Financial Stability Review (FSR) · The PDF format is downloadable from: ... [email protected] ......

168

Transcript of Financial Stability Review (FSR) · The PDF format is downloadable from: ... [email protected] ......

The preparation of the Financial Stability Review (FSR) is one of the avenues

through which Bank Indonesia achieves its mission “to safeguard the stability of the Indonesian

Rupiah by maintaining monetary and financial system stability for sustainable national

economic development”.

Publisher:

Bank Indonesia

Information and Orders:

This edition is published in September 2014 and is based on data and information available as of June 2014,unless stated otherwise.

Source: Bank Indonesia, unless stated otherwise.

The PDF format is downloadable from: http://www.bi.go.id

For inquiries, comments and feedback please contact:

Bank Indonesia

Macroprudential Policy Department (DKMP)

Jl.MH Thamrin No.2, Jakarta, Indonesia

Email: [email protected]

FSR is published biannually with the objectives:

To improve public insight in terms of understanding financial system stability.

To evaluate potential risks to financial system stability.

To analyze the developments of and issues within the financial system.

To offer policy recommendations to promote and maintain financial system stability.

Financial Stability Review( No.23, September 2014)

MACROPRUDENTIAL POLICY DEPARTMENT

ii

“Maintaining Financial Stabilityamid Economic Slowdown”

iii

Table of Contents ........... ................................................................................................................................................. iii

Glossary ............ ............................................................................................................................................................... vii

Foreword.......... ................................................................................................................................................................ ix

......................................................................................................................................................... 3 Chapter 1. Financial System Stability ................................................................................................................................ 9 1.1. Development of Risks on Global and Regional Financial Markets .................................................................. 9

........................................................................................... 12 1.3. Financial System Stability in Indonesia ........................................................................................................... 14 1.4. The Financial Cycle of Indonesia .................................................................................................................... 15 1.5. Sources of Financial Imbalances .................................................................................................................... 17 1.6. Sources of Vulnerability ................................................................................................................................. 24 Box 1.1. Financial Cycle of Indonesia ................................................................................................................... 32

........................................................................................ 36.......................................................... 38

Chapter 2. Financial Markets ........................................................................................................................................... 43 2.1. Financial Market Risks .................................................................................................................................... 43 2.2. The Financial Market as a Source of Non-Bank Financing ............................................................................. 55

.................................................................................... 59 Box 2.2. Shadow Banking in Indonesia ................................................................................................................. 63 Chapter 3. The Household and Corporate Sectors ........................................................................................................... 69 3.1. Household Sector Assessment ....................................................................................................................... 69 3.2. Corporate Sector Assessment ........................................................................................................................ 76

................................................................................. 85 ................................................................................. 86

............................................................................ 91 4.1. The Banking Sector ......................................................................................................................................... 91

......................................................................................................... 114 ........................................................................... 118

........................... 120

Chapter 5. Financial System Infrastructure ...................................................................................................................... 125 ....................................................................................................................... 126

................................................................................................... 127 ............................................................................................................................ 128

.................................................................................................. 130 .......................................................................................... 131

.............................................................................................................................................................. 133 .......................................................................................... 135

............................................................................................................... 145

Bibliography ..... ................................................................................................................................................................ 153

able ntent

iv

i t able a an Fi e

able1.1. . 101.2. .. 161.3. Stress/Crisis ........................................................ 171.4. Several Countries with the Strongest

............................ 28Box Table 1.1.1. Concordance Index of Financial Cycle Variables (Narrow Credit) ..................................... 33Box Table 1.1.2. Concordance Index of Financial Cycle Variables (Broad Credit) ..................................... 33

Business Cycle ................................................... 34

onset of Crisis/Stress ......................................... 34

2.1. 10-Year SBN Yield and Regional Yields ............. 482.2. .. 48

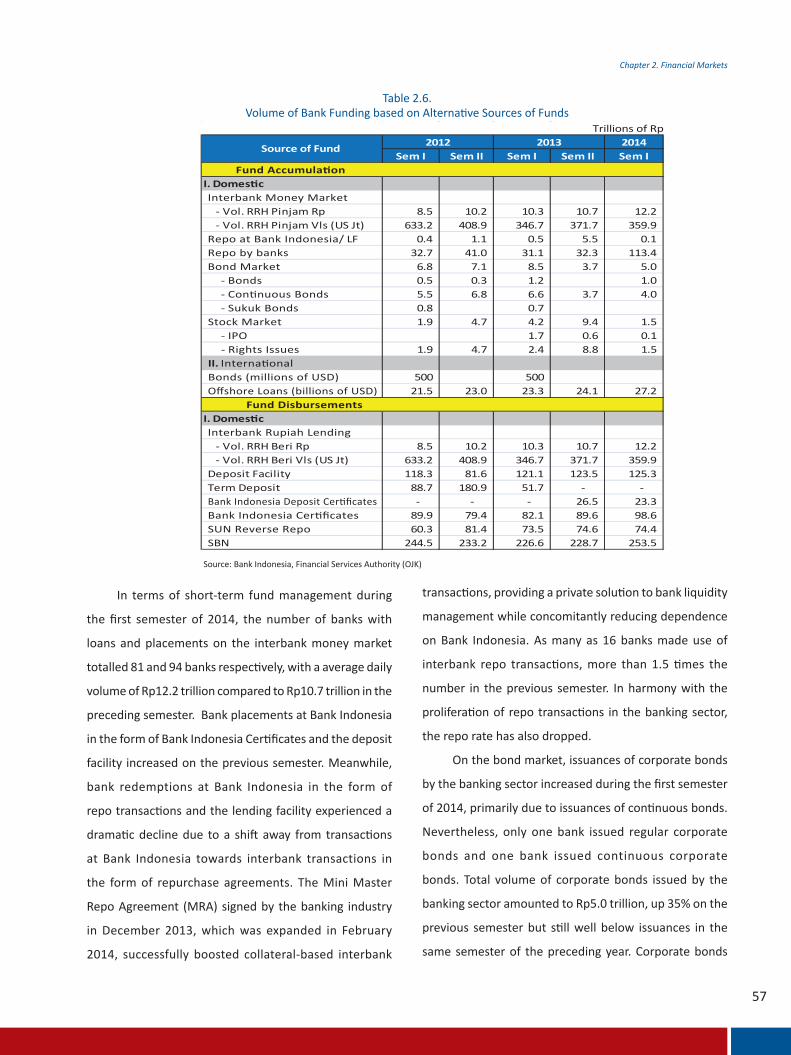

............. 512.4. Bank and Non-Bank Financing ......................... 552.5. .. 562.6. Volume of Bank Funding based on

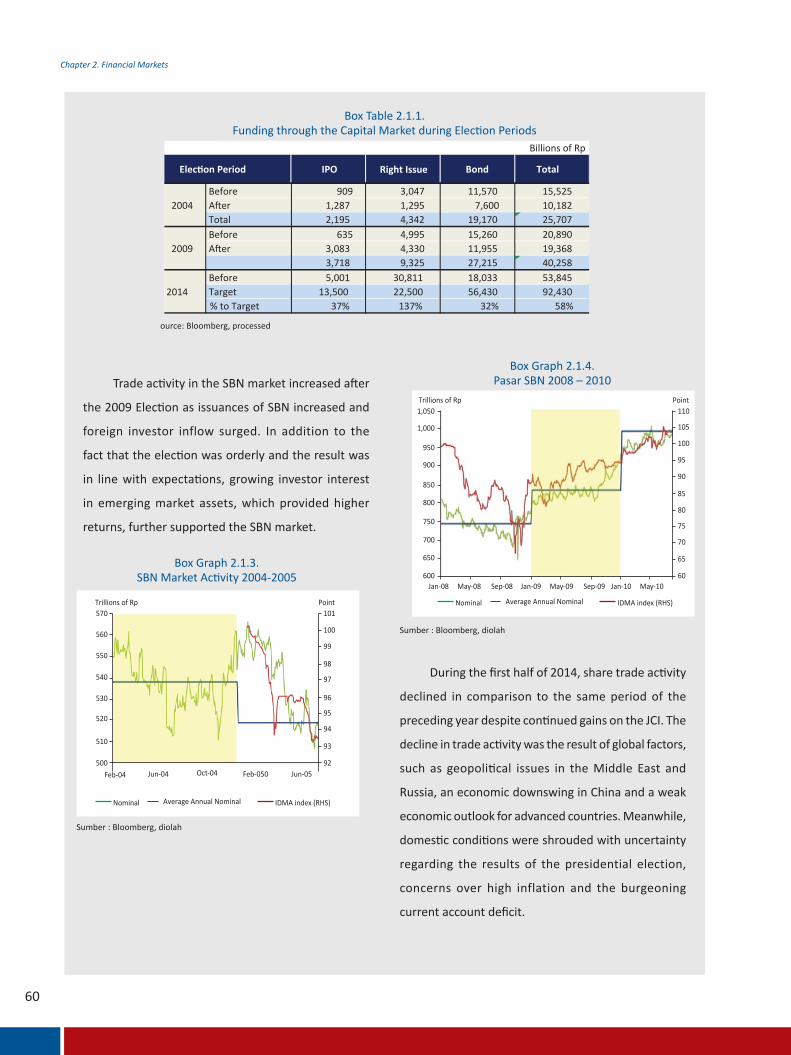

........................... 57Box Table 2.1.1. Funding through the Capital Market

.................................... 60

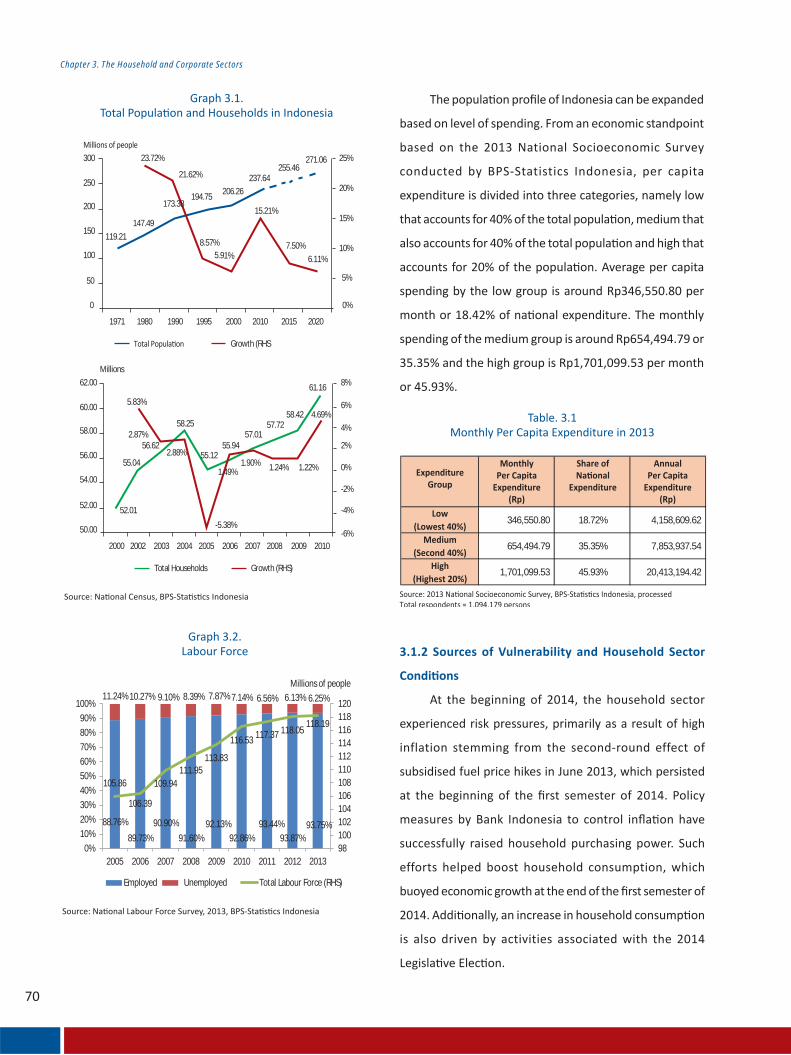

......... 703.2. and Savings based on Monthly Income .............. 73

............................................ 733.4. .. 74

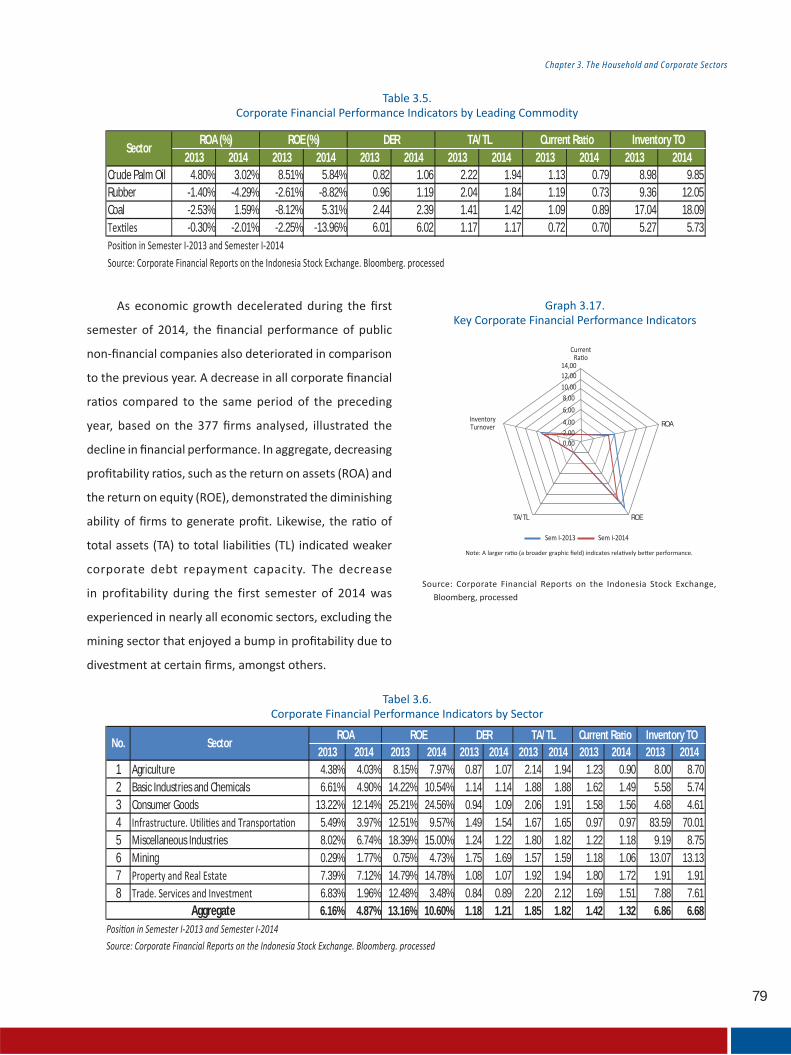

.................................... 793.6. by Sector ........................................................... 79

