Full Employment or Bust · Full Employment or Bust Global Economic Outlook Issues, 51st Annual...

129

Global Economic Outlook Issues, 51 st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014. Full Employment or Bust Full Employment or Bust

Transcript of Full Employment or Bust · Full Employment or Bust Global Economic Outlook Issues, 51st Annual...

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Full Employment or Bust

Full Employment or Bust

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

2

When will the Fed’s rates go back to normal?

Nominal federal funds rate and core inflation¹ (percent per annum and % ch. from 12 months earlier)

¹ Chain price index for personal consumption expenditures excluding food and energy.

Source: Federal Reserve Board. Updated through October 31, 2014.

0

4

8

12

16

20

0

4

8

12

16

20

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Core PCE

chain price

inflation ( % ch. from 12 months earlier)

Nominal federal funds rate

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

3

Where are bond yields headed?

Components of the 5-year Treasury yield five years in the future (percent per annum)

Source: Federal Reserve Board. Updated through October 31, 2014.

-1

0

1

2

3

4

5

6

7

-1

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Five-year forward Treasury yield (5 x 5)

Five-year forward real Treasury yield (5 x 5 TIPS)

Five-year forward inflation expectations plus inflation risk premium (5 x 5 breakeven)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

High yield spread (basis points)

Sources: Federal Reserve Board, JPMorgan. Updated through November 7, 2014.

Can credit spreads narrow further?

4

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Ibbotson Associates J.P. Morgan Securities LLC high-yield index

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Wilshire 5000 (Dec 31, 1970 = 830.27) After-tax GDP profits (billions of dollars)

Note: scales aligned to reflect the historical P/E of 11 times ex. the multiples of 1997 through 2001.

Sources: US Department of Commerce; Dow Jones. Updated through 2014 Q3 (profits) and Nov. 26, 2014.

Whither stocks? Fairly valued to current earnings ...

5

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

34,000

36,000

1990 1995 2000 2005 2010 2015 2020

Line represents the Wilshire 5000 index (left scale)

Shaded area represents after-tax GDP profits (right scale)

Note: Since 1952, the Wilshire 5000 P/E climbs to 14 times earnings near cyclical peaks, excluding the unprecedented multiples during 1997 - 2001, and that would occur when the line floats at the upper boundary of earnings.

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Wilshire 5000 (Dec 31, 1970 = 830.27) After-tax GDP profits (billions of dollars)

Note: scales aligned to reflect the historical P/E of 11 times ex. the multiples of 1997 through 2001.

Sources: US Department of Commerce; Dow Jones. Updated through 2014 Q3 (profits) and Nov. 26, 2014.

... but what about tomorrow’s?

6

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

34,000

36,000

1990 1995 2000 2005 2010 2015 2020

Line represents the Wilshire 5000 index (left scale)

Shaded area represents after-tax GDP profits (right scale)

Note: Since 1952, the Wilshire 5000 P/E climbed to 14 times earnings near cyclical peaks, excluding the unprecedented multiples during 1997 - 2001, and that would occur when the line floated at the upper boundary of earnings.

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

7

Powering Up ... No Surprise

Real GDP, selected developed economies (ratio to 1997 Q4, 2005 US dollars, PPP basis)

Sources: US Dep. of Commerce; Haver Analytics; JPMorgan Chase & Co. Updated through 2014 Q3.

0.90

0.91

0.92

0.93

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

1.08

0.90

0.91

0.92

0.93

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

1.08

2007 2008 2009 2010 2011 2012 2013 2014

28-member European Union

Japan

United States

2014 Q3

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

8

And there’s nothing artificial about this

Labor force and selected measures of employment (thousands)

Source: US Department of Labor. Updated through October 2014.

128,000

130,000

132,000

134,000

136,000

138,000

140,000

142,000

144,000

146,000

148,000

150,000

152,000

154,000

156,000

158,000

128,000

130,000

132,000

134,000

136,000

138,000

140,000

142,000

144,000

146,000

148,000

150,000

152,000

154,000

156,000

158,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Labor force

Household employment adjusted for breaks in the population

Household employment adjusted to match the concepts and coverage of nonfarm payrolls

Nonfarm payrolls

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

9

Those who know, know

Real GDP (percent change from 4 quarters earlier) Jobless claims (thousands weekly, scale reversed)

Sources: US Deps. of Labor and Com. Updated through 2014 Q3 (GDP) and November 22, 2014 (claims).

50

100

150

200

250

300

350

400

450

500

550

600

650

700-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018

Real GDP growth (left)

Jobless claims (right, scale is reversed)

Real GDP

growth forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Recovery and time heals

10

0

25

50

75

100

125

150

175

200

225

0

25

50

75

100

125

150

175

200

225

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

CoreLogic measure of house prices

Scenario above assumes that

house prices rise 4%

annually in the

future.

