Thought Amidst Waste: Conjunctural Notes on the Democratic Project in South Africa

Upload

annis-jenningsCategory

view

213download

0

General Directorate of Annual Programs and Conjunctural Evaluations

1

15 February 2010

Turkish Economy: Macroeconomic Developments in

2009 and Medium Term Programme (2010-

2012)

Ahmet Sabri EROGLU, Ph.D.State Planning Organization

ECO – 20th Meeting of Regional Planning Council

Antalya, Turkey

General Directorate of Annual Programs and Conjunctural Evaluations

2

OUTLINE:•World Economy•Turkish Economy•Measures Against Crisis•Medium Term Program

General Directorate of Annual Programs and Conjunctural Evaluations

3

WORLD ECONOMYin 2009 and 2010

General Directorate of Annual Programs and Conjunctural Evaluations

4

2.9

3.6

4.94.5

5.1 5.2

3.9

-0.8

3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2002 2003 2004 2005 2006 2007 2008 2009 (*) 2010 (*)

Source: IMF, World Economic Outlook, January 2010.

(*) Estimate.

World Output (Annual % Change)

General Directorate of Annual Programs and Conjunctural Evaluations

5

-0.8

-2.5

-3.9

6.5

3.9

2.7

1.0

8.4

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

World USA Euro Area Developing Asia

2009 2010

Source: IMF, World Economic Outlook, January 2010.

Estimations for Output Growth (%)

General Directorate of Annual Programs and Conjunctural Evaluations

6

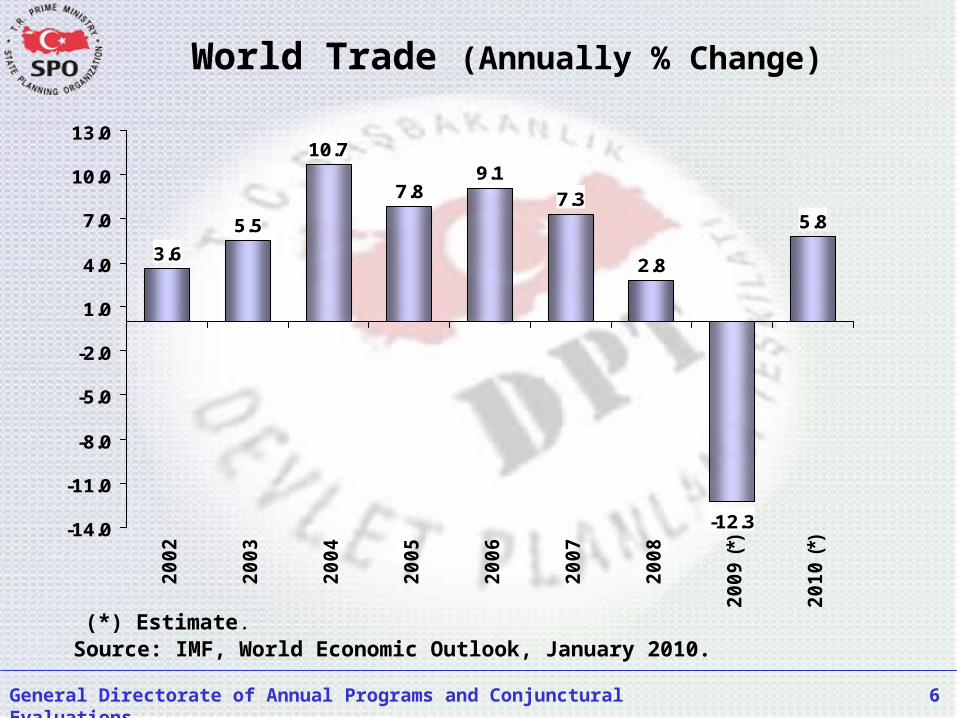

3.6

5.5

10.7

7.89.1

7.3

2.8

5.8

-12.3-14.0

-11.0

-8.0

-5.0

-2.0

1.0

4.0

7.0

10.0

13.0

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

(*)

20

10

(*)

(*) Estimate. Source: IMF, World Economic Outlook, January 2010.

World Trade (Annually % Change)

General Directorate of Annual Programs and Conjunctural Evaluations

7

Global Crisis Affected Turkish Economy in Three Channels:

Foreign Trade,

Foreign Financing,

Expectations.

The Effects of Global Crisis on the

Turkish Economy

General Directorate of Annual Programs and Conjunctural Evaluations

8

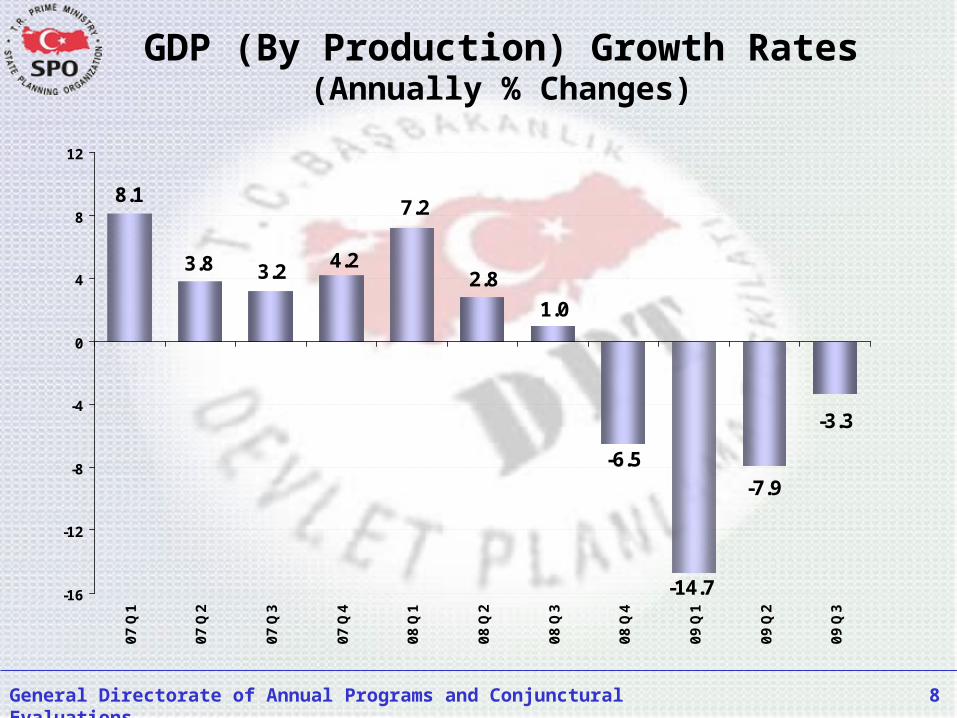

8.1

3.8 3.2 4.2

7.2

2.8

1.0

-6.5

-14.7

-7.9

-3.3

-16

-12

-8

-4

0

4

8

12

07

Q1

07

Q2

07

Q3

07

Q4

08

Q1

08

Q2

08

Q3

08

Q4

09

Q1

09

Q2

09

Q3

GDP (By Production) Growth Rates(Annually % Changes)