............ 823.8. Corporate Credit by Economic Sector .............. 82

Economic Sector ............................................... 83

Direct Investment by Economic Sector ............ 84Box Table

................ 87Box Table

................. 87

Box Table 3.2.3 Altman Z-score ................................... 88Box Table

Exchange Rates ................................................ 88

....................... 93 ............................... 93

........................ 94 ... 95

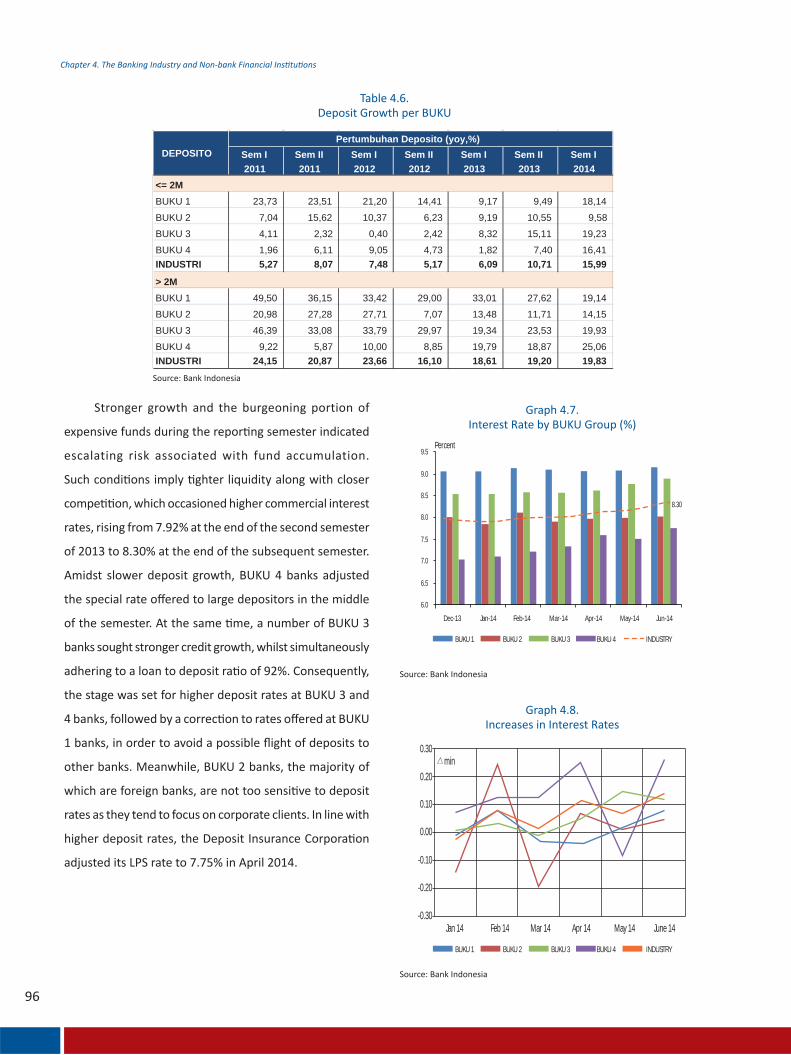

........................ 95 ............................... 96

.............. 98 ..................... 99

........................................ 101 ............. 101

4.11. Deposit Rates .................................................. 103 ......................... 104

the Banking Sector ........................................... 1054.14. SBN Holdings in the Banking Sector ................. 106

(in trillions of rupiah) ....................................... 1064.16. Breakdown of Income Accounts (in trillions of rupiah) ....................................... 1074.17. Breakdown of Cost Accounts (in trillions of rupiah) ....................................... 107

...................... 108 ............................... 110

........ 116 .......................... 117

Box Table 4.1.1. Granger Causality Test ....................... 118Box Table 4.1.2. Regression of MSME Credit Risk ............ 118

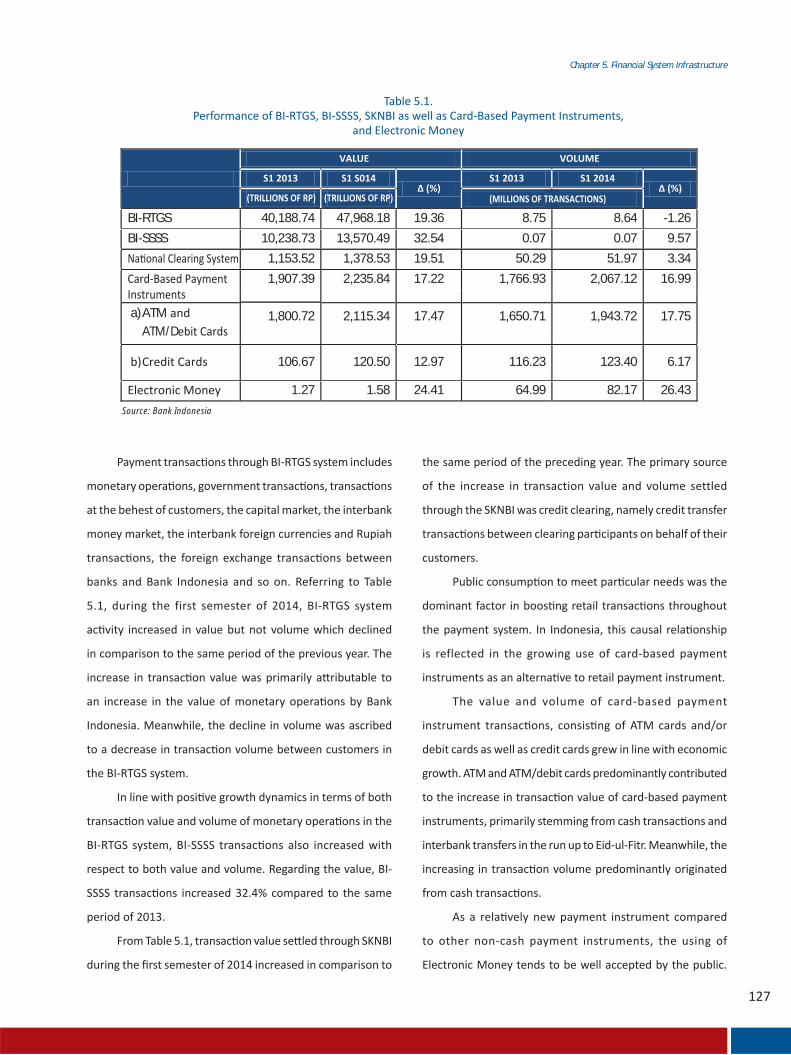

and Electronic Money ...................................... 127

v

a .......................... 11

............... 11 ......... 12

........................................ 131.5. External Debt ................................................... 131.6. Financial System Stability Index ....................... 14

in June 2014 ....................................................... 141.8. Financial Cycle of Indonesia ............................. 15

............................. 18 ........................... 18

...................... 19

............................ 19

.............................................. 201.14. ............ 20

................. 21 ..................... 23

1.17. Sources of Funds and Instruments of ..... 23

1.18. External Debt by Tenor ..................................... 231.19. External Debt by Economic Sector ................... 241.20. Fed Fund Survey: .................. 251.21. Growth in Emerging Market Countries ............ 251.22. CDS in Advanced Countries .............................. 261.23. CDS in Neighbouring Countries ........................ 261.24. CDS in Several Emerging Market Countries ...... 27

Emerging Market Countries ............................. 27

and SBN ............................................................ 281.27. Financial Account ............................................. 291.28. Current Account and Exchange Rate ............... 29

............................ 301.30. RI Counterpart Exports in 2013 ........................ 30

........................................... 311.32. Value of Bond Issuances ................................... 311.33. Growth of Deposits and Credit as well as

................................ 31Box Graph 1.1.1. A Common Cycle of the Financial Cycle (Narrow Credit) and Business Cycle ........ 33Box Graph 1.1.2. A Common Cycle of the Financial Cycle (Broad Credit) and Business Cycle .......... 33Box Graph 1.2.1.Macroeconomic Indicators of Indonesia during the 2008 Crisis and Current .. 36Box Graph 1.2.2 Credit Imbalances ............................. 37Box Graph 1.2.3 Deposit Imbalances ........................... 37

2.1. Non-Resident Flows: Shares, SBN & SBI .......... 442.2. .. 44

..................... 44....................... 45

...... 452.6. Foreign Exchange Interbank Money Market .... 45

.... 45 ...... 46

Behaviour ......................................................... 46 ........................... 46 ............................ 46

......... 47 ............................... 47

.... 47 ... 47

2.16. Foreign Net Flow to SBN and IDMA Index ....... 482.17. SBN Holdings .................................................... 40

..................................... 492.19. Rebased SBN Yield by Tenor ............................. 49

.................. 502.21. Rebased Corporate Bond Yield by Tenor .......... 502.22. Corporate Bond Yield Curve ............................. 50

.................... 502.24. Foreign Net Flow and Holdings of Corporate Bonds.. 50

............... 51 ...................... 51

2.27. Flow to Shares and JCI ...................................... 51 ............................... 52

............................. 52 ...................... 52

................. 522.32. Growth of Mutual Funds (yoy) ........................ 53

................................ 532.34. NAV trend of Mutual Funds by Type ............... 532.35. NAV of Mutual Funds by Type ......................... 54

............... 542.37. Nominal Value of Bonds ................................... 552.38. Capital Market Financing ................................. 56

..... 59 ..... 59

....... 60 ....... 60

2013-Semester I 2014 ........................................ 61

2013-Semester I 2014 ...................................... 61 ..................................... 61

................................... 61

vi

aBox Graph 2.1.9. JCI, Yield and the Rupiah in 2014 ..... 62Box Graph 2.1.10. Actual and Forecasted Indicators ... 62Box Graph 2.2.1. Exposure of Non-Bank Financial

Intermediaries .................................................. 64Box Graph 2.2.2. Growth of Non-Bank Financial

