First Quarter 2009 Results - Norfolk Southern Quarter 2009 Results ... Merchandise. $2,083 $36 2%....

20

First Quarter 2009 Results Donald W. Seale Executive Vice President and Chief Marketing Officer

Transcript of First Quarter 2009 Results - Norfolk Southern Quarter 2009 Results ... Merchandise. $2,083 $36 2%....

First Quarter 2009 ResultsDonald W. SealeExecutive Vice President and Chief Marketing Officer

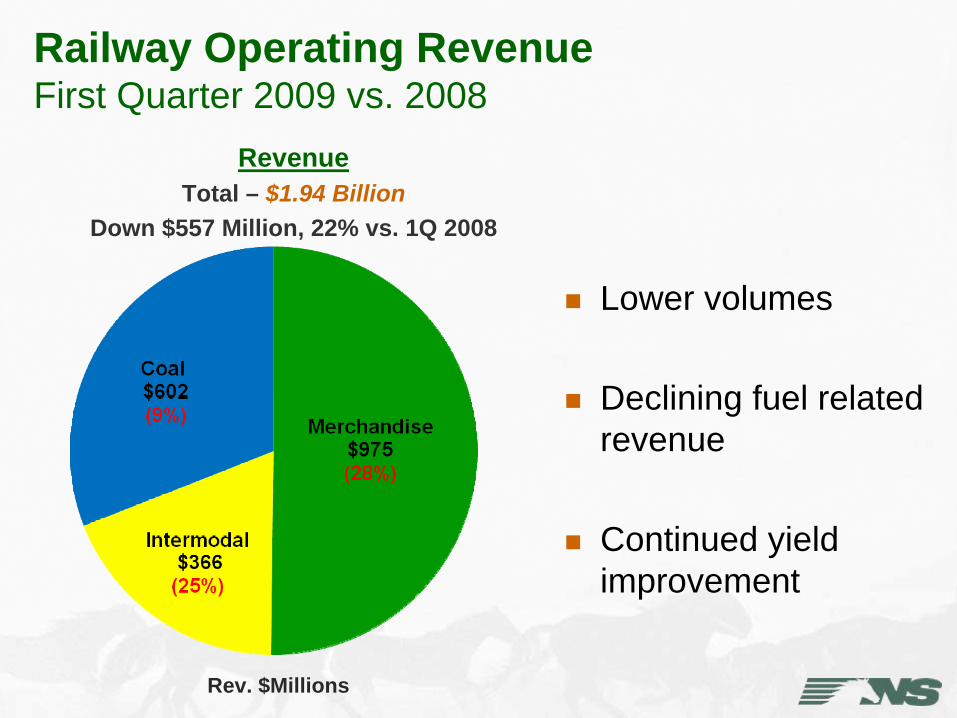

Railway Operating Revenue First Quarter 2009 vs. 2008

RevenueTotal – $1.94 Billion

Down $557 Million, 22% vs. 1Q 2008

Rev. $Millions

Lower volumes

Declining fuel related revenue

Continued yield improvement

Revenue Per Unit First Quarter 2009 vs. 2008

1Q 2009 vs. 1Q 2008

Rev/Unit Abs. % Chg.

Agriculture $2,129 $161 8%

MetCon $1,514 ($122) (7%)

Paper $2,222 $83 4%

Chemicals $2,941 ($45) (2%)

Automotive $1,817 ($91) (5%)

Merchandise $2,083 $36 2%

Intermodal $604 ($52) (8%)

Coal $1,581 $30 2%

Total $1,335 ($32) (2%)

