Fiscal Year at a Glance WASBO New School Administrator & Business Support Staff Workshop August 16,...

101

Fiscal Year at a Glance WASBO New School Administrator & Business Support Staff Workshop August 16, 2007 Lori Ames, Consultant-DPI Brad Adams, Consultant-DPI Robert Borch, Assistant Superintendent-Elmbrook

-

Upload

corey-dickerson -

Category

Documents

-

view

213 -

download

0

Transcript of Fiscal Year at a Glance WASBO New School Administrator & Business Support Staff Workshop August 16,...

Fiscal Year at a Glance

WASBO New School Administrator & Business Support Staff Workshop

August 16, 2007

Lori Ames, Consultant-DPIBrad Adams, Consultant-DPI

Robert Borch, Assistant Superintendent-Elmbrook

Agenda

9:00 – 10:15: Introduction, Website Review 10:15 – 10:30: Break 10:30 – 12:00: DPI reporting requirements,

district budgeting 12:00 – 1:00: Lunch 1:00 – 2:15: Building Trust 2:00-2:30: Break 2:30-4:00: Money Saving Tips

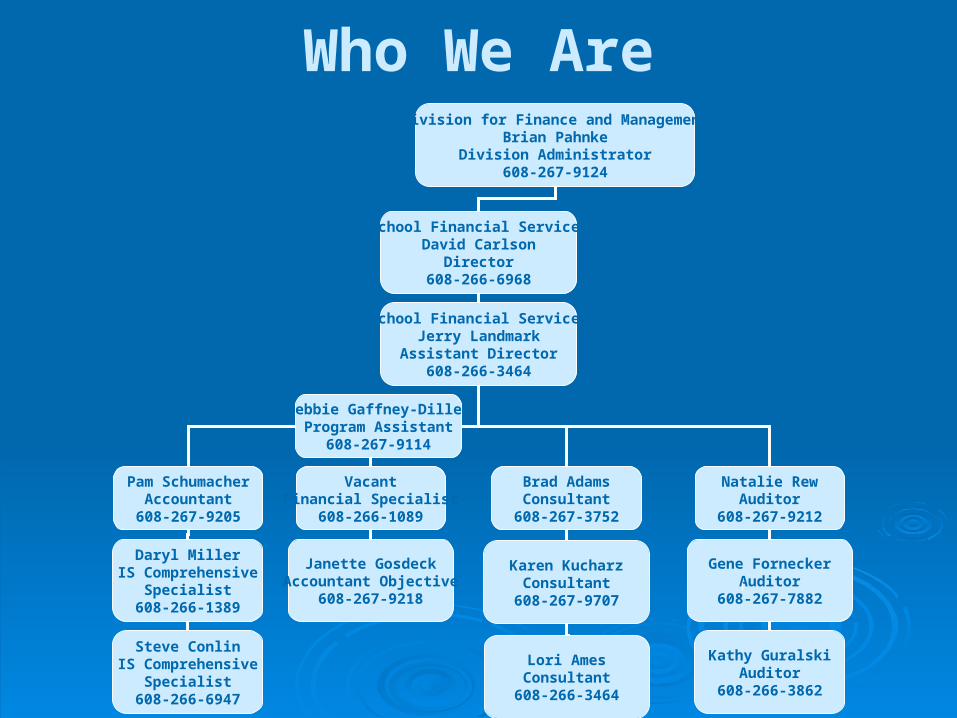

Division for Finance and ManagementBrian Pahnke

Division Administrator608-267-9124

School Financial ServicesDavid Carlson

Director608-266-6968

School Financial ServicesJerry Landmark

Assistant Director608-266-3464

Debbie Gaffney-DilleyProgram Assistant

608-267-9114

Pam SchumacherAccountant

608-267-9205

VacantFinancial Specialist

608-266-1089

Brad AdamsConsultant

608-267-3752

Natalie RewAuditor

608-267-9212

Daryl MillerIS Comprehensive

Specialist608-266-1389

Steve ConlinIS Comprehensive

Specialist608-266-6947

Janette GosdeckAccountant Objective

608-267-9218

Karen KucharzConsultant

608-267-9707

Gene ForneckerAuditor

608-267-7882

Kathy GuralskiAuditor

608-266-3862

Lori AmesConsultant

608-266-3464

Who We Are

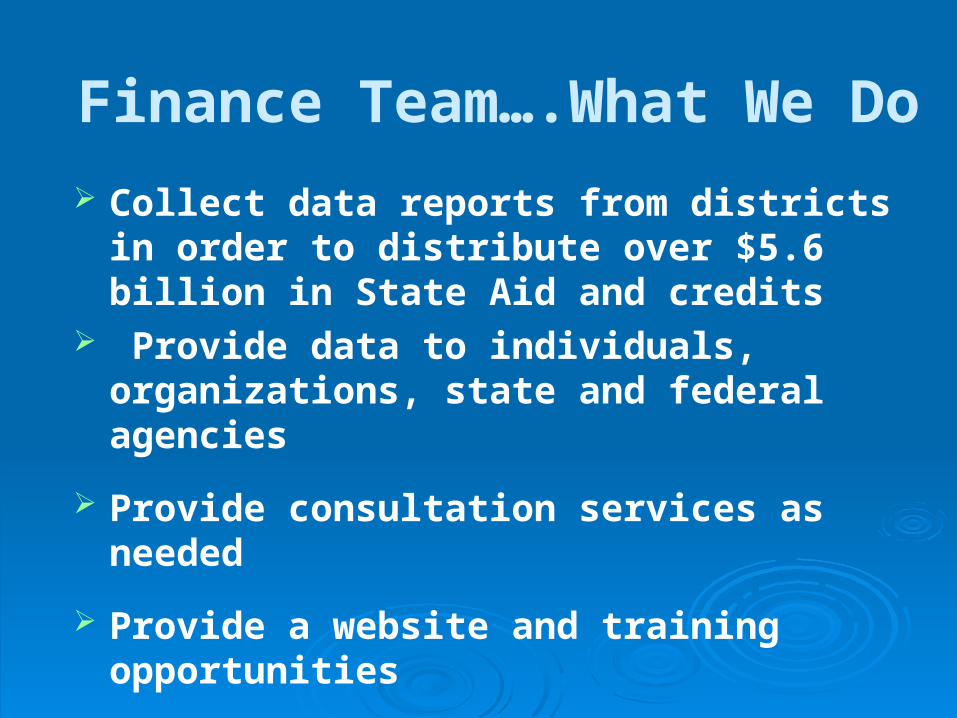

Finance Team….What We Do

Collect data reports from districts in order to distribute over $5.6 billion in State Aid and credits

Provide data to individuals, organizations, state and federal agencies

Provide consultation services as needed

Provide a website and training opportunities

How We Can Help You

Web page publications & tutorials

Phone calls, e-mail

Listserv notices

Conferences and workshops

What Should You Do…Today!

Bookmark this website

http://www.dpi.wi.gov/sfs/index.html

Subscribe to our list serv http://www.dpi.wi.gov/sfs/mailings.html Click on the link to “subscribe”

Website Review

Why “Fiscal Year at a Glance?”

Answer the basic questions that we receive throughout the year

Show how data elements translate into the payment of aid

Show connections between fiscal years

Show connections between various pieces of data

Master “Multi-Tasker”

How many years can you juggle at one time……

July - December

What activities take place relating to the prior fiscal year

(2006-07)?

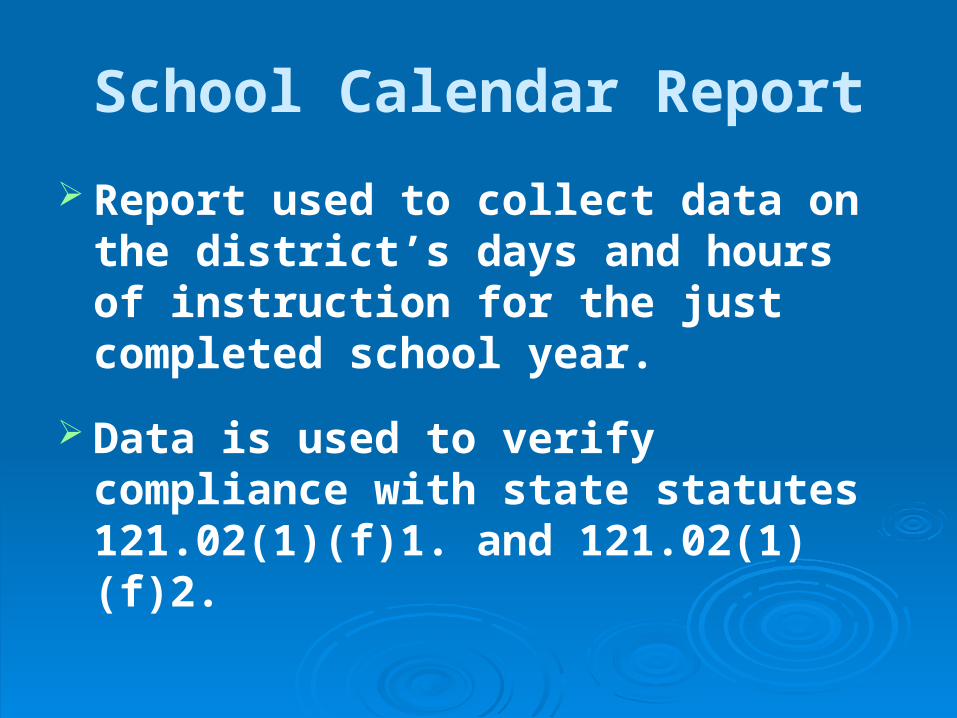

School Calendar Report

Report used to collect data on the district’s days and hours of instruction for the just completed school year.

Data is used to verify compliance with state statutes 121.02(1)(f)1. and 121.02(1)(f)2.

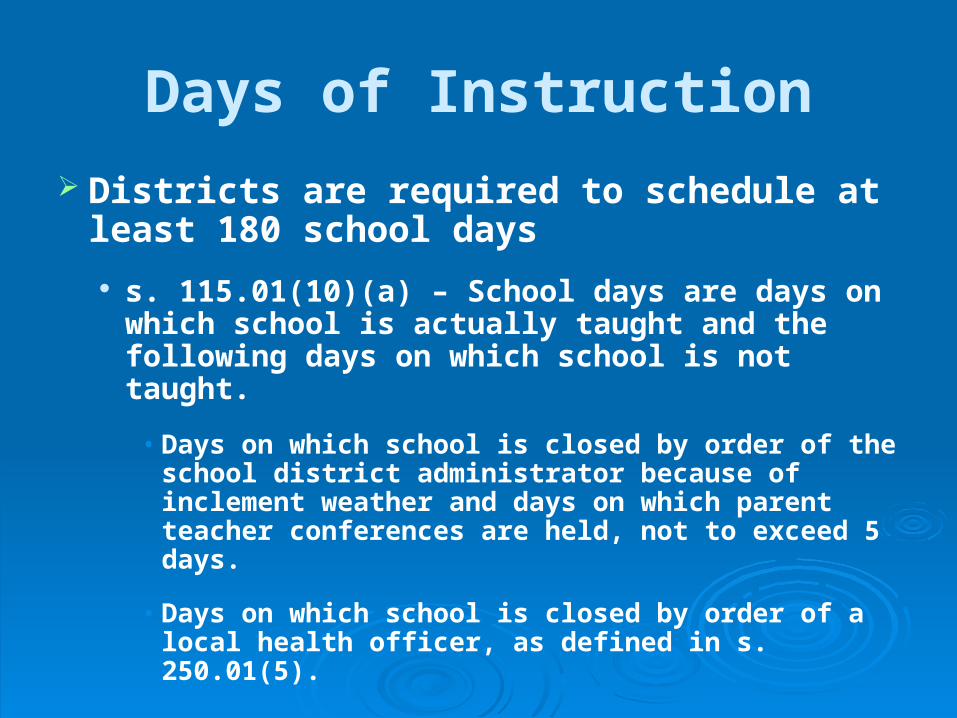

Days of Instruction

Districts are required to schedule at least 180 school days

s. 115.01(10)(a) – School days are days on which school is actually taught and the following days on which school is not taught.

• Days on which school is closed by order of the school district administrator because of inclement weather and days on which parent teacher conferences are held, not to exceed 5 days.

• Days on which school is closed by order of a local health officer, as defined in s. 250.01(5).

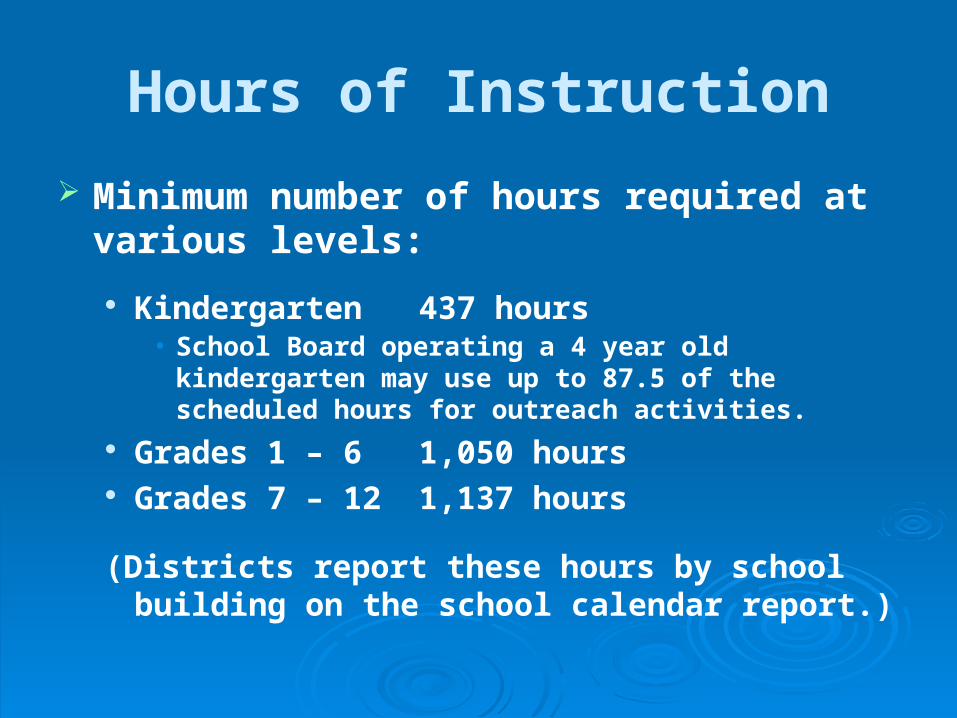

Hours of Instruction

Minimum number of hours required at various levels:

Kindergarten 437 hours• School Board operating a 4 year old kindergarten may

use up to 87.5 of the scheduled hours for outreach activities.

Grades 1 – 6 1,050 hours Grades 7 – 12 1,137 hours

(Districts report these hours by school building on the school calendar report.)

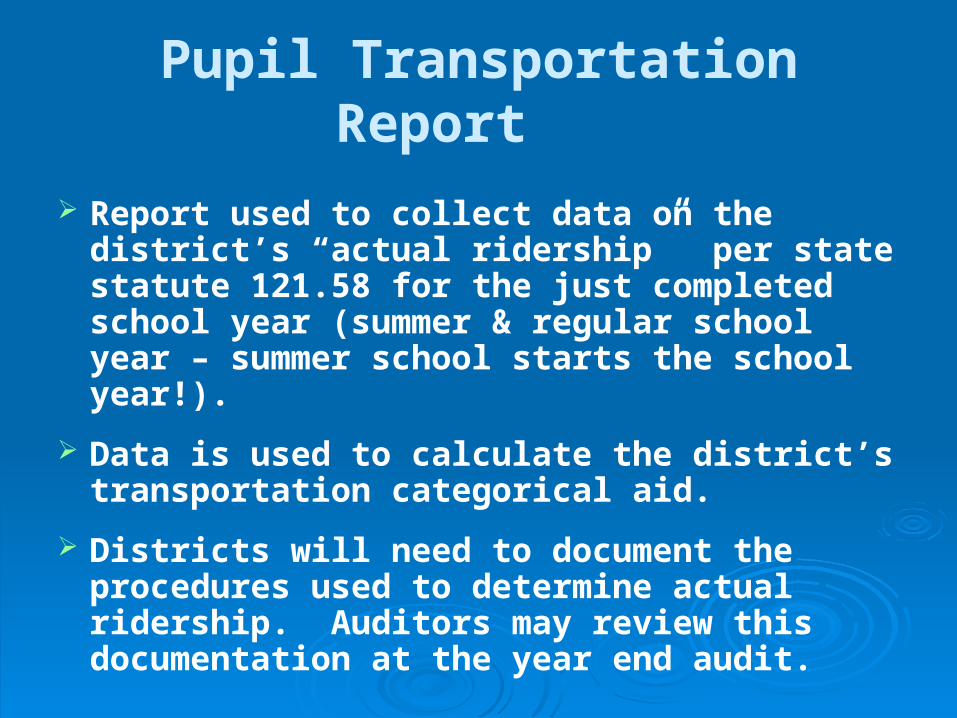

Pupil Transportation Report

Report used to collect data on the district’s “actual ridership” per state statute 121.58 for the just completed school year (summer & regular school year – summer school starts the school year!).

Data is used to calculate the district’s transportation categorical aid.

Districts will need to document the procedures used to determine actual ridership. Auditors may review this documentation at the year end audit.