Intermediaries .................................................. 64

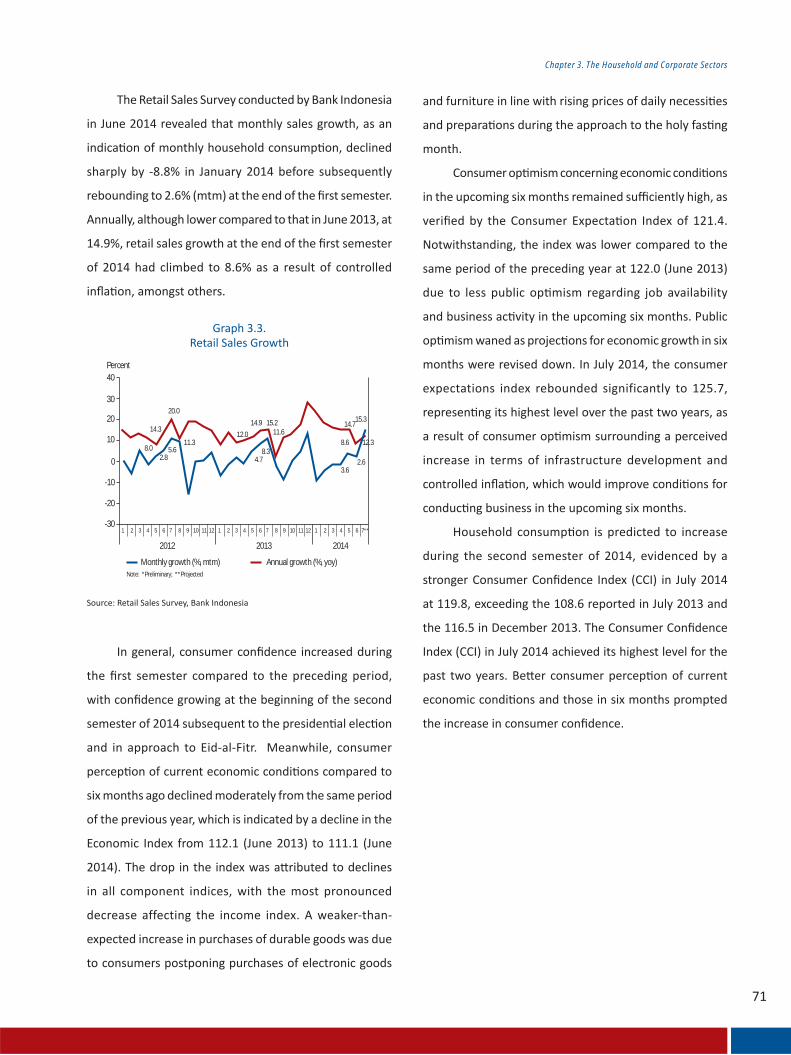

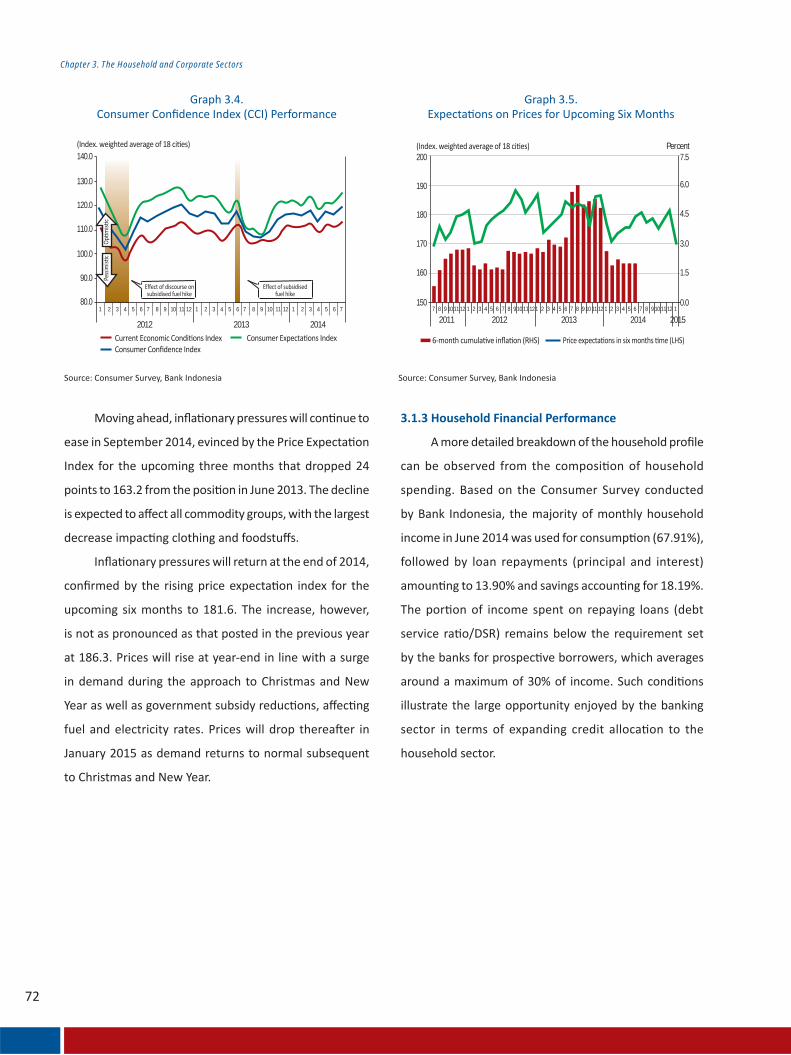

3.1. .. 70 .................................................... 70

3.3. Retail Sales Growth .......................................... 713.4. .. 723.5. .. 72

............... 73 ......................... 74

......... 75

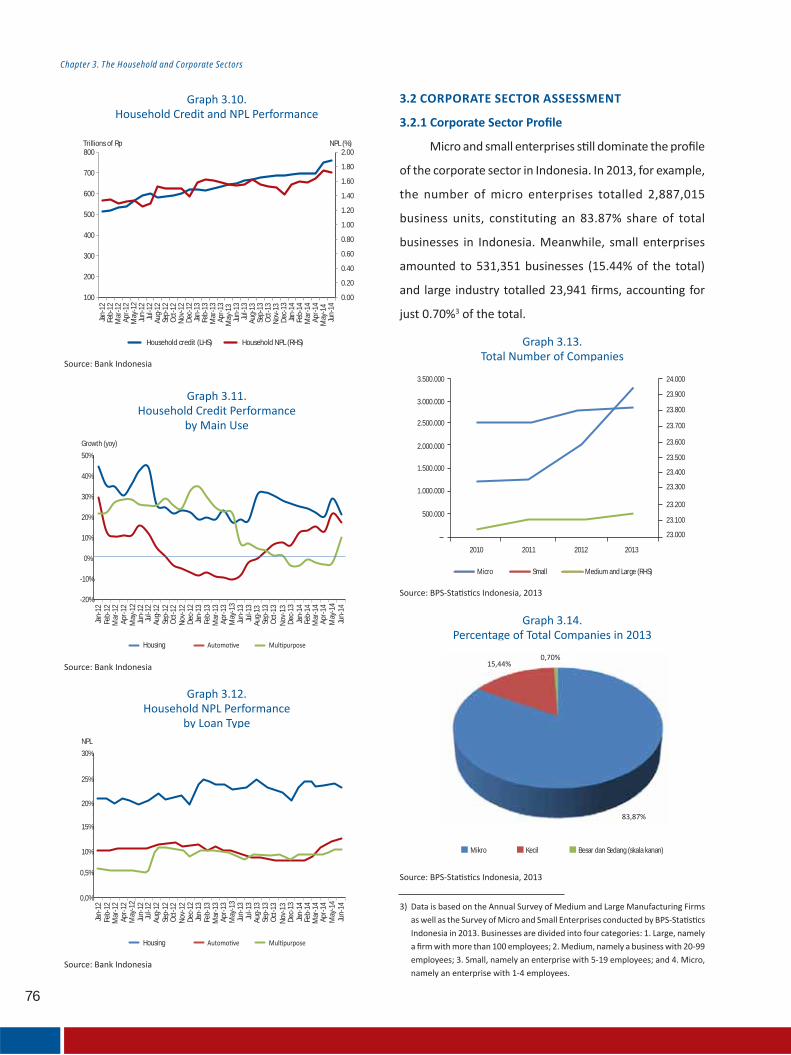

(per June) ......................................................... 75 .......... 76

... 76 .... 76

3.13. Total Number of Companies ............................ 76 .... 77

................................. 77

..................................................... 783.17. .. 79

Z-score .............................................................. 80 ... 80

................................ 80 .... 81 .... 81

................................. 82Box Graph 3.1.1. Non-Regional Commercial Bank Credit

.............................. 85Box Graph 3.2.1 . 87

.................................................. 924.2. . 92

.... 924.4. Deposit Growth (yoy) ....................................... 944.5. .... 94

......................... 94 ..................... 96

4.8. Increases in Interest Rates ............................... 964.9. Credit Growth .................................................. 974.10. Credit Growth by Currency .............................. 97

............................. 974.12. Credit Growth by Economic Sector .................. 98

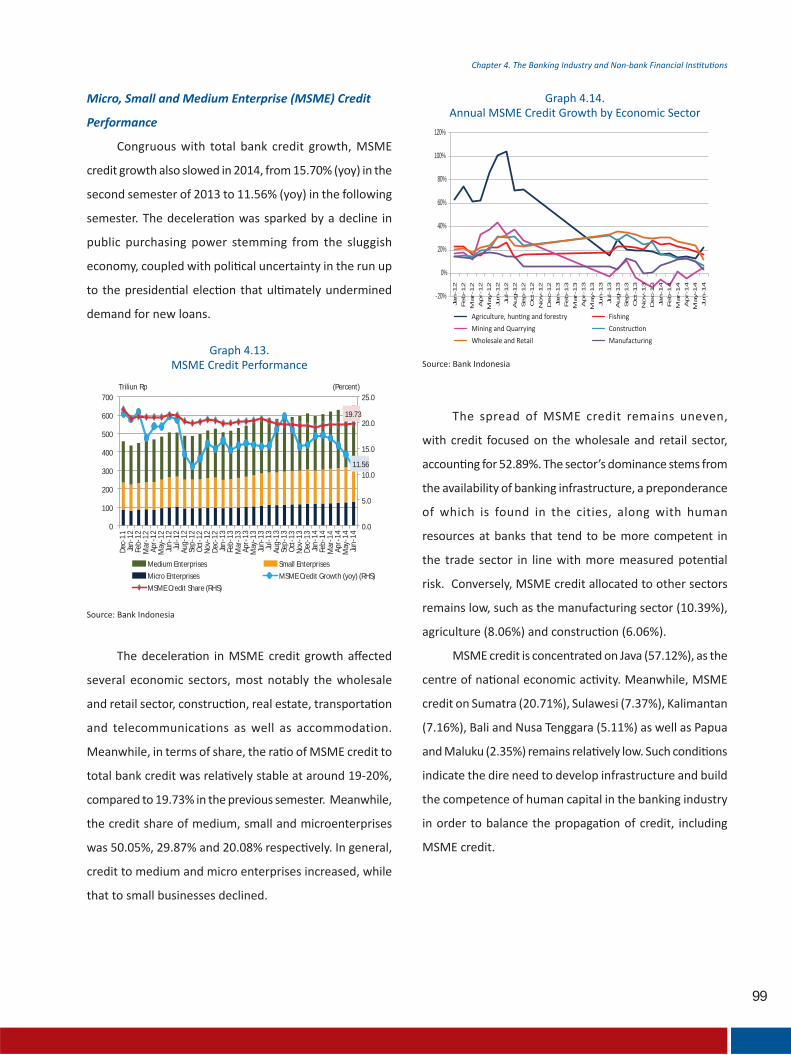

.............................. 99

4.14. Annual MSME Credit Growth by Economic Sector 99 ............... 100 ................ 100

......................... 100

............................................................ 101 ............ 102

Semester I-2014 ............................................... 104 ......................................................... 105

............ 108 .................... 108

........................................ 109 ......... 109

................................. 110 .................... 110

4.28. ...................... 111

................................................. 111 ................. 112

Higher Interest Rates ........................................ 112 .................. 112

......................................... 113 ....................... 113

.............................................. 1134.36. Finance Company Financing by Business Sector . 114

....................... 114 ..................... 114

4.39. Sources of Funds .............................................. 115 ...... 116

in Semester I-2014 ........................................... 1164.42. Share of Industry Assets by Business Sector (per December 2013) ....................................... 1164.43. Insurance Industry Assets and Investments ...... 1164.44. . 1164.45. Insurance Industry Growth and Density........... 117Box Graph 4.1.1. Credit Risk and Economic Growth .... 119

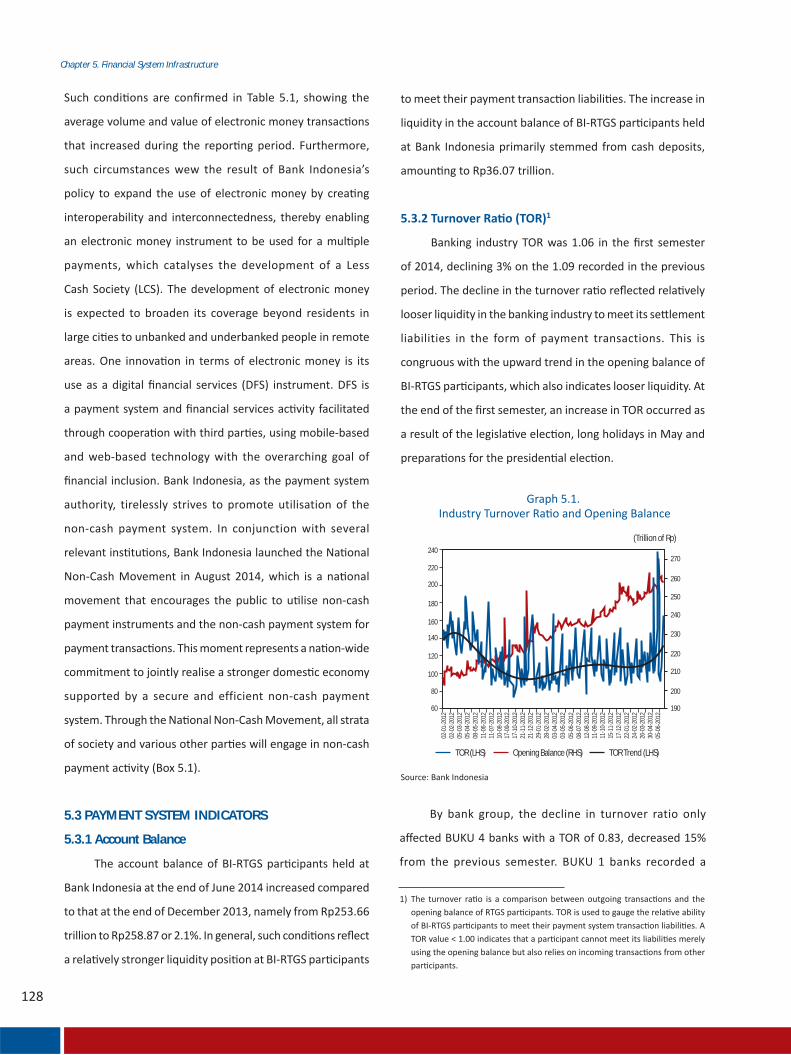

5.1. .. 128 ......................... 129

.......................... 129 ....................... 129

vii

GlossaryAFS: Available for SaleUS: United StatesAPMK: Card-based payment instrumentsASEAN: AssociationofSoutheastAsianNationsATM: AutomaticTellerMachineATMR: Risk-weightedassetsBCBS: BaselCommitteeonBankingSupervisionBIS: BankforInternationalSettlementsBI-RTGS: BankIndonesia–RealTimeGross

Settlement(BI-RTGS)systemBI-SSSS: BankIndonesiaScriplessSecurities

SettlementSystemBOPO: Efficiencyratioofoperatingcoststo

operatingincomeBPD: Regional bankBPR: Rural Bankbps: basis pointBUKU: Classificationofcommercialbanksbasedon

businessactivityBUS: Islamic bankCAR: CapitalAdequacyRatioCCB: CountercyclicalcounterbufferCDS: Credit Default SwapCPO: Crude palm oilDER: DebttoequityratioDTI: DebttoincomeratioDPK: DepositsD-SIB: Domestic–SystemicallyImportantBankDP: DownpaymentDRC: Disaster Recovery CentreDSR: DebtServiceRatioEM: EmergingMarketFDI: Foreign Direct InvestmentFKSSK: FinancialSystemStabilityCoordination

ForumFSAP: Financial Sector Assessment ProgramFSB: Financial Stability BoardFSI: Financial Stability IndexG20: TheGroupofTwentyGDP: GrossDomesticProductIDMA: InterdealerMarketAssociationIHK: ConsumerPriceIndex(CPI)IHSG: IDX Composite IndexIKK: ConsumerConfidenceIndex(CCI):IKNB: Non-bankfinancialinstitutionIMF: InternationalMonetaryFundISIK: FinancialInstitutionStabilityIndexISPK: FinancialMarketStabilityIndexISSK: Indonesia Financial Stability Index

KI: Investment CreditKIK: Consumer LoansKMK: Working Capital CreditKPMM: MinimumStatutoryCapitalRequirementKPR: MortgageloanLCR: LiquidityCoverageRatioLDR: LoantodepositratioLKD: Digital Financial ServicesLTV: Loan to valueLPS: TheDepositInsuranceCorporationL/R: Profit/lossMinerba: MineralandCoalMiningNAB: NetAssetValueNFA: NetForeignAssetsNFL: NetForeignLiabilitiesNII: NetInterestIncomeNIM: NetInterestMarginNPF: Non-performingfinancingNPI: Indonesia Balance of PaymentsNPL: Non-performingloansOJK: TheFinancialServicesAuthority(OJK)OTC: OverthecounterPUAB: TheInterbankMoneyMarketPD: Probability of DefaultPDB: GrossDomesticProductPDN: NetOpenPositionPMK: MinisterofFinanceRegulationPLN: External debtPP: Finance CompanyRBB: Bank Business PlanROA: Return on assetsROE: Return on equitySBDK: Prime lending rateSBI: BankIndonesiaCertificateSBN: TradeableGovernmentSecuritiesSBT: NetweightedbalanceSKDU: Business SurveySKNBI: BankIndonesia-NationalClearingSystemSUN: GovernmentbondTOR: TurnoverratioTPT: TextilesandtextileproductsUMKM: Micro,SmallandMediumEnterprises

(MSMEs)

viii

This page is intentionally left blank

ix

rd

2014. The Financial Stability Review represents one form of transparency and accountability to the public in terms of

an expansionary period as well as provide space to absorb risk during an economic downturn.

the forms of spiralling private external debt, uncertainty surrounding the economic recovery in advanced countries as

amongst others.

In closing, this 23rd

of the Financial Stability Review.

Foreword

Jakarta, September 2014

Martowardo o

This page is intentionally left blank

1

ec ve S ary

2

3

ec ve S ary

4

7

Chapter 1. Financial System Stability

Financial System Stability

Chapter 1

8

Chapter 1. Financial System Stability

9

Chapter 1. Financial System Stability

1.1 DEVELOPMENT OF RISKS ON GLOBAL AND

REGIONAL FINANCIAL MARKETS

Financial System StabilityChapter1

Chapter 1. Financial System Stability

Advanced Countries

United States 1.80 (16.44) (41.98) (43.65) 22.04 6.05 - -

UK 9.29 (11.65) (61.51) (31.85) 8.50 (0.08) (11.07) (3.53)

Japan -33.65 (23.62) (53.28) (7.11) 10.86 45.86 2.21 (3.63)

Germany -27.95 (35.46) (38.05) (19.74) 23.54 38.46 (4.97) 0.83

East Asia

China 13.30 (11.47) (44.32) (3.54) 3.49 (3.20) 1.07 2.32

Hong Kong -0.10 (12.63) - - 11.48 (0.50) (0.08) (0.06)

Indonesia 15.17 (2.83) (22.37) (32.15) 1.24 13.02 18.70 (2.74)

South Korea -6.72 (11.79) (50.84) (19.38) 7.45 (0.03) (11.40) (4.14)

Malaysia 12.58 (2.02) (28.45) (22.48) 6.16 0.84 1.60 (2.53)

the Philippines - - (30.91) (23.03) 5.86 16.78 1.21 (1.67)

Singapore -1.20 (9.68) - - 3.34 2.79 (1.68) (1.66)

Thailand 2.20 (2.31) (14.30) (13.84) 2.33 5.67 4.47 (1.14)

Source: Bloomberg

(%)

(%)

Exchange RateStock IndexYield of 10-yearGovernment

Bonds (%)

5-year CDS (%)

y-o-y y-t-d y-o-y y-t-d y-o-y y-t-d y-o-y y-t-d

Chapter 1. Financial System Stability

45

Dow Jones

40

35

30

25

20

15

10

5

0

Jan

-13

Feb

-13

Mar

-13

Ap

r-13

May

-13

Jun

-13

Jul-

13

Au

g-13

Sep

-13

Oct

-13

No

v-13

Dec

-13

Jan

-14

Feb

-14

Mar

-14

Ap

r-14

May

-14

Jun

-14

MSCI AsiaMSCI EuroMSCI World

160

150

140

130

120

110

100

90

80Jan-10 Jul-10 Jul-11Jan-11 Jul-12Jan-12 Jul-13Jan-13 Jul-14Jan-14

80

90

100

110

120

130Index

Composite Stock Index Performance(Rebased 1/1/2010=100)