Declining fuel related revenue

Negative RCAF impact

Continued yield improvement

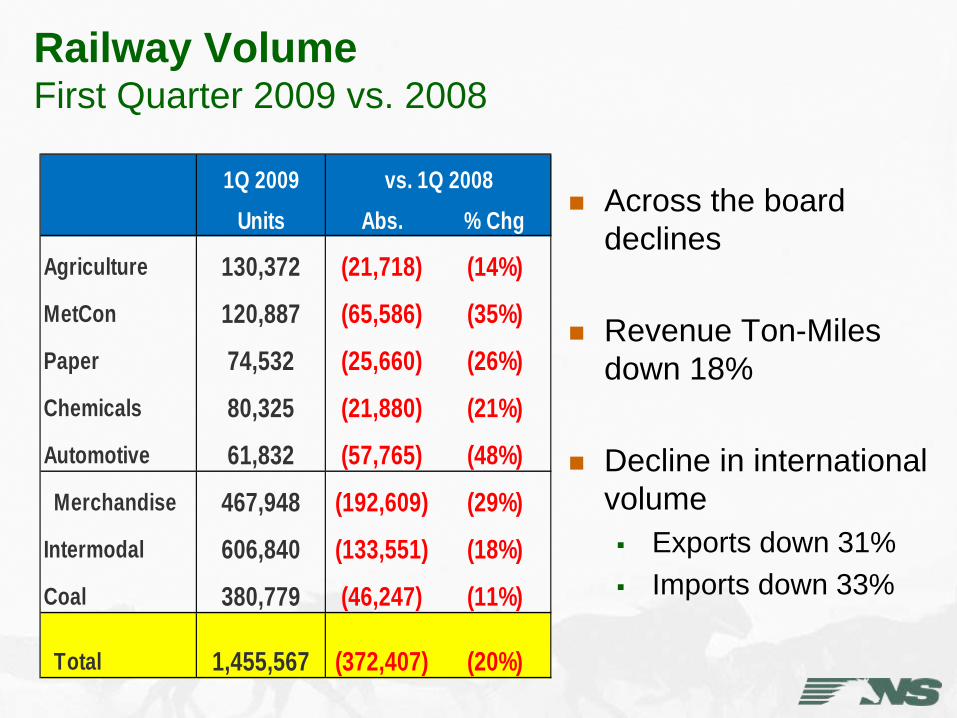

Railway Volume First Quarter 2009 vs. 2008

1Q 2009 vs. 1Q 2008Units Abs. % Chg

Agriculture 130,372 (21,718) (14%)MetCon 120,887 (65,586) (35%)Paper 74,532 (25,660) (26%)Chemicals 80,325 (21,880) (21%)Automotive 61,832 (57,765) (48%) Merchandise 467,948 (192,609) (29%)Intermodal 606,840 (133,551) (18%)Coal 380,779 (46,247) (11%)

Total 1,455,567 (372,407) (20%)

Across the board declines

Revenue Ton-Miles down 18%

Decline in international volume

Exports down 31%Imports down 33%

Coal Variance Analysis First Quarter 2009 vs. 2008

Revenue Carloads Rev/Car

1Q 2009 1Q 2008 ChangeRevenue ($Millions) $602 $662 ($60)

Volume 380,779 427,026 (46,247)

