Financial Services Risk and Regulation Being better informed€¦ · Financial Services Risk and...

32

Being better informed FS regulatory, accounting and audit bulletin Financial Services Risk and Regulation PwC FS Risk and Regulation Centre of Excellence May 2016 In this edition: • Turning around investment banking • Retirement reform in South Africa • New rules for securities financing • A snapshot of our observations of the SAM comprehensive parallel run • IMF considers virtual currencies and blockchain • New PwC illustrative IFRS financial statements www.pwc.co.za/beingbetterinformed

Transcript of Financial Services Risk and Regulation Being better informed€¦ · Financial Services Risk and...

Being better informedFS regulatory, accounting and audit bulletin

Financial Services Risk and Regulation

PwC FS Risk and Regulation Centre of Excellence

May 2016

In this edition:

• Turning around investment banking• Retirement reform in South Africa• New rules for securities financing• A snapshot of our observations of the SAM

comprehensive parallel run• IMF considers virtual currencies and blockchain• New PwC illustrative IFRS financial statements

www.pwc.co.za/beingbetterinformed

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 2

Executive summary

Irwin Lim Ah Tock Banking and Capital Markets – Regulatory Practice Leader

note which outlined the ‘top of mind’ issues for discussions with bank boards during the year.

From an insurance perspective, with full Solvency Assessment and Management (SAM) implementation having now been moved out to 1 January 2017, insurers have an additional year to improve and embed the calculation and reporting process within the business-as-usual environment. In this edition, we set out some of our insights on key considerations for insurers as a result of this.

The scale of regulatory change facing the banking industry is sizeable, with many commentators now openly using the term ‘Basel IV’ as a useful short-hand to aggregate the wave of new regulatory proposals even if the term is yet to gain official acknowledgement.

Banks are facing significantly more disclosure requirements under the new Pillar 3 framework. The Basel Committee published a second consultation in March 2016 on various additions and revisions to the Pillar 3 disclosure rules, including introducing new disclosures in some areas, such as total loss-absorbing capacity (TLAC) and global systemically important bank (G-SIB) indicators. Elsewhere in the

Executive summary

Welcome to the first edition of Being better informed for 2016, our quarterly FS regulatory, accounting and audit bulletin. This publication aims to keep you up to speed with significant developments and their implications across all financial services sectors.

The start of the new year is traditionally busy for the financial services sector as firms, regulators and standard-setters sharpen their focus on key activities for the year ahead. This year has been no different. The Minister of Finance set out his tax plans in the annual national budget in February 2016, while the South African Reserve Bank issued an annual guidance

prudential space, the Basel Committee has been extremely busy, issuing its second consultation on a standardised measurement approach for calculating operational risk capital. This is in response to concerns that previous proposals would have had a disproportionate impact on certain business models. As in the first consultation, the Committee maintained its proposal for scrapping the advanced models approach and is now proposing banks use ten years of historical operational loss data in their calculations.

At the same time, a second consultation was issued in March 2016 by the Basel Committee on the revised standardised approach for credit risk. The key change introduced in the new proposal is the reintroduction of external credit ratings into the credit risk measurement framework for regulatory capital. However, taken together with other revisions and changes introduced in the consultation, the new proposals will have a significant impact on banks from an operational perspective, as a key feature of the new proposals – a ‘due diligence’ and enhanced ‘operational’ requirements – will mean banks will have to take a hard look at the robustness of their current credit risk management processes and controls.

The changes and new proposals do not stop there. In early April 2016, the Basel Committee proposed new revisions to the leverage ratio framework, building on the initial framework issued in January 2016. Here too, we think that the impact for banks could be sizeable, as the intersection between accounting, risk management and operational processes will continue to be critical in navigating the extensive number of changes to the regulatory framework on the horizon.

We trust you will continue to find our latest edition of Being better informed to be an insightful read. Any thoughts or comments you may have on how we can continue to enhance the publication are welcomed.

Irwin Lim Ah Tock Banking and Capital Markets Regulatory Practice Leader PwC South Africa

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 3

How to read this bulletin?

Review the Table of Contents in the relevant Sector sections to identify the news of interest. We recommend you go directly to the topic/article of interest by clicking on the active links within the table of contents.

Contents

Executive summary 2

Contents 3

Turning around investment banking 4

Cross-sector announcements 6

Banking and capital markets 6

Asset management and market-based financing 14

Insurance 15

Taxation 17

Accounting updates 21

Other 25

Contacts 32

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 4

Turning around investment bankingAn agenda for reviving profitable and sustainable growth Investment banks have faced a series of challenges over the last several years. The new regulations that followed the financial crisis have changed the industry in a number of ways, making it difficult to profit from many traditional lines of business by creating onerous capital, funding, and liquidity requirements and increased costs and operational complexity. At the same time, advances in technology have upended client interaction models, execution platforms, and operational processes.

In the post-crisis environment, global banks — investment banking divisions, in particular — have experienced significant financial challenges. In our most recent annual study of bank performance at the global level, we estimated that in 2014 the 29 global systemically important banks (G-SIBs) collectively missed their cost-of-equity thresholds by about three per cent, thereby incurring an aggregate economic loss of about US$90 billion.

Though the best strategy for growth will, of course, differ from one bank to another, all investment banks will likely need to consider the restructuring and

repositioning of their businesses if they are to achieve sustainable growth and profitability in the current environment. Our global strategy consulting thought leadership discusses five key areas of transformational change that we believe are critical to all investment banks:

• Building strategic coherence

• Progressing from technical to strategic optimisation

• Rethinking client profitability

• Accelerating operational efficiency and organisational change, and

• Focusing on change execution.

Banks need to invest significantly in the strategic optimisation of their business portfolios. Doing so requires identifying the most effective ways to boost performance in each line of business and across the group, taking account all performance factors. These factors include franchise and operational synergies as well as financial and other costs and constraints, while retaining or, ideally, enhancing the coherence of business models.

Turning around investment banking

Years of high returns during the pre-crisis years masked banks’ lack of attention to which clients were the main contributors to profitability and which weren’t, as well as the inefficiencies in their approach to client segmentation and coverage. Capital market players have typically been less focused than purely consumer-oriented companies on analysing the profitability of their customers and using client segmentation to determine which activities are creating or eroding value. However, a client-centric approach to profitability — understanding economic performance at the client level — is the best way to assess the effect of the external macroforces, including changes in market structure, changes in counterparty behaviour, and regulatory pressure, all of which have been squeezing revenues and increasing business costs.

Client segmentation has traditionally been driven by three core dimensions: industry, geography, and historical revenues. Although these dimensions are important overlays, we believe that client segmentation should be ‘value-driven’. This means considering the client’s

current value, potential value, and, finally, behaviour as related to interaction with the bank.

Outsized and unprofitable cost bases in many businesses are one of the legacies of the pre-crisis era, when profit margins were much higher, banks were expanding, and insufficient attention was paid to costs. Going forward, banks must improve their operational efficiency by aligning and transforming their existing infrastructure and technology platforms to fit the requirements of the businesses with which they choose to compete. In many cases, a fundamental transformation of the operating model may be required.

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 5

An illustrative view of the ‘new’ investment banking target operating model (TOM)

The new TOM for capital markets requires a centralised database for underlying engines such as valuation, risk management, and profit and loss (P&L) substantiation, supported by the introduction of a governance structure with direct accountability. External technologies should be combined with industry utilities. Depending on the state of the institution’s technology, internal platforms can be combined and outsourced. In many organisations, years of consolidating businesses and underinvesting in IT have created technology platforms that are fundamentally misaligned, and a more transformational or ‘greenfield’ approach is often best served.

