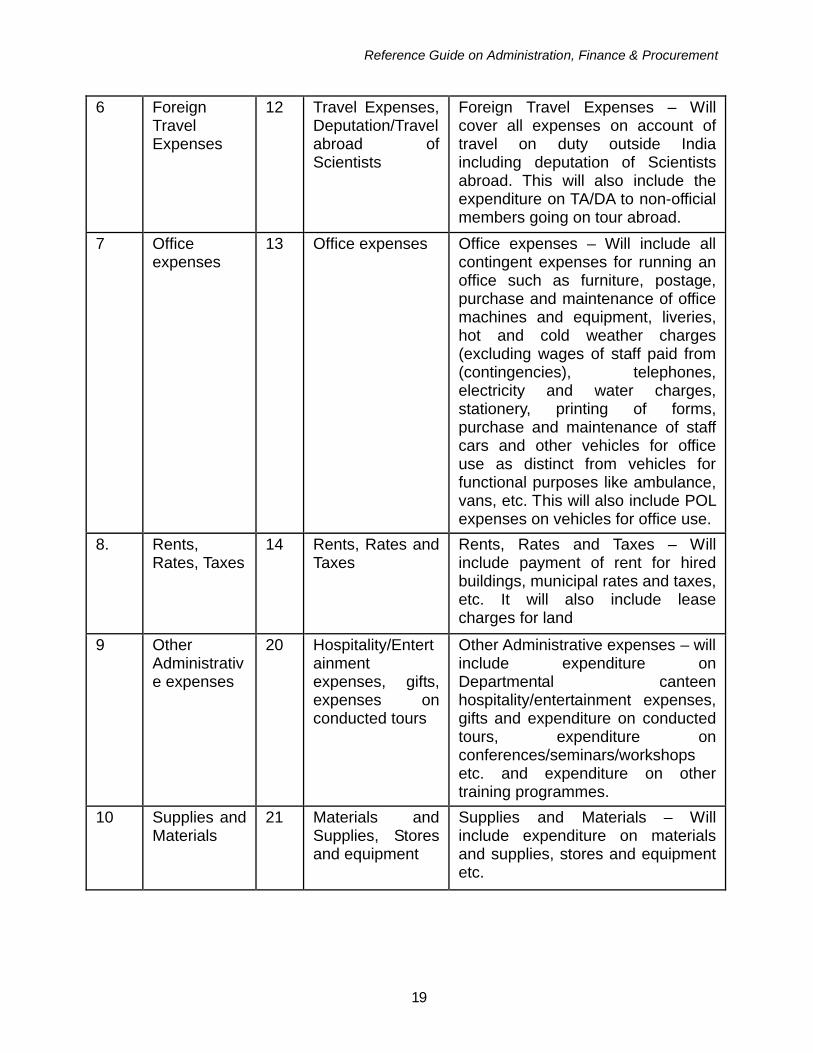

6 Foreign Travel Expenses

12 Travel Expenses, Deputation/Travel abroad of Scientists

Foreign Travel Expenses – Will cover all expenses on account of travel on duty outside India including deputation of Scientists abroad. This will also include the expenditure on TA/DA to non-official members going on tour abroad.

7 Office expenses

13 Office expenses Office expenses – Will include all contingent expenses for running an office such as furniture, postage, purchase and maintenance of office machines and equipment, liveries, hot and cold weather charges (excluding wages of staff paid from (contingencies), telephones, electricity and water charges, stationery, printing of forms, purchase and maintenance of staff cars and other vehicles for office use as distinct from vehicles for functional purposes like ambulance, vans, etc. This will also include POL expenses on vehicles for office use.

8. Rents, Rates, Taxes

14 Rents, Rates and Taxes

Rents, Rates and Taxes – Will include payment of rent for hired buildings, municipal rates and taxes, etc. It will also include lease charges for land

9 Other Administrative expenses

20 Hospitality/Entertainment expenses, gifts, expenses on conducted tours

Other Administrative expenses – will include expenditure on Departmental canteen hospitality/entertainment expenses, gifts and expenditure on conducted tours, expenditure on conferences/seminars/workshops etc. and expenditure on other training programmes.

10 Supplies and Materials

21 Materials and Supplies, Stores and equipment

Supplies and Materials – Will include expenditure on materials and supplies, stores and equipment etc.

Reference Guide on Administration, Finance & Procurement

20

11 Minor works 27 Minor works, Maintenance

Minor works – Will also record expenditure on repairs and maintenance of works, machinery and equipment(<50 Lacs)

12 Professional Services

28 Payments for professional and special services, fees to staff artistes

Professional Services – will include charges for legal services, consultancy fees, fees to staff artistes, remuneration to the examiners, invigilators etc. for conducting examinations, remuneration to casual artistes, by the all India Radio, Doordarshan and all other types of remunerations. It will also include payments for services rendered, supplies made by other departments such as Railways, Police etc. a distinction being made in respect of supplies made, services rendered for running of an office in which case the expenditure will be recorded under office expenses.

13 Other Contractual services

30 Service or commitment charges, notional values of gifts received

Other Contractual services – Will include expenditure on service or commitment charges and notional value of gifts received etc.

14 Advertising & Publicity

26 Advertising & Publicity

Commission to agents for sell & printing of Publicity material.Expenditure on exhibitions.

