Genworth 2015 investor day final2

52

1 Genworth MI Canada Inc. 2015 Investor Day December 7 th , 2015 2015 INVESTOR DAY Proven Business Model

-

Upload

genworthfinancial -

Category

Investor Relations

-

view

954 -

download

0

Transcript of Genworth 2015 investor day final2

1Genworth MI Canada Inc.2015 Investor Day

December 7th, 2015

2015 INVESTOR DAY

Proven Business Model

2Genworth MI Canada Inc.2015 Investor Day

Forward-looking and non-IFRS statements

DRIVING VALUE THROUGH CUSTOMIZED SERVICE EXPERIENCE

Public communications, including oral or written communications such as this document, relating to Genworth MI Canada Inc. (the“Company”, “Genworth Canada” or “MIC”) often contain certain forward-looking statements. These forward-looking statementsinclude, but are not limited to, statements with respect to the Company’s future operating and financial results, expectationsregarding premiums written, losses on claims and investment income, the Canadian housing market, and other statements that arenot historical facts. These forward-looking statements may be identified by their use of words such as “may”, “would”, “could”, “will,”“intend”, “plan”, “anticipate”, “believe”, “seek”, “propose”, “estimate”, “expect”, and similar expressions. These statements are basedon the Company’s current assumptions, including assumptions regarding economic, global, political, business, competitive, marketand regulatory matters. These forward-looking statements are inherently subject to significant risks, uncertainties and changes incircumstances, many of which are beyond the control of the Company. The Company’s actual results may differ materially fromthose expressed or implied by such forward-looking statements, including as a result of changes in the facts underlying theCompany’s assumptions, and the other risks described in the Company’s Annual Information Form dated March 23, 2015, its ShortForm Base Shelf Prospectus dated June 18, 2014, the Prospectus Supplements thereto, its most recently issued Management’sDiscussion and Analysis and all documents incorporated by reference in such documents. Management’s current views regardingthe Company’s financial outlook are stated as of the date hereof and may not be appropriate for other purposes. Other than asrequired by applicable laws, the Company undertakes no obligation to publicly update or revise any forward-looking statement,whether as a result of new information, future developments or otherwise.

To supplement its financial statements, the Company uses select non-IFRS financial measures. Non-IFRS financial measuresinclude net operating income, interest and dividend income (net of investment expenses), operating earnings per common share(basic), operating earnings per common share (diluted), shareholders’ equity excluding accumulated other comprehensive income(“AOCI”), operating return on equity and underwriting ratios such as loss ratio, expense ratio and combined ratio. The Companybelieves that these non-IFRS financial measures provide meaningful supplemental information regarding its performance and maybe useful to investors because they allow for greater transparency with respect to key metrics used by management in its financialand operational decision making. Non-IFRS measures do not have standardized meanings and are unlikely to be comparable to anysimilar measures presented by other companies. These measures are defined in the Company’s glossary, which is posted on theCompany’s website at http://investor.genworthmicanada.ca. A reconciliation from non-IFRS financial measures to the most readilycomparable measures calculated in accordance with IFRS, where applicable can be found in the Company’s most recentmanagement’s discussion and analysis, which is posted on the Company’s website and is also available at www.sedar.com.

3Genworth MI Canada Inc.2015 Investor Day

Stuart LevingsPresident and CEO

Strategic Overview

4Genworth MI Canada Inc.2015 Investor Day

Agenda and key themes

Strategic overview

Prudent risk management

Delivering a superior customer experience

Financial management and results

Question and answer session

Proven business model

5Genworth MI Canada Inc.2015 Investor Day

~$3 billion Market capitalization

92 million Shares outstanding

$6.1 billion Total assets

$3.4 billion Shareholders’ equity

Genworth Canada overview

WHO WE ARE

LARGEST private residential mortgage insurer in Canada

Helped ~1M+ families achieve homeownership

Supported 250+ Canadian lenders

WHAT WE DO1

1 2

4 3

Mortgage ApplicationMortgage Insurance Application and Premium

Mortgage Loan Insurance Contract

MARKET FACTS (Sept. 30th, 2015)

• Mandatory for less than 20% down payment

• Covers 100% of loan, secured by property

• Upfront non-refundable premium

• Lender receives protection against loss from mortgage default

• Capital relief for lenders

Homebuyer Mortgage lender(originates mortgage)

Mortgage insurer

Note: Company sources

1. Denotes transactional mortgage insurance.

6Genworth MI Canada Inc.2015 Investor Day

Key accomplishments

DRIVING VALUE THROUGH CUSTOMIZED SERVICE EXPERIENCE

Strong but prudent top line growth

High quality and diversified insurance portfolio1

2015 loss ratiotrending towards lower end

Cumulative 25% recent price increases translate into earnings tailwinds

Strong ROE and EPS / BVPS growth

~34%

Current market share

25%

CREDITSCORE

742

20% to 30% range

Note: Company sources

1. Credit score references the Q3 2015 YTD timeframe.

7Genworth MI Canada Inc.2015 Investor Day

Win-win solutions for borrowers experiencing temporary difficulties

Well-established risk culture supported by advanced risk / underwriting tools

Proven business model

Sound product design

Advanced risk management

Supportive regulatory environment

Proactive loss mitigation

Effective collaboration between mortgage insurance industry and prudential regulators

Mandatory, single up-front premium, prime mortgage product design

8Genworth MI Canada Inc.2015 Investor Day

Key strengths

How we measure success

Market share

High quality, diversified portfolio

EPS and BVPS growth

Strong employee engagement

Strong market presence

Focus on customer experience & operational excellence

Best-in-class technology & processes

Experienced and engaged workforce

IMPRESSIVE LONG-TERM TRACK RECORD

Prudent risk management

20+ years of performance data

9Genworth MI Canada Inc.2015 Investor Day

Served market: first time homebuyers

Purchase price <300K >300K - <=500K >500K

NATIONALVANCOUVERTORONTOCALGARY

…and what our prudent home buyers purchase

What our prudent home buyer profile looks like…

53%

31%

11%5%

<= 100K >100K - 150K >150K - 200K > 200K

53%

28%

13%

5%

<= 35 >35 - <= 45 >45 - <= 55 > 55

Detached Condo Row

69% 13% 12% 47% 17% 19% 52% 25% 21% 72% 10% 10%

3% immigrated to Canada1

67% bought with spouse/partner1

742 average credit score2

Average household

income = $97K

Average borrower age

= 36 years

Avg. price3

$428,000Avg. price3

$322,000Avg. price3

$455,000Avg. price3

$421,000

Note: Company sources.1. Nov14-Oct15 timeframe; Purchase Business only. 2. Credit score references the Q3 2015 YTD timeframe3. Average price represents Greater Calgary Area, Greater Toronto Area and Greater Vancouver Area, ex. re-financings.