EM Asia

World

G7

Asia P

Index

Chapter 1. Financial System Stability

1.2 DEVELOPMENT OF RISKS IN THE DOMESTIC

ECONOMY

13.0

11.0

9.0

7.0

5.0

3.0

1.0

GDP Growth (%. yoy) Interest Rate Spread (%)

-1.0

Mar

-07

Sep

t-07

Mar

-08

Sep

t-08

Mar

-09

Sep

t-09

Mar

-10

Sep

t-10

Mar

-11

Sep

t-11

Mar

-12

Sep

t-12

Mar

-13

Mar

-14

Sep

t-13

Chapter 1. Financial System Stability

20.0M

ar-0

7

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Mar

-14

Sep

-13

15.0

10.0

5.0

-5.0

0.0

-10.0

Current Account (billions of US$)

-15.0

Capital and Financial Account (billions of US$)

Overall Balance (billions of US$)

300.0

millions US$

Private – Non bank

250.0

200.0

150.0

100.0

50.0

0.02009 2010 2011 2012 2013 June 2014

Private – Bank Government andCentral Bank

Chapter 1. Financial System Stability

1.3. FINANCIAL SYSTEM STABILITY IN INDONESIA

nd

nd

3,0

2,5

1,5

0,5

2,0

1,0

2002

M01

2002

M05

2002

M09

2003

M01

2003

M05

2003

M09

2004

M01

2004

M05

2004

M09

2005

M01

2005

M05

2005

M09

2006

M01

2006

M05

2006

M09

2007

M01

2007

M05

2007

M09

2008

M01

2008

M05

2008

M09

2009

M01

2009

M05

2009

M09

2010

M01

2010

M05

2010

M09

2011

M01

2011

M05

2011

M09

2012

M01

2012

M05

2012

M09

2013

M01

2013

M05

2013

M09

2014

M01

2014

M05

1.2%

10.5%

2.6%6.4%

0.1%

0.5%

Banks

78.6%

Rural Banks

Insurers

Pension Funds

Finance Companies

Guarantors

Pawnbrokers

Chapter 1. Financial System Stability

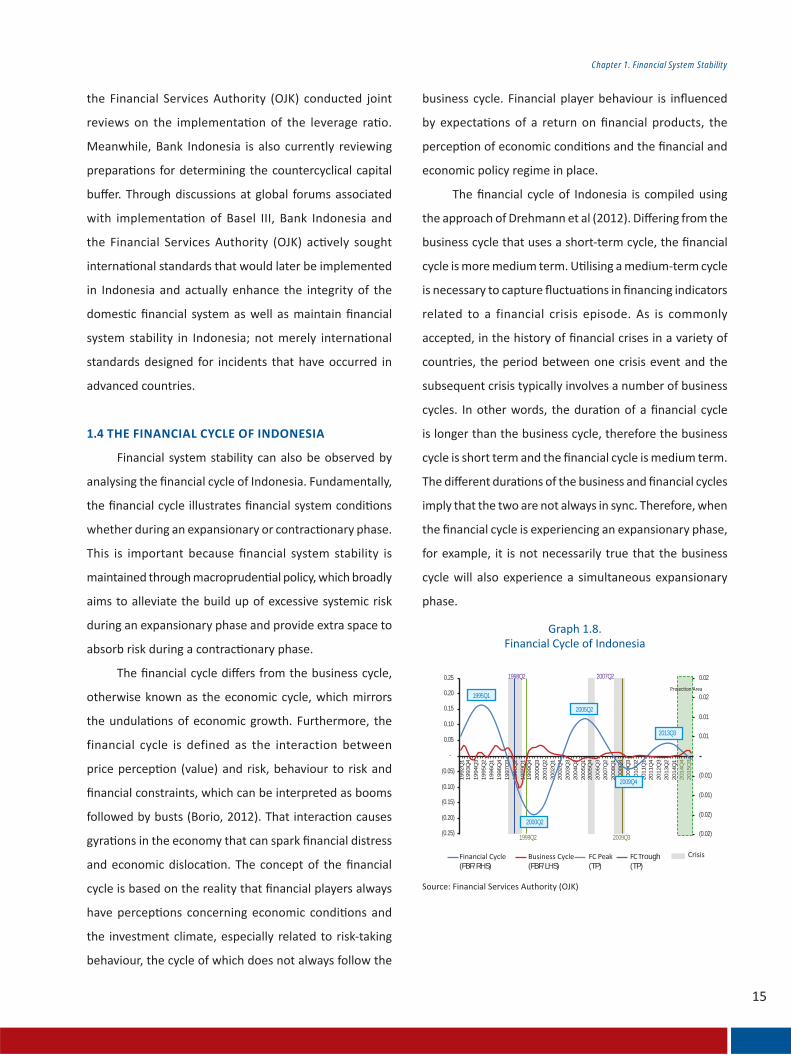

1.4 THE FINANCIAL CYCLE OF INDONESIA

0.25 0.02

0.02

0.01

0.01

(0.01)

(0.01)

(0.02)

(0.02)

2007Q2

0.20

0.15

0.10

0.05

-

(0.05)

19

92

Q1

19

93

Q4

19

94

Q3

19

95

Q2

19

96

Q1

19

96

Q4

19

97

Q3

19

98

Q2

19

99

Q1

19

99

Q4

20

00

Q3

20

01

Q2

20

02

Q1

20

02

Q4

20

03

Q3

20

04

Q2

20

05

Q1

20

05

Q4

20

06

Q3

20

07

Q2

20

08

Q1

20

08

Q4

20

09

Q3

20

10

Q2

20

11

Q1

20

11

Q4

20

12

Q3

20

13

Q2

20

14

Q1

20

14

Q4

20

15

Q3

(0.10)

(0.15)

(0.20)

(0.25)

1995Q1

2000Q2

2009Q4

2013Q3

2005Q2

1998Q2

1999Q2

(FBF/RHS)

2009Q3

(FBF/LHS) (TP)rough

(TP)

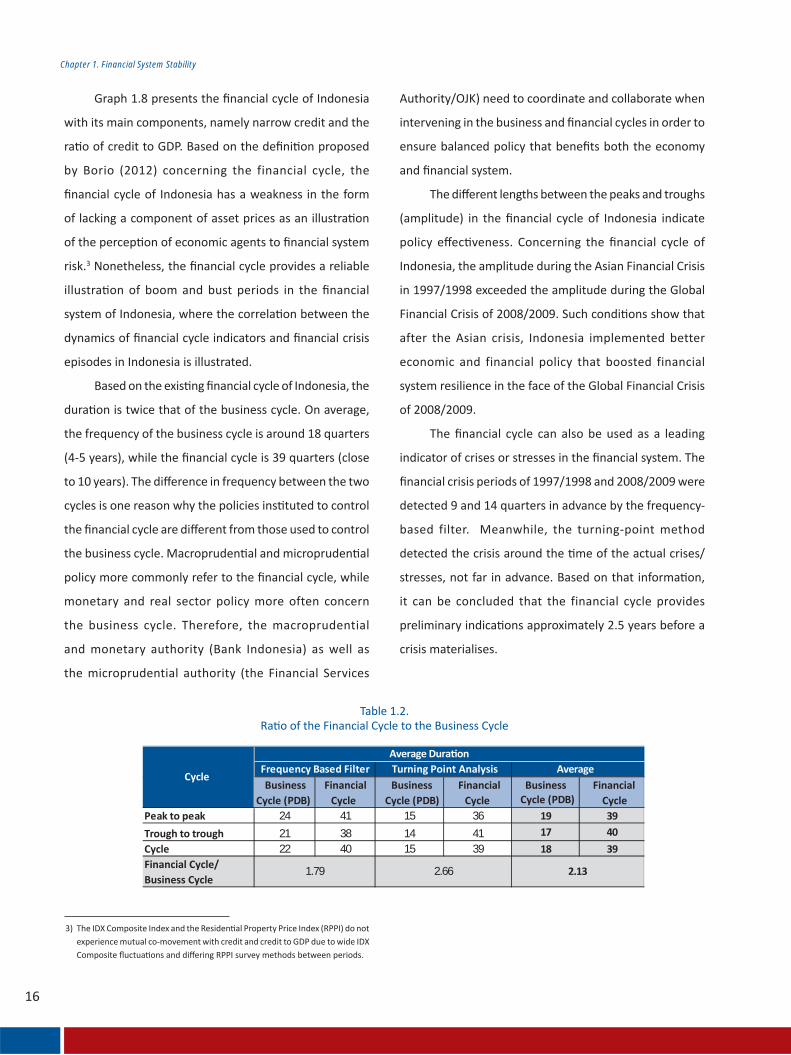

Chapter 1. Financial System Stability

Peak to peak 24 41 15 36 19 39

Trough to trough 21 38 14 41 17 40

Cycle 22 40 15 39 18 39Financial Cycle/Business Cycle

BusinessCycle (PDB)

FinancialCycle

1.79 2.66 2.13

Cycle

Average Dura onFrequency Based Filter Turning Point Analysis AverageBusiness

Cycle (PDB)Financial

CycleBusiness

Cycle (PDB)Financial

Cycle

Chapter 1. Financial System Stability

7

8

Frequency based lter

Turning point

analysis

1997Q3 -10 3Economic crisis and

2005Q3 -1 - Mini economic crisis2008Q4 -14 -6 Economic crisis

Crisis Descrip on

Peak (Quarterly)

1.5 SOURCES OF FINANCIAL IMBALANCES

1.5.1 Banking Procyclicality

Chapter 1. Financial System Stability

40.0 8.0

7.0

5.0

4.0

3.0

2.0

1.0

6.0

35.0

30.0

25.0

20.0

15.0

10.0

5.0

0.0

Sep-

01M

ar-0

2Se

p-02

Credit Growth (%. yoy) GDP Growth (%. RHS)

Mar

-03

Sep-

03M

ar-0

4Se

p-04

Mar

-05

Sep-

05M

ar-0

6Se

p-06

Mar

-07

Sep-

07M

ar-0

8Se

p-08

Mar

-09

Sep-

09M

ar-1

0Se

p-10

Mar

-11

Sep-

11M

ar-1

2Se

p-12

Mar

-13

Sep-

13M

ar-1

4Se

p-14

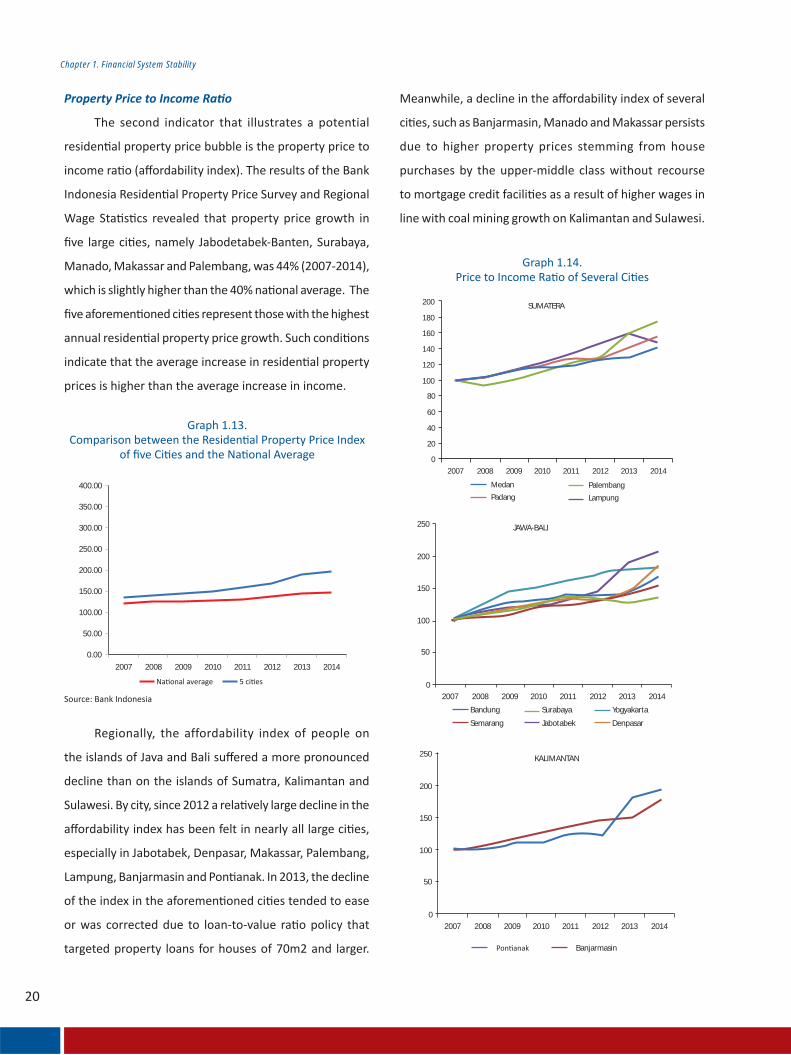

1.5.2 Rising Property Prices

9

40.0 3.0

2.5

1.5

1.0

0.5

0.0

-0.5

-1.0

-1.5

-2.0

2.035.0

30.0

25.0

20.0

15.0

10.0

Sep-

01M

ar-0

2Se

p-02

Credit/GDP Gap (%. RHS) Credit/GDP (%) Trend

Mar

-03

Sep-

03M

ar-0

4Se

p-04

Mar

-05

Sep-

05M

ar-0

6Se

p-06

Mar

-07

Sep-

07M

ar-0

8Se

p-08

Mar

-09

Sep-

09M

ar-1

0Se

p-10

Mar

-11

Sep-

11M

ar-1

2Se

p-12

Mar

-13

Sep-

13M

ar-1

4Se

p-14

40%

Overheated Overheated

Overheated

Overheated

35

30

25

20

15

Sep-

01M

ar-0

2Se

p-02

Mar

-03

Sep-

03M

ar-0

4Se

p-04

Mar

-05

Sep-

05M

ar-0

6Se

p-06

Mar

-07

Sep-

07M

ar-0

8Se

p-08

Mar

-09

Sep-

09M

ar-1

0Se

p-10

Mar

-11

Sep-

11M

ar-1

2Se

p-12

Mar

-13

Sep-

13M

ar-1

4Se

p-14

Credit/GDP (%) Trend

Chapter 1. Financial System Stability

180.00

170.00

160.00

150.00

140.00

130.00

120.00

110.00

100.00

2007 2008 2009 2010 2011 2012 2013 2014

240.00

220.00

200.00

180.00

160.00

140.00

120.00

2007 2008 2009 2010 2011 2012 2013 2014

Bandung Jabotabek-Banten

220.00

200.00

180.00

160.00

140.00

120.00

100.00

2007 2008 2009 2010 2011 2012 2013 2014

Palembang Bandar Lampung

240.00

220.00

200.00

180.00

160.00

140.00

120.00

100.00

2007 2008 2009 2010 2011 2012 2013 2014

Chapter 1. Financial System Stability

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

2007 2008 2009 2010 2011 2012 2013 2014

200

180

SUMATERA

Medan

Padang

Palembang

Lampung

160

140

120

100

80

60

40

20

2007 2008 2009 2010 2011 2012 2013 2014

0

250

200

150

100

50

02007 2008 2009 2010 2011 2012 2013 2014

JAWA-BALI

Bandung

Semarang

Surabaya

Jabotabek

Yogyakarta

Denpasar

250

200

150

100

50

02007 2008 2009 2010 2011 2012 2013 2014

KALIMANTAN

Banjarmasin

Chapter 1. Financial System Stability

180

160

140

120

100

80

60

40

20

02007 2008 2009 2010 2011 2012 2013 2014

Menado Makasar

2007 2008 2009 2010 2011 2012 2013 2014

1.20

1.10

1.00

0.90

0.80

0.70

0.60

Tw I Tw II Tw IIITw IV Tw I Tw II Tw IIITw IV Tw I Tw II Tw IIITw IV Tw I Tw II Tw IIITw IV Tw I Tw II Tw IIITw IV Tw I Tw II Tw IIITw IV Tw I Tw II Tw IIITw IV Tw I Tw II