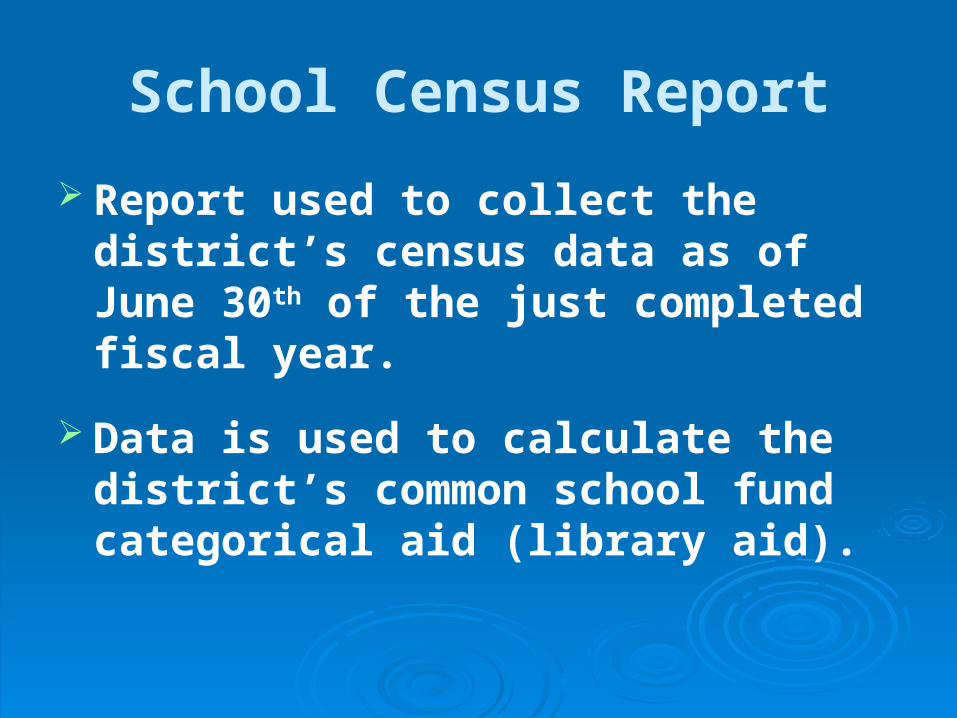

School Census Report

Report used to collect the district’s census data as of June 30th of the just completed fiscal year.

Data is used to calculate the district’s common school fund categorical aid (library aid).

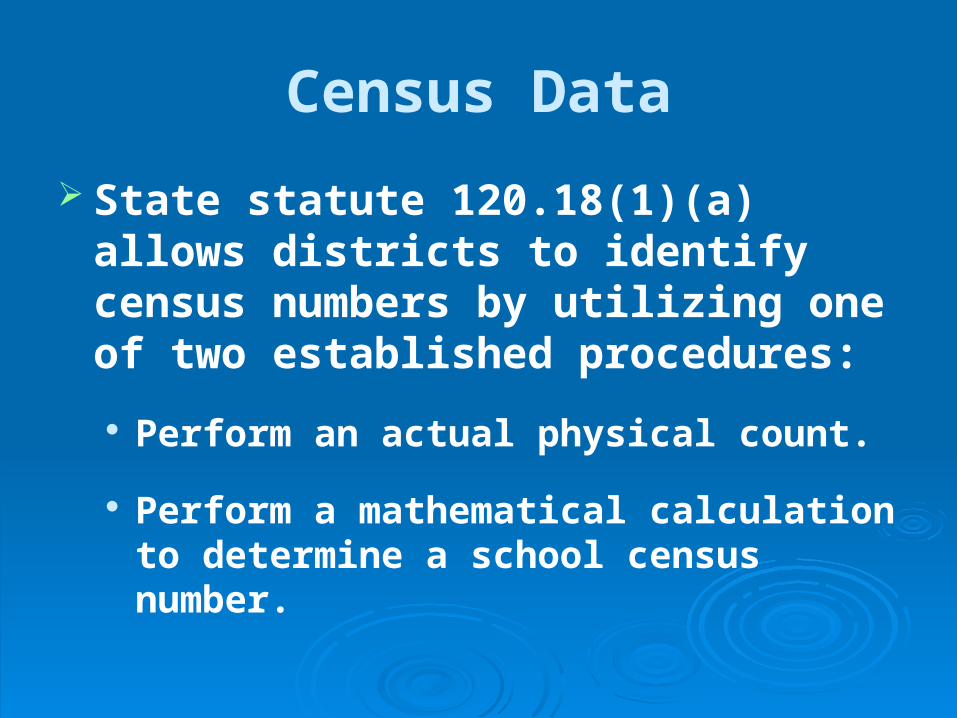

Census Data

State statute 120.18(1)(a) allows districts to identify census numbers by utilizing one of two established procedures:

Perform an actual physical count.

Perform a mathematical calculation to determine a school census number.

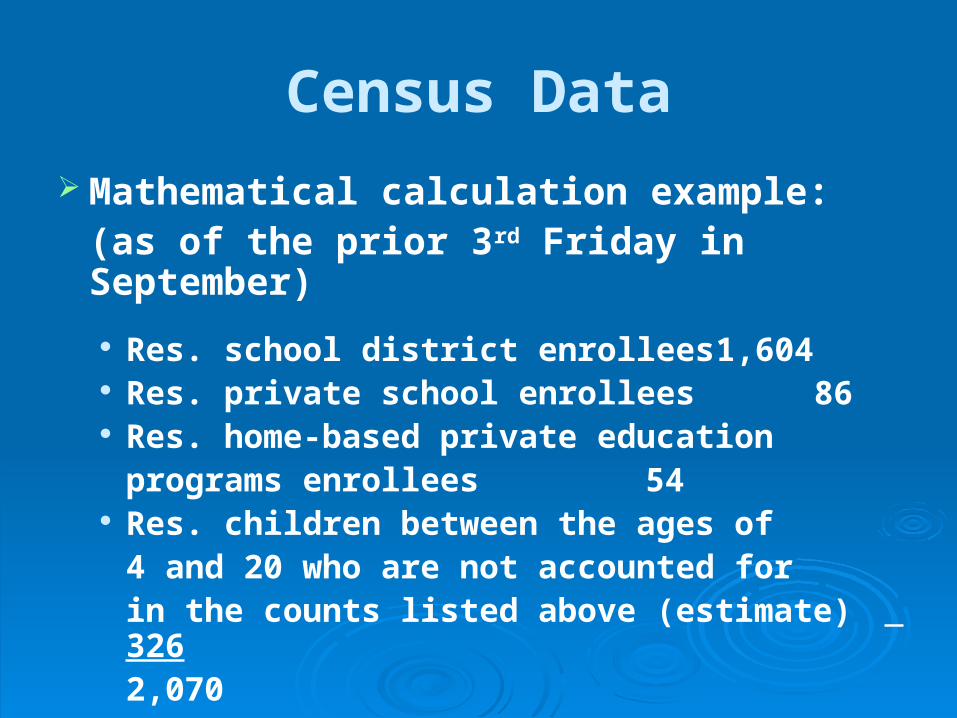

Census Data

Mathematical calculation example:(as of the prior 3rd Friday in September)

Res. school district enrollees 1,604 Res. private school enrollees 86 Res. home-based private education

programs enrollees 54 Res. children between the ages of

4 and 20 who are not accounted forin the counts listed above (estimate) 326

2,070

Common School Fund

The common school fund is one of the State Trust Funds.

Managed by the Board of Commissioners of Public Lands (BCPL)

Net earnings of the fund are distributed as library aid each year to public school districts for the purchase of school library materials

Common School Fund Aid

Districts are given an estimate of common school fund aid in January with an actual aid payment on May 1st.

The entire allocation must be spent by June 30th of the year in which it is received.

The Department annually verifies that the full amount of aid has been spent. District may receive an inquiry if it appears funds may go unspent.

Common School Fund Aid

Common School Fund Aid may be spent on: WUFAR Function 222 000 - Object Codes:

• Audiovisual materials 431• Library books 432• Newspapers 433• Periodicals 434• Instructional software 435• Microfilm 438• Other Media 439

PI 1505AC (Aid Certification)

Report used to collect critical financial data from the district’s ledger for the just completed fiscal year.

Data is used to calculate the district’s October 15th aid certification.

District data entered on the PI 1505AC is verified by the auditor via the PI 1506AC (report completed by the auditor).

PI 1505 – Full Annual Report

Report used to collect the district’s final revenues, expenditures, assets, liabilities, and equity for all funds for the just completed fiscal year.

Data used to calculate the district’s final aid eligibility as per state statute 121.54(4)(b).

Special Education Annual Report

Report used to collect the district’s special education (fund 27) expenditures for the just completed fiscal year.

Data used to calculate the district’s special education categorical aid.

Audit

Annual audit of district financial records is statutorily required.

The independent auditors will verify that the financial statements present fairly the balance sheet as of June 30th and the results of operations for the year ended June 30th.

Purpose of the Audit

Maintain public confidence in the reliability of published financial data.

Assure users that the financial statements are fairly presented in accordance with Generally Accepted Accounting Principles (GAAP).

Determine compliance with state and federal requirements.

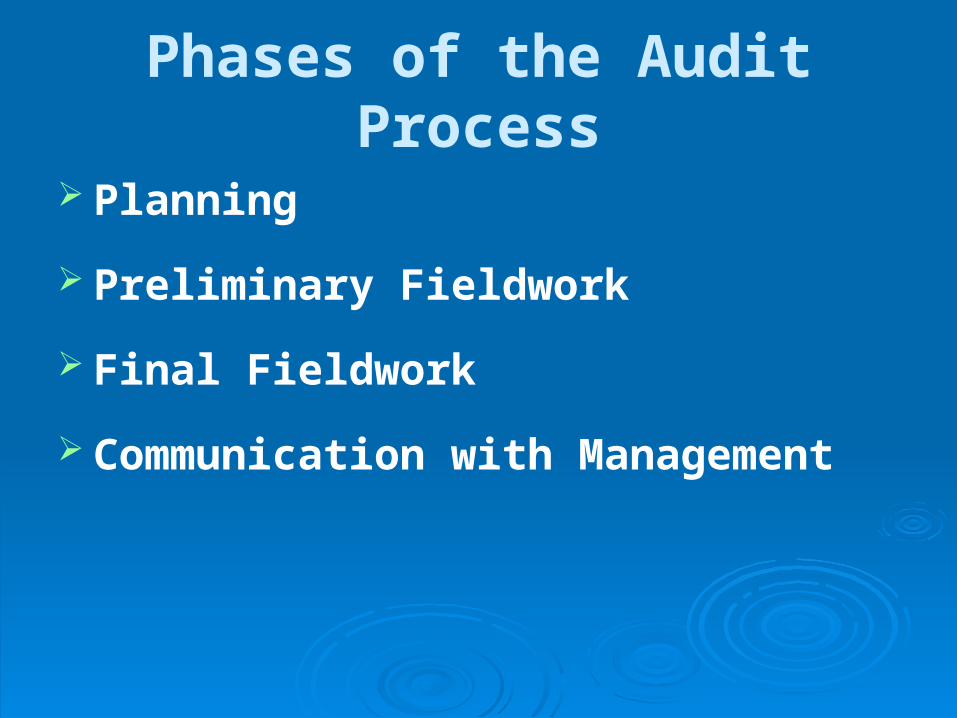

Phases of the Audit Process

Planning

Preliminary Fieldwork

Final Fieldwork

Communication with Management

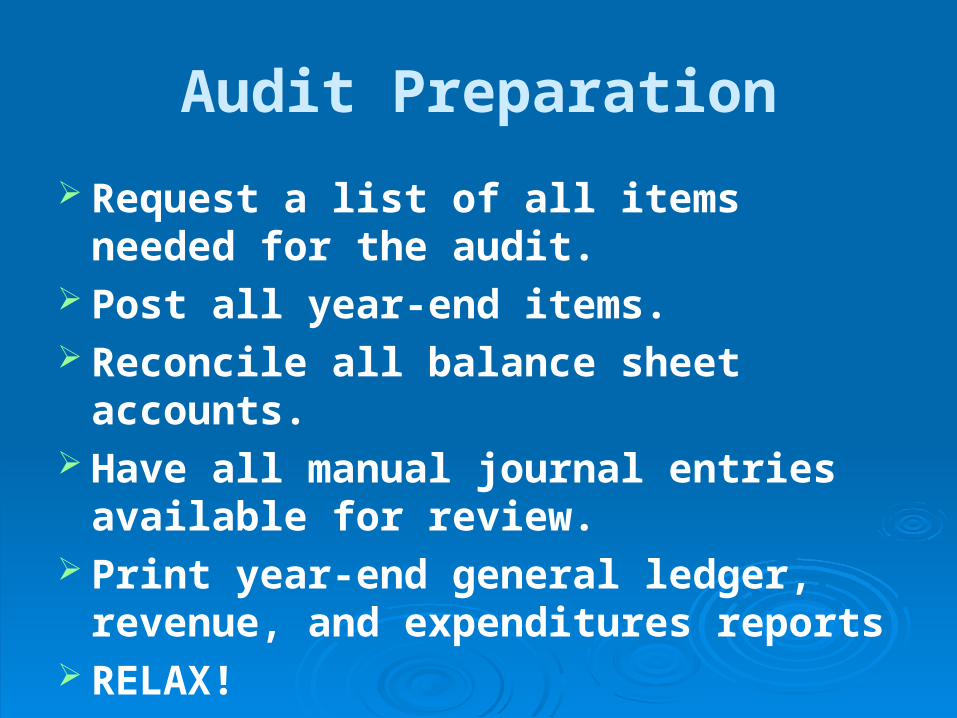

Audit Preparation

Request a list of all items needed for the audit.

Post all year-end items. Reconcile all balance sheet accounts. Have all manual journal entries

available for review. Print year-end general ledger, revenue,

and expenditures reports RELAX!

July - December

What activities take place relating to the current fiscal year

(2007-08)?

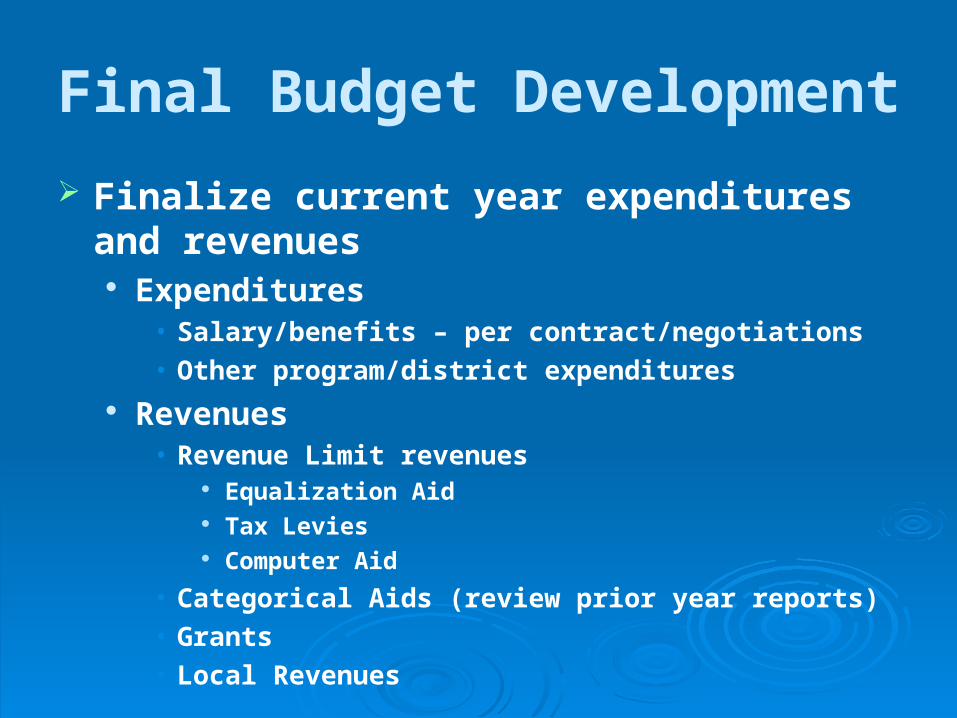

Final Budget Development

Finalize current year expenditures and revenues

Expenditures• Salary/benefits – per contract/negotiations• Other program/district expenditures

Revenues• Revenue Limit revenues

Equalization Aid Tax Levies Computer Aid

• Categorical Aids (review prior year reports)• Grants• Local Revenues

Final Budget Development

The district’s budget is a roadmap based on the district’s best estimations.

Two major revenues remain an estimate until mid-October – when the district can calculate the revenue limit for taxing purposes:

Equalization Aid Tax Levy

Budget Hearing & Adoption

The Budget Hearing and Adoption process is outlined in state statute 65.90.

All districts are required to have a budget hearing.

Common and Unified High School Districts are required to hold the budget hearing at the same time and place as the annual meeting.