Over the past several years our global team has published a series of reports on the challenges facing capital market participants. Recent reports include Banking industry reform — a new equilibrium, De-leverage take 2: Making a virtue of necessity, Capital Markets 2020: Will it change for good?, and Post-trade services in financial markets: Moving from backstage to center stage. In recent months, based on our analyses of market conditions, regulatory initiatives, and discussions with clients, it has become clear that the challenges confronting the industry have increased in severity. We believe that banking organisations need to change in ways that are more structured and more complex than at any time in the past, and we have reached several conclusions about the transformation imperatives for 2016 and beyond.

For the full report: http://www.strategyand.pwc.com/reports/turning-around-investment-banking

Turning around investment banking

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 6

Cross-sector announcements

Cross-sector announcements Banking and capital markets

Capital and liquidity

Basel Committee reconsiders credit risk

The Basel Committee published a consultative document, Revisions to the Standardised Approach for credit risk, on 10 December 2015. The original proposals removed all reference to external credit ratings and assigned risk weights based on a limited number of alternative risk drivers. Feedback indicated that removing ratings completely was unnecessary and undesirable. The revised proposals reintroduce the use of ratings for banks and corporate exposures, but with a due diligence override that could result in higher risk weights. The proposals also include alternative approaches for jurisdictions that do not allow the use of external ratings for regulatory purposes, and modify the risk weights for real estate loans with the loan-to-value ratio being the main risk driver for risk weighting purposes, together with the use of a three-category classification hierarchy. While the revised proposals no longer include the debt service coverage ratio as the main risk driver, the assessment of a borrower’s ability to pay is required

and urge the addition of macro-prudential tools to the policy toolkit. The Basel Committee identifies three areas for ongoing reforms:

• Enhancing the risk sensitivity and robustness of standardised approaches

• Reviewing the role of internal models in the capital framework, and

• Finalising the design and calibration of the leverage ratio and risk-weighted capital floors. It plans to issue final standards covering the outstanding revisions to the regulatory framework by the end of 2016. The Basel Committee expects to consult soon on a package of reforms to enhance the comparability of risk-weighted assets calculated using internal ratings-based approaches for credit risk. Around the end of the year it expects to finalise the revised market risk framework, which includes greater standardisation of traded market risk model requirements.

track to meet the Basel standards. All Basel Committee members had implemented risk-based capital regulations by the end of 2013, and all but two members had published final regulations to implement the liquidity coverage requirements. Of the 27 Committee members as at the end of September 2015, 23 had issued final or draft rules on or for the leverage ratio, with 25 issuing final or draft rules for their global or domestic SIB framework. Only four had issued final rules for NSFR. The report found substantial progress in non-Basel Committee jurisdictions’ adoption of Basel III standards and concludes that regulations are more consistent with the Basel III framework because of the Committee’s efforts to monitor and assess implementation. The annex to the report contains an assessment of the consistency of capital regulations in the EU, Hong Kong, Saudi Arabia, South Africa and the US.

Basel Committee reports on reform

On 13 November 2015, the Basel Committee published Finalising post-crisis reforms: an update – A report to G20 Leaders. Describing the post-crisis financial reforms, it covers efforts to increase the quality and level of capital, enhance risk capture, limit leverage and concentration,

and is a key underwriting criterion. The proposals also address exposures to multilateral development banks, retail and off-balance sheet items. The approach to the treatment of sovereign, central bank and public sector entity exposures is not within the scope of these proposals. The Basel Committee is considering these exposures as part of a broader and more holistic review of sovereign-related risks. The Committee intends to conduct an impact study in 2016 and will review the calibrations in the proposals against the results of that study. Whilst the Basel Committee aims to balance risk sensitivity and complexity, it recognises that there could be a lack of comparability between jurisdictions that use ratings for regulatory purposes and those that do not. The Committee intends to finalise the revised standard by the end of 2016.

Good implementation of Basel III

The Basel Committee published Implementation of Basel standards – a report to G20 leaders on the implementation of the Basel III regulatory reforms – on 13 November 2015. It found that implementation of the Basel III capital and liquidity standards has been timely in general. Quantitative monitoring of Basel III regulations shows that banks are on

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 7

Significant revisions to market risk capital

The Basel Committee issued an exploratory note on the revised minimum capital requirements for market risk on 14 January 2016. The framework will come into effect on 1 January 2019. The reforms address issues not resolved in Basel 2.5, such as an inadequate regulatory boundary between the banking and trading book, and weaknesses in the value-at-risk framework. The Basel Committee believes this incentivised banks to arbitrage their capital requirements between the banking book and the trading book, and take on ‘tail risks’ (the risk of loss due to rare events). The Basel Committee confirmed which instruments can be included in the trading book and set strict limits for any deviation. It also proposed a limit on moving instruments between trading and banking books. Banks will pay a fixed capital charge for any reduction in capital charge due to moving the instruments. The proposal replaces normal and stressed value at risk, with a single expected shortfall metric for both standardised and internal models approaches. Banks should calibrate it to a period of significant market stress and consider varying liquidity horizons. These changes aim to address both tail risk and market illiquidity risk. Bank supervisors are able to review the use of internal models for each trading desk, in

contrast to the current framework, where this is only possible at a firm-wide level. This makes it easier for supervisors to take decisions on disallowing the use of internal models where necessary.

More capital to cover market risk

On 18 November 2015, the Basel Committee published Fundamental review of the trading book – interim impact analysis. It looked at 44 banks and calculated that total non-securitisation market risk capital charges would be equivalent to a 4.7% share of the overall Basel III minimum capital requirement under the revised market risk framework. The change is reduced to 2.3% on excluding the bank with the largest value of market RWAs. The Basel Committee expects the proposed market risk framework to result in a weighted average increase of 74% in aggregate market risk capital charges. The increase in capital requirements is estimated at 54% for internally modelled approaches and 128% for the standardised approach. Based on a sample of 16 banks, 88% pass the P&L attribution measure at bank level, but the pass rates were much lower at the more granular trading desk level. The Basel Committee expects to publish the results of the fundamental review of the trading book by the end of the year.

Capital requirements for securitisations

The Basel Committee consulted on capital treatment for ‘simple, transparent and comparable’ (STC) securitisations on 10 November 2015. The EC had proposed broadly similar regulations on the structuring and capital requirements for such securitisations in September 2015. The Basel Committee recommends equalising the total capital required for a securitisation with that required for the underlying assets, justifying this on the basis that STC transactions have reduced structural risk. Its approach is similar to the EC’s, but stricter:

• The Committee requires investors to independently validate originator compliance with STC criteria, whereas the EC places compliance responsibility with issuers (which means an investor would be required to make the determination before applying alternative capital treatment independently of the originator’s certification under the Committee’s approach).

• The Committee would exclude asset-backed commercial paper from its proposed capital benefits, whereas the

EC includes such products, subject to some additional requirements.

• The EC allows synthetic securitisations to apply more favourable risk weights in certain circumstances when backed by a pool of loans to SMEs, while such an approach is not available under the Committee’s framework.

• The Basel Committee recommended that regulators reduce the risk weight floor for senior tranches of STC securitisations to between 10%–12%, from the current 15% requirement. This is in line with the EC’s proposals, where the floor for senior tranches is reduced to 10% and a 15% floor is retained for mezzanine tranches in light of their increased risk.