15 Motor Vehicle

51 Purchase & maintenance of Transport

Purchase & maintenance of Transport

Thus Standard 15 digit numeric code is in detailed demand of grants. These codes are allotted by comptroller-General of Accounts. All Expenditure to be booked in 15 digit numeric code only

Reference Guide on Administration, Finance & Procurement

21

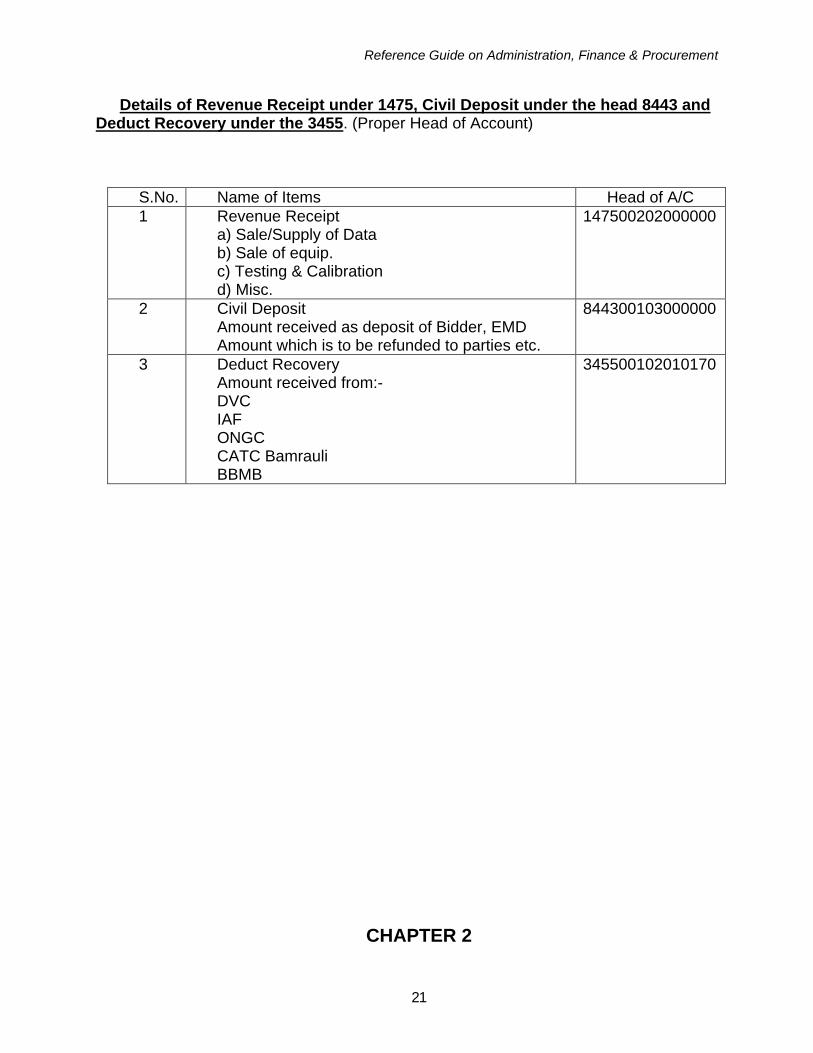

Details of Revenue Receipt under 1475, Civil Deposit under the head 8443 and Deduct Recovery under the 3455. (Proper Head of Account)

S.No. Name of Items Head of A/C1 Revenue Receipt

a) Sale/Supply of Datab) Sale of equip.c) Testing & Calibrationd) Misc.

147500202000000

2 Civil DepositAmount received as deposit of Bidder, EMDAmount which is to be refunded to parties etc.

844300103000000

3 Deduct RecoveryAmount received from:-DVCIAFONGCCATC BamrauliBBMB

345500102010170

CHAPTER 2

Reference Guide on Administration, Finance & Procurement

22

PROCUREMENT

Every Ministry / Department spends a sizeable amount of its budget forpurchasing various types of goods to discharge the duties and responsibilities assigned to it. It is imperative that these purchases are made following a uniform, systematic, efficient and cost effective procedure, in accordance with the relevant rules and regulations of the Government. The Ministries / Departments have been delegated powers to make their own arrangements for procurement of goods under the Delegation of Financial Power Rules, which have to be exercised in conformity with the orders and guidelines issued by competent authorities coverings financial, vigilance, security, safety, counter trade and other regulatory aspects. Without purporting to be a comprehensive compendium of all statutory provisions, rules, regulations, orders andguidelines on the subject of public procurement, the “MANUAL ON POLICIES & PROCEDURES FOR PURCHASE OF GOODS” prepared by Ministry of Finance, Department of Expenditure, Government of is intended to serve as a portal to enter this vast area and draw attention to basic norms and practices governing public procurement.

To achieve what has been stated in the above paragraphs, it is essential that the purchase officials be provided with all the required rules, regulations, instructions, directives, and guidance on best practices in the form of a Manual. This Manual is intended to serve this objective. This manual contains guidelines and directives concerning purchase of goods with public funds as well as some allied areas such as installation of equipment, operators’ training, after sales services, maintenance contract, etc. Relevant aspects of purchase management techniques have been incorporated in proper sequence under separate chapters. The text incorporated in each chapter has been highlighted with appropriate sub-heads. This arrangement will help the users to readily locate the desired subjects/sub-subjects.

