Fixed-Mobile Interconnection Issues - TT Dec fixed-mobile.pdf · Fixed-Mobile Interconnection...

27

Fixed Fixed - - Mobile Interconnection Mobile Interconnection Issues Issues The views expressed in this paper are those of the author and do not necessarily reflect the opinions of the ITU or its Membership. Dr Kelly can be contacted by e-mail at [email protected] Dr Tim Kelly, ITU Workshop on international settlement reform and the costing and pricing of telecom services, Hanoi, 11-13 December 2000

-

Upload

nguyenxuyen -

Category

Documents

-

view

222 -

download

0

Transcript of Fixed-Mobile Interconnection Issues - TT Dec fixed-mobile.pdf · Fixed-Mobile Interconnection...

FixedFixed--Mobile Interconnection Mobile Interconnection IssuesIssues

The views expressed in this paper are those of the author and do not necessarily reflect the opinions of the ITU or its Membership. Dr Kelly can be contacted by e-mail at [email protected]

Dr Tim Kelly, ITU�Workshop on international settlement reform and the

costing and pricing of telecom services�, Hanoi,

11-13 December 2000

Fixed-Mobile Interconnection Issues

Pricing mobile services:Pricing mobile services:AgendaAgenda

� A Mobile Revolution! Worldwide and in the sub-region

� Pricing Mobile! Options! Price comparisons and trends! Price trends! Average Revenue Per User (ARPU)

� Fixed-Mobile Interconnect� A Mobile Future

A Mobile RevolutionA Mobile Revolution

Source: ITU World Telecommunication Indicators Database.

0

200

400

600

800

1'000

1'200

1'400

1993 1995 1997 1999 2001 2003

Mobile UsersFixed Lines

Fixed Lines vs. Mobile Users, worldwide, Million

Mobile subscribers Mobile subscribers per 100 inhabitants per 100 inhabitants

YearYear--end 1999end 1999SubSub--regionregion

Source: ITU World Telecommunication Indicators Database.

13.70

3.84

3.42

3.66

1.22

1.06

0.81

0.42

0.17

Malaysia

Thailand

China

Philippines

Sri Lanka

Indonesia

Cambodia

Viet Nam

Lao P.D.R.

Mobile subscribers Mobile subscribers as % of total as % of total

telephone telephone subscribers subscribers

YearYear--end 1999end 1999SubSub--regionregion

Source: ITU World Telecommunication Indicators Database.

76.3%

48.5%

40.3%

31.0%

28.5%

26.8%

25.1%

20.8%

13.5%

Cambodia

Philippines

Malaysia

Thailand

China

Indonesia

Sri Lanka

Lao P.D.R.

Viet Nam

Fixed-Mobile Interconnection Issues

The secret of mobile success" Why is mobile currently growing ten times

faster (~55% p.a.) worldwide than fixed lines networks (~5.5% p.a.)?

" Why is the average mobile user much youngerthan the average fixed-line user?

" Why do users make calls using a mobilephoneeven when a fixed-line telephone is available and cheaper?

" What is the secret of the success of mobile?

Price Options

Plan name Monthlycharge for

single phone

Standard talktime included(per month)

Peak timecall charges(per minute)

Off-peakcall charges(per minute)

Chat 60 £17.63 60 off-peakminutes

40p 5p

Talk 30 £17.50 30 minutes 30p 5pTalk 120 £25.00 120 minutes 24p 5pTalk 400 £58.75 400 minutes 22p 5p

Talk 1300 £176.25 1�300 minutes 17p 5pTalk 3700 £470.00 3�700 minutes 15p 5pTalk 7500 £940.00 7�500 minutes 15p 5p

Everyday 50 50p/day 50 minutes/day 40p 1p

A selection of price optionsA selection of price optionsFrom Orange (UK)From Orange (UK)

Source: http://www.uk.orange.net/kit/index.html.

