FROM QUALITY TO SERVICE TO SUCCESS - … Pharma MNE Wholesale ... Separate strategy-driven...

42

FROM QUALITY TO SERVICE TO SUCCESS Belgrade, 31/03/2014

-

Upload

vuongkhanh -

Category

Documents

-

view

214 -

download

2

Transcript of FROM QUALITY TO SERVICE TO SUCCESS - … Pharma MNE Wholesale ... Separate strategy-driven...

FROM QUALITY TO SERVICE TO SUCCESS

Belgrade, 31/03/2014

Agenda

1. Outline of the PHOENIX Group

2. PHOENIX Group in the Balkans

3. What makes a successful company ?

4. The invisible Edge : innovation

5. The invisible Edge: cost efficiency

6. The invisible Edge: winning business model

7. What does a business leader do?

2

1. OUTLINE OF THE PHOENIX

GROUP

PHOENIX Group at a glance

4

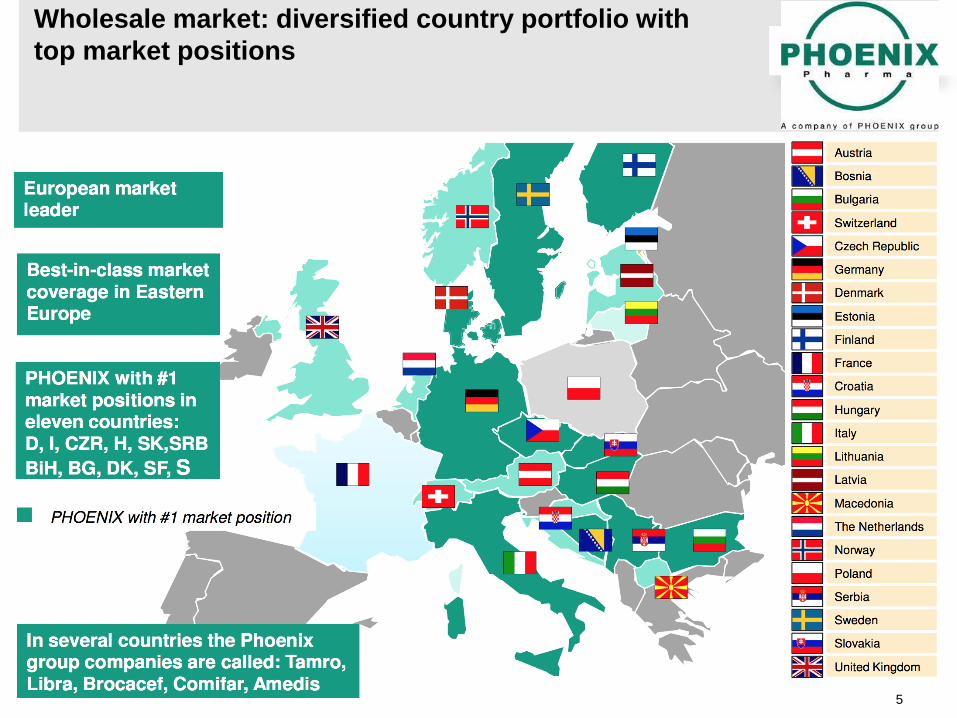

Wholesale market: diversified country portfolio with

top market positions

5

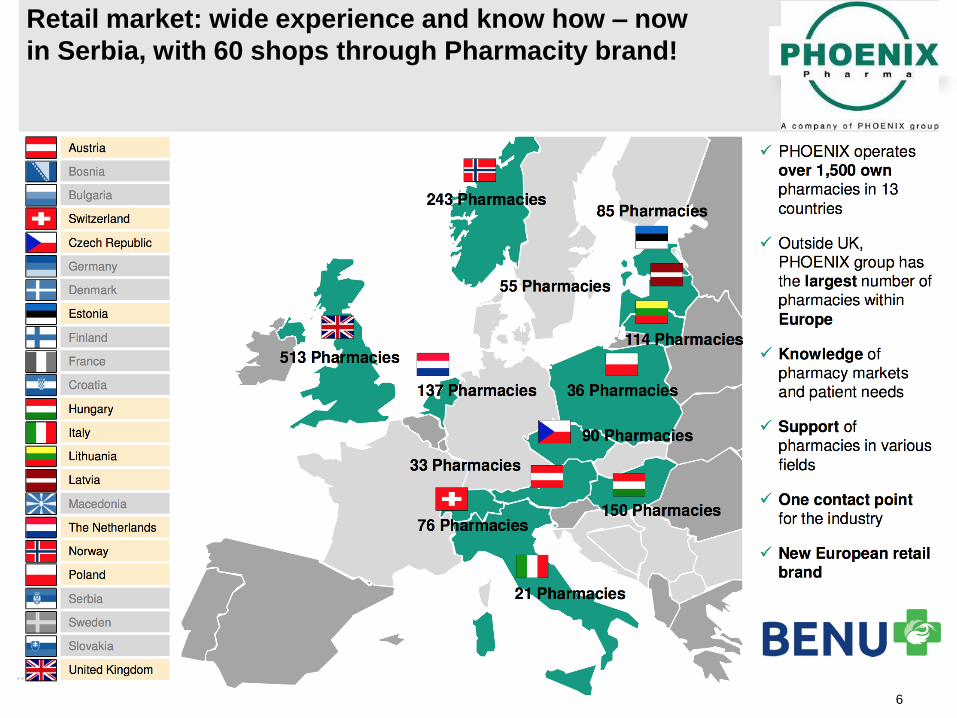

Retail market: wide experience and know how – now

in Serbia, with 60 shops through Pharmacity brand!

6

2. PHOENIX GROUP IN THE

BALKANS

Balkan group corporate development timeline - From Wholesale regional leader to Pharma services regional