• Both the Basel Committee and EC propose permitting STC securitisations to apply the same risk weights that they would enjoy for internal ratings-based approaches to external approaches.

The consultation period closes on 5 February 2016.

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 8

Higher capital requirements for SFTs

• On 5 November 2015, BCBS consulted on setting higher capital requirements for securities financing transactions (SFTs) that impose haircuts below the proposed haircut floors. BCBS is exploring this approach to incentivise banks to set collateral haircuts above the floors instead of simply holding more capital. BCBS emphasised the floors are intended to serve only as a ‘backstop’ and should not replace thoughtful self-assessments. It suggests the higher capital requirements would only apply to non-centrally cleared transactions, with a number of other carve-outs to limit their scope being proposed (e.g. when the transaction references government securities or is with a central bank). The proposed haircut levels for securitised products involve the following:

• 1% for debt securities and floating rate notes with a maturity of less than or equal to one year

• 4% for debt securities with a maturity between more than one year and equal to or less than five years

• 6% for debt securities with a maturity between more than five years and less than or equal to ten-year debt securities, and

• 7% for debt securities with a maturity of more than ten years.

The consultation closes to comments on 5 January 2016.

with different timelines based on the respective disclosure requirements. The phase two proposals include:

• The addition of a ‘dashboard’ of key metrics

• Disclosure of hypothetical risk-weighted assets calculated based on the basel framework’s standardised approaches, and

• Enhanced granularity for disclosure of prudent valuation adjustments.

The proposals also incorporate additions to the Pillar 3 framework to reflect ongoing reforms to the regulatory framework. These include disclosure requirements for:

• The total loss-absorbing capacity (tlac) regime for global systemically important banks

• The proposed operational risk framework, and

• The final standard for market risk.

The comment period closes on 10 June 2016.

Circular 8 of 2015: Implementation of Countercyclical Buffer

The purpose of the circular is to provide information in respect of matters related to phasing in the implementation of the countercyclical capital buffer (CCB) in South Africa. It provides some details with regard to how the rates are determined as well as details of the disclosure of key information.

Leverage ratios ‘mutually reinforcing’

On 27 November 2015, the ECB published The impact of the Basel III leverage ratio on risk-taking and bank stability. The report states that the leverage ratio requirement will lead to a limited increase in risk taking which is more than offset by the benefits of increasing loss-absorbing capacity – thus resulting in more stable banks. It further suggests that any increase in banks’ risk taking (which may be caused by the non-risk-based leverage ratio) should be minimal as long as the risk weights approach is also adopted and calibrated at an appropriate level. Use of both measures ensures banks have an incentive to limit their risk taking while operating with reasonable levels of leverage. The Basel III leverage ratio is expected to become a minimum international requirement on 1 January 2018.

Revised Pillar 3 framework

On 11 March 2016, the BCBS published the second phase of the revised Pillar 3 framework, Pillar 3 disclosure requirements – enhanced and consolidated framework. The proposed enhancements issued in the latest consultation document build on revisions to the Pillar 3 disclosure requirements that the Committee finalised in January 2015, which the SARB endorsed in December 2015 through Directive 11/2015. Taken together with the Committee’s 2015 proposals, the latest set of proposals forms the consolidated and enhanced Pillar 3 framework that banks will need to comply with – albeit

Rates

• The CCB add-on rate will be set in a range of between 0 per cent and 2,5 per cent of risk-weighted assets (RWA). The add-on rate:

• Will be calculated as the weighted average of the buffers in effect in the jurisdictions to which banks have private sector credit exposures; and

• Will apply to bank-wide total rwa (including credit, market, and operational risk) as used in the calculation of all risk-based capital ratios, consistent with it being an extension of the capital conservation buffer.

• The credit-to-GDP gap will be the main indicator informing the activation of the countercyclical capital buffer in South Africa, though other indicators may be used together with the credit-to-GDP gap.

• A sectoral CCB may be set if this is deemed appropriate.

• Private sector credit exposures is defined as exposures to private sector counterparties which attract a credit risk capital requirement in the banking book, and the risk-weighted equivalent trading book capital requirement for specific risk, the incremental risk requirement, and securitisation. In this regard, interbank exposures and exposures to the public sector are excluded, but non-bank financial sector exposures are included.

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 9

Reporting and disclosure requirements

• The CCB must be reported on form BA 700. Furthermore, a different percentage should be reported in form BA 610, which is based on that particular entity’s weighted average of the CCB rates that apply in the jurisdiction where the relevant private sector credit exposures are located.

• The CCB must therefore be applied on a consolidated, bank-solo and foreign entity level.

• A geographic breakdown must be provided of the private sector credit exposures they have used in the calculation of the CCB.

• Banks are required to maintain a list of the location of all their credit exposures, setting out CCBs in place in the various jurisdictions and private sector credit exposures to those jurisdictions that do not operate and publish buffer add-ons.

The CCB becomes effective in South Africa as from 1 January 2016. However, the rate is set at 0% until further notice from the SARB.

Circular 9 of 2015: Postponement of the effective date of the amended regulations

The circular indicates that the effective date of the amended Banks Act regulations, originally scheduled for 1 January 2016, has been postponed to 1 April 2016.

Circular 2 of 2016: Clarification of interpretive matters with respect to the liquidity coverage ratio calculation (LCR)

The SARB issued Circular 2 of 2016 on 9 February 2016 to clarify certain interpretive matters with regard to LCR as follows:

a. Investments in foreign currency-denominated HQLA to cover domestic currency cash outflows will be limited to 5% of the total ZAR HQLA and subject to an 8% haircut. Furthermore, the circular clarifies that the SARB will allow foreign currency inflow limited to 75% of the foreign currency outflow to be included in the combined currency calculation.

b. The SARB accepts the fact that the daily LCR reported on the BA 325 at month end may differ from the monthly BA 300 return, provided such difference is ‘immaterial’. The circular, however, does not define ‘immaterial’.

c. Banks should use the daily average rules specified in Regulation 8.

d. In the calculation of the consolidated LCR for the group, banks should limit

the recognition of HQLA from banks in foreign jurisdictions to the prescribed limit during the phase-in period (70% of net inflows in 2017), unless the excess HQLA above this limit can be proven to meet minimum transferability and fungibility criteria. This clarifies a major issue in the industry where certain banks were not limiting their HQLA to the phase-in limits, while others were.

e. Clarification is given that the NSFR should not be subject to the regulatory audit until such time as an amended NSFR form has been adopted by the SARB.

The circular is effective immediately.

SARB Directive 10 of 2015

Directive 10 of 2015 was issued on 30 November 2015 and covers matters related to changes to the AMA operational risk management and measurement system used for the calculation of required capital for operational risk. The directive sets out the requirements for the approval and notification of changes to AMA banks’ existing operational risk management and measurement system. It requires banks to classify changes to the AMA operational risk management and measurement system under three categories (based on established criteria) and prescribes how to interact with the Registrar’s office on each of the three classes. These three classes are described in more detail below.

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 10

Material changes (including extensions)

Material changes or extensions (be they quantitative or qualitative) require prior written approval from the Registrar’s Office. From a qualitative perspective these can be either material changes to the AMA operational risk management and measurement system (e.g. changes to how insurance contracts are recognised within the model, changes to the measurement system – including how the four data elements are combined or change the capital allocation drivers within the group, changes in the organisational and operational structure of the independent risk management function for operational risk which reduce the ability of the operational risk management function to oversee and inform the decision-making processes, etc.) or extensions to the AMA operational risk management and measurement system (e.g. first-time adoption of elements such as the introduction of operational risk mitigation techniques (for example insurance), the introduction of recognition of correlations, etc.).

