Financial Stability Review (FSR) - Bank · PDF fileThe preparation of the Financial Stability...

130

-

Upload

nguyennguyet -

Category

Documents

-

view

215 -

download

0

Transcript of Financial Stability Review (FSR) - Bank · PDF fileThe preparation of the Financial Stability...

The preparation of the Financial Stability Review (FSR) is one of the avenues

through which Bank Indonesia achieves its mission “to safeguard the stability of the Indonesian

Rupiah by maintaining monetary and financial system stability for sustainable national

economic development”.

Publisher :

Bank Indonesia

Jl. MH Thamrin No.2, Jakarta

Indonesia

Information and Orders:

This edition is published in March 2011 and is based on data and information available as of December 2010, unless stated

otherwise.

The PDF format is downloadable from: http://www.bi.go.id

For inquiries, comments and feedback please contact:

Bank Indonesia

Directorate of Banking Research and Regulation

Financial System Stability Bureau

Jl.MH Thamrin No.2, Jakarta, Indonesia

Phone : (+62-21) 381 8902, 381 8075

Fax : (+62-21) 351 8629

Email : [email protected]

FSR is published biannually with the objectives:

To improve public insight in terms of understanding financial system stability.

To evaluate potential risks to financial system stability.

To analyze the developments of and issues within the financial system.

To offer policy recommendations to promote and maintain financial system stability.

Financial Stability Review

( No. 16, March 2011)

Bolstering Financial System Stability amid a deluge of Foreign Capital Inflows

Theme:

Directorate of Banking Research and Regulation

Financial System Stability Bureau

ii

iii

Foreword .............. .................................................................................................................................................. vi

Overview ......... ........................................................................................................................................................ 1

Chapter 1. Risk from the Global Environment ............................................................................................................ 5

1.1. Sources of Vulnerability ........................................................................................................................... 8

1.2. Strengthening Risk in Indonesia............................................................................................................... 12

Chapter 2. Financial System Resilience ....................................................................................................................... 21

2.1. Financial System Structure and Resilience ................................................................................................. 23

2.2. Banking System Risk................................................................................................................................. 24

2.3. Potential Financial Market Risk and Financing........................................................................................... 36

Boks 2.1. Bank Liquidity Resilience ................................................................................................................. 46

Boks 2.2. Undisbursed Loans.......................................................................................................................... 49

Boks 2.3. Impact of Credit on Inflation ........................................................................................................... 52

Boks 2.4. Prime Lending Rate Policy Transparency .......................................................................................... 54

Boks 2.5. Sources of Bank Profitability ............................................................................................................ 56

Chapter 3. Strengthening Financial Infrastructure....................................................................................................... 59

3.1. Payment System Efficiency ....................................................................................................................... 61

3.2. Payment System Performance and Risk Mitigation.................................................................................... 65

Chapter 4. Special Topic ............................................................................................................................................ 67

4.1. Financial Sector Reform ........................................................................................................................... 69

4.2. Financial System Safety Net: Cooperation To Create And Maintain Financial System Stability.................... 76

4.3. Crisis Management Protocol (CMP) .......................................................................................................... 77

Boks 4.1 Financial Inclusion ............................................................................................................................. 79

Boks 4.2 Green Banking.................................................................................................................................. 82

Chapter 5. Financial System Stability Challenges and Prospects .................................................................................. 85

5.1. Future External and Internal Economic Conditions .................................................................................... 87

5.2. Financial System Stability Challenges ........................................................................................................ 88

5.3. Financial System Stability Outlook ............................................................................................................ 90

Article........................................................................................................................................................................ 91

Article 1 Risk Behaviour in the Monetary Policy Transmission Mechanism in Indonesia .................................. ... 93

Article 2 Towards Stronger ASEAN financial System : A Proposal for Regional Financial Stability Framework .... 107

Table of Contents

iv

List of Tables and Figures

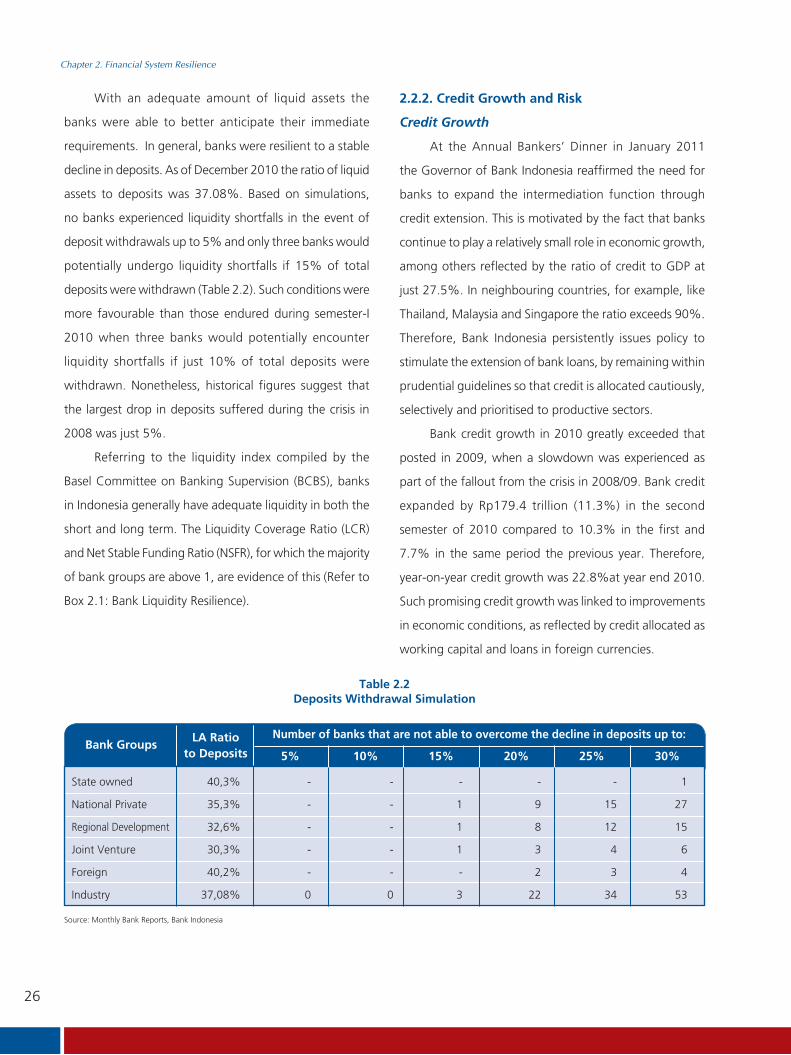

Tables Figures

1.1 Breakdown of Global Economic Growth......... 81.2 State Budget Realisation for Semester I & II, 2010 151.3 Household Expenses and Income.................... 171.4 Effect of Rupiah Depreciation on

Conglomerate Equity ..................................... 19

2.1 Number of Financial Institutions ..................... 232.2 Deposit Withdrawals Simulation..................... 262.3 Profit/Loss ...................................................... 342.4 VaR SUN ........................................................ 382.5 SBN Ownership .............................................. 382.6 Indices of several Global Stock Markets .......... 402.7 Share Price Indices by Sector .......................... 402.8 Jakarta Composite Index (Commodities) ..... 402.9 Financial Ratios of Finance Companies ........ 442.10 NPL of Finance Companies.......................... 442.11 NPL performance of Finance Companies ..... 45

3.1 BI-SSSS Transactions ................................... 63

4.1 Salient Regulations and ImplementationSchedule of Basel III .................................... 72

4.2 Recapitulation of Capital Ratio andLeverage Ratio............................................ 73

5.1 Projections of GDP and Inflation ................. 875.2 Economic Growth in Indonesia according

to Type....................................................... 88

Tables Box

2.1.1 LCR by Bank Group .................................... 472.1.2 NSFR by Bank Group................................... 47

1.1 Global Stock Market Indices (2000=100)........ 91.2 CDS in GIIPS countries and Germany.............. 91.3 CDS in leading Eurozone countries and

Switzerland .................................................... 91.4 CDS in several Asian Countries....................... 101.5 Stock Market Indices in several Countries

in 2010.......................................................... 101.6 Private Capital Flows – FDI and Portfolio to

EM in Asia, Europe and Latin America ............ 101.7 Private Capital Flows to Emerging Markets ..... 111.8 Global Price Indices ........................................ 111.9 Price Indices of several International

Commodities ................................................. 111.10 UBS CMCI Composite Price Index by Sector.... 121.11 Indonesian Development of Non-Oil Export

Import............................................................ 121.12 Indonesia Development of Total Exports and

Imports .......................................................... 121.13 Rupiah Exchange Rate.................................... 131.14 Rupiah Exchange Rate Volatility...................... 131.15 Composition of Direct and Portfolio Investment

to Indonesia ................................................... 131.16 Inflation in Indonesia (Core and Headline) ...... 141.17 Price Indices of Foodstuffs and Oil in Indonesia,

2006 = 100.................................................... 141.18 Inflation in several Advanced Countries .......... 141.19 Inflation in several ASEAN Countries .............. 141.20 Real Interest Rates.......................................... 151.21 Consumer Confidence Index .......................... 161.22 Composition of Household Expenditure

2009-2010..................................................... 161.23 Price Expectation Index for 3 & 6 Months ....... 171.24 Credit and NPL in the Household Sector ......... 171.25 ROA& ROE of Non-financial Public Listed

Companies..................................................... 181.26 DER and TL/TAof Non-financial

Public Listed Companies................................. 181.27 Key Financial Indicators for the Corporate

Sector ............................................................ 181.28 Ratio of Net Foreign Liabilities to Equity.......... 19

v

Figures Box

2.1 Asset Compositions of Financial Institutions ... 232.2 Financial Stability Index, 1996-2010 ............... 242.3 Share of Bank Funding and Financing............. 242.4 Deposit Growths by Semester ........................ 242.5 Deposit Growth based on Ownership............. 252.6 Liquid Assets by Component .......................... 252.7 Share of Placements held at Bank Indonesia ... 252.8 Credit Growth by Type................................... 272.9 Property Credit Growth.................................. 272.10 Credit Growth by Currency ............................ 272.11 Loan to Deposit Ratio by Currency ................. 272.12 MSM Credit Growth (yoy) .............................. 282.13 MSM Lending Rates (%)................................. 282.14 Share of MSM Credit ..................................... 292.15 Loans to Deposits Ratio (LDR) ......................... 292.16 Non-Performing Loans (NPL)........................... 292.17 NPL Ratio by Loan Type .................................. 302.18 NPL Ratio by Currency.................................... 302.19 NPL Ratio by Economic Sector ........................ 312.20 NPL Ratio of Property Loans ........................... 312.21 Gross NPL Ratio of MSM and Non-MSM Loans 312.22 Results of Stress Testing Credit Risk................ 322.23 Rupiah Maturity Profile................................... 322.24 USD Maturity Profile....................................... 322.25 Results of Stress Testing Interest Rate Increases 332.26 Net Open Position (NOP) ................................ 332.27 Results of Stress Testing Rupiah Depreciation . 332.28 Results of Stress Testing a decline in SUN Price 332.29 Rupiah interest Rate Spread ........................... 342.30 Composition of Operational Profit/Loss .......... 342.31 Net Interest Income (monthly) ........................ 352.32 Share of Bank Interest Income........................ 352.33 Capital ........................................................... 352.34 Risk-Weighted Assets .................................... 352.35 Tier 1 and Tier 2............................................. 362.36 Foreign Investments (SBI, SUN and Stock) ....... 362.37 Foreign Portfolio of Rupiah Financial Assets

