Global Financial Crisis and Foreign Currency Borrowing ... · 1 Global Financial Crisis and Foreign...

44

1 Global Financial Crisis and Foreign Currency Borrowing 1 Philippe Bacchetta 2 Ouarda Merrouche University of Lausanne University of Lausanne Swiss Finance Institute CEPR CEPR First draft: February 2015 Abstract Despite international financial disintegration, we document a dramatic increase in foreign currency borrowing among leveraged Eurozone corporates in the aftermath of the US financial crisis. Using firm- level borrowing data, we trace this increase to two main symptoms of the global financial crisis: (1) a domestic credit crunch causing leveraged corporates to switch to foreign banks; and (2) a higher funding cost in the borrower home currency causing foreign banks to increasingly transfer currency risk to the borrower. While large high-credit quality corporates could tap the bond market during the credit crunch, lower-credit quality borrowers turned to foreign banks. Although global bank lending is often reported to amplify the international credit cycle, we show that foreign banking acted as a shock absorber that weathered the real consequences of the credit crunch for Eurozone corporates that suffered most from the credit crunch. JEL classification numbers: G21, G30, E44 Keywords: Money market, credit crunch, corporate debt, foreign banks, currency risk 1 Financial support from the ERC Advanced Grant #269573 is gratefully acknowledged. 2 Authors’ emails: [email protected] and [email protected]

Transcript of Global Financial Crisis and Foreign Currency Borrowing ... · 1 Global Financial Crisis and Foreign...

1

Global Financial Crisis and Foreign Currency Borrowing1

Philippe Bacchetta2 Ouarda Merrouche University of Lausanne University of Lausanne

Swiss Finance Institute CEPR CEPR

First draft: February 2015

Abstract Despite international financial disintegration, we document a dramatic increase in foreign currency borrowing among leveraged Eurozone corporates in the aftermath of the US financial crisis. Using firm-level borrowing data, we trace this increase to two main symptoms of the global financial crisis: (1) a domestic credit crunch causing leveraged corporates to switch to foreign banks; and (2) a higher funding cost in the borrower home currency causing foreign banks to increasingly transfer currency risk to the borrower. While large high-credit quality corporates could tap the bond market during the credit crunch, lower-credit quality borrowers turned to foreign banks. Although global bank lending is often reported to amplify the international credit cycle, we show that foreign banking acted as a shock absorber that weathered the real consequences of the credit crunch for Eurozone corporates that suffered most from the credit crunch. JEL classification numbers: G21, G30, E44

Keywords: Money market, credit crunch, corporate debt, foreign banks, currency risk

1 Financial support from the ERC Advanced Grant #269573 is gratefully acknowledged. 2 Authors’ emails: [email protected] and [email protected]

2

1. Introduction

Global banking flows have been a major victim of the US financial crisis. While gross capital

flows declined sharply in general (e.g., Broner et al., 2013), the decline has been particularly

steep for banking flows among developed economies (Milesi-Ferretti and Tille, 2011). The

literature shows evidence of a flight home effect in syndicated bank loans (Giannetti and Laeven,

2012a) and of financial protectionism in bank lending (Rose and Wieladek, 2014). We also

observe that global banks have increased the use of their local currency in their lending (e.g.,

Ivashina et al., 2012). More generally, the evidence indicates that global banking flows amplify

international credit cycles (Giannetti and Laeven, 2012b).

In this context of substantial financial disintegration, it is surprising that foreign currency

borrowing by leveraged Eurozone non-financial corporates increased dramatically. While the

proportion of dollar borrowing by non-investment grade firms was about 30% in 2003-2006, it

increased to 90% in the second half of 2008.3 Importantly, this increase in foreign currency debt

comes mainly from newly issued syndicated loans by leveraged corporates, and not in bonds, as

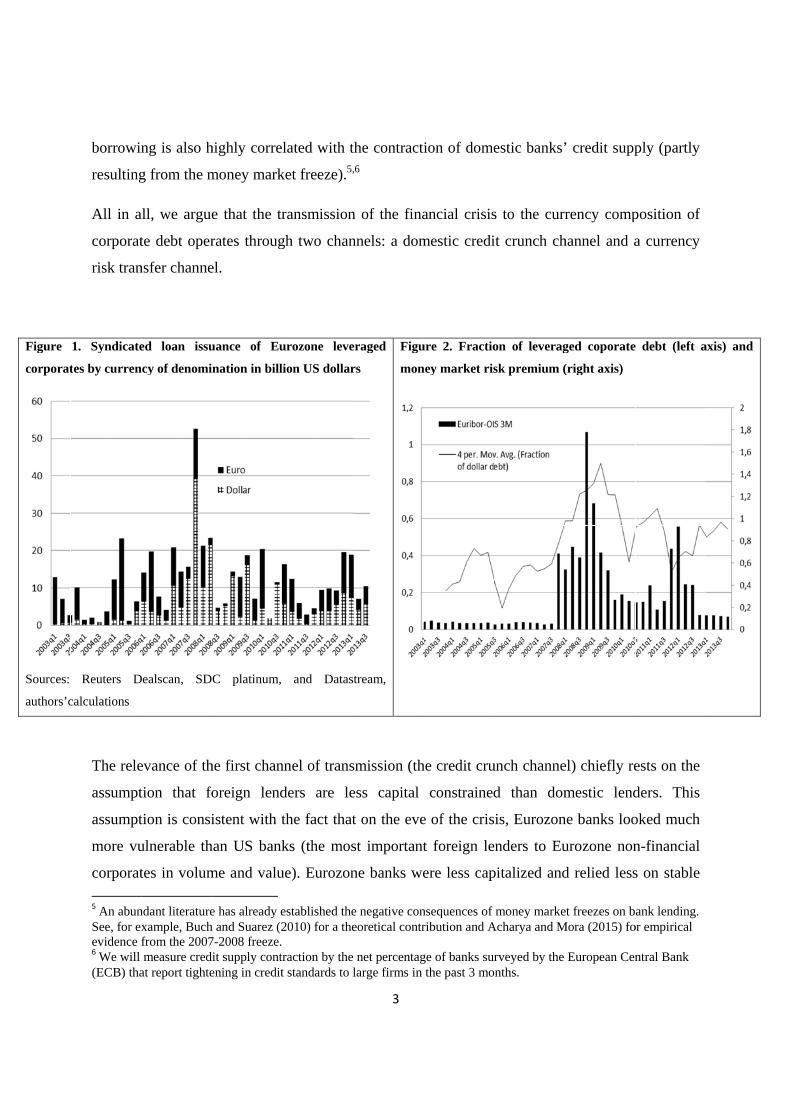

illustrated in Figure 1. The purpose of this paper is to document this surprising aspect of

international banking flows and identify the factors that led to that development. Moreover, we

show that foreign banking could mitigate the transmission of the credit crunch to employment

and investment.

We argue that the increase in foreign currency borrowing by Eurozone leveraged4 firms is a

consequence of two main (and related) symptoms of the global financial crisis: the domestic

credit crunch and the drying up of the Euro interbank market. Figure 2 plots the evolution of

dollar lending together with the Euro interbank risk premium measured by Euribor-OIS 3-month

spread. The two series are highly positively correlated: a higher cost of bank funding in home

currency is associated with an increase in foreign currency borrowing. Foreign currency

3 This increase cannot be attributed to a valuation effect: the Euro appreciated against the dollar by about 20% during the period when the increase was strongest, i.e., Q2-2007 and Q3-2008. 4 Throughout the paper we use the terms leveraged, non-investment grade, and low-credit quality interchangeably. Non-investment grade firms in our sample have a leverage ratio (or a ratio of long-term debt over total debt) of 19.5% against 5.7% for investment grade firms.

Figure

corporat

Sources:

authors’c

borrowin

resulting

All in a

corporat

risk tran

1. Syndicate

tes by curren

Reuters D

calculations

The rele

assumpt

assumpt

more vu

corporat

5 An abunSee, for exevidence 6 We will (ECB) tha

ng is also h

g from the m

all, we argue

te debt oper

nsfer channe

ed loan issu

ncy of denomi

Dealscan, SD

evance of th

tion that fo

tion is consi

ulnerable th

tes in volum

ndant literaturexample, Buchfrom the 2007measure cred

at report tighte

highly corre

money mark

e that the tr

rates throug

el.

uance of Eu

ination in bill

C platinum,

he first chan

foreign lend

istent with t

han US bank

me and valu

e has already eh and Suarez (27-2008 freeze. dit supply contrening in credit

lated with t

ket freeze).5,

ransmission

gh two chan

urozone leve

ion US dollar

and Datas

nnel of trans

ders are le

the fact that

ks (the mos

ue). Eurozon

established the2010) for a the raction by thet standards to l

3

the contracti,6

n of the fina

nnels: a dom

eraged

rs

stream,

Figu

mon

smission (th

ess capital

t on the eve

st important

ne banks we

e negative coneoretical contr

e net percentaglarge firms in

ion of dome

ancial crisis

mestic credi

ure 2. Fractio

ney market ris

he credit cru

constrained

e of the cris

t foreign le

ere less cap

nsequences of ribution and A

ge of banks surthe past 3 mo

estic banks’

s to the curr

it crunch ch

on of leverag

sk premium (

unch channe

d than dom

is, Eurozon

nders to Eu

pitalized and

money markeAcharya and M

rveyed by the nths.

’ credit supp

rency comp

hannel and a

ged coporate

(right axis)

el) chiefly re

mestic lend

ne banks loo

urozone non

d relied less

et freezes on bMora (2015) fo

European Cen

ply (partly

position of

a currency

debt (left a

ests on the

ders. This

oked much

n-financial

s on stable

ank lending. or empirical

ntral Bank

axis) and

4

forms of funding.7 According to Merrouche and Mariathasan (2012) Eurozone banks also

required much more public capital injections compared with US banks. Relatedly, Laeven and

Valencia (2013) find that a much bigger fraction of the banking system failed or was intervened

in the Eurozone than in the US, reaching 80% of total banking sector assets in some countries

like Greece, Belgium, or France.