10Genworth MI Canada Inc.2015 Investor Day

• Spotlight on mortgage industry

• Potential mortgage rule changes

• MIC is uniquely positioned to consult with key stakeholders

Regulatory changes

• Flat mortgage originations

• Pipeline of qualifiedfirst-time homebuyers

• Focus on quality within the lending industry

Market dynamics

• Private sector share increasing

• Competing primarily on service differentiation

• Adding value beyond the mortgage insurance transaction

Competitive environment

• Housing market and economic growth

• Consumer indebtedness and affordability pressures

• Low interest rates

Economic environment

Key themes facing the business today

11Genworth MI Canada Inc.2015 Investor Day

Our top strategic priorities

BUILDING ON SOLID BUSINESS FUNDAMENTALS

1

Prudent market share expansion

4

Strategic expansion; evaluating ancillary opportunities to enhance core mortgage insurance business

3

Proactive loss mitigation programs

(e.g. Homeowner Assistance Program)

2

Navigating 2016 with a keen focus on risk management

12Genworth MI Canada Inc.2015 Investor Day

Craig Sweeney Chief Risk Officer

Prudent Risk Management

13Genworth MI Canada Inc.2015 Investor Day

Risk categories

Strategic planning process & risk appetite

Strategic Operational Legal & Compliance Credit Market InsuranceModel

Strong enterprise risk management

EMERGING RISKS ARE IDENTIFIED, MANAGED & INCORPORATED INTO THE RISK MANAGEMENT PROCESS

Risk management processes & tools

Identification, assessment, measurement, management & controls

Risk monitoring & reporting

Governance framework

Oversight, culture, tone

14Genworth MI Canada Inc.2015 Investor Day

• Portfolio analytics

• Identification of emerging loss trends

• Dynamic underwriting policies

Portfolio Risk management

• Underwriting fundamentals

• Risk limits and triggers

• Robust quality assurance

Manage the quality of new business

Insurance risk framework

RISK PILLARS

• Macro-economic environment

• Housing market trends

• Regional risk factors

Identify & assesskey performance risks

15Genworth MI Canada Inc.2015 Investor Day

Key delinquency drivers

STRONG CORRELATION BETWEEN UE RATE AND MORTGAGE ARREARS RATE

Mortgage arrears and unemployment rate Mortgage arrears and mortgage rate

Sources: Statistics Canada, CBA

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

200

2

200

4

200

5

200

6

200

7

200

9

201

0

201

1

201

2

201

4

201

5

Mortgage Arrears UE Rate (R)

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

Mortgage Arrears 5 Yr Mtg. Rate

Strong correlation Modest correlation

16Genworth MI Canada Inc.2015 Investor Day

Government policy actions

GOVERNMENT POLICY ACTIONS REDUCE RISK ... QUALITY OF NEW BUSINESS IMPROVES

‘07 Today

Maximum amortization(insured mortgages)

40 years 25 years

LTV1 limit for newmortgages

100% 95%

LTV limit for mortgagerefinancing

95% 80%

LTV limit for investmentproperties

90% 80%

Debt-service criteria for> 80% LTV

No mandated

max

GDS2 capped at 39% &

TDS2 ratio at 44%

Purchase price for> 80% LTV

No max $1 mil.

‘07 / ‘08 ‘14 / ’15 YTD

% > 25 yearamortizations

61%

0%3

% > 95% LTV 14%

% of > 80% LTV refinance mortgages

23%

% of > 80% LTV for investment properties

1%

Average GDS 23% 24%

Average credit score 717 739

Improved credit quality

Note: Company sources

1. Loan-to-value.

2. GDS represents gross debt service ratio, and TDS represents total debt service ratio.

3. % of new originations > 25 year amortizations and over 80% LTV.

17Genworth MI Canada Inc.2015 Investor Day

Limiting stacked risk factors

UNDERWRITING DISCIPLINE LIMITS EXPOSURE TO VULNERABLE BORROWERS

71%

23%

4%1%1%

>90-95 >85-90 >80-85 >75-80 <=75

95 LTV – credit score

6%6%

10%

29%33%

17%

<=660 <=680 <=700 <=740 <=780 780+

28%

35%

21%

17%

>40 >35-40 >30-35 <=30%

95 LTV – TDSR

Stacked risks (% of NIW)

Halifax Montreal Ottawa Toronto Calgary Vancouver National

0.8% 0.8% 1.2% 0.7% 0.9% 0.8% 1.0%

LTV mix - transactional

Note: Company sources.

Based on July ‘14 to June ‘15 New Insurance Written (NIW), purchase only deal, excludes Alt-A.

Stacked Risk = >90% LTV and <= 660 score and >40 total debt service ratio (TDSR).

18Genworth MI Canada Inc.2015 Investor Day

Strong portfolio quality & mix

73% 74% 75% 79% 82%

18% 18% 17%15% 13%

9% 8% 8% 6% 5%

2011 2012 2013 2014 15YTD

>=700 660 - 669 <660

20%

4%

44%

14%

5%

13%

Alberta Atlantic Ontario B.C. Prairies Quebec

2. Based on Company’s estimate.1. % based on transactional new insurance written for 3Q’15 year to date.

Credit score dispersion1 Regional dispersion2 (as at June 30, 2015)

Note: Company sources.