Note: The red zone represents an estimate ($875 billion) of the aggregate amount of remaining under-water mortgages, before chargeoffs

House prices (January 2000 = 100)

Source: CoreLogic. Updated through 2014 Q2.

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

11

That’s why they’re moving to the front of the line ...

Nonfarm employment in selected areas (ratio to 2000 Q4 level)

Source: US Department of Labor. Updated through September 2014 (US) and September 2014 (state).

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US

California

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

12

... and why you will be

Nonfarm employment in selected areas (ratio to 2000 Q4 level)

Source: US Department of Labor. Updated through September 2014 (US) and September 2014 (state).

0.97

0.99

1.01

1.03

1.05

1.07

1.09

1.11

1.13

1.15

1.17

1.19

0.97

0.99

1.01

1.03

1.05

1.07

1.09

1.11

1.13

1.15

1.17

1.19

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Arizona

US

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

13

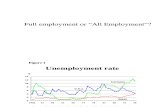

The economy and the motion of the ocean

The economic cycle, unemployment rate (percent of the labor force)

Source: US Department of Labor. Updated through October 2014.

0

1

2

3

4

5

6

7

8

9

10

11

12

13

0

1

2

3

4

5

6

7

8

9

10

11

12

13

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Nairu (where we want to be)

Official unemployment rate (U-3)Official unemployment plus part-timers plus job-force exits under 49 years of age (U-3 ++)

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Unemployment rate (percent)

Sources: Vertical bars denote recessions and are designated by the NBER; US Department of Labor. Updated

through October 2014 (unemployment) and September 17, 2014 (FOMC forecast). 14

The unemployment rate doesn’t know everything ...

0

1

2

3

4

5

6

7

8

9

10

11

12

0

1

2

3

4

5

6

7

8

9

10

11

12

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Horizontal bars denote the Fed's view

(central tendency) about the near-term and sustainable unemployment rate (often referred to as the Nairu, or nonincreasing

inflationary rate of unemployment)¹

Note: The red boxes identify the first step in each Fed tightening sequence.

Proved to be premature and the Fed backed down

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

... but what it knows is getting better ...

Duration of unemployment spells (thousands)

Source: US Department of Labor. Updated through October 2014. 15

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Unemployed for less than 27 weeks (left scale)

Percent of the labor force unemployed for less than 27 weeks (right scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

... that long-term unemployed are getting jobs too

Duration of unemployment spells (thousands)

Source: US Department of Labor. Updated through October 2014. 16

0%

1%

2%

3%

4%

5%

6%

7%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Unemployed for more than 27 weeks (left scale)

Percent of the labor force unemployed for more than 27 weeks (right scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Selected elderly populations (percent of the population)

Source: US Department of Labor. Updated through July 2014.

17

Demographics are in the background but are just a footnote

0.00

0.05

0.10

0.15

0.20

0.25

0.00

0.05

0.10

0.15

0.20

0.25

1947 1957 1967 1977 1987 1997 2007 2017 2027 2037 2047

The projected five percentage point rise in the fraction of the population over the age of 65 represents an increase of about 16 million people in today's terms. That represents an average increase of one million annually when spread out over the next 15 years.

The percentage of the population over the age of 69.

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Involuntary part-timers are called “employed” ... not so

Involuntary part-time (thousands) (percent of the labor force)

Source: US Department of Labor. Updated through September 2014. 18

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Percent of the labor force (right scale)

Number of people (left scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Dropouts are nowhere ... but they aren’t retiring

Participation rate for selected age groups (percent of the respective population)

Source: US Department of Labor. Updated through October 2014. 19

54

55

56

57

58

59

60

61

78

79

80

81

82

83

84

85

2007 2008 2009 2010 2011 2012 2013 2014

35 to 44 year olds (left scale)

25 to 34 year olds (left scale)45 to 54 year olds (left scale)

16 to 24 year olds (right scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Selected unemployment rate measures (percent of the labor force)

Source: US Department of Labor. Updated through September 2014.

20

Thinking outside the unemployment box ... 5th inning

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

U-6 (official plus involuntarily part-time plus marginally attached)

Official unemployment plus part-timers plus job-force exits under 49 years of age (U-3 ++)

Official unemployment plus one half of above-normal number of part-timers (U-3 +)

Official unemployment rate (U-3)

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

We don’t live in silos

Output gap in selected regions (actual less potential real GDP as a percent of potential real GDP)

Source: US Department of Commerce; JPMorgan. Updated through 2014 Q3. 21

-14

-12

-10

-8

-6

-4

-2

0

2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Japan

EU-28

US

Australia

Canada

Sweden

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

The proof is in the tasting ... hourly compensation ...