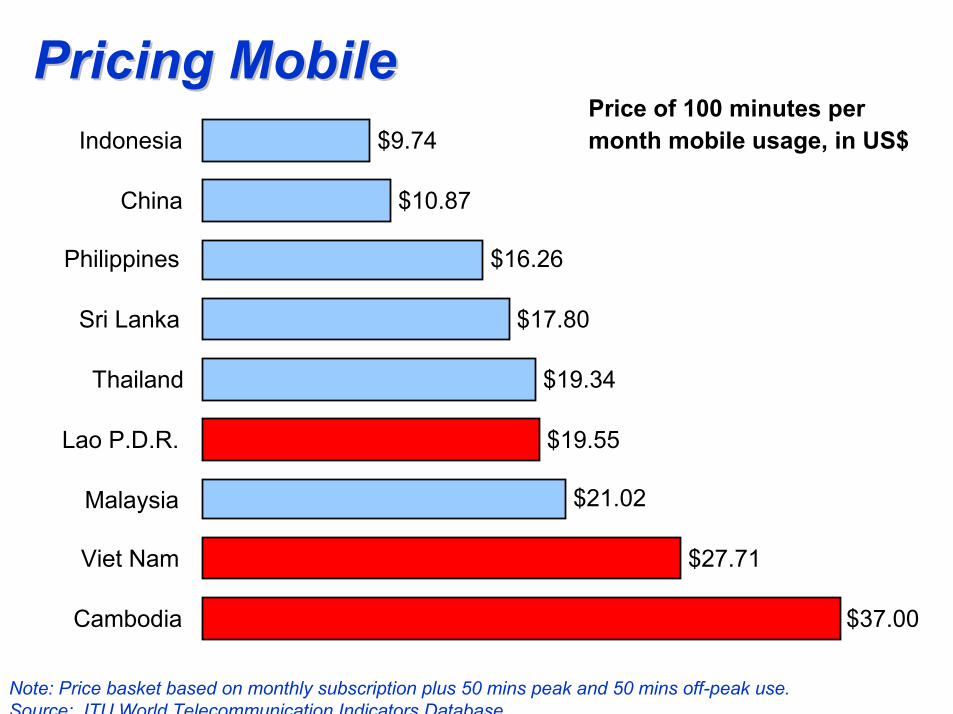

Pricing MobilePricing Mobile

Note: Price basket based on monthly subscription plus 50 mins peak and 50 mins off-peak use.Source: ITU World Telecommunication Indicators Database.

$37.00

$27.71

$21.02

$19.55

$19.34

$17.80

$16.26

$10.87

$9.74

Cambodia

Viet Nam

Malaysia

Lao P.D.R.

Thailand

Sri Lanka

Philippines

China

IndonesiaPrice of 100 minutes per month mobile usage, in US$

Declining prices for mobile access, global average, in US$, 1992-98

547

410

231180

1992 1994 1996 1998

Connection charge, US$

CAGR, 1992-98 = -16.9% p.a.547

410

231180

1992 1994 1996 1998

Connection charge, US$

CAGR, 1992-98 = -16.9% p.a. 44.938.1

34.2 31.3

1992 1994 1996 1998

Monthly subscription, US$

CAGR, 1992-98 = -5.8% p.a.

Note: CAGR = Compound Annual Growth rate.Source: ITU �World Telecommunication Development Report 1999: Mobile cellular�

Average revenue per user (ARPU)Bell Mobility (Canada)

0

20

40

60

80

100

120

90 91 92 93 94 95 96 97 98

Rev

enue

/cos

t per

sub

scrib

er

per m

onth

(US$

)

0

200

400

600

800

1'000

1'200

1'400

1'600

Subs

crib

ers

('000

s)

Revenue per sub/month

Cost per sub/month

Subscribers

Source: ITU �World Telecommunication Development Report 1999: Mobile cellular�

14%

22%

24%

40%

53%

36%

8%

3%

Customers

Average revenueper user (ARPU)

Expe

nditu

re p

er m

onth

40 per cent of low-spending customers

generate 3% ofrevenue

14 per cent of high-spending customers

generate 53% ofrevenue

Cultivate the highCultivate the high--spendersspenders

Source: Price Waterhouse Coopers, based on Canadian data.

Mobile ARPU converging with Fixed-line ARPU, Japan (Yen �000s p.a.)

0

50

100

150

200

250

300

1990 1991 1992 1993 1994 1995 1996 1997

Mobile ARPU

Fixed-line ARPU

Source: ITU �World Telecommunication Development Report 1999: Mobile cellular�

Pricing mobile and fixed:Monthly subscription charges (US$)

0

5

10

15

20

25

MalaysiaIndonesia

CambodiaThailand

HK SarSri Lanka

Residential fixed-lineDigital cellular

3.0

2.4 1.1 5.0 1.7

5.0

Ratio: Cellular/fixed

0.0

0.2

0.4

0.6

0.8

1.0

HK SarSri Lanka

CambodiaMalaysia

ThailandIndonesia

Residential fixed-lineDigital cellular

18.26.7

10.03.0 7.5

Ratio:Cellular/fixed

0

n.a.

Pricing mobile and fixed:Pricing mobile and fixed:Price of 3 minute local calls (US$)Price of 3 minute local calls (US$)

Fixed-Mobile Interconnection Issues

RPP vs. CPP: Mobile users don�t always pay to talk

Receiving Party Pays# Mobile party pays for

incoming calls and fixed party pays only local tariff

# Often, no interconnect arrangement is negotiated with the fixed operator for F-M calls. Mobile operators bill mobile consumer directly for �airtime�.