Another fundamental difference between US and Eurozone banks is the fact that US banks are

not subject to Basel II; until now their capital requirement is still fixed under the Basel I

framework. Under the Basel I framework, the risk weight on risky and safe corporate debt is the

same. This means that US banks have greater incentive than Eurozone banks to load onto risky

corporate debt.8

The second channel means that lenders have been less willing to bear currency risk. Foreign

lenders found it more convenient to get their funding in their own currency, mainly dollars, and

avoid a currency mismatch by lending in the same currency. The main reason is that they found it

more costly to get their funding in euros or to hedge foreign currency exposure through FX swaps

given the violations of covered interest parity (CIP) during this period.

Using quarterly bond and syndicated loans issuance data by currency of denomination and lender

nationality at the firm level (from Thomson-Reuters SDC platinum for the period Q1-2003 to Q3-

2013), we find evidence for both channels being at work. Looking at the composition of newly

issued debt by instrument we find that when the domestic supply of bank credit contracts,

investment grade firms shift to bonds while non-investment grade firms shift to foreign bank

loans. 9 We find that the shift to bonds is stronger for large investment grade firms and for firms

that are located in non-GIIPS countries. On the other hand, the shift to foreign bank loans is

stronger for risky firms, irrespective of their size. Moreover, foreign banks manage exchange rate

risk by lending more in their home currency as funding conditions deteriorate in the borrowers’

home currency. These two combined effects explain why the increase in foreign currency 7 For example see The Economist “Reshaping banking: the retreat from everywhere”, April 2012. According to Bankscope data in 2007 Eurozone banks had a Tier1 leverage ratio of 5% and a ratio of retail deposits to total assets of 44% against 9% and 72% respectively for US banks. 8 Relatedly, Duchin and Sosyura (2013) show that after receiving government support, US bank rebalance toward riskier assets and that this shift in risk occurs mostly within the same asset class and therefore remains undetected by regulatory capital ratios. 9 In our setting we define foreign banks as banks headquartered outside the Eurozone. Moreover, we define a foreign bank loan as a syndicated loan with at least one lead foreign bank.

5

borrowing is dramatic during the period 2007-2009 and significant only for non-investment grade

firms.

In addition, we find that foreign banking alleviates the financial constraints of risky firms: risky

firms cut employment and investment less when they have a relationship with a foreign lender

and when they have a natural hedge against foreign currency risk.

We specify a linear probability model with firm fixed effects to model the borrower choice

among different sources of finance and among different currencies. We examine whether this

choice is a function of a firm exposure to the two transmission channels mentioned above.

Exposure to the credit crunch channel is captured by the interaction between home country credit

supply conditions and a borrower credit quality. Exposure to the currency risk transfer channel is

captured by the interaction between home currency risk premium and a dummy for whether

lending is by foreign banks.

The fact that we focus on within-firm time variations means that our results cannot be driven by

changes in the composition of firms tapping different forms of finance, by changes in the

aggregate demand for debt, or by changes in the demand for a particular currency over time.

Further, the fact that we focus on Eurozone countries means that our results cannot be driven by

differences in the stance of monetary policy across countries.

Our findings on the role of foreign banks extends earlier work by Haselmann and Watchel (2011)

and Bruno and Hauswald (2012). Haselmann and Watchel (2011) document that foreign banks

(banks headquartered outside the borrower home country) play a prominent role in the syndicated

loan market and that they lend more to riskier borrowers in developed markets. They however do

not study the role of foreign banks during a crisis. Using country-level data, Bruno and Hauswald

(2012) find a positive effect of foreign banks’ presence on real growth and this effect is stronger

during banking crises and in contexts where informational and legal frictions loom larger,

hindering firms’ access to credit. Our firm-level data allow for a better identification of the

channel through which the presence of foreign banks alters firm performance during a crisis.

Our paper extends two other strands of literature on the reshaping of corporate financing during

the credit crunch and on the real effects of the credit crunch. We confirm the result of Ivashina

and Becker (2014) that Eurozone corporates increased their reliance on the bond market but we

6

show that the shift to bond markets does not concern debt raised for real investment finance

purposes (which matters more for real outcomes) and we do not find supporting evidence that

firms that tapped the bond market increasingly did so because they faced a reduction in bank

lending rather than because bond markets became more attractive for them due to flight to

quality.10

A theoretical literature studies the choice between bank finance and bond finance. Diamond

(1991) explains this choice by the interaction between borrower reputation and monitoring.

Reputation effects eliminate the need for monitoring (when interest rates are low and expected

future profitability is high) so that borrowers with higher credit ratings choose to raise debt

directly from the market rather than via financial intermediaries. Holmstrom and Tirole (1997)

use a model with firms that are heterogeneous in their net worth to study the effect of a credit

contraction on the forms of financing. In line with our findings they obtain that a contraction in

credit induces an increase in bank finance for firms with low net worth. Fiorella de Fiore and

Uhlig (2013) develop a general equilibrium model with firms that differ in their risk of default

that can replicate the aggregate shift from bank finance to bond finance witnessed in Europe since

2009.

The literature on foreign currency borrowing or lending focuses on emerging markets in the

context of financial crises11, but there is little work on advanced economies. The empirical

evidence shows that firms are more likely to borrow in foreign currency when they are exporters

or with large cross-currency interest differentials (e.g., Keloharju and Niskanen, 2001 or

McCauley et al., 2015). For the recent financial crisis, Ivashina et al. (2012) find that Eurozone

banks reduced their dollar lending.

The growing literature on the real consequences of the 2008-2009 credit crunch includes

Chodorow-Reich (2013); Bentolila et al. (2013), and Haltenhof et al. (2014) who study the

impact on employment; and Acharya et al (2014) and Cingano et al. (2014) who also analyse the

10 Our samples are however quite different. We do include credit lines as well as term loans, but do not cover small loans because we are also interested in studying the changing patterns of corporate financing towards foreign banks. Ivashina and Becker (2014) collect additional debt data from CapitalIQ which unfortunately are not sufficiently granular to know whether the loans are from domestic banks or from foreign banks. And we do not cover three countries due to the unavailability of the credit supply contraction index. 11 For theoretical papers, see Aghion et al. (2004), Burnside et al. (2004), Jeanne (2005), or Schneider and Tornell (2004).

7

effect on investment. Like our paper, all these papers find a significant effect on both

employment and investment exploiting micro (firm or industry) level data. But none of these

papers studies the mitigating role of foreign banks which is a main focus of this paper. Our

findings also contrast with some papers, using US data, showing that bond market access

mitigates the real effect of the credit crunch. Using Eurozone data we show instead that the

increase in bond market activity concerned only non-real investment purpose debt and did not

concern firms that suffered most from the credit crunch.

The remainder of the paper is organized as follows. The next section develops the theoretical

hypotheses that guide our empirical analysis and interpretation of the data. Section 3 describes

the methodology and the data. Section 4 discusses the results and Section 5 concludes with policy

lessons.

2. Theoretical Predictions

Consider an economy where three categories of agents co-exist: firms, banks, and bond investors.

Firms differ along two dimensions: credit quality and transparency (or size). And banks are split

into domestic and foreign banks. Loans are denominated in domestic currency or in foreign

currency. Banks borrow from other banks in either the domestic or the foreign interbank market

to fund their loans. Following Holmstrom and Tirole (1997) and Diamond (1992) we make the

following key assumptions:

(i) Bonds are contracts that depend only on public information. As a consequence, they

are used primarily by high-quality and transparent borrowers. Nonetheless financing

through bonds is a risky choice for firms because a situation of financial distress can

only be resolved with liquidation and the total loss of the firm’s net worth.

(ii) Bank loans are an information intensive source of finance. Banks spend resources to

acquire information and monitor borrowers hence they reduce the amount of required

collateral. Therefore low-credit quality (non-investment grade) firms demand more

information intensive finance. However, the fact that banks spend resources to acquire

information implies that bond finance is less costly than bank finance.

8

And we add assumption (iii):

(iii) Foreign loans are more costly than domestic loans and bonds because foreign banks

are newer in the market and unlike domestic banks cannot capitalize on past

information production. In other words, domestic banks have an informational

advantage over foreign banks.

The currency denomination of loans can be determined by several factors (see Shapiro, 1985, for

an early analysis). First, assume that banks prefer to fully hedge currency risk. This can be done

by lending and borrowing in the same currency. For example, a foreign bank can lend in

domestic currency borrowing from the domestic interbank market. Alternatively, a foreign bank

may borrow in foreign currency and lend in domestic currency using FX swaps. In these cases, a

foreign bank can offer a domestic currency loan to a domestic firm at not risk. However, if the

domestic funding market or the FX swap market are not functioning efficiently or are costly to

use, a foreign bank may prefer borrowing and lending in foreign currency. In that case, the

domestic firm bears the exchange rate risk (which may become a credit risk for the bank).

However, exporting firms should be less sensitive to a change in currency denomination.

When domestic currency depreciations are anticipated, it may be that domestic firms prefer

borrowing in foreign currency because they find the domestic interest rate “too high”. The reason

is that domestic firms are less affected by a depreciation than lenders: in case of a large

depreciation firms may default (Aghion et al., 2004).12 Then domestic firms may prefer foreign

currency borrowing with high income and currency risk.

We are interested in the effect of the financial crisis on the choice between different sources of

finance, the currency denomination of newly issued loans, employment, and investment. We

discuss two channels of transmission: a credit crunch channel which operates through domestic

banks and a currency risk transfer channel which operates through foreign banks.

12 Firms may also receive a government subsidy in case of large depreciation (Burnside et al., 2004, Schneider and Tornell, 2004).

9

i. Credit crunch channel

A financial crisis causes domestic banks to cut credit to firms. Following from assumptions (i) to

(iii) we can derive the following hypotheses regarding the impact of a domestic credit crunch on

the forms of financing for different categories of firms.