Hourly wage & salary rates (percent change from four quarters earlier)

Sources: US Departments of Commerce and Labor. Updated through 2014 Q2. 22

0

1

2

3

4

5

0

1

2

3

4

5

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

ECI, private-sector compensation, excluding incentive-based pay

ECI, privae-sector compensation

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Core PCE chain price index (percent change from 12 months earlier)

¹ Chain price index for personal consumption expenditures.

Sources: Vertical bars denote recessions and are designated by the NBER; US Department of Commerce.

Updated through October 2014 (inflation) and September 17, 2014 (FOMC forecast).

... inflation ... all of it looks and feels like the 5th inning

23

-2

0

2

4

6

8

10

12

-2

0

2

4

6

8

10

12

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

The range of FOMC's forecast

for PCE chain

price inflation, including its

longer-run goal

Overall PCE inflation¹

Core PCE inflation¹

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

After-tax GDP profits of all US businesses (percent of nominal Gross Domestic Income)

Sources: Vertical bars denote recessions and are designated by the NBER; US Department of Commerce.

Updated through 2014 Q3.

Meanwhile there’s still a lot for equity markets to digest

24

0

1

2

3

4

5

6

7

8

9

10

11

0

1

2

3

4

5

6

7

8

9

10

11

1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012 2017

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

25

Doing Well, Despite All, ...

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

26

Powering Up

Real GDP, selected developed economies (ratio to 1997 Q4, 2005 US dollars, PPP basis)

Sources: US Dep. of Commerce; Haver Analytics; JPMorgan Chase & Co. Updated through 2014 Q3.

0.90

0.91

0.92

0.93

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

1.08

0.90

0.91

0.92

0.93

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

1.08

2007 2008 2009 2010 2011 2012 2013 2014

28-member European Union

Japan

United States

2014 Q3

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

27

There’s nothing artificial about this

Labor force and selected measures of employment (thousands)

Source: US Department of Labor. Updated through October 2014.

128,000

130,000

132,000

134,000

136,000

138,000

140,000

142,000

144,000

146,000

148,000

150,000

152,000

154,000

156,000

158,000

128,000

130,000

132,000

134,000

136,000

138,000

140,000

142,000

144,000

146,000

148,000

150,000

152,000

154,000

156,000

158,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Labor force

Household employment adjusted for breaks in the population

Household employment adjusted to match the concepts and coverage of nonfarm payrolls

Nonfarm payrolls

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

28

Those who know, know

Real GDP (percent change from 4 quarters earlier) Jobless claims (thousands weekly, scale reversed)

Sources: US Deps. of Labor and Com. Updated through 2014 Q3 (GDP) and November 22, 2014 (claims).

50

100

150

200

250

300

350

400

450

500

550

600

650

700-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018

Real GDP growth (left)

Jobless claims (right, scale is reversed)

Real GDP

growth forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

29

If it’s over at Ground Zero, it’s over

Nonfarm employment in selected areas (ratio to 2000 Q4 level)

Source: US Department of Labor. Updated through September 2014 (US) and September 2014 (state).

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US

California

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

30

... ditto ...

Nonfarm employment in selected areas (ratio to 2000 Q4 level)

Source: US Department of Labor. Updated through September 2014 (US) and September 2014 (state).

0.95

1.00

1.05

1.10

1.15

0.95

1.00

1.05

1.10

1.15

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Florida

US

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

31

... double ditto ...

Nonfarm employment in selected areas (ratio to 2000 Q4 level)

Source: US Department of Labor. Updated through September 2014 (US) and September 2014 (state).

0.97

0.99

1.01

1.03

1.05

1.07

1.09

1.11

1.13

1.15

1.17

1.19

0.97

0.99

1.01

1.03

1.05

1.07

1.09

1.11

1.13

1.15

1.17

1.19

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Arizona

US

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

32

... triple ditto

Nonfarm employment in selected areas (ratio to 2000 Q4 level)

Source: US Department of Labor. Updated through September 2014 (US) and September 2014 (state).

0.97

1.02

1.07

1.12

1.17

1.22

1.27

0.97

1.02

1.07

1.12

1.17

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Nevada

US

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

33

Shale activity is big but isn’t the whole story ...

Nonfarm employment in selected areas (ratio to December 2007 level)

Source: US Department of Labor. Updated through September 2014 (US) and September 2014 (state).

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US Forecast US ND UT WY TX AK MT

NV ID AZ HI AL AR CA CO

CT DE DC FL GA IL IN IA

KS KY LA ME MD MA MI MN

MS MO NE NH NJ NM NY NC

OH OK OR PA RI SC SD TN

VT VA WA Wva WI

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

34

... because just about everyone is swimming upstream

Nonfarm employment in selected areas (ratio to December 2007 level)

Source: US Department of Labor. Updated through September 2014 (US) and September 2014 (state).