Calling Party Pays# Mobile party does

not pay for incoming calls and fixed party pays a premium to call the mobile party

# Call termination paid by fixed operators is a significant part of mobile operator revenues

Fixed-Mobile Interconnection Issues

Components of a Fixed to Mobile Call

Orig. Access

Switching

Authentication

Orig. Access

Switching

Authentication

CoreNetwork

Switching

CoreNetwork

Switching

Locating theCustomer

Switching

Term. Access

Locating theCustomer

Switching

Term. Access

Call Origination Call TerminationCalling Party

(FIXED)

Called Party

(MOBILE)

Transit service

Source: Adapted from ECTA

Fixed-Mobile Interconnection Issues

Fixed-Mobile Interconnection" Interconnect prices are a major determinant of

retail prices" Evidence of �market failure�

⇒ Interconnect prices are variable but generally very high⇒ In Calling Party-Pays environments, caller may not be aware of

the charge they will be paying⇒Calling party does not have a choice of operator to terminate the

call" Fixed-to-mobile and mobile-to-fixed highly

asymmetric" By 2003, 75% of all calls worldwide will involve a

mobile

Fixed-Mobile Interconnection Issues

Problems in calling-party-pays (CPP) environments

" Lack of tariff transparency " Mobile operators not subject to commercial

consequences of keeping rates elevated" Vertical integration further reduces incentives to lower

rates

Inefficient pricing

Non-transparent Tariffs

Market Structure

Fixed-Mobile Interconnection Issues

Calling opportunities worldwide

89.7%

5.0%5.0% 0.3%

199352.7%

19.9%

19.9%

7.5%

1998

23.4%

25.0%25.0%

26.7%

2003

Fixed-to-fixed

Fixed-to-mobile

Mobile-to-fixed

Mobile-to-mobile

Source: ITU Fixed-Mobile Interconnect website: http://www.itu.int/interconnect

Fixed-Mobile Interconnection Issues

Calling opportunities, CambodiaFixed-to-mobile17%

Mobile-to-fixed17%

Mobile-to-mobile, with interconnect

34%

Fixed-to-fixed5%

Mobile-to-mobile, without

interconnect27%

Note: Mobile subscribers = March 2000; fixed-line subscribers = December 1999. Source: ITU World Telecommunication Indicators Database.

Fixed-Mobile Interconnection Issues

Calling opportunities, Lao PDR

Note: Mobile subscribers = March 2000; fixed-line subscribers = December 1999. Source: ITU World Telecommunication Indicators Database.

Fixed-to-mobile18%

Mobile-to-mobile, without

interconnect6%

Fixed-to-fixed58%

Mobile-to-fixed18%

Fixed-Mobile Interconnection Issues

Calling opportunities, Viet Nam

Note: Mobile subscribers = March 2000; fixed-line subscribers = December 1999. Source: ITU World Telecommunication Indicators Database.

Fixed-to-mobile10%

Mobile-to-mobile, with interconnect

0.71%

Mobile-to-fixed10%

Mobile-to-mobile, without

interconnect0.74%

Fixed-to-fixed78%

Fixed/Mobile interconnect rates in selected calling-party-pays countries

0.293

0.208

0.205

0.078

0.070

0.064

0.047

0.034

0.017

0.293

0.052

0.051

0.042

0.050

0.026

0.047

0.034

0.017

Antigua

Botswana

Philippines

Dom. Rep.

Cambodia

Mexico

Guatemala

Malaysia

Costa Rica

Mobile-to-fixedinterconnect rate

Fixed-to-mobileinterconnect rate

Source: ITU.

Fixed-Mobile Interconnection Issues

Sample prices in RPP environments

0.092

0.005

0.020

0.001

0.056

0.009

0.020

0.009

0.008

0.008

0.007

0.002

0.000

0.000

0.008

0.000

CPP

RPP

USA

Sri Lanka

Singapore

HK SAR

Canada

China

Mobile-to-fixedinterconnect rateFixed-to-mobileinterconnect rate

RPP countries

Average

The race for 3rd Generation mobiles: IMT-2000

0

32

64

9.6

128

144

384

2,000 1G 2G 3G

VoiceVoice

Text MessagingText Messaging

Video StreamingVideo Streaming

StillStillImagingImaging

Audio StreamingAudio Streaming

Dat

a Tr

ansm

issi

on S

peed

-kb

it/s

ElectronicNewspaper

RemoteMedicalService(Medicalimage)

VideoConference

(High quality)

Telephone(Voice)

VoiceMail

E-MailFax

ElectronicPublishing

Video onDemand:

Sports, NewsWeather

Karaoke

VideoConference

(Lower quality)

JPEGStill Photos

MobileRadio

Video Surveillance,Video Mail, Travel

Image

AudioVoice-driven Web PagesStreaming Audio

DataWeather, Traffic, News,Sports, Stock updates

Mobile TV

E-Commerce

TimeSource: Adapted from Motorola.

Fixed-Mobile Interconnection Issues

Future Trends: Mobile Internet" Pricing and billing

⇒unmetered flat-rate (Internet) ⇒per-minute charges (Mobile)

" From circuit-switching to packet-switching⇒ Impact on nature of interconnection agreements?

" Evolution of the interconnection value chain: connectivity, capacity, content �⇒How to measure value? How to split revenue among

players?

For more information ... ITU Website at For more information ... ITU Website at www.itu.int/interconnectwww.itu.int/interconnect

Case studies" Finland" India" Mexico" China/HK

Trends in Telecom Reform, 2001 edition: Interconnection