Hypothesis 1. In response to a contraction in the supply of domestic credit, investment

grade (and large or transparent) firms shift to bonds while non-investment grade firms (of

all size) shift to foreign loans.

Holmstrom and Tirole (1997) show that a credit crunch hits more severely non-investment grade

firms. If investment grade firms are unaffected by the credit crunch we ought to observe that they

do not shift to bonds or that any shift to bonds is not attributable to the fact that these firms are

financially constrained. A simultaneous flight to quality in the bond market is a plausible

confounding factor; it renders bond finance more attractive than bank finance for investment

grade firms.

Now consider what happens to small investment-grade firms. Since large investment-grade firms

shift to bonds, that may crowd-in domestic bank credit for small investment-grade firms.

Hypothesis 2. During a domestic credit-crunch, small investment-grade firms shift from

foreign to domestic loans. This follows directly from the assumption that foreign bank loans

are more onerous than domestic bank loans (foreign premium).

This should hold if the cost of domestic loans remains below the cost of foreign loans for this

category of borrowers.

ii. Currency risk transfer channel

Foreign banks react to the increase in the cost of funding in host currency by lending less in host

currency and more in foreign currency.13

13 Ivashina et al. (2012) show that the disruption in the FX swap markets led Eurozone banks to lend less in dollars.

10

Hypothesis 3. When host country interbank markets dry up, foreign banks increasingly

transfer the currency risk to borrowers: they lend less in the borrower home currency and

more in their home currency.

We may also expect that low-credit quality firms are more willing to assume the currency risk as

the cost of borrowing in domestic currency increases relative to the cost of borrowing in foreign

currency (Aghion et al., 2004).

The spillover of interbank markets turbulence has also consequences on the use of currency

swaps for funding in foreign currency and this in turn has potential consequences on the demand

and supply of bank credit in foreign currency. Ivashina et al. (2012) and Baba et al. (2008) have

shown that the reduced access to interbank dollar funding led to an increased use of synthetic

dollar funding. The subsequent increase in the cost of dollar funding through swaps should cause

a reduced supply of dollar loans by domestic banks and an increase in the demand for dollar loans

by exporters which is more likely to be met by foreign banks.

Hypothesis 4. An increase in the cost of synthetic foreign currency borrowing leads to a

decline in the supply of foreign currency loans by domestic banks and an increase in the

supply of foreign currency loans by foreign banks.

Typically when the swap market is well-functioning a Eurozone exporter would find it attractive

to raise dollar through swapping euro against dollar with a US exporter. The dollar interest rate

paid to the US exporter would tend to be lower than the dollar interest rate she would pay to a

bank. However when liquidity in the swap market evaporates, as it did since 2007, synthetic

dollar borrowing becomes more onerous. One should then observe an increase in dollar lending

from foreign banks and this effect should be larger for exporters.

iii. Real effect of the credit crunch

In light of Hypotheses 1 and 2, what will be the consequence of the credit crunch on employment

and investment and the mitigating role of foreign banking?

Hypothesis 5. The real effects of the credit crunch are mitigated for non-investment grade

firms that have a relationship with a foreign bank.

11

Firms and banks form relationships and cannot costlessly or swiftly switch to borrowing from

less capital constrained foreign banks (Chodorow-Reich, 2013). However the benefit of using a

previous foreign bank relationship, or conversely the lemons cost to switching to a foreign lender,

should decline with the transparency (size) of the borrower (Sufi, 2007; Williamson, 1987).

Following from Hypothesis 3, if the chief purpose of foreign banks is to limit their exposure to

risk, they will refrain from transactions that rather than transferring the currency risk transform it

into credit risk. This happens the more they extend foreign currency loans to borrowers who do

not earn foreign currency revenues.

Hypothesis 6. The real benefit of foreign banking during a credit crunch is stronger for

firms with a natural hedge against currency risk

In the next section we present the methodology and data that we use to test these hypotheses.

3. Methodology and Data

First, we investigate the relevance of the credit crunch channel: we relate a direct country-level

time-varying measure of domestic credit supply contraction (CCI) to the choice between different

sources of finance.

Our prior interpretation is that firms switch to alternative sources of finance when domestic credit

is tight because they are financially constrained. For this interpretation to be valid we must also

show that domestic credit supply conditions are not negatively correlated with bond market

liquidity or with changes in the supply of foreign banks’ credit.

Second, we document the currency risk transfer channel using a specification that relates the

currency denomination of newly issued loans with the lender cost of funding in the borrower

home currency.

a. Methodology

i. Credit crunch channel

12

Hypothesis 1 posits that more risky firms tend to borrow with foreign loans. We test this

hypothesis in two steps using the following baseline regression:

(1) ∗ ∗

In the first regression, the left-hand side variable is a dummy that takes value one if firm i

headquartered in country j issues a bond at time t and 0 if it issues a loan. In the second

regression, is a dummy that takes value one if the firm issues a syndicated loan at least partly

subscribed by a foreign (extra-Eurozone) lead bank and zero if it issues a (fully) domestic loan or

a bond. Hence all the firms in our analysis have a positive demand for debt.

is a firm fixed effect and a time fixed effect.14 Risky is a dummy that indicates whether the

firm is rated investment grade and Not risky whether it is rated below investment grade or not

rated. is a country level credit contraction index, i.e. a measure of the decline in the supply

of domestic bank credit which varies over time as well as across countries. The inclusion of firm

fixed effects is key to our analysis: it rules out the possibility that our results could be driven by

changes over time in the composition of firms raising debt. And the fact that we focus on changes

in the debt composition rather than the debt level means that we abstract from changes in the

demand for debt.

The coefficients of interest are and estimated by OLS.15 They are interpreted as average

effects on the probability that a firm issues a bond or borrows from a foreign bank. If Hypothesis

1 is verified we should obtain 0 and 0. We estimate equation (1) for the full sample

and for a sub-sample of debt issued for real investment purposes (general corporate purpose and

working capital).

14 All our results are also robust to the inclusion of country*time fixed effects. 15 We specify a linear probability model in order to include firms fixed effects. Our analysis would not

benefit from using non-linear models such as probit or logit (see Angrist and Pischke, 2009). All predicted probabilities from our model range between 0 and 1. Horrace and Oaxaca (2006) show that, as the relative proportion

of linear probability models (LPM)’ predicted probabilities that fall outside the unit interval increases, the potential bias of the LPM increases. Conversely if no (or very few) predicted probabilities lie outside the unit interval then the LPM is expected to be unbiased and consistent (or largely so).

13

To test Hypothesis 2, we run an augmented version of equation (1) allowing and to vary

across firm size bins.

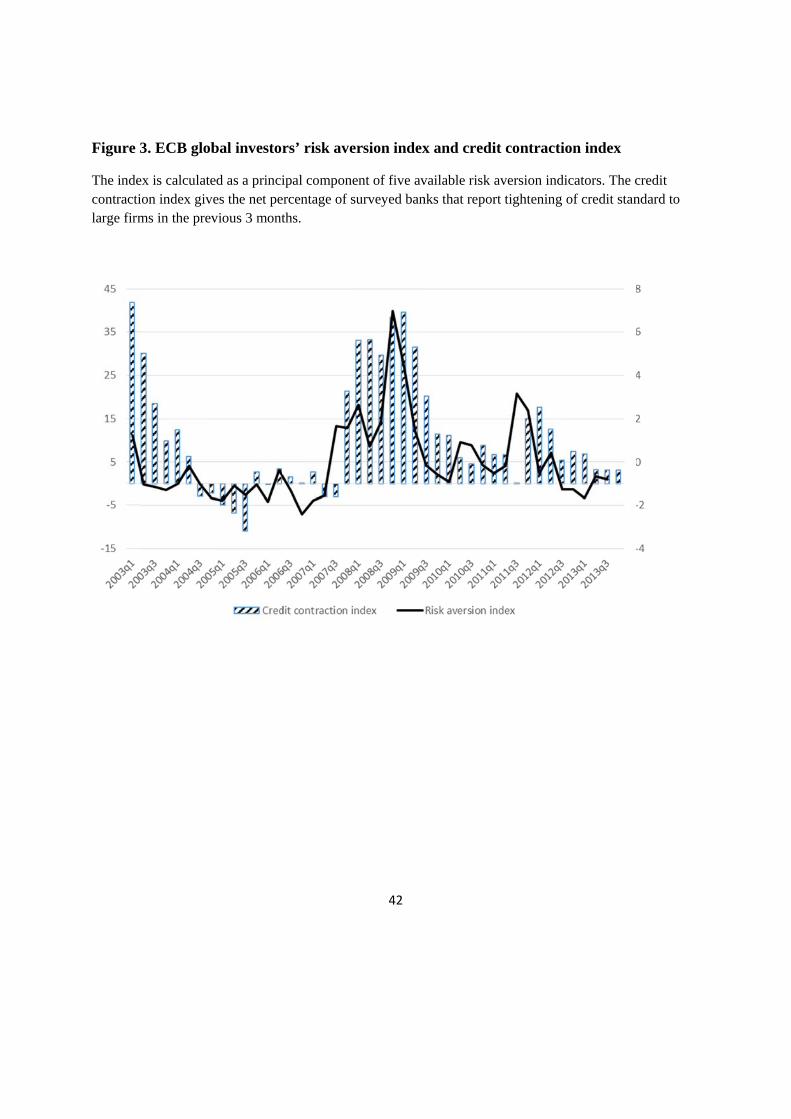

ii. Competing Interpretation

A competing interpretation for being positive is that bonds or foreign loans become more

attractive independently of the deterioration of the domestic supply of bank credit. A flight to

quality or liquidity in bond markets may render bonds more attractive for investment-grade

borrowers. Figure 3 shows a high correlation between CCI and bond investors risk aversion.

Foreign loans may become more attractive if the cost of funding of foreign banks falls relative to

the cost of funding of domestic banks due to looser monetary policy abroad. To test the relevance

of these alternative interpretations we proceed as follows:

1. In the case of the shift to bonds we let the coefficients and differ between firms

headquartered in countries that experienced a severe disruption in bond markets due to

heightened sovereign risk (GIIPS countries) and firms headquartered in other countries

(Not-GIIPS countries). If the shift to bonds is more significant for GIIPS corporates that

gives more credibility to the prior interpretation that the shift is due to the contraction in

bank credit rather than to the flight to quality in the bond market.