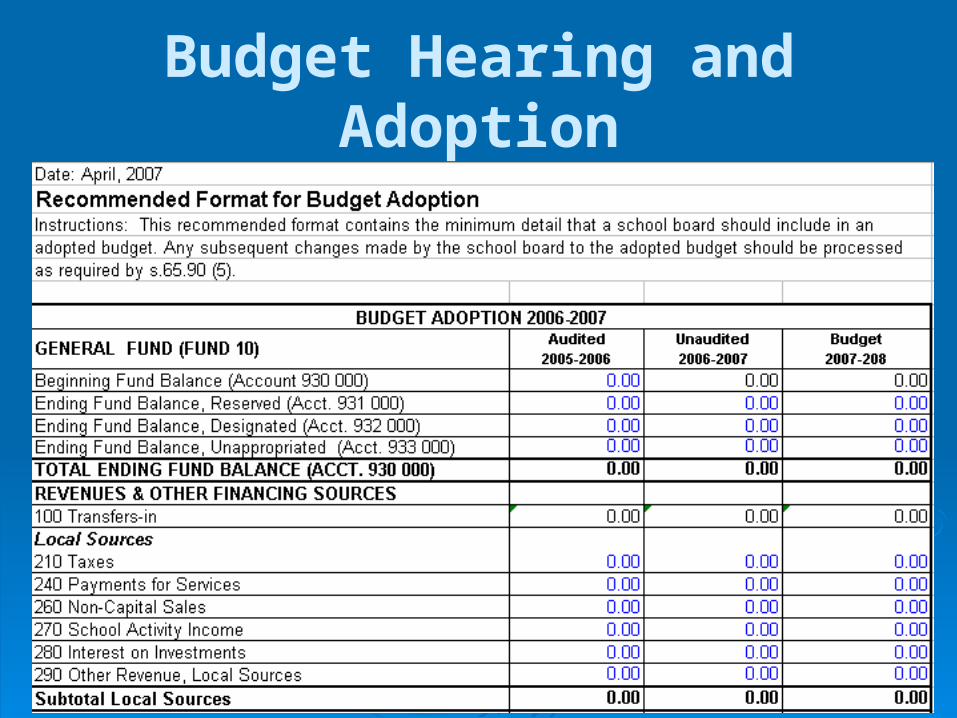

Budget Hearing and Adoption

School boards are required to approve a “proposed” budget for presentation at the budget hearing.

An excel file is available to assist with the recommended format for budget presentation and publication.

http://www.dpi.wi.gov/sfs/budhear.html

Budget Hearing and Adoption

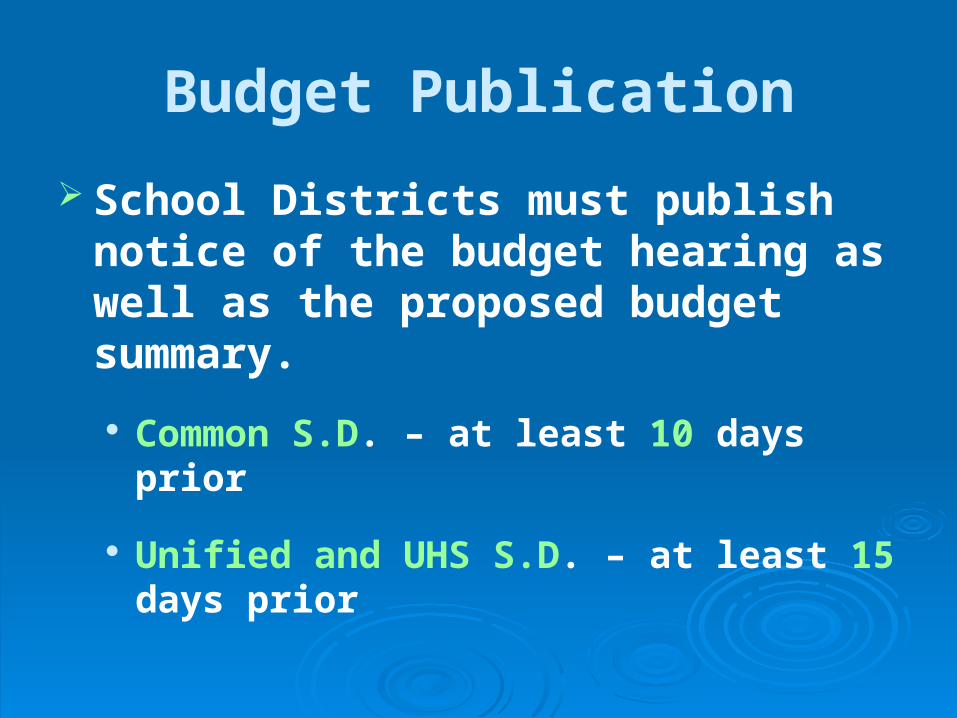

Budget Publication

School Districts must publish notice of the budget hearing as well as the proposed budget summary.

Common S.D. – at least 10 days prior

Unified and UHS S.D. – at least 15 days prior

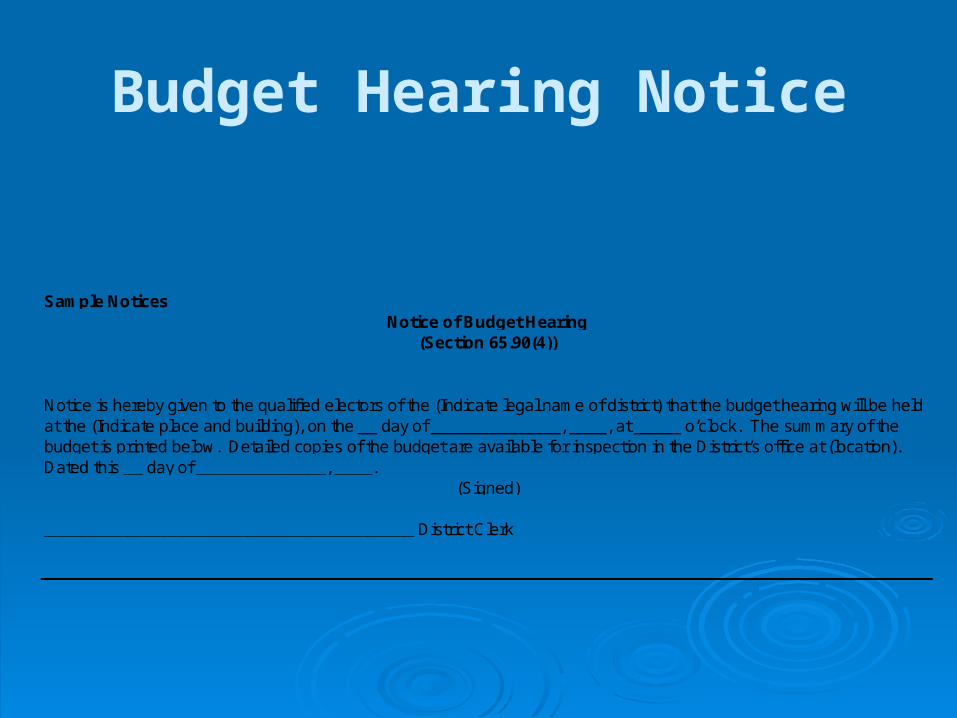

Budget Hearing Notice

________________________________________ District Clerk

Notice is hereby given to the qualified electors of the (Indicate legal name of district) that the budget hearing will be held at the (Indicate place and building), on the __ day of ______________, ____, at _____ o’clock. The summary of the budget is printed below. Detailed copies of the budget are available for inspection in the District’s office at (location).Dated this __ day of ______________, ____.

(Signed)

Sample NoticesNotice of Budget Hearing

(Section 65.90(4))

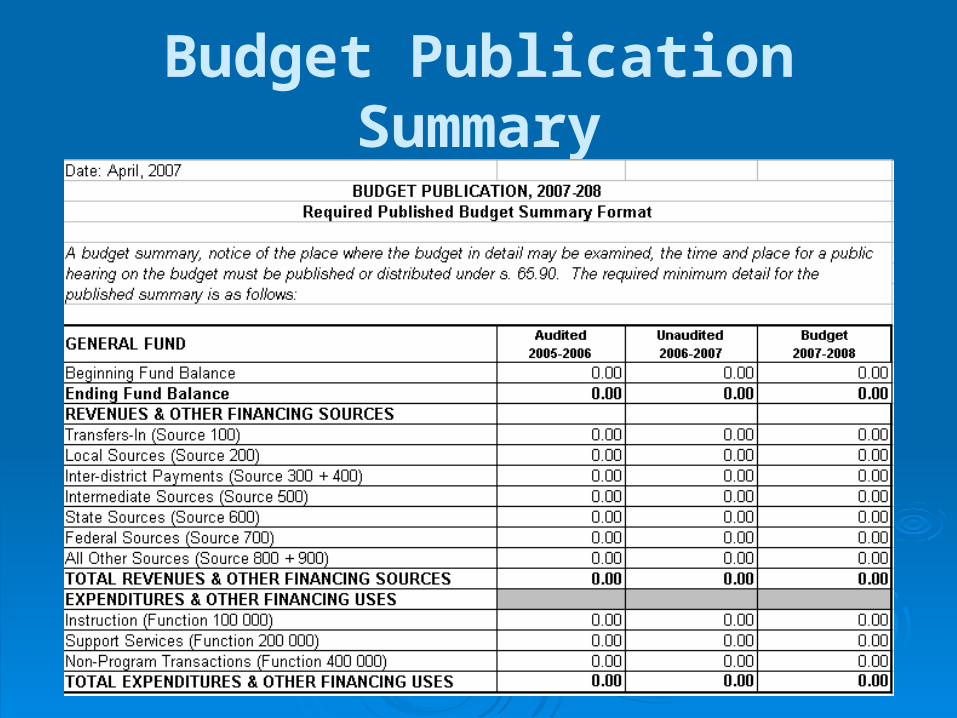

Budget Publication Summary

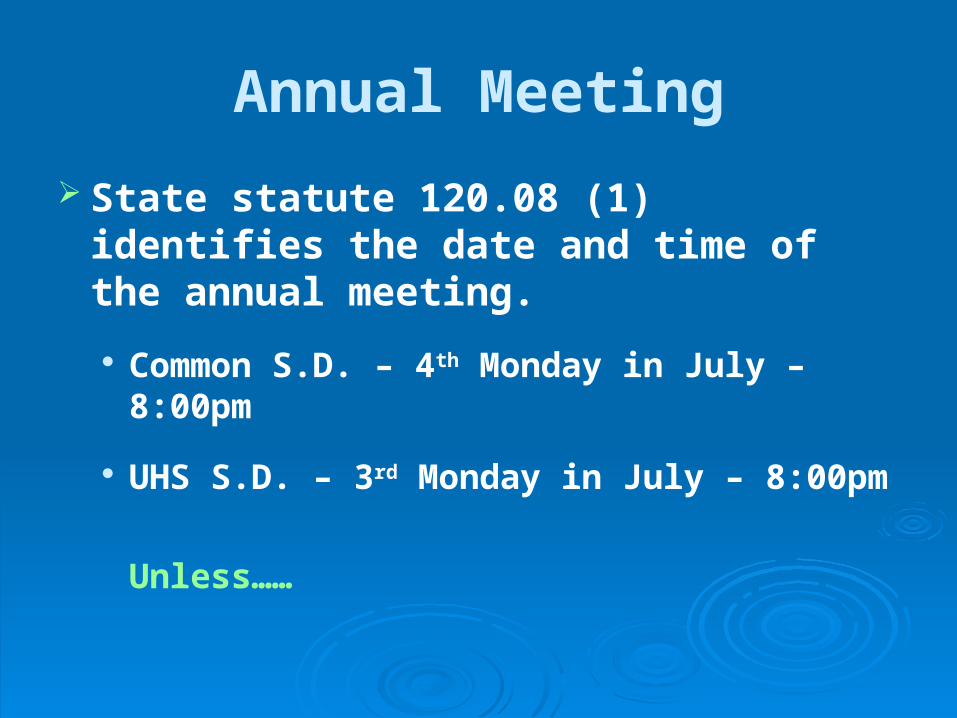

Annual Meeting

State statute 120.08 (1) identifies the date and time of the annual meeting.

Common S.D. – 4th Monday in July – 8:00pm

UHS S.D. – 3rd Monday in July – 8:00pm

Unless……

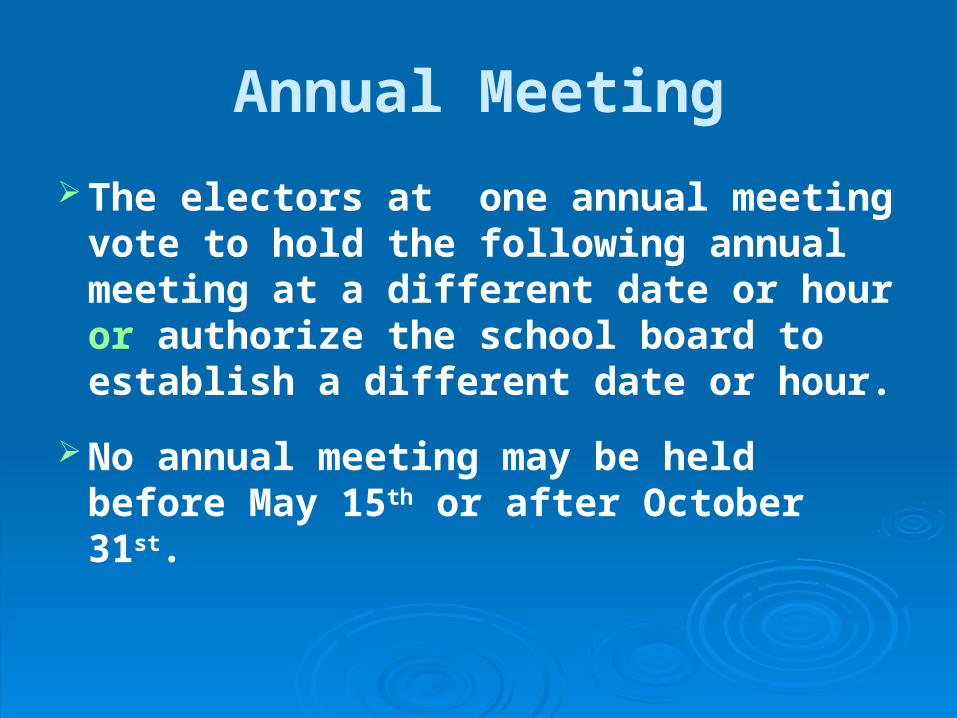

Annual Meeting

The electors at one annual meeting vote to hold the following annual meeting at a different date or hour or authorize the school board to establish a different date or hour.

No annual meeting may be held before May 15th or after October 31st.

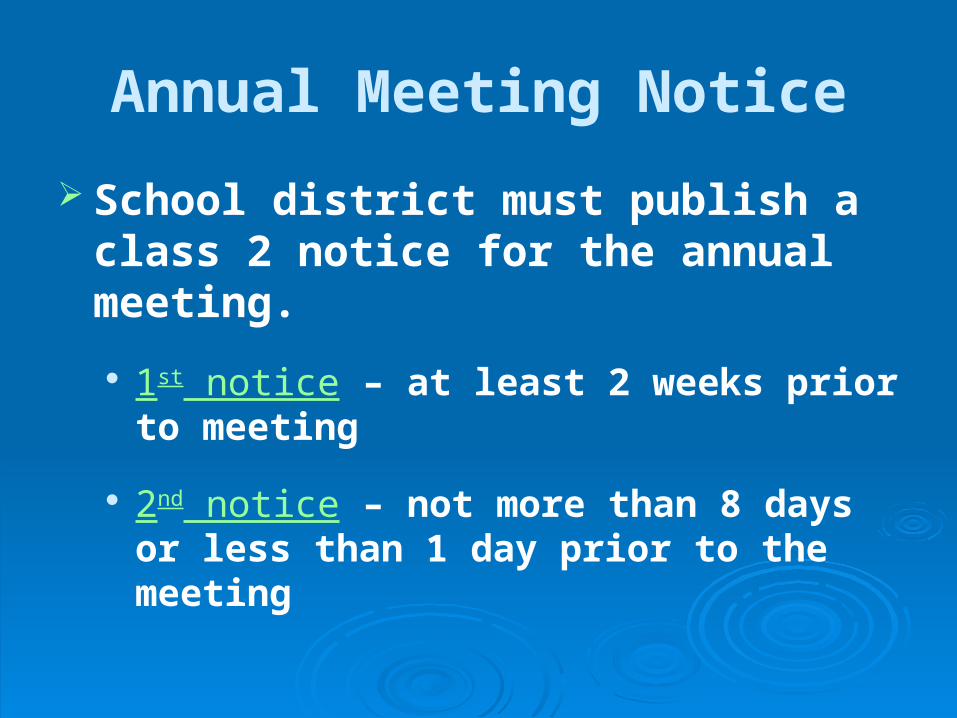

Annual Meeting Notice

School district must publish a class 2 notice for the annual meeting.