(SBI, SUN and Stock) ...................................... 372.38 Foreign Capital Inflows and the Exchange Rate,

IDMA Index and JSX....................................... 372.39 SUN Price of Benchmark FR Series .................. 372.40 Average Monthly SUN Price............................ 372.41 VaR SUN ........................................................ 382.42 Maturity Profile SUN ...................................... 382.43 Corporate Bond and SUN Yield (December 2009) 392.44 Corporate Bond and SUN Yield (December 2010) 392.45 Bond Yields in ASEAN (December 2009)......... 392.46 Bond Yields in ASEAN (December 2010)......... 392.47 JSX Composite as well as Global & Regional

Indices (Indexed against the position on31st December 2005)..................................... 39

2.48 Correlation between Commodities andShare Index .................................................... 41

2.49 Volatility of several Asian Bourse Indices......... 412.50 Bank Share Prices ........................................... 412.51 Changes in Bank Share Prices......................... 412.52 Performance of Mutual Funds ........................ 422.53 Net Asset Value by Type of Fund

(in trillions of rupiah) ...................................... 422.54 Capitalization Value and Value of Issuances ... 422.55 Issuances and Position of Corporate Bonds..... 422.56 Business Activity of Finance Companies.......... 432.57 Financing Growth by Finance Companies ....... 432.58 Finance Companies’ Sources of Funds ............ 43

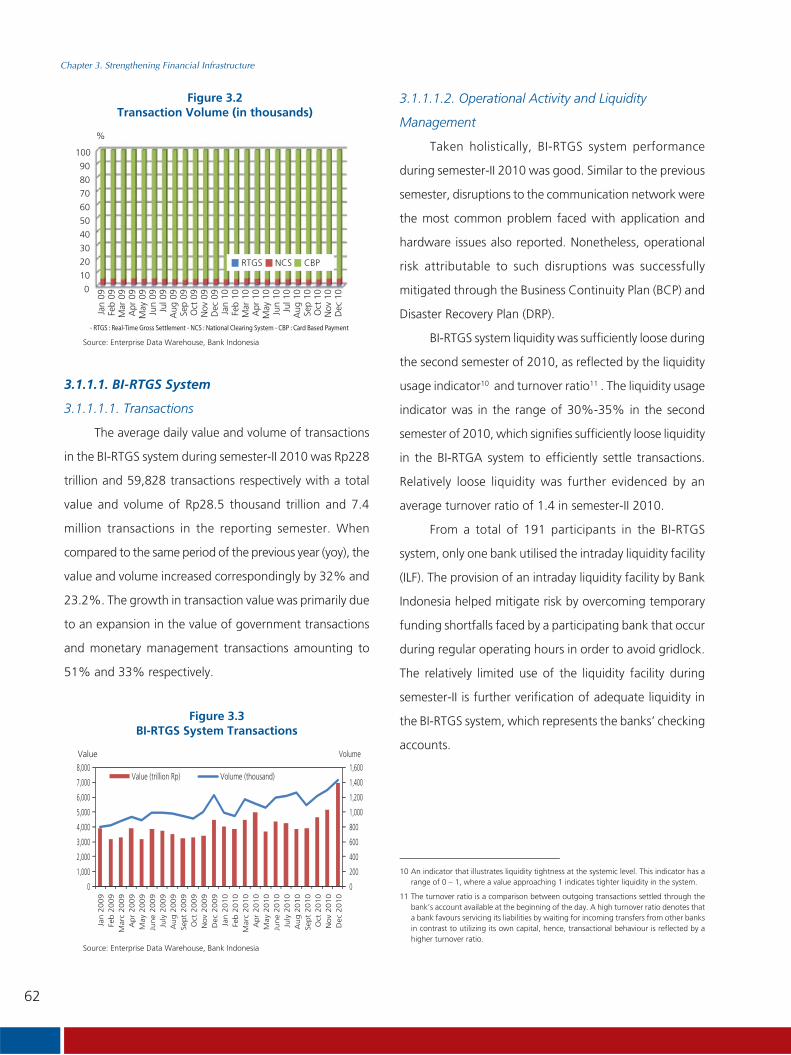

3.1 Nominal Transactions (billions of rupiah) ........ 613.2 Transaction Volume (in thousands)................. 623.3 BI-RTGS System Transactions.......................... 623.4 BI-SSSS Transactions....................................... 633.5 National Clearing System Transactions ........... 643.6 ATM/Debit Card Transactions......................... 643.7 Credit Card Transactions ................................ 643.8 E-money Transactions .................................... 65

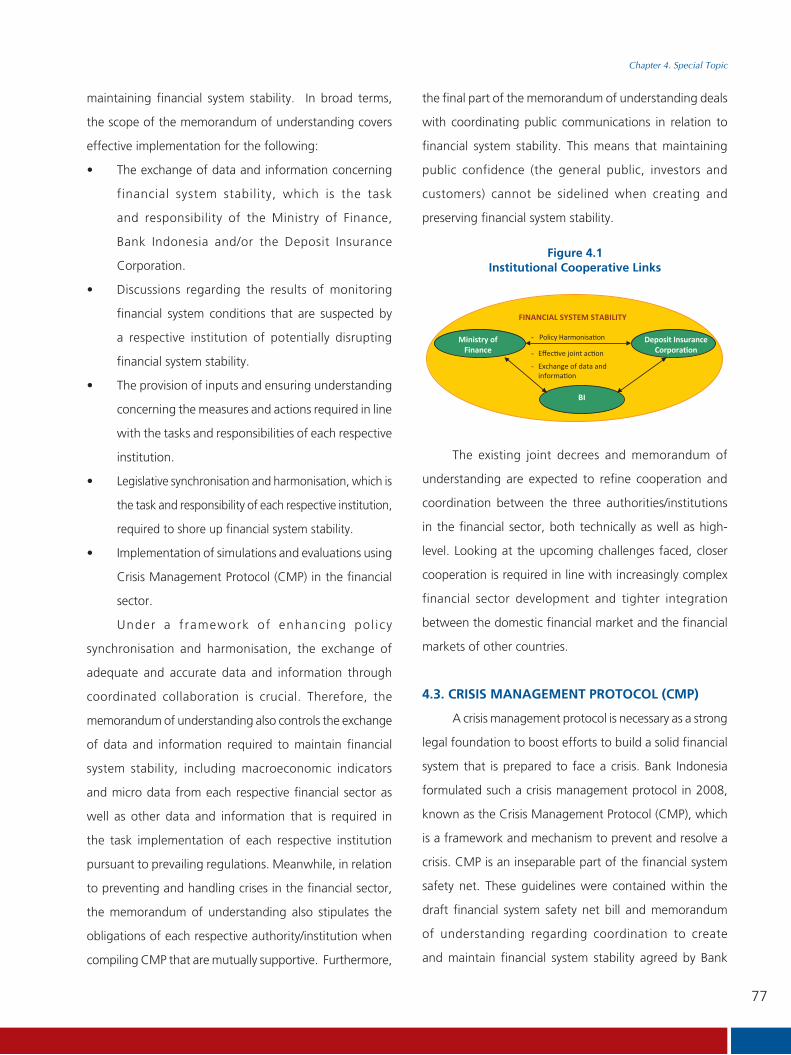

4.1 Institutional Cooperative Links........................ 77

5.1 Flow of Direct Investment............................... 885.2 Growth Projections for several Countries........ 88

2.1.1 LCR by Bank Group........................................ 462.1.2 NSFR by Bank Group...................................... 482.2.1 Undisbursed Loans and Liquid Funds .............. 502.2.2 Share of Undisbursed Loans by Bank Group ... 502.2.3 Share of Undisbursed Loans by Type .............. 502.2.4 Share of Undisbursed Loans by Economic Sector 512.3.1 Factors that Influence Inflation.......................... 522.5.1 Share of main sources of Income to

Operational Income (%) ................................. 562.5.2 Share of Fee Based Income to

Operational Income (%) ................................. 562.5.3 Bank Foreign Currency/Derivative Transactions

(trillions of rupiah).......................................... 57

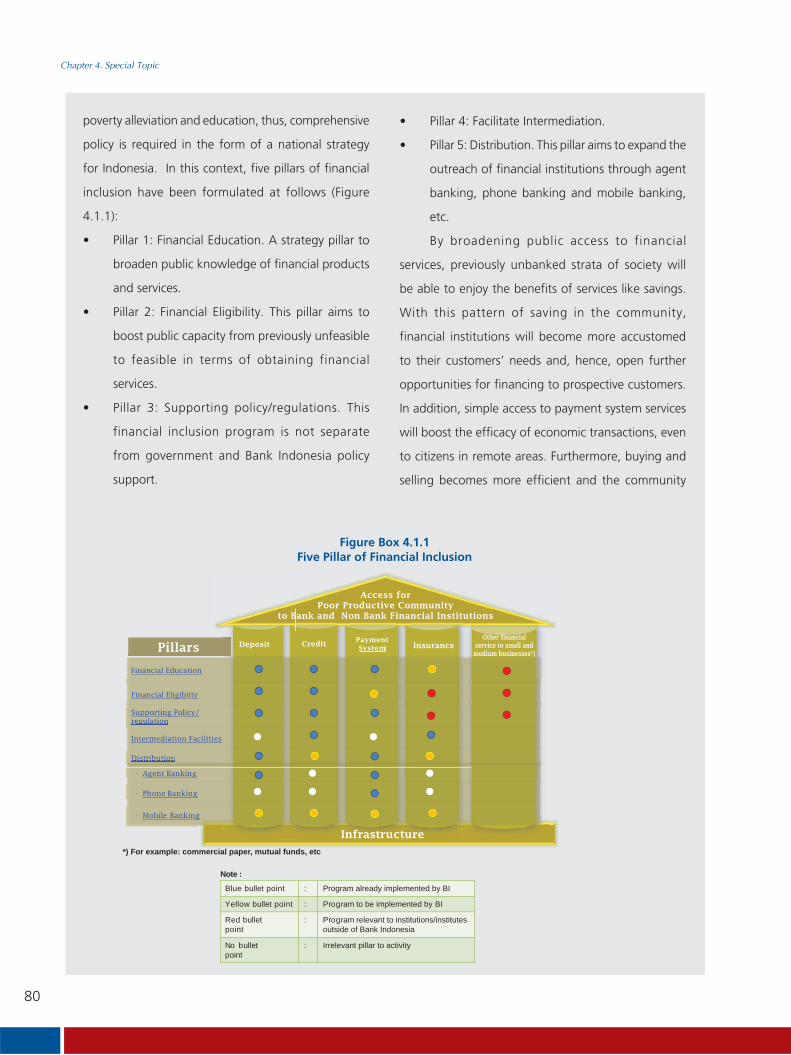

4.1.1 Five Pillars of Financial Inclusion...................... 80

vi

Foreword

A core purpose of Bank Indonesia is to maintain financial system stability in Indonesia. This is accomplished through

macroprudential monitoring and research to comprehensively understand risks in the financial system and factors that

can trigger a crisis. The outcome of surveillance activities, which represents a form of accountability, is published in a

review, the current being the Financial Stability Review (FSR) No. 16. The printing of FSR is considered important because

through this publication the performance and future prospects of financial system stability can be communicated in detail.