2. In the case of the shift to foreign loans we test the robustness of our estimates to adding as

a control variable the interaction between and the monetary policy rate abroad.

3. In addition, we test whether the difference in the spread between safe and risky borrowers

varies positively with CCI for bonds (indicating a positive correlation with a flight to

quality in the bond market) and negatively with CCI for foreign loans (indicating a

positive correlation with heightened search for yield among foreign lenders). For this we

estimate the following regression:

(2) ∑ ∑ ∗ ∑ ∗

Where spread is the cost of debt issued, are country*time fixed effects,∑ are issue type

fixed effects (bond, foreign loan, or domestic loan), and X is a vector of control variables including the

issue size, maturity, and issue purpose dummy (real investment purpose dummy). The other

variables are as previously defined (see Equation 1). Here too the inclusion of firm fixed effects

14

is important since otherwise, because of flight to quality or search for yield interest rate, spreads

across periods would not be comparable.

If >0, that indicates that the difference in the cost of bond debt between good and bad

borrowers widens during the credit crunch which is suggestive of CCI being positively correlated

with a flight to quality or liquidity in the bond market. That would cast doubt on the validity of

our prior interpretation.

If <0, that indicates that the difference in the cost of foreign debt between good and

bad borrowers narrows during the credit crunch, which is suggestive of CCI being positively

correlated with heightened search for yield among foreign lenders. Again that would cast doubt

on the validity of our prior interpretation.

iii. Currency risk transfer channel

Hypothesis 3 is tested using the following specification:

3 ∗ ∗ ∗

Where the left-hand side variable is a dummy that indicates if the loan issued is not in the

borrower home currency; RP is a vector of domestic (Euro) and foreign (Dollar) interbank risk

premium; Foreign indicates whether the lender is a foreign bank; and is a vector of control

variables including the borrower credit-quality, a dummy for whether the borrower has a natural

hedge against currency risk16, and the Euro-Dollar interest rate differential. The coefficients of

interest are , . A positive coefficient indicates that an increase in the cost

of funding in the borrower home currency reduces the probability that foreign banks lend in the

borrower home currency.

We run alternative specifications where we include triple interactions to test whether the

willingness of the borrower (or lender) to assume exchange rate risk vary with her natural hedge

against currency risk. We also run a specification where the main explanatory variable is the cost

of hedging against currency risk, the Euro basis, to assess how the spillover of money market

16 We measure this by whether she belongs to an export intensive sector (a sector with higher than median export sale to total sales)

15

disturbance to cross-currency swap markets affects the supply and demand of bank credit in

foreign currency (Hypothesis 4).

The specification reads as follows:

4 ∗ ∗ ∗ ∗ ∗

Where now also includes relevant partial terms and Hedged is a dummy that indicates

whether the firm belongs to an export intensive industry. If Hypothesis 4 is verified we should

obtain that 0 and 0.

iv. Real Effects of the Credit Crunch

To test Hypotheses 5 & 6 we estimate the difference in the change in employment and investment

during the credit-crunch for low-credit quality firms, between firms that have a relationship with

a foreign bank and firms that do not have such a relationship. The regression for the change in

real outcome R reads:

5 ∆ ∆ ∗ ∗ ∗

where ∆ is the lagged dependent variable; and are country and industry-sector fixed

effects; indicates whether the firm was rated below investment grade before the credit

crunch and capture the firm’s exposure to the credit crunch; is a vector of variables which

control for credit demand (cash holdings before the credit crunch, whether the last pre-crisis debt

issued was a credit line rather than a term loan or a bond, and whether the firm has a debt

maturing during the credit crunch), access to the bond market, and other relevant firm

characteristics (total assets and age). ( is a dummy that indicates whether

the firm belongs to a sector with higher (lower) than median export sales over total sales.

If foreign banking alleviates the financial constraint of firms we should expect to be

significant and negative only in the sample of firms that do not have a relationship with a foreign

bank. A firm with a foreign bank relationship is defined as a firm that has borrowed from a bank

headquartered outside the Eurozone at least once between 2003 and 2012 (our sample period).

16

Further if Hypothesis 6 is verified we should find that is not significantly different between

the sample of firms with and without a foreign bank relationship.

b. Data

Our benchmark sample covers the quarterly debt issuance of Eurozone non-financial corporates

during the period Q1-2003 to Q3-2013. The data source for bonds and syndicated loans is

Thomson-Reuters SDC platinum and Dealscan. We are able to distinguish between three sources

of finance: bonds, domestic syndicated loans, and foreign syndicated loans. For each form of debt

we observe the amount in US dollars, the purpose of the debt, the currency denomination, and

can separate real investment purpose debt and debt raised for other purposes such as mainly

refinancing and restructuring purposes (leveraged-buyouts, mergers and acquisitions). We also

obtain the (partially populated) spread to benchmark at issuance and maturity of the debt. We

include only non-convertible bonds and exclude mortgage backed-securities, asset-backed

securities, and preference shares which are listed as bonds. And include both term loans and

credit lines.

Foreign loans are defined as syndicated loans underwritten by at least one lead bank

headquartered outside the Eurozone. US banks participate in about 9% of all syndicates and other

foreign (i.e. extra-Eurozone) banks 20% on average over the sample period with peaks at 20%

and 30% respectively after 2008-Q3. Syndicated loans are often subscribed by more than one

lead bank, but we do not observe the contribution of each bank. In order to get a proxy for the

amount extended by foreign banks we prorate the total amount by the number of lead banks in a

syndicate.

The data are organized as a panel of firm-quarter observations with positive debt issuance over

the sample period. As our regression model includes firm fixed effects we eliminate firms that tap

only one source of finance because the coefficients in equation (1) can be identified only for

switchers, i.e. firms that switch from one source of finance to another.17

17 Hence our analysis will deliver lower band estimates of the real effect of the credit crunch because it misses firms that are excluded from all sources of finance.

17

We match the firm-level data with macroeconomic variables used in the analysis. The credit

contraction index (CCI) is from the ECB bank lending survey and measures the net percentage of

banks that report having tightened their lending standard for large firms in the past 3 months.

Although the method of calculation of this index is not harmonized across countries that does not

affect our analysis because our regressions include firms fixed effects. Three countries for which

the index is not available, Greece, Finland, and Belgium, are excluded from the sample. We use

the Fed fund target from Datastream to proxy for the stance of monetary policy abroad. This is

motivated by the fact that US banks are the main source of bank finance from abroad.

Table 1 reports summary statistics for the variables issued in regressions (1), (2), and (3) for the

sample of firms that issue both bonds and loans (Panel A); the sample of firms that issue both

domestic and foreign loans (Panel B); and the sample of firms that issue both foreign and

domestic currency denominated syndicated loans (Panel C). Non-investment grade firms

represent about one third of the observations in both samples. Bond spreads at issuance are

calculated as yields above the equal maturity ECB yield curve spot rate. Loan spreads at issuance

are all in drawn spreads above Libor. In Panel A, bonds represent 63 per cent of total debt issued,

the average spread to benchmark is about 137 basis points for bonds and 112 basis points for

loans, and maturity on average about 9 years for bonds (value weighted average by quarter) and 5

years for loans. The average spread for non-investment grade borrowers (all instruments

confounded) is 212 basis points and the average maturity 9 years indicating that low-credit

quality borrowers are charged higher spreads but borrow at longer maturities compared to high-

credit quality borrowers. Average issue size is above 1 billion USD. The characteristics of debt

instruments in the second sample are about the same. Here the share of bank debt subscribed by

at least one foreign bank is above 60 per cent.

The credit contraction index experienced important variations over the sample period from -7% at

the 10th percentile to 39.2% at the 90th percentile. Variations across country are important with

an earlier, more persistent, and deeper contraction of credit in southern countries. The period

covered also witnessed important fluctuations in the stance of US monetary policy with the

average quarterly fed funds target varying between 1.76% and 5.22%. Hence the importance of

controlling for US monetary policy, as loose monetary policy could trigger higher risky taking

18

among US banks and therefore would contribute also to explain changes in the pattern of

corporate financing across different types of Eurozone corporates.

In Panel B, foreign loans represent more than 60% of the sample. The sample is comparable to

the sample used in specification 1 as regards the characteristics of the debt issued, the

characteristic of the average borrower, and macroeconomic variables. In Panel C we report the

average interbank market risk premium for the domestic market and the US market and the

currency basis (the cost of hedging against EUR/USD exchange rate risk). The US premium

reached significantly higher values following the Lehman default and significantly lower values

since the break out of the Eurozone sovereign debt crisis. The currency basis is the difference

between the FX-swap implied dollar rate and the USD Libor 3 month, a measure of the cost of

hedging against EUR/USD exchange rate risk. The FX-swap implied dollar rate is calculated as

1 3 to which we add a spread which we assume to equal the difference

between USD Libor 3 M and Euro OIS 3 month. is the ratio between the EUR/USD 1 year

forward exchange rate and the spot rate. Rates and exchange rate data are downloaded from

Reuters. The currency basis experienced two peaks in Q4-2008 (Lehman collapse) and Q3-Q4

2011 (Greek crisis).

Table 2 summarizes the composition of our sample by country. Columns I and III show the

number of observations for the sample of firms with access to the bond market and for the sample

of firms with a foreign bank relationship by country. In column II the share of bond debt seems

high for Portugal and Austria which is attributable to the fact that we do not cover small loans. In

column IV the percentage of debt that are subscribed by foreign banks is generally high at around

60% on average (74% for Spain and Portugal), and the average prorated contribution of foreign

banks (column V) is about 35%. When we consider the full sample of firms with and without a

foreign bank relationship, the participation of foreign banks is much higher in foreign currency

loans than in domestic currency loans, 75% and 42%, respectively.