1st notice – at least 2 weeks prior to meeting

2nd notice – not more than 8 days or less than 1 day prior to the meeting

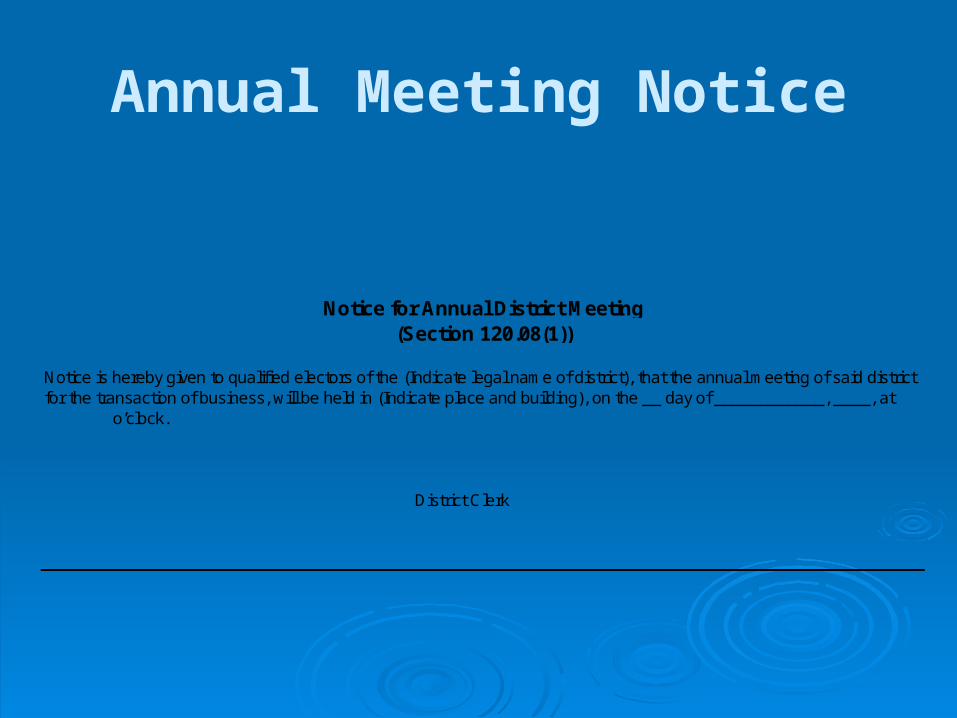

Annual Meeting Notice

________________________________________ District Clerk

Notice is hereby given to qualified electors of the (Indicate legal name of district), that the annual meeting of said district for the transaction of business, will be held in (Indicate place and building), on the __ day of ____________, ____, at _______ o’clock.

Notice for Annual District Meeting(Section 120.08(1))

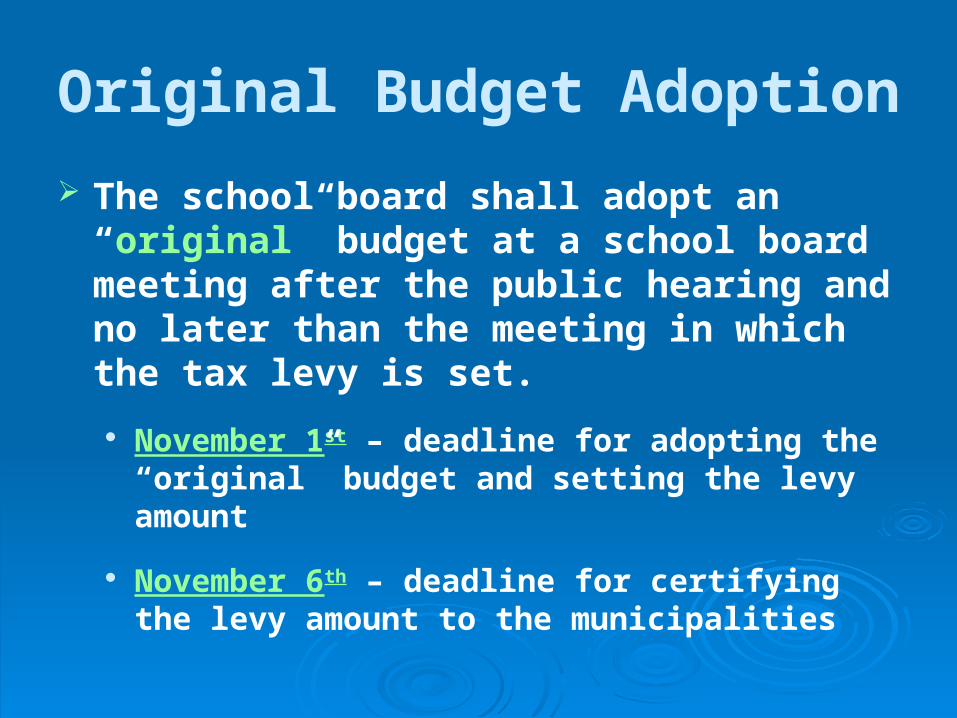

Original Budget Adoption

The school board shall adopt an “original” budget at a school board meeting after the public hearing and no later than the meeting in which the tax levy is set.

November 1st – deadline for adopting the “original” budget and setting the levy amount

November 6th – deadline for certifying the levy amount to the municipalities

Summer School FTE Report

Report used to collect district FTE data for the just ended summer term. (Summer school starts the school year!)

FTE data is used in the calculation of a district’s revenue limit and equalization aid.

The summer school report is one of the few reports that ask for an FTE count as opposed to a head count.

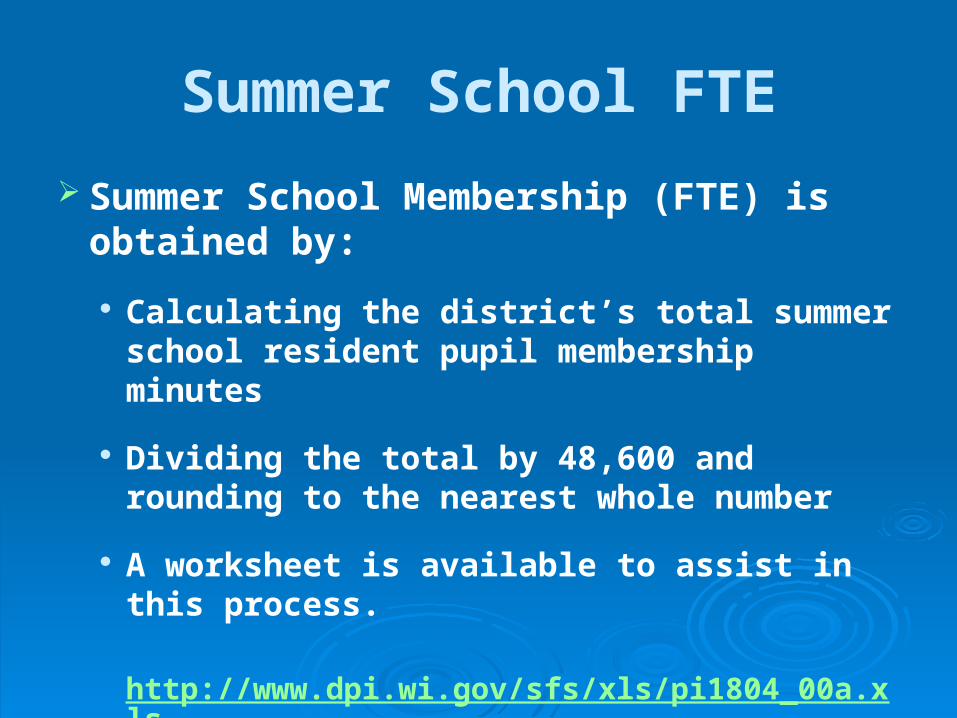

Summer School FTE

Summer School Membership (FTE) is obtained by:

Calculating the district’s total summer school resident pupil membership minutes

Dividing the total by 48,600 and rounding to the nearest whole number

A worksheet is available to assist in this process.

http://www.dpi.wi.gov/sfs/xls/pi1804_00a.xls

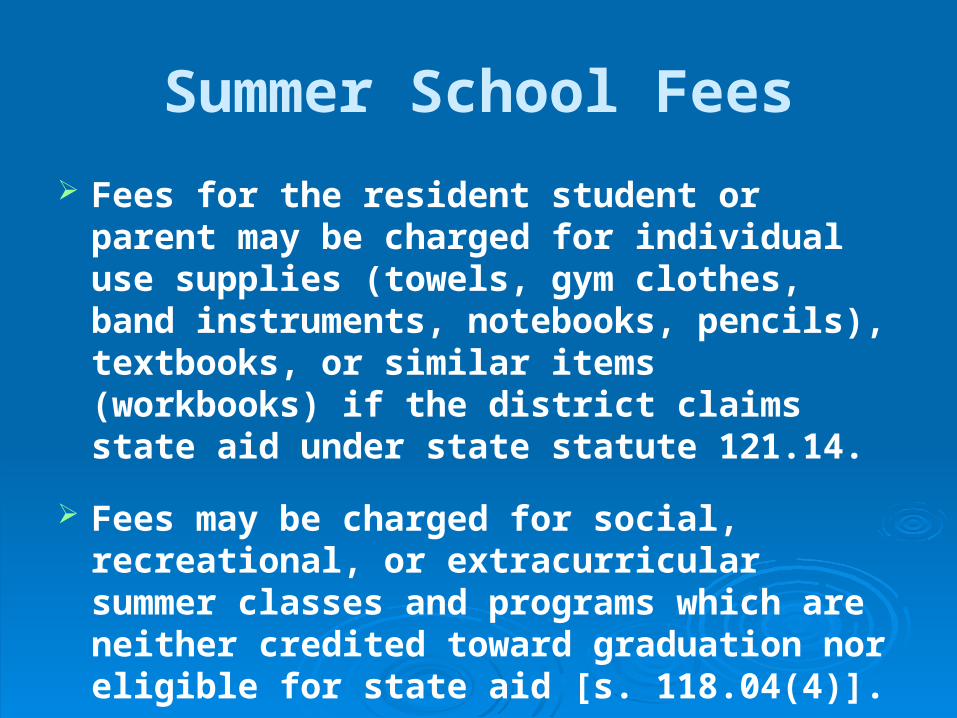

Summer School Fees

Fees for the resident student or parent may be charged for individual use supplies (towels, gym clothes, band instruments, notebooks, pencils), textbooks, or similar items (workbooks) if the district claims state aid under state statute 121.14.

Fees may be charged for social, recreational, or extracurricular summer classes and programs which are neither credited toward graduation nor eligible for state aid [s. 118.04(4)].

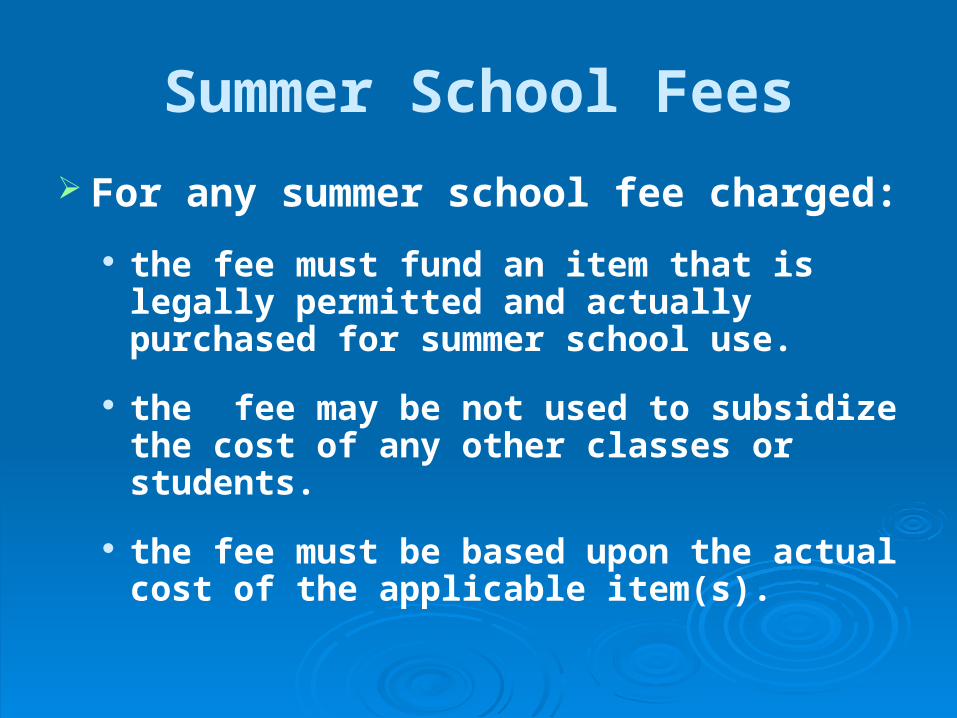

Summer School Fees

For any summer school fee charged:

the fee must fund an item that is legally permitted and actually purchased for summer school use.

the fee may be not used to subsidize the cost of any other classes or students.

the fee must be based upon the actual cost of the applicable item(s).

Audit of Summer School Fees

If you district is required to have a membership audit, the auditor will review your summer school fte and any associated summer school fees.

The auditor will question fees if:

the fee does not appear to be legal.

the amount of the fee exceeds the actual cost.

Audit of Summer School Fees

If a fee is deemed excessive or inappropriate: The district may be asked to provide

assurance that fees charged in the future will be in accordance with statutory requirements.

The summer school fte claimed may be adjusted or disallowed.

The district will be required to have a membership audit of summer school fte in the following year.

September Pupil Count Report

Report used to collect district count data for the 3rd Friday in September.

Data is converted to full-time equivalency and used in the calculation of a district’s revenue limit and equalization aid.

General Count Guidelines

In general, count the student if:

The student is a district resident.

The District is financially responsible for the student’s educational program.

The student is present for instruction on the count date or meets the before and after rule.

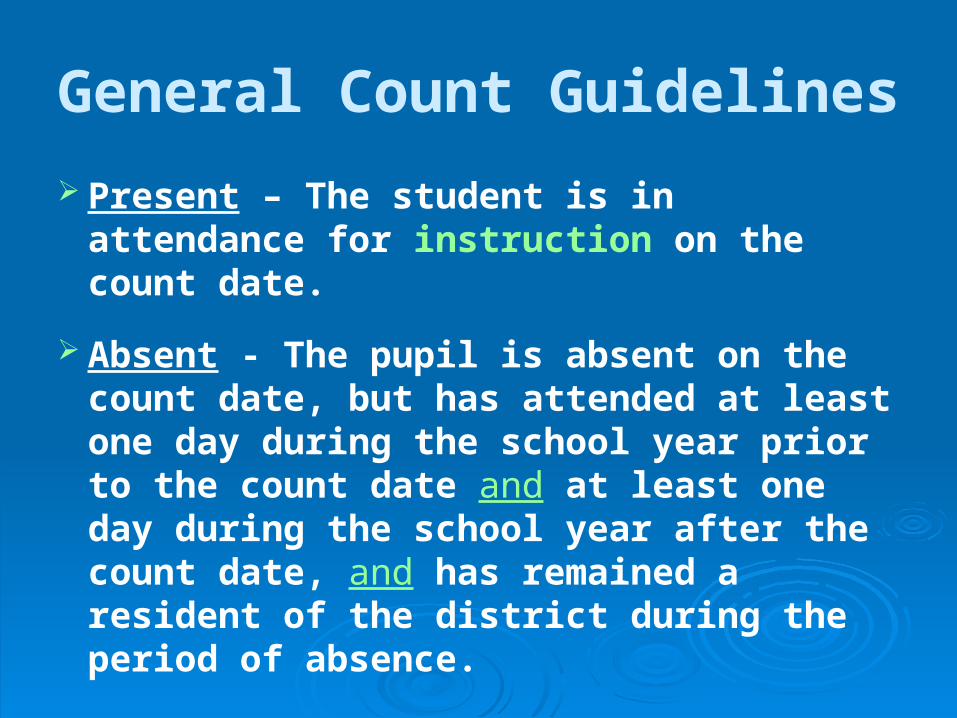

General Count Guidelines

Present – The student is in attendance for instruction on the count date.

Absent - The pupil is absent on the count date, but has attended at least one day during the school year prior to the count date and at least one day during the school year after the count date, and has remained a resident of the district during the period of absence.