General Directorate of Annual Programs and Conjunctural Evaluations

9

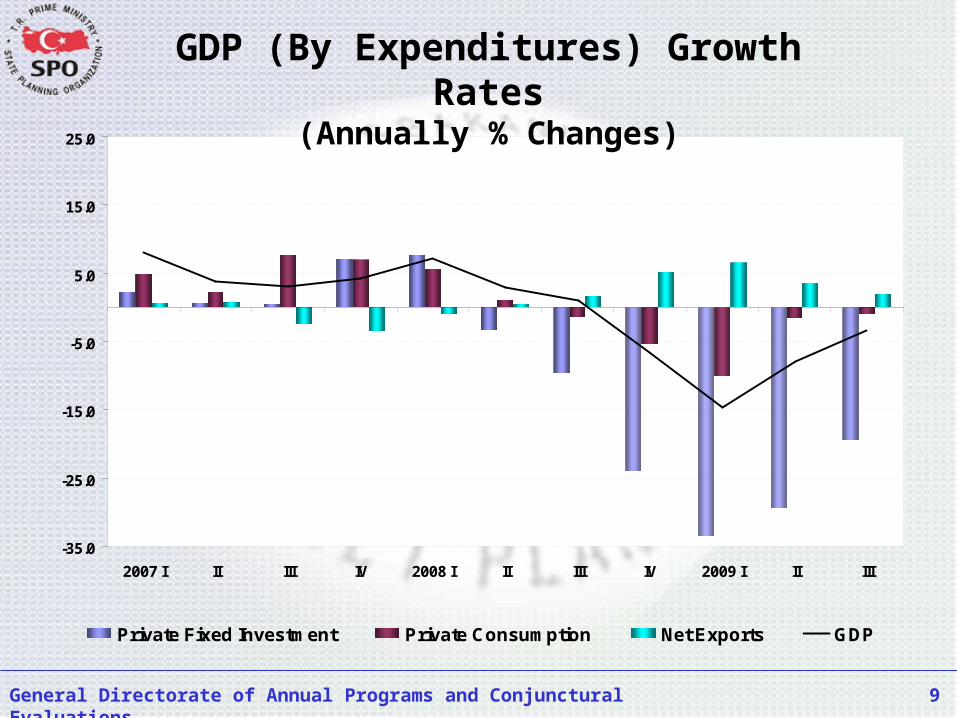

-35.0

-25.0

-15.0

-5.0

5.0

15.0

25.0

2007 I II III IV 2008 I II III IV 2009 I II III

Private Fixed Investment Private Consumption Net Exports GDP

GDP (By Expenditures) Growth Rates

(Annually % Changes)

General Directorate of Annual Programs and Conjunctural Evaluations

10

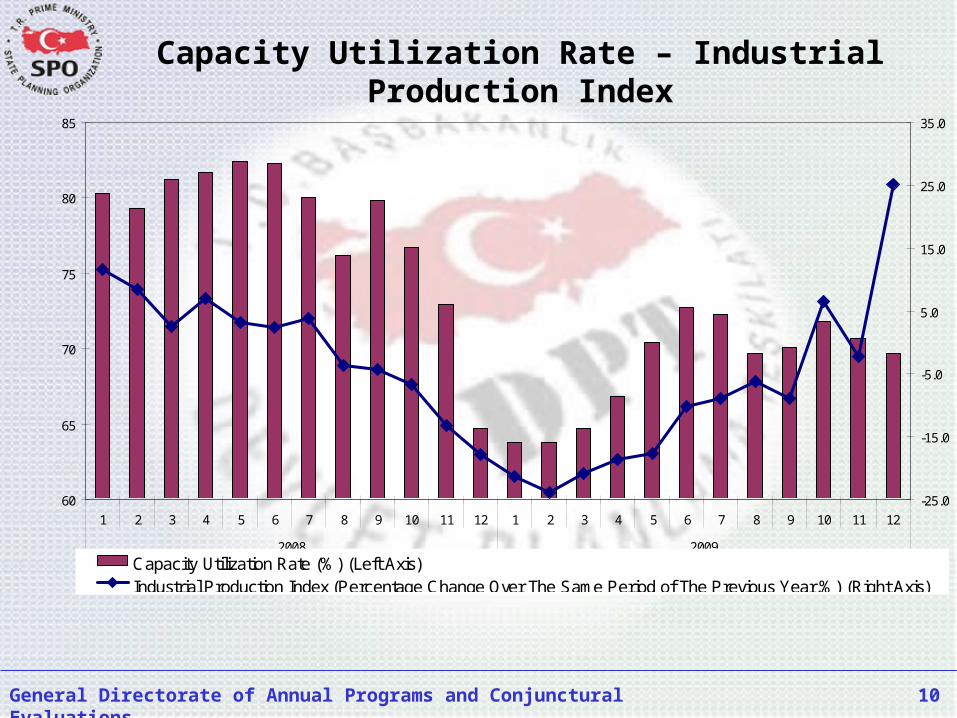

60

65

70

75

80

85

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

2008 2009

-25.0

-15.0

-5.0

5.0

15.0

25.0

35.0

Capacity Utilization Rate (%) (Left Axis)Industrial Production Index (Percentage Change Over The Same Period of The Previous Year,%) (Right Axis)

Capacity Utilization Rate – Industrial Production Index

General Directorate of Annual Programs and Conjunctural Evaluations

11

0

100

200

300

400

500

600

2008-Jan.

April July Oct. 2009-Jan.

April July Oct.