Outstanding balance of insured mortgages as at June 30, 2015 of

$178B

19Genworth MI Canada Inc.2015 Investor Day

1,1771,415

1,2321,047

735 619 517 395 365

108

240387

492

480

342295

268 200

165

484862 1,048

722

437

284

222258

413

561

645 552

554

515

482569 578

183

240

255 262

261

240

252302 314

2007 2008 2009 2010 2011 2012 2013 2014 3Q15

Ontario BC Alberta Quebec Other

Current delinquency rate1

0.29%

0.41%

0.18%

0.25%

0.09%

Delinquency rates

Number of reported delinquencies

REFLECTS MACROECONOMIC ENVIRONMENT & IMPROVED PORTFOLIO QUALITY

Loss ratio 2 19% 31% 42% 33% 37% 33% 25% 20% 20%

3,381 3,401

2,752

2,153

1,830 1,756 1,715

2,940

2,046

Ontario

BCAlberta

Quebec

Other

~50%decline over

5 years

Note: Company sources.

1. Based on outstanding insured mortgages, as at June 30, 2015.

2. Loss ratio in 2009 excludes the impact of the change to the premium recognition curve in the first quarter of 2009.

20Genworth MI Canada Inc.2015 Investor Day

Ho

us

ing

ris

k

Economic riskLow High

High

GTA

GVA

Quebec

Alberta

Regional risk assessment

Market risk

Atlantic

Ontario

Prairies

Targeted underwriting actions Alberta & Saskatchewan

Monitoring housing risk in GTA and GVA

Balanced risk profile Quebec and Ontario

Note: Based on Company estimates.

21Genworth MI Canada Inc.2015 Investor Day

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2007 2009 2011 2013 2015100,000

200,000

300,000

400,000

500,000

600,000

700,000

2007 2009 2011 2013 2015

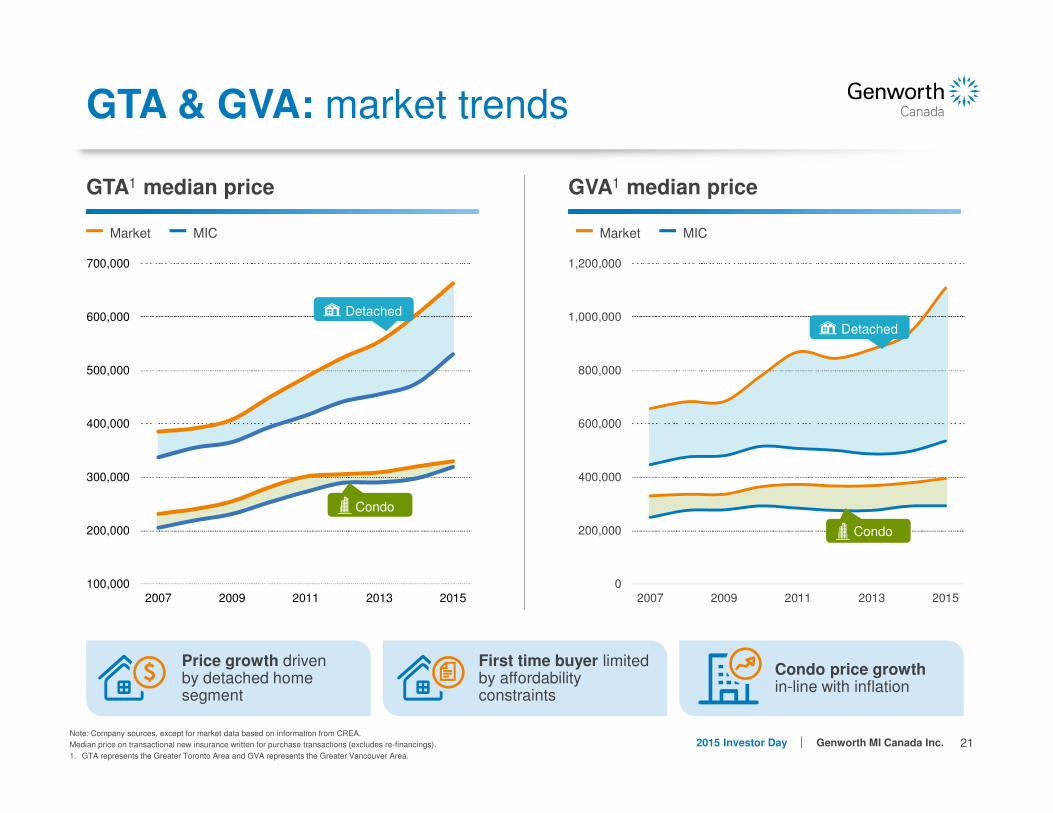

GTA & GVA: market trends

Price growth driven by detached home segment

First time buyer limited by affordability constraints

Condo price growth in-line with inflation

GTA1 median price GVA1 median price

Market MICMarket MIC

Detached

Condo

Detached

Condo

Note: Company sources, except for market data based on information from CREA.

Median price on transactional new insurance written for purchase transactions (excludes re-financings).

1. GTA represents the Greater Toronto Area and GVA represents the Greater Vancouver Area.

22Genworth MI Canada Inc.2015 Investor Day

GTA & GVA: embedded equity

*Estimated outstanding balance of insured mortgages as at June 30, 2015.

Note: GTA represents the Greater Toronto Area and GVA represents the Greater Vancouver Area.