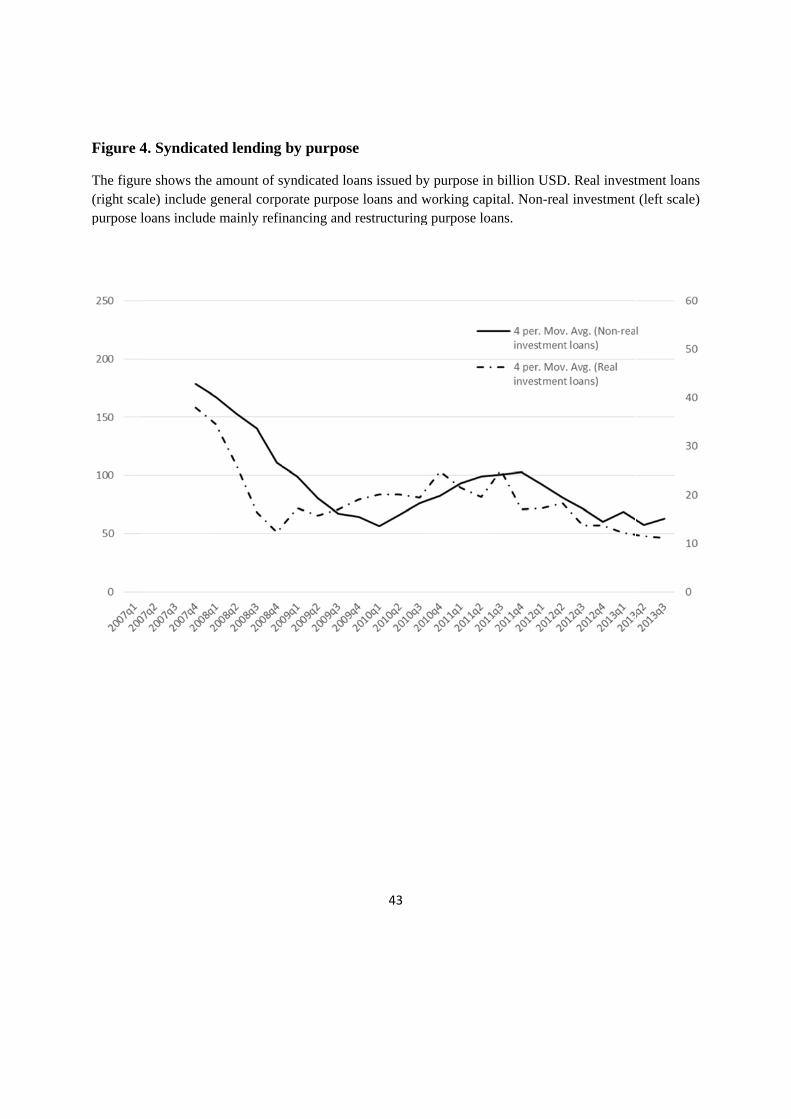

Figure 4 shows the sharp decline in syndicated lending since 2007 by loan purpose, with a more

immediate decline in real investment purpose loans.

To estimate regressions (4) and (5) we hand-matched the SDC data with the Bureau van Djink

Amadeus data which contains the number of employees by firm and firms’ balance sheet data.

19

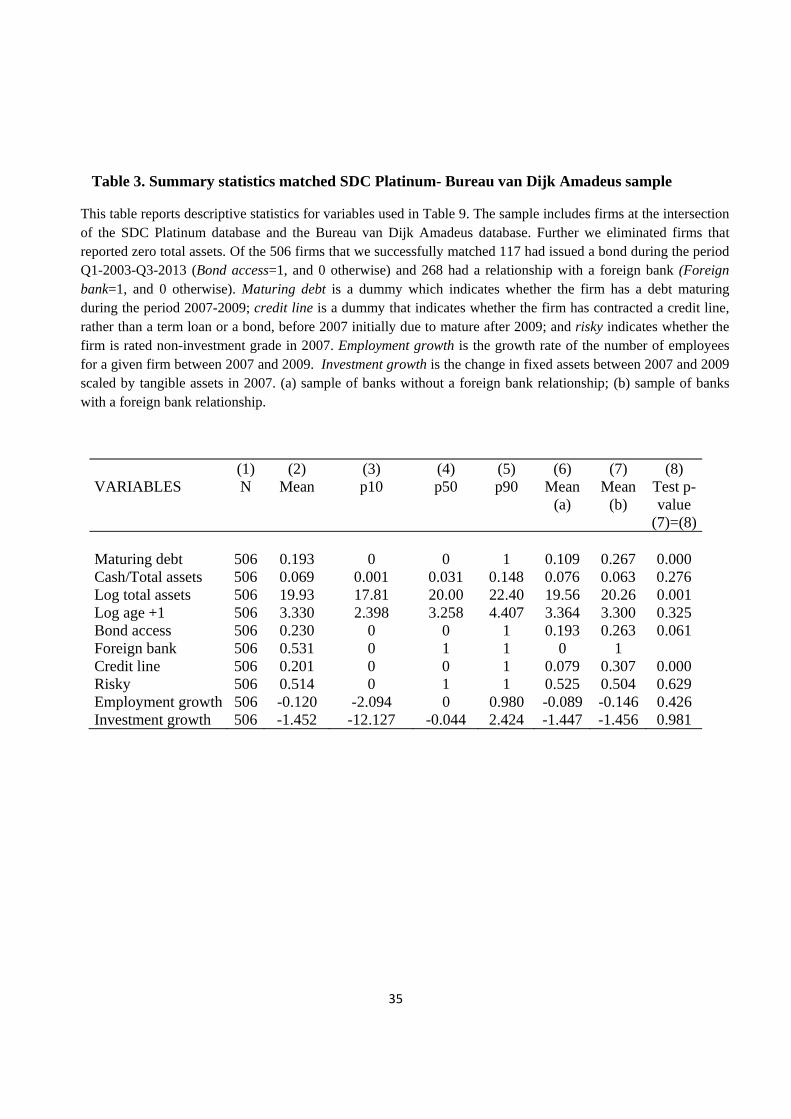

We could exactly match 691 firms and after eliminating firms that reported zero total assets in

2007 we were left with a sample of 506 firms and nine countries. Of these 506 firms about half

are non-investment grade firms or leveraged firms, 116 have issued a bond over the SDC sample

period and 268 firms had a relationship with a foreign bank, which means that they borrowed at

least once from a foreign lead bank between 2003 and 2012.

Table 3 reports the descriptive statistics of the variables used in the regressions for the sample of

firms at the intersection of SDC and Amadeus. The sample is about equally split between firms

with and without a foreign bank relationship and risky and safe firms. We notice that about 20%

of the firms have debt maturing during the credit crunch and the same proportion had contracted

a credit line rather than a term loan or a bond pre-crisis initially due to mature after 2009.18 Both

proportions are significantly higher for the sample of firms that have a relationship with a foreign

bank. Another variable we obtain to capture the demand for credit is the cash to total assets ratio

in 2007. Cash includes bank accounts and cash equivalents such as marketable securities and

short-term government bonds.

The growth rate in the number of employees per firm (winsorized at the 1% and 99% level to

remove outliers) is on average -12% between 2007 and 2009, and twice higher in the sample with

a foreign bank relationship, suggesting that the fact that these firms had greater reliance on credit

lines, were slightly less liquid, and were more likely to have debt maturing during the credit

crunch, caused them to lay off more. Because firms with and without a foreign bank relationship

differ in all these dimensions which matter for employment it is important to control for all these

factors to be able to properly identify the role of foreign banking as a cushion against domestic

credit shocks.

Figure 5 shows that the drop in the number of employees per firm between 2005 and 2012

coincides with the timing of the credit crunch. We observe a decline already starting in 2006 but

this is due to an increase in the number of firms reporting to Amadeus in 2007, for this reason we

focus our analysis on the change between 2007 and 2009.

We also calculate investment growth as the ratio of the change in fixed assets between 2007 and

2009 scaled by tangible assets in 2007 (also winsorized at the 1% and 99% level to remove 18 This is meant to capture whether the firm raised an instable or a stable form of debt to cover its liquidity needs during the credit crunch.

20

outliers). We set negative values to zero. We next turn to the multivariate regression analysis of

our data testing one hypothesis at a time. This will allow accounting for confounding factors

which a simple comparison of means cannot do.

4. Results

This section is organized as follows. First, we document the switch to alternative forms of finance

in reaction to the credit crunch and discuss estimates of equation (1). We discuss estimates of

equation (2) which we use to assess the validity of our prior interpretation that borrowers

increasingly tap alternative sources of finance because they are credit constrained rather than

because these alternative sources of finance become more attractive due to (simultaneous) flight

to quality or search for yield. Then we assess the relevance of the currency risk transfer channel

using equation (3). Finally, we turn to the estimation of equation (4) which we use to study the

real cost of the credit crunch and the mitigating role of foreign banking.

a. Safe borrowers shift to bonds

In Table 4 we report estimates of equation (1) when the dependent variable is a dummy that takes

value 1 if the firms issues a bond and 0 if it issues a loan. Hence the estimates are interpreted as

average effects on the probability of issuing a bond. In column I, is positive and statistically

significant at the 5 per cent level and is negative and statistically significant at the 10 per cent

level, which confirms hypotheses 1: as domestic bank credit contracts investment grade firms

shift to bonds and non-investment grade firms shift to loans. The effect is also economically

significant: a contraction of credit from the 10th percentile to the 90th percentile is associated with

an increase 7.5 percentage point increase in the probability of issuing a bond for investment grade

firms and an 8 percentage point increase in the probability of issuing a loan for non-investment

grade firms.

Next we split the sample of firms into three size bins (large, medium, and small) and re-estimate

the coefficients and for firms falling in each bin. The results reported in column II confirm

that larger or more transparent firms have a better access to the bond market. For the investment

grade medium size firm a contraction of credit from the 10th percentile to the 90th percentile is

21

associated with a 9.7 per cent increase in the probability of issuing a bond. In contrast the effect

is insignificant for small firms irrespective of their credit quality and significantly different

statistically from the effect for large and medium size firms.