In the current edition, Bank Indonesia directly appeals to market participants to take a number of measures to mitigate

potential risk in the financial sector.

An evaluation of financial system conditions revealed that financial system stability was well preserved during the

reporting period. The banking industry and financial market demonstrated impressive performance in the second half of

2010. The total assets of commercial banks swelled to Rp3,008.8 trillion, which is equivalent to 18.73% growth, buoyed by

22.8% (yoy) credit growth. Furthermore, expansion of the intermediation function was accompanied by an improvement

in banks’prudence, as evidenced by a 2.6% decline in the gross NPL ratio (as of December 2010), which took NPL to

its lowest level since the year 2000. In terms of profitability, positive bank performance throughout 2010 was coupled

with improved net profits, achieving Rp57.31 trillion; up 26.74% on the previous year. Congruent with developments

in the banking sector, business activities on the non-bank financial market escalated in the second semester of 2010.

Accordingly, the assets of financing companies expanded by 32% on the back of a 30.74% increase in financing activity.

Meanwhile, the increase in assets of pension funds was inseparable from a 46.13% rally on the Jakarta Composite Index

(JCI), considering that the composition of investment on the capital market accounted for 68.99% of total pension fund

investment.

In general, this increase in business activity by financial institutions coexisted with increasingly resolute financial

sector stability, which was reflected by a decline in the Financial Stability Index (FSI) from 1.87 in June 2010 to 1.75 in

December of the same year. Greater stability in the financial system was linked to improved macroeconomic stability and

a favourable domestic economic outlook as well as an easing of risk in the banking sector, lower bond yield spread and

less volatility on the stock market.

Notwithstanding, vigilance and caution remained necessary when addressing financial sector development. Amid

future macroeconomic conditions that are expected to continue improving, the inundation of foreign capital flows is

expected to persist, thereby, amplifying the already excessive liquidity situation. Excess liquidity must be well managed

in order to avoid the emergence of financial system instability. In addition, the possibility of a sudden reversal of short-

term foreign capital must be continuously monitored, as it would place additional pressures on the rupiah and foreign

exchange reserves.

vii

In closing, we hope that FSR will fulfil its mission as an effective media to communicate to all relevant stakeholders

the results of surveillance activities conducted by Bank Indonesia in the context of financial system stability. Moreover,

as the saying goes, there is no ivory that is not cracked, therefore, we sincerely hope to receive any comments and

suggestions to ensure future editions of FSR live up to all of our expectations.

Jakarta, April 2011

DEPUTY GOVERNOR OF BANK INDONESIA

Muliaman D. Hadad

This page intentionally blank

Overview

1

Overview

2

Overview

This page intentionally blank

Overview

3

1. MACROECONOMY

The economic recovery proceeded rapidly in

emerging and developing economies, including Indonesia,

while, conversely the recovery was languid in more

advanced countries, therefore, emerging markets (EM)

remained an attractive investment destination. Abundant

liquidity on global markets encouraged foreign capital

to flow into emerging markets. In the case of Indonesia,

foreign capital inflows have raised assets prices and drove

rupiah appreciation.

The excess of liquidity increased the supply of short

term deposits which was mainly utilized as portfolio

investments. Nonetheless, excess liquidity necessitated

competent management in order to avoid the emergence

of additional risks that could undermine financial system

stability if utilised to finance imported goods that were

cheaper as a result of rupiah appreciation. Consequently,

the resultant pressures on the rupiah and foreign exchange

reserves would be compounded in the event of capital

outflows.

Potential inflationary pressures stemmed from

spiralling food and commodities prices, as well as

interregional distribution constraints. Under such

circumstances, the financial burden on households and

the corporate sector became more onerous. Furthermore,

the food and commodities price hikes weakened

corporate sector performance. Therefore, high inflation

had the potential to undermine the purchasing power

of households and the corporate sector, which would

ultimately raise credit risk in the financial system.

Bank Indonesia’s message to the banks and financial

market participants is as follows:

globally that could trigger the selling of securities

and, thereby, intensify volatility on the stock and SUN

markets. Such conditions could result from a sudden

and severe foreign capital reversal and would spur

financial system instability.

Bab 1 Overview

Financial system continues to be resilience in Indonesia during the second

semester of 2010. Amid a torrent of foreign capital inflows to Indonesia

and mounting inflationary pressures, the banking industry remained solid

by controlling the risks faced, which consequently tended to ease. Looking

ahead macroeconomic conditions are projected to improve, therefore, the

influx of foreign capital flows is expected to persist and, hence, exacerbate

excess liquidity conditions, which is one of the challenges confronting the

financial system in Indonesia. Additionally, the possibility of a sudden reversal

of short-term foreign capital requires vigilance.

4

Overview

2. INDONESIAN FINANCIAL SYSTEM

2.1. Profitability, Balance Sheets and Capital

2.2. Bank Liquidity and Funding

2.3. Risk transfer betwen Banks, Insurance

companies and Pension funds

5

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

Chapter 1Risk from the Global Environment:Global Imbalances, a Torrent of ForeignCapital Inflows and rising Inflation

6

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

This page intentionally blank

7

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

Chapter 1 Risk from the Global Environment:

Global Imbalances, a Torrent of Foreign Capital

Inflows and rising Inflation

Global imbalances remained a key contributing factor to the deluge of foreign

capital inflows to emerging market countries, including Indonesia, during

semester-II 2010. In addition, improved economic performance in Indonesia,

strong domestic demand as well as a sound and stable banking sector were

also salient determinants of the inrush of foreign capital flows. Nevertheless,

mounting inflationary pressures spurred by spiralling food (volatile foods)

and commodity prices on the international market overshadowed robust

economic performance.

The escalation of inflationary pressures did not have any significant impact on

the purchasing power of the household sector during the reporting period. In

fact, the household sector maintained adequate financial resilience, which was

reflected by the relatively small ratio of total household debt to total assets.

Notwithstanding, if inflationary pressures continue to persist the financial

burden on households will become more onerous and while income is not

experiencing a corresponding increase the level of welfare will decline. Such

conditions ultimately have the potential to undermine household purchasing

power, thereby, exacerbating credit risk in the financial system.

Soaring inflation in the second half of 2010, stemming from rising food prices,

impinged upon corporate sector performance in the third quarter of 2010,

reflected by the weaker financial performance of non-financial public listed

companies on the Indonesian Bourse, which was evidenced by a decline in

ROA and ROE.

8

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

1.1. SOURCES OF VULNERABILITY

1.1.1.The Global Economy and Financial Markets

The global economic recovery endured throughout

the second semester of 2010 unevenly across regions

and with a decreasing intensity. The global recovery

was signalled by an increase in global economic activity.

Manufacturing activities, exports as well as retail and

automotive sales drove economic activity in the US.

Meanwhile, manufacturing activities in Germany and

France shored up the economic recovery in Europe.

A number of risk factors slowed economic growth in

advanced countries, including high unemployment (9.4%

in December 2010) and lower property prices in the US as

well as concerns in Europe that the fiscal crises affecting

a handful of countries could spread.

Based on IMF estimates (Table 1.1), the economies of

advanced countries grew by 3.0% in quarter-IV 2010 (yoy),

much lower than that posted in emerging markets, namely

7.1%. Robust growth in emerging market countries was

attributable to strong domestic consumption in each

respective country, improved external performance in line

with the continuing global economic recovery, and soaring

commodity prices on the international market. Holistically,

global economic growth in 2010 achieved 5%.

Although the global economic landscape was mired

by uncertainty concerning the recovery in established

countries, international financial market conditions

continued to improve during the second semester of 2010

(Figure 1.1). A number of financial markets in advanced

countries, which had experienced pressures when the

crisis peaked in 2008, began to indicate much better

performance due to several factors. The economic recovery

in advanced countries, among others the United States,

United Kingdom and Japan, garnered positive sentiment

on global financial markets and gained global economic

recovery momentum. The US financial system began to

improve and annual economic growth returned to positive

subsequent to the expansionary policy of quantitative

easing1 instituted by the Federal Reserve, consisting

of additional liquidity to the tune of USD600 billion in

November 2010. Moreover, economic growth in Japan

also experienced a significant rebound, in fact posting

stronger growth than pre-crisis levels.

Problems in the financial system emerged in the

Eurozone2 as a follow-through effect from fiscal difficulties

Source: World Economic Outlook Update, January 2011. Data for Indonesia is from BPS-Statistics Indonesiaand the projections for 2010 are calculated by Bank Indonesia

2009(%)

2010(%)

Projection2010 (%)

Table 1.1Breakdown of Global Economic Growth

World Output -0.6 5.0 4.4

Advanced Economies -3.4 3.0 2.5

United States of America -2.6 2.8 2.7

Euro Area -4.1 1.8 1.7

German -4.7 3.6 2.0

France -2.5 1.6 1.8

Italy -5.0 1.0 1.0

Spain -3.7 -0.2 0.6

Japan -6.3 4.3 1.6

United Kingdom -4.9 1.7 2.0

Canada -2.5 2.9 2.3

Others -1.2 5.6 3.8

Newly Industrialized

Asian Economies -0.9 8.2 4.7

European Union -4.1 1.8 1.7

Emerging & Developing

Economies 2.6 7.1 6.5

Developing Asia 7.0 9.3 8.4

China 9.2 10.3 9.5

India 5.7 9.7 8.0

ASEAN-5 1.7 6.7 5.7

Indonesia 4.6 6.1 6.3

Latin America and

Caribbean Islands -1.8 5.9 4.3

Brazil -0.6 7.5 4.5

Mexico -6.1 5.2 4.2

1 Quantitative easing is a non-conventional policy response introduced by the central bank, which injects liquidity into the economy in order to provide economic stimuli amid disruptions stemming from a crisis.

2 EThe Eurozone incorporates those countries in the European Union that have adopted the euro as their common currency and sole legal tender.

9

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

Leading countries in the Eurozone, particularly

Germany, have already demonstrated a significant rebound

in economic growth, however, the periphery countries

continued to attract negative sentiment to the European

financial markets. Issues in other GIIPS countries will

continue to be monitored by the global market, hence,

handling the vulnerabilities exposed in the Eurozone

will determine the success of economic recovery in the

region.

