Finis Milling &BakingNews MarketFAX MARKET UPDATE February 2005.

10

finis Milling &BakingNews MarketFAX MARKET UPDATE February 2005

-

date post

22-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of Finis Milling &BakingNews MarketFAX MARKET UPDATE February 2005.

finis

Milling &BakingNews

MarketFAX

MARKET UPDATEFebruary 2005

2

PBI Market Summary Update

February 10, 2005

Dear Valued Customer:

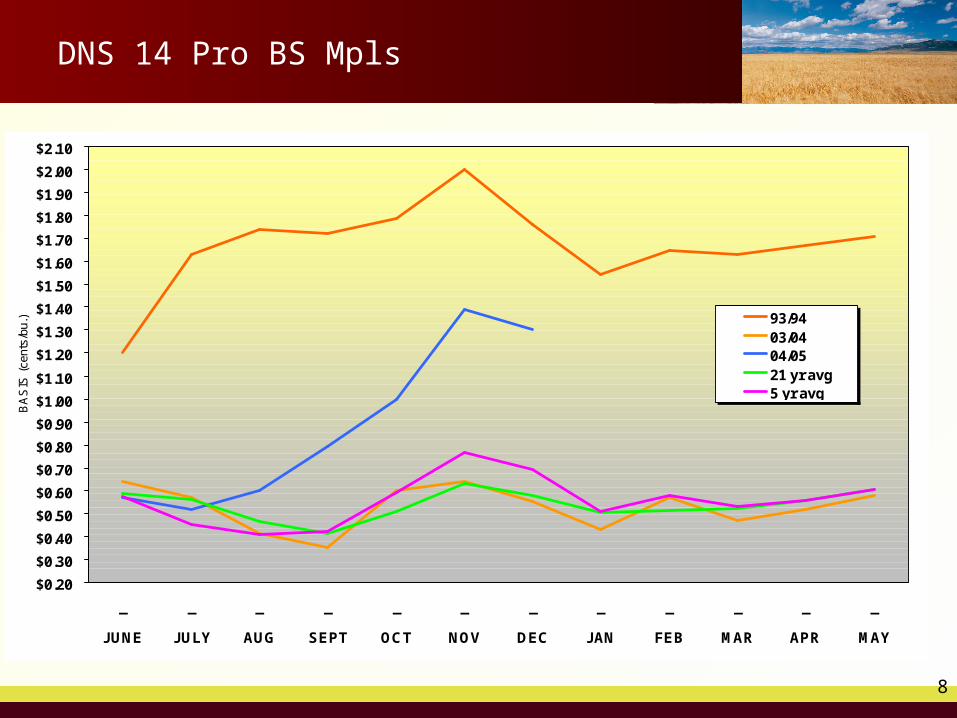

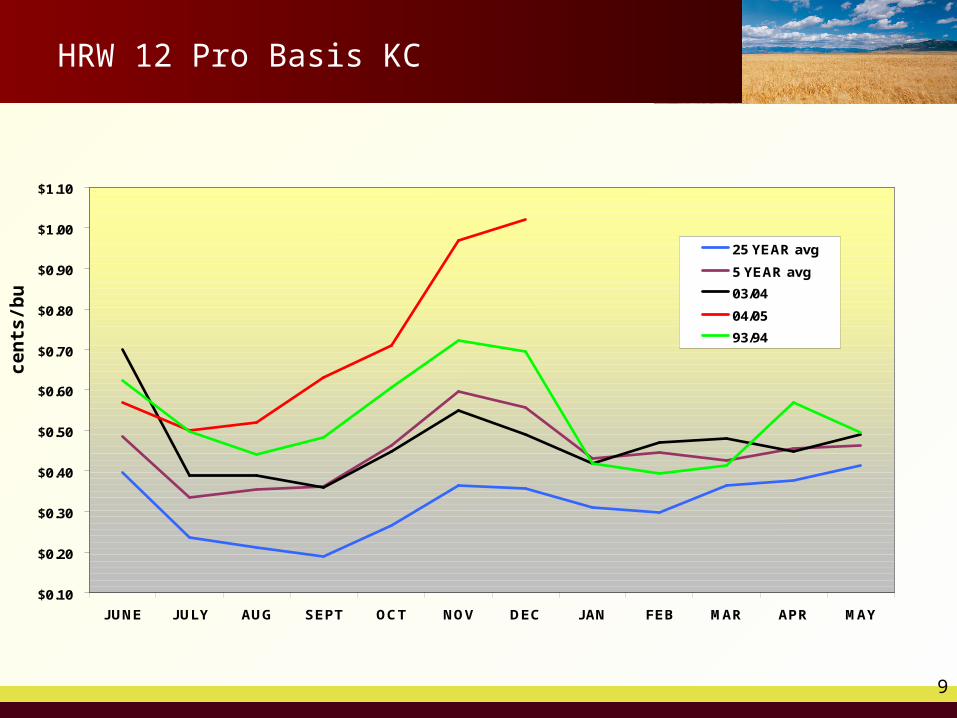

In our December update we outlined some of the key events that had transpired through the end of 2004. The storage and transportation problems that were having a dramatic affect on the protein premiums (basis) are beginning to ease somewhat but, as illustrated in the charts (pages 8 & 9) are still at historically high values. This is due primarily to limited farmer selling, a lower futures board, low protein in the HRS crop, and quality problems in the HRW crop. The farmer has been reluctant to sell many bushels with the board continuing to move lower. Premiums have remained firm, and both Minneapolis and Kansas City have inverted. If this does not convince the farmer to sell, the next way to get more bushels sold is a futures rally.

Record high premium levels have caused both markets to invert in an effort to induce more farmer selling.. Premiums in both the Kansas City and Minneapolis markets will be driven by quality, freight, export demand, and the willingness of the farmer to sell grain.

6 KEY FACTORS TO WATCH

