Foreign Direct Investments 1218215823748473 9

33

Foreign Direct Investments By Prof. Augustin Amaladas M.Com., AICWA.,PGDFM.,DIM.,B.Ed.

-

Upload

roopendrawardlaw -

Category

Documents

-

view

224 -

download

0

Transcript of Foreign Direct Investments 1218215823748473 9

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 1/33

Foreign Direct Investments

By

Prof. Augustin AmaladasM.Com., AICWA.,PGDFM.,DIM.,B.Ed.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 2/33

definition

• FDI is defined as a company from one

country making a physical investment into

building a factory in another country. Itsdefinition can be extended to include

investments made to acquire lasting interest

in enterprises operating outside of theeconomy of the investor.[1]

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 3/33

Minimum Requirements

In order to qualify as FDI the investment

must afford the parent enterprise control

over its foreign affiliate. The UN definescontrol in this case as owning 10% or more

of the ordinary shares or voting power of an

incorporated firm or its equivalent for anunincorporated firm; lower ownership

shares are known as portfolio investment.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 4/33

Reasons for FDI

• economic growth, de-regulation, liberal

investment rules, and operational

flexibility.All the factors that helpincrease the inflow of Foreign Direct

Investment.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 5/33

Types of Foreign collaboration

agreements• Joint ventures

• Technical collaborations

• Setting up of branches/project office

• FDI- investment by non-residents and

overseas corporate bodies.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 6/33

Foreign collaboration agreements

• 1. Technical collaboration agreements

• 2.Financial and technical collaboration

agreements

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 7/33

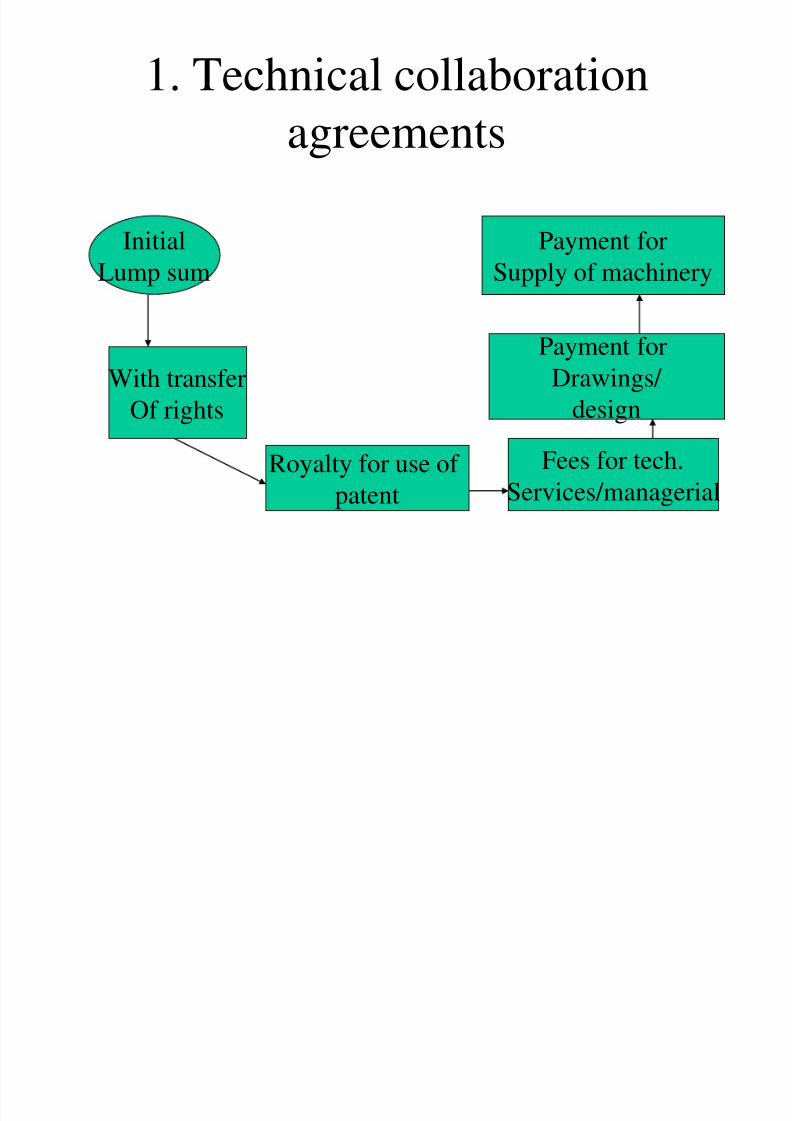

1. Technical collaboration

agreements

Initial

Lump sum

With transfer

Of rights

Royalty for use of

patent

Fees for tech.

Services/managerial

Payment for

Drawings/

design

Payment for

Supply of machinery

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 8/33

2. Financial and technical

collaboration agreements• In addition to technical agreements makes

investment in the capital of the Indian

collaborator besides transfer of technology• The collaborator receives payments and also

dividend on shares/Interest on money lent.