GENERAL FINANCIAL RULES No expenditure can be incurred against a sanction unless funds are made

available to meet the expenditure by valid appropriation or re-appropriation. The government authorities have to comply with rules prescribed in the General

Financial Rules and the Delegation of Financial Power Rules in all financial matters.

In order to maintain proper control, the controlling officer obtains information on not only what has actually been spent from the grants but also what commitments and liabilities have been and will be incurred against them.

COMPETENT AUTHORITY ‘Administrative approval’ of a scheme, proposal or work. - is the formal acceptance

thereof by the competent authority for the purpose of incurring expenditure. ‘Competent Authority’- means, in respect of the power to be exercised under any of

these provisions, the President or such other authority to which the power is delegated by or under the General Financial Rules, 2005, Delegation of Financial

Reference Guide on Administration, Finance & Procurement

23

Powers Rules, 1978 or any other general or special orders issued by the Government of India.

‘Head of Department’ - means an officer declared as such by Government. (As per list given in the Delegation of Financial Powers Rules).

ROLE OF DEPARTMENTS IN SPENDING AND CONTROL

‘Financial Adviser’- means an officer appointed by Government in a Ministry/Department to look after the matters related to financial advice, budget/ accounts, expenditure control/ audit etc. for and on behalf of Finance Ministry

The relevant administrative ministry has the main responsibility for ensuring that The expenditure is incurred for the approved purpose, it is within the sums allotted, it has been incurred under the authority competent to sanction it, and Due prudence has been shown in its incurrence.

REFERENCE TO BUDGET & PLANNING SECTIONHead of Account for expenditure should be approved before placing the order. Post facto allocation of Head of Account is against financial norms.If Head of Account needs to be changed the same should be approved by competent authority and concurred by F.O. IMD / IFD as the case may be.The status of Balance should be inquired from DDO who maintains the Appropriation Register. If the supply order is old and Head of Account no longer exist, the case should be processed through indenting unit.

Reference Guide on Administration, Finance & Procurement

24

Financial Aspect of Procurement

Presentation by Sh. R. P. LAL Director (Budget & planning)

General Financial Rules (GFRs) are a compendium of general provisions to be followed by all offices of Government of India while dealing with matters of a financial nature. General Financial Rules were first issued in 1947 and were in the form of executive instructions. These were subsequently modified and issued as General Financial Rules, 1963.General Financial Rules, 2005 have evolved as a result of the wide consultations and extensive review. The rules have been simplified and put in a logical sequence for easy comprehension.

The Manuals on Policies and Procedures for Goods, Works and services have been prepared by Ministry of Finance in conformity with the applicable directives contained in the GFR 2005. Concerted effort have been made to cover all major aspects of procurement in these manuals in a user friendly manner taking into account the developments in the economy and need to introduce quality, competition and transparency in public procurement. Departments have to supplement these manuals by issuing detailed operating instructions to serve as practical instructions for their officers, evolve checklists to ensure completeness of examination of cases and customize the format to suit local/special needs.

Some other important and budget related Delegation of Financial Rules (DFPR) provisions are briefly as under-

GFR Rule 6, Effect of Sanction: It provides that no expenditure shall be incurred against a sanction unless funds are made available to meet the expenditure or liability by valid Appropriation or Reappropriation.

GFR Rule 8, Primary Units of Appropriation: This Rule lists the standardized list of the Primary Units of Appropriation or the Object Heads and the six tier classification system in the Government accounts.

GFR 2005: Rule 25. PROVISION OF FUNDS FOR SANCTION

(1) All sanctions to the expenditure shall indicate the details of the provisions in the relevant grant or appropriation wherefrom such expenditure is to be met.(2) All proposals for sanction to expenditure shall indicate whether such expenditure can be met by valid appropriation or reappropriation.(3) In cases where it becomes necessary to issue a sanction to expenditure before funds are communicated, the sanction should specify that such expenditure is subject to funds being communicated in the Budget of the year.

Reference Guide on Administration, Finance & Procurement

25

PROCEDURE FOR COMMUNICATION OF SANCTIONS

GFR 2005: RULE 29. : All financial sanctions and orders issued by a competent authority shall be communicated to the Audit Officer and the Accounts Officer. (i) All financial sanctions issued by a Department of the Central Government which relate to a matter concerning the Department proper and on the basis of which payment is to be made or authorized by the Accounts Officer, should be addressed to him.(ii) All other sanctions should be accorded in the form of an Order, which need not be addressed to any authority, but a copy thereof should be endorsed to the Accounts Officer concerned.(iv) All financial sanctions and orders issued by a Department of the Central Government with the concurrence of the Internal Finance Wing or Ministry of Finance, as applicable, should be communicated to the Accounts Officer in accordance with the procedure laid down in Rule 25 of the Delegation of Financial Powers Rules, 1978, and orders issued there-under from time to time.

LAPSE OF SANCTIONS

GFR 2005: Rule 30. A sanction for any fresh charge shall, unless it is specifically renewed, lapse if no payment in whole or in part has been made during a period of twelve months from the date of issue of such sanction. Provided that -(i) When the period of currency of the sanction is prescribed in the departmental regulations or is specified in the sanction itself, it shall lapse on the expiry of such periods; or(ii) When there is a specific provision in a sanction that the expenditure would be met from the Budget provision of a specified financial year, it shall lapse at the close of that financial year; or(iii) in the case of purchase of stores, a sanction shall not lapse, if tenders have been accepted (in the case of local or direct purchase of stores) or the indent has been placed (in the case of Central Purchases) on the Central Purchase Organization within the period of one year of the date of issue of that sanction, even if the actual payment in whole or in part has not been made during the said period.