Rev/Car $1,581 $1,551 $30

Coal Markets First Quarter 2009 vs. 2008

Lower electricity demand & higher stockpiles

Competition from natural gas

Decline in domestic & global steel production

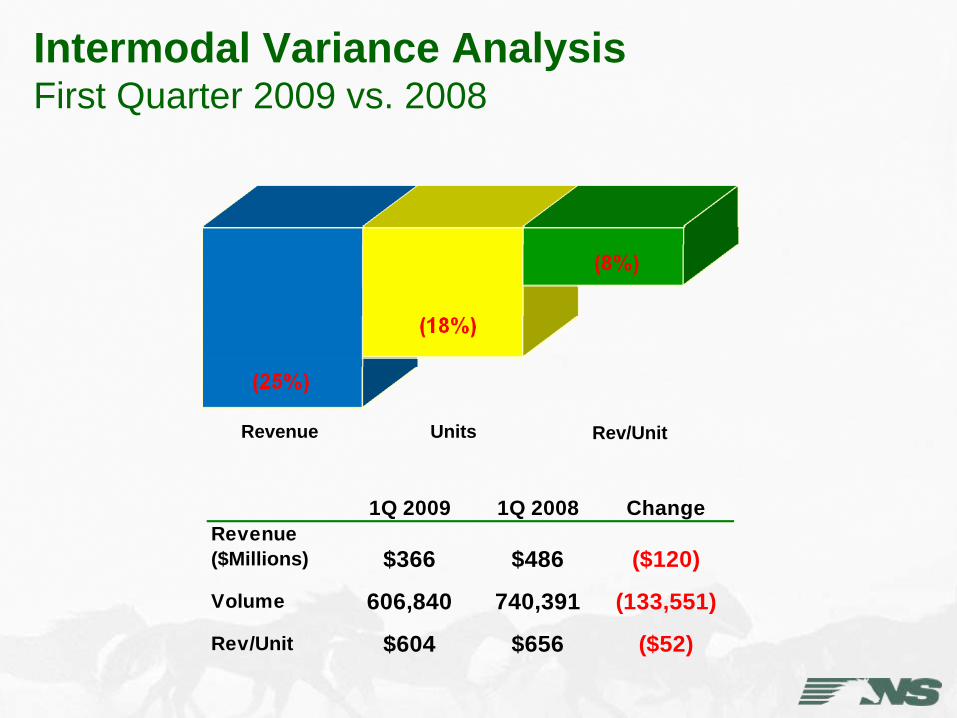

Intermodal Variance Analysis First Quarter 2009 vs. 2008

Revenue Units Rev/Unit

1Q 2009 1Q 2008 ChangeRevenue ($Millions) $366 $486 ($120)

Volume 606,840 740,391 (133,551)

Rev/Unit $604 $656 ($52)