leader to starting our retail operations

2014

Retail

Serbia

transmed

Balkan

region

2008 2009 2010 2011 2012

Acquisition

PHOENIX

Serbia

Acquisition

Evropa Lek

Serbia

Acquisition

PHOENIX

Macedonia and

Libra Serbia

Acquisition

PHOENIX

Bosnia

Open

Evropa Lek

Bosnia &

Macedonia

Open

Evropa Lek

Kosovo and

Montenegro

Acquisition

InoPharm

Merger

Bomil

Farm

subsidiary

Wholesale

carve out

Evropa Lek

Asset

acquisition

Zdravlje

Trade

Merger

Libra

Serbia to

Evropa Lek

Trf Macedonia

from Serbia to

PHOENIX Pib

Austria

transmed

Serbia

2013

Open

Evropa Lek

Albania

Merge Bulgarian

activities to

become Balkan

group

8

PHOENIX Pharma MAC

PHOENIX Beteiligung

PHOENIX Pharma BG

Libra pharma

PHOENIX PiB Austria

PHOENIX Pharma BiH PHOENIX Pharma SRB BENU

EL Pharma BiH

EL Pharma ALB

EL Pharma KOS

EL Pharma MAC

EL Pharma SRB

EL Pharma MNE

Wholesale

Pharma services Retail

Balkan group corporate structure

- Thirteen companies managed through three holding companies

9

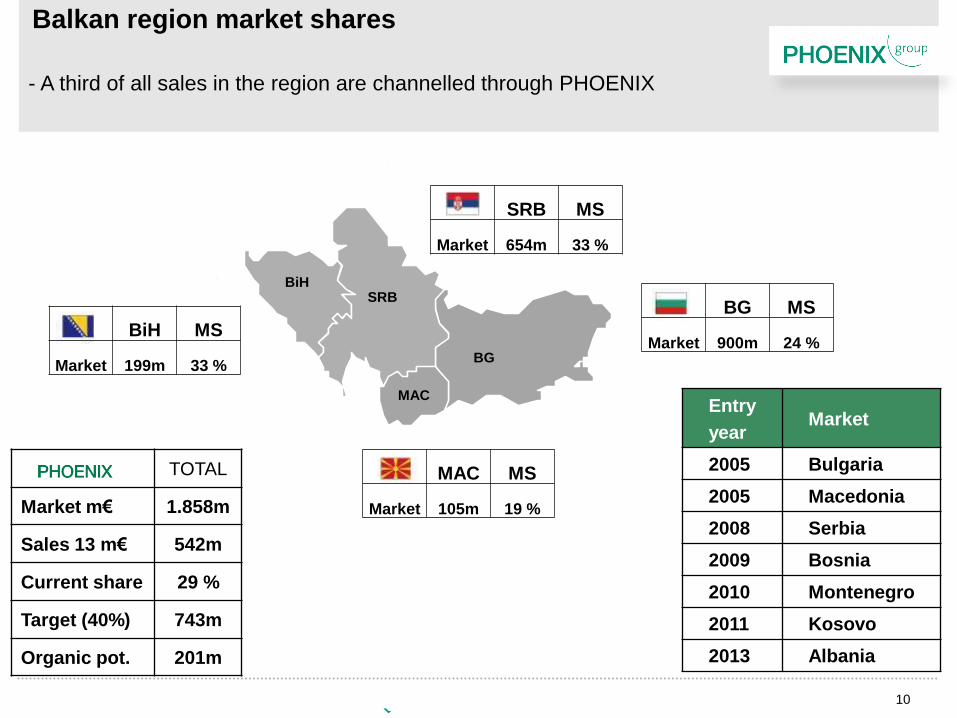

Balkan region market shares

BiH SRB

BG

MAC

TOTAL

Market m€ 1.858m

Sales 13 m€ 542m

Current share 29 %

Target (40%) 743m

Organic pot. 201m

- A third of all sales in the region are channelled through PHOENIX

Entry

year Market

2005 Bulgaria

2005 Macedonia

2008 Serbia

2009 Bosnia

2010 Montenegro

2011 Kosovo

2013 Albania

BiH MS

Market 199m 33 %

SRB MS

Market 654m 33 %

MAC MS

Market 105m 19 %

BG MS

Market 900m 24 %

10

Creating Sustainable profitable growth

MAT Net sales development

11

3. WHAT MAKES A