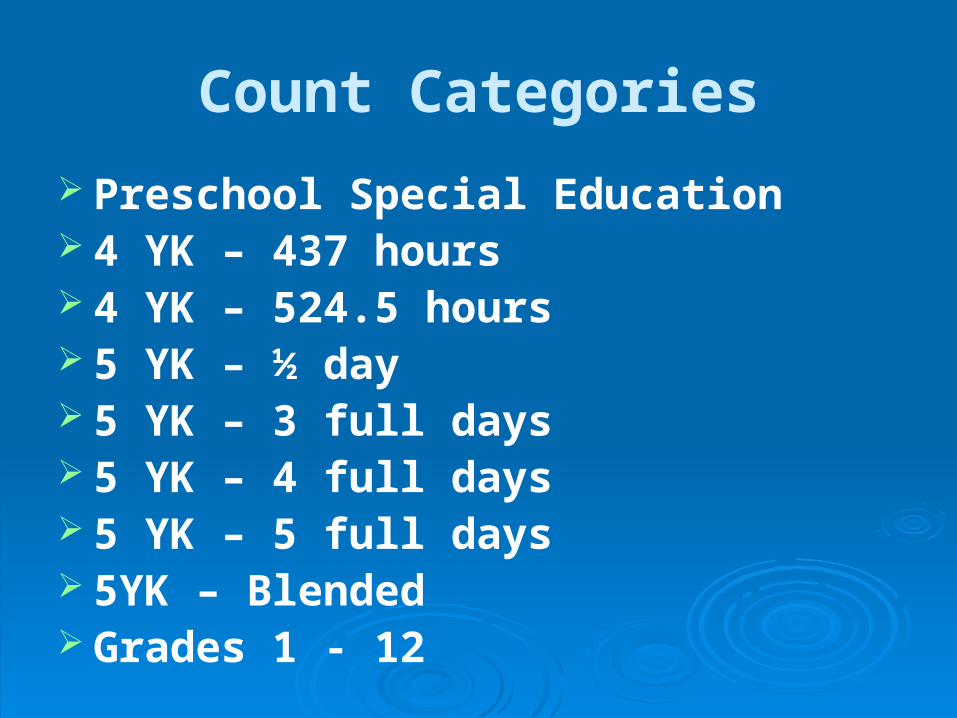

Count Categories

Preschool Special Education 4 YK – 437 hours 4 YK – 524.5 hours 5 YK – ½ day 5 YK – 3 full days 5 YK – 4 full days 5 YK – 5 full days 5YK – Blended Grades 1 - 12

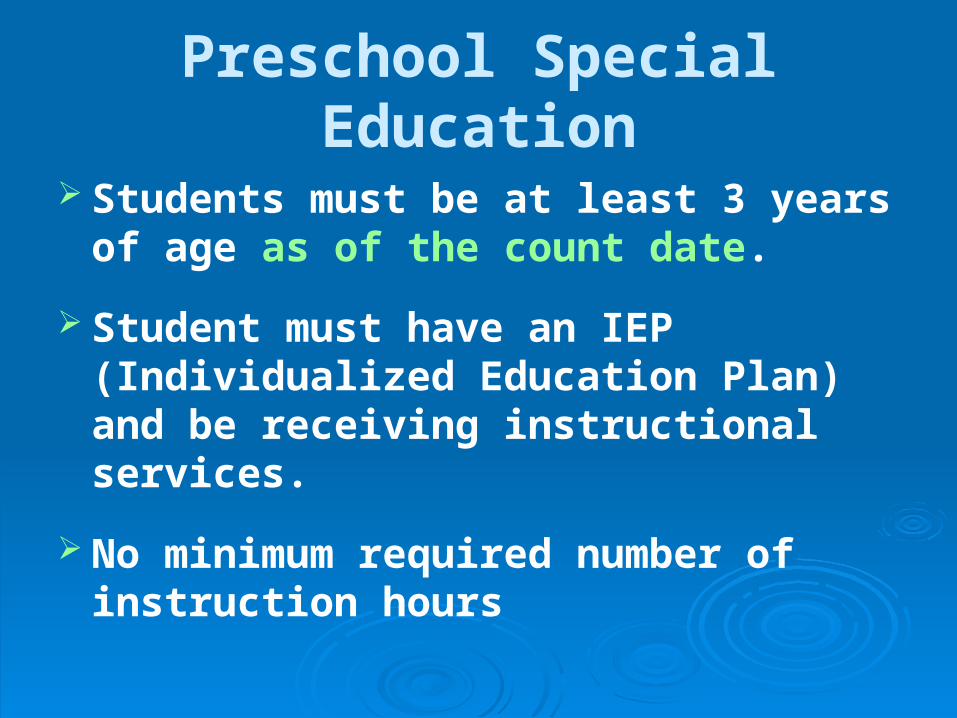

Preschool Special Education

Students must be at least 3 years of age as of the count date.

Student must have an IEP (Individualized Education Plan) and be receiving instructional services.

No minimum required number of instruction hours

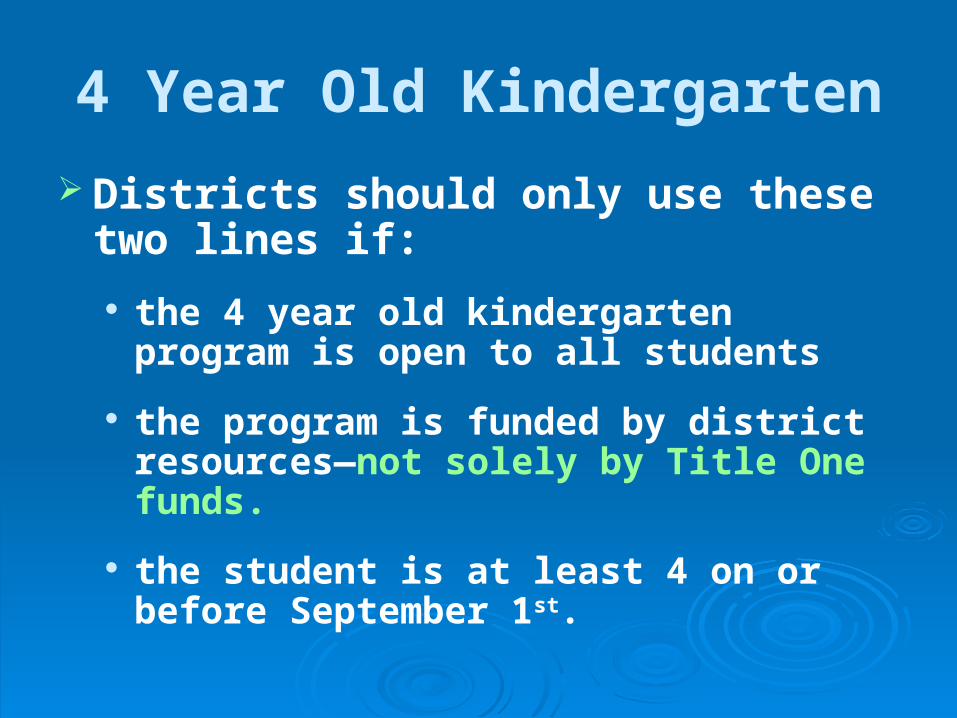

4 Year Old Kindergarten

Districts should only use these two lines if:

the 4 year old kindergarten program is open to all students

the program is funded by district resources—not solely by Title One funds.

the student is at least 4 on or before September 1st.

4 Year Old Kindergarten

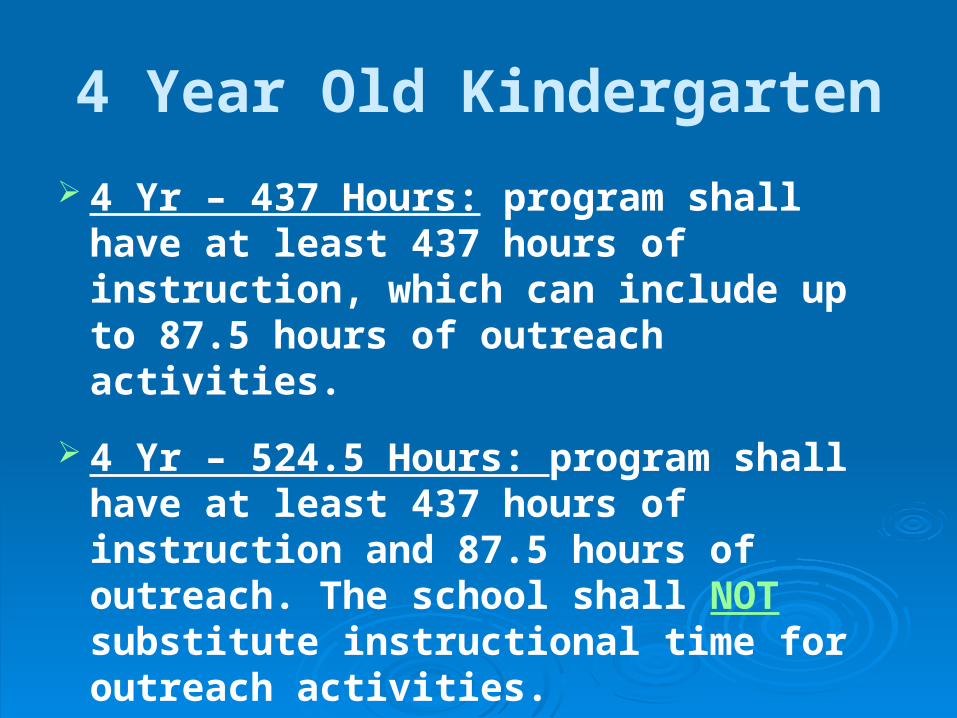

4 Yr – 437 Hours: program shall have at least 437 hours of instruction, which can include up to 87.5 hours of outreach activities.

4 Yr – 524.5 Hours: program shall have at least 437 hours of instruction and 87.5 hours of outreach. The school shall NOT substitute instructional time for outreach activities.

4 Year Old Kindergarten

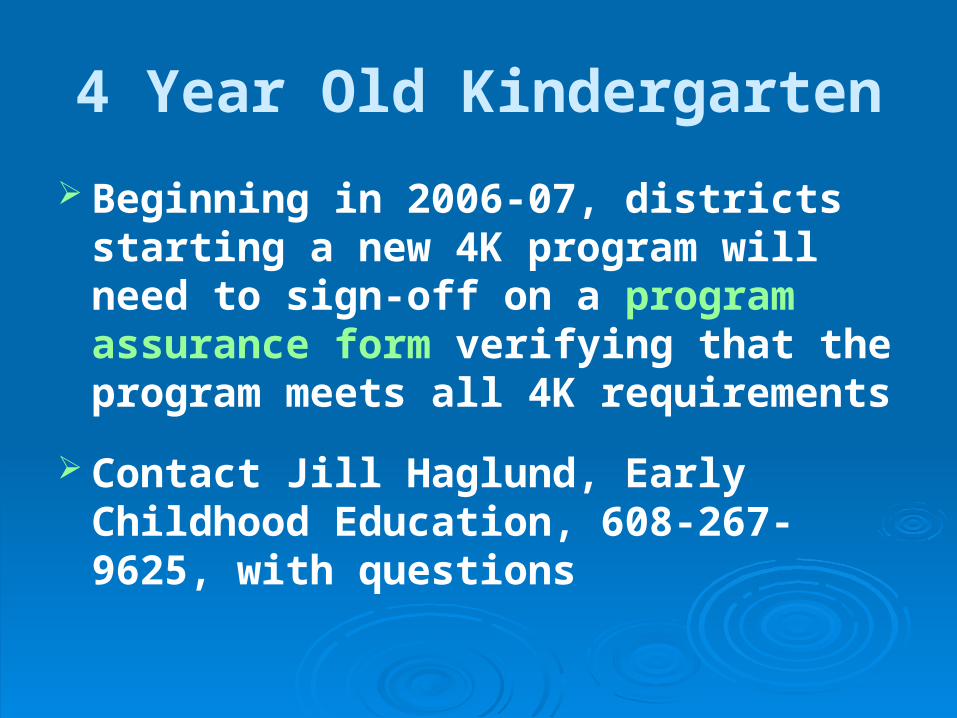

Beginning in 2006-07, districts starting a new 4K program will need to sign-off on a program assurance form verifying that the program meets all 4K requirements

Contact Jill Haglund, Early Childhood Education, 608-267-9625, with questions

5 Year Old Kindergarten

5 Yr Old – Half Day Program 5 Yr Old – Three Full Day Program 5 Yr Old – Four Full Day Program 5 Yr Old – Five Full Day Program 5 Yr Old – Blended Program

The student must be at least 5 years of ageThe student must be at least 5 years of age

on or before September 1on or before September 1stst..

Grades 1 - 12

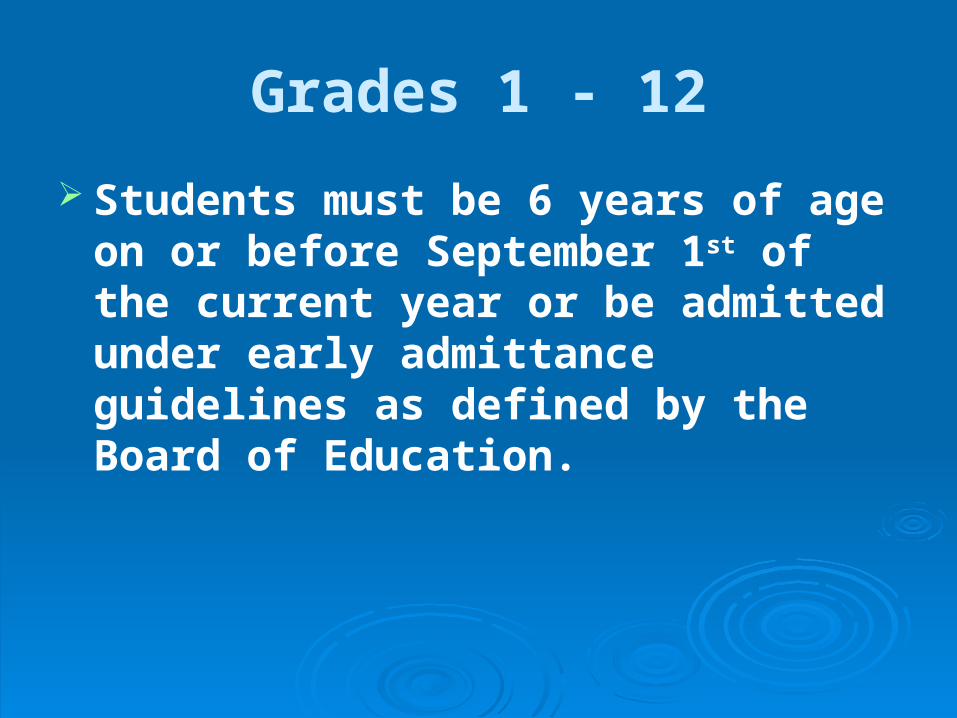

Students must be 6 years of age on or before September 1st of the current year or be admitted under early admittance guidelines as defined by the Board of Education.

October 15th Aid Certification

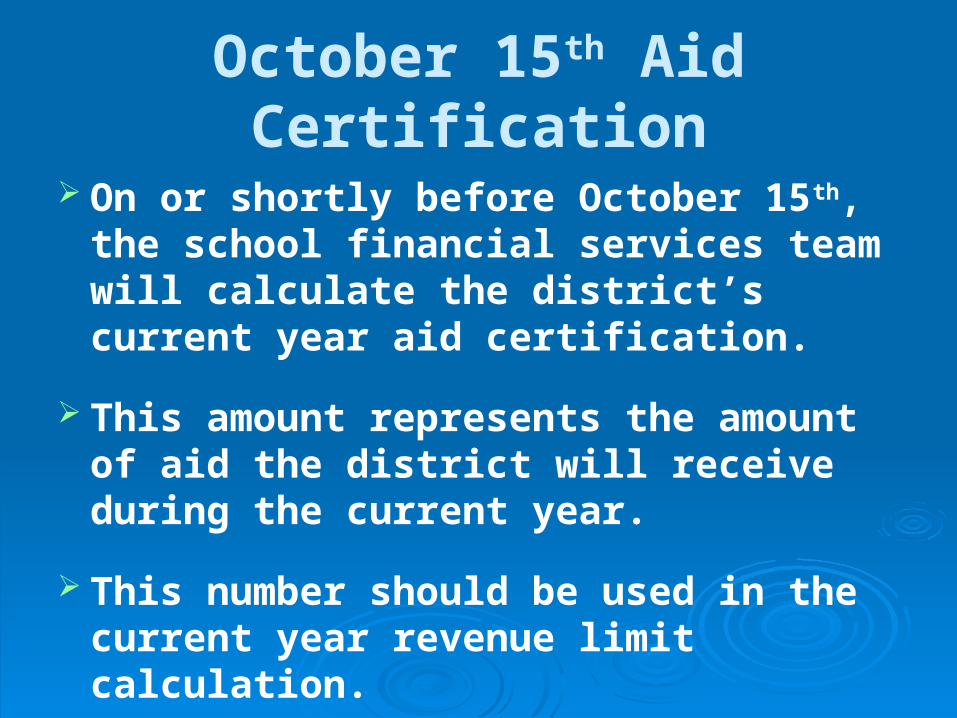

On or shortly before October 15th, the school financial services team will calculate the district’s current year aid certification.

This amount represents the amount of aid the district will receive during the current year.

This number should be used in the current year revenue limit calculation.