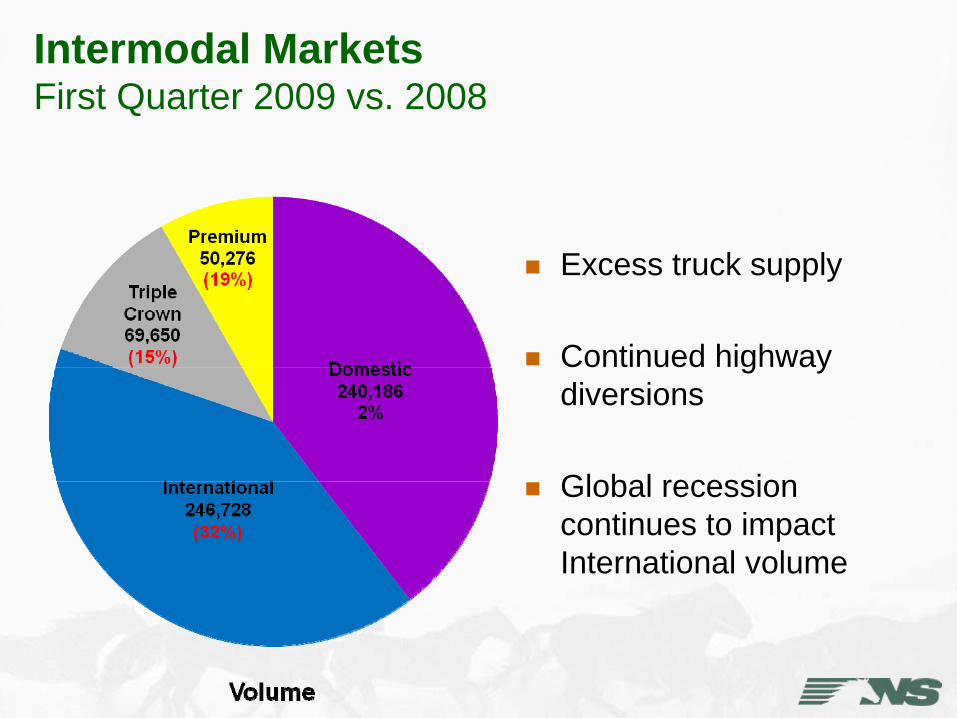

Intermodal Markets First Quarter 2009 vs. 2008

Excess truck supply

Continued highway diversions

Global recession continues to impact International volume

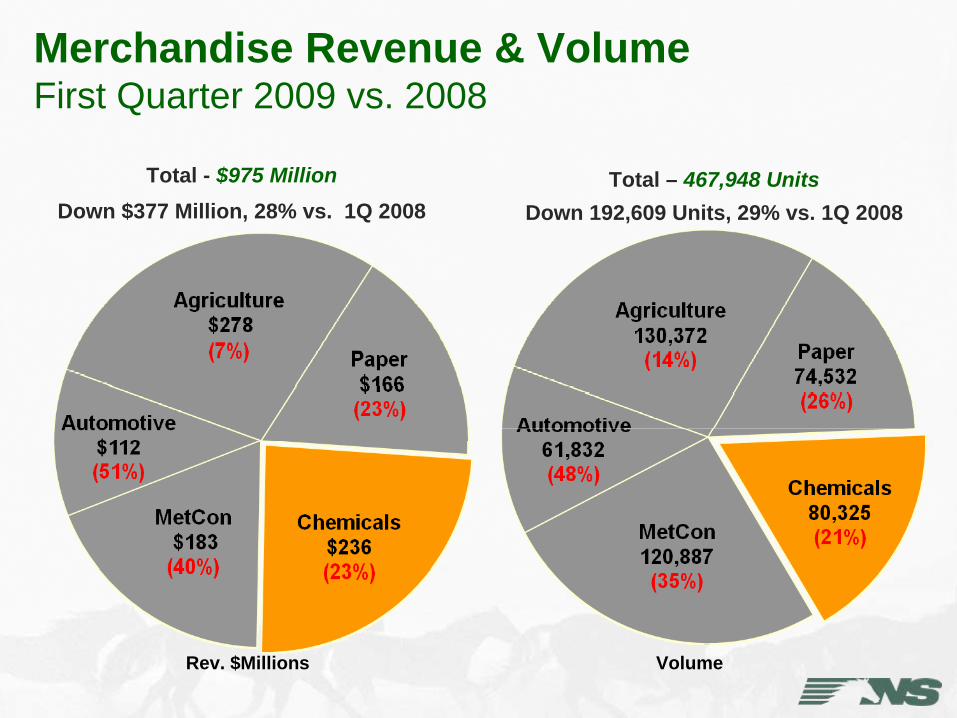

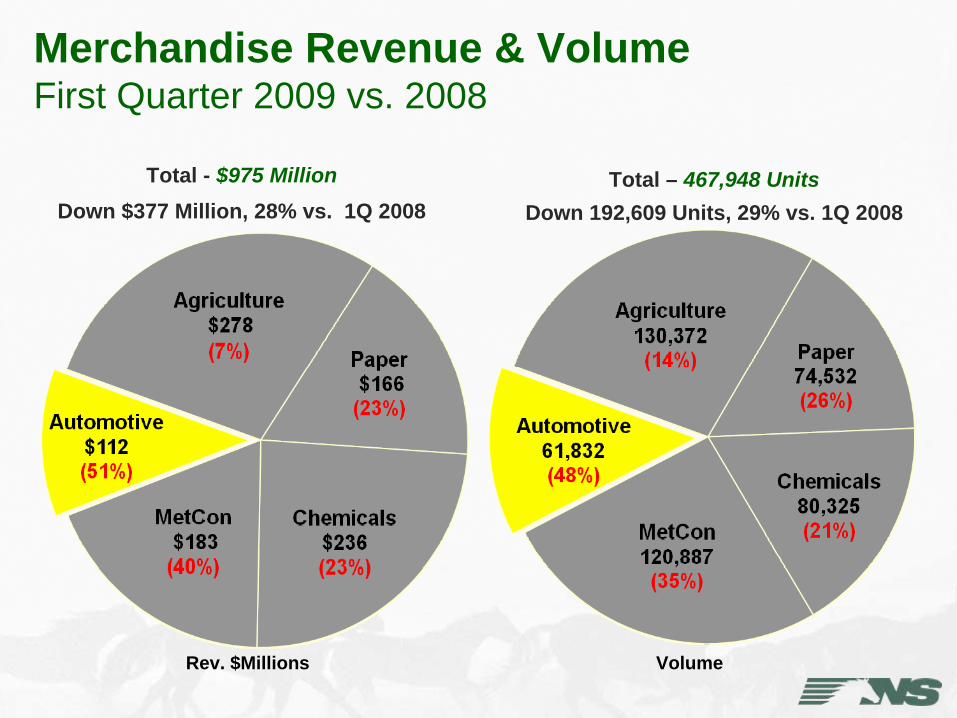

Merchandise Variance Analysis First Quarter 2009 vs. 2008

Revenue Carloads Rev/Car

1Q 2009 1Q 2008 ChangeRevenue ($Millions) $975 $1,352 ($377)

Volume 467,948 660,557 (192,609)

Rev/Car $2,083 $2,047 $36

Merchandise Revenue & Volume First Quarter 2009 vs. 2008

Total - $975 MillionDown $377 Million, 28% vs. 1Q 2008

Rev. $Millions

Total – 467,948 UnitsDown 192,609 Units, 29% vs. 1Q 2008

Volume

Merchandise Revenue & Volume First Quarter 2009 vs. 2008

Total - $975 MillionDown $377 Million, 28% vs. 1Q 2008

Rev. $Millions

Total – 467,948 UnitsDown 192,609 Units, 29% vs. 1Q 2008

Volume

Merchandise Revenue & Volume First Quarter 2009 vs. 2008

Total - $975 MillionDown $377 Million, 28% vs. 1Q 2008

Rev. $Millions

Total – 467,948 UnitsDown 192,609 Units, 29% vs. 1Q 2008

Volume

Merchandise Revenue & Volume First Quarter 2009 vs. 2008

Total - $975 MillionDown $377 Million, 28% vs. 1Q 2008

Rev. $Millions

Total – 467,948 UnitsDown 192,609 Units, 29% vs. 1Q 2008

Volume

Merchandise Revenue & Volume First Quarter 2009 vs. 2008

Total - $975 MillionDown $377 Million, 28% vs. 1Q 2008