The fiscal difficulties that have beset the Eurozone

are an invaluable lesson for the international community,

especially in terms of crisis resolution. Financial crises

require a quick and accurate resolution. A lack of fiscal

policy discipline in a number of countries resulted in a

difference of opinion in terms of resolving the crisis in the

euro area, which prolonged crisis resolution. Independent

fiscal policy among countries in the Eurozone and the

drawn out resolution of fiscal problems in one country

led to negative sentiment on financial markets in the

euro area and exacerbated the impact of the global crisis

in Europe.

This clearly provides a valuable lesson for ASEAN

member countries that have agreed to officially inaugurate

the ASEAN Economic Community in 2013. Despite strong

economic integration in the euro area, no adequate crisis

resolution mechanism was set in place that could be

executed immediately in order to dampen the crisis before

conditions on the financial markets became more severe.

Accordingly, fiscal problems triggered systemic risk on the

regional financial market. The European Central Bank (ECB)

as lender of last resort in the Eurozone was also unable to

act as the sole source of funds to resolve the fiscal crisis.

Fiscal crises in Greece (loan of £110 billion) and Ireland

(loan of £22.5 billion) were resolved through cooperation

among the European Commission, ECB and International

Monetary Fund (IMF).

3 GIIPS: Greece, Ireland, Italy, Portugal and Spain.

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

Jan

- 07

Apr -

07

Jul -

07

Oct

- 07

Jan

- 08

Apr -

08

Jul -

08

Oct

- 08

Jan

- 09

Apr -

09

Jul -

09

Oct

- 09

Jan

- 10

Apr -

10

Jul -

10

Oct

- 10

Hongkong (left scale) Dow Jones (left scale)Singapore (right scale) Inggris (right scale)

in GIIPS3 countries. Fiscal problems that peaked in Ireland

broadened CDS spread in GIIPS countries, which signaled

the existence of fiscal troubles, including in countries where

the fiscal problems were not as pronounced (Figure 1.2

and 1.3).

0

200

400

600

800

000

200

Jan

- 09

Mar

- 09

May

- 09

Jul -

09

Sep

- 09

Nov -

09

Jan

- 10

Mar

- 10

May

- 10

Jul -

10

Sep

- 10

Nov -

10

Greece

Ireland

Italy

Portugal

Spain

Germany

Source: Bloomberg (CDS USD Senior 5Y)

Source: Bloomberg (CDS USD Senior 5Y)

Source: Bloomberg

Figure 1.3CDS in leading Eurozone countries and Switzerland

Figure 1.1Global Stock Market Indices (2000=100)

Figure 1.2CDS in GIIPS countries and Germany

0

50

100

150

200

250

300

350

400

Germany

Perancis

Italy

Spain

Netherlands

Belgium

Austria

Switzerland

Jan

- 09

Mar

- 09

May

- 09

Jul -

09

Sep

- 09

Nov

- 09

Jan

- 10

Mar

- 10

May

- 10

Jul -

10

Sep

- 10

Nov

- 10

10

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

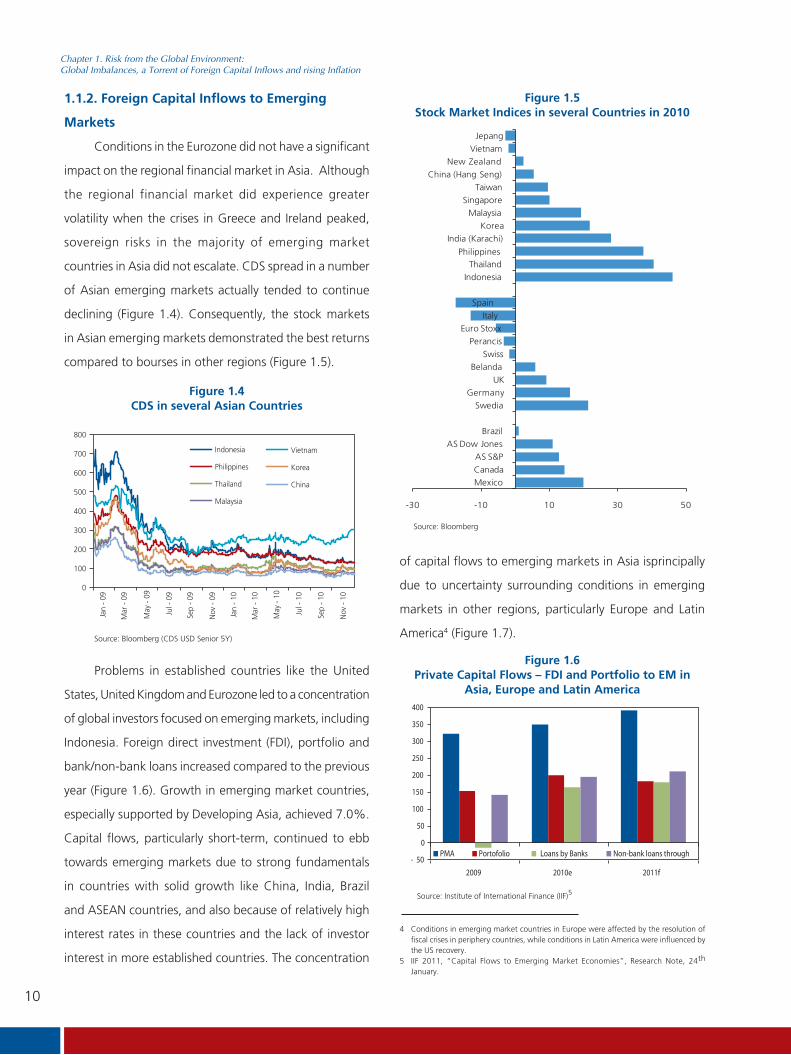

1.1.2. Foreign Capital Inflows to Emerging

Markets

Conditions in the Eurozone did not have a significant

impact on the regional financial market in Asia. Although

the regional financial market did experience greater

volatility when the crises in Greece and Ireland peaked,

sovereign risks in the majority of emerging market

countries in Asia did not escalate. CDS spread in a number

of Asian emerging markets actually tended to continue

declining (Figure 1.4). Consequently, the stock markets

in Asian emerging markets demonstrated the best returns

compared to bourses in other regions (Figure 1.5).

4 Conditions in emerging market countries in Europe were affected by the resolution of fiscal crises in periphery countries, while conditions in Latin America were influenced by the US recovery.

5 IIF 2011, “Capital Flows to Emerging Market Economies”, Research Note, 24th

January.

Figure 1.4CDS in several Asian Countries

0

100

200

300

400

500

600

700

800

Indonesia

Philippines

Thailand

Malaysia

Vietnam

Korea

China

Jan

- 09

Mar

- 09

May

- 09

Jul -

09

Sep

- 09

Nov

- 09

Jan

- 10

Mar

- 10

May

- 10

Jul -

10

Sep

- 10

Nov

- 10

Source: Bloomberg (CDS USD Senior 5Y)

Figure 1.5Stock Market Indices in several Countries in 2010

Source: Bloomberg

-30 -10 10 30 50

Mexico

Canada

AS S&P

AS Dow Jones

Brazil

Swedia

Germany

UK

Belanda

Swiss

Perancis

Euro Stoxx

Italy

Spain

Indonesia

Thailand

India (Karachi)

Philippines

Korea

Malaysia

Singapore

Taiwan

China (Hang Seng)

New Zealand

Vietnam

Jepang

of capital flows to emerging markets in Asia isprincipally

due to uncertainty surrounding conditions in emerging

markets in other regions, particularly Europe and Latin

America4 (Figure 1.7).

Figure 1.6Private Capital Flows – FDI and Portfolio to EM in

Asia, Europe and Latin America

Source: Institute of International Finance (IIF)5

- 50

0

50

100

150

200

250

300

350

400

2009 2010e 2011f

PMA Portofolio Loans by Banks Non-bank loans through-

Problems in established countries like the United

States, United Kingdom and Eurozone led to a concentration

of global investors focused on emerging markets, including

Indonesia. Foreign direct investment (FDI), portfolio and

bank/non-bank loans increased compared to the previous

year (Figure 1.6). Growth in emerging market countries,

especially supported by Developing Asia, achieved 7.0%.

Capital flows, particularly short-term, continued to ebb

towards emerging markets due to strong fundamentals

in countries with solid growth like China, India, Brazil

and ASEAN countries, and also because of relatively high

interest rates in these countries and the lack of investor

interest in more established countries. The concentration

11

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

Note: According to IIF emerging markets are grouped

into the following brackets: 1) Emerging Europe: Bulgaria,

Czech Republic, Hungary, Poland, Rumania, Russia, Turkey

and Ukraine; 2) Emerging Asia: China, India, Indonesia,

Malaysia, the Philippines, Korea and Thailand; 3) Emerging

Latin America: Argentina, Brazil, Chili, Colombia, Ecuador,

México, Peru and Venezuela; and 4) Emerging Africa/

Middle East: Egypt, Lebanon, Morocco, Nigeria, Saudi

Arabia, South Africa andUnited Arab Emirates.

The liquidity injected into the US financial market

as a part of quantitative easing by the Federal Reserve

also increased potential capital flows to emerging market

countries. From a macroprudential standpoint, the deluge

of foreign capital flows could have created an asset price

bubble and the risk of sudden reversal in emerging market

countries. Furthermore, capital inflows led to currency

appreciation in emerging market countries, which on one

hand benefitted the advanced countries to provide stimuli

for their exports. However, on the other hand a number

of emerging market countries depended on income from

their own exports that became less competitive on the

international market6. Therefore, several emerging markets

began to apply policy to reduce the unrelenting deluge

of capital inflows. Brazil, for instance, levied a tax on

capital flowing into the country. Additionally, a number of

countries like Brazil, México, Korea, Taiwan, South Africa,

Thailand, Indonesia and China used active intervention on

the forex markets to curb exchange rate appreciation.

1.1.3. Soaring International Commodity Prices

Rising commodity prices compounded the problems

experienced by the global economy. The global commodity

price index posted a significant spike (Figure 1.8). The price

of crude oil on the West Texas Intermediate(WTI) spot

market reached USD90 per barrel in December 2010. A

similar trend was also noted for commodities like gold,

copper and rubber (Figure 1.9). Referring to the UBS CMCI

composite price index, all sectors experienced price hikes,

especially the agricultural sector (Figure 1.10).

Figure 1.7Private Capital Flows to Emerging Markets

0

50

100

150

200

250

300

2009 2010e 2011f

Asia

Eropa

Amerika Latin

Source: Institute of International Finance (IIF)

6 A currency war began to emerge in October 2010. Quantitative easing, as implemented by established countries to overcome the impacts of the global crisis in 2007-2008, was one way to devalue their domestic currency.