CLASSIFICATION OF TRANSACTIONS 15 DIGIT CODE

GFR Rule 72. : The six tiers of classification of transactions in Government Accounts are represented by a unique 15 digit numeric code.

Major Heads (4), Sub-major Head (2), Minor Heads (3), Sub Heads (2), Detailed Heads (2), Object Heads (2).

The Major Heads (comprising Sub-Major Heads) of account, generally correspond to functions of Government

The Minor Heads identify the programmes undertaken to achieve the objectives of the functions represented by the Major Head.

The Sub Head represents schemes,

Reference Guide on Administration, Finance & Procurement

26

The Detailed Head denotes sub scheme Object Head represent the primary unit of appropriation showing the economic

nature of expenditure such as salaries and wages, office expenses, travel expenses, professional services, grants-in-aid, etc.

AUTHORITY TO OPEN A NEW HEAD OF ACCOUNT

The List of Major and Minor Heads of Accounts of Union and States is maintained by the Ministry of Finance (Department of Expenditure – Controller General of Accounts) which is authorised to open a new head of account on the advice of the Comptroller and Auditor General of India .

Ministries/ Departments may open Sub-Heads and Detailed Heads asrequired by them in consultation with the Budget Division of the Ministry of Finance. Their Principal Accounts Offices may open Sub/Detailed Heads required under the Minor Heads falling within the Public Account of India subject to the above stipulations.

The Object Heads have been prescribed under Government of India’sOrders below Rule 8 of Delegation of Financial Power Rules. The power toamend or modify these object heads and to open new Object Heads rest with Department of Expenditure of Ministry of Finance on the advice of the Comptroller and Auditor General of India.

Rule 52 of the GFR lays down provisions relating to the Responsibility for control of Expenditure,

Rule 53 of GFR, Maintenance of Liability Register for effecting proper control over expenditure: In order to maintain proper control over expenditure, a Controlling Officer should obtain from the spending authorities liability statements in Form GFR 6-A every month, starting from the month of October in each financial year.

The Controlling Officer should also maintain a Liability Register in Form GFR 6.

Rule 54 of GFR, Personal attention of the Head of Department / Controlling Officer required for estimating savings or excesses:A Head of Department or Controlling Officer should be in a position to estimate the likelihood of savings or excesses every month and to regularize them in accordance with the instructions laid down in Rule 56.

Rule 62 of GFR, Inevitable Payments:(i) Subject to the provisions of Article 114 (3) of the Constitution, money indisputably payable by Government shall not ordinarily be left unpaid.(ii) Suitable provision for anticipated liabilities should invariably be made in Demands for Grants to be placed before Parliament.

Reference Guide on Administration, Finance & Procurement

27

The Secretary of a Ministry / Department who is the Chief Accounting Authority of the Ministry /Department shall(i) be responsible and accountable for financial management of his Ministry or Department.(ii) ensure that the public funds appropriated to the Ministry or Department are used for the purpose for which they were meant.(iii) be responsible for the effective, efficient, economical and transparent use of the resources of the Ministry or Department in achieving the stated project objectives of that Ministry or Department, whilst complying with performance standards. (viii) shall ensure that his Ministry or Department follows the Government procurement procedure for execution of works, as well as for procurement of services and supplies, and implements it in a fair, equitable, transparent, competitive and cost-effective manner;

As per the new charter of duties and responsibilities issued by the Secretary, Department of Expenditure, Ministry of Finance, as part of the Revised Redefined Charter for Financial Advisers, the following functions in relation to Internal Audit will be carried out by the Chief Controllers of Accounts as per the guidelines issued by the Controller General of Accounts from time to time-(i) The appraisal, monitoring and evaluation of individual schemes;(ii) Assessment of adequacy and effectiveness of internal controls in general, and soundness of financial systems and reliability of financial and accounting reports in particular;(iii) Identification and monitoring of risk factors including those contained in the Outcome Budget;(iv) Critical assessment of economy, efficiency and effectiveness of service delivery mechanism to ensure value for money; and(v) Providing an effective monitoring system to facilitate mid course corrections.

FORM GFR-6 : LIABILITY REGISTER

Reference Guide on Administration, Finance & Procurement

28

PROCUREMENT OF GOODS AND SERVICES

Presentation by Sh D.K. Nim F.O.(IMD)

Fundamental Principles of Govt. Procurement Availability of Fund for that purpose if Plan procurement Approval of Scheme/ Project to be seen before process in case of plan

procurement Specification, quality, quantity of goods Fair, Transparent and Reasonable Procedure Selected offer should meet all requirements Reasonability of Price Price Preference to SSIs Purchase Preference to CPSUs

Mode of Procurement

Without any quotation up to Rs.15000/- Through Purchase Committee of 3 members for Rs.15001/- to Rs.100,000/- Through Rate Contract of DGS&D Directly from firm at rate contract of DGS&D Advertised Tender Enquiry (ATI) for more than Rs.25 Lakhs value Limited Tender Enquiry up to Rs.25 Lakhs Single Tender Inquiry in case of No other firm/company manufactures the goods b) Emergent procurement c) Compatibility/suitability of Spare parts/machinery

