Gérard Naulleau, 2006 1 Management Control Management Control Systems and Procedures MBA 2006...

25

Gérard Naulleau, 2006 1 Management Control Management Control Systems and Procedures MBA 2006 Gérard Naulleau

-

Upload

camron-doyle -

Category

Documents

-

view

218 -

download

4

Transcript of Gérard Naulleau, 2006 1 Management Control Management Control Systems and Procedures MBA 2006...

Gérard Naulleau, 2006 1

Management Control

Management Control Systems and Procedures

MBA 2006Gérard Naulleau

Gérard Naulleau, 2006 2

Session objectives

1. Get familiar with key management planning and control procedures

2. Discuss current trends and developments in management control

Gérard Naulleau, 2006 3

• 2 years as a junior consultant : KPI for productivity analysis and Management Information Systems Implementation

• 10 years as a trainer in the banking sector for profitability analysis and implementation of planning, budgeting and reporting procedures

• ESCP (1984 -1991) + EAP (1992-1999) + ESCP-EAP (2000 …)

• Consultant for the French Ministries of Finance and Defence on the implementation of performance contracts (Implementation of the new law on resource allocation) • Academic Director of ESCP-EAP MS “International Project Management”

Current fields of interest : (1) inter-organizational collaborative performance (2) implementation of performance driven cultures

Gérard Naulleau

Gérard Naulleau, 2006 4

“Provide information to support decisions and guide managers and employees behaviour towards the organization’s strategies and goals “ Kaplan, 2002

Management Control ?

“Process by which managers ensure that resources are used effectively and efficiently to attain organizational goals” Anthony RN & Dearden J, 1976

Defining the scope of Management Control

What Gets Measured Gets Managed !

Gérard Naulleau, 2006 5

“ A management planning and control system can be defined as the set of processes and practices used to align and control an organization”

Management planning and control systems include the procedures for :

• aligning strategies between business units and corporate level, • setting goals and objectives, • setting capital and operating budgets, • forecasting financial expenses, revenues and results • measuring and rewarding performance • reporting progress to senior management• conducting performance review meetings

Kaplan, Harvard Business Review, 2006

What Management control systems should cover …

Gérard Naulleau, 2006 6

• Strategic Planning

• Financial Budgeting

• Performance Review/Analysis

• Reporting

Management Control Support Key Processes

Gérard Naulleau, 2006 7

Resources OperationalProcess

Outcome

Measurement

Feedback Analysis

References : Objectives

Past performances Comparable performances

Objectives

Influence on resources allocation

Influence onprocess

Influence on planning

2

3

1

4

The management control loop

Gérard Naulleau, 2006 8

1880/1920Division Profitability Divisional

Costing and Ratios

Divisional Costing and Ratios

Decentralization Profit Centres andDirect Costing

Profit Centres andDirect Costing

Resource Allocation Process

Planning and budgeting

Planning and budgeting

1930/1940

1950/1975

Phase 1 : The Foundations

Gérard Naulleau, 2006 9

1980 …Total Quality Management

Business Process Reengineering

Key Performance Indicators

Key Performance Indicators

Balanced Scorecard

Activity Based Costing / EVA

Activity Based Costing / EVA 1995 …

2000 / Strategic Control

Phase 2 : The “Add-ons”

Gérard Naulleau, 2006 10

1) A relevant Management Control Information System

2) Clear Areas of Accountability : “Profit Centers / Cost Centers / Processes ”

3) Well understood / accepted “Planning, Budgeting and Reporting Procedures”

Management Control : What it needs to be effective

3 Requirements

Gérard Naulleau, 2006 11

(1) The fundamentals of a

Management Control Information Systems

1) Profitability Calculations2) Key Performance Indicators

3) Quarterly and Monthly Reports and Scorecards including Planned / Actual Comparisons

Gérard Naulleau, 2006 12

• SALES

• EBITDA : Earnings Before Interests Tax Depreciation and Amortisation (+- French EBE)

• EBIT : Earnings Before Interests Tax (+- French RBE)

• Operating Margin (EBIT/Sales)