• Such collaboration should match withpolicies of Government of India.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 9/33

Tax Implications of foreign

collaboration• 1. In the hands of Foreign collaborator

• 2. In the hands of Indian collaborator

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 10/33

Important sections as per IT Act

• Section 44AD-computation of income who is engaged in the business of

civil construction if gross receipt does not exceed Rs.40 lakhs-8% of the

gross receipts paid /payable to the tax payer.

• Section 44DA-Computation of income by way of royalties and technical

service fees in the case of foreign companies if agreements made after

March 31st, 1976 but before 1-4-2003., -ia-10% tax on royalty

payable/paid.

• If agreement after March 31, 2003 where royalty or technical fees is

effectively connected to Permanent establishment(PE) in India-10%

• 30% -agreement made before june 1, 199720% after May 31, 1997 but before June 1, 2005.

•

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 11/33

115A, 115AB, 115AC, 115AD,

115BBA and 115D

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 12/33

Foreign Collaborator Indian Collaborators

1.Non residents-Income received,deemed to be received and accrued,

or deemed to accrue in India-

taxable

2.Exempted income U/S 10 of IT

Act.3. Special computation of Income

u/s 44DA, 115A, 115AB, 115AC

and 115AD

4.Double taxation avoidance

agreements.

1.Revenue expenditure-deduction isallowed.

2. Capital expenditure-depreciation

u/s 32 is allowed.

3. Payment to foreign personnel in

India-installation of equipment-

capitalised-depreciation allowed.4.Training expenditure-allowed

deduction

5.Payment for acquisition of plantand machinery-depreciation allowed

6.Interest-allowed deduction u/s

36(1)(iii)

6. Interest paid to acquire capital

asset-capitalised upto the date of putinto use/ready to use.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 13/33

Tax planning• 1. Do not allot shares as dividend paid outside India tax to be deducted at source

and deemed to receive in India.

• 2. Foreign collaborator should be a company registered outside India as theybecome non-resident in India. If it is a partnership firm entire control andmanagement should be outside India.

• 3. Separate contract for separate work. Each job like supply of plant andmachinery, installation, supply of design, patents, trade mark.

• 4.Property in goods to pass on outside India- foreign collaborator need not pay

tax in India as the ownership passed outside India.The goods shipped in the nameof the Indian company.

• 5.Make payments abroad. Acceptance of payments through banks in India shouldbe avoided. But tax liability can not be reduced for the payments of royalty,dividend, Interest, technical services .

• 6.Spare parts – there should be a separate agreement and should be supplied only

after the year of commissioning of plant and machinery

• 7.Salary to foreign technicians- paid in India is taxable but daily allowances andliving allowances are exempt u/s10(14) to the extent expended.

• 8.The foreign technician should not stay more than certain number of days inIndia

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 14/33

Tax planning for Indian

collaborators• 1.Capitalisation of installation expenses provided

the business setup before such expense incurred

• 2.Treating purchase of spares as revenueexpenditure-make separate contract and receive

such spares only in the year subsequent to the year

of commissioning.

• 3. Claim depreciation on plans and drawings.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 15/33

Important Notes

• 1. Technical collaboration fees attract-20% TDSu/s 115A.Otherwise it is 40% tax.

• 2.If total income of a foreign company does notexceed 1 crore-no surcharge.

• 3.TDS paid by Indian company on behalf of foreign company for royalty payable under the

terms of an agreement entered before 1st

June2002 relating to matter included in Industrialpolicy is exempt from tax u/s 10(6A)[Grossing theincome is not required.]

C t d 1

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 16/33

Case study-1

• 1. S Ltd a foreign company entered into an agreement with K ltd. an

Indian company.This agreement is related to industrial policy of the

central government and is in accordance with the policy. The royalty paid

by K ltd is 100 lakh to S ltd.compute the tax payable by S ltd.under the

following circumstances.

• A) K ltd pays Income tax payable by S ltd.as per the terms of agreement

entered before 1st June 2002.

• B) The agreement does not provide that K ltd will bear the tax but

understanding that 100 lakh is net of tax.

• C) The agreement entered on 1st June 2006.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 17/33

-1

A) No grossing up is required as it was entered into an agreement before

1st June 2002 and the agreement indicates the TDS.

Total Income 100 lakhs

Tax on royalty @20.6%(20%+3%) 20.6 lakhs

B) Royalty income 100 lakhs

(net)

Gross income (100 lakhs x 100/(100-20.6)=125.945 lakhsTax to be paid (125.945 lakhs x 20.6%) =25.945 lakhs.

(Since the agreement does not indicate the TDS we have to grossing up the

income.)

C) If agreement entered on after 1st June 2002 grossing up of Income is

required.The amount of tax payable by K ltd, on behalf S ltd. will otbe exempt under section 10(6A).