Mode of Publicity of Invite

ITJ and at least One National daily along with uploading on website in case of ATI

Registered/Speed Post invitation letters to minimum 3 firms in case of LTI and uploading on website

Invitation letter to the firm asking quote in single inquiry General conditions/ Principles of Contract May withdraw, revise or modify his offer before its opening date and time All contracts shall be executed on behalf of the President Contract document should be invariably executed in case of turnkey works or

AMC, or provision of service No work of any kind should be commenced without proper execution of an

agreement Contracts should include provision for payment of all Taxes applicable

Reference Guide on Administration, Finance & Procurement

29

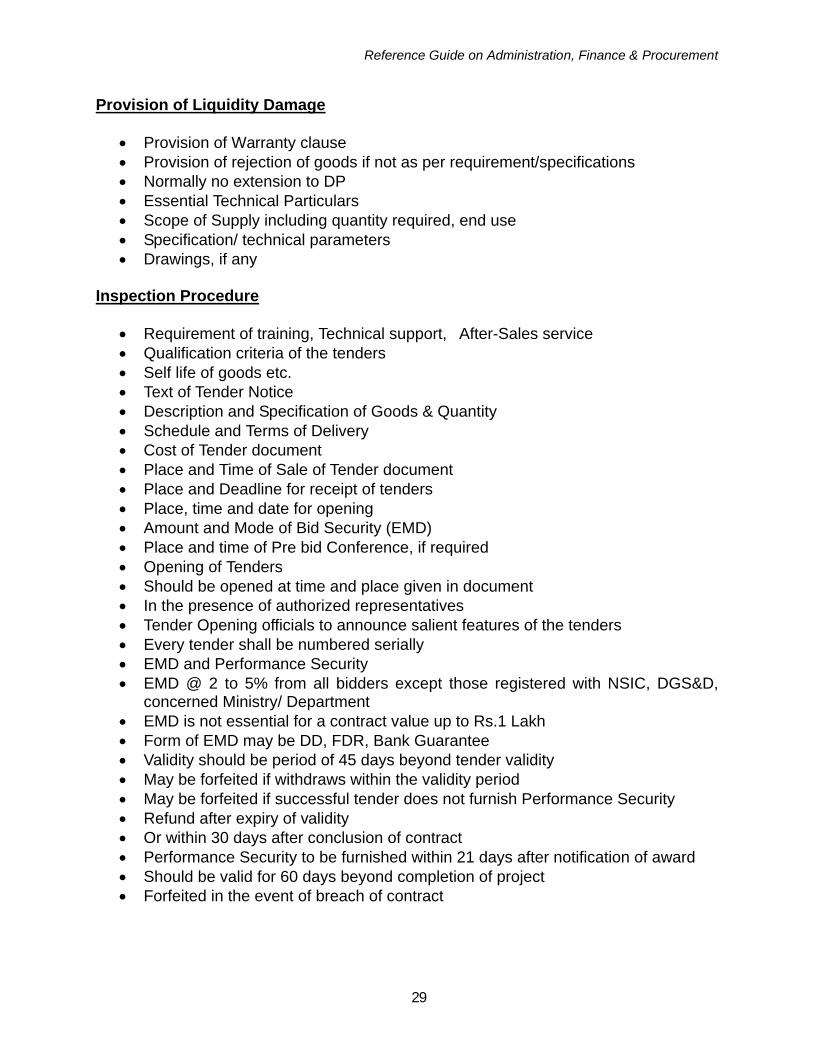

Provision of Liquidity Damage

Provision of Warranty clause Provision of rejection of goods if not as per requirement/specifications Normally no extension to DP Essential Technical Particulars Scope of Supply including quantity required, end use Specification/ technical parameters Drawings, if any

Inspection Procedure

Requirement of training, Technical support, After-Sales service Qualification criteria of the tenders Self life of goods etc. Text of Tender Notice Description and Specification of Goods & Quantity Schedule and Terms of Delivery Cost of Tender document Place and Time of Sale of Tender document Place and Deadline for receipt of tenders Place, time and date for opening Amount and Mode of Bid Security (EMD) Place and time of Pre bid Conference, if required Opening of Tenders Should be opened at time and place given in document In the presence of authorized representatives Tender Opening officials to announce salient features of the tenders Every tender shall be numbered serially EMD and Performance Security EMD @ 2 to 5% from all bidders except those registered with NSIC, DGS&D,

concerned Ministry/ Department EMD is not essential for a contract value up to Rs.1 Lakh Form of EMD may be DD, FDR, Bank Guarantee Validity should be period of 45 days beyond tender validity May be forfeited if withdraws within the validity period May be forfeited if successful tender does not furnish Performance Security Refund after expiry of validity Or within 30 days after conclusion of contract Performance Security to be furnished within 21 days after notification of award Should be valid for 60 days beyond completion of project Forfeited in the event of breach of contract