• NOPAT : Net Operating Profit After Tax

• Net Result

Reporting Structure of Profitability Calculation

Gérard Naulleau, 2006 13

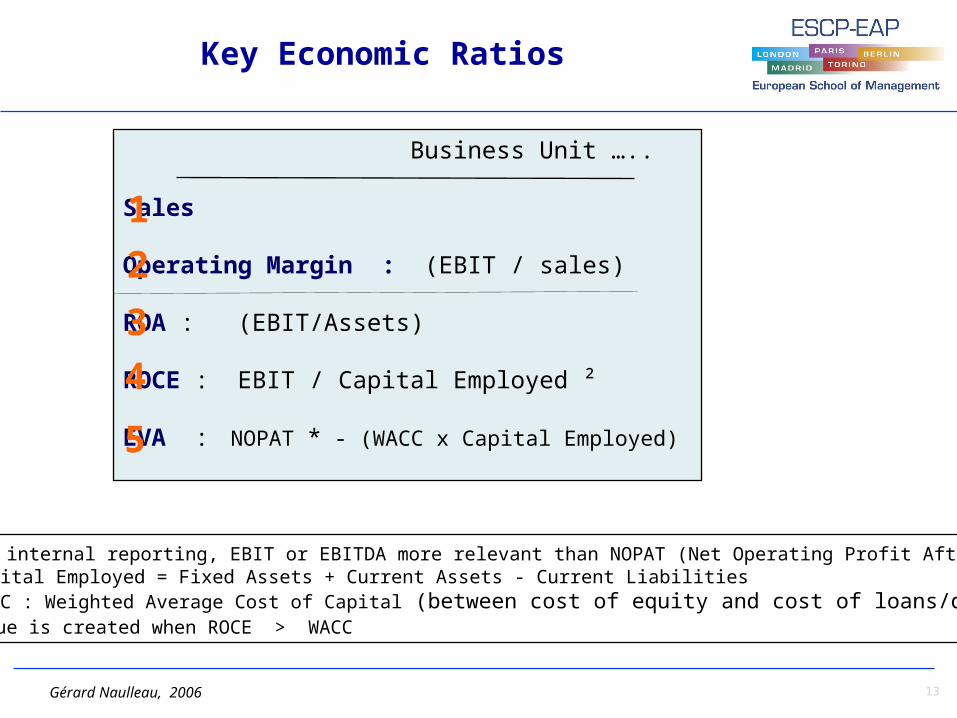

Business Unit …..

Sales

Operating Margin : (EBIT / sales)

ROA : (EBIT/Assets)

ROCE : EBIT / Capital Employed ²

EVA : NOPAT * - (WACC x Capital Employed)

• * For internal reporting, EBIT or EBITDA more relevant than NOPAT (Net Operating Profit After Tax) • ² Capital Employed = Fixed Assets + Current Assets - Current Liabilities • WACC : Weighted Average Cost of Capital (between cost of equity and cost of loans/debt)• Value is created when ROCE > WACC

3

4

5

Key Economic Ratios

2

1

Gérard Naulleau, 2006 14

Key Performance Indicators

• Customer Satisfaction• Churn Rate

• Revenue per Mile per Seat • Average Capacity Utilization Rate

• Quality Indicators (number of incidents …) • Productivity per employee • Revenue / Cost per Unit Sold• Time to Market• Employee Absenteeism• Employee Turnover• Social Climate

Gérard Naulleau, 2006 15

Reporting Additional Information

Typical BU indicators required for corporate reporting

• Period Key Points (faits marquants)• Orders• Sales • Work Load • Inventories • Activity (Production, R & D, Investments) • Headcounts

• Finance (cash position, working capital) • Working Capital • Free Cash Flow (Cash flow – (Capex + increase in WC)) • Currency Position

Gérard Naulleau, 2006 16

An integrative framework to support Management Control

Information : The Balanced Scorecard

Gérard Naulleau, 2006 17

Objectives Measures Targets Results

Balanced Scorecard model

• Green : on target

• Yellow : below target but better than last period

• Red : below target and worst or not better than last period

Strategic Focused Metrics

Gérard Naulleau, 2006 18

The challenge of Management Information : Seven functions attached to Management Control Information !