SUCCESSFUL COMPANY ?

Increased penetration in sales

channels through regional focus

Remain the No1 market leader

Strategy Improving the quality of our

assortment through selective

partnerships with suppliers

Objective

Develop beyond supply to demand

services

Investment in the development of our

people and our processes

Keep your strategy simple and easy to communicate

13

STRATEGY: Increased penetration in sales channels - Sales channel strategic focus

2012 2013 2014

Grow aggressively Private

pharmacies State pharmacies

Private pharmacies

Grow selectively State pharmacies Private pharmacies

State pharmacies

Maintain

aggressively Hospitals

Maintain selectively Hospitals

Hospitals

Divest/ exit Wholesalers

Question mark

14

Brand Portfolio

Balkan Region

Wholesaler - Bosnia

- Macedonia

- Serbia

- Bulgaria (rebrand)

Loyalty program - Bosnia

- Serbia

- Macedonia

- Bulgaria

Retail - Serbia

Transport Services - Serbia

- Macedonia

- Bosnia

Pharma Services - Bosnia

- Macedonia

- Serbia

- Montenegro

- Kosovo

- Albania

- Bulgaria (Libra Pharma)

Develop a winning brand portfolio

- The Brand portfolio Balkan Region

PHABIS - Serbia

- Bulgaria

- Bosnia

- Macedonia

15

Develop long term plans

- Long-term planning - Development Graphs

16

4. THE INVISIBLE EDGE:

INNOVATION

Introducing a B to C marketing concept in order to

change the pharmacy market in the Balkan

BETTER PHARMACY

BETTER SERVICE

BETTER BUY

BETTER BUSINESS

BETTER HEALTHCARE

BETTER LIFE

SIMPLY BETTER…

18

Shaping markets takes dedication and planning - easy when it is your destiny…..