Jabodetabek

Chapter 1. Financial System Stability

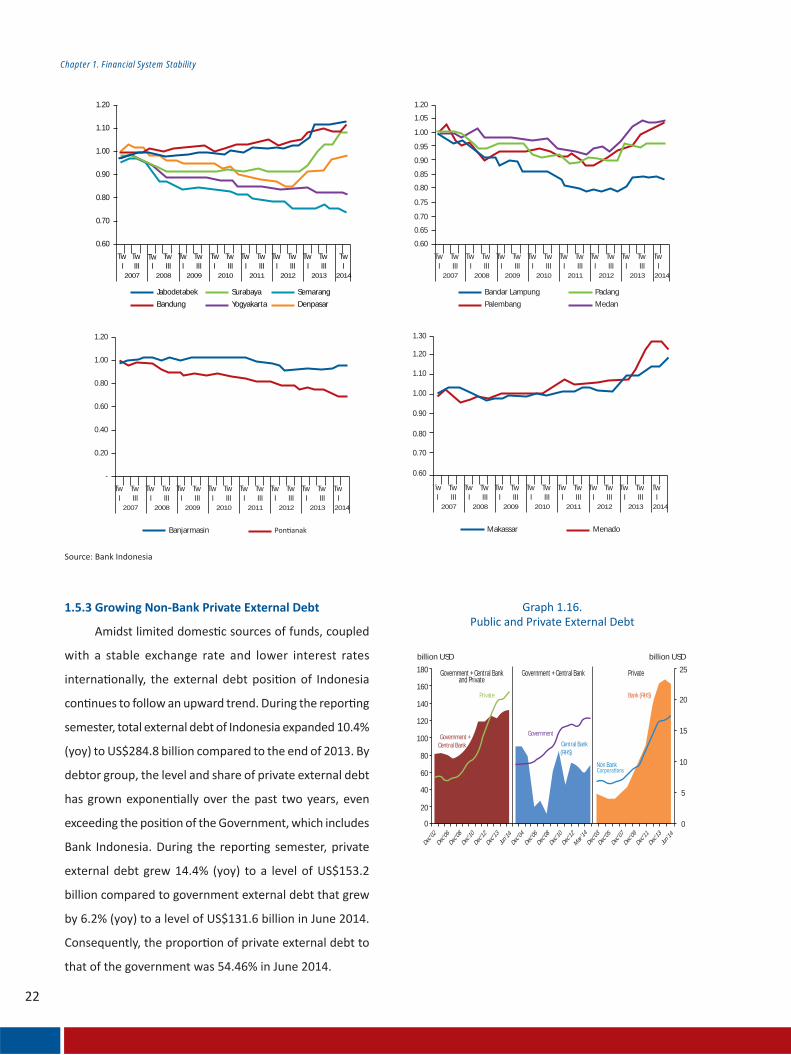

1.5.3 Growing Non-Bank Private External Debt

180

billion USD billion USD

25

20

15

10

5

0

Government + Central Bankand Private

Government + Central Bank

Private

Private

160

140

120

100

80

60

40

20

0

Government + Central Bank

Government

Central Bank (RHS)

Non Bank

Bank (RHS)

Dec’02

Dec’06

Dec’08

Dec’10

Dec’12

Dec’13

Jun’14

Dec’04

Dec’06

Dec’08

Dec’10

Dec’12

Mar

’14

Dec’03

Dec’05

Dec’07

Dec’09

Dec’11

Dec’13

Jun’14

2007

Jabodetabek

Bandung

Tw I

Tw III

2008

Tw I

Tw III

2009

Tw I

Tw III

2010

Tw I

Tw III

2011

Tw I

Tw III

2012

Tw I

Tw III

Tw I

Tw III

Tw I

1.20

1.10

1.00

0.90

0.80

0.70

0.60

2013 2014

Surabaya

Yogyakarta

Semarang

Denpasar

2007

Bandar Lampung

Palembang

Tw I

Tw III

2008

Tw I

Tw III

2009

Tw I

Tw III

2010

Tw I

Tw III

2011

Tw I

Tw III

2012

Tw I

Tw III

Tw I

Tw III

Tw I

1.20

1.05

1.00

0.95

0.85

0.90

0.80

0.70

0.75

0.60

0.65

2013 2014

Padang

Medan

2007

Banjarmasin

Tw I

Tw III

2008

Tw I

Tw III

2009

Tw I

Tw III

2010

Tw I

Tw III

2011

Tw I

Tw III

2012

Tw I

Tw III

Tw I

Tw III

Tw I

1.20

1.00

0.80

0.60

0.40

0.20

-

2013 2014

2007

Makassar Menado

Tw I

Tw III

2008

Tw I

Tw III

2009

Tw I

Tw III

2010

Tw I

Tw III

2011

Tw I

Tw III

2012

Tw I

Tw III

Tw I

Tw III

Tw I

1.30

1.20

1.10

1.00

0.90

0.80

0.70

0.60

2013 2014

Chapter 1. Financial System Stability

Government and Central Bank

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Dec

09

Dec

10

Dec

11

Dec

12

Dec

13

Jan

14

Feb1

4

Mar

14

Apr

14

May

14

Jun

14

Stocks16%

Bonds10%

ExternalDebt29%

Credit45%

LOANAGREEMENT

73.4%

BONDS19.9%

OTHERS0.4%

PAYABLES6.4%

Short Term20%

Long Term80%

24

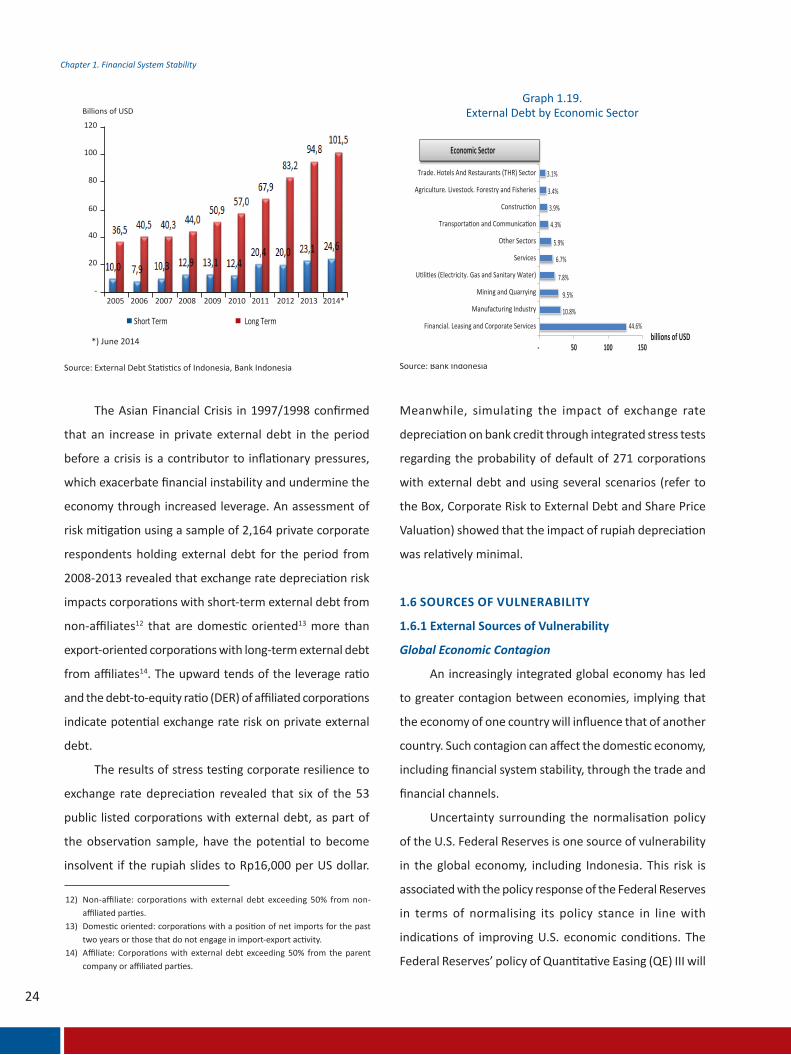

Chapter 1. Financial System Stability

Source: External Debt Statistics of Indonesia, Bank Indonesia

*) June 2014

Source: Bank Indonesia

Graph 1.19.External Debt by Economic Sector

The Asian Financial Crisis in 1997/1998 confirmed

that an increase in private external debt in the period

before a crisis is a contributor to inflationary pressures,

which exacerbate financial instability and undermine the

economy through increased leverage. An assessment of

risk mitigation using a sample of 2,164 private corporate

respondents holding external debt for the period from

2008-2013 revealed that exchange rate depreciation risk

impacts corporations with short-term external debt from

non-affiliates12 that are domestic oriented13 more than

export-oriented corporations with long-term external debt

from affiliates14. The upward tends of the leverage ratio

and the debt-to-equity ratio (DER) of affiliated corporations

indicate potential exchange rate risk on private external

debt.

The results of stress testing corporate resilience to

exchange rate depreciation revealed that six of the 53

public listed corporations with external debt, as part of

the observation sample, have the potential to become

insolvent if the rupiah slides to Rp16,000 per US dollar.

12) Non-affiliate: corporations with external debt exceeding 50% from non-affiliated parties.

13) Domestic oriented: corporations with a position of net imports for the past two years or those that do not engage in import-export activity.

14) Affiliate: Corporations with external debt exceeding 50% from the parent company or affiliated parties.

Meanwhile, simulating the impact of exchange rate

depreciation on bank credit through integrated stress tests

regarding the probability of default of 271 corporations

with external debt and using several scenarios (refer to

the Box, Corporate Risk to External Debt and Share Price

Valuation) showed that the impact of rupiah depreciation

was relatively minimal.

1.6 SOURCES OF VULNERABILITY

1.6.1 External Sources of Vulnerability

Global Economic Contagion

An increasingly integrated global economy has led

to greater contagion between economies, implying that

the economy of one country will influence that of another

country. Such contagion can affect the domestic economy,

including financial system stability, through the trade and

financial channels.

Uncertainty surrounding the normalisation policy

of the U.S. Federal Reserves is one source of vulnerability

in the global economy, including Indonesia. This risk is

associated with the policy response of the Federal Reserves

in terms of normalising its policy stance in line with

indications of improving U.S. economic conditions. The

Federal Reserves’ policy of Quantitative Easing (QE) III will

120

Billions of USD

100

80

60

40

20

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*-

Short Term Long Term

- 50 100 150

44.6%

10.8%

9.5%

7.8%

6.7%

5.9%

4.3%

3.9%

3.4%

3.1%

billions of USD

Economic Sector

Trade. Hotels And Restaurants (THR) Sector

Agriculture. Livestock. Forestry and Fisheries

Construction

Transportation and Communication

Other Sectors

Services

Utilities (Electricity. Gas and Sanitary Water)

Mining and Quarrying

Manufacturing Industry

Financial. Leasing and Corporate Services

25

Chapter 1. Financial System Stability

14.0

12.0

10.0

8.0

6.0

4.0

2.0

-

INDI IND0 CHN KOR TUR

Q1 Q2

2010

Q3 Q4 Q1 Q2

2011

Q3 Q4 Q1 Q2

2012

Q3 Q4 Q1 Q2

2013

Q3 Q4 Q1 Q2

2014

Q3 Q4

2014 2015 2016

PercentAppropriate pace of policy firming

Target federal funds rate at year-end6

5

4

3

2

1

0

Longer Run

be discontinued by the Federal Open Market Committee in

October 2014 and the federal funds rate (FFR) is expected

to increase thereafter in the second or third quarter of

2015 in line with the ongoing U.S. economic recovery. In

addition, the median survey of FOMC members revealed

that the FFR will increase from 1% at the end of 2015

(FOMC March 2014) to 1-1.25% (FOMC June 2014). Such

conditions were further confirmed by the slightly hawkish

statement issued by the chairman of the Federal Reserves

at the FOMC on 30-31st July 2014.

In addition to uncertainty surrounding the

normalisation policy of the Federal Reserves, the economy

will also confront risk linked to vulnerabilities in emerging

market countries, an economic downswing in China

as well as global growth spillover and spillback. Risk in

Indonesia stemming from vulnerabilities in emerging

market countries is moderate compared to peer countries.

Improving conditions are the result of lower inflation,

burgeoning foreign exchange reserves and a relatively

strong exchange rate. Risk stemming from vulnerabilities

in emerging market countries will also be mitigated

as concerns are allayed regarding the banking crisis in

Portugal. Meanwhile, the impact of Argentina defaulting

will be limited as the episode is seen as a temporary

interruption rather than a permanent default. On the

other hand, risk associated with the economic rebalancing

process in China requires attention due to the large role

China plays as a trade partner of Indonesia. Furthermore,

the economic downturn in China also has an impact on

commodity prices, growth (investment) and the financial

system (shadow banking). Meanwhile, there is also the risk

of global growth spillover and spillback between advanced

countries and emerging market countries through four

channels, namely the trade channel, commodity prices,

the global financial system and the neighbourhood effect.