0.85

0.87

0.89

0.91

0.93

0.95

0.97

0.99

1.01

1.03

1.05

1.07

1.09

1.11

0.85

0.87

0.89

0.91

0.93

0.95

0.97

0.99

1.01

1.03

1.05

1.07

1.09

1.11

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US Forecast US

TX DC

AK UT

CO SD

OK NY

MA NE

MN MT

LA IA

W Va WA

VA MD

KS WY

CA NH

PA TN

VT IN

HI WI

AR SC

MO DE

KY NC

OR RI

ID ME

OH GA

FL IL

CT MI

NJ MS

NM AZ

AL NV

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Household income and house prices (ratio to 1970)

Sources: US Dep. of Commerce; CoreLogic. Updated through 2014 Q2 (income) and 2014 Q2 (house prices).

All this, despite the real estate hangover

35

0

1

2

3

4

5

6

7

8

9

10

11

12

13

0

1

2

3

4

5

6

7

8

9

10

11

12

13

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18

CoreLogic house price index (ratio to 1970)

Gross nominal income per household (ratio to 1970)Forecast

(assumes nominal income

grows 5% annually in the coming

decade's recovery)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Contribution of government spending (cont. to real GDP over 4-qtr spans, percentage points)

Sources: NBER-designated recession bars; U.S. Department of Commerce. Updated through 2014 Q3.

All this, despite the unprecedented fiscal swing

36

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

37

All this, despite severe headwinds in Europe and Japan

Real GDP in selected regions (percent change from four quarters earlier)

Sources: World Bank; US Dep. of Commerce; JPMorgan Chase & Co. Updated through 2014 Q3.

-9-8-7-6-5-4-3-2-1012345678910111213

-9-8-7-6-5-4-3-2-10123456789

10111213

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

China

India

All others

US (thick line)

Japan

28-member European Union

Global (shaded grey region)

Forecasts

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

38

For us, despite Sandy’s washout

Nonfarm employment in selected areas (ratio to December 2007 level)

Source: US Department of Labor. Updated through September 2014 (US) and September 2014 (state).

0.85

0.87

0.89

0.91

0.93

0.95

0.97

0.99

1.01

1.03

1.05

1.07

1.09

1.11

0.85

0.87

0.89

0.91

0.93

0.95

0.97

0.99

1.01

1.03

1.05

1.07

1.09

1.11

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US Forecast US

TX DC

AK UT

CO SD

OK NY

MA NE

MN MT

LA IA

W Va WA

VA MD

KS WY

CA NH

PA TN

VT IN

HI WI

AR SC

MO DE

KY NC

OR RI

ID ME

OH GA

FL IL

CT MI

NJ MS

NM AZ

AL NV

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

39

... And Probably Will Do Better in 2015 ...

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

40

In the US, done with the “slow” ...

Real GDP (annualized percent change)

Source: US Department of Commerce. Updated through 2014 Q3.

2.9

0.2

2.0

4.4

3.1 3.0

2.41.9

-2.8

-0.2

2.7

1.7 1.6

3.1

2.5

3.53.2 3.2 3.2

3.0

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

% change from the previous quarter

% change from four quarters earlier

% change over the four quarters of the year

Forecast (growth over the four

quarters of the year)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

High yield spread (basis points)

Sources: Federal Reserve Board, JPMorgan. Updated through November 7, 2014.

Credit conditions are all good ...

41

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Ibbotson Associates J.P. Morgan Securities LLC high-yield index

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

US vehicle sales and production (millions of units at an annualized rate)

Sources: US Department of Commerce; Federal Reserve Board. Updated through October 2014.

... and vehicle sales prove it

42

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

43

... But There’s Room to Run

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Unemployment rate (percent)

Sources: Vertical bars denote recessions and are designated by the NBER; US Department of Labor. Updated

through October 2014 (unemployment) and September 17, 2014 (FOMC forecast). 44

The unemployment rate doesn’t know everything ...

0

1

2

3

4

5

6

7

8

9

10

11

12

0

1

2

3

4

5

6

7

8

9

10

11

12

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Horizontal bars denote the Fed's view

(central tendency) about the near-term and sustainable unemployment rate (often referred to as the Nairu, or nonincreasing

inflationary rate of unemployment)¹

Note: The red boxes identify the first step in each Fed tightening sequence.

Proved to be premature and the Fed backed down

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

... but what it knows is getting better ...

Duration of unemployment spells (thousands)

Source: US Department of Labor. Updated through October 2014. 45

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Unemployed for less than 27 weeks (left scale)

Percent of the labor force unemployed for less than 27 weeks (right scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

... that long-term unemployed are getting jobs too

Duration of unemployment spells (thousands)

Source: US Department of Labor. Updated through October 2014. 46

0%

1%

2%

3%

4%

5%

6%

7%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Unemployed for more than 27 weeks (left scale)

Percent of the labor force unemployed for more than 27 weeks (right scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Selected elderly populations (percent of the population)

Source: US Department of Labor. Updated through July 2014.