Rev. $Millions

Total – 467,948 UnitsDown 192,609 Units, 29% vs. 1Q 2008

Volume

Looking Ahead

Coal

Merchandise

Weak metallurgical demand in U.S. and export markets

Lower electricity demand

Stockpiles at or above target levels

Competition from Natural Gas

Automotive and housing markets – the bottom may be at handProject growth – Scrubber Stone, AgriFuels, Military Traffic and Waste Products

Looking Ahead

IntermodalLocal domestic market growth

Weak international shipments

Continued progress on corridor initiatives and new products

CN-NS MidAmericaCorridor Initiative

In partnership with the CN and WTNN Railroad

Shorter/Faster routes between Midwest and Southeast

New coal route – Illinois Basin to Southeast

Longer term potential as Intermodal route from Chicago to Florida

Titusville, Florida Intermodal Terminal

Opened February 16, 2009

Access to Orlando and Tampa markets

New Intermodal services between major markets

It’s a BLAST!

Joint Venture with Pan Am Railways

STB approved March 10

Closed on April 9

Faster, more reliable service into New England

Expanded auto, Intermodal and transload terminals

Looking Ahead

Pricing EnvironmentStrong safety and service performance

Lower fuel revenue

Continued yield growth reflecting the value of our product

70% of book priced for 2009 on January 1

80% of book priced through first quarter