Equalization Aid

Purpose of Equalization Aid is to:

Cause the State to assume a greater portion of costs

Relieve the property tax burden

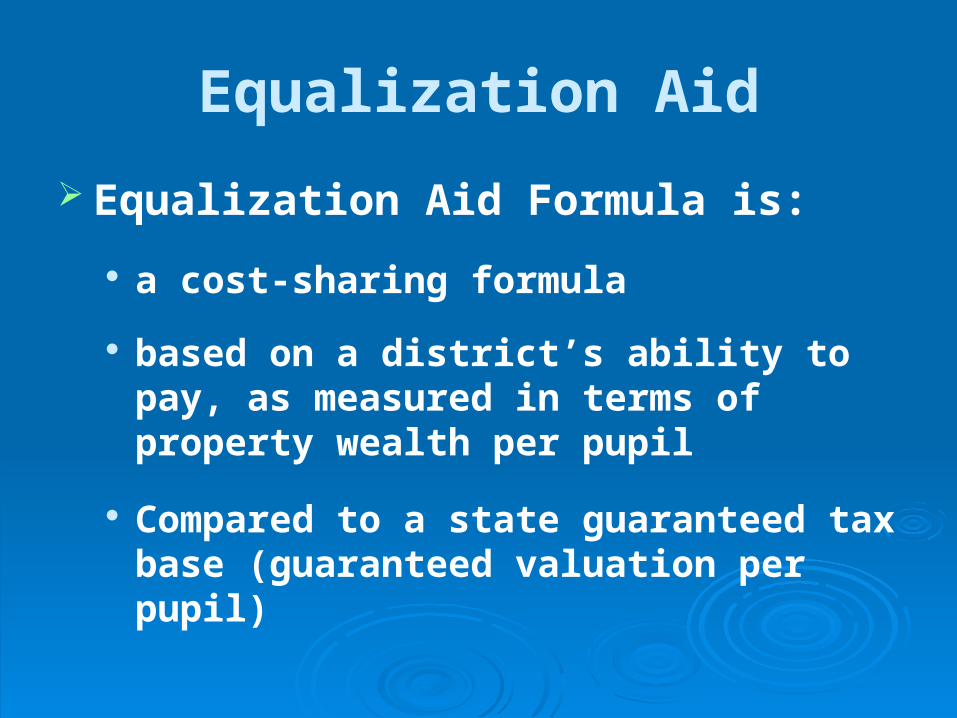

Equalization Aid

Equalization Aid Formula is:

a cost-sharing formula

based on a district’s ability to pay, as measured in terms of property wealth per pupil

Compared to a state guaranteed tax base (guaranteed valuation per pupil)

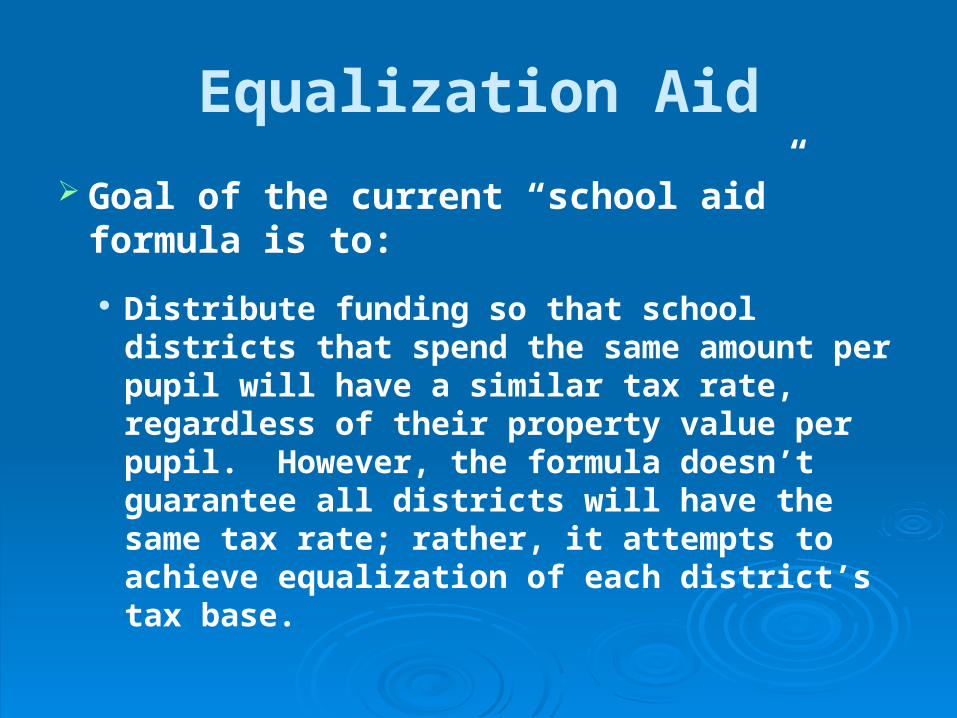

Equalization Aid

Goal of the current “school aid” formula is to:

Distribute funding so that school districts that spend the same amount per pupil will have a similar tax rate, regardless of their property value per pupil. However, the formula doesn’t guarantee all districts will have the same tax rate; rather, it attempts to achieve equalization of each district’s tax base.

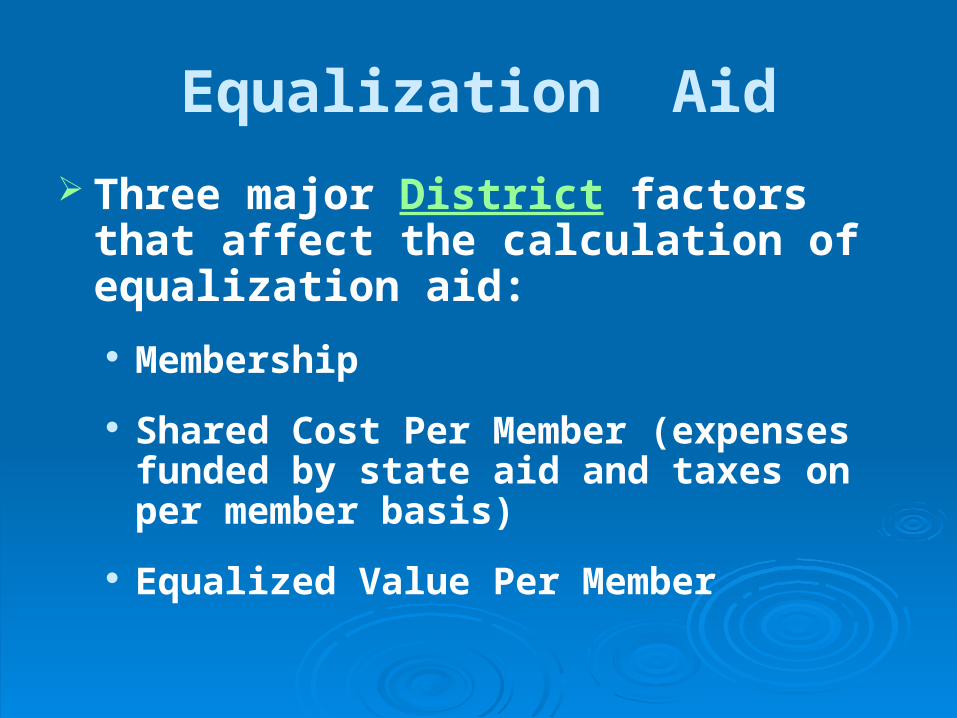

Equalization Aid

Three major District factors that affect the calculation of equalization aid:

Membership

Shared Cost Per Member (expenses funded by state aid and taxes on per member basis)

Equalized Value Per Member

Equalization Aid

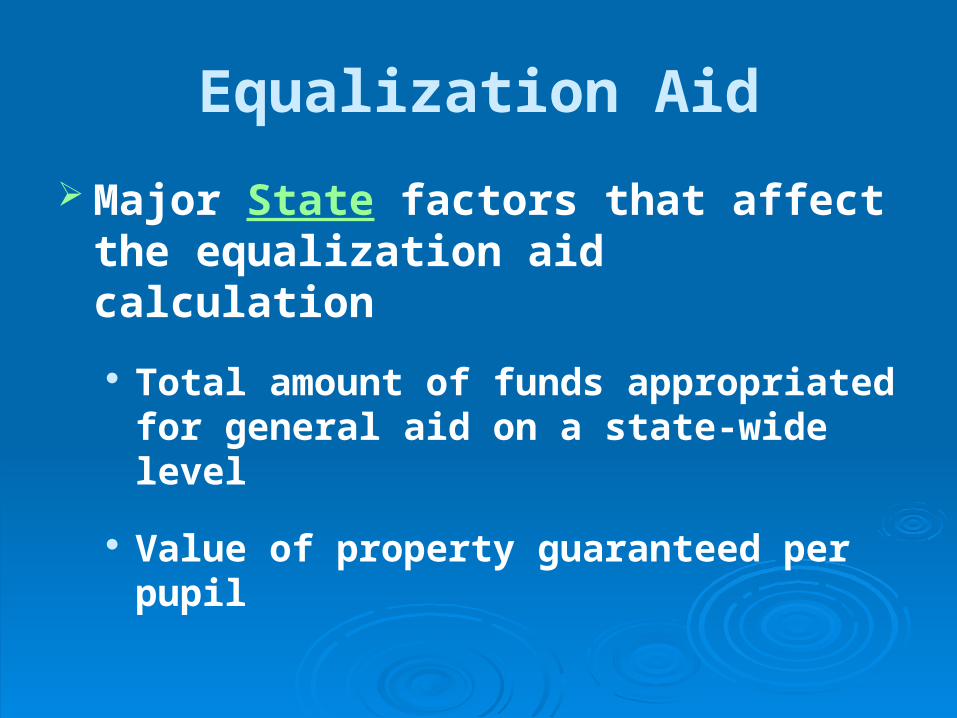

Major State factors that affect the equalization aid calculation

Total amount of funds appropriated for general aid on a state-wide level

Value of property guaranteed per pupil

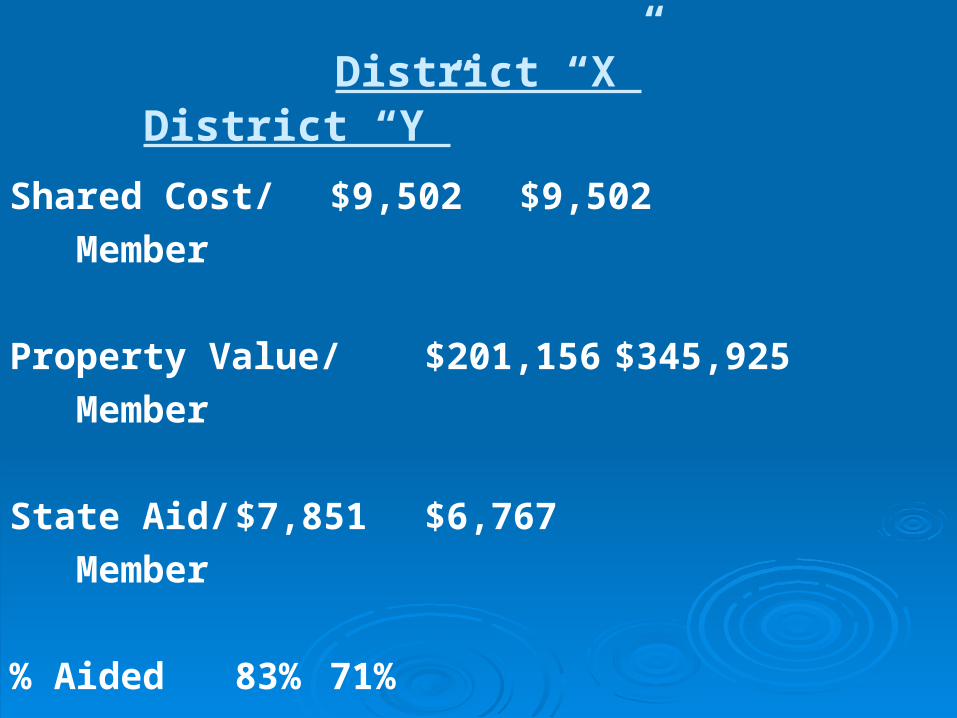

District “X” District “Y”

Shared Cost/ $9,502 $9,502

Member

Property Value/ $201,156 $345,925

Member

State Aid/ $7,851 $6,767

Member

% Aided 83% 71%

Equalization Aid

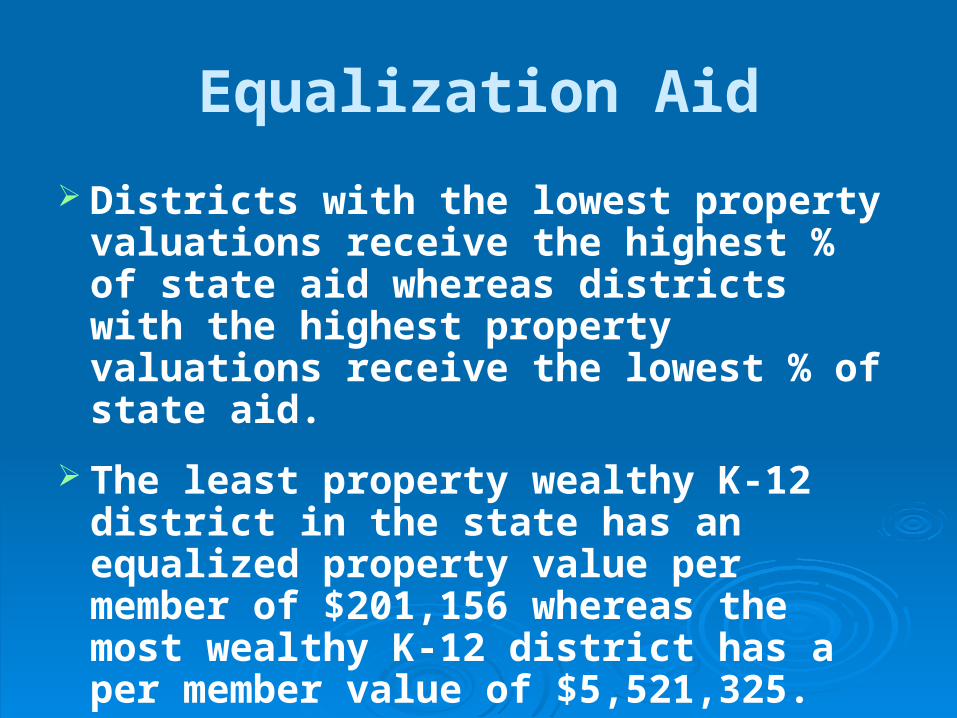

Districts with the lowest property valuations receive the highest % of state aid whereas districts with the highest property valuations receive the lowest % of state aid.

The least property wealthy K-12 district in the state has an equalized property value per member of $201,156 whereas the most wealthy K-12 district has a per member value of $5,521,325.

Revenue Limits

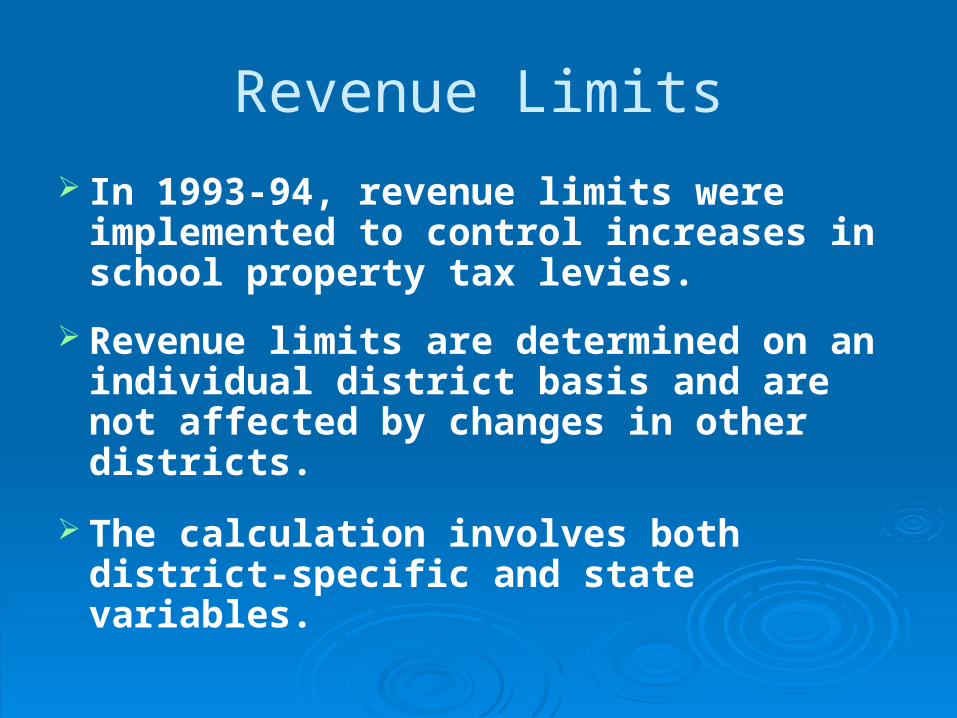

In 1993-94, revenue limits were implemented to control increases in school property tax levies.

Revenue limits are determined on an individual district basis and are not affected by changes in other districts.

The calculation involves both district-specific and state variables.