47

Demographics are in the background but are just a footnote

0.00

0.05

0.10

0.15

0.20

0.25

0.00

0.05

0.10

0.15

0.20

0.25

1947 1957 1967 1977 1987 1997 2007 2017 2027 2037 2047

The projected five percentage point rise in the fraction of the population over the age of 65 represents an increase of about 16 million people in today's terms. That represents an average increase of one million annually when spread out over the next 15 years.

The percentage of the population over the age of 69.

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

December 3, 2014

Commercial Banking

What it doesn’t know (hidden unemployment) is improving

48

Change

2009 since Steady-state

peak the peak assumptions Excess vs steady state Sep 2014 Oct 2014

Unemployment (thousands) 15,352 -6,357 8,595 8,126 7,033 400 869 1,962 9,262 8,995

% of the labor force 10.0% (5.5%) (5.2%) (4.5%) (at 5.5%) (at 5.2%) (at 4.5%) 5.9% 5.8%

Unemployed fewer than 27 weeks 9,781 -3,579 5.860 342 6,307 6,202

% of the labor force 6.4% (3.7%) 4.0% 4.0%

Unemployed 27 weeks or more 5,643 -2,727 1,172 1,744 2,954 2,916

% of the Labor force 3.7% (0.75%) 1.9% 1.9%

Part-time for economic reasons (‘000) 8,979 -1,952 4,676 3,516 2,351 3,511 7,103 7,027

% of the labor force 5.9% (3.0%) (2.25%) (at 3.0%) (at 2.25%) 4.6% 4.5%

‘Work is slow’ (thousands) 6,681 -2,467 2,186 2,028 4,162 4,214

4.4% (1.4%) 2.7% 2.7%

‘Full-time work not available’ (thousands) 2,018 429 991 1,456 2,562 2,447

1.3% (0.6%) 1.6% 1.6%

20- to 49-yr old dropouts (thousands) 2,797 -140 0 2,657 2,704 2,657

20-year olds 1,205 -42 0 1,163 1,193 1,163

30-year olds 521 -58 0 464 467 464

40-year olds 1,070 -40 0 1,031 1,044 1,031

Memo: 16- to 19-year olds 971 -59 0 913 935 913

Note: Blue-shaded area marks the components of hidden unemployment.

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Involuntary part-timers are called “employed” ... not so

Involuntary part-time (thousands) (percent of the labor force)

Source: US Department of Labor. Updated through September 2014. 49

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Percent of the labor force (right scale)

Number of people (left scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Dropouts are nowhere ... but they aren’t retiring

Participation rate for selected age groups (percent of the respective population)

Source: US Department of Labor. Updated through October 2014. 50

54

55

56

57

58

59

60

61

78

79

80

81

82

83

84

85

2007 2008 2009 2010 2011 2012 2013 2014

35 to 44 year olds (left scale)

25 to 34 year olds (left scale)45 to 54 year olds (left scale)

16 to 24 year olds (right scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Selected unemployment rate measures (percent of the labor force)

Source: US Department of Labor. Updated through September 2014.

51

Thinking outside the unemployment box ... 5th inning

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

U-6 (official plus involuntarily part-time plus marginally attached)

Official unemployment plus part-timers plus job-force exits under 49 years of age (U-3 ++)

Official unemployment plus one half of above-normal number of part-timers (U-3 +)

Official unemployment rate (U-3)

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

It’s no surprise that Europe is disinflating

Output gap in selected regions (actual less potential real GDP as a percent of potential real GDP)

Source: US Department of Commerce; JPMorgan. Updated through 2014 Q2. 52

-14

-12

-10

-8

-6

-4

-2

0

2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Japan

EU-28

US

Australia

Canada

Sweden

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Hourly pay trends don’t feel like the 9th inning ...

Hourly labor compensation (percent change from four quarters earlier)

Sources: US Departments of Commerce and Labor; Updated through 2014 Q2. 53

-2

0

2

4

6

8

10

-2

0

2

4

6

8

10

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

ECEC (unweighted

version of the Employment Cost Index)

Employment Cost Index (fixed-weighted by industry and occupation)

Nonfarm business sector (unweighted), from the Productivity & Costs report

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

... incentive-based pay is behind the latest comp wiggle

Hourly labor compensation (percent change from four quarters earlier)

Sources: US Departments of Commerce and Labor; Updated through 2014 Q2. 54

0

1

2

3

4

5

0

1

2

3

4

5

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

ECI, private-sector compensation, excluding incentive-based pay

ECI, privae-sector compensation

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

... incentive-based pay is behind the latest wage wiggle

Hourly wage & salary rates (percent change from four quarters earlier)

Sources: US Departments of Commerce and Labor; Updated through 2014 Q2. 55

0

1

2

3

4

5

0

1

2

3

4

5

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

ECI, private-sector compensation, excluding incentive-based pay

ECI, privae-sector compensation

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

... ditto for hourly wage rates

Hourly labor compensation (percent change from four quarters earlier)