HRW and HRS premiums (Pages 8, 9) continue to trade at near record highs for 04/05. This is due primarily to limited farmer selling, a lower futures board, low protein in the HRS crop, and quality problems in the HRW crop. Record high premium levels have caused both markets to invert in an effort to induce more farmer selling.

• New HRS demand has surfaced for later this year. In the most recent export report, 60,000 metric tons of HRS was reported sold to Egypt for opening Lakes time period. Deliverable stocks in Superior are relatively low at just over 11 million bushels, and if the Egypt sale is a sign of more business to come, we could see a significant rally in Minneapolis premiums and futures.

• The size of the commodity funds continues to grow. Over $118 billion invested in 2004, and we continue to see record net and gross shorts in both wheat and corn. Current gross short of 195,000 in corn, net 106,000, and gross short of 114,000 in wheat, net 56,000. The wheat market will be susceptible to short term spikes higher until the fund short is reduced.

3

Continued From Page 2

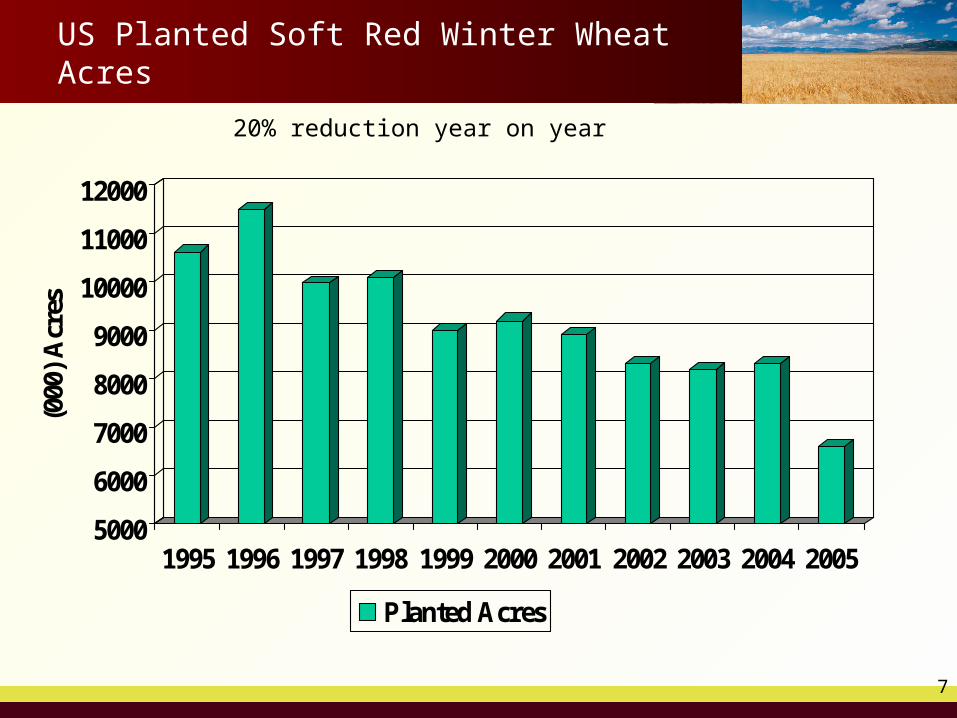

• Winter wheat acreage (Pages 6 & 7) down 4% overall from last year with SRW acreage down 19%. Would expect SRW export and domestic demand to be reduced enough to avoid any serious problems, provided the growing conditions stay ideal. But Chicago futures could rally hard at the first sign of SRW production problems.

• The US continues to lose export business to aggressive world offers. In the most recent GASC tender, Argentina offered wheat at a $33/ton discount to US SRW, and EU offers should move down in February with the addition of export subsidies.