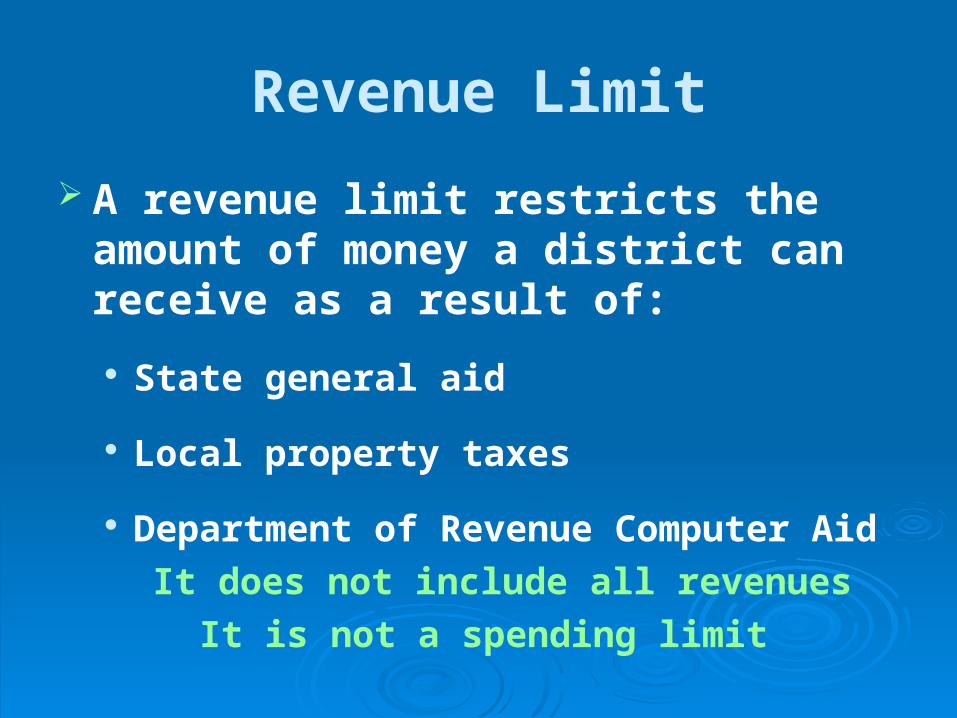

Revenue Limit

A revenue limit restricts the amount of money a district can receive as a result of:

State general aid

Local property taxes

Department of Revenue Computer Aid

It does not include all revenues

It is not a spending limit

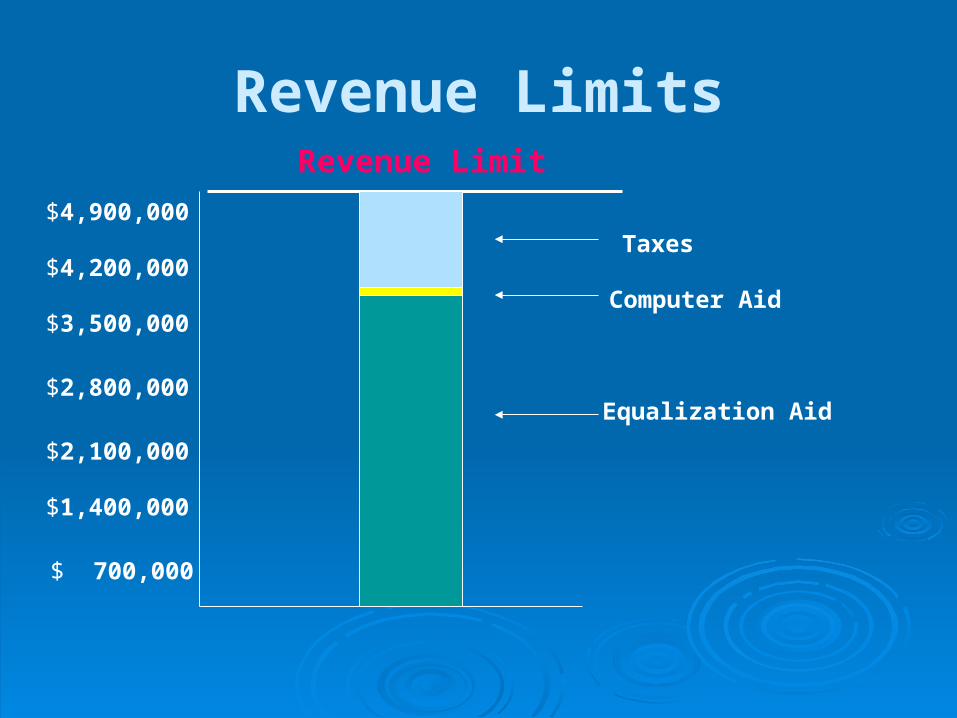

Revenue Limits

$ 700,000

$1,400,000

$2,100,000

$2,800,000

$3,500,000

$4,200,000

$4,900,000

Revenue Limit

Equalization Aid

Computer Aid

Taxes

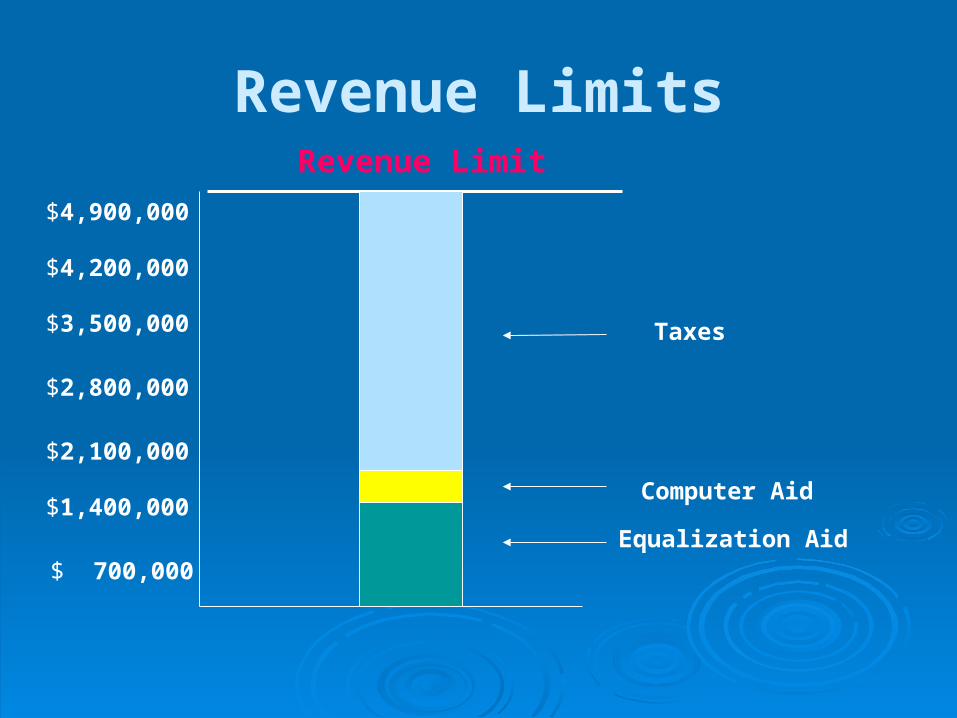

Revenue Limits

$ 700,000

$1,400,000

$2,100,000

$2,800,000

$3,500,000

$4,200,000

$4,900,000

Revenue Limit

Equalization Aid

Computer Aid

Taxes

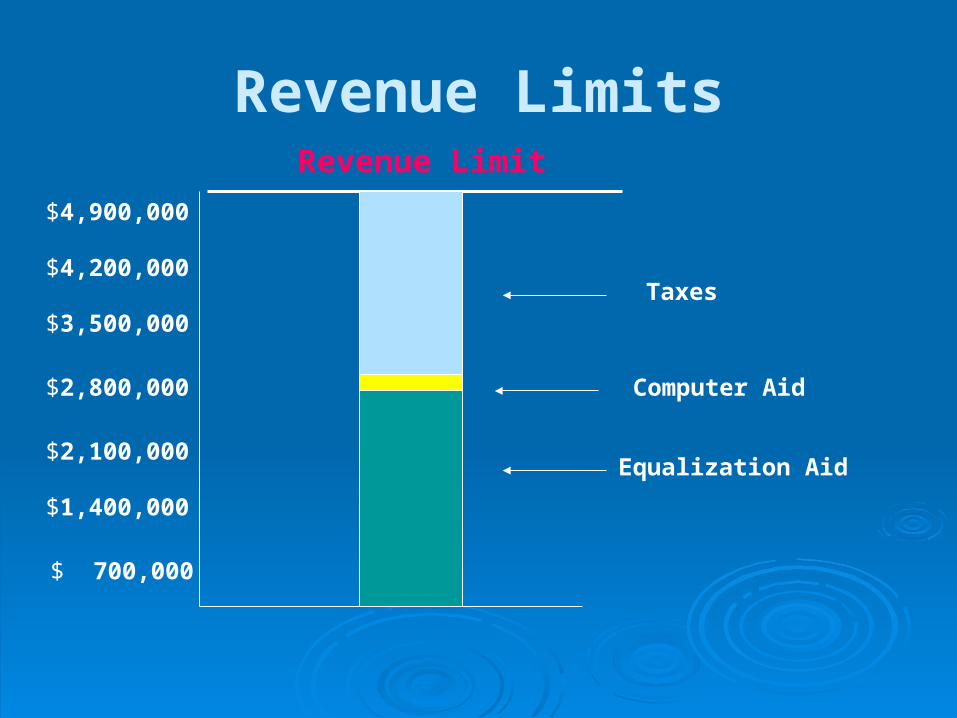

Revenue Limits

$ 700,000

$1,400,000

$2,100,000

$2,800,000

$3,500,000

$4,200,000

$4,900,000

Revenue Limit

Equalization Aid

Computer Aid

Taxes

Revenue Limits

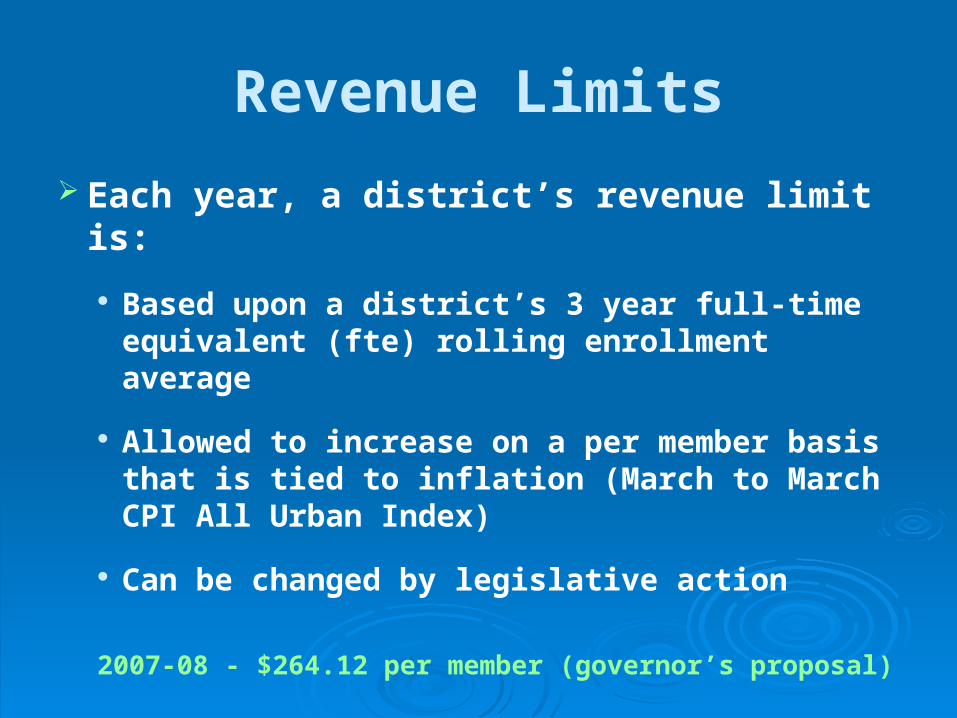

Each year, a district’s revenue limit is:

Based upon a district’s 3 year full-time equivalent (fte) rolling enrollment average

Allowed to increase on a per member basis that is tied to inflation (March to March CPI All Urban Index)

Can be changed by legislative action

2007-08 - $264.12 per member (governor’s proposal)

Revenue Limits

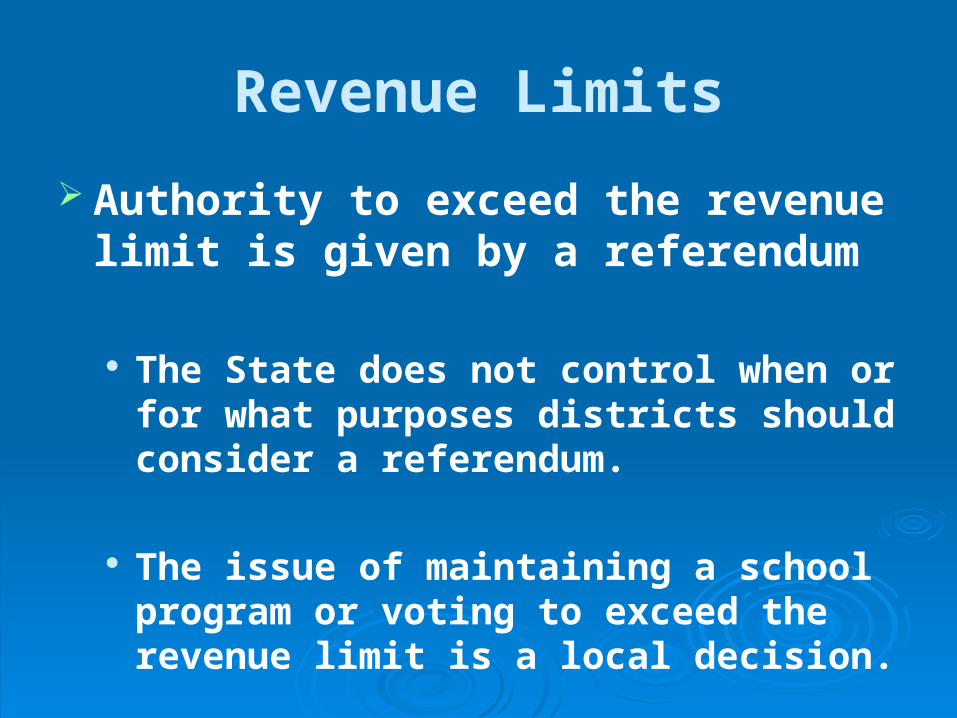

Authority to exceed the revenue limit is given by a referendum

The State does not control when or for what purposes districts should consider a referendum.

The issue of maintaining a school program or voting to exceed the revenue limit is a local decision.

Referendum

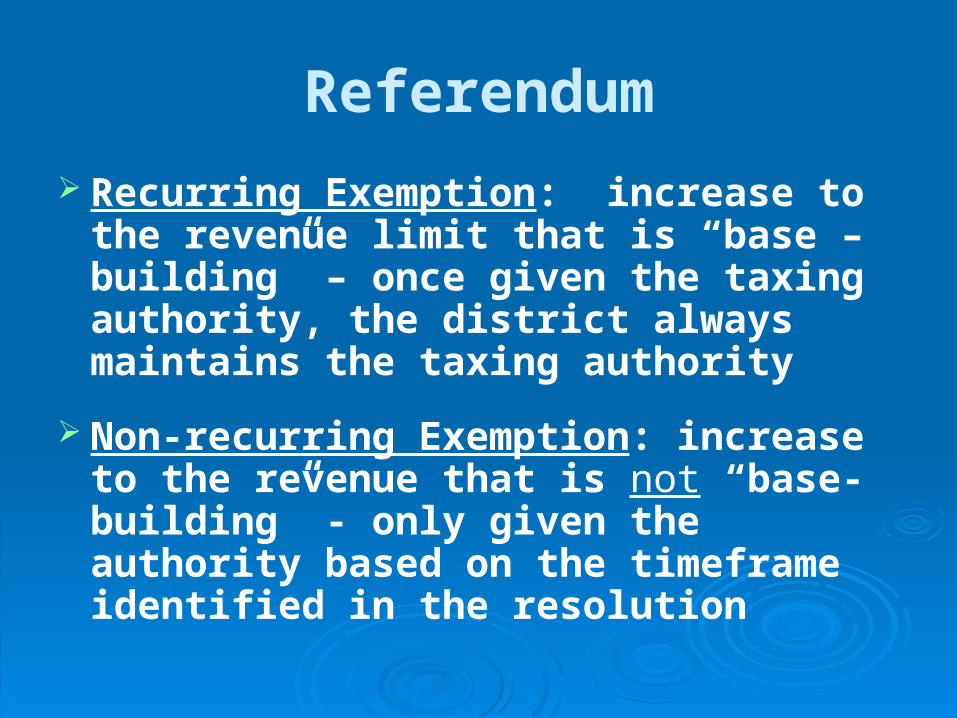

Recurring Exemption: increase to the revenue limit that is “base –building” – once given the taxing authority, the district always maintains the taxing authority

Non-recurring Exemption: increase to the revenue that is not “base-building” - only given the authority based on the timeframe identified in the resolution

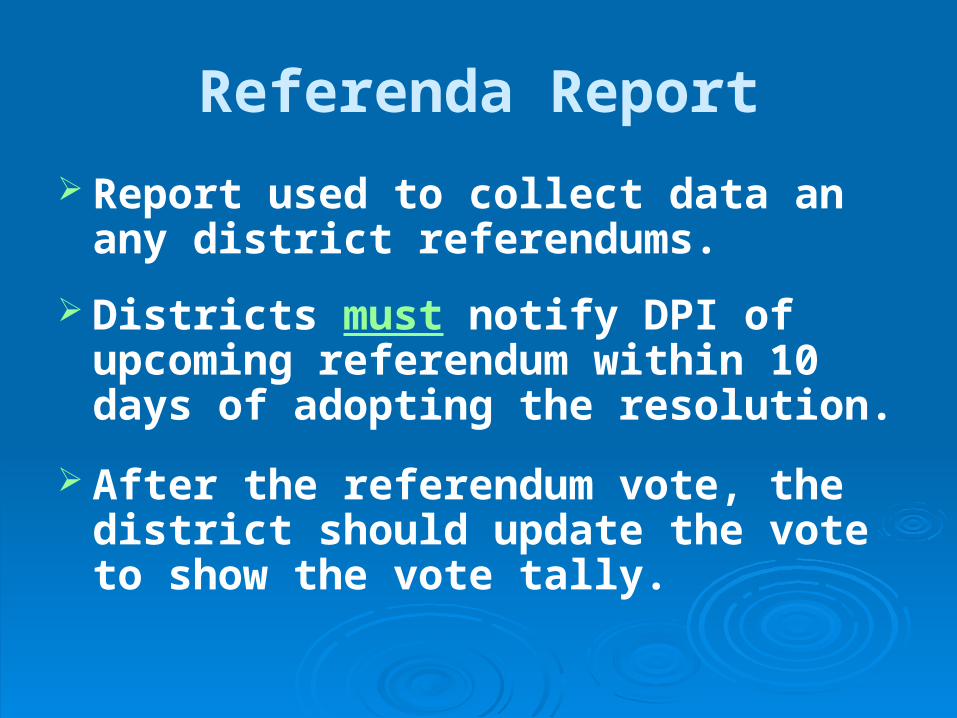

Referenda Report

Report used to collect data an any district referendums.