COVERAGE

IT SYSTEM and VISUAL IDENTITY

CATEGORY MANAGEMENT AND LOYALTY CARDS

LAYOUT AND PHARMACY INTERIOR

19

Changing the market will create long term rewards

- Loyalty of both consumers and customers….

from

to

20

Bolja komunikacija

Smanjenje troškova

Povećanje produktivnosti

Zaposleni

Upravnik

Vlasnik

Stvaramo lojalne kupce

EduPharma A K A D E M I J A

Know-how is key to affecting change

21

Changing our approach and collaboration with suppliers

PHOENIX

current position

Transactional Relational

Trading Field selling KAM/category Mngt ECR Partnership

Pricing & trade

terms

Generate volume Conditional rebates Enhance margin Direct product profitability

X

Collaboration Price negotiation only Ad-hoc Win-Lose Planned mutual benefit Open-book

X

Delivery Direct to consignee Direct import Consignment stock

Regional consignment

stock

X

Relationship Buyer/seller only

Buyer/seller & activity

planning (only)

Multi functional planning &

execution of activity

Multi-level and cross

functional management

X

Information

sharing

None/little Some shared research and

top line sales information

Limited EDI in transactions

and sales information only

Seamless EDI and EPOS

interfaces and shared

access

X

Business Planning No/little coordination

Separate strategy-driven

approaches

Jointly activity planning &

sharing of performance

analyses

Joint strategy, planning,

execution & measurement

full ECR scorecard

X

22

segment strategy Imp 1 (by Q113) Imp 2 (by Q313) Plan (by Q114)

Optimize

demand

Efficient use of market data New customer

classification Market analiysis

Efficient promotions (number and type for category

growth)

Promo planning system Efficient promotional

analysis

High innovation capacity

Efficient transaction every day (flow of info, goods,

money) TELEMARKETING TELEMARKETING TELEMARKETING

Tools to create customer loyalty BETTY BETTY BETTY

Efficient introductions Internet training Field force advance

Secure

Supply

High innovation capacity

Stable product quality every day Product category

analysis

Efficient assortment

analysis

Reduction of SKU’s per

category

Fast and accurate customer complaint handling Customer complaints

manage

Efficient assortment (right SKU’s for consumer

demand)

Out of stocks analysis

and reduction

SKU for efficient

promotions

Align strategy

Understanding and alignment with top 10 suppliers

Pricing strategy which stimulates good behavior Pricing strategy

Understanding and alignment with top 10

customers

Customer profitability

analysis

Customer training

platform

Enable the

team

Decision mapping to make business building

proposals

SharePoint platform

for data sharing

High market knowledge (customers, competitors) Stakeholder organ

mapping with platform

Financial analysis within

platform

Knowledge of best industry practices

Creating an innovation process…

….creativity and innovation momentum is achieved….

23

5. THE INVISIBLE EDGE: COST

EFFICIENCY

Productivity reporting

- Not a dirty word – the way winning economies measure performance

72,18

LE 76,53

62,08

BJ 69,71 69,77

SJ 73,28

71,70

SK 74,43

60,84

NS 62,40

72,16

BG 77,38

64,81

BIH 71,17

69,08

SRB 72,99

68,47

BMS Group 72,78

72,78

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

90

0 5.000 10.000 15.000 20.000 25.000 30.000 35.000 40.000

[lin

es

/ho

urs]

[lines / days]

25

Using tools to measure financial performance

- budgets...forecasts...variance analysis....

-938.812

-689.933

-361.798

-105.993

-34.269

-30.763

-77.854

BU 2014/15

Transport

Lease

Marketing

Other

F2 2013/14

YE 2012/13

Comments

Transport: transmed

effect (items below

EBITDA line transfered

to transport expenses)

Marketing: 57 MRSD

Betty effect

Lease: Leskovac

bulding effect (sold and

leased back)

Other: Fx

compensation from

suppliers not budgeted

26

Credit management as a core tool

- A sale is not a sale until it is cashed in…

Please insert 4 field diagram

27

Balance sheet reporting – focus on NWC

- the best way to optimize business performance

PY 2013/14 BU 2014/15 AC 2014/15 AC - BU PY 2013/14 BU 2014/15 AC 2014/15 AC - BU

Index Index

Inventories before stock provisions 16.431 20.392 18.107 -2.285 88,8 16.551 21.449 17.945 -3.504 83,7