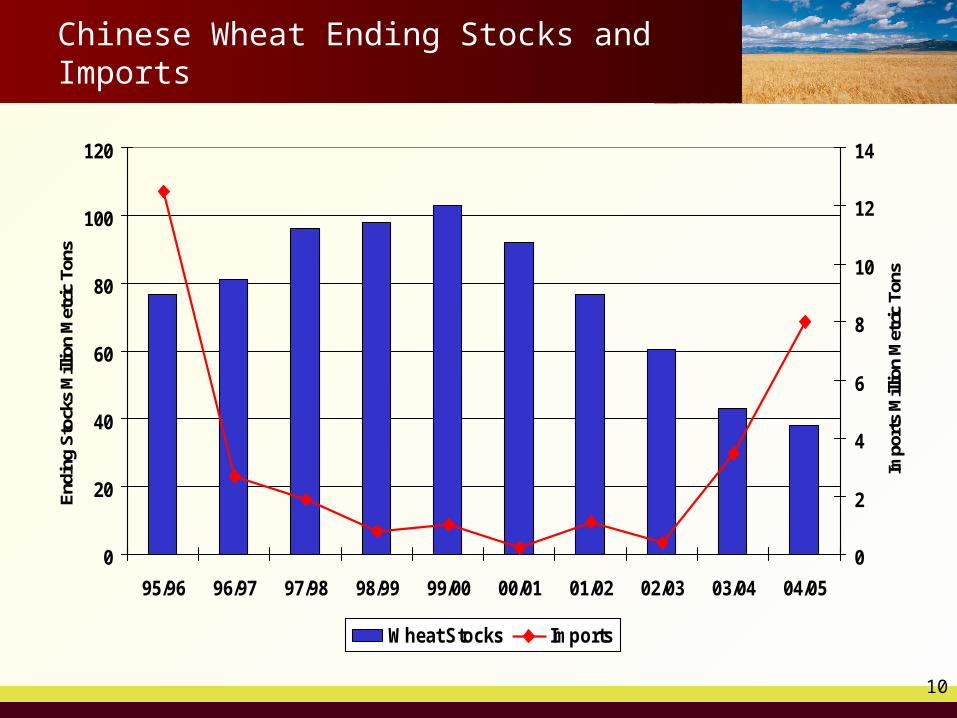

• Chinese wheat imports (Page 10) from the US for 05/06 could be much lower than originally expected. The Chinese government has imposed a 13% tax on wheat imports for 2005 and Chinese winter wheat acreage increased 4-5% this fall. In addition, China signed an agreement with the Canadian Wheat Board for 1 million metric tons of wheat in the 05/06 crop year.

In summary, basis prices are beginning to trend downward as are the wheat futures, which in turn, is helping flour prices, these declines, primarily in the basis, are coming much slower than had been projected but should continue to do so nonetheless. The grain industry anticipates further declines going into the spring months barring any major weather problems. If this trend continues, it is our intent to average forward with the lower futures that would allow for some price relief from our current positions.

The information we’ve provided is a reflection of where the grain markets are today and is not necessarily an indication of what the markets may or may not do going forward. Please feel free to contact Lauri Gritten our Vice President of Sales at 800-826-1200 or 317-837-0478 or your PBI customer service representative with any questions you may have.

Sources:Horizon Flour Milling, LLCMilling & Baking News /MarketFAXPizza Blends Inc.

4

Board vs. Basis

5

World Wheat Ending Stocks

100

120

140

160

180

200

220

Mil

lion

s M

etri

c T

ons

1980 1983 1986 1989 1992 1995 1998 2001 2004

Ending Stocks

6

US Planted Hard Red Winter Wheat Acres

27000280002900030000310003200033000340003500036000

(000

) A

cres

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Planted Acres

1.5% reduction year on year

7

US Planted Soft Red Winter Wheat Acres

5000

6000

7000

8000

9000

10000

11000

12000

(000

) A

cres

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Planted Acres

20% reduction year on year

8

DNS 14 Pro BS Mpls

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

$1.80

$1.90

$2.00

$2.10

_ _ _ _ _ _ _ _ _ _ _ _

JUNE JULY AUG SEPT OCT NOV DEC JAN FEB MAR APR MAY

BA

SIS

(ce

nts/

bu.) 93/94

03/0404/0521 yr avg5 yr avg

9

HRW 12 Pro Basis KC

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

JUNE JULY AUG SEPT OCT NOV DEC JAN FEB MAR APR MAY

25 YEAR avg

5 YEAR avg

03/04

04/05

93/94

cen

t s/b

u

10

Chinese Wheat Ending Stocks and Imports

0

20

40

60

80

100

120

95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05

End

ing

Sto

cks

Mill

ion

Met

ric

Tons

0

2

4

6

8

10

12

14

Impo

rts

Mill

ion

Met

ric

Tons

Wheat Stocks Imports