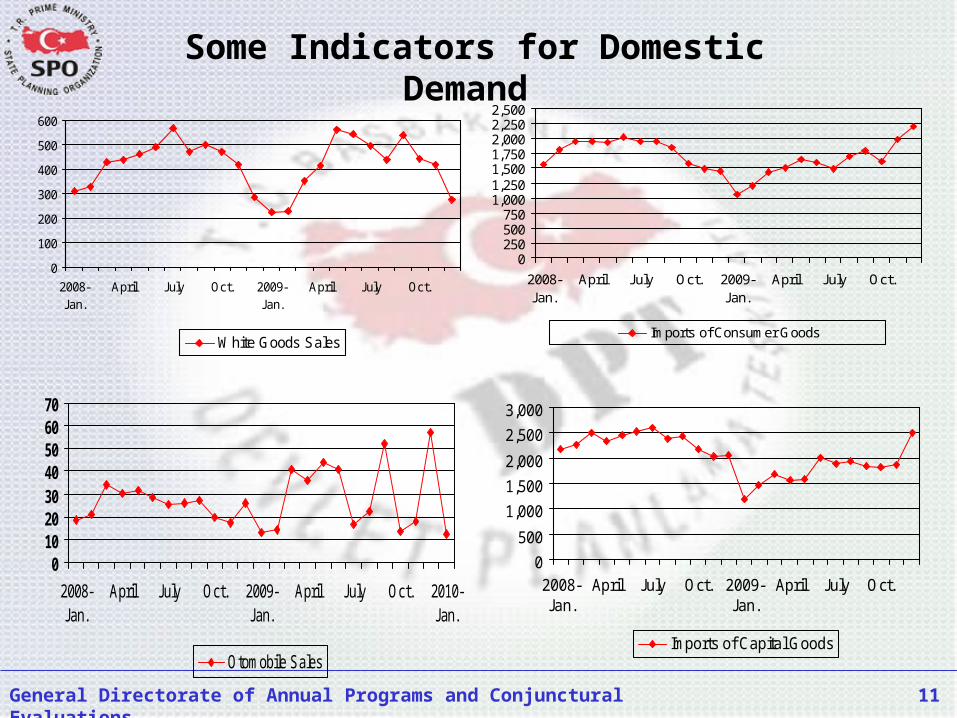

White Goods Sales

0250500750

1,0001,2501,5001,7502,0002,2502,500

2008-Jan.

April July Oct. 2009-Jan.

April July Oct.

Imports of Consumer Goods

010203040506070

2008-Jan.

April July Oct. 2009-Jan.

April July Oct. 2010-Jan.

Otomobile Sales

0

500

1,000

1,500

2,000

2,500

3,000

2008-Jan.

April July Oct. 2009-Jan.

April July Oct.

Imports of Capital Goods

Some Indicators for Domestic Demand

General Directorate of Annual Programs and Conjunctural Evaluations

12

50

60

70

80

90

100

110

12020

08-1

2008

-3

2008

-5

2008

-7

2008

-9

2008

-11

2009

-1

2009

-3

2009

-5

2009

-7

2009

-9

2009

-11

CBRT Consumer Confidence Index CNBC-e Consumer Confidence Index

Consumer Confidence Indices

General Directorate of Annual Programs and Conjunctural Evaluations

13

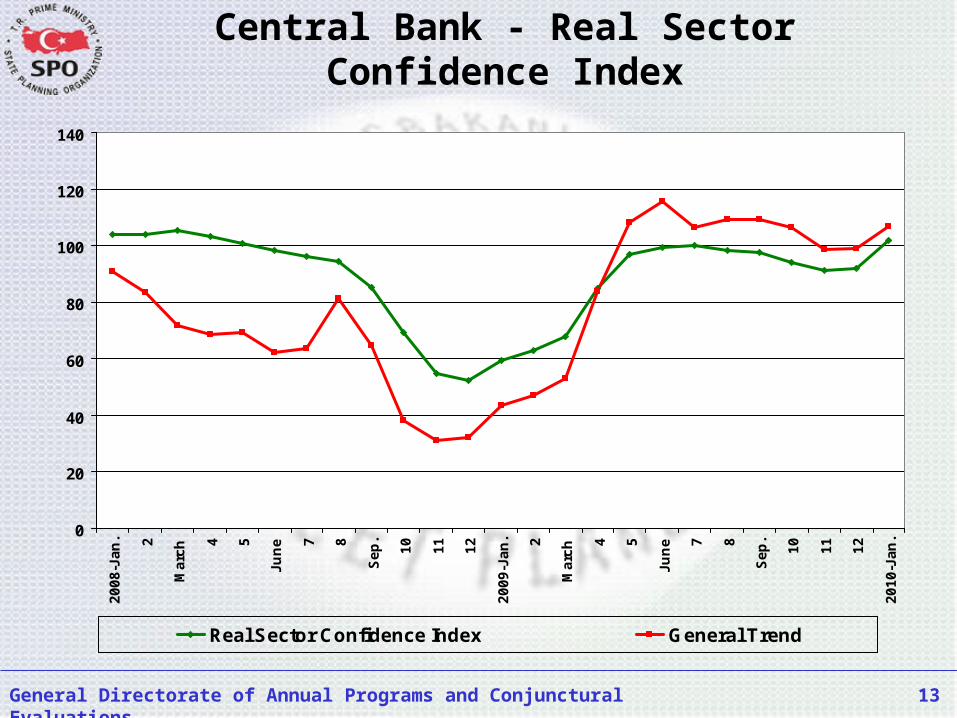

Central Bank - Real Sector Confidence Index

0

20

40

60

80

100

120

1402

00

8-J

an

. 2

Ma

rch 4 5

Ju

ne 7 8

Se

p.

10

11

12

20

09

-Ja

n. 2

Ma

rch 4 5

Ju

ne 7 8

Se

p.

10

11

12

20

10

-Ja

n.

Real Sector Confidence Index General Trend

General Directorate of Annual Programs and Conjunctural Evaluations

14

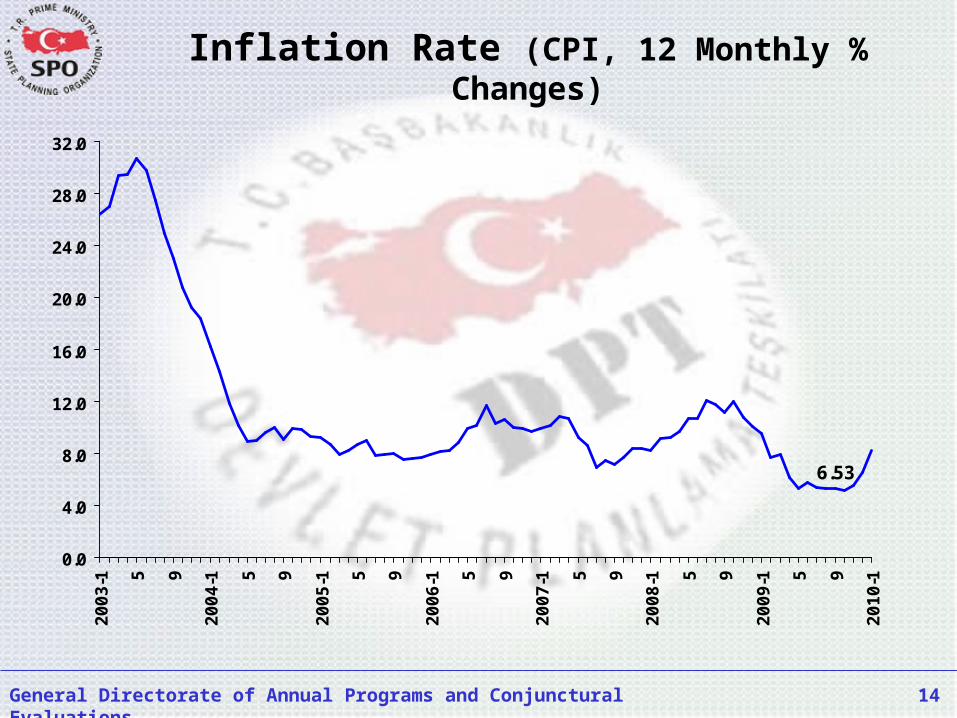

6.53

0.0

4.0

8.0

12.0

16.0

20.0

24.0

28.0

32.0

20

03

-1 5 9

20

04

-1 5 9

20

05

-1 5 9

20

06

-1 5 9

20

07

-1 5 9

20

08

-1 5 9

20

09

-1 5 9

20

10

-1

Inflation Rate (CPI, 12 Monthly % Changes)