Stock days 45,16 52,78 46,01 -6,77 87,2 45,49 55,52 45,60 -9,92 82,1

Gross trade receivables incl. notes 52.330 52.758 60.866 8.108 115,4 52.028 52.709 59.346 6.638 112,6

Sold under ABS / Factoring (off balance)

Total trade receivables before ABS / Factoring 52.330 52.758 60.866 8.108 115,4 52.028 52.709 59.346 6.638 112,6

Debtor days 143,84 136,56 154,66 18,10 113,3 143,01 136,43 150,80 14,36 110,5

Trade payables ST 39.267 42.634 43.776 1.142 102,7 39.672 42.510 43.043 534 101,3

Creditor days 107,94 110,36 111,23 0,88 100,8 109,05 110,03 109,37 -0,66 99,4

Net Working Capital 29.494 30.516 35.197 4.681 115,3 28.907 31.648 34.248 2.600 108,2

NWC days 81,07 78,99 89,43 10,45 113,2 79,46 81,92 87,02 5,10 106,2

Turnover w/o turnover service fees/other 21.828 23.180 23.613 433 101,9 21.828 23.180 23.613 433 101,9

* Calculated as average of AC 1302 to AC 1307 + F1 1310 + F1 1401

End of period Average

28

Investment analysis – where do i put my money? - Return on Capital Employment

Year to Date

AC 2013/14 BU 2014/15 AC 2014/15 AC - BU

Index

EBIT 368 976 616 -360 63,1

Intangible Assets (including Goodwill*) 11.101 10.443 10.475 33 100,3

Property, plant and equipment 2.515 3.749 3.594 -156 95,9

Participations

Tax claims income taxes LT

Non-financial fixed assets 13.615 14.192 14.069 -123 99,1

Inventories 16.447 21.421 17.852 -3.569 83,3

Trade receivables total 51.563 52.140 58.688 6.549 112,6

Prepaid expenses 444 954 835 -119 87,5

Other assets 2.150 2.061 742 -1.319 36,0

Tax claims - income taxes

Interest free current assets 70.603 76.574 78.116 1.542 102,0

Sold under ABS / Factoring (off balance)

Considered assets 84.218 90.766 92.185 1.419 101,6

Provisions for taxes

Other current provisions 42 48 55 8 115,8

Other provisions LT

Accruals for personnel costs LT

Non-current interest free liabilities

Trade payables ST 39.672 42.510 43.043 534 101,3

Other liabilities ST 2.343 734 1.212 479 165,2

Other liabilities LT

Deductible positions 42.056 43.291 44.310 1.020 102,4

Capital employed * 42.162 47.475 47.875 400 100,8

ROCE 5,24% 12,33% 7,72% -4,61% 62,6

* on Subgroup and higher level

** Average calculation of the respective periods

29

6. THE INVISIBLE EDGE:

WINNING BUSINESS MODEL

In order to create a sustainable competitive advantage we

need to develop BENU’s positioning as a

National pharmacy chain

Market leader in retailer formats pharmacy segment

Market leader as local neighborhood pharmacy

How?

Through acquisition of the chains which dominate retailing

format segment

Through acquisition of two chains already well positioned

as local neighborhood pharmacies, then through selective

add-ons

5

2

2

10

2 9 4 2

11

25

2

14 3

Total

shops

Market

total 7 8 3 13 10 15 3 2 61 (100%)

Celsius 6 7 1 14 (23%)

Pharmacity 1 4 7 12 (20%)

Leut SI 1 5 2 1 9 (15%)

Primax 3 3 ( 5%)

Total

(BENU) 6 7 1 7 6 7 3 1 38 (62%)

Pharmacity

Oaza zdravlja

Celsius

Primax

Leut SI

Our pharmacy strategy

- Building a national retail chain through selected acquisitions to create a

sustainable leadership position

Retailer

Pharmacy

31

Pharmacity is growing on strong pace, plenty of potential remains within retailer formats 18 pharmacies opened from June 30th