Source: US Department Labor; Updated through 2014 Q3 (ECI) and Oct. 2014 (average hourly earnings). 56

0.00.30.50.81.01.31.51.82.02.32.52.83.03.33.53.84.04.34.54.85.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

0.00.30.50.81.01.31.51.82.02.32.52.83.03.33.53.84.04.34.54.85.0

Average hourly earnings, production and nonsupervisory workers (thin black line)¹Average hourly earnings, total private industries (thick black line)¹ECI for private wages (orange line)

¹ Average hourly earnings for produduction workers are shown only up until March 2006 in order to provide historical context for the newer measure of average hourly earnings for all workers. The measure for all private -sector workers is available only since March 2006.

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Not all wage shifts are about wages

Hourly average wages (percent change from four quarters earlier)

Source: US Dep. of Labor; Updated through 2014 Q3 (ECI) and October 2014 (wages). 57

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

AHE, production and non-supervisory workers

AHE, all private-sector workers¹

ECI, hourly private sector wage rates

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Core PCE chain price index (percent change from 12 months earlier)

Sources: Vertical bars denote recessions and are designated by the NBER; US Department of Commerce.

Updated through August 2014 (inflation) and June 18, 2014 (FOMC forecast).

Inflation doesn’t look like the 9th inning, and it rules

58

-2

0

2

4

6

8

10

12

-2

0

2

4

6

8

10

12

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

The range of FOMC's forecast

for PCE chain

price inflation, including its

longer-run goal

Overall PCE inflation¹

Core PCE inflation¹

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

59

It’s Not News (Nor Interesting) that the Fed will Tighten and Rates Will Go Up

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

60

It would be news if it delayed

Forecasts of the federal funds rate (percent)

Source: Federal Reserve Board; Bloomberg. Updated through November 7, 2014.

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75

5.00

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75

5.00

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Dashes & Columns:Range of FOMC forecasts (lighter

columns)

Central tendency of FOMC

forecasts (darker columns)

Median FOMC forecast (horizontal line)

Lines:Current market forecast (solid blue line)¹

Glassman, midpoint of range rounded to the next 1/4 point

(dotted line)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

61

The outlook for long-term interest rates

Decomposition of 10-year Treasury yield (percent per annum)

Source: Federal Reserve Board. Updated through October 31, 2014.

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

819

99

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Estimated term premium embedded in a 10-year Treasury zero-coupon yield

Estimated average level of zero-coupon short-term interest rates anticipated over the subsequent 10 years

Average level of expected short-term interest rates plus an assumed term premium of 50 basis points

Average level of zero-coupon short-term interest rates anticipated over the subsequent 10 years (based on the assumed fed funds path, the dashed line)

Federal funds rate path (actual to date and assumed after that)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

62

Conclusion ... Implications of 5th Versus 8th Inning

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Actual and potential real GDP (2009 chained dollars)

Source: JPMorgan Chase & Co. Updated through 2014 Q2.

Why it matters

63

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

2007 2009 2011 2013 2015 2017 2019 2021

Potential real GDP = 2.1%

Actual real GDP

Potential real GDP = 2.5%

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Wilshire 5000 (Dec 31, 1970 = 830.27) After-tax GDP profits (billions of dollars)

Note: scales aligned to reflect the historical P/E of 11 times ex. the multiples of 1997 through 2001.

Sources: US Dep. of Commerce; Dow Jones. Updated through 2014 Q3 (profits) and Nov. 26, 2014 (stocks).

5th inning means there’s more of everything ahead

64

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

34,000

36,000

1990 1995 2000 2005 2010 2015 2020

Line represents the Wilshire 5000 index (left scale)

Shaded area represents after-tax GDP profits (right scale)

Note: Since 1952, the Wilshire 5000 P/E climbed to 14 times earnings near cyclical peaks, excluding the unprecedented multiples during 1997 - 2001, and that would occur when the line floated at the upper boundary of earnings.

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

After-tax GDP profits of all US businesses (percent of nominal Gross Domestic Income)

Sources: Vertical bars denote recessions and are designated by the NBER; US Department of Commerce.

Updated through 2014 Q3.

Meanwhile there’s still a lot for equity markets to digest

65

0

1

2

3

4

5

6

7

8

9

10

11

0

1

2

3

4

5

6

7

8

9

10

11

1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012 2017

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

66

Post Scripts

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

67

How Speculative Excesses Were Addressed

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

New housing starts (thousands at an annual rate) Unsold homes (months’ worth of sales)

Source: US Department of Commerce. Updated through August 2014

.

Builders had to under build ...

68

0

2

4

6

8

10

12

14

16

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

Total housing starts (left)

Unsold single family houses (right)

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Housing sales and starts (ratio to June 2005)

Source: US Department of Commerce. Updated through August 2014

.