Although external vulnerabilities require vigilance,

the risk premium improved as evidenced by a decline in

credit default swaps (CDS). Meanwhile, persistent investor

interest was maintained after a number of authorities

in advanced countries instituted economic stabilisation

policy. China relaxed taxes for small and medium

enterprises (SME) and is accelerating infrastructure

spending during the second half of 2014. The Bank of

Japan projects a rebound in terms of GDP commencing in

the second semester of 2014. Furthermore, the European

Central Bank (ECB) vowed to provide cheap loans for banks

to extend to small and medium enterprises and implement

the ECB’s version of quantitative easing if required. Market

Source: FOMC

Graph 1.20.Fed Fund Survey: FOMC June 2014

Source: Bank Indonesia

Graph 1.21.Growth in Emerging Market Countries

Chapter 1. Financial System Stability

100

90

80

70

60

50

40

30

20

10

0

Jan-

13

Feb-

13

Mar

-13

Apr-

13

May

-13

Jun-

13

Feb-

14

Mar

-14

Apr-

14

May

-14

Jun-

14

Jul-1

3

Aug-

13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

USA UK GER JAP

i o n al

300

250

200

150

100

50

INDO

Jan-

13

Feb-

13

Mar

-13

Apr-

13

May

-13

Jun-

13

Feb-

14

Mar

-14

Apr-

14

May

-14

Jun-

14

Jul-1

3

Aug-

13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

THAI KOR PHI

Chapter 1. Financial System Stability

-150

-100

-50

0

50

100

150

200

250

20

05

Q1

20

05

Q2

20

05

Q3

20

05

Q4

20

06

Q1

20

06

Q2

20

06

Q3

20

06

Q4

20

07

Q1

20

07

Q2

20

07

Q3

20

07

Q4

20

08

Q1

20

08

Q2

20

08

Q3

20

08

Q4

20

09

Q1

20

09

Q2

20

09

Q3

20

09

Q4

20

10

Q1

20

10

Q2

20

10

Q3

20

10

Q4

20

11

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

12

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

Billion USD2

0000

8Q

1

20

08

QQ22

20

08

QQ33

20

08

Q4

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

GlobalFinancialCrisis

TaperingIssue

0

100

200

300

400

500

600

700

800

2005

Q1

2005

Q2

2005

Q3

2005

Q4

2006

Q1

2006

Q2

2006

Q3

2006

Q4

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

BrazilSouth Africa

TurkeyIndonesia

MexicoSouth Korea

3 4 1 2

GlobalFinancialCrisis

TaperingIssue

2 3 4 1

TaperingIssue

Chapter 1. Financial System Stability

Period (T=Quarter) Country Sample

Prior to GlobalFinancial Crisis

T1 2007 –T2 2008 India, Hong Kong, South Korea Brazil, Russia, India,Hong Kong,South Africa,Turkey, Indonesia,Mexico andSouth Korea

Prior toTapering Issue

T1 2012 – T1 2013 India, South Korea, Turkey

T3 2013 – T4 2013 Indonesia, Hong Kong, Russia

50Trillions of Rp Shares

40

30

2010

2011

2012

2013

2014

20

10

0

-10

-20

2010

2011

2012

2013

2014

110

90

70

50

30

10

-10

Trillions of Rp

Chapter 1. Financial System Stability

Billions of USD

20

15

10

5

0

2010 2011 2012 2013-5

up to Q2 2014

Direct Investment

Other Investment

4,000

2,000

0

-2,000

-4,000

-6,000

-8,000

-10,000

-12,000

Current Account (million of US$) (LHS)

12,500

12,000

11,500

11,000

10,500

10,000

9,500

9,000

8,500

8,000

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2014

Q1

2014

Q2

2013

Q3

2013

Q4

Exchange Rate (Rp/$) (RHS)

Chapter 1. Financial System Stability

1.6.2 Internal Sources of Vulnerability

130 rebased 1/1/2013

125

120

115

110

105

100

95

90

85

80

Indonesia

Jan-

13

Feb-

13

Mar

-13

Apr

-13

May

-13

Jun-

13

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

3

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Thailand South Korea the Philippines

Japan13.7%Others

44.4%

China15.0%

US9.0%

Europe8.8%

Singa-pore

Chapter 1. Financial System Stability

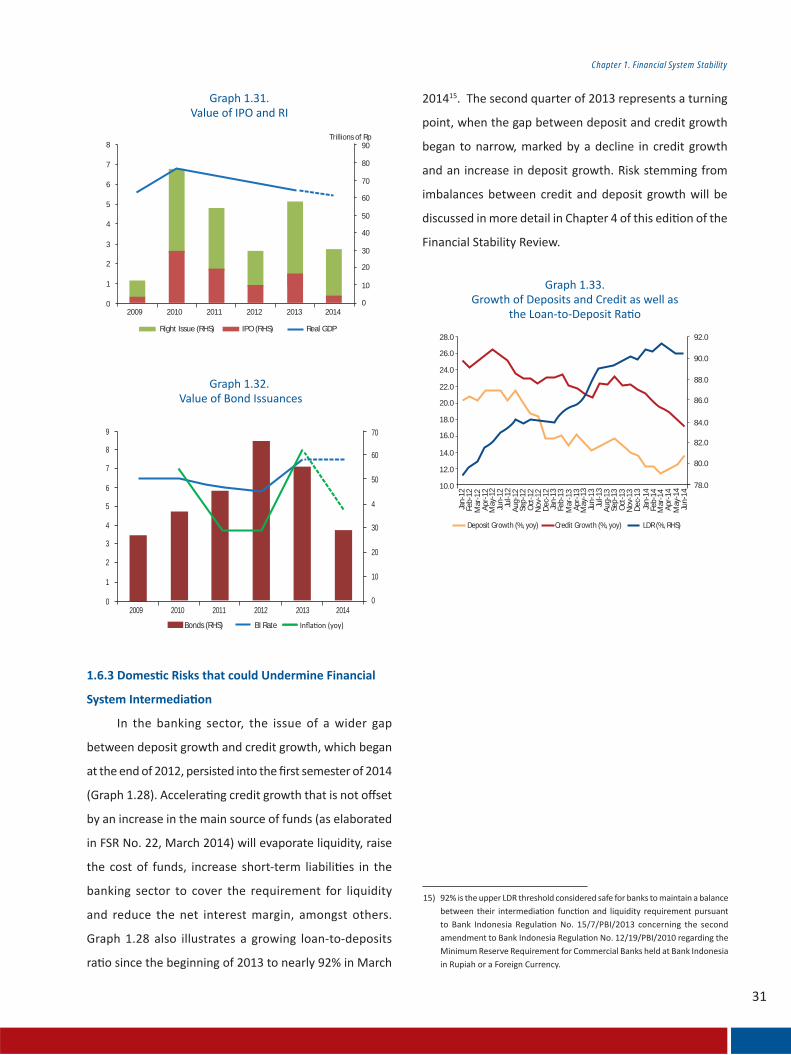

1.6.3 Domes c Risks that could Undermine Financial

System Intermedia on

8

7

6

5

4

3

2

1

02009

Right Issue (RHS) Real GDPIPO (RHS)

Trillions of Rp

2010 2011 2012 2013 2014

90

80

70

60

50

40

30

20

10

0

9

Bonds (RHS) BI Rate

8

7

6

5

4

3

2

1

02009 2010 2011 2012 2013 2014

70

60

50

4

30

20

10

0

28.0 92.0

90.0

88.0

86.0

84.0

82.0

80.0

78.0

26.0

24.0

22.0

20.0

18.0

16.0

14.0Ja

n-12

Feb-

12M

ar-1

2A

pr-1

2M

ay-1

2Ju

n-12

Jul-1

2A

ug-1

2Se

p-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13Fe

b-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug

-13

Sep-

13O

ct-1

3N

ov-1

3D

ec-1

3Ja

n-14

Feb-

14M

ar-1

4A

pr-1

4M

ay-1

4Ju

n-14

12.0

10.0

Credit Growth (%, yoy)Deposit Growth (%, yoy) LDR (%, RHS)

Chapter 1. Financial System Stability

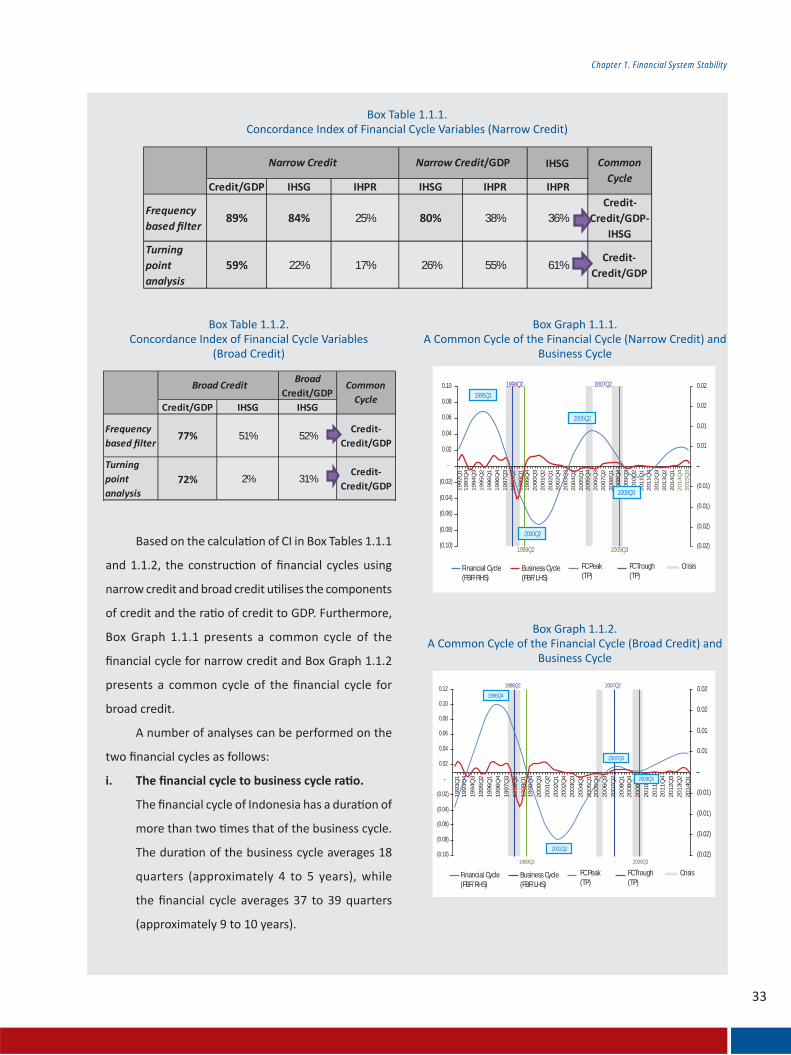

Box 1.1 Financial Cycle of Indonesia

= 1 [ + (1 )(1 )]=1

Chapter 1. Financial System Stability

i. The nancial cycle to business cycle ra o.

IHSG

Credit/GDP IHSG IHPR IHSG IHPR IHPR

Frequency based lter

89% 84% 25% 80% 38% 36%Credit-

Credit/GDP-IHSG

Turning point analysis

59% 22% 17% 26% 55% 61%Credit-

Credit/GDP

Narrow Credit Narrow Credit/GDP Common Cycle

Broad Credit/GDP

Credit/GDP IHSG IHSG

Frequency based lter

77% 51% 52%Credit-

Credit/GDP

Turning point analysis

72% 2% 31%Credit-

Credit/GDP

Broad Credit Common Cycle

2007Q2

0.10

0.12

0.08

0.06

0.04

0.02

-

(0.02)

(0.04)

(0.06)

(0.08)

(0.10)

1996Q4

2002Q2

2007Q3

0.02

0.02

0.01

0.01

(0.01)

(0.01)

(0.02)

(0.02)

19

93

Q1

19

93

Q4

19

94

Q3

19

95

Q2

19

96

Q1

19

96

Q4

19

97

Q3

19

98

Q2

19

99

Q1

19

99

Q4

20

00

Q3

20

01

Q2

20

02

Q1

20

02

Q4

20

03

Q3

20

04

Q2

20

05

Q1

20

05

Q4

20

06

Q3

20

07

Q2

20

08

Q1

20

08

Q4

20

09

Q3

20

10

Q2

20

11

Q1

20

11

Q4

20

12

Q3

20

13

Q2

20

14

Q1

1998Q2

1999Q2 2009Q3

2009Q3

Financial Cycle(FBF/RHS)

Business Cycle(FBF/LHS)

FC Peak(TP)

FC Trough(TP)

Crisis

0.10 0.02

0.02

0.01

0.01

(0.01)

(0.01)

(0.02)

(0.02)

2007Q2

0.08

0.06

0.04

0.02

-

(0.02)

19

92

Q1

19

93

Q4

19

94

Q3

19

95

Q2

19

96

Q1

19

96

Q4

19

97

Q3

19

98

Q2

19

99

Q1

19

99

Q4

20

00

Q3

20

01

Q2

20

02

Q1

20

02

Q4

20

03

Q3

20

04

Q2

20

05

Q1

20

05

Q4

20

06

Q3

20

07

Q2

20

08

Q1

20

08

Q4

20

09

Q3

20

10

Q2

20

11

Q1

20

11

Q4

20

12

Q3

20

13

Q2

20

14

Q1

20

14

Q4

20

15

Q3

(0.04)

(0.06)

(0.08)

(0.10)

1995Q1

2000Q2

2009Q3

2005Q2

1998Q2

1999Q2 2009Q3

Financial Cycle(FBF/RHS)

Business Cycle(FBF/LHS)

FC Peak(TP)

FC Trough(TP)

Crisis

Chapter 1. Financial System Stability

ii. Financial cycle and nancial crisis/stress in the

nancial system.

iii. Financial cycle amplitude

Peak to peak 19 38 40Trough to trough 17 39 35Cycle 18 39 37Financial cycle/Business cycle

2.10 2.04

Average Dura on (in quarters)

Cycle BusinessCycle (GDP)

Financial Cycle(Narrow Credit)

Financial Cycle(Broad Credit)

FBF TP FBF TP

1997Q3 -9 3 -3 3 Economic Crisis and Financial Crisis

2005Q3 -1 - - - Mini Economic Crisis2008Q4 -14 -6 -5 -6 Economic Crisis

FBF = frequency-based ter , TP = turning-point

Crisis/Stress

Narrow CreditFinancial Cycle

Broad CreditFinancial Cycle Descrip on

Chapter 1. Financial System Stability

Chapter 1. Financial System Stability

Box 1.2 Macropruden al and Monetary Policy Nexus

13.0 12000

11000

10000

9000

8000

12.0

11.0

10.0

9.0

8.0

7.0

6.0

5.0

4.03.0

GDP Growth (%, yoy) Exchange Rate ($/Rp, RHS)BI Rate (%)

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Mar

-13

Sep-

13

Mar

-14

Sep-

12

3.0

4.0

Exchange Rate ($/Rp. RHS)