General Directorate of Annual Programs and Conjunctural Evaluations

15

15

Central Bank Short Term Interest Rates (%)

13.2515

10.5

15.2515

22

20

14.25

17.5 16.75

6.5

0

4

8

12

16

20

24

28

20

04

-1 3 5 7 91

1 2

00

5-1 3 5 7 91

12

00

6-1 3 5 7 91

12

00

7-1 3 5 7 91

12

00

8-1 3 5 7 91

12

00

9 1 3 5 7 9

11

Policy Rates

General Directorate of Annual Programs and Conjunctural Evaluations

16

16

Source: Turkstat

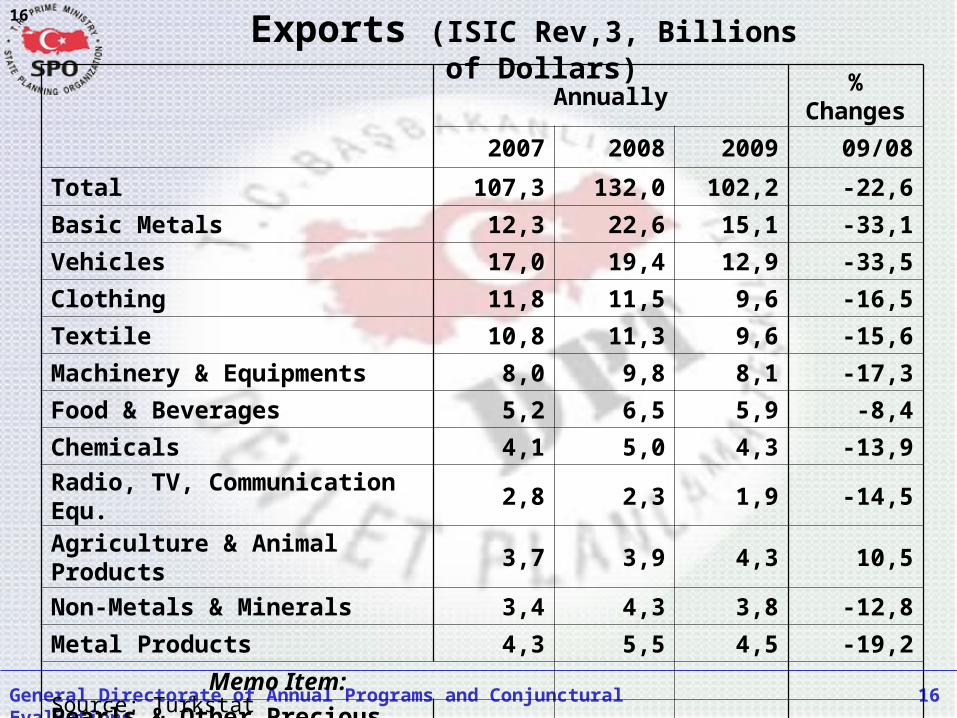

Exports (ISIC Rev,3, Billions of Dollars)

Annually%

Changes2007 2008 2009 09/08

Total 107,3 132,0 102,2 -22,6Basic Metals 12,3 22,6 15,1 -33,1Vehicles 17,0 19,4 12,9 -33,5Clothing 11,8 11,5 9,6 -16,5Textile 10,8 11,3 9,6 -15,6Machinery & Equipments 8,0 9,8 8,1 -17,3Food & Beverages 5,2 6,5 5,9 -8,4Chemicals 4,1 5,0 4,3 -13,9Radio, TV, Communication Equ.

2,8 2,3 1,9 -14,5

Agriculture & Animal Products

3,7 3,9 4,3 10,5

Non-Metals & Minerals 3,4 4,3 3,8 -12,8Metal Products 4,3 5,5 4,5 -19,2 Memo Item:Pearls & Other Precious Stones

2,6 5,4 5,9 10,1

General Directorate of Annual Programs and Conjunctural Evaluations

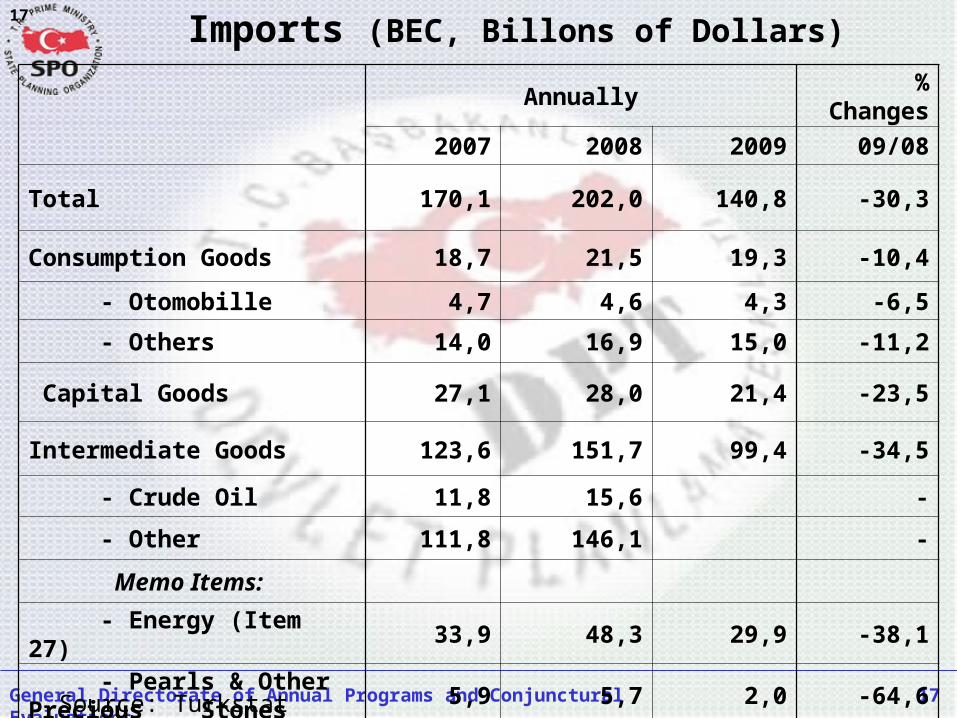

17

17

Source: Turkstat

Imports (BEC, Billons of Dollars)