4440

5964

7175

8388

43

51

6772

75 76

84

90

0

20

40

60

80

100

Portfolio <=2009 2010 2011 2012 2013 2014 2015

Effective loan-to-value by book year

GVA

GTA

Original NIW ($B) 65.2 69.4 6.9 6.3 5.2 4.5 4.9 2.5

Remaining NIW ($B)* 27 6.8 2.9 3.7 3.7 3.7 4.5 2.5

STRONG RUN-OFF AND EMBEDDED EQUITY IN OLDER BOOKS REDUCING RISK

23Genworth MI Canada Inc.2015 Investor Day

13%

4%719

747

2007 2008 2009 2010 2011 2012 2013 2014 15YTD

% of <660 credit score Average credit score

GVA portfolio quality

GTA & GVA: lower risk profile

STEADY CREDIT SCORE IMPROVEMENT & DECLINING EXPOSURE TO HIGHER RISK LOANS SINCE 2007

16%

3%

714

747

2007 2008 2009 2010 2011 2012 2013 2014 15YTD

% of <660 credit score Average credit score

GTA portfolio quality

Note: Company sources for transactional new insurance written.

Note: GTA represents the Greater Toronto Area and GVA represents the Greater Vancouver Area.

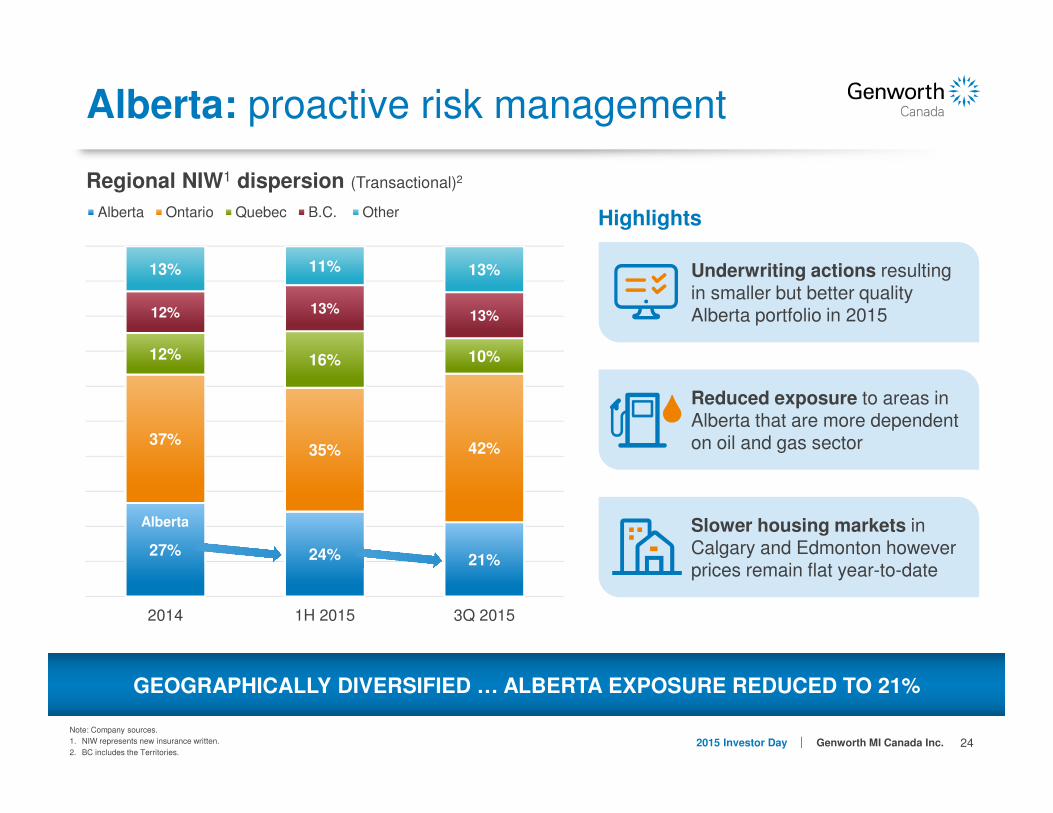

24Genworth MI Canada Inc.2015 Investor Day

Highlights

Alberta: proactive risk management

GEOGRAPHICALLY DIVERSIFIED … ALBERTA EXPOSURE REDUCED TO 21%

Underwriting actions resulting in smaller but better quality Alberta portfolio in 2015

Reduced exposure to areas in Alberta that are more dependent on oil and gas sector

Slower housing markets in Calgary and Edmonton however prices remain flat year-to-date

27% 24% 21%

37%35% 42%

12% 16% 10%

12% 13% 13%

13% 11% 13%

2014 1H 2015 3Q 2015

Alberta Ontario Quebec B.C. Other

Regional NIW1 dispersion (Transactional)2

Alberta

Note: Company sources.