From a quantitative perspective, the directive defines a material change as a change (including extensions) that results in an increase or decrease in capital of 10% or more of the AMA operational risk model at the various levels, including bank, bank-consolidated or controlling company-consolidated levels. In making the above

assessment, the impact on the capital must refer only to the impact of the change on the AMA operational risk model; that is, the impact of the change should be isolated. Therefore, the operational risk profile must be assumed to remain constant.

All other changes (including extensions) that are not classified as material when assessed based on the above criteria must be classified as non-material changes.

Non-material changes requiring prior notification

These are defined as being changes of lesser materiality but which still, due to their degree of materiality, require notification to the Registrar’s Office at least 15 days before their implementation. Examples include changes to the way the operational risk management and measurement system is integrated into the day-to-day management process; changes in the organisational and operational structure of the independent risk management function for operational risk; changes to validation processes; internal review changes to the standards relating to internal data, scenario analysis and business environment, and internal control factors; etc.

Non-material changes requiring post-notification

These are defined as changes with a low level of materiality. These changes only need to be brought to the attention of the Registrar’s Office at regular intervals, after their implementation. They must be reported to the Registrar on a bi-annual basis, aligned with the Model Descriptive Statistics submissions for June and December.

This directive requires banks to seek written approval for any material extension or change for which approval was obtained but which the bank has decided not to implement. The directive also requires banks to notify the Registrar when there are delays in the implementation of approved changes or extensions.

SARB Directive 10 of 2015 also sets out the documentation that has to accompany a notification by a bank to the Registrar’s office for material and non-material changes or extensions to the AMA operational risk management and measurement system used for the calculation of required capital for operational risk.

Structural reform and other prudential rules

Valuing derivative liabilities in resolution

The EBA published the final draft RTS on the methodology for the valuation of derivative liabilities for the purposes of bail-in resolutions on 17 December 2015. Through the methodology, the EBA aims to provide EU resolution authorities with a means of valuing the derivative liabilities of credit institutions placed under resolution. BRRD gives resolution authorities write-down and bail-in powers in relation to a credit institution’s liabilities, including liabilities from derivatives contracts. Under the draft RTS, derivative counterparties are given the chance to provide evidence of commercially reasonable replacement trades within a given time period. If they fail to exercise this option, resolution authorities will apply a statutory methodology supported by observable market data or other relevant information. For centrally cleared derivatives, the draft RTS takes into account the EMIR framework and provides for a process that leans on the CCP default and valuation procedure. The draft RTS has been submitted to the EC for endorsement. It will also be subject to scrutiny from the EP and the Council before being published in the official journal.

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 11

Tweaking TLAC

The FSB published an overview of the post-consultation revisions to the TLAC Principles and Term Sheet on 9 November 2015. It sets out the changes it made to its TLAC term sheet as a result of comments received from its 2014 consultation. These changes include an adjustment where the sum of TLAC requirements for the multiple-point-of-entry resolution entities is more than would be the case for the hypothetical minimum requirement under a single-point-of-entry resolution strategy.

The new term sheet has adopted the concept of a material sub-group rather than a material entity in relation to internal TLAC. It also provides for a small allowance for firms pursuing structural subordination where the presence of liabilities in holding companies which rank equivalent or junior to TLAC will be unavoidable. This allowance is not permitted to exceed 5% of the resolution entity’s external TLAC. There is an allowance of 2.5% of RWAs for liabilities that could count as external TLAC, which will rise to 3.5% of RWAs in 2022. The FSB maintained its expectation that 33% of TLAC must be met by long-term debt in the final term sheet and structured notes’ ineligibility to be held for TLAC. The internal TLAC requirement of 75%–90% also remains unchanged. Finally, the FSB introduced a new disclosure requirement for entities that are part of a material subgroup and issue internal TLAC to a

resolution entity to disclose liabilities which rank equivalently with or junior to its internal TLAC.

Holding other banks’ TLAC

On 9 November 2015, in parallel with its paper on TLAC term sheets, the Basel Committee released TLAC Holdings – consultative document. It sets out the proposed approach for the deduction treatment of banks’ investments in TLAC, and proposals on the extent to which instruments that rank equivalently to TLAC should be subject to the same deduction treatment. The proposals are intended to limit the effects of contagion through banks holding the TLAC of other banks. The Basel Committee proposes that all internationally active banks, not just G-SIBs, should be required to deduct their net TLAC holdings, where these do not qualify as Basel III capital, from their own tier 2 capital. This is the same approach adopted under the Basel III framework for banks’ investments in the tier 2 capital of other banks. The term ‘TLAC holdings’ is defined by the Basel Committee and may include those instruments that would otherwise have counted as TLAC but don’t because they have less than one year until maturity, and also subordinated instruments that rank pari passu with TLAC instruments but never qualified as TLAC. The Basel Committee further suggests that instruments eligible for an exemption from the subordination requirements, which rank equivalently

with excluded liabilities, must have an original maturity of more than one year to qualify as TLAC. The approach is proposed to come into effect on 1 January 2019 (at the same time as the TLAC regime). The consultation closes for comments on 12 February 2016.

Subordination challenge for TLAC

On 9 November the FSB summarised Findings from the TLAC Impact Assessment Studies. Its work included:

• A quantitative impact assessment

• An economic impact assessment

• A market survey, and

• A verification of historical losses and recapitalisation needs.

The FSB found that market participants (including G-SIBs, other market participants such as asset managers and CRAs) expect the TLAC requirements to cause bond spreads to rise by 30 basis points from their current levels. On average, they expected G-SIBs to hold a TLAC buffer equivalent to 1.8% of RWAs above the minimum TLAC requirement. In their responses, G-SIBs most frequently cited subordination as a challenge in meeting the TLAC requirements. A significant number of market participants considered that market conditions were currently attractive for G-SIBs as issuers, due to unconventional monetary policies prompting a search for yield by investors.

TLAC: Good for the economy

On 9 November 2015, BIS published Assessing the economic costs and benefits of TLAC implementation. BIS found that TLAC benefits in terms of GDP were in the range of 45 to 60 basis points and were significantly higher than the implementation costs for firms. Benefits are expected to arise from enhanced market discipline, leading G-SIBs to reduce risk taking. It is also expected to improve the resilience of the financial system and reduce the probability of systemic crises. The costs were calculated by assuming that increased funding costs for G-SIBs translate to higher lending costs for firms, and estimating the effect of higher costs of credit to clients on GDP. Depending on the calibration of TLAC chosen, this was expected to lead to a 1.9 to 5.3 basis point drag on GDP resulting from increased lending interest rates of between 5 and 15 basis points. Spill-overs transmitted via trade, financial and commodity price linkages are expected to account for a quarter of the output loss.

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 12

FSB finalises TLAC

On 9 November 2015, the FSB released Principles on Loss-absorbing and Recapitalisation Capacity of G-SIBs in Resolution and TLAC Term Sheet. The foremost policy objective for TLAC is that G-SIBs should have sufficient loss-absorbing and recapitalisation capacity to ensure an orderly resolution in the event of failure. It also aims to minimise the impact on financial stability, ensure the continuity of critical functions and avoid exposing tax payers to loss.