Contract with the Delthaize taken over from Celsius pharmacy chain, delivering 11 pharmacies and expansion plan

DIS is continuing expansion throughout Serbia, Pharmacity is following on preferred partnership basis

Delivering our strategy

- Focusing on the retail segment – growing and winning segment

Our flagship pharmacy in Delta City shopping mall With potential to become a 1mn EUR pharmacy in 2014

Pilot project with METRO initiated in July Potential for 8 additional pharmacies in 2014

Total

Market total 10 8 3 34 23 15 5 10 11 119

Pharmacity Oct 5 6 1 4 10 2 28 (24%)

32

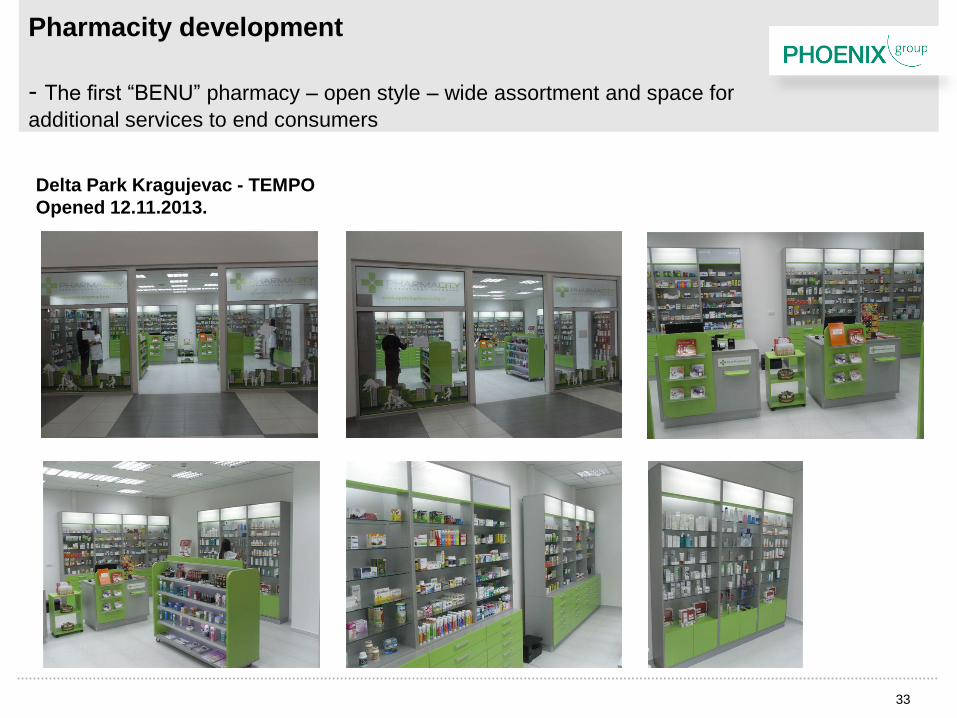

Pharmacity development

- The first “BENU” pharmacy – open style – wide assortment and space for

additional services to end consumers

Delta Park Kragujevac - TEMPO

Opened 12.11.2013.