... new and existing

69

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Sales of existing houses

Housing startsSales of new houses

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Household income and house prices (ratio to 1970)

Sources: US Dep. of Commerce; CoreLogic. Updated through 2014 Q2 (income) and 2014 Q2 (house prices).

Economic recovery and time

70

0

1

2

3

4

5

6

7

8

9

10

11

12

13

0

1

2

3

4

5

6

7

8

9

10

11

12

13

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18

CoreLogic house price index (ratio to 1970)

Gross nominal income per household (ratio to 1970)Forecast

(assumes nominal income

grows 5% annually in the coming

decade's recovery)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Rising prices are draining underwater mortgages

71

0

25

50

75

100

125

150

175

200

225

0

25

50

75

100

125

150

175

200

225

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

CoreLogic measure of house prices

Scenario above assumes that

house prices rise 4% annually in

the future.

Note: The red zone represents an estimate of the aggregate amount of under-water mortgages (see the note below)

House prices (January 2000 = 100)

Source: CoreLogic. Updated through 2014 Q2.

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Loan charge-offs (billions of dollars quarterly) Cumulative charge-offs since 2006 (billions of dollars)

Source: Federal Deposit Insurance Corporation. Updated through 2014 Q2.

Mark-to-market discipline

72

0

100

200

300

400

500

600

700

0

10

20

30

40

50

60

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Net chargeoffs by all FDIC institutions (left scale)

Cumulative "excess" net chargeoffs of all FDIC institutions since 2007 (right scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

That’s how leverage got reduced

Debt service (percent of monthly income) Household debt (ratio to income)

Source: Federal Reserve Board. Updated through 2013 Q3. 73

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

0

5

10

15

20

25

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Financial obligations (left)

Debt service (left)

Household debt (right)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

... and household net worth is back in record territory

Personal saving (percent of disposable income) Household net worth (ratio to income)

‘Sources: US Dep. of Com.; FRB. Updated through August 2013 (saving) and 2013 Q4 (net worth). 74

3.6

3.8

4.0

4.2

4.4

4.6

4.8

5.0

5.2

5.4

5.6

5.8

6.0

6.2

6.4

6.6

6.81

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Ratio of household net worth to income (right scale, reversed).

Household saving rate (left)

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Which left little market on the consumer industry

Nominal consumer spending (percentage of nominal GDP)

Source: US Department of Commerce. Updated through 2014 Q2. 75

0.57

0.58

0.59

0.60

0.61

0.62

0.63

0.64

0.65

0.66

0.67

0.68

0.69

0.70

0.57

0.58

0.59

0.60

0.61

0.62

0.63

0.64

0.65

0.66

0.67

0.68

0.69

0.70

1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

REITs stepping in as GSEs exit

Credit provided by selected (percent of all credit provided)

‘Source: Federal Reserve Board. Updated through 2013 Q3. 76

0

10

20

30

40

50

60

70

80

90

100

1949 1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

Federal Reserve System

Life Insurance and Property Casualty Companies

Private and Public Pension Funds

Securities Brokers and Dealers, Finance Companies, Funding Corporations, and Holding Companies

Money Market Mutual Funds

Mutual Funds, Closed-End Funds, Exchange-Traded Funds, and REITs

GSEs, Mortgage Pools, and Issuers of Asset-Backed Securities

Private Depository Institutions

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

77

The stagnant “secular stagnation” theory

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

78

Why the “secular stagnation” idea isn’t interesting

The economic cycle, unemployment rate (percent of the labor force)

Source: US Department of Labor. Updated through October 2014.

0

1

2

3

4

5

6

7

8

9

10

11

12

13

0

1

2

3

4

5

6

7

8

9

10

11

12

13

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Nairu (where we want to be)

Official unemployment rate (U-3)Official unemployment plus part-timers plus job-force exits under 49 years of age (U-3 ++)

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

79

The US Structural Fiscal Challenge Is About Healthcare

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

What we see isn’t what matters

Federal deficit over the most recent 12 months (percent of nominal GDP)

Note: Black boxes denote the fiscal year end.

Sources: Vertical bars denote NBER-designated recessions; US Treasury. Updated through July 2014. 80

-11

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

-11

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Forecast

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

It’s what is in our (the CBO’s) mind’s eye that’s key

Long-term revenue and spending projections (percent of GDP)

Source: Congressional Budget Office. Updated through October 2012. 81

0

5

10

15

20

25

30

0

5

10

15

20

25

30

1960 1970 1980 1990 2000 2010 2020 2030 2040 2050 2060 2070 2080

Debt service

Other

Medicare and Medicaid

Social Security

Revenues (shown holding at the historical average of 18.1% of nominal GDP)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

The fiscal issue is a healthcare issue, not a fiscal issue

Federal healthcare spending (percentage of GDP)

Source: Congressional Budget Office. Updated through 2012. 82

0.00

0.01

0.02

0.03

0.04

0.05

0.06

0.00

0.01

0.02

0.03

0.04

0.05

0.06

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

83

The Industrial Sector

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Selected trade weighted US dollar indexes (March 1973 = 100)

Source: Federal Reserve Board. Updated through July 2014.