1. NIW represents new insurance written.

2. BC includes the Territories.

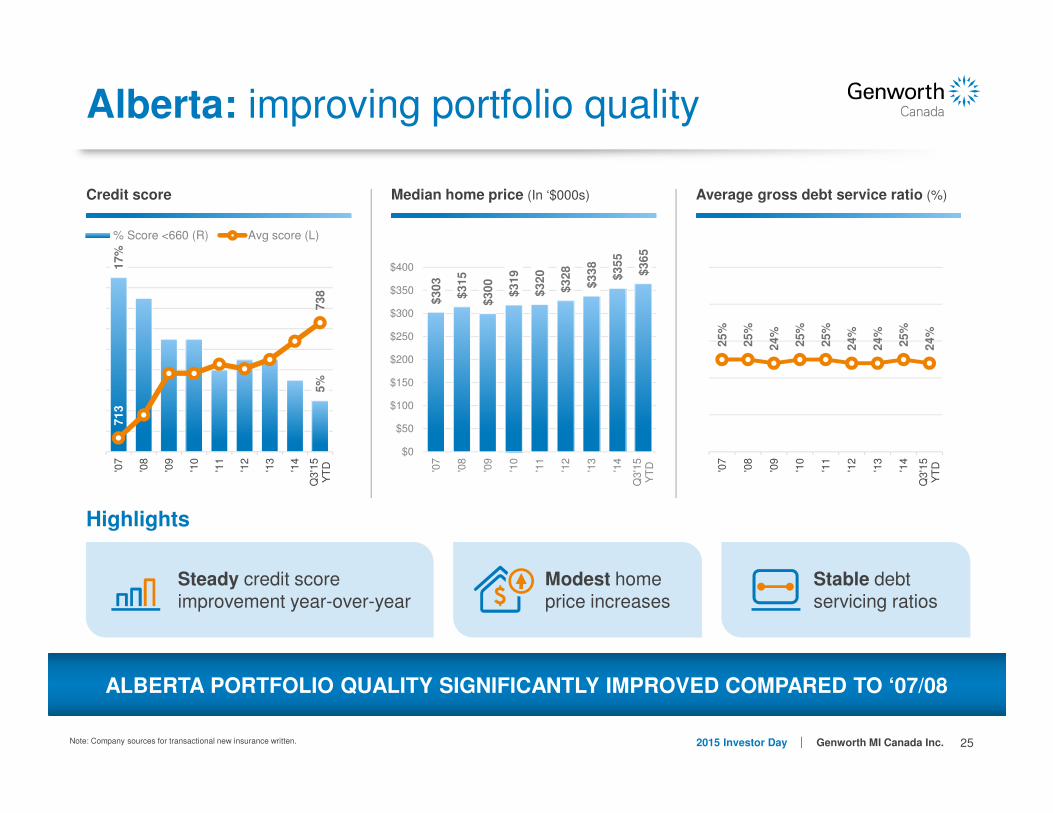

25Genworth MI Canada Inc.2015 Investor Day

Highlights

Alberta: improving portfolio quality

ALBERTA PORTFOLIO QUALITY SIGNIFICANTLY IMPROVED COMPARED TO ‘07/08

Credit score Average gross debt service ratio (%)

17

%

5%

71

3

73

8

'07

'08

'09

'10

'11

'12

'13

'14

Q3'1

5Y

TD

% Score <660 (R) Avg score (L)

25

%

25

%

24

%

25

%

25

%

24

%

24

%

25

%

24

%

'07

'08

'09

'10

'11

'12

'13

'14

Q3'1

5Y

TD

Steady credit score improvement year-over-year

Modest home price increases

Stable debt servicing ratios

Note: Company sources for transactional new insurance written.

Median home price (In ‘$000s)

$3

03

$3

15

$3

00

$3

19

$3

20

$3

28

$3

38

$3

55

$3

65

$0

$50

$100

$150

$200

$250

$300

$350

$400

'07

'08

'09

'10

'11

'12

'13

'14

Q3'1

5Y

TD

26Genworth MI Canada Inc.2015 Investor Day

2016 annual loss ratio expectations

MIC loss ratio & CBA1 delinquency rates2

PRELIMINARY 2016 ANNUAL LOSS RATIO RANGE: MID-20% TO MID-TO-HIGH 30%

1 Source: Canadian Bankers Association (CBA) and Company sources. 2 2009 excludes the impact of the change to the premium recognition curve in 1Q’09* CBA delinquency rates as of Q2 2015.

• Canada delinquency rate

should benefit from stronger

economy in ‘16

• Higher quality MIC portfolio

since 2009

• Impact of lower oil prices

should be less severe on

MIC’s loss ratio this cycle

2016 Loss Ratio Range

Alberta delq. rate (CBA) (LS)

Canada delq. rate (CBA) (LS)

0%

10%

20%

30%

40%

50%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

2006 2007 2008 2009 2010 2011 2012 2013 2014 Q3'15YTD*

Canada loss ratio - MIC (RS) Alberta DR-CBA

27Genworth MI Canada Inc.2015 Investor Day

Key takeaways

Prudent risk management

Underwriting actions reducing risk

Well positioned to address regional economic pressures

2016 annual loss ratio range: mid-20% to mid-to-high 30%

Strong portfolio quality

28Genworth MI Canada Inc.2015 Investor Day

Scott GormanSVP, Operations

Delivering a Superior Customer Experience

Debbie McPhersonSVP, Sales & Marketing

29Genworth MI Canada Inc.2015 Investor Day

Customer centric culture

FOCUSED ON DRIVING VALUE THROUGH A SUPERIOR CUSTOMER EXPERIENCE

30Genworth MI Canada Inc.2015 Investor Day

Key takeaways

Competitive differentiation

driven by innovative customer

experience strategy

Risk appetite integrated into our sales and underwriting strategies

Proactive loss mitigation programs provide benefit to lenders, homeowners and MIC

Delivering added value through an integrated and cross-functional approach to customer service

Market share gains achieved through relationships, collaboration and transparency

31Genworth MI Canada Inc.2015 Investor Day

Philip MayersSVP and Chief Financial Officer

Financial Management and Results

32Genworth MI Canada Inc.2015 Investor Day

Proven business model…

Superior customer experience and value added relationships have produced market share gains

Demonstrated results

Prudent risk management driving improved portfolio quality and strong loss performance

Proactive loss mitigation keeps borrowers in their homes and reduces our loss exposure

Loss ratio

Market share (Transactional)1

25% 20% 20%

2013 2014 YTD 2015

28% 34%

Q1 2014 Q3 2015

56% 57%

2014 YTD 2015

Workout penetration rate2

Note: Company sources.

1. Market share based on management estimates.

2. Workout penetration means the ratio (expressed as a percentage) of the number of total workouts approved, including shortfall sales, divided by the number of new delinquencies and re-delinquencies over the same period. Workout penetration ratio measures the number of workouts performed relative to the number of existing workout opportunities and is used to assess the success of the loss mitigation homeowner’s assistance program.

33Genworth MI Canada Inc.2015 Investor Day

Strong earnings profile

114 11184 84

235 255

199 196

349366

283 280

2013 2014 Q3 YTD 2014 Q3 YTD 2015

Note: Company sources.

1. Net Operating Income, Operating EPS (diluted) and Operating ROE are non-IFRS measures. See “Forward looking and non-IFRS statements” at the beginning of the presentation.