The TLAC principles concern the following:

• Calibration of tlac

• Availability of tlac to facilitate the resolution of cross-border groups

• Determination of instruments eligible to meet tlac requirements

• Interaction with regulatory requirements and consequences of breaching tlac

• Disclosure of information

• Limitation of contagion

• The need for a review over the medium term to ensure consistent implementation, and

• Any further modifications to the term sheet.

The term sheet has remained consistent following the November 2014 consultation, adopting a phasing-in approach for implementation and setting the minimum requirement at 16% of RWAs and 6% of the Basel III leverage ratio denominator (LRE minimum) from 1 January 2019. This will increase to 18% of RWAs from 1 January 2022 and 6.75% of the LRE minimum from 1 January 2022. For G-SIBs in emerging market economies (EMEs), the lower requirement applies from 1 January 2025 and the higher threshold must be met by 1 January 2028. But this can be accelerated if the amount of an EME G-SIB’s outstanding financial and non-financial corporate debt securities or bonds exceeds 55% of its home jurisdiction GDP. As these are minimum standards, local regulators can still set a firm’s TLAC to be higher than the requirements (which we’ve already seen in prior announcements from the Swiss authorities and US Fed). Capital used to satisfy minimum regulatory capital requirements can also count towards TLAC – subject to certain conditions. But CET1 contributing to minimum TLAC should not be used to meet regulatory buffers. The FSB intends to conduct a review of the technical implementation of the TLAC standard by the end of 2019, which coincides with a review that the EU authorities will be undertaking of the MREL.

Taking stock of resolvability obstacles

On 9 November 2015, the FSB released Removing Remaining Obstacles to Resolvability: Report to the G20 on progress in resolution. The report found that resolution planning within CMGs for GSIBs has advanced significantly but that substantial work remains to remove obstacles to resolvability and make resolution strategies and plans operational. It also found that only a subset of FSB jurisdictions, mostly G-SIB home jurisdictions, have a resolution regime with powers in line with the key attributes. The powers most commonly lacking are bail-in powers and the power to impose a temporary stay on early termination rights. Impediments that are yet to be addressed for G-SIBs include:

• Funding and liquidity needs

• Availability of unencumbered assets in resolution

• Continuity of shared services that are necessary to maintain the provision of a firm’s critical functions in resolution

• Continued access to payment, settlement and clearing services

• Capabilities to generate accurate and timely information in resolution

• Implementation of the new tlac standard making bail-in operational, and

• Cross-border effectiveness of resolution actions.

The FSB plans to undertake further work in the coming year on maintaining continuity of access to FMIs, addressing the legal and operational complexities in relation to bail-in, and developing implementation guidance with relation to TLAC – particularly internal TLAC. The FSB also expects to perform more work on CCP resolution planning, as reforms to resolution regimes and resolution planning are less advanced for insurers and FMIs than for banks.

Conduct

Reducing misconduct risk

On 6 November 2015, the FSB published a progress report on the work it is co-ordinating to address misconduct in the financial industry. The report sets out the actions the FSB and international standard setters are taking in this regard. In looking at the role of incentives in reducing misconduct, the FSB states that it will further examine the effectiveness of mechanisms like malus and clawback to determine their impact as deterrents to conduct risks. It will also establish a working group to exchange national good practices on the use of governance frameworks to address misconduct risks. In relation to the international coordination of conduct in FICC markets, the FSB notes that work is underway in a number of national jurisdictions to address the gaps in standards of market practice. IOSCO established a task force on market

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 13

conduct in October 2015, which will publish its final report in June 2016. The FSB will also publish a monitoring report at this time on progress in implementing its work plan on interest rate benchmarks. In May 2017, the BIS Markets Committee is due to finalise its FX code of conduct standards and principles. On coordinating the application of conduct regulation, senior officials from prudential and conduct financial authorities will share information on their respective powers and approaches to supervision and enforcement of conduct rules on an ongoing basis. This will include ensuring enforcement action as a credible deterrent.

Progress on compensation practices

The FSB published Implementing the FSB Principles for Sound Compensation Practices and their Implementation Standards (fourth progress report) on 10 November 2015. The standards were developed following a 2011 G20 request, and it published the last progress report in November 2014. The FSB notes that since 2014, nearly all countries have implemented the practices and standards, but significant implementation gaps still remain in a number of other countries due to local legal and other restraints. Most regulators now include compensation structures within their ongoing supervision of firms and report that most firms have implemented the practices and standards – though typically,

fewer compensation rules exist for insurers than banks. But the FSB expects this to change in 2016 (in the EU) with Solvency II implementation.

Other

Using AML/CFT data effectively

The FATF released guidance on AML/CFT-related data and statistics on 27 November 2015. The guidance provides options for collecting, maintaining and presenting AML/CFT-related statistics, advice on how to analyse the statistics, and concrete examples of how statistics may be used to assess the effectiveness of AML/CFT systems under the methodology.

FATF identifies eleven immediate outcomes that are central to a robust AML/CFT system, as follows:

• Understand money laundering and terrorist financing risks and, where appropriate, coordinate actions domestically to combat money laundering and the financing of terrorism, and the proliferation thereof.

• Obtain information, financial intelligence, and evidence about and facilitate action against criminals and their assets through international co-operation.

• Competent authorities use financial intelligence and all other relevant information appropriately for money laundering and terrorist financing investigations.

• Investigate money laundering offences and activities, and prosecute offenders and subject them to effective, proportionate and dissuasive sanctions.

• Prevent terrorists, terrorist organisations and terrorist financiers from raising, moving and using funds.

This FAFT guidance document notes that statistics may be a complement to the qualitative data.

More guidance for effective banking supervision

On 21 December 2015, the Basel Committee consulted on Guidance on the application of the core principles for effective banking supervision to the regulation and supervision of institutions relevant to financial inclusion. The consultation builds on the Committee’s previous work to expand guidance on applying its core principles for effective banking supervision. The paper examines the risks posed by financial institutions working to reach unserved and underserved customers, who are categorised as individuals without an account at a formal financial institution.

The guidance aims to support supervisors with their regulatory and supervisory approach to changes and innovation in products, services and delivery channels of institutions approaching these customers. It also addresses issues relating to consumer protection, AML and CTF. The Committee sets out additional guidance for 19 of its core principles, which is required when applying the principles to the supervision of institutions engaging with unserved and underserved customers. The Committee doesn’t create any new principles or exclude the applicability of any core principle to developments relating to financial inclusion. The consultation closes on 31 March 2016.

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 14

Mitigating systemic risks of shadow banking

The Basel Committee published a consultation on Identification and measurement of step-in risk on 17 December 2015, proposing a conceptual framework to mitigate systemic risks of the shadow banking system and their impact on banks. Step-in risk is the risk that a bank will provide financial support beyond its contractual obligations to another entity that experiences financial stress. The proposed framework focuses on identifying entities that are outside of the regulatory scope of group consolidation, but to which a bank may provide financial support to protect itself from reputational risk arising from its connection to the entities. Step-in risk indicators that help determine the relationship between the bank and the shadow banking entity may include criteria such as capital ties, sponsorship, decision-making or operational ties. Supervisors and banks may also consider other secondary indicators in their final assessment. The Basel Committee sets out possible approaches to address step-in risks through prudential measures, including:

• A conversation approach, imposing quantitative requirements on the bank where the entity that poses step-in risk remains unconsolidated, and

• A consolidation approach, so that the entity would be included in the scope of regulatory consolidation. The Basel Committee will conduct a QIS in the first half of 2016 to collect data on the nature and extent of step-in risks which, together with consultation responses, will inform its deliberations on the final framework. The consultation closes on 17 March 2016.