Reference Guide on Administration, Finance & Procurement

30

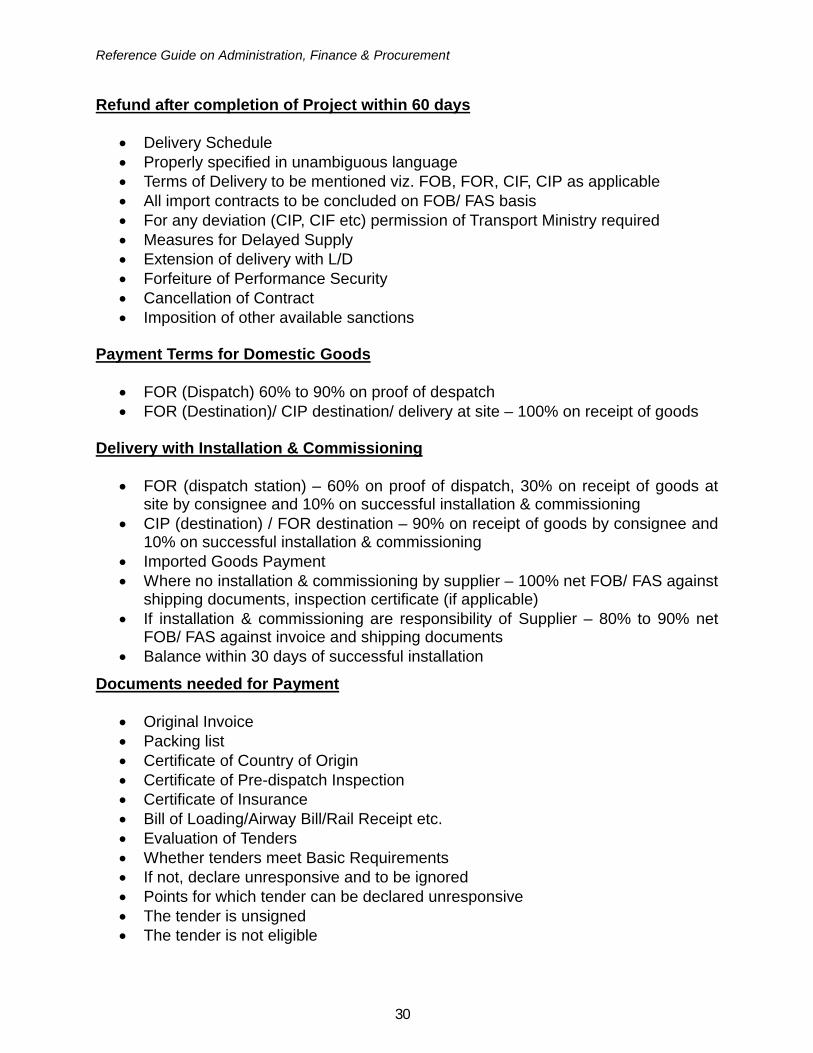

Refund after completion of Project within 60 days

Delivery Schedule Properly specified in unambiguous language Terms of Delivery to be mentioned viz. FOB, FOR, CIF, CIP as applicable All import contracts to be concluded on FOB/ FAS basis For any deviation (CIP, CIF etc) permission of Transport Ministry required Measures for Delayed Supply Extension of delivery with L/D Forfeiture of Performance Security Cancellation of Contract Imposition of other available sanctions

Payment Terms for Domestic Goods

FOR (Dispatch) 60% to 90% on proof of despatch FOR (Destination)/ CIP destination/ delivery at site – 100% on receipt of goods

Delivery with Installation & Commissioning

FOR (dispatch station) – 60% on proof of dispatch, 30% on receipt of goods at site by consignee and 10% on successful installation & commissioning

CIP (destination) / FOR destination – 90% on receipt of goods by consignee and 10% on successful installation & commissioning

Imported Goods Payment Where no installation & commissioning by supplier – 100% net FOB/ FAS against

shipping documents, inspection certificate (if applicable) If installation & commissioning are responsibility of Supplier – 80% to 90% net

FOB/ FAS against invoice and shipping documents Balance within 30 days of successful installation

Documents needed for Payment

Original Invoice Packing list Certificate of Country of Origin Certificate of Pre-dispatch Inspection Certificate of Insurance Bill of Loading/Airway Bill/Rail Receipt etc. Evaluation of Tenders Whether tenders meet Basic Requirements If not, declare unresponsive and to be ignored Points for which tender can be declared unresponsive The tender is unsigned The tender is not eligible

Reference Guide on Administration, Finance & Procurement

31

Shorter validity Without the required authority letter from OEM Declined to give Performance Security Goods quoted are substandard Tenderer has not quoted for entire requirement Tenderer has not agreed to some essential conditions

Qualification Criteria

Responsive bids are to be examined for Qualification Criteria If not meets Qualification Criteria, not be considered further Evaluation of Price to include Taxes, duties etc. Price Reasonableness Parameters Last Purchase Price Current Market Price Price of Raw Materials required for production Receipt of Budgetary quote from different sources Award of Contract Before Expiry of Tender Validity period If validity expired, request to extend validity before awarding Ask to furnish Performance Security within 21 days Ask to accept unconditionally the contract within 15 days

Reference Guide on Administration, Finance & Procurement

32

RFP AND TENDER DOCUMENT

Presentation on By S.K.Jain DDGM (P)

Instead of naming as RFP, document is to be named as document containing complete technical specifications, Terms of reference, List of deliverables.

(a)Specifications and allied technical details.

b)Terms of reference: Shall include Qualification criterion of bidder, delivery schedule of store(time may be taken from date of establishment of LC and not from the date of placement of supply order in case store is to be supplied from foreign country) and must be realistic for completion of project within delivery period itself, Warranty period after delivery, Schedule of Installation & Commissioning, AMC and spares if required. It must be clearly mentioned that AMC and spares are to be treated as main store (cost to be included in CST) or as optional items (cost to be excluded in CST).