2. Pro-forma for 2015 MCT Guideline.

SOLID PROFITABILITY AND FINANCIAL PROFILE

Operating EPS (diluted)1 $ 3.60 $ 3.86 $ 2.96 $ 3.02

BVPS (diluted, incl. AOCI) $ 32.53 $ 35.02 $ 34.57 $ 36.14

Operating ROE1 12% 12% 12% 12%

MCT Ratio 223% 228%2 224% 228%

Long-term debt: Total capital 12% 12% 12% 11%

Investment income net of interest expense

(after taxes)

Underwriting profit (after taxes)

Net operating income1

34Genworth MI Canada Inc.2015 Investor Day

Transactional insurance

$20

$22

$16

$19

2013 2014 Q3 YTD2014

Q3 YTD2015

+$2.6B

+$3.1B

STRONG YoY GROWTH REFLECTS SOLID BUSINESS FUNDAMENTALS

~5-points of market share gains over the past 18 months

Modestly largerorigination market

Two rounds of price increases totaling 25%

$447

$512

$368

$466

$43

$22

$57

2013 2014 Q3 YTD2014

Q3 YTD2015

$555

Average premium rate

2.29% 2.51% 2.45% 2.75%

New insurance written ($ billions)

+$133M$523

$390

Net premiums written ($ millions)

+$108M

YoY impact of price increases

Note: Company sources.

35Genworth MI Canada Inc.2015 Investor Day

Portfolio insurance

$15

$20

$17$16

2013 2014 Q3 YTD2014

Q3 YTD2015

+$4.6B

-$1.3B

$65

$83

$70 $71

2013 2014 Q3 YTD2014

Q3 YTD2015

+$18M+$1M

New insurance written ($ billions) Net premiums written ($ millions)

PROPOSED REGULATORY CHANGE IN 2016 MAY LIMIT VOLUMES…PORTFOLIO INSURED MORTGAGES WOULD BE REQUIRED TO BE SECURITIZED IN GOV’T MBS PROGRAMS

Note: Company sources.

Strong portfolio insurance volumes in recent years have enhanced lender relationships

36Genworth MI Canada Inc.2015 Investor Day

Premiums earned growth

LARGER RECENT BOOKS PROVIDE TAILWIND FOR PREMIUMS EARNED

COMBINATION OF HIGHER INSURED VOLUMES AND PRICE INCREASESEXPECTED TO DRIVE 5%+ GROWTH IN PREMIUMS EARNED IN 2016 AND BEYOND

$272 $234 $254

$1,095 $1,086 $1,127

$370 $443$578

Q3 2013 Q3 2014 Q3 2015

6 years & prior Previous 4 books Most recent

+20% +30%

-1% +4%

-14% +9%$144 $141 $143

$143 $141 $144

$143 $140 $148

$142 $143

2013 2014 2015

Q1 Q2 Q3 Q4

-2%Q3 YTD

+3%Q3 YTD

Q3 YTD

$431 $422 $435

Unearned premiums reserve ($ millions) Premiums earned ($ millions)

FY $573 FY $565$1.7B $1.8B

$2.0B

Note: Company sources.

37Genworth MI Canada Inc.2015 Investor Day

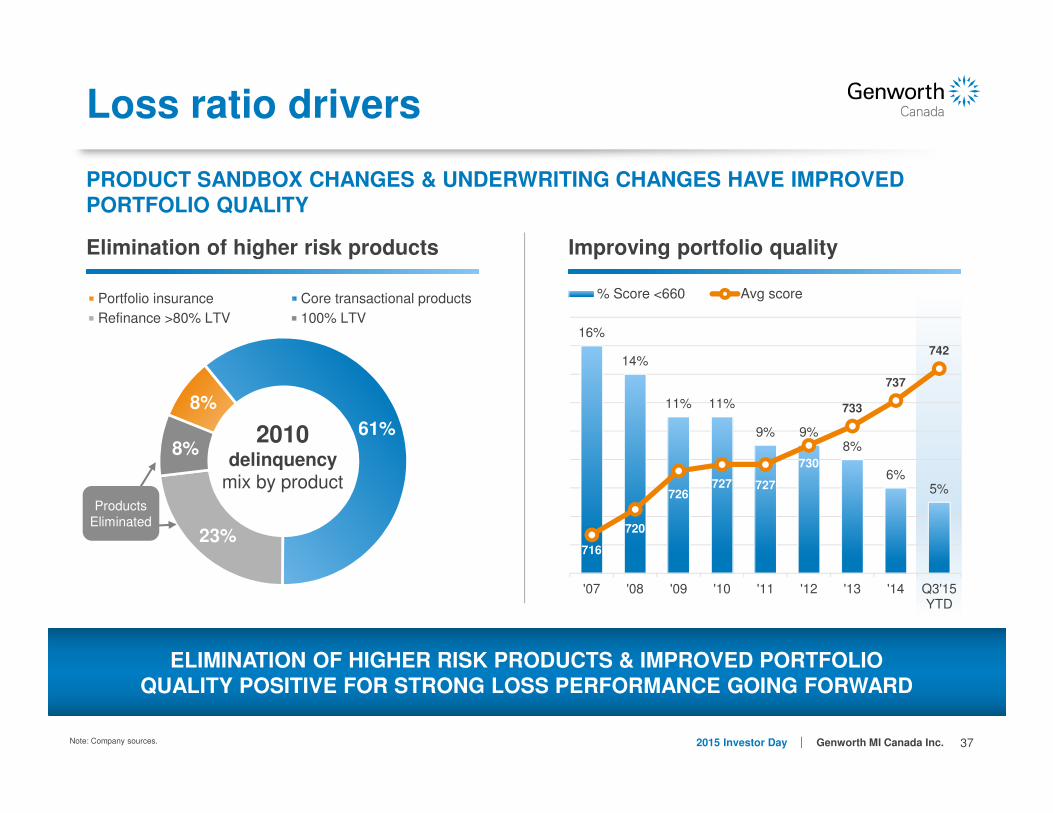

Loss ratio drivers

PRODUCT SANDBOX CHANGES & UNDERWRITING CHANGES HAVE IMPROVED PORTFOLIO QUALITY

ELIMINATION OF HIGHER RISK PRODUCTS & IMPROVED PORTFOLIOQUALITY POSITIVE FOR STRONG LOSS PERFORMANCE GOING FORWARD

Elimination of higher risk products Improving portfolio quality

8%

61%

23%

8%

Portfolio insurance Core transactional products

Refinance >80% LTV 100% LTV

Products Eliminated

16%

14%

11% 11%

9% 9%8%

6%5%

716

720

726727 727

730

733

737

742

'07 '08 '09 '10 '11 '12 '13 '14 Q3'15YTD

% Score <660 Avg score

2010 delinquency

mix by product

Note: Company sources.