Implementing risk data aggregation principles

The Basel Committee published Progress in adopting the Principles for effective risk data aggregation and risk reporting on 16 December 2015, its third report since the principles were published in January 2013. It concludes that although banks have made progress towards implementation, important challenges remain and it is expected that some banks will not meet the principles on time. It made recommendations, including that national supervisors should conduct more in-depth and specialised examinations to evaluate weaknesses and that banks’ compliance should be subject to independent evaluation in early 2016. Banks designated as G-SIBs were required to implement the principles in full by 2016.

The Basel Committee also recommended that national supervisors apply the principles to banks identified as D-SIBs within three years of their designation.

Asset management and market-based financing

New rules for securities financing

On 12 November, the FSB published Transforming Shadow Banking into Resilient Market-based Finance: An Overview of Progress and its Global Shadow Banking Monitoring Report 2015. The FSB provided an update on its framework for monitoring shadow banking and its development of policies to strengthen oversight and the regulation of shadow banking. Using a narrow definition of shadow banking, it found that credit intermediation associated with investment vehicles has grown more than 10% on average over the past four years, while the level of securitisation-based credit intermediation has fallen. The FSB’s broad measure of shadow banking activity found that the assets of other financial intermediaries, pension funds and insurance companies grew by 9% to $137 trillion over the past year. The FSB also published a regulatory framework for haircuts on non-centrally cleared securities financing transactions. The framework provides quantitative and qualitative standards for calculating haircuts on collateral for non-centrally cleared securities financing transactions. It sets numerical haircut floors for non-bank to non-bank transactions. The framework provides an exemption from the numerical haircut floors for cash-

collateralised securities lending, but expects that collateral upgrades will be included unless certain conditions are met. The FSB recommends that the Basel Committee incorporate the numerical haircut floors into capital requirements for securities financing transactions under the Basel frameworks by the end of 2015. Jurisdictions with a large volume of securities financing transactions are advised to apply the floors using market regulation by the end of 2018, which represents a delay of one year compared to the October 2014 framework document.

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 15

Insurance

A snapshot of our observations of the SAM comprehensive parallel run

With full SAM implementation having now been moved out to 1 January 2017, insurers have an additional year to improve and embed the calculation and reporting process within the business-as-usual environment. From an audit perspective, the Financial Services Board will require the SAM balance sheet, the solvency capital requirement (SCR), the minimum capital requirement (MCR) as well as other key disclosures such as the analysis of surplus (AoS) to be audited post-implementation. However, the Financial Services Board will also require insurers to carry out the comprehensive parallel run (CPR) in 2016 until the implementation of SAM. The 2016 CPR will be subject to external audit.

As a result of the external audit questionnaire issued as part of the 2015 CPR and in anticipation of the audit requirements, a number of insurers have obtained an independent review of the calculations and reporting process so as to gain comfort on indicative figures reported to risk and audit committees over 2015. PwC has performed a number of CPR reviews, at various levels of detail, to assist insurers in gauging readiness for the post-implementation audit requirements. These reviews have allowed us to identify some

of the key challenges facing the industry, as shared below:

• Data: Whilst insurers are comfortable that the data is generally of good quality and sufficiently detailed, limited documentation and controls exist around data management to evidence/support this view.

• Software: The majority of insurers are making use of the CPR submission spreadsheets and manual excel spreadsheets. Governance and controls in respect of these models are limited, resulting in a number of ‘finger’ and/or unintentional errors not being picked up.

• Automation: Insurers are finding that there is a need to automate more of the regulatory reporting processes to reduce the time it takes to report, reduce manual errors, increase controls and ensure the process is scalable.

• Use of expert judgment: Various elements of the return require the use of ‘expert judgment’. These subjective judgments may materially impact the solvency margin; however, the level of governance and controls in respect of these judgments is not commensurate with the associated risk.

• Documentation: Documentation of the valuation process is limited. This increases key man risk and reduces the level of transparency.

• Interpretation of the principles: To a large extent, the proposed requirements are principles-based as opposed to rules-orientated. Thus a common question asked is, ‘Does my interpretation align to yours/our auditor’s and/or that of the rest of the market?’ We have found numerous instances where different interpretations apply across different insurers.

• Allowance for loss absorbency of deferred taxes: The allowance for the loss absorbency of a deferred tax asset following an SCR event can significantly reduce the SCR. However, insurers are grappling with the appropriate process, approach and assumptions to be used – to a large extent, insurers have ignored some key considerations related to the potential deferred tax adjustment and hence the appropriate adjustment.

• Principle of proportionality/materiality: Most insurers have applied the principle of proportionality/materiality for some elements of the submission, including areas where simplifications/approximations are applied. However, some insurers were not able to demonstrate consistent understanding and application of materiality/proportionality across all elements of the submission, as no central policy was in place to guide users.

Client assets/Client money

IOSCO published its final report standards for the custody of CIS’ assets on 10 November 2015. It updates the original 1996 standards to reflect market changes and align with other IOSCO activities. In particular, IOSCO focuses on the increased activities in stock lending, putting more pressure on the custody of assets that are reused to generate additional returns.

The updated standards focus on:

• Establishing a regulatory regime for CIS custodial arrangements

• Segregating cis assets from a custodian’s other assets

• Requiring custodians to be functionally independent from the asset owner/manager

• Disclosing custody arrangements to investors

• Selection criteria for appointing a custodian, and

• Ongoing monitoring of the custodian’s activities.

No changes should be necessary in the EU, given the recent AIFMD implementation and forthcoming UCITS V implementation (in March 2016). But outside the EU, existing practices might need revision.

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 16

• Asset templates: The volume of asset information that is required in the templates is onerous, and insurers are still spending a large part of their SAM projects ensuring the quality of this data.

• Ownership of the reporting process: There has been debate at a number of insurers about the ownership of the reporting template and the reporting process. A number of insurers have assigned a regulatory reporting manager as the owner of the reporting template and the reporting process; however, it is evident that the reporting requirements require increased collaboration between risk, financial and actuarial teams and a coordinated delivery.

The diagram illustrates our view of industry readiness for audit, taking into account the findings we have noted across various reviews conducted in the past year.

Maturity of SAM implementation

QRT Status

Technical provisions – Non-life

SCR – Non-life

Technical provisions – Life

SCR – Life

Assets

Own funds

General preparation

Audit ready, with audit differences not expected tobesignificant Audit ready, but may not be able to rely on controls Not audit ready

The above challenges perhaps reflect the maturity of SAM implementation in the industry. However, with a year to go before final implementation and the Financial Services Board indicating audit requirements for the 2016 CPR submissions, limited time remains for refining and improving the process, especially given the limited involvement of external audit to date.

General insurance illustrative accounts 2015

Our publication Proforma-Gen Limited Annual Report 31 December 2015 includes illustrative UK GAAP financial statements for a fictitious UK general insurance group, Proforma-Gen Limited, for the year ended 31 December 2015.

They reflect the requirements of new UK GAAP, including FRS 102 – The Financial Reporting Standard, applicable in the UK and Republic of Ireland and FRS 103 – Insurance Contracts (including its implementation guidance) and include example disclosures on the transition to new UK GAAP.