Figure 1.8Global Price Indices

Figure 1.9Price Indices of several International Commodities

Source: Bloomberg

Source: Bloomberg

0

200

400

600

800

1000

1200

1400

1600

1800

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

JPMorganAggregatePrice Index

S&P GSCI Index

UBS CMCI Price Index

0

100

200

300

400

500

600

Jan

- 07

May

- 07

Sep

- 07

Jan

- 08

May

- 08

Sep

- 08

Jan

- 09

May

- 09

Sep

- 09

Jan

- 10

May

- 10

Sep

- 10

Oil Copper Gold Rubber

12

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

Despite assisting economic recoveries in commodity-

producing countries, soaring commodity prices also raised

global inflation. Central banks in several countries were

confronted by a dilemma of whether to raise interest rates

in order to control inflation or let interest rates remain low

to buttress the economic recovery. Raising interest rates

in emerging market countries would broaden the spread

with advanced countries, hence encouraging a further

inundation of capital flows.

1.2. STRENGTHENING RISK IN INDONESIA

1.2.1. Impact on Indonesia’s Macroeconomy

The ongoing global economic recovery coupled with

solid public purchasing power bolstered domestic economic

performance. Similar to the case in other emerging market

countries, economic performance in Indonesia during

semester-II 2010 showed adequate resilience, which in fact

tended to strengthen. Economic growth in Indonesia has

been maintained at a relatively robust level since the crisis

in 2008 up to the fourth quarter of 2010. Consequently,

the economy of Indonesia expanded by 6.14% in 2010,

which far exceeds growth posted in 2009 at 4.51%.

Domestic export performance, particularly non-oil/

gas exports based on natural resources, was buoyed by

increased global economic activityin line with high prices on

international markets. At the end of the second semester

of 2010 the value of non-oil/gas exports from Indonesia

totalled USD13.6 million; up 29.24% on the previous year.

In comparison, the value of Indonesian imports at the end

of semester-II 2010 was USD10.8 million, which represents

just 18.40% growth over the position at the end of

semester-I 2010. The higher value of exports compared to

imports led to a current account surplus of USD1.3 million

in December 2010 (end of quarter-IV 2010), which was

larger than that recorded in June 2010 (end of quarter-II

2010) of USD1.2 million (Figure 1.11 and 1.12).

Source: SEKI

Sourcer: SEKI

Sourcer: Bloomberg

Figure 1.10UBS CMCI Composite Price Index by Sector

0

500

1000

1500

2000

2500

Jan

- 04

Jul -

04

Jan

- 05

Jul -

05

Jan

- 06

Jul -

06

Jan

- 07

Jul -

07

Jan

- 08

Jul -

08

Jan

- 09

Jul -

09

Jan

- 10

Jul -

10

Jan

- 11

Agriculture Energy IndustrialPrecious Metal Livestock

Figure 1.11Indonesian Development of Non-Oil Export Import

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

Thousand USD

Non Oil Export Non Oil Import

Jan

- 07

Apr -

07

Jul -

07

Oct

- 07

Jan

- 08

Apr -

08

Jul -

08

Oct

- 08

Jan

- 09

Apr -

09

Jul -

09

Oct

- 09

Jan

- 10

Apr -

10

Jul -

10

Oct

- 10

Figure 1.12Indonesia Development of Total Exports and Imports

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

Thousand USD

Total Exports Total Imports

Jan

- 07

Apr -

07

Jul -

07

Oct

- 07

Jan

- 08

Apr -

08

Jul -

08

Oct

- 08

Jan

- 09

Apr -

09

Jul -

09

Oct

- 09

Jan

- 10

Apr -

10

Jul -

10

Oct

- 10

13

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

Impressive export/import performance in Indonesia

helped solidify the performance of the balance of payments

(BOP). The balance of payments registered a surplus of

USD11.3 billion at the end of semester-II 2010, which

was an increase of 109% compared to the position at

the end of the first semester totalling USD5.4 billion. In

congruence, foreign exchange reserves at the end of

semester-II 2010 increased to USD96.2 billion; equivalent

to seven months of imports and servicing foreign debt.

In line with the favourable BOP performance, the

rupiah exchange rate strengthened with low volatility.

Compared to the end of semester-I 2010 the rupiah

appreciated by 78 points, or 0.86%, by the end of

semester-II 2010 to a level of Rp8,996 per USD. The value

of the rupiah peaked in the fourth quarter at Rp8,982

(Figure 1.13). Meanwhile, average rupiah volatility against

the USD was 0.15% during the second semester of 2010,

which was far below the average volatility recorded in

semester-I 2010 at 0.31% (Figure 1.14).

The amount of investment in Indonesia in the fourth

quarter of 2010 was USD9.9 billion, which represents

a significant leap over the previous year at just USD2.5

billion. As a whole, the amount of money flowing into

Indonesia during 2010 was USD26.2 billion, up 433.7%

compared to 2009 at just USD4.9 billion. From the total

amount of investment flowing into Indonesia throughout

2010 the majority (58%) was in the form of portfolio

investment, followed by foreign direct investment (38%)

and other investment (Figure 1.15).

Source: Bloomberg (processed data)

Figure 1.13Rupiah Exchange Rate

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

2007 2008 2009 2010

Monthly average

Average quarterly

Average semester

Figure 1.14Rupiah Exchange Rate Volatility

-2

1,5

-1

0,5

0

0,5

1

1,5

2

1 12 23 34 45 56 67 78 89 100

111

122

133

144

155

166

177

188

199

210

221

232

243

254

Lower limit Upper limit Actual

Period 253 days

Source: Bloomberg (processed data)

Figure 1.15Composition of Direct and Portfolio Investment to

Indonesia

61

4541

75

32

4539

5559

25

68

55

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010

%Direct investmentInvestment Portofolio

Source: Directorate of Monetary and Economic Statistics, Bank Indonesia

14

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

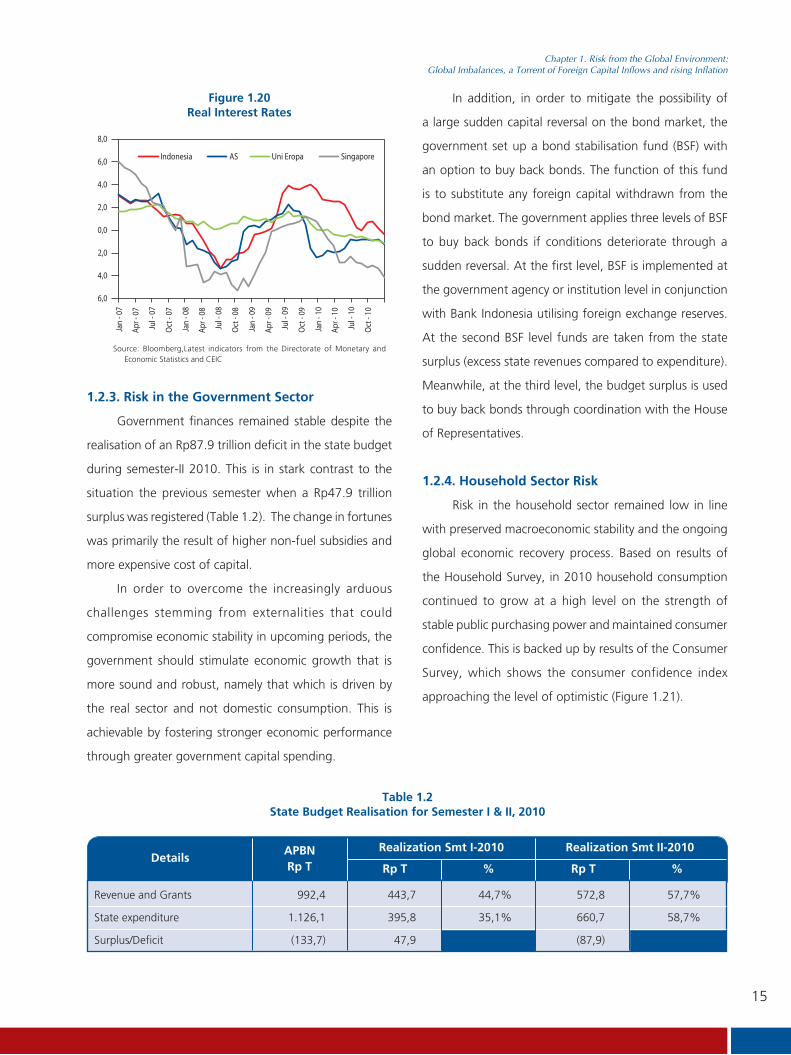

The upward inflation trend not only affected

Indonesia but also nearly all countries, including established

and emerging market countries alike (Figure 1.18 and

1.19). Although the level of inflation was highest in

Indonesiacompared to other countries in ASEAN+5,

the investment climate in Indonesia remained attractive

considering the relatively high interest rates compared

to other ASEAN countries and advanced countries. As a

result, despite the gap narrowing between the interest rate

and inflation rate, in real terms interest rates in Indonesia

exceeded real interest rates in several other ASEAN

countries as well as in the United State and European

Union (Figure 1.20).

1.2.2. Mounting Inflationary Pressures

Inflation tended to escalate in semester-II 2010,

with headline inflation reaching 6.96% (yoy)at the end

of semester-II 2010 (Figure 1.16), in excess of its target

for 2010 at 5%±1%. The rise in headline inflation was

driven by non-fundamental factors, especially inflation of

volatile foods, which was 5.79% (ytd) in June 2010 and

peaked at 15.64% in December 2010 (ytd) (Figure 1.17).

This was primarily attributable to a lack of supply compared

to demand for staple foods. Supply was constrained by

harvest disruptions and damaged crops due to seasonal

anomalies, extreme weather and natural disasters. In

addition, high rainfall and a lack of infrastructure increased

the cost of distribution and, hence, inflated prices.

Figure 1.16Inflation in Indonesia (Core and Headline)

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

Core Inflation(yoy)

Inflation IHK (yoy)

Jan

- 07

Apr -

07

Jul -

07

Oct

- 07

Jan

- 08

Apr -

08

Jul -

08

Oct

- 08

Jan

- 09

Apr -

09

Jul -

09

Oct

- 09

Jan

- 10

Apr -

10

Jul -

10

Oct

- 10

Figure 1.17Price Indices of Foodstuffs and Oil in Indonesia,

2006 = 100

0

50

100

150

200

250

300

Dec -

200

6

Mar

- 07

Jun

- 07

Sep

- 07

Dec -

200

7

Mar

- 08

Jun

- 08

Sep

- 08

Dec -

200

8

Mar

- 09

Jun

- 09

Sep

- 09

Dec -

200

9

Mar

- 10

Jun

- 10

Sep

- 10

Dec -

201

0

Rice Cayenne

Petroleum Cooking Oil

Figure 1.18Inflation in several Advanced Countries

(5)

(2)

1

4

7

Jan-

07

Apr-0

7

Jul-0

7

Oct

-07

Jan-

08

Apr-0

8

Jul-0

8

Oct

-08

Jan-

09

Apr-0

9

Jul-0

9

Oct

-09

Jan-

10

Apr-1

0

Jul-1

0

Oct

-10

y.o.y %

Japan US Uni Eropa Singapore

Figure 1.19Inflation in several ASEAN Countries

(6)

(2)

2

6

10

y.o.y %

Philippines ThailandMalaysia Indonesia

Jan

- 07

Apr -

07

Jul -

07

Oct

- 07

Jan

- 08

Apr -

08

Jul -

08

Oct

- 08

Jan

- 09

Apr -

09

Jul -

09

Oct

- 09

Jan

- 10

Apr -

10

Jul -

10

Oct

- 10

Source: Directorate of Monetary and Economic Statistics, Bank Indonesia

Source: Latest indicators from the Directorate of Monetary and Economic Statistics

Source: CEIC

Source: CEIC

15

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

1.2.3. Risk in the Government Sector

Government finances remained stable despite the

realisation of an Rp87.9 trillion deficit in the state budget

during semester-II 2010. This is in stark contrast to the

situation the previous semester when a Rp47.9 trillion

surplus was registered (Table 1.2). The change in fortunes

was primarily the result of higher non-fuel subsidies and

more expensive cost of capital.