The industrial sector has the wind at its back ...

84

75

85

95

105

115

125

135

75

85

95

105

115

125

135

1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2008 2013

Nominal trade-weighted dollar

index versus G10 countries (1972-76

= 100)

Broad real trade-

weighted dollar index

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Real GDP and industrial output (percent change from 12 months earlier)

Sources: FRB; Macroeconomic Advisers. Updated through June 2014 (IP) and May 2014 (GDP).

Industrial activity is plodding along

85

-6

-4

-2

0

2

4

6

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Manufacturing output, line (left)Industrial Output, line (left)

Real GDP, grey shaded area (right)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

ISM indexes (50+ = increasing) Real GDP (percent change from 12 months earlier)

Source: Federal Reserve Board. Updated through July 2014 (ISM) and May 2014 (GDP).

ISM sentiment surveys and the economy

86

-6

-4

-2

0

2

4

6

15

20

25

30

35

40

45

50

55

60

65

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Manufacturing ISM, line (left)Nonmanufacturing ISM, line (left)

Real GDP, grey shaded area (right)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

ISM indexes (50+ = inc) Manufacturing output (annualized percent change from 3 months earlier)

Sources: Federal Reserve Board; ISM. Updated through June 2014 (IP) and July 2014 (ISM).

ISM sentiment surveys and factory output

87

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Manufacturing ISM, line (left)Nonmanufacturing ISM, line (left)

Manufacturing output, grey shaded area (right)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Selected sectors (2007 =100)

Source: Federal Reserve Board. Updated through January 2014.

The business equipment sector

88

-20

-15

-10

-5

0

5

10

15

20

25

30

-20

-15

-10

-5

0

5

10

15

20

25

30

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Energy

High-tech equipment

Nonenergy, non-tech output Manufacturing output (shaded area)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Selected sectors (2007 =100)

Source: Federal Reserve Board. Updated through June 2014.

The energy sector is driving much now

89

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Crude oil extraction

Natural gas liquid extraction

Natural gas extraction

Oil and gas well drillingMetal ore mining

Petroleum and coal products

Chemicals

Coal miningNonmetalic mineral mining

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Selected sectors (2007 =100)

Source: Federal Reserve Board. Updated through August 2014 (output) and August 2014 (sales).

So is the motor vehicle sector

90

4

6

8

10

12

14

16

18

20

22

4

6

8

10

12

14

16

18

20

22

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Vehicle sales

Domestic vehicle output

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Capital goods orders and shipments (billions of dollars)

Source: US Department of Commerce. Updated through August 2014.

Capital goods activity

91

45

50

55

60

65

70

75

80

45

50

55

60

65

70

75

80

2007 2008 2009 2010 2011 2012 2013 2014

Orders of nondefense capital equipment excluding nondefense aircraft (line)

Shipments of nondefense aircraft

Shipments of nondefense capital equipment excluding aircraft

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Backlogs of unfilled orders (billions of dollars)

Source: US Department of Commerce. Updated through August 2014.

Backlogs of unfilled orders for capital goods

92

0

50

100

150

200

250

300

350

400

450

500

550

600

650

0

50

100

150

200

250

300

350

400

450

500

550

600

650

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Backlogs of (military and nondefense) aircraft orders

Backlogs of nondefense capital goods other than aircraft

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Backlogs of unfilled orders (months’ supply)

Source: US Department of Commerce. Updated through August 2014.

Backlogs of unfilled orders for capital goods

93

10

20

30

40

50

60

70

80

2

3

4

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Backlogs of (military and nondefense) aircraft orders

Backlogs of nondefense capital goods other than aircraft

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Selected sectors (2007 =100) Factory utilization rate (percent)

Source: Federal Reserve Board. Updated through June 2014.

The industrial sector still has unused capacity

94

60

65

70

75

80

85

90

95

100

20

30

40

50

60

70

80

90

100

110

1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

Manufacturing output (left scale)

Manufacturing capacity utilization (right scale)

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Factory payrolls (millions)

Sources: Vertical bars denote recessions and are designated by the NBER; US Department of Labor. Updated

through July 2014.

... but it will look different

95

10

11

12

13

14

15

16

17

18

19

20

1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012

10

11

12

13

14

15

16

17

18

19

20

Full Employment or Bust

Global Economic Outlook Issues, 51st Annual Economic Forecast Luncheon, Chase-W. P. Carey School of Business, Arizona State University, Phoenix, Arizona, December 3, 2014.

Prices of oil and natural gas, thermally-equivalent comparison (dollars per barrel)