Annually%

Changes2007 2008 2009 09/08

Total 170,1 202,0 140,8 -30,3

Consumption Goods 18,7 21,5 19,3 -10,4

- Otomobille 4,7 4,6 4,3 -6,5

- Others 14,0 16,9 15,0 -11,2

Capital Goods 27,1 28,0 21,4 -23,5

Intermediate Goods 123,6 151,7 99,4 -34,5

- Crude Oil 11,8 15,6 -

- Other 111,8 146,1 -

Memo Items:

- Energy (Item 27) 33,9 48,3 29,9 -38,1

- Pearls & Other Precious Stones

5,9 5,7 2,0 -64,6

General Directorate of Annual Programs and Conjunctural Evaluations

18

102.1

132.0

107.3

85.5

73.563.2

47.336.1

140.8

202.0

170.1

139.6

116.8

97.5

69.3

51.6

0.0

50.0

100.0

150.0

200.0

2002 2003 2004 2005 2006 2007 2008 2009

Exports Imports

Foreign Trade (Billions of Dollars)

General Directorate of Annual Programs and Conjunctural Evaluations

19

Current Account Deficit(% of GDP)

3.7

4.6

5.9 5.7

2.3

6.0

2.5

0

1

2

3

4

5

6

7

2003 2004 2005 2006 2007 2008 2009

General Directorate of Annual Programs and Conjunctural Evaluations

20

Current Account Balance (Excluding Energy Price Effects , % of GDP)

2.9 2.9

0.2

1.8

3.43.5

2.3

-2

-1

0

1

2

3

4

2003 2004 2005 2006 2007 2008 2009

General Directorate of Annual Programs and Conjunctural Evaluations

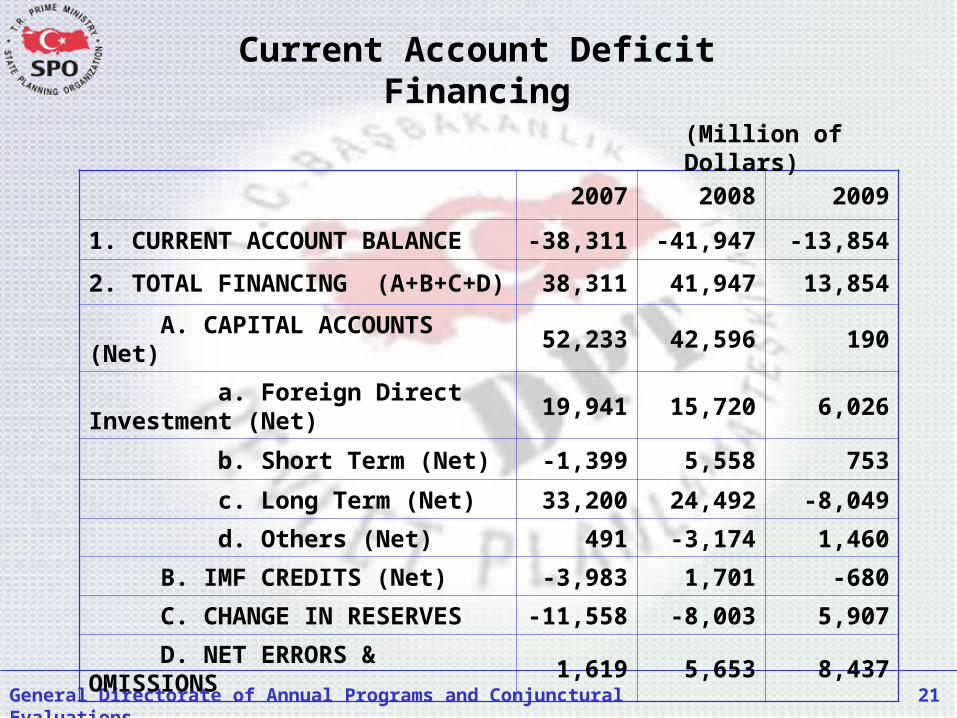

21

Current Account Deficit Financing

2007 2008 2009

1. CURRENT ACCOUNT BALANCE

-38,311 -41,947 -13,854

2. TOTAL FINANCING (A+B+C+D)

38,311 41,947 13,854

A. CAPITAL ACCOUNTS (Net)

52,233 42,596 190

a. Foreign Direct Investment (Net)

19,941 15,720 6,026

b. Short Term (Net) -1,399 5,558 753

c. Long Term (Net) 33,200 24,492 -8,049

d. Others (Net) 491 -3,174 1,460

B. IMF CREDITS (Net) -3,983 1,701 -680

C. CHANGE IN RESERVES -11,558 -8,003 5,907

D. NET ERRORS & OMISSIONS

1,619 5,653 8,437

(Million of Dollars)

General Directorate of Annual Programs and Conjunctural Evaluations

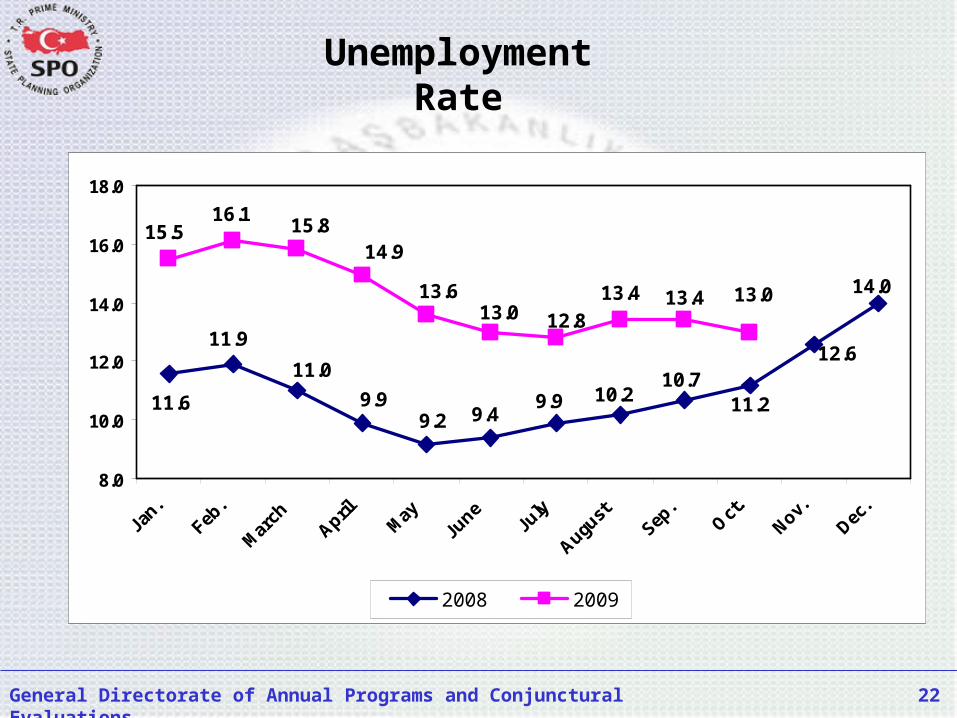

22

11.6

11.9

11.0

9.9

14.0

9.2 9.49.9 10.2

10.711.2

12.6

15.516.1

15.814.9

13.613.0 12.8

13.4 13.4 13.0

8.0

10.0

12.0

14.0

16.0

18.0

Jan.