33

The widest service offer in the market

- We continue to develop our services in each market

SALES SUPPORT

SOLUTIONS

PRE-WHOLESALE

SOLUTIONS

REGULATORY

AFFAIRS

MARKETING

FIELD FORCE

INTERVENTION

IMPORT

CONSIGNMENT

CLINICAL TRIALS

LOGISTICS

LABELLING

DISTRIBUTION

SRB BIH BG

SRB

SRB BIH MAK

KOS MAK

BIH

BG

MNE SRB

SRB MNE

MAK KOS

BG BIH MAK SRB

BIH

SRB

SRB

MNE BG

BIH MAK

MAK

MNE BG

BIH KOS

MAK

34

The business model is based on a new business

stream and cross selling services to current clients

SALES SUPPORT

SOLUTIONS

PRE-WHOLESALE

SOLUTIONS

REGULATORY

AFFAIRS

MARKETING

FIELD FORCE

INTERVENTION

IMPORT

CONSIGNMENT

CLINICAL TRIALS

LOGISTICS

LABELLING

DISTRIBUTION

35

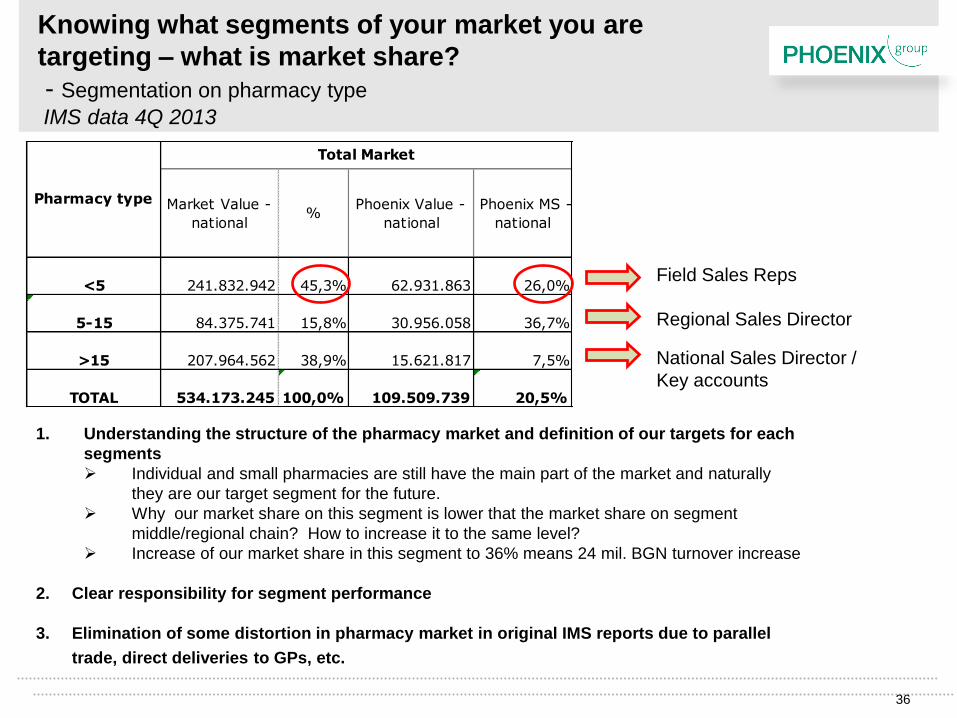

Knowing what segments of your market you are

targeting – what is market share?

- Segmentation on pharmacy type

IMS data 4Q 2013

Market Value -

national%

Phoenix Value -

national

Phoenix MS -

national

<5 241.832.942 45,3% 62.931.863 26,0%

5-15 84.375.741 15,8% 30.956.058 36,7%

>15 207.964.562 38,9% 15.621.817 7,5%

TOTAL 534.173.245 100,0% 109.509.739 20,5%

Pharmacy type

Total Market

1. Understanding the structure of the pharmacy market and definition of our targets for each

segments

Individual and small pharmacies are still have the main part of the market and naturally

they are our target segment for the future.

Why our market share on this segment is lower that the market share on segment

middle/regional chain? How to increase it to the same level?

Increase of our market share in this segment to 36% means 24 mil. BGN turnover increase

2. Clear responsibility for segment performance

3. Elimination of some distortion in pharmacy market in original IMS reports due to parallel

trade, direct deliveries to GPs, etc.

Field Sales Reps

Regional Sales Director

National Sales Director /

Key accounts

36

7. WHAT DOES A BUSINESS

LEADER DO?

The life of a CEO……

38

The life of a CEO……

.......is far too busy.......

39

So we have to set priorities……

50% of time is

spent on

Operational

Strategy

50% of time is

spent on

Organizationa

l Strategy

40

Organizational strategy…..

- How to implement your winning best practice....

Our people

How are they

organized?

How are they

developed?

What

opportunities do

they have?

Where are they

placed?

Have they the

right training?

Do they have

what they need?

41

THANK YOU

![MNE Det[1]](https://static.fdocuments.us/doc/165x107/577d2e0a1a28ab4e1eaea763/mne-det1.jpg)