In order to overcome the increasingly arduous

challenges stemming from externalities that could

compromise economic stability in upcoming periods, the

government should stimulate economic growth that is

more sound and robust, namely that which is driven by

the real sector and not domestic consumption. This is

achievable by fostering stronger economic performance

through greater government capital spending.

Figure 1.20Real Interest Rates

6,0

4,0

2,0

0,0

2,0

4,0

6,0

8,0

Indonesia AS Uni Eropa Singapore

Jan

- 07

Apr -

07

Jul -

07

Oct

- 07

Jan

- 08

Apr -

08

Jul -

08

Oct

- 08

Jan

- 09

Apr -

09

Jul -

09

Oct

- 09

Jan

- 10

Apr -

10

Jul -

10

Oct

- 10

In addition, in order to mitigate the possibility of

a large sudden capital reversal on the bond market, the

government set up a bond stabilisation fund (BSF) with

an option to buy back bonds. The function of this fund

is to substitute any foreign capital withdrawn from the

bond market. The government applies three levels of BSF

to buy back bonds if conditions deteriorate through a

sudden reversal. At the first level, BSF is implemented at

the government agency or institution level in conjunction

with Bank Indonesia utilising foreign exchange reserves.

At the second BSF level funds are taken from the state

surplus (excess state revenues compared to expenditure).

Meanwhile, at the third level, the budget surplus is used

to buy back bonds through coordination with the House

of Representatives.

1.2.4. Household Sector Risk

Risk in the household sector remained low in line

with preserved macroeconomic stability and the ongoing

global economic recovery process. Based on results of

the Household Survey, in 2010 household consumption

continued to grow at a high level on the strength of

stable public purchasing power and maintained consumer

confidence. This is backed up by results of the Consumer

Survey, which shows the consumer confidence index

approaching the level of optimistic (Figure 1.21).

Source: Bloomberg,Latest indicators from the Directorate of Monetary and Economic Statistics and CEIC

APBNRp T

DetailsRp T

Realization Smt I-2010 Realization Smt II-2010

Rp T% %

Revenue and Grants 992,4 443,7 44,7% 572,8 57,7%

State expenditure 1.126,1 395,8 35,1% 660,7 58,7%

Surplus/Deficit (133,7) 47,9 (87,9)

Table 1.2State Budget Realisation for Semester I & II, 2010

16

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

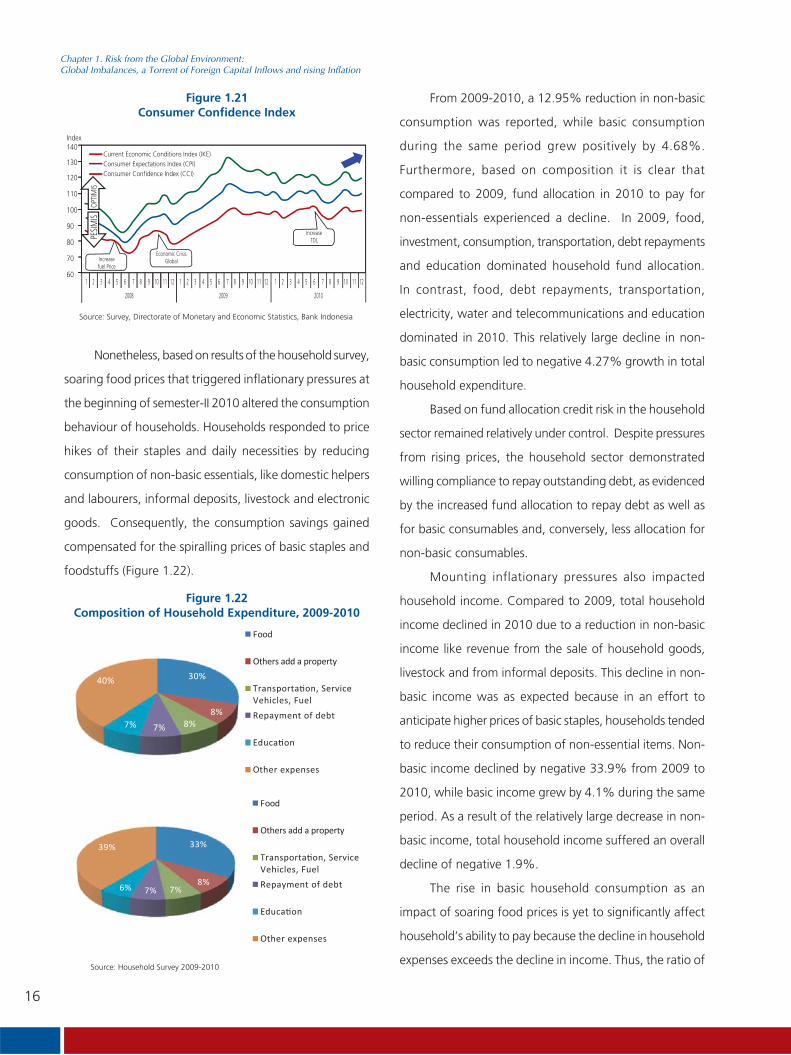

Nonetheless, based on results of the household survey,

soaring food prices that triggered inflationary pressures at

the beginning of semester-II 2010 altered the consumption

behaviour of households. Households responded to price

hikes of their staples and daily necessities by reducing

consumption of non-basic essentials, like domestic helpers

and labourers, informal deposits, livestock and electronic

goods. Consequently, the consumption savings gained

compensated for the spiralling prices of basic staples and

foodstuffs (Figure 1.22).

From 2009-2010, a 12.95% reduction in non-basic

consumption was reported, while basic consumption

during the same period grew positively by 4.68%.

Furthermore, based on composition it is clear that

compared to 2009, fund allocation in 2010 to pay for

non-essentials experienced a decline. In 2009, food,

investment, consumption, transportation, debt repayments

and education dominated household fund allocation.

In contrast, food, debt repayments, transportation,

electricity, water and telecommunications and education

dominated in 2010. This relatively large decline in non-

basic consumption led to negative 4.27% growth in total

household expenditure.

Based on fund allocation credit risk in the household

sector remained relatively under control. Despite pressures

from rising prices, the household sector demonstrated

willing compliance to repay outstanding debt, as evidenced

by the increased fund allocation to repay debt as well as

for basic consumables and, conversely, less allocation for

non-basic consumables.

Mounting inflationary pressures also impacted

household income. Compared to 2009, total household

income declined in 2010 due to a reduction in non-basic

income like revenue from the sale of household goods,

livestock and from informal deposits. This decline in non-

basic income was as expected because in an effort to

anticipate higher prices of basic staples, households tended

to reduce their consumption of non-essential items. Non-

basic income declined by negative 33.9% from 2009 to

2010, while basic income grew by 4.1% during the same

period. As a result of the relatively large decrease in non-

basic income, total household income suffered an overall

decline of negative 1.9%.

The rise in basic household consumption as an

impact of soaring food prices is yet to significantly affect

household’s ability to pay because the decline in household

expenses exceeds the decline in income. Thus, the ratio of

Figure 1.21Consumer Confidence Index

Current Economic Conditions Index (IKE)Consumer Expectations Index (CPI)Consumer Confidence Index (CCI)

Index140

130

120

110

100

90

80

70

60 1 2 3 4 5 6 7 8 9 10 11 12

2008

1 2 3 4 5 6 7 8 9 10 11 12

2009

1 2 3 4 5 6 7 8 9 10 11 12

2010

Increasefuel Price

Economic CrisisGlobal

IncreaseTDL

Figure 1.22Composition of Household Expenditure, 2009-2010

30%

8%8%7%7%

40%

Food

Others add a property

Repayment of debt

E

Other expenses

Food

Others add a property

Repayment of debt

E

Other expenses

33%

8%7%7%6%

39%

Source: Household Survey 2009-2010

Source: Survey, Directorate of Monetary and Economic Statistics, Bank Indonesia

17

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

household expenses to household income also experienced

a slight decline. Based on survey data, the ratio of total

household expenses to total household income was

97.75% in 2010, which is down on the previous year at

100.64% (Table 1.3). A score of less than 100% indicates

that household income is sufficient to cover household

expenses.

1.2.5. Corporate Sector Risk

Escalating inflation potentially undermined the

performance of firms listed on the Indonesian Stock

Exchange (ISE), which limited expansionary activity

and drove up product prices, especially for companies

operating in the non-food sector and even more so for

those in the restaurants, hotels and tourism subsectors.