The fact that investment grade firms shift to bonds may be interpreted as evidence that they

experience a decline in bank lending and that the bond market acts as a shock absorber.

However, this interpretation fails if simultaneously to the contraction of credit the bond market

experiences a flight to quality. Indeed if that is the case one could suppose that investment grade

firms shift to bonds because bond finance becomes more attractive for them (see Figure 3). In

column III we report a first test for this competing interpretation. We estimate and for

firms headquartered in GIIPS countries and Not-GIIPS countries. There is evidence that bond

markets in GIIPS countries have witnessed important disruptions due to heightened sovereign

risk (Almeida et al, 2014). We find that is not significant for firms in the GIIPS countries but

is significant for firms in the countries that benefited from a flight to quality which casts doubt on

the validity of our initial interpretation and is suggestive of the fact that high-credit quality firms

shift to bonds not because they are financially constrained but because they enjoy a flight to

quality in the bond market. Further in columns IV to VI the shift to bonds is not significant

whatever the size of firms when we restrict the sample to real investment purpose debt, which are

expected to matter more for real outcomes like employment and investment. Throughout the

estimated difference in the shift to bonds between high credit quality and low credit quality firms

is robust to including country*quarter fixed effects.

All in all, at this stage we are not able to rule out the possibility that firms that increasingly tap

the bond market during the credit crunch do so because they benefit from a flight to quality and

not to compensate for a decline in bank lending.

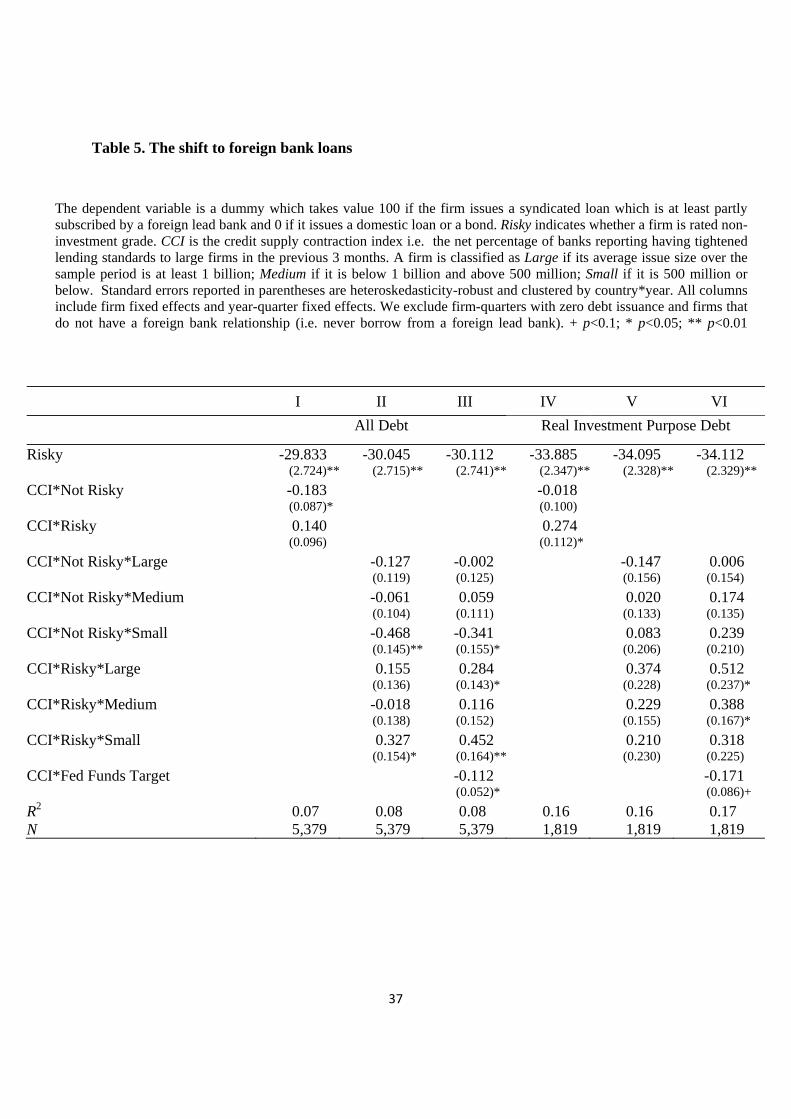

b. Risky borrowers shift to foreign loans

In Table 5 we report estimates of equation (1) when the dependent variable is a dummy that

indicates whether a firm borrows from a foreign bank in a given quarter. In column I we confirm

that high credit quality firms shift away from loans ( < 0) and is positive but not

statistically significant. In column II we report the estimates for different size bins. Here

interestingly and in line with Hypothesis 2 we find that is bigger in magnitude, negative and

22

statistically significant for small investment grade firms. Indeed this result, combined with the

result reported in Table 4, indicates that this category of borrowers switches from foreign loans to

domestic loans.

is positive and statistically significant at the 5 per cent level for small non-investment grade

firms. In other words, the switch to foreign loans is economically and statistically significant for

low-credit quality and small firms, i.e., those firms that are most likely to be credit constrained

and have limited access to bond finance.

In column III we control for the fed funds target to account for the fact that the stance of foreign

monetary policy affects the supply of credit of foreign banks to low-credit quality Eurozone

firms. And consistent with Hypothesis 1, is positive and statistically significant for both

small and large firms. For small firms a contraction of credit from the 10th percentile to the 90th

percentile is associated with about a 15 percentage point increase in the probability to borrow

from a foreign bank.

In columns IV to VI, the previous results for non-investment grade firms are verified when we

restrict the sample to real investment purpose loans, whatever their size, low-credit quality firms

shift to foreign loans. And the fact that the estimates are not altered when we control for the

stance of monetary policy abroad suggests that the increased reliance on foreign loans is caused

by an increase in the demand for credit by credit-constrained firms rather than an increase in the

supply of credit by foreign lenders.

The estimated difference in the shift to foreign debt between high credit quality and low credit

quality firms is robust to including country*quarter fixed effects. And to using as dependent

variable the (prorated) proportion of the amount of debt extended by foreign lenders.

In order to strengthen our interpretation of the results we next turn to the estimation of equation

(2).

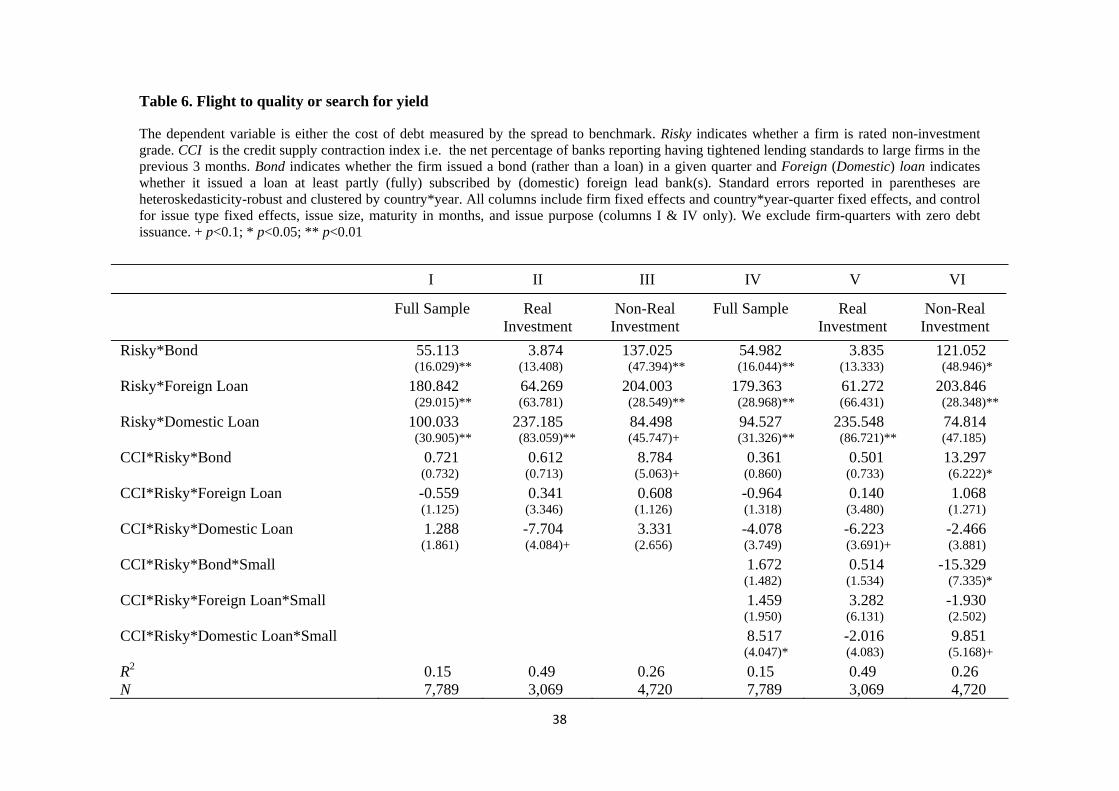

c. Competing interpretation: flight to quality or search for yield

The results are reported in Table 6. The dependent variable is the cost (spread) of new debt issued

in a given quarter and for three samples: the full sample, the sample of real investment purpose

debt, and the sample of non-real investment purpose debt.

23

In columns I and II we report the estimates for the spread on the full sample of debt issued and

for the sample of real investment purpose debt. As predicted is positive and

is negative but none of these estimates are significant statistically. Now if we focus on the sample

of non-real investment purpose debt for which we found the shift to bonds to be most significant,

we find that is positive, large, and statistically significant. Further we find that both

and are statistically insignificant consistent with Holmstrom and

Tirole (1997) who predict that credit crunches increase the interest rate spread between

intermediated debt and market debt. They further demonstrate that when both intermediary

capital and firm capital contract, the sign of the change in the interest rate depends crucially on

the change in the relative amounts of capital. Our estimates indicate that bonds become cheaper

than loans for investment grade borrowers and the contrary for non-investment grade borrowers.