Feb.

Mar

chApril

May

June

July

August

Sep.

Oct

.Nov.

Dec.

2008 2009

Unemployment Rate

General Directorate of Annual Programs and Conjunctural Evaluations

23

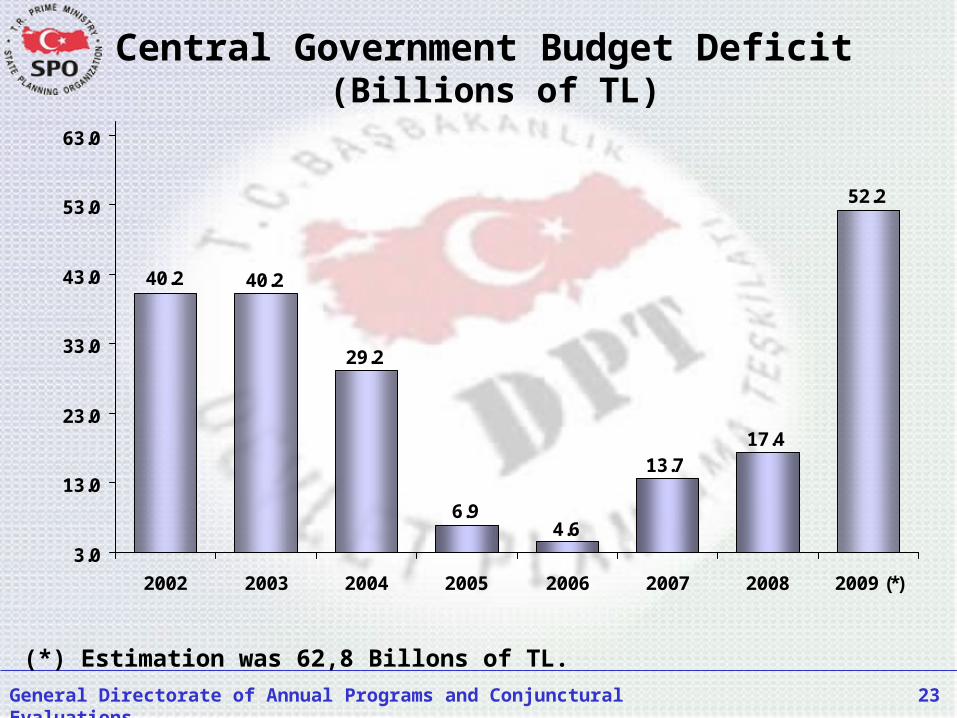

4.6

52.2

17.413.7

40.2 40.2

29.2

6.9

3.0

13.0

23.0

33.0

43.0

53.0

63.0

2002 2003 2004 2005 2006 2007 2008 2009 (*)

(*) Estimation was 62,8 Billons of TL.

Central Government Budget Deficit (Billions of TL)

General Directorate of Annual Programs and Conjunctural Evaluations

24

0.6

5.5

1.81.6

11.5

8.8

5.2

1.1

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2002 2003 2004 2005 2006 2007 2008 2009 (*)

(*) Estimation was 6,6 percent.

Central Government Budget Deficit / GDP (%)

General Directorate of Annual Programs and Conjunctural Evaluations

25

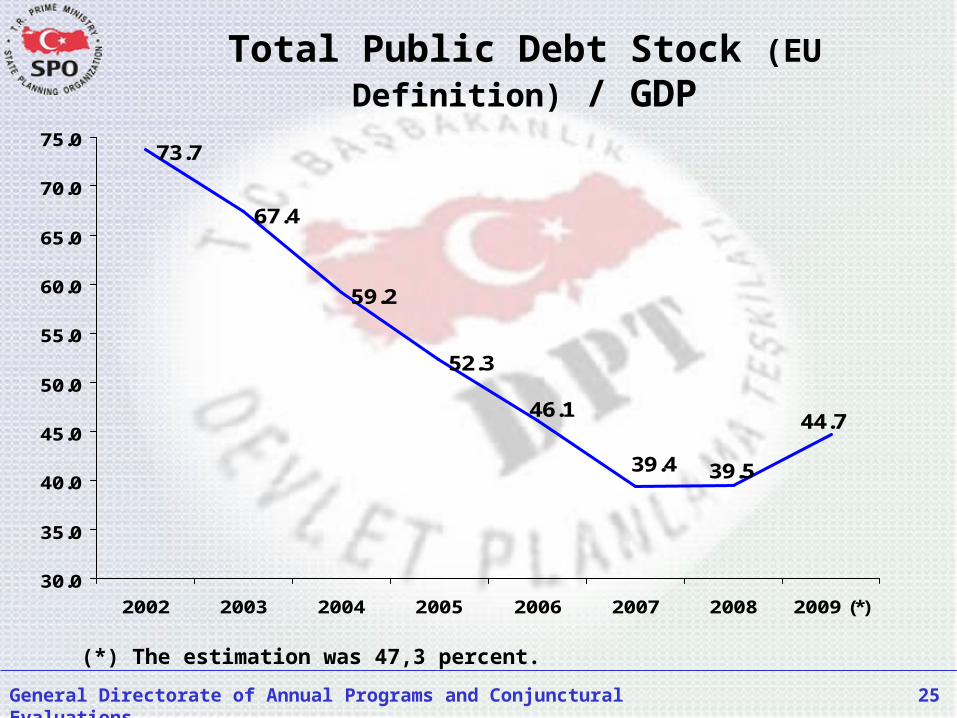

46.144.7

39.539.4

73.7

67.4

59.2

52.3

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

75.0

2002 2003 2004 2005 2006 2007 2008 2009 (*)

(*) The estimation was 47,3 percent.