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 18/33

Case study-2

Shanthi Ltd.a foreign company entered into a collaboration agreement on 1st

June 2006 with an Indian company and was in receipt of the following

payments during the previous year 2007-08.a) Interest on 10% debentures of Rs.100 lakhs issued by Indian company

on 1st January 2008 in consideration of providing of technical

knowhow, manufacturing process and designs.

b) Services charges @ 2.5% of the value of plant and machinery for

Rs.800 lakhs leased out to Indian company payable each year before31st March,

c) How do you deal with them for computation in case of Shanthi Ltd.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 19/33

Answer-2

• Since debentures issued for technical services and service charges amounts

to royalty which is paid by an Indian company it shall be deemed to accrue

or arise in India as per section 9(1)(v),( vi),(vii).It is taxed u/s 115A.It istaxed at 20% rate. Otherwise they are taxed at 40% rate.

• Income to be taxed-debentures 100 lakhs x20%=10 lakhs

• Interest on debentures (3 months)100 x10% x3/12 x20% = 0.5 lakhs

• Service charges (800 lakhs x 2.5% x20% =4.0 lakhs• Total tax before education cess =14.5 lakhs

• Educational cess[3% x14.5 lakhs] = 0.435 lakhs

• Total tax liability = 14.935 lakhs

• Note:No surcharge is imposed as the total income does not exceed for the

foreign company rupees 1 crore.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 20/33

• FDI or Foreign Direct Investment is any

form of investment that earns interest in

enterprises which function outside of thedomestic territory of the investor.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 21/33

• FDIs require a business relationship between a

parent company and its foreign subsidiary.

Foreign direct business relationships give rise tomultinational corporations. For an investment to

be regarded as an FDI, the parent firm needs to

have at least 10% of the ordinary shares of its

foreign affiliates. The investing firm may alsoqualify for an FDI if it owns voting power in a

business enterprise operating in a foreign country.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 22/33

• Types of Foreign Direct Investment: An

Overview

• FDIs can be broadly classified into two types:outward FDIs and inward FDIs. This classification

is based on the types of restrictions imposed, and

the various prerequisites required for these

investments.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 23/33

•

Vertical Foreign Direct Investment takes place

when a multinational corporation owns someshares of a foreign enterprise, which supplies input

for it or uses the output produced by the MNC.

Horizontal foreign direct investments happenwhen a multinational company carries out a

similar business operation in different nations.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 24/33

• An outward-bound FDI is backed by thegovernment against all types of associated risks.This form of FDI is subject to tax incentives aswell as disincentives of various forms. Risk coverage provided to the domestic industries andsubsidies granted to the local firms stand in theway of outward FDIs, which are also known as

“direct investments abroad.”

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 25/33

Economic factors-Inward FDI

• These include interest loans, tax breaks,

grants, subsidies, and the removal of

restrictions and limitations. Factorsdetrimental to the growth of FDIs include

necessities of differential performance and

limitations related with ownership patterns.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 26/33

real estate sector

• The Government of India in March 2005 amendedexisting norms to allow 100 per cent FDI in theconstruction business. This liberalization actcleared the path for foreign investment to meet thedemand into development of the commercial andresidential real estate sectors. It has alsoencouraged several large financial firms andprivate equity funds to launch exclusive fundstargeting the Indian real estate sector.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 27/33

• Until now, only Non Resident Indians (NRIs) and Persons of Indian Origin (PIOs)

were permitted to invest in the housing andthe real estate sectors. Foreign investorsother than NRIs were allowed to invest onlyin development of integrated townships and

settlements either through a wholly ownedsubsidiary or through a joint venturecompany in India along with a local partner.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 28/33

Foreign players

• Lee Kim Tah Holdings,

• CESMA International Pvt Ltd.,

• Evan Lim,• and Keppel Land from Singapore,

• Salim Group from Indonesia,

• Edaw Ltd., from USA,

• Emaar Group from Dubai,

• IJM, Ho Hup Construction Co., from Malaysiaetc.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 29/33

Motives

• Foreign Direct Investment is guided by differentmotives. FDIs that are undertaken to strengthenthe existing market structure or explore the

opportunities of new markets can be called“market-seeking FDIs.” “Resource-seeking FDIs”are aimed at factors of production which havemore operational efficiency than those available in

the home country of the investor.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 30/33

• Some foreign direct investments involve thetransfer of strategic assets. FDI activities

may also be carried out to ensureoptimization of available opportunities andeconomies of scale. In this case, the foreigndirect investment is termed as “efficiency-

seeking.”

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 31/33

Real estate is on the high

growth path•

In 2003-04, India received total FDI inflow

of US$ 2.70 billion, of which only 4.5%was committed to real estate sector. In

2004-05 this increased to US$ 3.75 billion

of which, the real estate shares was 10.6%.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 32/33

2005-06

• However, in 2005-06, while total FDIs in

India were estimated at US$ 5.46 billion,

the real estate share in them was around16%. The Study, nevertheless projects that

in 2006-07, total FDIs will touch about US$

8 billion in which the real estate share isestimated to be about 26.5%.

8/2/2019 Foreign Direct Investments 1218215823748473 9

http://slidepdf.com/reader/full/foreign-direct-investments-1218215823748473-9 33/33