Look aheadand prepare

Look backand understand

Cascade down goals and targets

Compare and Learn

Motivate and Align Compensate

Source : M W Meyer Rethinking Performance Measurement, Cambridge University Press, 2002

Roll up initiatives and action plans

Gérard Naulleau, 2006 19

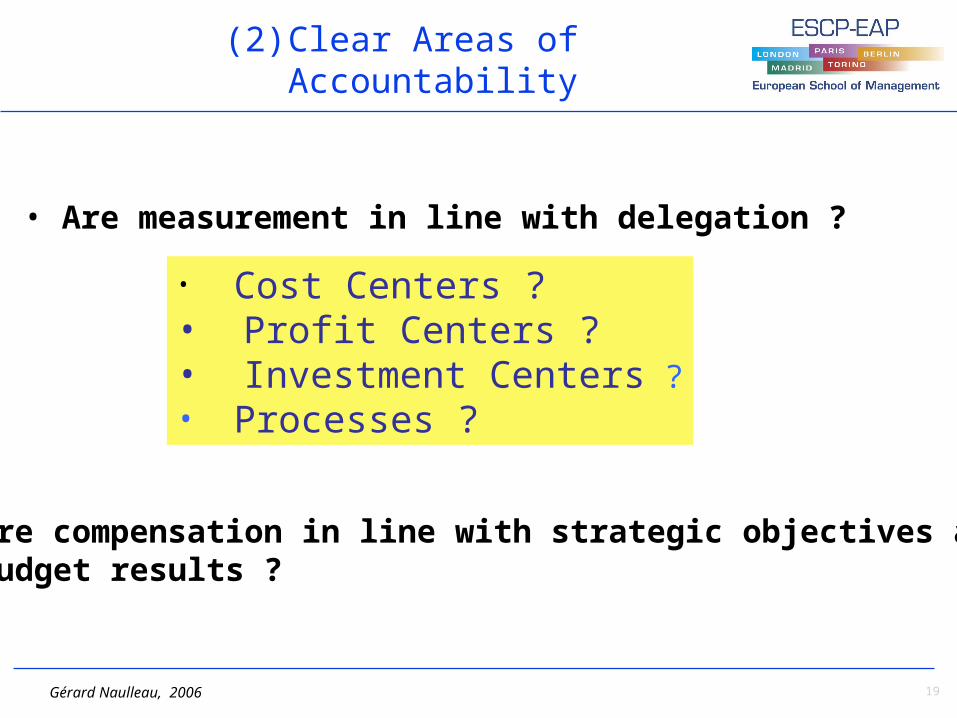

(2) Clear Areas of Accountability

• Are measurement in line with delegation ?

• Cost Centers ? • Profit Centers ? • Investment Centers ?• Processes ?

• Are compensation in line with strategic objectives and budget results ?

Gérard Naulleau, 2006 20

Cost Centers

• Accountability on Costs :

either in VALUE (Expenses Budgeted) or linked to VOLUMES (Cost per Unit)

Where

• Support Centers (Back Office / Logistics …)• Structure Centers (Administration, Public Relations …)

Gérard Naulleau, 2006 21

Profit Centers

• Accountability on Margins : ROS (Return on Sales)

Delegation on COSTS (Volume of Inputs/Resources) Delegation on REVENUES (Volume and possibly Price)

Where

• Business unit

• Regional Sales / Retail unit• Manufacturing or servicing unit selling at transfer prices (market or price less based)

Gérard Naulleau, 2006 22

Investment Centers

• Accountability on ROA and or ROCE

• Delegation on COSTS • Delegation on REVENUES• Delegation on INVESTMENTS (Assets)

Where • Business Units

Gérard Naulleau, 2006 23

Processes

• Accountability on Costs + KPI or ROS + KPI

• Delegation on COSTS • Delegation on REVENUES• Delegation on Operational Performance Criteria (KPI)

Where

• Companies organized with Processes/Programs • Examples : Procurement, Customer Support, Product Development

Gérard Naulleau, 2006 24

Accounting methods for transfer price calculation

Actual costsActual costs

Cost plus (cost + margin)Cost plus (cost + margin)

Standard costsStandard costs

Price less (Market price - discount) Price less (Market price - discount)

Market priceMarket price

COST

PRICE

Gérard Naulleau, 2006 25

APPLIX

Case Study

![sous la direction de Gérard Nicolini et Nadine Dieudonné ...artefacts.mom.fr/Publis/Tassinari_1998_[De_l_objet_a_l_atelier]].pdf · sous la direction de Gérard Nicolini et Nadine](https://static.fdocuments.us/doc/165x107/5e8d60a16026b957c65bb465/sous-la-direction-de-grard-nicolini-et-nadine-dieudonn-delobjetalatelierpdf.jpg)