This potentially eroded corporate revenue, exacerbated

further by fluctuations in the exchange rate during the

reporting semester. Consequently, the performance of

non-financial companies listed on the Indonesian Bourse

The difference between income and expenses in

2010 could be utilised as household savings in order to

cover potential price hikes in upcoming periods. Consumer

survey results have shown that respondents expect the

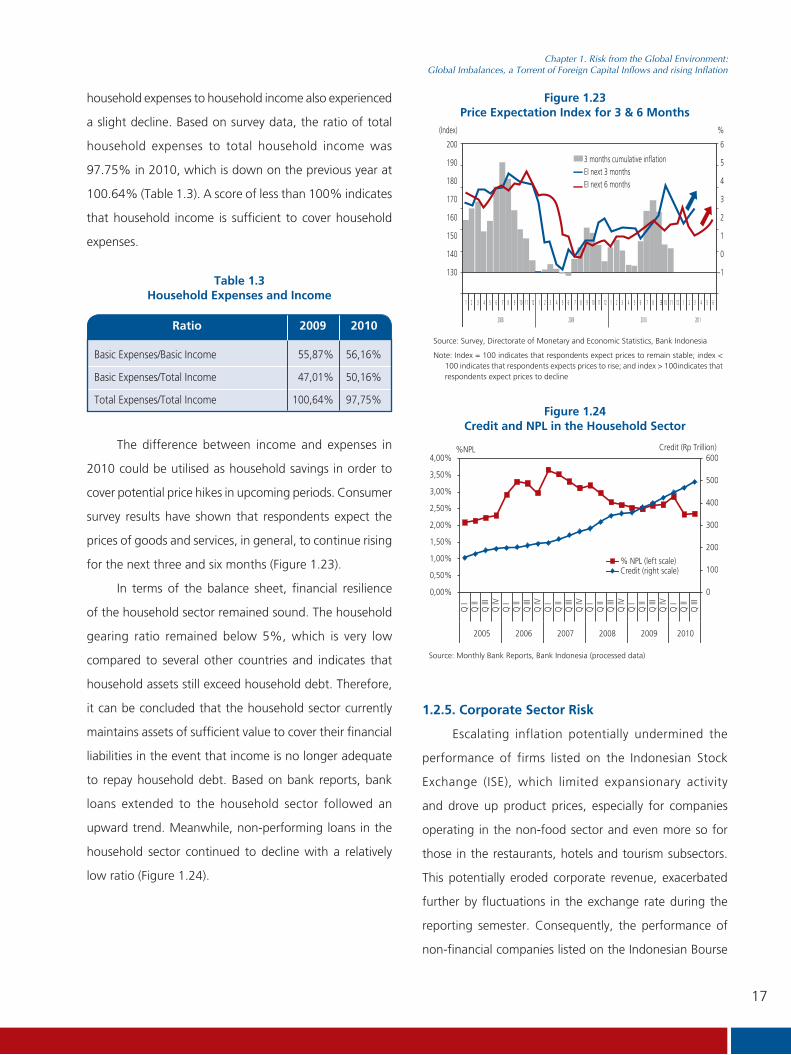

prices of goods and services, in general, to continue rising

for the next three and six months (Figure 1.23).

In terms of the balance sheet, financial resilience

of the household sector remained sound. The household

gearing ratio remained below 5%, which is very low

compared to several other countries and indicates that

household assets still exceed household debt. Therefore,

it can be concluded that the household sector currently

maintains assets of sufficient value to cover their financial

liabilities in the event that income is no longer adequate

to repay household debt. Based on bank reports, bank

loans extended to the household sector followed an

upward trend. Meanwhile, non-performing loans in the

household sector continued to decline with a relatively

low ratio (Figure 1.24).

Ratio 2009 2010

Basic Expenses/Basic Income 55,87% 56,16%

Basic Expenses/Total Income 47,01% 50,16%

Total Expenses/Total Income 100,64% 97,75%

Table 1.3Household Expenses and Income

Figure 1.23Price Expectation Index for 3 & 6 Months

1 2

2008 2009 2010 2011

3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 10 11 12 1 2 3 4 5 63

(Index)

200

190

180

170

160

150

140

130

%

6

5

4

3

2

1

0

-1

3 months cumulative inflationEI next 3 months EI next 6 months

Note: Index = 100 indicates that respondents expect prices to remain stable; index < 100 indicates that respondents expects prices to rise; and index > 100indicates that respondents expect prices to decline

Source: Survey, Directorate of Monetary and Economic Statistics, Bank Indonesia

0

100

200

300

400

500

600

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%Q

IQ

IIQ

III

Q IV

Q I

Q II

Q II

IQ

IVQ

IQ

IIQ

III

Q IV

Q I

Q II

Q II

IQ

IVQ

IQ

IIQ

III

Q IV

Q I

Q II

Q II

I

2005 2006 2007 2008 2009 2010

Credit (Rp Trillion)%NPL

% NPL (left scale)Credit (right scale)

Figure 1.24Credit and NPL in the Household Sector

Source: Monthly Bank Reports, Bank Indonesia (processed data)

18

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

deteriorated, as reflected by declining ROA and ROE ratios

in the third quarter of 2010 compared to the same period

in the previous year. In comparison to quarter-III 2009,

ROAdeclined slightly by 2.59% to 2.15% in quarter-III

2010. Meanwhile, ROE dropped from 5.73% in quarter-III

2009 to 4.36% in QIII 2010 (Figure 1.25).

In terms of financing, the corporate sector preferred

to rely on its own capital (equity) and tended to shy away

from borrowed capital from banks or from the issuance

of other bonds and securities. This is evidenced by the

declining debt to equity ratio (DER) from 1.19 (quarter-III

2009) to 1.03 (QIII 2010) and the drop in total liabilities to

total assets (TL/TA) in the third quarter of 2010 compared

to the previous year (Figure 1.26).

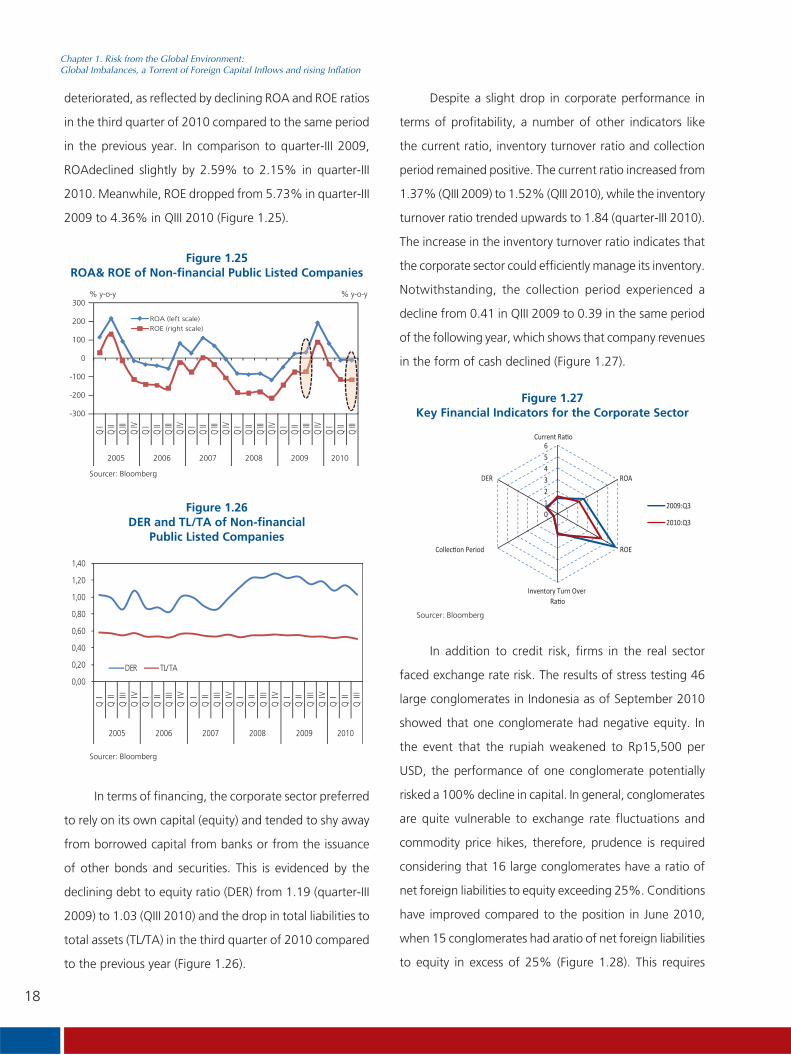

Despite a slight drop in corporate performance in

terms of profitability, a number of other indicators like

the current ratio, inventory turnover ratio and collection

period remained positive. The current ratio increased from

1.37% (QIII 2009) to 1.52% (QIII 2010), while the inventory

turnover ratio trended upwards to 1.84 (quarter-III 2010).

The increase in the inventory turnover ratio indicates that

the corporate sector could efficiently manage its inventory.

Notwithstanding, the collection period experienced a

decline from 0.41 in QIII 2009 to 0.39 in the same period

of the following year, which shows that company revenues

in the form of cash declined (Figure 1.27).

Figure 1.25ROA& ROE of Non-financial Public Listed Companies

Figure 1.26DER and TL/TA of Non-financial

Public Listed Companies

-300

-200

-100

0

100

200

300

Q I

Q II

Q III

Q IV

Q I

Q II

Q III

Q IV

Q I

Q II

Q III

Q IV

Q I

Q II

Q III

Q IV

Q I

Q II

Q III

Q IV

Q I

Q II

Q III

2005 2006 2007 2008 2009 2010

% y-o-y % y-o-y

ROA (left scale)

ROE (right scale)

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

QI

QII

QIII

QIV

QI

QII

QIII

QIV

QI

QII

QIII

QIV

QI

QII

QIII

QIV

QI

QII

QIII

QIV

QI

QII

QIII

2005 2006 2007 2008 2009 2010

DER TL/TA

Figure 1.27Key Financial Indicators for the Corporate Sector

0123456

ROA

ROE

DER

2009:Q3

2010:Q3

In addition to credit risk, firms in the real sector

faced exchange rate risk. The results of stress testing 46

large conglomerates in Indonesia as of September 2010

showed that one conglomerate had negative equity. In

the event that the rupiah weakened to Rp15,500 per

USD, the performance of one conglomerate potentially

risked a 100% decline in capital. In general, conglomerates

are quite vulnerable to exchange rate fluctuations and

commodity price hikes, therefore, prudence is required

considering that 16 large conglomerates have a ratio of

net foreign liabilities to equity exceeding 25%. Conditions

have improved compared to the position in June 2010,

when 15 conglomerates had aratio of net foreign liabilities

to equity in excess of 25% (Figure 1.28). This requires

Sourcer: Bloomberg

Sourcer: Bloomberg

Sourcer: Bloomberg

19

Chapter 1. Risk from the Global Environment:Global Imbalances, a Torrent of Foreign Capital Inflows and rising Inflation

anticipatory measures by conglomerates to mitigate the

risks (Table 1.4).

Figure 1.28Ratio of Net Foreign Liabilities to Equity

(200)

(150)

(100)

(50)

0

50

100

150

200

R P S AK T AD A O AN N AI AC Y V M I AF Q AJ AS U W K

%

Ratio of net liabilitiescurrency against the equity> 25%

Source: Indonesian Stock Exchange (processed data)

Percentage ofequity decrease

IDR / USD

10.5009.500 11.00010.000 11.500 12.000 12.500 13.000 13.500 14.000 14.500 15.000 15.500 16.000

10% 3 5 10 10 10 8 6 6 6 6 4 4 420% 1 2 2 2 5 9 8 5 4 2 3 330% 1 2 2 1 2 5 4 8 5 540% 1 2 1 2 2 5 350% 1 1 1 2 1 260% 1 1 2 170% 1 1 280% 1 90% 1 1100% 1 1

Number of corporateswith impacted equity 0 3 6 13 13 15 16 19 19 19 19 19 20 20

Table 1.4Effect of Rupiah Depreciation on Conglomerate Equity

Source: Indonesian Stock Exchange (processed data)

This page intentionally blank

21

Chapter 2. Financial System Resilience

Chapter 2Financial System Resilience

22

Chapter 2. Financial System Resilience

This page intentionally blank

23

Chapter 2. Financial System Resilience

Chapter 2 Financial System Resilience

Favourable economic conditions during the second semester of 2010

contributed to the preservation of financial system stability in Indonesia. Amid

an influx of foreign capital flows the banks performed amicably, coupled with

solid credit growth. Similar conditions were reported on the stock and SUN

markets, while a steady interest rate was underpinned by financing through

the capital market.