38Genworth MI Canada Inc.2015 Investor Day

Underwriting profitability

Combined ratio

STRONG UNDERWRITING PERFORMANCE DRIVING IMPROVED PROFITABILITY

42%33% 37% 33%

25% 20% 18% 20%

15%

17%17%

18%

20%19% 18% 19%

57%50%

53% 51%44%

39% 36% 39%

2009* 2010 2011 2012 2013 2014 Q3 YTD 2014 Q3 YTD 2015

Loss ratio Expense ratio

Potential impact on loss ratio

Improvedportfolio quality

Lowoil prices

• Trending towards lower end of 2015 loss ratio target range of 20% to 30%

• Targeting a mid 20% to mid-to-high 30%loss ratio range for full year 2016

Decreasing loss ratio Increasing loss ratio

Note: Company sources.

* Excludes the impact of change to the premium recognition curve in the first quarter of 2009.

2014/2015 price increases

39Genworth MI Canada Inc.2015 Investor Day

Loss performance & economic scenarios

MI PRICED TO COVER TYPICAL ECONOMIC CYCLE

Illustration:Expected over

economic cycleStress

scenario

Unemployment rate change over 5 years

1% to 2% increase 2% to 4% increase

Cumulative HPA / HPD over 5 years

5% to 7% -15% to -20%

Loss ratio (national)over 5 years

25% to 30% 60% to 70%

Note: Company estimates based upon historical data and performance trends; expected ranges are approximations.Actual results may differ materially from those expressed above.

40Genworth MI Canada Inc.2015 Investor Day

Strong balance sheet

EXPECTED EMBEDDED FUTURE PROFITS ENHANCES SHAREHOLDER VALUE

$26.94$30.62 $32.53

$35.02 $36.14 $36.14

$6.98

2011 2012 2013 2014 Q3 2015 Q3 2015*

Illustration:

Unearned premiums $ 2.0B

Future losses on claims & expenses1 (1.1)

Future pre-tax underwriting income 0.9

Future net income $ 0.6B

Incremental book value per share $ 6.98

($ millions) Sept. 30, 2015

Assets

Cash and investments $ 5,678

Other assets 411

Total assets $ 6,089

Liabilities

Loss reserves 121

Unearned premiums 1,959

Long term debt 432

Other liabilities 220

Total liabilities 2,732

Shareholders’ equity (w/AOCI)

3,357

Total liabilities and shareholders’ equity

$ 6,089

Book value per share (incl. AOCI, diluted)

$2.0B OF UNEARNED PREMIUMS REPRESENT FUTURE REVENUES & PROFITS

Note: Company sources.

1. Theoretical example - future losses on claims and expenses calculated using 55% combined ratio. *Pro-forma.

41Genworth MI Canada Inc.2015 Investor Day

HIGH QUALITY PORTFOLIO CONTRIBUTES ~35% OF NET OPERATING INCOME…PORTFOLIO GROWTH SHOULD PARTIALLY OFFSET YIELD PRESSURE

Well diversified investment portfolio

17% Federal Bonds

Government of Canada bond yields remain unattractive at low levels

17% Fed. Agency / NHA MBS

Federal Agency and NHA MBS provide incremental yield

18% Provincials

Diversified average credit rating of AA

3% Preferred Shares

Preferred shares yields are attractive

5% Emerging Markets Debt (Inv. Grade)

Selective geographic participation focused on non-resource sectors

0% High Dividend Common Shares

Higher level of regulatory capital and ongoing volatility

17%

17%

18%

36%5%

4%

3%

Represents current relative attractiveness

Note: Company sources.

1. Note: as of September 30, 2015.

36% Investment Grade Corporates

Spreads have widened significantly

$5,443$5,678

$235

4Q14 3Q15

$5.7B portfolio1

Duration: 3.8 years1

Book yield: 3.3%1

Cash

Invested assets(C$ millions)

42Genworth MI Canada Inc.2015 Investor Day

Intend to operate moderately above the 220% MCT holding target

Holding company cash and liquid securities of $120 million and leverage of 11%3

Capital management

$19,502

$22,112

$15,919

$19,012

2013 2014 Q3 YTD2014

Q3 YTD2015

Capital required at 220% MCT ($ millions)1

+$3.1B

Transactional new insurance written ($ millions)

$3,159$3,329

$3,448

$38

$116

$120

2013 Jan. 1/15 Q3 2015

Holdco cash2 $85M $143M $120M

MCT ratio 223% 228% 228%

FOCUSED ON DEPLOYING CAPITAL TO SUPPORT ORGANIC GROWTH OPPORTUNITIES

$3,197

+$2.6B

$3,445

$3,568+$248M

+$123M

Flexibility Efficiency

Strength

Note: Company sources.