Total Public Debt Stock (EU Definition) / GDP

General Directorate of Annual Programs and Conjunctural Evaluations

26

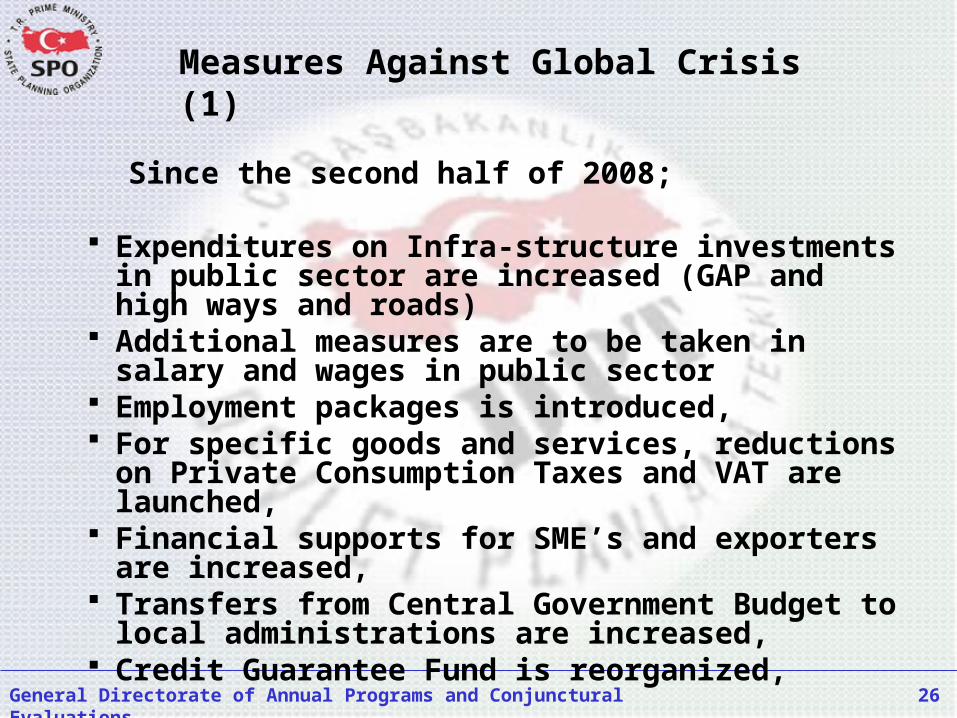

Since the second half of 2008;

Expenditures on Infra-structure investments in public sector are increased (GAP and high ways and roads)

Additional measures are to be taken in salary and wages in public sector

Employment packages is introduced, For specific goods and services, reductions

on Private Consumption Taxes and VAT are launched,

Financial supports for SME’s and exporters are increased,

Transfers from Central Government Budget to local administrations are increased,

Credit Guarantee Fund is reorganized,

Measures Against Global Crisis (1)

General Directorate of Annual Programs and Conjunctural Evaluations

27

Central Bank introduced some measures by monitoring the liqudity conditions of foreign currency and TL in the money markets. In this perspectives: Policy rates are reduced by 10,25

percentage points since November 2008 and down to 6,50 percentage in December 2009.

Central Bank extend credits to the banks that are the subject of uncertainty and lack of confidence in the event of acceleration of fund withdrawals and uncertainty and lack of confidence in the banking system,

Foreign currency required reserve ratio was lowered by the Bank, this reduction has provided an additional foreign exchange liquidity for the banking system.

Measures Against Global Crisis (2)

General Directorate of Annual Programs and Conjunctural Evaluations

28

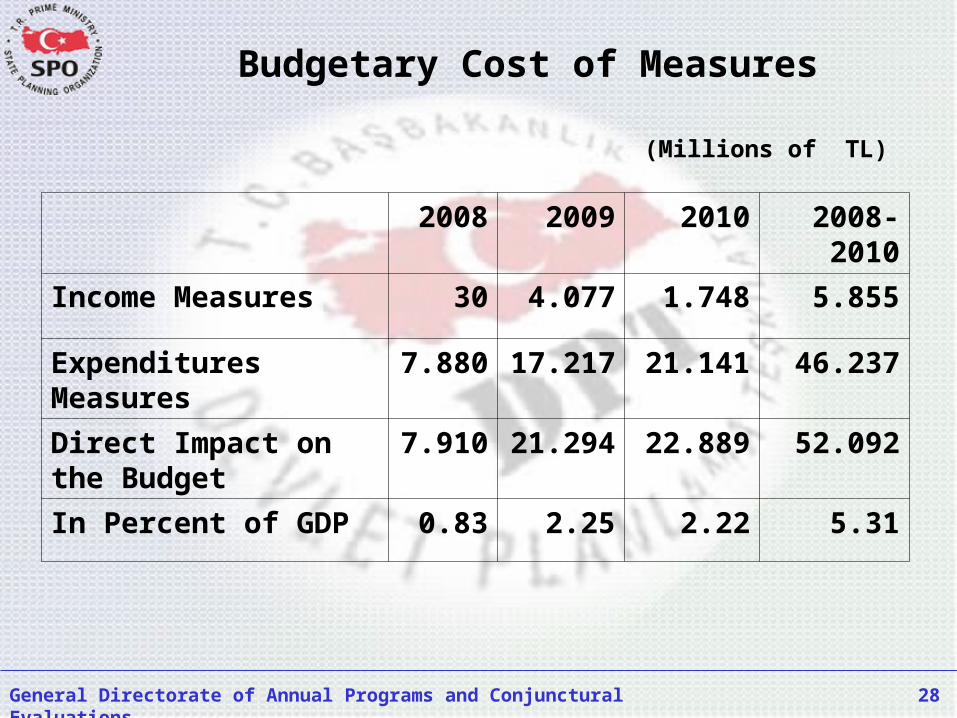

2008 2009 2010 2008-2010

Income Measures 30 4.077 1.748 5.855

Expenditures Measures

7.880

17.217

21.141 46.237

Direct Impact on the Budget

7.910

21.294

22.889 52.092

In Percent of GDP 0.83 2.25 2.22 5.31

Budgetary Cost of Measures

(Millions of TL)

General Directorate of Annual Programs and Conjunctural Evaluations

29

MEDIUM TERM PROGRAM(2010-2012)

General Directorate of Annual Programs and Conjunctural Evaluations

30

Main objective of the MTP is to provide a transition of the economy for a sustainable growth period again,

In this perspective, public sector has crucial role in reducing the effects of global crisis on economy,

The short term ones focus on increasing consumption expenditures and eliminating bottlenecks in credit system,

While the medium term ones concentrate on permanent increase in production, investment, employment and export in economy.

Macroeconomic Policies and MainObjectives in the MTP (2010-2012) and in the Annual Program 2010

General Directorate of Annual Programs and Conjunctural Evaluations

31

Following growth process would be realized with the leadership of the private sector

Gradual reduction in public sector borrowing requirement,

Maintaining the price stability,

are crucial to increase the available resources and the foresight of private sector in investment and production decisions.

General Directorate of Annual Programs and Conjunctural Evaluations

32

The recovery of our country from the influence of the global crisis is closely related with the improvements in the world economy.

Gradual and uneven recovery in the world economy is expected,

Targets in the program are determined by taking also forecasts about foreign economic conjuncture.

In many countries especially in the developed ones, rises in the unemployment rates are estimated to continue also in 2010.

Due to weak demand and employment conditions, global inflation is estimated to maintain at low levels also in 2010.

Constraints

General Directorate of Annual Programs and Conjunctural Evaluations

33

Macroeconomic Indicators in MTP

SECTORS 2010 (2)

2011 (2)

2012 (2)

GDP Growth Rates 3,5 4,0 5,0GDP (At Current Prices, Billions of Dollar) 641 669 723PER CAPITA GDP (At Current Prices, Dollar) 8.821 9.096 9.732

CPI (End of Year, % Change) 5,3 4,9 4,8(1) Estimate, (2) Program.

