Fiscal Union - Economie · • Some degree of fiscal harmonization (but also corporate governance...

12

Fiscal Union L’harmonisation fiscale européenne nécessaire ? Guntram Wolff Bercy September 24.2013

Transcript of Fiscal Union - Economie · • Some degree of fiscal harmonization (but also corporate governance...

Fiscal Union

L’harmonisation fiscale

européenne nécessaire ?

Guntram Wolff Bercy

September 24.2013

Fiscal union: yes or no?

9/25/2013 © Bruegel 2013 2

• Many new measures introduced since the crisis: increased surveillance, ESM, liquidity provision by the ECB, OMT • Main risk absorption channel in monetary union is capital and credit markets (~70%) (Asdrubali et al 1996). complete single market for capital and banking union •banking union: principle aim to de-link financing conditions from the government sector. • „It is imperative to break the vicious circle between banks and sovereigns“

Credit default swap risk premia on 5 year bonds by sector – Italy

Banking union: progress report

9/25/2013 © Bruegel 2013 5

• Banking union clearly not finished. Correlation between banks and soverereigns remains high. • What else is needed?

• More European banks, balance sheet exposure spread across several countries, including in terms of sovereign debt • identical standards as regards the pecking order of creditors • single resolution authority • common fiscal backstop (i.e. limited fiscal union)

• If this is achieved, more fiscal union needed?

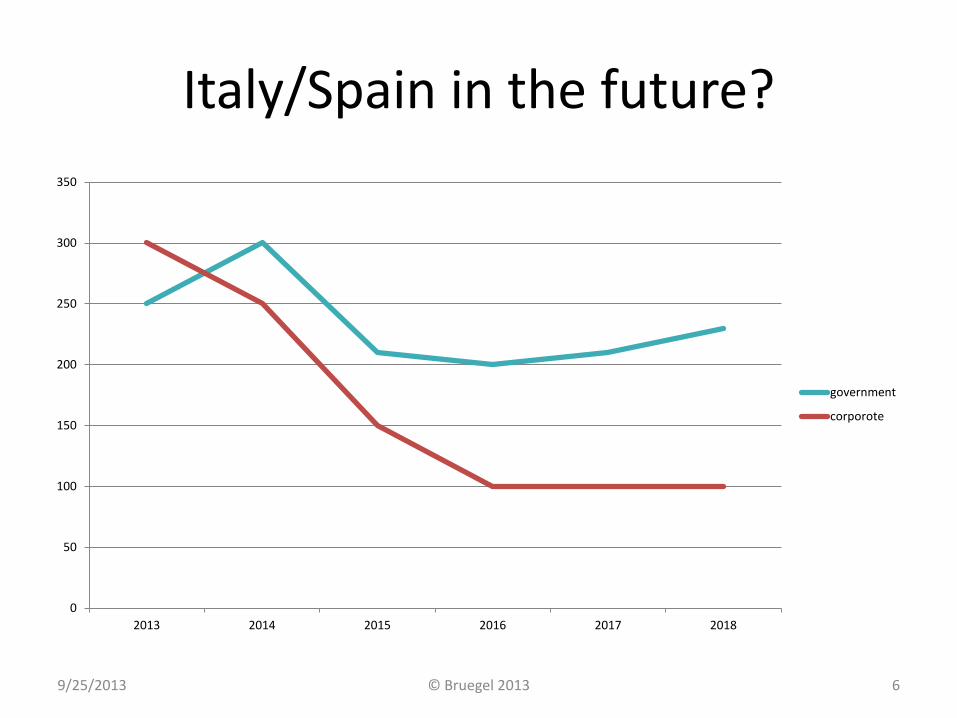

Italy/Spain in the future?

9/25/2013 © Bruegel 2013 6

0

50

100

150

200

250

300

350

2013 2014 2015 2016 2017 2018

government

corporote

How to complete single market for capital?

Harmonization of regulation and taxation

9/25/2013 © Bruegel 2013 7

• Capital markets are underdeveloped in Europe • They are predominantly national • This renders monetary union unstable as the main risk absorption channel is absent • Corporate governance, insolvency law, regulation and differences in taxation!

Fiscal union: yes or no?

9/25/2013 © Bruegel 2013 8

• Musgrave: public good, stabilization, redistribution • Capital markets: enough to provide adequate regional/aggregate stabilization in extraordinary circumstances? How to deal with deep balance sheet recessions? Net federal transfers to Nevada averaged $20 billion annually during the crisis, dwarfing the state government’s $2 billion average deficit and accounting for a significant fraction of its $130 billion GDP. •Aggregate fiscal stabilization With decentralized fiscal policy, the aggregate stablization effort will be sub-optimal

• euro area public good? (or EU?)

9/25/2013 © Bruegel 2013 9

Options for stabilization mechanisms

(i) A federal euro area budget of 2 % of GDP • Federal unemployment expenditure financed with a federal corporate tax

(ii) A support scheme based on deviations from potential output

• Introduce clear rules that trigger federal transfer payments when deviation is large

(iii) Quotas for the issuance of mutually guaranteed debt

• Recourse to limited federal borrowing during financial market volatility

9/25/2013 © Bruegel 2012 10

Options for stabilization mechanisms

Euro-area budget Automatic

transfer scheme

Guaranteed

bonds quota

Principle

Automatic

stabilization role of

federal budget

Transfers based on

output gap

Right to issue

jointly guaranteed

bonds (several

tranches with

increased

withdrawal of

sovereignty

Origin of

stabilisation

Income transfer

from partners

Income transfer

from partners

Borrowing capacity,

mutualisation of

default risk

Advantages True budget

Maximises

stabilization power

for any given level

of contributions

Re-establishes

credibility of public

debt

Drawbacks

Difficulty to agree

on euro-area public

goods. Budget

balance prone to

volatility

Relies on technical

potential output

assumptions.

Mechanical with

little flexibility.

Requires

Eurobonds with

difficult to

impossible

governance

challenge

9/25/2013 © Bruegel 2013 11

Governance

• What kind of commitment devices for mutual guarantees? operate on flows, not stocks • Creation of a euro area treasury

Key is the creation of tax resources, which the EA treasury can directly tax on households/corporations or else

• With credible tax resources, borrowing is easy and aggregate stabilization becomes possible

• Credible tax resources require sound legal basis • They also require sound administrative control (tax collection effort in

Bavaria is lower than other German states) • Political accountability

9/25/2013 © Bruegel 2013 12

Conclusions

• Some degree of fiscal harmonization (but also corporate governance and insolvency practice and legislation) is necessary to complete the single market for capital. • Key immediate priority is to finalize banking union •Minimum fiscal union beyond banking union is desirable to accommodate massive shocks and provide aggregate stabilization • Key issue is the governance of fiscal union • Question of the legacy: More OSI? More PSI?