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-12

2.0

1.0

0.0

-1.0

-2.0

-3.0

-4.0

-5.0

12000

11000

10000

9000

8000

Chapter 1. Financial System Stability

40.0 3.0

2.5

1.5

1.0

0.5

0.0

-0.5

-1.0

-1.5

-2.0

2.035.0

30.0

25.0

20.0

15.0

10.0

Sep-

01M

ar-0

2Se

p-02

Credit/GDP Gap (%, RHS) Credit/GDP (%) Trend

Mar

-03

Sep-

03M

ar-0

4Se

p-04

Mar

-05

Sep-

05M

ar-0

6Se

p-06

Mar

-07

Sep-

07M

ar-0

8Se

p-08

Mar

-09

Sep-

09M

ar-1

0Se

p-10

Mar

-11

Sep-

11M

ar-1

2Se

p-12

Mar

-13

Sep-

13M

ar-1

4Se

p-14

218

6

4

2

0

-2

-4

-6

-8

16

11

6

Deposit Growth Gap (%, RHS) Deposit Growth (%, yoy) Tren

1

2002

Q1

2002

Q4

2003

Q3

2004

Q2

2005

Q1

2005

Q4

2006

Q3

2007

Q2

2008

Q1

2008

Q4

2009

Q3

2010

Q2

2011

Q1

2011

Q4

2012

Q3

2013

Q2

2014

Q1

2014

Q4

Chapter 1. Financial System Stability

Box 1.3 The Importance of Macropruden al Regula on and Supervision

Chapter 1. Financial System Stability

Chapter 1. Financial System Stability

st

41

Chapter 2. Financial Markets

Financial Markets

Chapter 2

42

Chapter 2. Financial Markets

This page is intentionally left blank

43

Chapter 2. Financial Markets

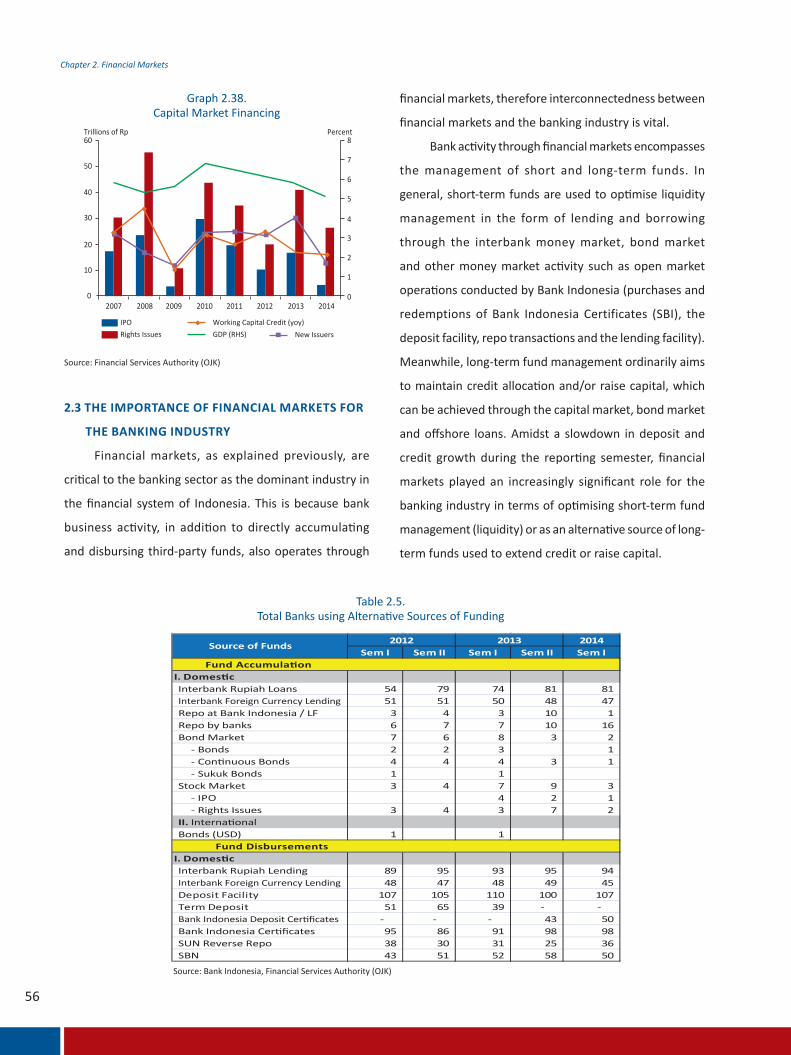

2.1 FINANCIAL MARKET RISKS

Domestic economic growth, which outpaced the

global economy, garnered investor confidence and

catalysed domestic financial market activity, coupled with

less intense financial market risks during the first semester

of 2014. Nonetheless, several potential risks continued to

demand vigilance in light of macroeconomic fundamentals

vulnerable to external imbalances. Furthermore,

uncertainty surrounding the global economy and domestic

political conditions affected near-term financial market

performance. Potential financial market risks emerged in

the guise of foreign capital flows as well as risks on the

money market, foreign exchange market, bond market,

stock market and mutual fund market.

National economic growth, which outperformed the global economy, helped stimulate domestic

financial market activity throughout the first semester of 2014. Such conditions were mirrored by a

maintained influx of foreign capital, greater transaction volume on the interbank money market (PUAB),

escalating interbank repurchase agreements (repo) and foreign exchange transactions, an increase in

outstanding tradeable government securities (SBN) and corporate bonds, gains on the IDX Composite

index as well as growth in managed investment funds. Furthermore, surging financial market activity

was accompanied by relatively well-mitigated risk, evidenced by declines in the interbank rate and its

volatility, a narrower spread between non-deliverable forwards and one-month onshore forwards,

lower SBN yields and volatility, less volatility on the stock market, an increase in net asset value

(NAV) as well as less volatility (beta coefficient) of mutual funds. Nevertheless, financial markets in

Indonesia remained vulnerable to potential risk stemming from external imbalances, primarily linked

to a possible sudden capital reversal.

2.1.1 Foreign Capital Flows

Growing investor confidence in the domestic

economy and financial markets was indicated by an

inflow of foreign purchases of domestic financial market

instruments, including Bank Indonesia Certificates (SBI),

tradable government securities (SBN), corporate bonds

and shares. On the SBI market, foreign holdings increased

from the beginning of the reporting semester to reach

Rp8.57 trillion in May 2014 before subsequently returning

to record an outflow of Rp3.87 trillion in June. In general,

however, foreign SBI holdings registered a net inflow

of Rp10.96 trillion. On the SBN market, foreign inflows

peaked at Rp20.15 trillion in May 2014, with a total value

for the reporting semester of Rp79.95 trillion. Concerning

the stock market, foreign inflows peaked in April 2014 at

Rp11.48 trillion, with a total inflow value of Rp48.07 trillion

Chapter2

Financial Markets

44

Chapter 2. Financial Markets

Source: Bloomberg, Bank Indonesia

Graph 2.1Non-Resident Flows: Shares, SBN & SBI

Source: Bank Indonesia

Graph 2.2Rupiah Interbank Money Market Performance

Source: Bank Indonesia

Graph 2.3Overnight Rupiah Interbank Rate

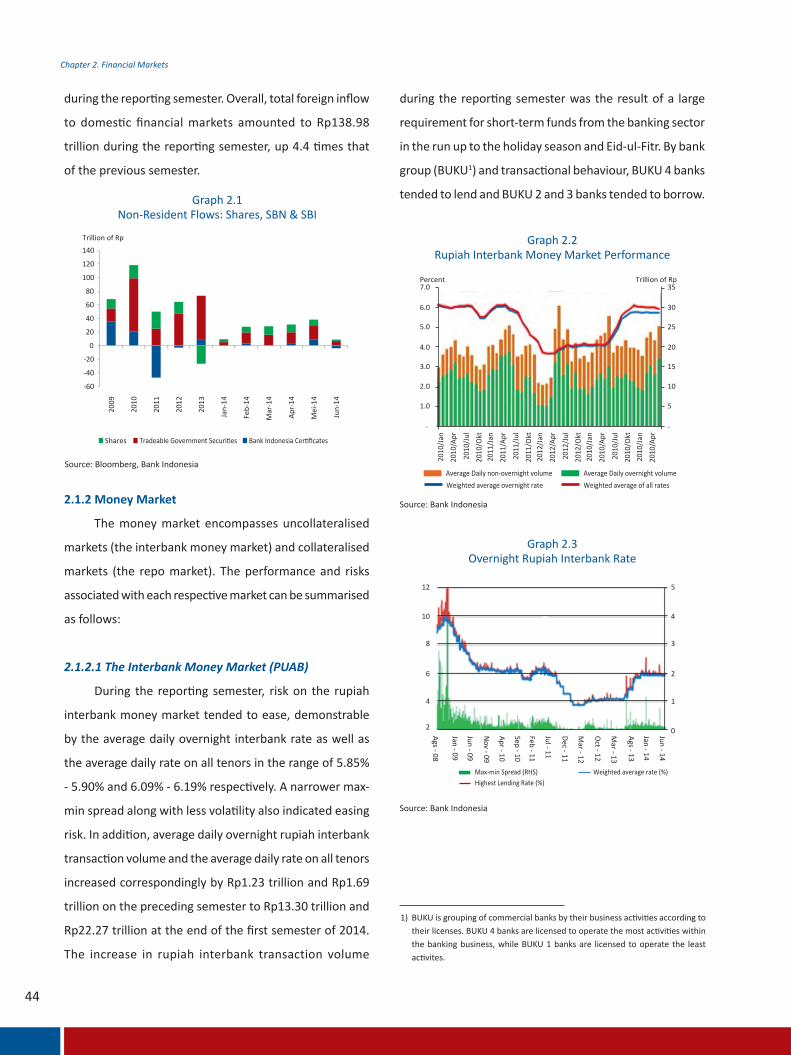

during the reporting semester. Overall, total foreign inflow

to domestic financial markets amounted to Rp138.98

trillion during the reporting semester, up 4.4 times that

of the previous semester.

during the reporting semester was the result of a large

requirement for short-term funds from the banking sector

in the run up to the holiday season and Eid-ul-Fitr. By bank

group (BUKU1) and transactional behaviour, BUKU 4 banks

tended to lend and BUKU 2 and 3 banks tended to borrow.

2.1.2 Money Market

The money market encompasses uncollateralised

markets (the interbank money market) and collateralised

markets (the repo market). The performance and risks

associated with each respective market can be summarised

as follows:

2.1.2.1 The Interbank Money Market (PUAB)

During the reporting semester, risk on the rupiah

interbank money market tended to ease, demonstrable

by the average daily overnight interbank rate as well as

the average daily rate on all tenors in the range of 5.85%

- 5.90% and 6.09% - 6.19% respectively. A narrower max-

min spread along with less volatility also indicated easing

risk. In addition, average daily overnight rupiah interbank

transaction volume and the average daily rate on all tenors

increased correspondingly by Rp1.23 trillion and Rp1.69

trillion on the preceding semester to Rp13.30 trillion and

Rp22.27 trillion at the end of the first semester of 2014.

The increase in rupiah interbank transaction volume

-60

-40

-20

0

20

40

60

80

100

120

140

2009

2010

2011

2012

2013

Jan-

14

Feb-

14

Mar

-14

Apr-

14

Mei

-14

Jun-

14

Trillion of Rp

Shares Tradeable Government Securities Bank Indonesia Certificates

7.0 35

30

25

20

15

10

5

--

6.0

5.0

4.0

3.0

2.0

1.0

2010

/Jan

2010

/Apr

2010

/Jul

2010

/Okt

2011

/Jan

2011

/Apr

2011

/Jul

2011

/Okt

2012

/Jan

2012

/Apr

2012

/Jul

2012

/Okt

2010

/Jan

2010

/Apr

2010

/Jul

2010

/Okt

2010

/Jan

2010

/Apr

Percent Trillion of Rp

Average Daily non-overnight volumeWeighted average overnight rate

Average Daily overnight volumeWeighted average of all rates

Ags - 08

Jan - 09

Jun - 09

Nov - 09

Apr - 10

Sep - 10

Feb - 11

Jul - 11

Dec - 11

Mar - 12

Oct - 12

Mar - 13

Ags - 13

Jan - 14

Jun - 14

512

10

8

6

4

2

4

3

2

1

0

Max-min Spread (RHS) Weighted average rate (%)Highest Lending Rate (%)

1) BUKU is grouping of commercial banks by their business activities according to their licenses. BUKU 4 banks are licensed to operate the most activities within the banking business, while BUKU 1 banks are licensed to operate the least activites.

45

Chapter 2. Financial Markets

foreign exchange interbank money market volume

increased moderately by US$3.3 million to US$492.22

million. The large decline in average daily transaction

volume on the foreign exchange interbank money market,

accompanied by an increase on the rupiah interbank

money market, demonstrated that the banking sector

favoured the rupiah interbank money market to manage

its short-term funds. By bank group and transactional

behaviour, BUKU 3 and 4 banks were lenders, while BUKU

2 banks were borrowers.

Source: Bank Indonesia

Graph 2.4Rupiah Interbank Rate Volatility

Source: Bank Indonesia

Graph 2.5Rupiah Interbank Transactional Behaviour

Source: Bank Indonesia

Graph 2.6Foreign Exchange Interbank Money Market

Source: Bank Indonesia

Graph 2.7Overnight Foreign Exchange Interbank Rate

Congruent with less risk on the rupiah interbank

money market, risk on the foreign exchange interbank

money market also eased, reflected by the average daily

overnight foreign exchange interbank rate and the average

daily rate on all tenors in the range of 0.12% - 0.15% and

0.14% - 0.18% respectively. Narrower spread between

the max-min overnight interbank rate, coupled with less

volatility, was also evidence of less risk. Average daily

foreign exchange interbank money market transaction

volume of all tenors dropped US$77.40 million on the

preceding semester to US$667.43 million at the end of the

first semester of 2014. Meanwhile, average daily overnight

Jan-

13Fe

b-13

Mar

-13

Apr-1

3

May

-13

Jun-

13Ju

l-13

Aug-

13

Sep-

13

Oct

-13

Nov

-13

Dec-

13

Jan-

14Fe

b-14

Mar

-14

Apr-1

4

May

-14

Jun-

14

90% 8.0

7.5

7.0

6.5

6.0

5.5

5.0

4.5

4.0

80%

70%

60%

50%

40%

30%

20%

10%

0%

BI Rate (RHS)

Lending Facility (RHS)

O/N Interbank Rate (RHS)O/N Rp Interbank VolatilityDeposit Facility (RHS)

2012/Jan

2012/Mar

2012/May

2012/Jul

2012/Sep

2012/Nov

2013/Jan

2013/Mar

2013/May

2013/Jul

2013/Sep

2013/Nov

2014/Jan

2014/Mar

2014/May

150

100

50

0

-50

-100

-150

Buku 4

Trillions of Rp

Buku 3 Buku 2 Buku 1

1,6000.35

Average Daily Non-O/N Volume

0.30

0.25

0.20

0.15

0.10

0.05

-

1,400

1,200

1,000

800

600

400

200

-

Millions of USDPercent

naJ/0102

rpA/0102

l uJ/0102

tgA/0102naJ/1102

r pA/1102

l uJ/1102

tgA/1102naJ/2102

r pA/2102

l uJ/2102

tgA/2102naJ/3102

r pA/3102

l uJ/3102

tgA/3102naJ/4102

r pA/4102

Weighted Average O/N RateAverage Daily O/N VolumeWeighted Average of All Rates

Max-min Spread (RHS) Weighted average rate (%)

0.50 1.8

1.6

1.4

1.2

1

0.8

0.6

0.4

0.2

0

0.45

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0.00Nov - 08Feb - 09M

ay - 09Ags- 09Nov - 09Feb - 10M

ay - 10Ags- 10Nov - 10Feb - 11M

ay - 11Ags- 11Nov - 11Feb - 12M

ay - 12Ags- 12Nov - 12Feb - 13M

ay - 13

Feb - 14M

ay - 14

Ags- 13Nov - 13

Highest Lending Rate (%)