In columns IV to VI, we re-run the regressions allowing the coefficients to be different for small

firms for which we found the shift to bonds to be weaker and the shift to foreign debt to be

stronger. Our findings are confirmed. In addition we find that the increase in the cost of domestic

bank debt is higher for small non-investment grade firms compared with small investment grade

firms during the credit crunch. In other words, firms that suffer most from the credit crunch are

small low-credit quality firms.

Importantly, with this additional tests we are not able to exclude the hypothesis that investment-

grade borrowers switch to bonds due to a flight to quality in bonds rather than due to a decline in

bank credit. Instead we can more firmly state that non-investment grade borrowers switch to

foreign loans because they are financially constrained rather than because foreign loans become

more attractive due to heightened search for yield.

Next we provide evidence through the estimation of equation (3) that foreign banks lend less in

the borrower home currency especially when the cost of funding in the borrower home currency

increases relative to the cost of funding in the lender home currency.

d. Currency risk transfer channel

Estimates of equation (3) are reported in Table 7. In column 1, we find that foreign banks

increasingly lend in their home currency (rather than the borrower home currency) when the

borrower home currency risk premium increases. Consistent with Hypothesis 3, an increase in the

24

Euro risk premium from the 10th to the 90th percentile is associated with a 26 percentage point

higher probability that a foreign bank loan is denominated in foreign currency. In columns II we

confirm that borrowers that have a natural hedge against currency risk are more willing to assume

the exchange rate risk. In column III the currency risk transfer channel remains significant if we

control for the interest differential between Eurozone and US. Here interestingly we confirm the

prediction of Aghion et al. (2004) and find that risky borrowers who deal with a foreign bank

increase their borrowing in dollar when the interest differential rises but not safe borrowers. In

column IV we find that the results are robust to the inclusion of country*year-quarter fixed

effects. In column V we test Hypothesis 4 using the currency basis instead of the interbank

premium. Here we find as expected that domestic banks reduce their supply of dollars to

exporters, in other words a domestic bank is less likely to lend in dollar to a borrower that has a

natural hedge against currency risk (an exporter) when the cost of synthetic dollar funding

increases. This effect is positive if the lender is a foreign bank (it is significant in column IV, but

not in column V). Further we find that exporters tap the currency swap market less (they borrow

more in dollar from foreign banks) as the currency basis rises. Instead when the currency basis is

zero they prefer borrowing from banks in Euro and exchanging the euro loan against dollars in

the swap market to benefit from a lower cost of dollar borrowing.

All in all, we find supporting evidence that foreign banks lend less in the borrower home

currency as the cost of funding in the borrower home currency increases so that a greater reliance

on foreign banks is increasingly associated with higher borrowing in foreign currency.

e. Robustness checks

In Table 8 we report two additional robustness checks. First we verify whether the shift to foreign

banks is driven by US banks being subject to Basel I regulation. Basel I does not attribute a risk

weight higher for risky corporates than for non-risky corporates potentially incentivizing US

banks to load onto risky corporate debt. To do that we first exclude loans extended by other

foreign banks from the sample and then loans extended by US banks for comparison. The results

are reported in columns I and II. For both samples we find the shift to US and non-US foreign

25

banks to be significant, however it is larger and more significant for non-US foreign banks which

indicates that the US banks are not driving our results.

Next, since most (95%) of the foreign currency lending is in dollar, we check whether the

currency risk transfer effect is driven by US banks; non-US foreign banks and domestic banks

being equally vulnerable to the dollar shortage. To do that we separate out the effect of the

increase in the Euro-risk premium and the currency basis for US and non-US foreign banks. The

results are reported in columns III and IV. In column III, we find that an increase in the Euro-risk

premium leads to a higher probability that a foreign bank lends in foreign currency (mostly

dollar) when the foreign bank is a US bank but not when it is a non-US foreign bank. The results

are robust if we exclude from the sample the few non-USD loans but become slightly weaker due

to small sample size. In column IV we confirm that an increase in the cost of synthetic dollar

funding affects non-US foreign banks and domestic banks similarly, both group of banks reduce

dollar lending when the basis rises (albeit not to exporters for the non-US foreign banks). In sum,

the currency risk transfer effect is mostly attributable to US banks’ lending more in dollar.

Next, irrespective of the currency in which foreign banks lend, we want to assess whether the

increased reliance of Eurozone corporates on foreign banks has real effects i.e. whether it has

contributed to mitigate the consequence of the credit crunch on employment and investment.

f. Foreign banking alleviates firms’ financial constraints

In Table 9 we report estimates of equation (5) when the dependent variable is either employment

growth (columns I and II) or investment growth (columns III and IV) between 2007 and 2009. In

columns I and III, we report estimates for the sample of firms without a foreign bank relationship

and in columns II and IV for the sample of firms with a foreign bank relationship. In line with

Hypothesis 5, low-credit quality firms do not downsize and do not cut investment more than high

credit quality firms in the sample of firms with a foreign bank relationship, but they do cut

investment more in the sample of firms without a foreign bank relationship. And the difference

between low and high-credit quality firms is economically significant if we compare the

estimates with mean investment growth (-1.452). Interestingly, we find that in the sample of

firms with a foreign bank relationship, firms downsize more if they contracted a credit line rather

than a term loan or a bond to cover their liquidity needs during the credit crunch but not in the

26

sample of firms without a foreign bank relationship (the estimate in column I is significantly

lower than in column II). This might suggest that foreign banks are more likely than domestic

banks to revoke credit lines in a crisis.19 Other results (unreported) indicate that in the full sample

firms which have a higher cash buffer in 2007 downsize less. Also, firms with access to the bond

market reduce investment less (column IV). This effect is not statistically different between the

samples of firms with and without a foreign bank relationship.

Importantly, we allow that transmission of the credit crunch to employment and investment to

vary for firms with and without a natural hedge against exchange rate risk. Consistent with

Hypothesis 6 we find that financially constrained firms (i.e. low-credit quality firms) downsize

more than other firms during the credit crunch when they have no natural hedge against currency

risk (column I). The difference in the coefficients between hedged and unhedged firms is

statistically significant. This may be attributable also to the fact that exporters have a larger

(global) client base and are therefore less vulnerable to local shocks. What is of more interest is

therefore the difference between firms with and without a foreign bank relationship. When the

dependent variable is employment, the difference in (equation 5) between column I and II is

not statistically significant. However when we turn to a more flexible adjustment variable,

investment growth, the difference in between column III and IV is insignificant for unhedged

firms but significant for hedged firms. Since foreign banks lend more in foreign currency than

domestic banks, the real benefit of having a relationship with a foreign bank is more important

for firms that have a natural hedge against currency risk. Arguably, employment is a less flexible

adjustment variable than investment due to labor market protection laws and hiring and firing

costs which may explain why this results holds only for investment growth.

In sum, the real consequences of the domestic credit crunch are weaker for low-credit quality

(exposed) firms that have a relationship with a foreign bank and for firms belonging to export

intensive sectors that would supposedly have a weaker mismatch between foreign-currency debt

and revenues. This is consistent with the theoretical prediction that risk-averse banks would cut

credit in foreign currency (or at least not augment it) when currency risk is transformed into

19 Acharya et al (2013) argue that credit lines are a less reliable form of finance in a crisis since banks retain the right

to revoke them when a firm is in financial distress.

27

credit risk rather than transferred to borrowers who can assume it (Shapiro, 1985). Further, the

additional cost of having to borrow in foreign currency is larger for firms without a natural hedge

against currency risk and this can eventually weigh on employment and investment growth.

Cowan (2006) predicts that if a bank knows that a firm is mismatched, it will pass on the

corresponding expected default costs immediately.

5. Conclusion

We have uncovered new mechanisms that explain cross-sectional and time-series variations in

foreign currency borrowing at the firm level. The existing literature emphasizes the role of

demand side factors in determining the currency denomination of debt, mainly the borrower’s

export intensity or foreign currency income and the interest rate differential between domestic

and foreign currency loans. In this paper we have shown that during liquidity crises supply side

factors matter more for low-credit quality firms: the lenders’ cost of funding in domestic currency

which alters both the supply of credit by domestic lenders and the currency risk management

strategy of foreign lenders (more precisely their willingness to assume currency risk or transfer it

to the borrower) is key in explaining higher foreign currency borrowing. By shifting attention to

funding issues as the constraint on bank lending, we have been able to explain changes in the

currency composition of debt. This could not be explained by a shock to bank capital alone as

such shock would tend to cause a reduction in credit across the board.

Our analysis also deliverers new results on the stabilizing role of foreign banks during crises. We

have shown that the real benefit of foreign banking is significant for foreign currency earners

(exporters). This suggests enhanced international risk sharing through global entrepreneurship

combined with global banking. While Eurozone banks have been the principal contributor to the

observed aggregate decline in international banking flows, non-Eurozone banks have experienced

the opposite trend taking advantage of the opportunity offered by the retreat of Eurozone banks

and increasing their share in cross-border credit including credit to Eurozone firms.

28

Finally, by showing that low-credit quality firms increasingly rely on foreign banks, we confirm

the theoretical prediction that the category of borrowers who suffer most from a credit crunch are

better served by financial intermediaries than by markets. Bond markets did not act as shock

absorbers for financially constrained corporates. The depth and duration of the great recession in

Europe is often explained by the over reliance of European corporates on bank finance and the

“underdevelopment” of the capital market. Multiple calls have been voiced to create better

conditions for firms to turn to markets when banks are distressed which culminated with

Commissioner Jean-Claude Junker’s idea to establish a so called capital markets union. 20 Our

analysis demonstrates that the bond market served firms that were least in need of finance, which

explains its timid role in mitigating the transmission of the credit crunch to the real economy. In

contrast, foreign banks proved to be more flexible due to monitoring, ease of renegotiation, and

their ability to diversify risk internationally. Foreign banking effectively contributed to alleviate

the financial constraint of poorly capitalized firms.