1. MCT denotes ratio for operating insurance company.

2. Represents capital in addition to capital in operating insurance company.

3. As at Sept. 30, 2015.

43Genworth MI Canada Inc.2015 Investor Day

New capital framework for 2017

COMPANY DOES NOT EXPECT A MATERIAL IMPACT ON CAPITAL REQUIREMENTS

1

New regulatory

capital framework for

mortgage insurers

expected to be

implemented

Jan. 1, 2017

2

Capital framework is

being designed to be

more risk sensitive

by using more loan

level risk attributes

3

New capital framework

is not expected to

change the total dollar

amount of capital

required at holding

target (which reflects

stress testing results

for tail events)

4

Company is working

with OSFI closely and

expects more granular

details on the proposed

framework in the first

half of 2016

44Genworth MI Canada Inc.2015 Investor Day

Key takeaways

Proven business model has positioned

MIC for future financial performance

Price increases & market share gains providing tailwind for premiums written and premiums earned

Track record of solid financial performance reflects proven business model

Improved insurance portfolio quality, positive for loss performance

Strong balance sheet built on conservative investment portfolio and capital strength

45Genworth MI Canada Inc.2015 Investor Day

Stuart LevingsPresident and CEO

Wrap Up

46Genworth MI Canada Inc.2015 Investor Day

Key takeaways

Customer service leader

Deep risk expertise

Sustainable business model

Momentum and staying power

MIC is well-positioned

forfuture

success

47Genworth MI Canada Inc.2015 Investor Day

48Genworth MI Canada Inc.2015 Investor Day

Senior management team

Stuart Levings, President & CEO15+ years of mortgage insurance experience

Mr. Levings assumed his current role as President and Chief Executive Officer in January 2015. Prior to that Mr. Levings served in such senior leadership positions as Senior Vice President, Chief Operating Officer, Senior Vice President, Chief Operations Officer and Senior Vice President, Chief Risk Officer. Mr. Levings joined the Company in July 2000 as the Financial Controller, and has also held positions in finance and product development, including five years as Chief Financial Officer. Before that, Mr. Levings spent seven years with Deloitte & Touche. Mr. Levings holds a CPA, CA professional designation with over 15 years of professional experience in a variety of industry sectors. Mr. Levings holds a Bachelor of Accounting Science degree from the University of South Africa and is a member of both the South African and Canadian Institutes of Chartered Accountants.

Philip Mayers, Chief Financial Officer25+ years of mortgage insurance experience

Mr. Mayers became Chief Financial Officer of the Company in 2009. He has over 25 years of finance and general management experience in financial services businesses. Since joining the Company in 1995, Mr. Mayers has held several senior positions, including Vice President, Finance, Vice President, Operations, and Senior Vice President, Business Development. Prior to joining the Company, he held finance positions with Mortgage Insurance Company of Canada (“MICC”), Esso Petroleum Canada and Deloitte & Touche. He holds CPA, CA and CMA professional designations and has a Master of Accounting degree from the University of Waterloo.

49Genworth MI Canada Inc.2015 Investor Day

Senior management team

Craig Sweeney, Chief Risk Officer15+ years of mortgage insurance experience

Mr. Sweeney has more than 18 years of professional experience in the mortgage and banking industry. Since joining the Company in 1998, Mr. Sweeney has held senior positions in Operations and Business Development, including Director of Risk Operations and Director of Product Development. Mr. Sweeney received an honours Bachelor of Arts degree in Economics from Carleton University in 1994.

Winsor Macdonell, SVP, General Counsel & Secretary15+ years of mortgage insurance experience

Mr. Macdonell is responsible for all of the Company’s legal and compliance matters, as well as government relations. Mr. Macdonell joined the Company in 1999. He was called to the Bar in Ontario in 1994. Prior to joining the Company, he spent three years in the life and property and casualty industry, and prior to that was in private practice. Mr. Macdonell received an honours Bachelor of Commerce degree from Queens University in 1988 and his LL.B. from Dalhousie University in 1992 and his ICD.D in 2014.

50Genworth MI Canada Inc.2015 Investor Day

Senior management team

Debbie McPherson, SVP, Sales and Marketing25+ years of mortgage insurance experience

Ms. McPherson has over 25 years of experience and success in sales and quality management with the Company. Prior to her current position, Ms. McPherson was the Company’s Ontario Regional Sales Director. Ms. McPherson plays an active role in many industry organizations, including the Canadian Association of Accredited Mortgage Professionals, the Canadian Homebuilders Association and the Canadian Real Estate Association. Ms. McPherson graduated from the University of Toronto with a Bachelor of Arts degree.

Scott Gorman, SVP, Operations15+ years of experience

Mr. Gorman has more than 19 years of International Industry and Consulting experience within the Financial Services Industry. Prior to joining Genworth Canada, Mr. Gormanworked for TD Financial Group as VP, Head of Card Operations & Initiatives, and Royal Sun Alliance (RSA) as the Regional Chief Operating Officer for their Asia and Middle East Region as well as VP of RSA’s Canadian National Operations. Mr. Gorman has a Bachelor’s of Commerce from Memorial University of Newfoundland and an MBA from Schulich School of Business, York University.

51Genworth MI Canada Inc.2015 Investor Day

Senior management team

Rhonda Lawson, SVP, Human Resources and Facilities20+ years experience

Ms. Lawson joined the Company early in 2013, and brings more than 20 years of leadership experience in senior human resource management roles with global public and private corporations, including Aviva, Intact (ING Canada), Allianz and TevaPharmaceuticals. Ms. Lawson has held Director roles on a number of corporate and not-for-profit Boards since 1993, most recently as a Director and Chair of the HR Committee on the Boards of DST Engineering Group and Rouge Valley Health Systems (RVHS).

Brian Hurley, Executive Chairman20+ years of mortgage insurance experience

Mr. Hurley led the establishment of Genworth into the Canadian marketplace in 1994 and later led it through its initial public offering in 2009. He stepped down as President and CEO of Genworth Canada and assumed the role of Executive Chairman in January 2015. Mr. Hurley has more than 20 years of senior management experience in the mortgage insurance industry worldwide, including leading Genworth’s activities in key international markets from 2004 to 2009. Prior roles include Senior VP, International of General Electric’s U.S. mortgage insurance business and Senior VP of Sales and Operations. Mr. Hurley graduated from Assumption College in Worcester, Massachusetts with a Bachelor of Science degree in Economics.

52Genworth MI Canada Inc.2015 Investor Day

Investor Relations

Jonathan A. Pinto, MBA, LL.M

Vice President, Investor Relations