Updated G-SIIs list

The FSB published the 2015 update of its list of global systemically important insurers (GSIIs) on 3 November 2015. It comprises a total of nine insurers (same as 2014), but one new insurer, Aegon, has been added and Generali has been removed. The updated list was compiled using 2014 data and the methodology published by the IAIS in July 2013. At present, only primary insurers are included on the list. The FSB plans to publish an updated list in November 2016. But by then the list might change fundamentally, because the IAIS published two related consultations on 25 November 2015:

• Global Systemically Important Insurers: Proposed Updated Assessment Methodology, and

• Non-traditional non-insurance (NTNI) Activities and Products.

It proposes to revise the assessment methodology for identifying GSIIs, including:

• Use of a five-phase assessment approach, including both quantitative and qualitative elements

• Adjustments to certain indicators to address issues related to indicator responsiveness, normalisation and data quality (including reliability) across both insurers and jurisdictions

• Adoption of absolute reference values for certain indicators to allow the methodology to be more responsive to changes in the insurance industry’s systemic profile in certain areas, and

• Establishment of specific procedures for an insurer’s entry and exit from the G-SII list.

The methodology proposed in this consultation is meant to be used to identify G-SIIs from 2016, and we would expect to see reinsurers included in the list alongside primary insurers for the first time. The second consultation considers how NTNI activities and products are treated in the assessment methodology and their use in determining the Basic Capital Requirement and Higher Loss Absorbency requirement for G-SIIs. In particular, the IAIS wants feedback on an analytical framework to classify insurance products and activities as non-traditional based on contractual features. The consultations close on 25 January 2016.

Cross-sector announcements

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 17

Taxation

Taxation

Retirement reform in South Africa

Background

The South African retirement fund industry is notoriously complex with complicated products and retirement savings solutions, all with varying tax treatments. Furthermore, saving for retirement is not compulsory. This results in relatively expensive retirement income solutions and a large portion of the South African population not enjoying the benefits of the system.

The intention behind government’s retirement reform proposals is to create a simpler, more cost-effective social security environment that provides retirement income protection to the entire South African population. National Treasury is the main driving force behind these proposals.

A range of proposals and changes has been formulated in legislation and draft bills. Additional discussion documents also provide insight into potential changes in future. These changes can be summarised as follows:

Targeted implementation date

Changes

1 March 2016 Alignment of tax treatment of contributions to pension, provident and retirement annuity funds

1 March 2018 Expected compulsory annuitisation of retirementbenefitsfrom provident funds

Expected in the next two years

Requirement for funds to provide default investment strategies, default preservation options and default retirement solutions

2018 or later Compulsory preservation of pre-retirementbenefits

Simplifying the industry from 1 March 2016

The changes that were implemented with effect from 1 March 2016 align the tax treatment of contributions to pension funds, provident funds and retirement annuities. Previously, different limits on tax deductible contributions applied to the different savings vehicles, adding to the complexity of these benefits.

From 1 March 2016, all employer contributions to retirement funds are taxable as a fringe benefit and are in effect treated the same as member contributions to such funds. Individuals are able to claim a tax deduction on all contributions (member and employer) of up to 27.5% of the higher of taxable income and remuneration, subject to an overall annual limit of R350 000.

The changes to the tax treatment of contributions should result in most individuals not paying any more tax on retirement savings contributions than they currently are. That said, some high-income earners who exceed the R350 000 annual contributions cap are now paying tax on contributions in excess of this limit.

In addition to these simplifying changes, the de minimis amount has also been increased to R247 500 from 1 March 2016. This means the retirement benefits from pension funds and retirement annuity funds may be taken entirely in cash if they are less than R247 500. (Benefits from provident funds may currently be taken fully in cash, irrespective of the benefit amount. See the next section for developments on this front.)

Changes from 1 March 2018

A big attraction of provident funds is the ability to take the entire retirement benefit in cash. Despite a relatively penal tax scale, this option is taken up by a large proportion of provident fund retirees. In contrast, members of pension funds and retirement annuities have to use at least two thirds of their retirement benefit to purchase an annuity-providing income in retirement (subject to the de minimis rule).

In order to align the treatment of pension and provident funds, the annuitisation requirement was to apply to provident funds as well from 1 March 2016, but it was postponed for two years to allow proper consultation with all stakeholders.

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 18

We can therefore expect to see this change implemented from 1 March 2018.

It is important to note that the existing rights of provident fund members will be protected and they will be able to take their accrued savings at implementation date, plus the return thereon, in cash at retirement. The requirement to use two thirds to purchase a pension at retirement will only apply to savings after 1 March 2018, and then only to members younger than 55 at this date.

Default regulations

In the latter part of last year, National Treasury released draft regulations on ‘defaults’ to be provided by retirement funds. These defaults apply to the investment strategies, in-fund preservation options and retirement income solutions of retirement funds. The default options will automatically be exercised for members who do not make a decision; for example, a member who does not make a decision at retirement will automatically be invested in the default retirement strategy of the fund.

The intention is to improve the retirement outcomes of members of retirement funds by encouraging the appropriate (cost-effective) investment of their savings during their working lifetime and at retirement. Members who are overwhelmed by the important decision

they are faced with will have an option available which is suitable based on their circumstances.

The industry has submitted comments on the draft regulations to National Treasury and are waiting for further developments on this front.

Likely future developments

Treasury recognises the devastating impact of non-preservation of retirement benefits when members change jobs, and has hinted at limiting the amount that members can take in cash before retirement. Compulsory preservation and possible mandatory participation in a retirement fund are contentious issues, and given the social impact, extensive consultation is required. We are therefore unlikely to see significant further developments on these topics in the next two years.

Conclusion

Significant changes are required to ensure a better retirement outcome for all South Africans and to reform an entire industry to progressively improve the financial security of all. The current changes to the industry are a step in the right direction.