References

Acharya V. V., H. Almeida, F. Ippolito, and A. Perez (2013). Credit Lines as Monitored

Liquidity Insurance: Theory and Evidence. Journal of Financial Economics, 112 (3), 287-319.

Acharya V.V., T. Eisert, C. Enger, and C. Hirsch (2014). Real Effects of the Sovereign Debt

Crisis in Europe: Evidence from Syndicated Loans. Working paper NYU Stern

Acharya V. V. and O. Merrouche (2013). Precautionary Hoarding of Liquidity and the Interbank

Markets: Evidence from the Sub-Prime Crisis. Review of Finance 17, (1), 107-160

Acharya V. V. and N. Mora (2015). A Crisis of Banks as Liquidity Providers. Journal of

Finance, Volume 70, Issue 1, pages 1–43

20 “Political Guidelines for the Next European Commission”, Opening Remarks, Jean-Claude Junker, European Parliament, 15 July 2014. See also Financial Times, « Europe needs a more flexible financial market”, September 2014; Steven Majoor, “Capital Markets Union: building competitive, efficient capital markets trusted by investors”, President, European Securities and Markets Authority November 2014; Reuters, “A capital markets union could kick start growth in Europe”, October 2014.

29

Aghion, Ph., Bacchetta, Ph., and Banerjee, A. (2004). A Corporate Balance-sheet Approach to

Currency Crises, Journal of Economic Theory 119, 6–30.

Almeida, H., I. Cunha, and M. Ferriera, 2014. The Real Effects of Credit Ratings: The Sovereign

Ceiling Channel. Working paper

Angrist, J. and J. Pischke (2009). Mostly Harmless Econometrics, Princeton University Press

Baba, Noahiko, Frank Packer and Teppei Nagano, 2008, “The Spillover of Money Market

Turbulence to FX Swap and Cross-Currency Swap Markets,” BIS Quarterly Review (Basel,

March).

Becker, B. and Ivashina, V. (2014). Cyclicality of Credit Supply: Firm Level Evidence. Journal

of Monetary Economics, 62, 76-93.

Bentolila S., Jansen M., Jiménez G., and Ruano S. (2013). When Credit Dries Up: Job Losses in

the Great Recession. Working paper CEMFI

Bernanke, B. (1983). Nonmonetary Effects of the Financial Crisis in the Propagation of the Great

Depression. American Economic Review, 73 (3), 257-276

Broner, F., Didier, T., Erce, A., Schmukler, S. (2013). Gross Capital Flows: Dynamics and

Crises. Journal of Monetary Economics 60, 113-133.

Bruno V. and R. Hauswald (2013). The Real Effect of Foreign Banks. Working paper American

University

Buch M. and J. Suarez (2010). Deposit insurance and money market freezes. Journal ofMonetary

Economics, 57 (2010), 45-61

Burnside, C., Eichenbaum, M. and Rebelo S. (2004). Government Guarantees and Self-Fulfilling

Speculative Attacks. Journal of Economic Theory 119, 31-63.

Chodorow-Reich G. (2013). The Employment Effect of Credit Market Disruptions: Firm-Level

Evidence from the 2008-9 Financial Crisis. The Quarterly Journal of Economics, October PP 1-

59

30

Cingano F., F. Manaresi, E. Sette (2013). Does Credit Crunch Investments Down? New Evidence

on the Real Effects of the Bank-Lending Channel. Working paper Bank of Italy

Cowan K. (2006). Firm Level Determinants of Dollar Debt?. (Central Bank of Chile, Santiago),

Mimeo

Diamond D. (1991). Monitoring and Reputation: The Choice between Bank Loans and Directly

Placed Debt. The Journal of Political Economy, 99 (4), 689-721

Duchin, R. and Sosyura D. (2014), Safer Ratios, Riskier Portfolios: Banks’ Response to

Government Aid. Journal of Financial Economics (113), 1-28

Giannetti, M and Laeven, L. (2012). The Flight Home Effect: Evidence from the Syndicated

Loan Market during Financial Crises. Journal of Financial Economics, 104 (1), 23-43

Giannetti, M. and Laeven, L. (2012b). Flight Home, Flight Abroad, and International Credit

Cycles. American Economic Review 102, 219-224.

Haltenhof S. , L. Seung Jung, and V. Stebunovs (2014). The Credit Crunch and Fall in

Employment during the Great Recession. Journal of Economic Dynamics and Control, vol. 43,

pp. 31-57

Haselmann R. and P. Wachtel 2011. Foreign Banks in Syndicated Loan Markets. Journal of

Banking and Finance, Volume 35, pp 2679-2689

Holmstrom B. and J. Tirole (1997). Financial Intermediation, Loanable Funds, and the Real

Sector. The Quarterly Journal of Economics, 112 (3), pp 663-691

Horracea W.C. and R. L. Oaxacab (2006). Results on the Bias and Inconsistency of Ordinary

Least Squares for the Linear Probability Model. Economics Letters, Volume 90, Issue 3, p 321–

327

Ivashina, Victoria, David S. Scharfstein, and Jeremy C. Stein. (2012). Dollar Funding and the

Lending Behavior of Global Banks. NBER Working Paper No. 18528.

31

Jeanne, O. (2005). Why Do Emerging Economies Borrow in Foreign Currency? in Other

People’s Money, B. Eichengreen and R. Hausmann eds., Chicago: University of Chicago Press,

pp. 190-217.

Keloharju, M. and M. Niskanen (2001). Why Do Firms Raise Foreign Currency Denominated

Debt? Evidence from Finland. European Financial Management 7, 481-496.

Laeven L. and F. Valencia (2013). The Real Effects of Financial Sector Interventions during

Crisis. Journal of Money, Credit, and Banking, Volume 45, Issue 1.

McCauley, Robert N., Patrick McGuire, and Vladyslav Sushko (2015). Global Dollar Credit:

Links to US Monetary Policy and Leverage. BIS Working Paper No. 483.

Milesi-Ferretti, G.-M. and Tille, C. (2011). The Great Retrenchment: International Capital Flows

during the Global Financial Crisis. Economic Policy 66, 289–346.

Rose, A., Wieladek, T. (2014). Financial Protectionism: The First Tests. Journal of Finance 69,

2127-2149.

Schneider, M. and Tornell, A. (2004). Balance Sheet Effects, Bailout Guarantees and Financial

Crises. Review of Economic Studies 71, 883-913.

Shapiro A. (1985). Currency Risk and Country Risk in International Banking. Journal of Finance,

Volume 40, Issue 3, pages 881–891

Sufi A. (2007). Bank Lines of Credit in Corporate Finance: An Empirical Analysis. The Review

of Financial Studies. 22 (3), pp 1057-1088

Uhlig H. and De Fiore F. (2013). Corporate Debt Structure and the Financial Crisis. Working

paper ECB

Williamson S. (1987). Costly Monitoring, Loan Contracts, and Equilibrium Credit Rationing.

The Quarterly Journal of Economics, 102 (1), pp 135-146.

32

Table 1. Summary statistics SDC Platinum sample

This table reports the number of firm-quarter observations with positive debt issuance (column I), means (column II) and percentiles (columns III-V) for the variables used in our regressions reported in Tables 4, 5, and 6. In column VI we report the mean for debt issued for real investment purposes only. Panel A covers the sample of firms that have issued at least one bond in the sample period 2003-Q1 to 2013-Q3 and Panel B the sample of firms that have issued syndicated loans at least once with a foreign bank (headquartered outside the Eurozone) as lead bank. Panel C covers the sample of firms that issue both domestic and foreign currency denominated loans. Risky is a dummy that indicates whether a firm is rated non-investment grade. The Credit Contraction Index (CCI) is from the ECB bank lending survey and gives the net percentage of banks that report having tightened credit standards to large firms in the previous 3 months. Share of bond debt is the percentage of debt issued in the form of bonds. Share of foreign bank debt is the percentage of debt that is issued in the form of a syndicated loan for which at least one of the lead bank is a foreign bank. The Euro (Dollar) premium is the spread between the 3 month Euribor (Libor USD) and equal maturity Euro (Dollar) OIS. The Basis is the difference between the FX-swap implied dollar rate and the USD Libor 3 month, a measure of the cost of hedging against EUR/USD

exchange rate risk. The FX-swap implied dollar rate is calculated as 1 3 to which we add a spread

which we assume to equal the difference between USD Libor 3 M and Euro OIS 3 month. is the ratio between the

EUR/USD 1 year forward exchange rate and the spot rate. Rates and exchange rate data are downloaded from Reuters.

A. Sample of Firms with Bond Market Access

I II III IV V VI VARIABLES N Mean

All debtp10 p50 p90 Mean

Real Investment purpose debt

Risky 5,379 0.317 0 0 1 0.231 Credit Contraction Index (CCI) 387 11.610 -7 6 39.2 Fed funds target 43 1.76 0.23 1 5.22 Share of bond debt 5,379 19.77 0 0 100 46.96 Spread to benchmark 4,572 150.2 0 40 392.0 106.8 Maturity in months 4,227 87.54 36 70.13 132 89.07 Share of foreign bank debt 5,379 61.41 0 100 100 41.12 Issue size in USD billion 5,379 1.095 0.085 0.478 2.328 0.910

33

B. Sample of Firms with a Foreign Bank Relationship

C. Sample of Firms which issue both domestic and foreign currency denominated loans

(1) (2) (3) (4) (5) VARIABLES N Mean p10 p50 p90 Risky 1,118 0.264 0 0 1 Share of foreign bank debt 1,118 0.742 0 1 1 Euro premium 43 0.303 0.055 0.126 0.727 Dollar premium 40 0.312 0.073 0.135 0.750 Basis 43 0.239 -0.003 0.109 0.729 Share of foreign currency loans 1,118 0.670 0 1 1

I II III IV V VI VARIABLES N Mean

All debt p10 p50 p90 Mean

Real Investment

purpose debt