(c) List of deliverables with complete specifications as per enclosed Performa must be submitted.

Document should not contain any commercial terms and condition. SAT and training in India if required may be included. In case FAT and foreign training is to be included, prior approval of MoES is to be taken by the division.

Document is to be submitted to the respective review committee by the consignee. Committee shall send it back to consignee with suggestions of modification, if any. Consignee shall submit it to DGM after incorporating the modifications for approval.

Following are the details of committees:For procurement value > Rs. 5.0 croresShri L.R. Meena, Sc’F (ISSD)’---- ChairmanShri K.C. Saikrishnan Sc”E’ (UI)--- Member Secretary

For procurement value >1.0 crore and upto Rs. 5.0 croresShri A.K. Sharma, Sc’F’(Sat Met)---- ChairmanShri B.M.S. Nayal, Director(CPU)-- Member Secretary

Further RFP>Rs.25.0Lakh and up to procurement value of 1.0 crore shall be submitted to DDGM(P) for vetting.

Approved document shall be submitted to CPU along with indent.

Indent duly filled is to be submitted in the enclosed Performa only and is to be signed by the Head of division. No column of indent is to be left unfilled.

Reference Guide on Administration, Finance & Procurement

33

PERFORMA OF INDENT

Name of store : Quality RequiCategory of Store ( DGS&D or Other ) :If DGS&D, please provide R/C No.& Item NoDetailed Specification (Soft Copy) consisting of Complete technical specifications:Terms of reference :List of deliverables (as per enclosed format) :Copy of approval of Competent Authority :Estimated Cost : Copy of Budgetary Quotation :Annual Consumption :Stock in hand :Supply Pending :Delivery Period :Delivery Schedule if any :List of likely Suppliers :P.A.C : Availability of Funds during the current financial :Year Head of A/c Plan/ Non-Plan If plan, Name of Scheme under whichApproved (copy to be enclosed)16. Details of last supply order : a) Order No. and date : b) Qty Ordered : c) Suppliers Name d) Rate per Unit paid/ total value : e) Performance of last suppliers :17. Mode of Supply( Road/Air/Shipment :18. a) Address of Consignee : b) Address of users where store to be delivered20. Any other information :Signature of Head of DivisionFile No.Office/Division:Dated:

Reference Guide on Administration, Finance & Procurement

34

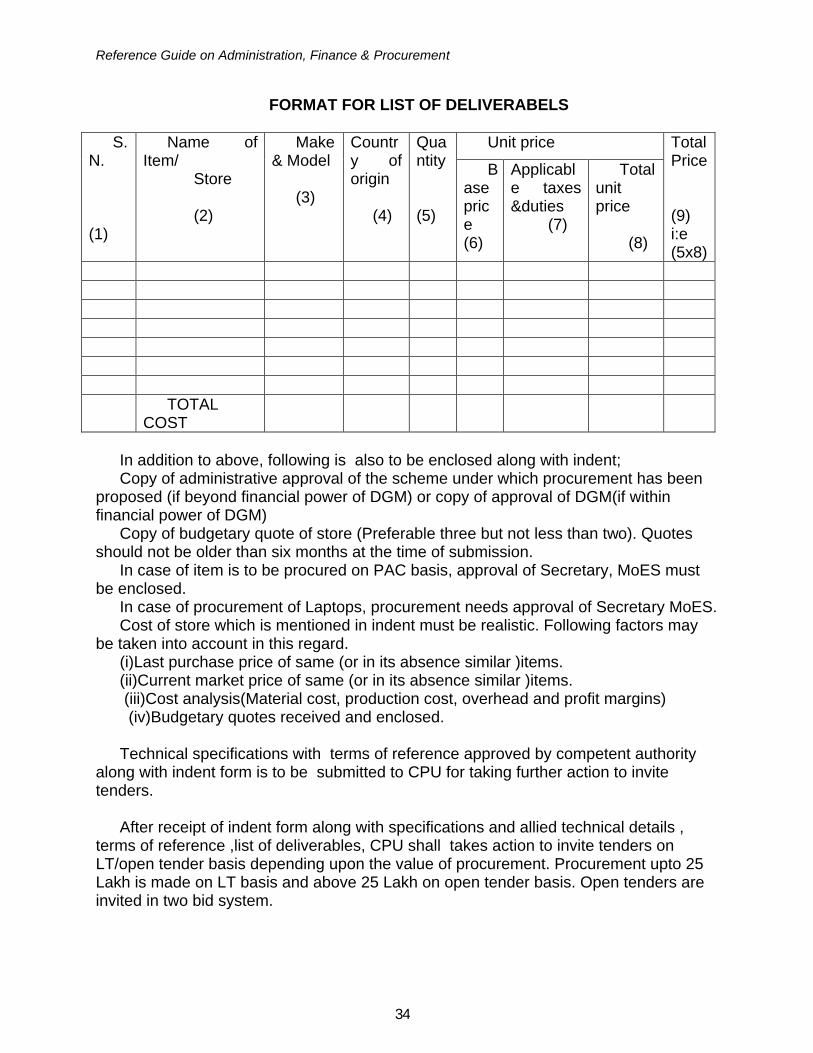

FORMAT FOR LIST OF DELIVERABELS

Unit priceS.N.