2.1. FINANCIAL SYSTEM STRUCTURE AND

RESILIENCE

The structure of the Indonesian financial system did

not experience any dramatic changes during the reporting

period. Commercial banks and rural banks continued to

dominate banking industry assets, accounting for 82.9% of

total assets in the financial sector (Figure 2.1). Meanwhile,

the total assets of the insurance and securities industry

experienced a comparatively smaller increase and, as such,

the corresponding share decreased slightly compared to

other industries like pension funds, finance companies

and pawnbrokers.The total assets of commercial banks grew by

Rp474.4 trillion (18.73%) to reach Rp3,008.8 trillion by

December 2010 on the back of 22.8% (yoy) credit growth.

Business activity on the non-bank financial market also

performed impressively during semester-II 2010. The

assets of finance companies expanded by 32% buoyed

by 30.74% growth in financing activity. Concurrently, the

increase in the assets of pension funds was linked to the

46.13% gain in the Jakarta Composite (JSX) considering

that the composition of investment on the capital market

is dominated (68.99%) by pension funds.

Greater business activity by financial institutions

was accompanied by improved financial sector stability.

Institutions Numbers

Table 2.1Number of Financial Institutions

Commercial Bank 122

Rural Bank 1,706

Finance Company 191

Insurance Company 142

Pawnbroker 1

Securities Company 119

Pension Funds 272

1.2%6.2%

5.8%0.5% 1.1% 3.3%

Banks

Rural Banks

Financing Company

Insurance Company

Pawnshop

Pension fund

81.7%

Source: various sources (processed data)

Figure 2.1Asset Compositions of Financial Institutions

24

Chapter 2. Financial System Resilience

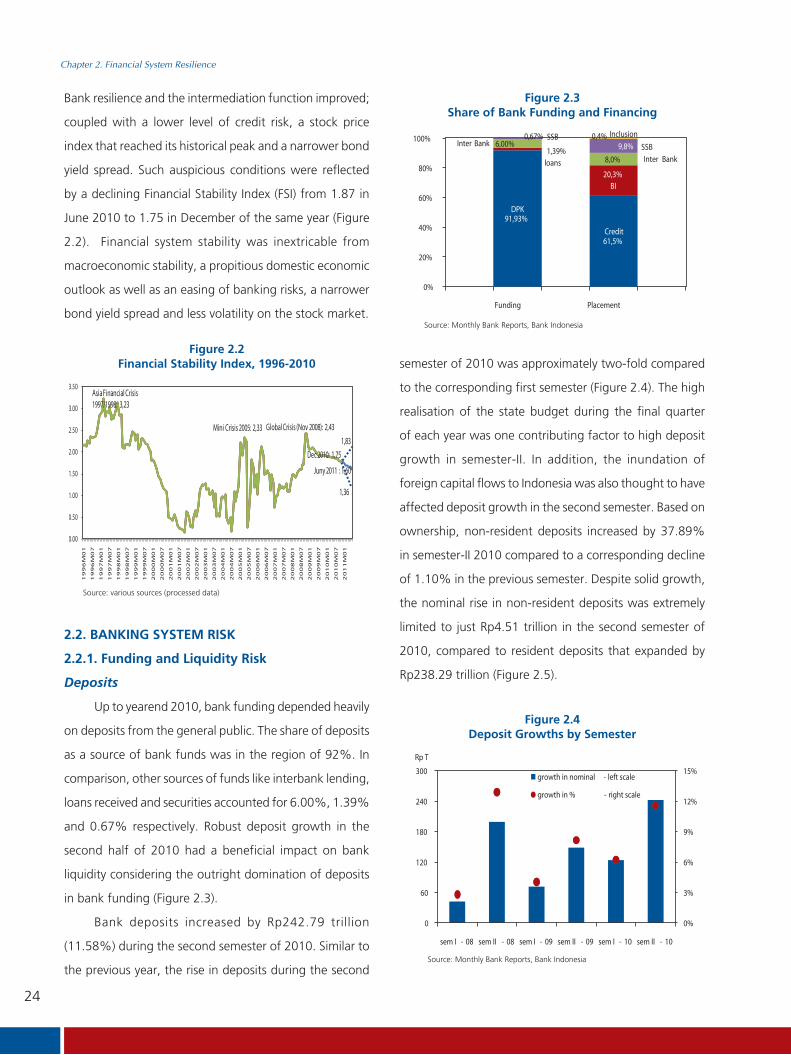

Bank resilience and the intermediation function improved;

coupled with a lower level of credit risk, a stock price

index that reached its historical peak and a narrower bond

yield spread. Such auspicious conditions were reflected

by a declining Financial Stability Index (FSI) from 1.87 in

June 2010 to 1.75 in December of the same year (Figure

2.2). Financial system stability was inextricable from

macroeconomic stability, a propitious domestic economic

outlook as well as an easing of banking risks, a narrower

bond yield spread and less volatility on the stock market.

91,93%

61,5%

1,39%

20,3%

6,00%

8,0%

0,67%9,8%

0,4%

0%

20%

40%

60%

80%

100%

Funding Placement

Credit

DPK

Inclusion

loans

BI

Inter Bank

Inter BankSSB

SSB

2.2. BANKING SYSTEM RISK

2.2.1. Funding and Liquidity Risk

Deposits

Up to yearend 2010, bank funding depended heavily

on deposits from the general public. The share of deposits

as a source of bank funds was in the region of 92%. In

comparison, other sources of funds like interbank lending,

loans received and securities accounted for 6.00%, 1.39%

and 0.67% respectively. Robust deposit growth in the

second half of 2010 had a beneficial impact on bank

liquidity considering the outright domination of deposits

in bank funding (Figure 2.3).

Bank deposits increased by Rp242.79 trillion

(11.58%) during the second semester of 2010. Similar to

the previous year, the rise in deposits during the second

semester of 2010 was approximately two-fold compared

to the corresponding first semester (Figure 2.4). The high

realisation of the state budget during the final quarter

of each year was one contributing factor to high deposit

growth in semester-II. In addition, the inundation of

foreign capital flows to Indonesia was also thought to have

affected deposit growth in the second semester. Based on

ownership, non-resident deposits increased by 37.89%

in semester-II 2010 compared to a corresponding decline

of 1.10% in the previous semester. Despite solid growth,

the nominal rise in non-resident deposits was extremely

limited to just Rp4.51 trillion in the second semester of

2010, compared to resident deposits that expanded by

Rp238.29 trillion (Figure 2.5).

0%

3%

6%

9%

12%

15%

0

60

120

180

240

300

sem I - 08 sem II - 08 sem I - 09 sem II - 09 sem I - 10 sem II - 10

Rp T

growth in nominal - left scale

growth in % - right scale

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

19

96

M0

1

19

96

M0

7

19

97

M0

1

19

97

M0

7

19

98

M0

1

19

98

M0

7

19

99

M0

1

19

99

M0

7

20

00

M0

1

20

00

M0

7

20

01

M0

1

20

01

M0

7

20

02

M0

1

20

02

M0

7

20

03

M0

1

20

03

M0

7

20

04

M0

1

20

04

M0

7

20

05

M0

1

20

05

M0

7

20

06

M0

1

20

06

M0

7

20

07

M0

1

20

07

M0

7

20

08

M0

1

20

08

M0

7

20

09

M0

1

20

09

M0

7

20

10

M0

1

20

10

M0

7

20

11

M0

1

Global Crisis (Nov 2008): 2,43

1,83

1,36

AsiaFinancial Crisis1997/1998: 3,23

Mini Crisis 2005: 2,33

Dec2010: 1,75

Juny 2011 : 1,60

Source: various sources (processed data)

Source: Monthly Bank Reports, Bank Indonesia

Source: Monthly Bank Reports, Bank Indonesia

Figure 2.2Financial Stability Index, 1996-2010

Figure 2.3Share of Bank Funding and Financing

Figure 2.4Deposit Growths by Semester

25

Chapter 2. Financial System Resilience

of statutory reserves based on the loan to deposit ratio

and the increase in the statutory reserve requirement for

foreign exchange.

7 Primary reserves include bank cask and checking accounts held at Bank Indonesia; secondary reserves include Bank Indonesia Certificates (SBI), other placements at Bank Indonesia and SUN (trading and available for sale); and tertiary reserves include SUN HTM.

(100)

0

100

200

CentralGovernment

LocalGovernment

PrivateIndividuals

Privatefinancial

institutions

PrivateCompany

OtherPrivate

Non Resident

Rp T

semester I 2010 semester II 2010

Based on component, the most impressive increase

in deposits was in the form of savings and term deposits,

which increased by 20.03% and 11.08% respectively.

Conversely, checking accounts grew by a mere 2.62%.

Despite well-maintained financial system stability

domestically, potential inflationary pressures stemming

from expectations of climbing interest rates as well as

global economic volatility could have been one factor that

steered the general public’s preference for investments

with a fixed yield, like savings accounts and term deposits.

Meanwhile, by currency, rupiah denominated deposits

continued to dominate growth in deposits. Of the total

increase in deposits during semester-II 2010, 93.13%

was attributable to rupiah based deposits. Consequently,

rupiah deposits grew by Rp226.11 trillion (12.82%) during

the reporting period compared to Rp16.68 trillion (5.03%)

for foreign currency denominated deposits.

Liquidity Risk

Strong deposit growth, in addition to benefitting

banks in terms of increasing credit, was also utilised to

manage liquidity by adding liquid assets7 (Figure 2.6).

Furthermore, banks were expected to require more

liquidity in 2010 to meet the planned implementation

600

700

800

900

0

200

400

600

Dec -09 Mar -10 Jun -10 Sep -10 Dec -10

Rp TRp T

Primary Reserves Secondary Reserves

Tertiary ReservesLiquid Assets (right scale)

As of December 2010, the total liquid assets of banks

reached Rp867.15 trillion, which represents a significant

increase compared to the position at the end of the

previous semester (June 2010), namely Rp709.28 trillion.

The most notable increase during semester-II 2010 was in

the form of primary reserves, which grew by 49.89% in line

with the mandatory increase in the primary rupiah reserve

requirement to 8% on 1st November 2010. Meanwhile,

secondary reserves increased by 18.82%. There were

indications of a shift during the reporting semester among

placements held at Bank Indonesia, namely from shorter-

term Bank Indonesia Certificates (SBI) and Term Deposits

(TD) to extended SBI (Figure 2.7).

Source: Monthly Bank Reports, Bank Indonesia

Source: Monthly Bank Reports, Bank Indonesia

Figure 2.5Deposit Growth based on Ownership

Figure 2.6Liquid Assets by Component

0%

20%

40%

60%

80%

100%

Jan -10 Mar -10 May-10 Jul -10 Sep -10 Nov -10