46

Chapter 2. Financial Markets

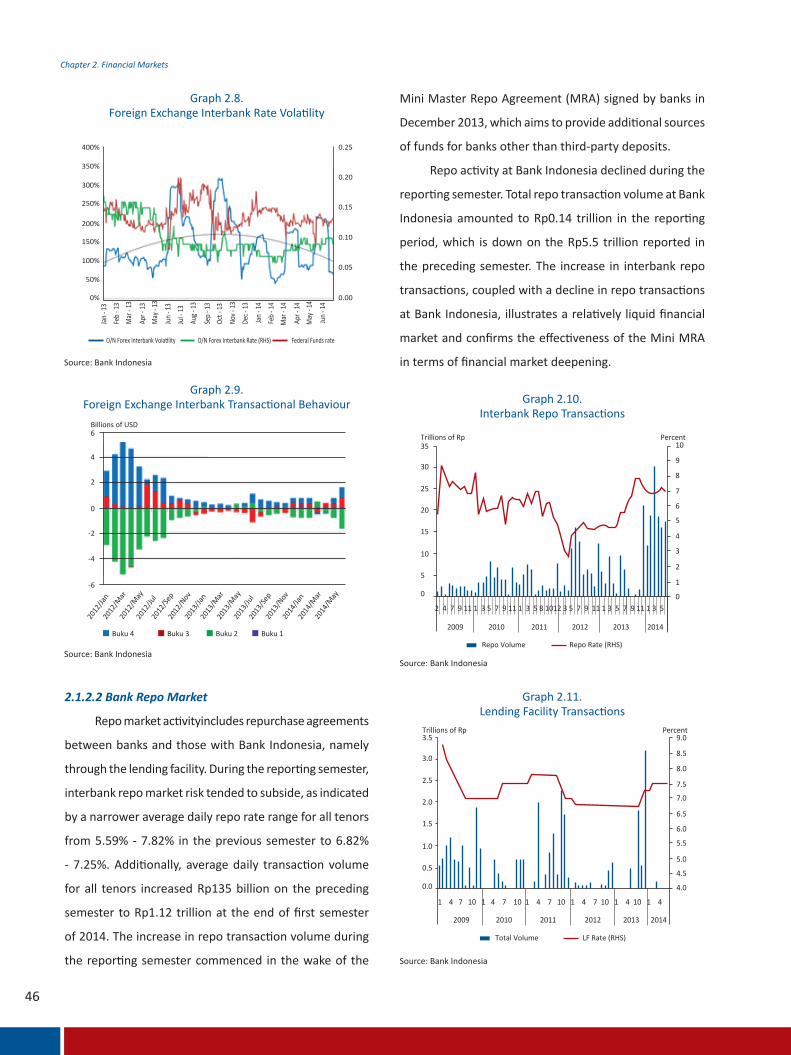

2.1.2.2 Bank Repo Market

Repo market activityincludes repurchase agreements

between banks and those with Bank Indonesia, namely

through the lending facility. During the reporting semester,

interbank repo market risk tended to subside, as indicated

by a narrower average daily repo rate range for all tenors

from 5.59% - 7.82% in the previous semester to 6.82%

- 7.25%. Additionally, average daily transaction volume

for all tenors increased Rp135 billion on the preceding

semester to Rp1.12 trillion at the end of first semester

of 2014. The increase in repo transaction volume during

the reporting semester commenced in the wake of the

Source: Bank Indonesia

Graph 2.8.Foreign Exchange Interbank Rate Volatility

Source: Bank Indonesia

Graph 2.9.Foreign Exchange Interbank Transactional Behaviour

Source: Bank Indonesia

Graph 2.10.Interbank Repo Transactions

Source: Bank Indonesia

Graph 2.11.Lending Facility Transactions

Mini Master Repo Agreement (MRA) signed by banks in

December 2013, which aims to provide additional sources

of funds for banks other than third-party deposits.

Repo activity at Bank Indonesia declined during the

reporting semester. Total repo transaction volume at Bank

Indonesia amounted to Rp0.14 trillion in the reporting

period, which is down on the Rp5.5 trillion reported in

the preceding semester. The increase in interbank repo

transactions, coupled with a decline in repo transactions

at Bank Indonesia, illustrates a relatively liquid financial

market and confirms the effectiveness of the Mini MRA

in terms of financial market deepening.

O/N Forex Interbank Rate (RHS) Federal Funds rateO/N Forex Interbank Volatility

Jan -

13

Feb -

13M

ar - 1

3

Apr -

13M

ay - 1

3

Jun -

13

Jan -

14

Feb -

14M

ar - 1

4

Apr -

14M

ay - 1

4

Jun -

14

Jul -

13

Aug -

13

Sep -

13Oc

t - 13

Nov -

13

Dec -

13

400% 0.25

0.20

0.15

0.10

0.05

0.00

350%

300%

250%

200%

150%

100%

50%

0%

6Billions of USD

4

2

0

-2

-4

-6

2012

/Jan

2012

/Mar

2012

/May

2012

/Jul

2012

/Sep

2012

/Nov

2013

/Jan

2013

/Mar

2013

/May

2014

/Jan

2014

/Mar

2014

/May

2013

/Jul

2013

/Sep

2013

/Nov

Buku 4 Buku 3 Buku 2 Buku 1

35Trillions of Rp Percent

9

10

8

7

6

5

4

3

2

1

0

30

25

20

15

10

5

0

2 4 7 9 11 1 3 5 7 9 11 1 3 5 8 1012 3 5 7 9 11 1 3 5 7 9 11 1 3 5

2009 2010 2011 2012 2013 2014

Repo Volume Repo Rate (RHS)

3.5Trillions of Rp Percent

9.0

8.5

8.0

7.5

7.0

6.5

6.0

5.5

5.0

4.5

4.0

3.0

2.5

2.0

1.5

1.0

0.5

0.0

1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 10 1 4

2009 2010 2011 2012 2013 2014

Total Volume LF Rate (RHS)

47

Chapter 2. Financial Markets

3.1.3 Foreign Exchange Market

Risk also eased on the foreign exchange market,

amongst others reflected by a narrower spread between

non-deliverable forwards and one-month onshore

forwards. Furthermore, adequate liquidity on the foreign

exchange market also signalled less risk. Total foreign

exchange transaction volume increased from US$262.03

billion in the second semester of 2013 to USD322.17 in

the reporting period.

In terms of composition, spot transactions

dominated the domestic foreign exchange market with a

volume accounting for 67.31% of total foreign exchange

transactions. Meanwhile, the portion of forward and swap

transactions amounted to 5.45% and 27.24% respectively.

The relatively small share of forward and swap transactions

in comparison to spot transactions is an indicator of a

shallow domestic foreign exchange market that requires

further financial deepening efforts.

Source: Bank Indonesia, Bloomberg, processed

Graph 2.12.Foreign Exchange Market Risk Premium

Source: Bank Indonesia, Bloomberg, processed

Graph 2.13.Swap Transaction Volume

Source: Bank Indonesia

Graph 2.14.Domestic Foreign Exchange Market Volume

Source: Bank Indonesia

Graph 2.15.Foreign Exchange Transaction Volume Trend

800Point Rp

13,000

12,500

12,000

11,500

11,000

10,500

10,000

9,500

9,000

8,500

8,000

600

400

200

-200

-400

-600

-800

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jan-

14

Mar

-14

May

-14

Jul-1

3

Sep-

13

Nop

-13

0

Spread NDF-FWD 1B RRH 10D Spread NDF 1B (RHS)

8.0%

7.0%120

100

80

60

40

20

Jun-12 Dec-12 Dec-13Jun-13 Jun-14

6.0%

5.0%

4.0%

3.0%

2.0%

1.0%

0.0%

Total Vol. Semesteran (RHS) Premi Swap Broker O/N

Billions of USD

Premi Swap Broker 1B Premi Swap Broker 3BPremi Swap Broker 6B

70

60

50

40

30

20

10

OPTION

0

2010

/Jan

2010

/Mar

2010

/May

2010

/Jul

2010

/Sep

2010

/Nov

2011

/Jan

2011

/Mar

2011

/May

2011

/Jul

2011

/Sep

2011

/Nov

2012

/Jan

2012

/Mar

2012

/May

2012

/Jul

2012

/Sep

2012

/Nov

2013

/Jan

2013

/Mar

2013

/May

2013

/Jul

2013

/Sep

2013

/Nov

2014

/Jan

2014

/Mar

2014

/May

Billions of USD

FORWARD SWAP SPOT

65

60

55

50

45

40

35

301 2 3 4 5 6 7 8 9 10 11 12

Billions of USD

2011 2012 2013 2014

48

Chapter 2. Financial Markets

2.1.4 Bond Market

On the bond market, economic stimulus packages

and low interest rates in a number of advanced countries

were important factors leading to an influx of foreign

capital into government securities (SBN), increasing from

Rp44.46 trillion in the second semester of 2013 to Rp79.95

trillion in the reporting semester. Foreign purchases of SBN

occurred on the secondary market as well as issuances on

the primary market by the government. Accordingly, the

portion of foreign SBN holdings increased from 32.54% on

the preceding semester to 35.66%.

Source: Bank Indonesia

Graph 2.16.Foreign Net Flow to SBN and IDMA Index

Source: CEIC

Graph 2.17.SBN Holdings

The surge in foreign inflow to SBN prompted higher

SBN prices, with the IDMA index rallying to 96.65 points

from 95.46 points in the previous semester. Meanwhile,

SBN market risk eased as yield and volatility decreased.

SBN yield for tenors of 10 years dropped 28 bps to 8.09%,

accompanied by a 46 bps decline in volatility to 2.18%,

one of the lowest in Asia.

Source: Bloomberg, processed

Source: Bloomberg, processed

Table 2.1.10-Year SBN Yield and Regional Yields

Table 2.2.10-Year SBN Volatility and Regional Volatility (%)

INDO INDI THAI MAL PHILJun-13 7.06 7.69 3.63 3.72 4.07Jul-13 8.52 8.86 4.13 4.04 3.18

Aug-13 8.32 8.97 3.87 3.76 3.61Sep-13 5.93 8.31 3.50 3.55 4.65Oct-13 5.65 8.33 3.30 3.43 4.67

Nov-13 8.59 9.09 3.91 4.30 3.35Dec-13 8.37 9.17 3.80 4.20 3.42Jan-14 8.81 8.86 3.78 4.22 4.24Feb-14 8.34 9.06 3.54 4.10 4.38Mar-14 7.99 9.11 3.51 4.01 3.85Apr-14 7.86 9.02 3.42 3.95 3.98

May-14 7.95 8.77 3.57 3.96 3.61Jun-14 8.09 8.58 3.57 3.93 3.78

INDO IND THAI MAL PHIJun-13 8.69 5.36 9.56 8.19 16.13 Jul-13 17.47 26.20 3.16 7.53 8.99

Aug-13 11.78 10.63 7.24 2.78 1.77 Sep-13 12.97 5.38 8.23 6.41 6.51 Oct-13 17.04 2.81 3.02 4.22 6.46 Nov-13 4.22 8.23 5.78 6.88 2.74 Dec-13 2.64 7.95 2.62 3.03 14.06 Jan-14 9.93 8.78 1.77 4.91 12.75 Feb-14 5.23 5.66 3.22 2.41 3.70 Mar-14 4.03 3.11 3.37 2.65 5.74 Apr-14 1.64 5.19 3.35 1.39 2.09

May-14 2.17 6.12 3.20 3.31 2.82 Jun-14 2.18 5.32 1.50 0.98 3.23

90Trillions of Rp Point

115

80

70

60

50

40

30

20

10

2009

2010

2011

2012

2013

Jan-

14

Feb-

14

Mar

-14

Apr-1

4

May

-14

Jun-

14

0

110

105

100

95

90

85

80

SBN IDMA (RHS)

1200Trillions of Rp

1000

800

600

400

200

0Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Jun-14Dec-13

Others Securities Pension Funds Foreign

Insurers Mutual Funds Central Bank Banks

49

Chapter 2. Financial Markets

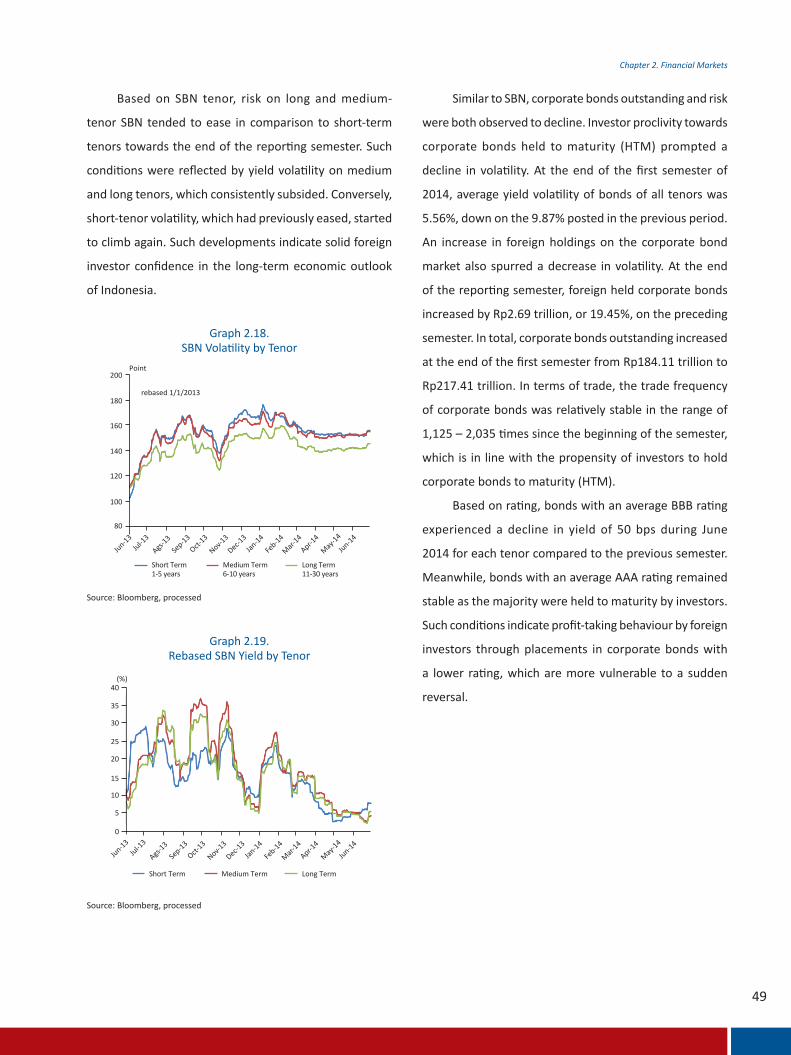

Based on SBN tenor, risk on long and medium-

tenor SBN tended to ease in comparison to short-term

tenors towards the end of the reporting semester. Such

conditions were reflected by yield volatility on medium

and long tenors, which consistently subsided. Conversely,

short-tenor volatility, which had previously eased, started

to climb again. Such developments indicate solid foreign

investor confidence in the long-term economic outlook

of Indonesia.

Source: Bloomberg, processed

Graph 2.18.SBN Volatility by Tenor

Source: Bloomberg, processed

Graph 2.19.Rebased SBN Yield by Tenor

Similar to SBN, corporate bonds outstanding and risk

were both observed to decline. Investor proclivity towards

corporate bonds held to maturity (HTM) prompted a

decline in volatility. At the end of the first semester of

2014, average yield volatility of bonds of all tenors was

5.56%, down on the 9.87% posted in the previous period.

An increase in foreign holdings on the corporate bond

market also spurred a decrease in volatility. At the end

of the reporting semester, foreign held corporate bonds

increased by Rp2.69 trillion, or 19.45%, on the preceding

semester. In total, corporate bonds outstanding increased

at the end of the first semester from Rp184.11 trillion to

Rp217.41 trillion. In terms of trade, the trade frequency

of corporate bonds was relatively stable in the range of

1,125 – 2,035 times since the beginning of the semester,

which is in line with the propensity of investors to hold

corporate bonds to maturity (HTM).

Based on rating, bonds with an average BBB rating

experienced a decline in yield of 50 bps during June

2014 for each tenor compared to the previous semester.

Meanwhile, bonds with an average AAA rating remained

stable as the majority were held to maturity by investors.

Such conditions indicate profit-taking behaviour by foreign

investors through placements in corporate bonds with

a lower rating, which are more vulnerable to a sudden

reversal.

200Point

rebased 1/1/2013