Districts must notify DPI of upcoming referendum within 10 days of adopting the resolution.

After the referendum vote, the district should update the vote to show the vote tally.

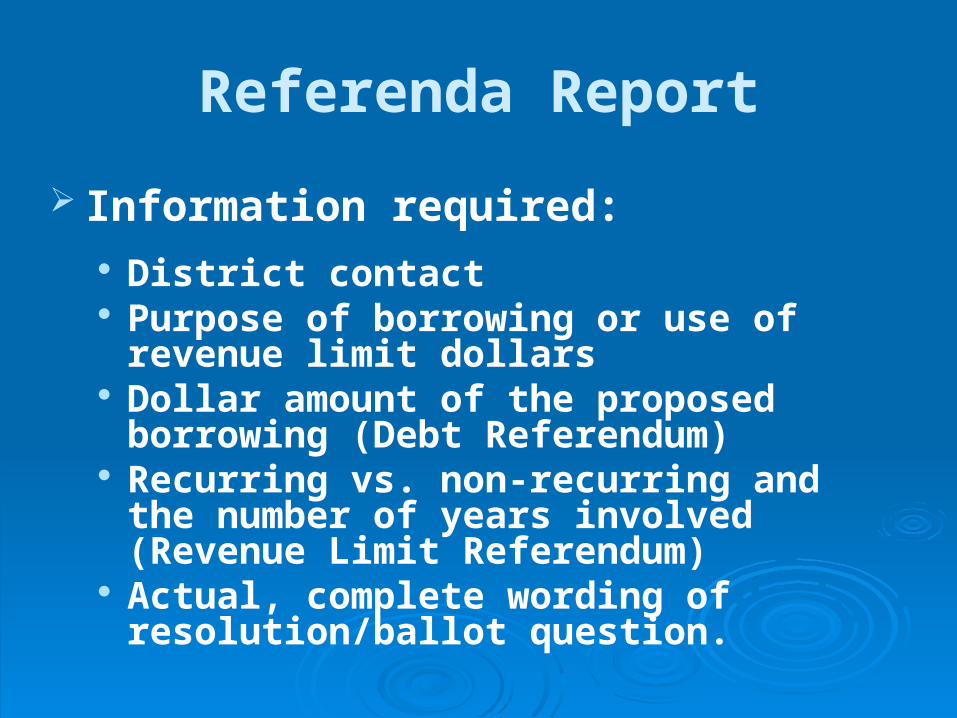

Referenda Report

Information required: District contact Purpose of borrowing or use of revenue

limit dollars Dollar amount of the proposed borrowing

(Debt Referendum) Recurring vs. non-recurring and the

number of years involved (Revenue Limit Referendum)

Actual, complete wording of resolution/ballot question.

Referenda Report

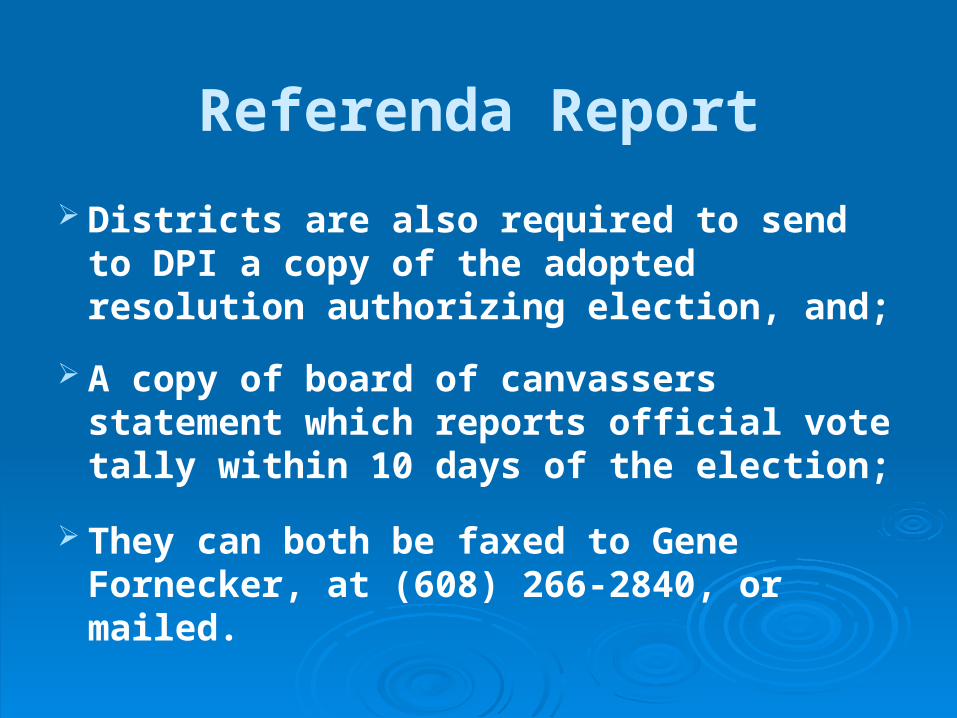

Districts are also required to send to DPI a copy of the adopted resolution authorizing election, and;

A copy of board of canvassers statement which reports official vote tally within 10 days of the election;

They can both be faxed to Gene Fornecker, at (608) 266-2840, or mailed.

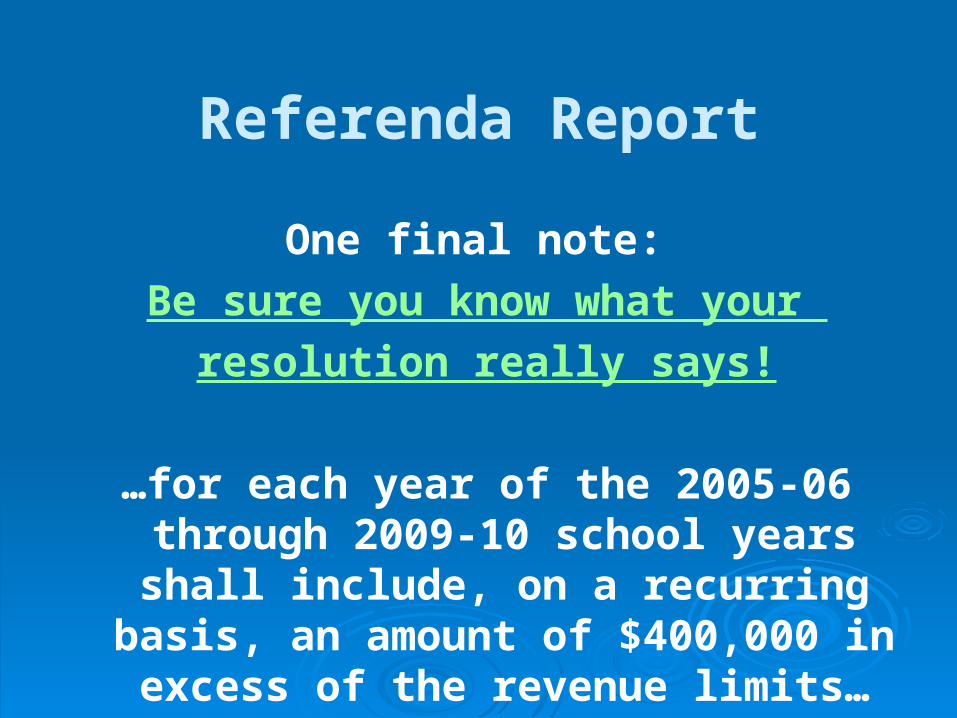

One final note:

Be sure you know what your

resolution really says!

…for each year of the 2005-06 through 2009-10 school years shall include, on

a recurring basis, an amount of $400,000 in excess of the revenue

limits…

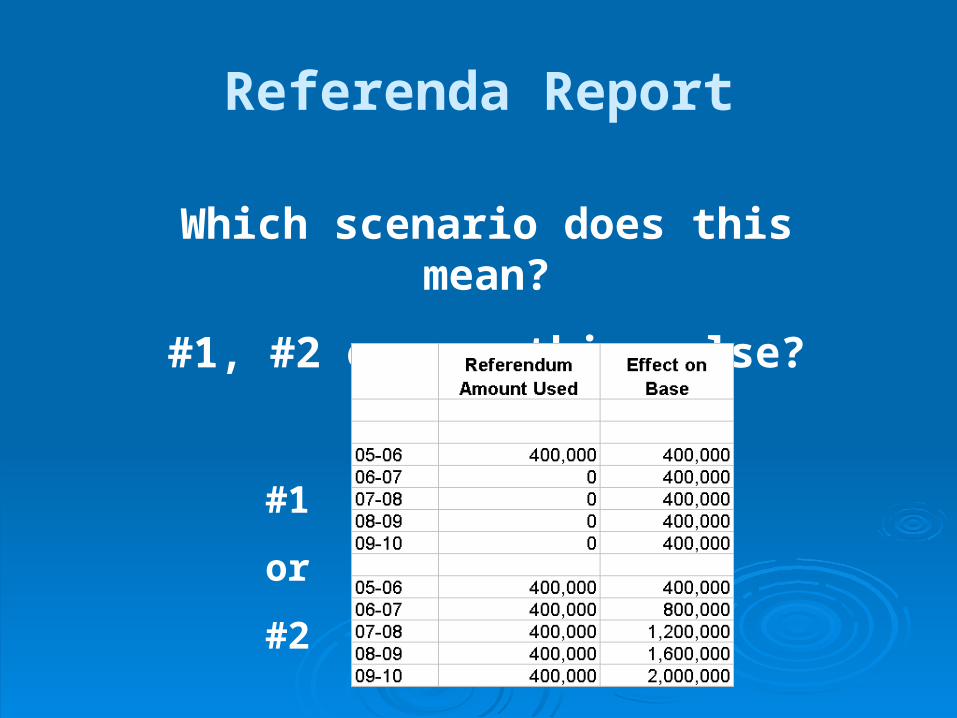

Referenda Report

Referenda Report

Which scenario does this mean?

#1, #2 or something else?

#1

or

#2

Revenue Limit

Although the district should be creating an estimated revenue limit throughout the entire budget development process, the revenue limit from which the tax is levied is calculated in late October.

Tax Levy Report

Report used to collect the district’s current year tax levies and mill rates.

Data from the report is automatically downloaded into tax levy certification forms that are sent by the district to the taxing municipalities.

Data from the report is automatically shared with the Department of Revenue.

Tax Levy On or before November 1, every public school board

must approve the levy amounts necessary

to operate and maintain district schools (s.120.12(3) Wis. Stats.),

to meet any irrepealable tax obligations (s.120.12(4) Wis. Stats.).

School district property taxes include levies for the general operations, debt service, capital expansion, and community service funds

On or before November 6, the school district clerk must certify to each municipal clerk the amount of school district tax to be assessed on the tax rolls of that municipality (s.120.12(3) Wis. Stats.).

PI 1504 – Budget Report

Report used to collect the district proposed revenue and expenses for all funds for the current fiscal year.

Data is used to calculate the district’s following year aid estimate provided on July 1st as per state statute 121.15(4)(b)

Special Education Budget Report

Report used to collect the district’s proposed special education (fund 27) expenditures and revenues.

Data is used to estimate future special education categorical aid payments.

July - December

What activities take place relating to the next fiscal year

(2008-09)?

2008-09 Budget Development

Although detailed budget development usually doesn’t start until late December/early January, you should be thinking about: Enrollment trends Changing district dynamics (development,

population trends, etc……) Revenue trends Impact of negotiations

6 Months zipped by!

Are you ready for 6 more???

January - June

What activities take place relating to the prior fiscal year

(2006-07)?

Prior Year Finishing Touches

The School Financial Services team is auditing the prior year annual and audit reports.

Prior year activity is primarily limited to responding to questions that arise as a result of those audits.

January - June

What activities take place relating to the current fiscal year

(2007-08)?

January Pupil Count Report

Report used to collect district count data for the 2nd Friday in January.

Data is converted to full-time equivalency and used in the calculation of a district’s equalization aid.

Membership Audit

On or about February 1st, the School Finance Team will announce which districts are required to have a membership audit.

The district’s auditor will verify the district’s reported counts for 2nd Friday in September 3rd Friday in January Summer School (as well as fees)

Debt Schedule Report

Report used to collect the district’s long-term debt repayment schedules for all district indebtedness.

Data used to project future equalization aid payments from a state-wide perspective.

Debt schedule report should be updated anytime new debt has been issued or existing debt has been amended.

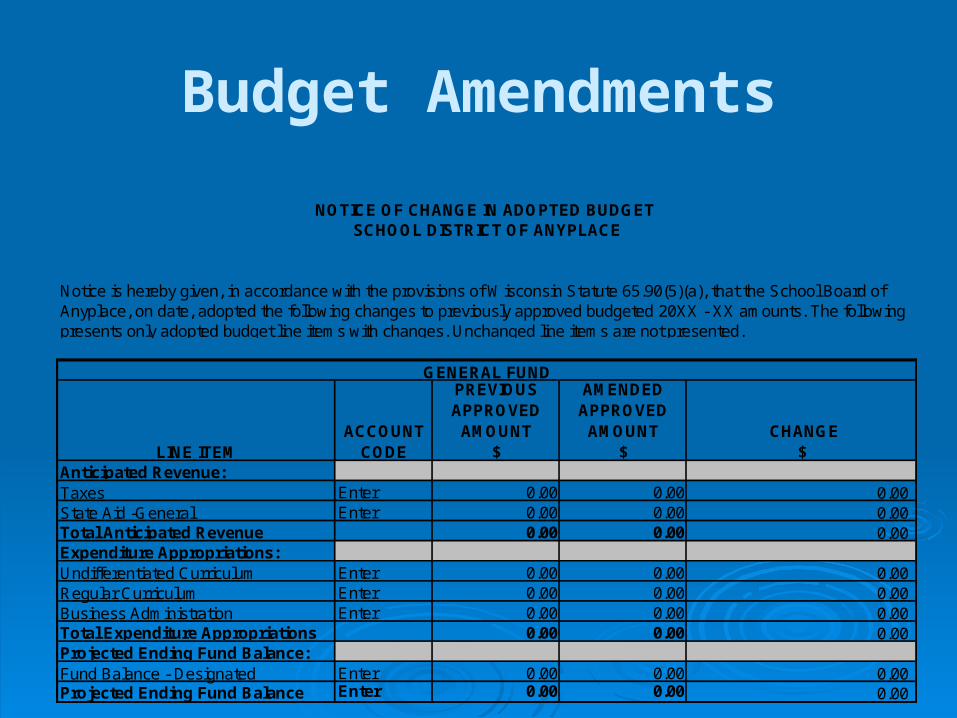

Budget Amendments

As the current budget year progresses, you may find expenditure needs that differ from the budget that was originally approved.

Changes in amount of appropriation and purposes (functions) must be approved by a two-thirds vote of the school board.

Publish a class 1 notice of the budget change within 10 days of Board approval.

Budget Amendments

GENERAL FUND

LINE ITEMACCOUNT

CODE

PREVIOUS APPROVED

AMOUNT $

AMENDED APPROVED

AMOUNT $

CHANGE $

Anticipated Revenue: Taxes Enter 0.00 0.00 0.00State Aid -General Enter 0.00 0.00 0.00Total Anticipated Revenue 0.00 0.00 0.00Expenditure Appropriations:Undifferentiated Curriculum Enter 0.00 0.00 0.00Regular Curriculum Enter 0.00 0.00 0.00Business Administration Enter 0.00 0.00 0.00Total Expenditure Appropriations 0.00 0.00 0.00Projected Ending Fund Balance:Fund Balance - Designated Enter 0.00 0.00 0.00Projected Ending Fund Balance Enter 0.00 0.00 0.00

NOTICE OF CHANGE IN ADOPTED BUDGET SCHOOL DISTRICT OF ANYPLACE

Notice is hereby given, in accordance with the provisions of Wisconsin Statute 65.90(5)(a), that the School Board of Anyplace, on date, adopted the following changes to previously approved budgeted 20XX - XX amounts. The following presents only adopted budget line items with changes. Unchanged line items are not presented.

January - June

What activities take place relating to the next fiscal year

(2008-09)?

2008-09 Budget Development

Review District Accounting Structure

Determine if the current accounting structure meets your information and reporting needs

Determine if the school financial services team has made any changes to WUFAR that would require new account codes http://www.dpi.wi.gov/sfs/wufar.html

2008-09 Budget Development

Develop enrollment projections

Used in the calculation of the revenue limit

Used in determining staffing needs

Used in calculating other revenues such as local fees

2008-09 Budget Development

Develop Preliminary Revenues

Calculate an estimated revenue limit – very important as this is the largest revenue source of the district and greatly impacts the district’s expenditure budgeting

Review trends to estimate categorical aids and other local revenues

Identify potential grant sources

2008-09 Budget Development

Develop Preliminary Expenditures

Reviewing staffing needs and expenditure levels – many contracts require advance notice in the event staff reductions, layoffs, non-renewals, etc……are needed

Review program offerings to see if expenditure requirements have changed

Review trends in utility, insurance, and other related expenses

Take a deep breath!

You are not alone……….

Questions???

Brad Adams, Consultant, 267-3752 Lori Ames, Consultant, 266-3464 Karen Kucharz, Consultant, 267-9707 Jerry Landmark, Asst. Dir., 267-9209 Kathy Guralski, Auditor, 266-3862 Gene Fornecker, Auditor, 267-7882 Natalie Rew, Auditor, 267-9212 David Carlson, Director, 266-6968