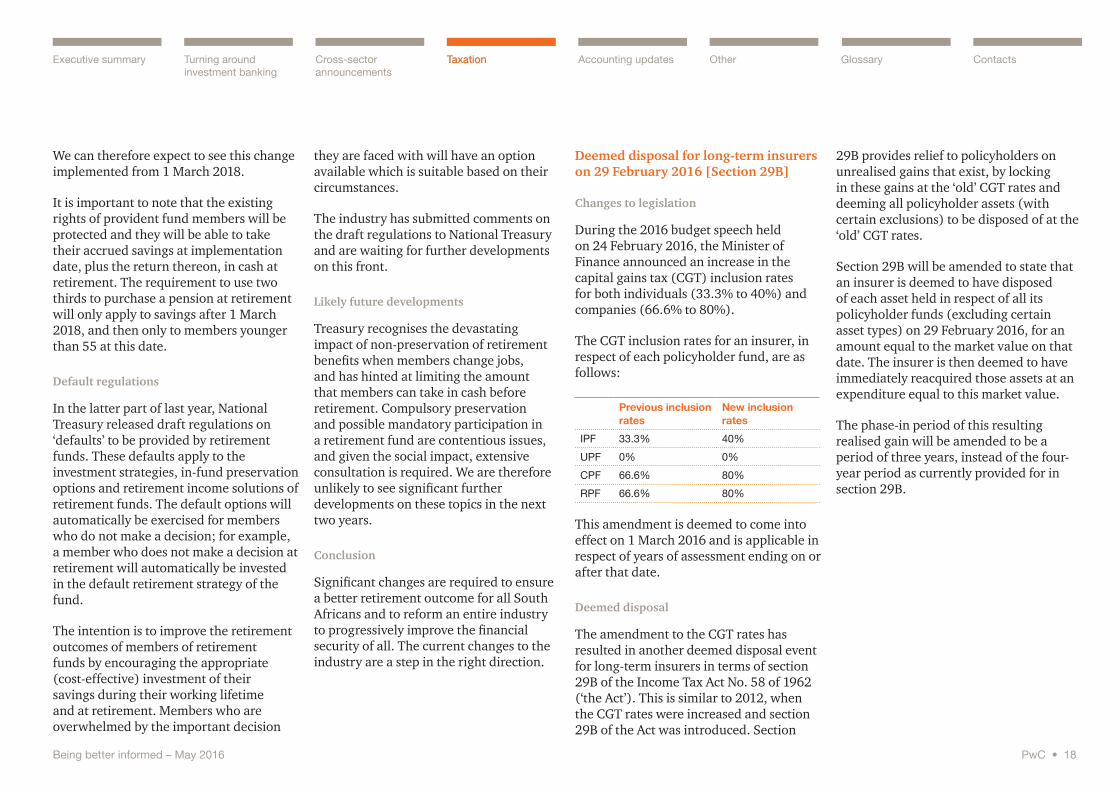

Deemed disposal for long-term insurers on 29 February 2016 [Section 29B]

Changes to legislation

During the 2016 budget speech held on 24 February 2016, the Minister of Finance announced an increase in the capital gains tax (CGT) inclusion rates for both individuals (33.3% to 40%) and companies (66.6% to 80%).

The CGT inclusion rates for an insurer, in respect of each policyholder fund, are as follows:

Previous inclusion rates

New inclusion rates

IPF 33.3% 40%

UPF 0% 0%

CPF 66.6% 80%

RPF 66.6% 80%

This amendment is deemed to come into effect on 1 March 2016 and is applicable in respect of years of assessment ending on or after that date.

Deemed disposal

The amendment to the CGT rates has resulted in another deemed disposal event for long-term insurers in terms of section 29B of the Income Tax Act No. 58 of 1962 (‘the Act’). This is similar to 2012, when the CGT rates were increased and section 29B of the Act was introduced. Section

29B provides relief to policyholders on unrealised gains that exist, by locking in these gains at the ‘old’ CGT rates and deeming all policyholder assets (with certain exclusions) to be disposed of at the ‘old’ CGT rates.

Section 29B will be amended to state that an insurer is deemed to have disposed of each asset held in respect of all its policyholder funds (excluding certain asset types) on 29 February 2016, for an amount equal to the market value on that date. The insurer is then deemed to have immediately reacquired those assets at an expenditure equal to this market value.

The phase-in period of this resulting realised gain will be amended to be a period of three years, instead of the four-year period as currently provided for in section 29B.

Taxation

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 19

Interaction between REITs and section 9C

It is proposed that a provision be added to the Act that section 9C(5) does not apply to shares in REITs. This proposal is made to resolve the anomaly whereby dividends received from REITs are taxable, but the expenditure incurred to produce these taxable dividends is effectively non-deductible.

Hybrid debt instruments [Section 8F]: Tax base protection

Effective 24 February 2016, government will implement measures to eliminate mismatches associated with hybrid debt instruments where the issuer is not a South African resident taxpayer. As interest payments on debt and dividend payments on equity are treated differently for tax purposes, these situations potentially result in double taxation.

Currently, existing rules reclassify an interest payment as a dividend payment for tax purposes; however, it is only possible to deny interest deductions for a South African resident that issues a debt instrument. This results in a mismatch in tax treatment between two countries, as the South African rules apply a low or zero tax rate to the reclassified dividend payment.

Hybrid debt instruments [Section 8F]: Debt instrument subject to subordination agreement

If a debt instrument becomes subject to a subordination agreement as a result of the issuer being in financial distress, that instrument (in terms of section 8F) may be regarded as a hybrid debt instrument.

It is proposed that a concession be made to exclude such instruments from being regarded as section 8F hybrid debt instruments.

Tax implications of securities lending arrangements [Section 10(1)(k)(i)(ff)]

Tax relief on the transfer of collateral in securities lending arrangements was granted in 2015. This relief resulted in no income tax and securities transfer tax implications if a listed share is transferred as collateral in a securities lending arrangement for a limited period of 12 months.

Concerns have been raised that the 12-month limitation rule is too restrictive. Therefore, this condition will be reviewed, along with taking into account corporate actions undertaken during the term of the securities lending agreement.

Budget 2016 – The effect on certain financial services tax provisions in a nutshell

During the 2016 budget speech held on 24 February 2016, the Minister of Finance announced certain tax proposals, summarised below.

Transitional tax issues resulting from regulation of hedge funds [Section 25BA]

The tax relief for amalgamation and asset-for-share transactions creates scenarios where the tax relief provided to assist the hedge fund industry’s transition to a new regulated tax regime is limited and inapplicable to certain hedge funds’ trust structures. It is proposed that provisions be made to address these scenarios.

Taxation of real estate investment trusts (REITs) [Section 25BB]

Qualifying distribution rule

It is proposed that the provisions relating to the qualifying distribution rule in section 25BB of the Act be reviewed to remove the anomaly caused whereby recoupments such as building allowances previously claimed are being included in gross income (as per the definition of section 1), which could affect the 75 per cent rental income analysis used to determine the applicability of the qualifying distribution provisions.

Taxation

ContactsGlossaryAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 20

Refinement of third party-backed share provisions [Section 8EA]

Pre-2012 legitimate transactions

In 2012, government introduced new rules to deal with avoidance concerns involving preference shares with dividend yields backed by third parties. Under the new rules, these dividend yields are treated as ordinary revenue. As these rules may affect some legitimate transactions, government will consider relaxing them, but only in respect of transactions entered into before 2012.

Addressing circumvention of anti-avoidance measures

Schemes have been identified where investors structure their transactions to circumvent third-party anti-avoidance rules, i.e. the formation of trust-holding mechanisms whereby investors acquire participation rights in trusts and the underlying investments of those trusts are preference shares. This effectively bypasses the anti-avoidance provisions, but achieves the same result that the anti-avoidance provisions were trying to curtail.

It is proposed that additional measures be considered to stop the circumvention of these anti-avoidance measures.

FATCA/CRS

South African financial institutions will already be aware of FATCA and its requirements. The landscape of international taxation information reporting has developed further with South Africa becoming a signatory to the Common Reporting Standard (CRS) of the Organisation for Economic Development (OECD) – a global taxation information sharing agreement – on 23 October 2014.

Largely similar to FATCA, financial institutions must report taxpayer information to the South African Revenue Service in order to curb tax evasion by hiding taxable income offshore. The largest difference between the two is that FATCA applies only to the United States, whereas the CRS applies to the foreign ‘competent authorities’ of any signatory jurisdictions – a truly global undertaking.

The necessary amendments to the primary South African legislation, the Tax Administration Act No. 28 of 2011 (for the implementation of the CRS in South Africa), have been in place since January 2016. The regulations to the Tax Administration Act were promulgated on 2 March 2016.

Taxation

ContactsAccounting updatesTaxation OtherCross-sector announcements

Turning around investment banking

Executive summary

Being better informed – May 2016 PwC • 21

Glossary

Accounting updatesIFRS news

The December 2015/January 2016 issue of our publication IFRS News covers:

• Revenue – TRG discusses optionalpurchases, licences and other topics

• Financial instruments – News from theTRG for impairment

• Definition of a business – FASB exposuredraft

• Update: IFRS in the US

• Year-end reminders.

IFRS 9 – Getting governance right