(1)

Name of Item/

Store

(2)

Make & Model

(3)

Country of origin

(4)

Quantity

(5)

Base price(6)

Applicable taxes &duties

(7)

Total unit price

(8)

Total Price

(9) i:e(5x8)

TOTAL COST

In addition to above, following is also to be enclosed along with indent;Copy of administrative approval of the scheme under which procurement has been

proposed (if beyond financial power of DGM) or copy of approval of DGM(if within financial power of DGM)

Copy of budgetary quote of store (Preferable three but not less than two). Quotes should not be older than six months at the time of submission.

In case of item is to be procured on PAC basis, approval of Secretary, MoES must be enclosed.

In case of procurement of Laptops, procurement needs approval of Secretary MoES.Cost of store which is mentioned in indent must be realistic. Following factors may

be taken into account in this regard.(i)Last purchase price of same (or in its absence similar )items.(ii)Current market price of same (or in its absence similar )items. (iii)Cost analysis(Material cost, production cost, overhead and profit margins) (iv)Budgetary quotes received and enclosed.

Technical specifications with terms of reference approved by competent authority along with indent form is to be submitted to CPU for taking further action to invite tenders.

After receipt of indent form along with specifications and allied technical details , terms of reference ,list of deliverables, CPU shall takes action to invite tenders on LT/open tender basis depending upon the value of procurement. Procurement upto 25 Lakh is made on LT basis and above 25 Lakh on open tender basis. Open tenders are invited in two bid system.

Reference Guide on Administration, Finance & Procurement

35

TENDER ENQUIRY DOCUMENT

Tender document is Vital document, which contains ;Name of store to be procuredTender cost in rupees (non refundable) depending upon the value of procurement.

Tender cost is to be drawn in favor of Asst. Meteorologist(DDO), DGM’s Office, New Delhi in the form of DD only. Following are the rates at which tender cost is charged

Rs 100/- for procurement value up to Rs.10.00 LakhRs.200/- for procurement value >10.00 Lakh and up to Rs.20.00 LakhRs.500/- for procurement value >20.00 Lakh and up to Rs.1.0 croreRs.1,000/- for procurement value >1.0 crore Starting date of sale of tender document.Date, time and venue of pre bid conference if required.Last date and time of submission of tender.Date, time and venue of tender opening.Details of EMD which cab be submitted in the form of DD/FDR/Bank Guarantee in

favor of Asst. Meteorologist(DDO), DGM’s Office, New Delhi. EMD is charged at 2% of procurement value.

Normally four weeks time is kept between invitation and submission of tender where pre bid conference is not there and five to six weeks where pre bid conference is there in case of open tender.

Tender enquiry document with other commercial terms & conditions also containing specifications and allied Technical details , terms of reference and list of deliverables is sent to;

DGM (Telecom) for placing same on IMD website.Submitted to DAVP for publishing in at least one national daily in wide circulation.Submitted to Director General of commercial intelligence & Statics ,Kolkata for

publishing in Indian Trade Journal(ITJ).Copies to those foreign embassies in India and Indian embassies abroad from which

countries, bids are expected to be received.

Pre bid conference: Pre bid conference is a meeting between interested tenderers and a committee constituted by DGM comprising of officers of IMD or is some cases from outside IMD as well . The meeting is in connection with clarifications regarding technical as well as commercial aspects related to tenders. Efforts are made to clarify the issues in the conference itself. However minutes of meeting duly approved by DGM are to be placed on IMD website sufficient in advance from the date of submission of tenders.

It may pl. be noted that advertisement of NIT in national daily as well publication in ITJ is to be ensured before pre bid meeting. Date of pre bid is to be extended, in case of non publication of NIT by due date.

Two bid system is the system in which technical and financial bids are submitted simultaneously. Financial bids are sealed in separate cover with marking on the envelope. This is due to reason that financial bids of technically acceptable bidders shall only be opened.

Reference Guide on Administration, Finance & Procurement

36

Opening of tender : Tender is to be opened on schedule date and specified time as mentioned in tender enquiry document by a committee with officers of CPU and one outside CPU, duly constituted by DGM. All technical bids are to be numbered serially on the front page and signed by committee members. Tenderer himself or their authorized representative (one representative of one tenderer only) to be allowed to attend opening . List of bidders is to be filled and authority letters of all the authorized representatives must be enclosed with the list. Signature of bidders/authorized representatives must be put in the list. Entries must also be made in tender opening register with the details of tenders received till specified time as mentioned in tender enquiry document. Tenders received, if any after specified date &time must be marked as “ Late tenders” and not to be opened.

Tender opening committee shall ensure that tender has been signed, EMD for required amount and for specified period as mentioned in tender document favoring “Asst. Meteorologist(DDO)”, DGM’s office, Payable at New Delhi has been enclosed. All column of Check list have been filled and signed and tender form have been signed. Necessary stamp have also been affixed at required pages.

Tender Evaluation Committee : All responsive bids are to be submitted by CPU for tender evaluation to a committee duly constituted by DGM which shall evaluate the tender in the light of tender enquiry document and submit TEC report with a recommendation of technically acceptable bidders. Compliance statement and List of deliverables in r/o each bidder are to be enclosed with the report. All pages of the report are to be signed by all committee members.

TEC report shall be submitted to competent authority for kind consideration and approval accordingly by CPU.

Price bids of technically acceptable bidders shall only be opened by CPU after acceptance of TEC report only.