General Directorate of Annual Programs and Conjunctural Evaluations

34

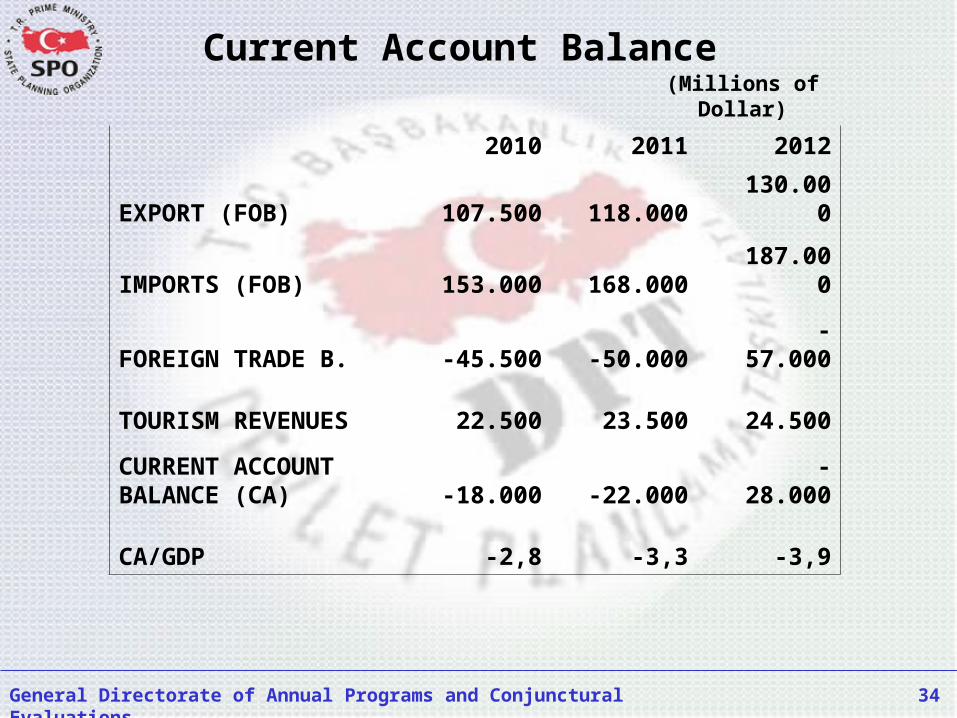

2010 2011 2012

EXPORT (FOB) 107.500 118.000130.00

0

IMPORTS (FOB) 153.000 168.000187.00

0

FOREIGN TRADE B. -45.500 -50.000-

57.000

TOURISM REVENUES 22.500 23.500 24.500

CURRENT ACCOUNT BALANCE (CA) -18.000 -22.000

-28.000

CA/GDP -2,8 -3,3 -3,9

(Millions of Dollar)

Current Account Balance

General Directorate of Annual Programs and Conjunctural Evaluations

35

4.94.0

3.2

0.0

2.0

4.0

6.0

8.0

10.0

2010 2011 2012

Central Govern. Budget Deficit / GDP (%)

General Directorate of Annual Programs and Conjunctural Evaluations

36

-0.3

0.4

1.0

-0.50

-0.30

-0.10

0.10

0.30

0.50

0.70

0.90

1.10

1.30

1.50

2010 2011 2012

Public Sector Primary Surplus / GDP (%)

General Directorate of Annual Programs and Conjunctural Evaluations

37

47.8

48.849.0

46.0

47.0

48.0

49.0

50.0

2010 2011 2012

Public Sector Debt Stock (*) / GDP

(*) EU Definition

General Directorate of Annual Programs and Conjunctural Evaluations

38

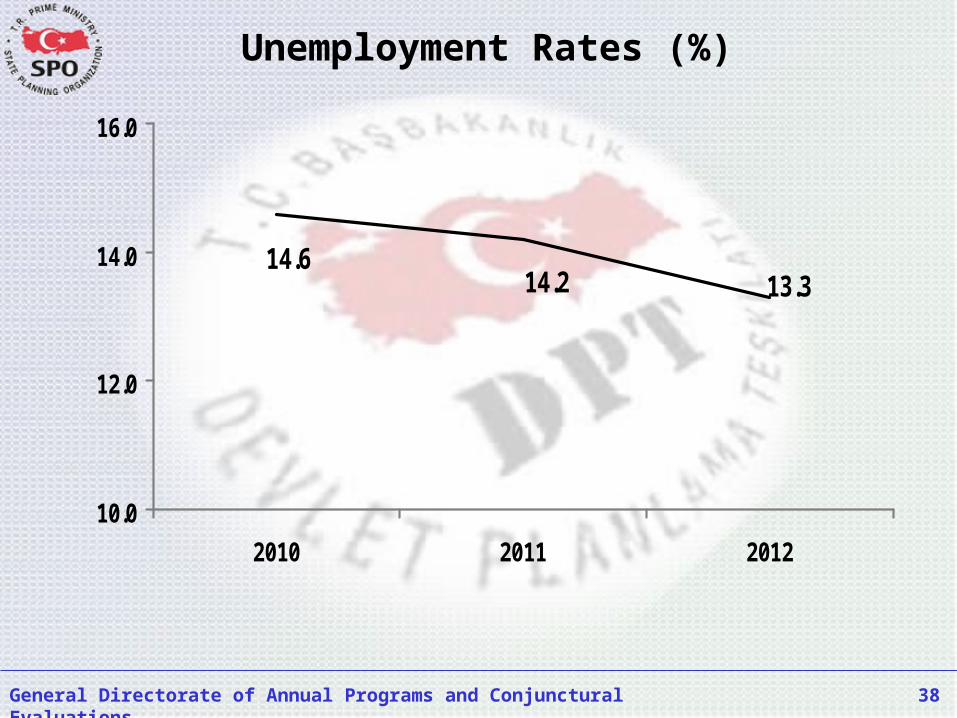

14.614.2 13.3

10.0

12.0

14.0

16.0

2010 2011 2012

Unemployment Rates (%)

General Directorate of Annual Programs and Conjunctural Evaluations

39

•Fiscal rules will be implemented.

A new governance model in SEEs will be implemented.

In the financing of investments, the use of public-private collaboration models will be expanded.

Health services and expenditures will be made efficient.

Appropriateness and efficiency in social aids will be achieved.

Agricultural supports will be rearranged.

Structural Reforms in the MTP and in the Annual Program 2010

General Directorate of Annual Programs and Conjunctural Evaluations

40

Tax reform will be finalized.

Arrangements will be made for the local governments to increase their own revenues and improve their financial management.

Training the man power will be accelerated in the nature that the business world demands.

Forms of flexible employment will be expanded.

Development agencies, of which organization process completed, will be put into operation.

State aids will be made more transparent and efficient.

The efficiency of Credit Guarantee Fund will be increased.